H E A L T H W E A L T H C A R E E R

M E R C E R W E B C A S T

M A R K E T E N V I R O N M E N T

July 21, 2016

Anthony BrownUS Director of Strategic Research

Lucy TusaPrincipal

© MERCER 2016 1

L I Q U I D I T Y S W A M P E D T H E I M P A C T O F B R E X I T

Past performance is no guarantee of future results. Please see Important Notices for further information.

-2.6-1.5

0.10.60.7

1.11.7

2.12.5

2.73.23.4

3.63.73.8

5.512.512.8

-5 0 5 10 15

Intl Sm-Cap StksIntl Large-Cap Stks

T-BillsFunds of Hedge Funds

Emerg Mkt StksUS MBSUS TIPS

US TreasuriesUS Large-Cap Stks

Emerg Mkt Debt (Local)US Mid-Cap Stks

Global FixedUS I/G Corp Bonds

Global REITsUS Small-Cap Stks

US High Yield BondsNatural Res Stks

Commodity Futures

Second Quarter Performance (%)

Source: Datastream

© MERCER 2016 2

B R E X I T : T H E P O L I T I C S

• The result of the EU Referendum held on June 23, 2016was a 52% / 48% victory for the “Leave” campaign

• David Cameron resigned and Theresa May has replacedhim as Prime Minister

• Given the strong support for “Remain” in Scotland, NicolaSturgeon has held talks with EU leaders and may seek asecond referendum on Scottish independence

• Similarly, senior politicians in Northern Ireland havesuggested that they may also seek some special statuswithin the EU and there have been calls for a vote onIrish re-unification.

• Jeremy Corbyn lost a vote of no confidence by 172 to 40and a leadership election is underway

• The UK now faces several years of politicaluncertainty Source: The Guardian.

Graphic shows geographic support for Remain /Leave weighted by voter populations

© MERCER 2016 3

G I L T S A N D S T E R L I N G

• UK gilt yields at all time lows:– 10 year gilts yield 1% lower than at the start of

2016– 30 year nominal gilts yielded 1.7% as of July

1st.

• Mark Carney has suggested that the BoE is likelyto ease policy over the summer– This could include rate cuts and quantitative

easing– Markets are now expecting no rate hikes until

after 2020– The March 2018 gilt dipped below a zero yield

(the first negative-yielding nominal UK gilt)

• The pound sterling has reached its lowest levelagainst the US dollar since 1985

• S&P downgraded the UK from AAA to AA– Fitch downgraded the UK from AA+ to AA and

Moody’s placed the UK on a “negative watch”

© MERCER 2016 4

K N O W N U N K N O W N S

• Short-term impact on UKeconomy expected to benegative

• Medium to longer-termeffects much harder topredict.

• General election / anotherreferendum?

• UK ‘s negotiating stance?

• Scottish referendum?

• Irish referendum?

• EU negotiating stance?

• Calls for referenda in othercountries?

• Elections in Germany,France and Netherlands in2017 and a constitutionalreferendum in Italy(October 2016)

• Markets remain fragile dueto heightened uncertaintyand reduced liquidity

• Policy-maker response willalso be important (i.e.monetary and fiscal policy)

DOMESTICPOLITICS

EUROPEANPOLITICS

ECONOMICEFFECTS

MARKETEFFECTS

Brexit is not taking place within a vacuum – it is just one part of a complex macro-economicpicture containing many sources of uncertainty (e.g. China and the US)

© MERCER 2016 5

P O S S I B L E B R E X I T M O D E L S

Tariff free tradewith EU

Negotiates owntrading terms withcountries outside

the EU?

Freemovementof persons

Contributionto EU budget

Eurozonemembership

Require domesticlegislation

equivalent to EU lawVotes on EU

law?

The NorwayModel (EEA

Model)Yes Yes Yes Yes No Yes, except on fishing

or farm policies No

The SwissModel

Partially – mostgoods, but notmost services

Yes Yes Yes No Yes No

The TurkishModel

Partially – somegoods, notservices

Yes, but tariffsmust be aligned

with EU.No No No

Yes in certain areassuch as consumer

protection,competition and

intellectual property

No

The CanadianModel

Partially – somegoods, notservices

Yes No No No No No

The WorldTrade

OrganizationModel

Exports wouldface EU’s

WTO tariff ratesand will continueto have to meet

EU productstandards

Yes No No No No No

Source: Based on information in the HM Government “Alternatives to membership” paper (March 2016).

© MERCER 2016 6

R I S K O F C O N T A G I O N

• Brexit is at least in part the result of secularglobal forces – economic inequality and loss oftrust in “mainstream” politicians- that have takenhold in the aftermath of the financial crisis

• Symptoms of this broader malaise include therise of far-right and far-left parties acrossEurope (e.g. Syriza in Greece, Freedom Partyin Austria, National Front in France); the rise ofTrump in the US; the rise of UKIP and theelection of Corbyn as Labour leader in the UK

• Public support for a referendum is above 50% inboth France and Italy– Both countries have also seen rising support

for populist / extremist political parties

• The exit of a major Eurozone member would bean order of magnitude more destabilising thanBrexit

Source: HSBC

© MERCER 2016 7

B R E X I T S H O U L D H A V E L I M I T E D I M P A C T O N G L O B A LG R O W T H , B U T C O N T A G I O N R I S K S R E M A I N

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Oct

'14

Dec

'14

Feb

'15

Apr'

15

Jun

'15

Aug

'15

Oct

'15

Dec

'15

Feb

'16

Apr'

16

Jun

'16

Apr'

15

Jun

'15

Aug

'15

Oct

'15

Dec

'15

Feb

'16

Apr'

16

Jun

'16

Perc

enta

gech

ange

Month of Forecast

Consensus GDP Growth Forecasts

United States

Source: Bloomberg

Eurozone

United Kingdom

2016 Forecast 2017 Forecast

Japan

© MERCER 2016 8

E M G R O W T H S T A B I L I Z I N G

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

(%)

2016 GDP GrowthConsensus Expectations

China India

Brazil Russia

Source: Bloomberg

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

(%)

2017 GDP GrowthConsensus Expectations

China India

Brazil Russia

Source: Bloomberg

© MERCER 2016 9

U S I N T E R E S T R A T E S R E A C H E D N E W L O W S

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Jan-

16

US 10-year Treasury Yield

Source: Bloomberg

0.0

0.5

1.0

1.5

2.0

2.5

Jan-

15Fe

b-15

Mar

-15

Apr-1

5M

ay-1

5Ju

n-15

Jul-1

5Au

g-15

Sep-

15O

ct-1

5N

ov-1

5D

ec-1

5Ja

n-16

Feb-

16M

ar-1

6Ap

r-16

May

-16

Jun-

16Ju

l-16

(%)

Fed Funds Futures

Dec-16

Dec-17

Source: Bloomberg

© MERCER 2016 10

W H A T ’ S T H E M E S S A G E F R O M T H E B O N DM A R K E T ?

0

2

4

6

8

10

12

14

16

18

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

(%)

10-Year Treasuryand Nominal GDP Growth

10-Year Treasury YieldRolling 10-year Nominal GDP Growth

Source: Bloomberg

-1

0

1

2

3

4

5

1957

1961

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

2009

2013

(%)

Productivity Growth(Non-farm Business Output Per Hour)

Rolling 3 yrs

Rolling 10 years

Source: Bloomberg

© MERCER 2016 11

G L O B A L C O N D I T I O N S S I G N I F I C A N T L YI N F L U E N C I N G U S R A T E S

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-

14

Apr-1

4

Jul-1

4

Oct

-14

Jan-

15

Apr-1

5

Jul-1

5

Oct

-15

Jan-

16

Apr-1

6

10-Year Yields on Select GovernmentBonds

Germany Swiss

UK US

Source: Bloomberg

60

65

70

75

80

85

90

95

100

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Jan-

16M

ay-1

6

Trade-Weighted DollarMajor Currencies

TW Dollar (Major)

200d m.a.

Source: Bloomberg

© MERCER 2016 12

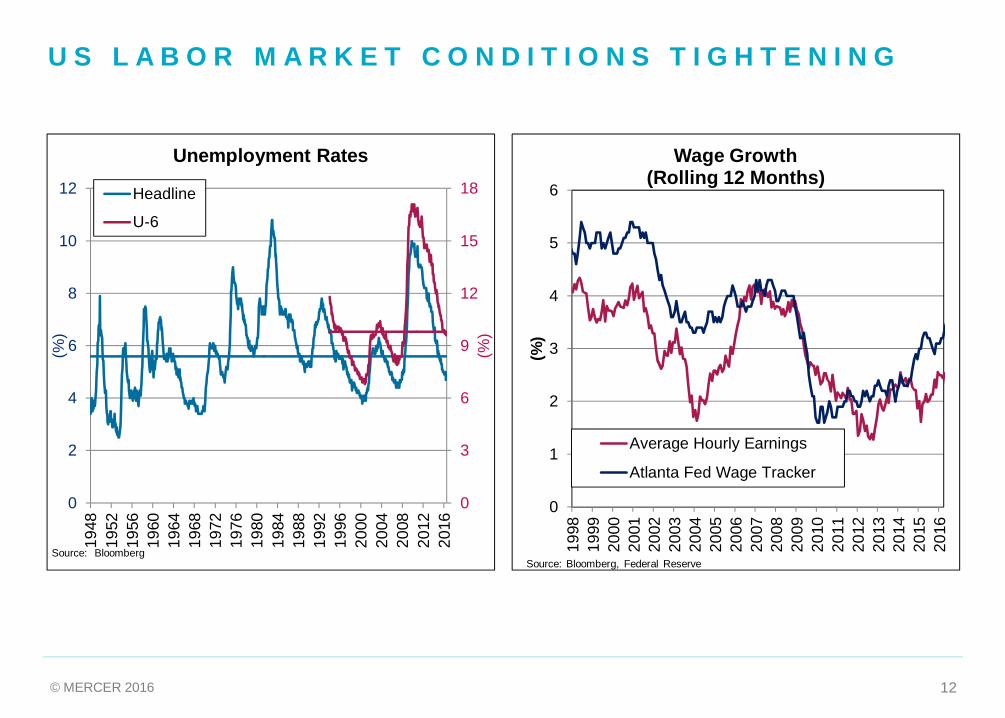

U S L A B O R M A R K E T C O N D I T I O N S T I G H T E N I N G

0

1

2

3

4

5

6

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(%)

Wage Growth(Rolling 12 Months)

Average Hourly Earnings

Atlanta Fed Wage Tracker

Source: Bloomberg, Federal Reserve

0

3

6

9

12

15

18

0

2

4

6

8

10

12

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

(%)

(%)

Unemployment Rates

Headline

U-6

Source: Bloomberg

© MERCER 2016 13

C O R E I N F L A T I O N M E A S U R E S T R E N D I N GH I G H E R , W H I L E E X P E C T A T I O N S D E C L I N I N G

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

(%)

InflationRolling 12-months

Core CPI Core PCE DeflatorSource: Bloomberg

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Mar

-09

Sep-

09M

ar-1

0Se

p-10

Mar

-11

Sep-

11M

ar-1

2Se

p-12

Mar

-13

Sep-

13M

ar-1

4Se

p-14

Mar

-15

Sep-

15M

ar-1

6

(%)

Inflation Breakeven Rate on TIPS

5-year

5-yr / 5 yrs Forward

Source: Bloomberg, Mercer

© MERCER 2016 14

L O W E X P E C T E D R E T U R N S F R O M F I N A N C I A LA S S E T S

-2

0

2

4

6

8

10

12

14

1619

50

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

(%)

Real Expected Returns on Stocks and BondsExpected Real Yield on 10-yr TreasuriesNormalized Earnings Yield on S&P 50060/40 Blend Expected Real Return

Source: S&P, Federal Reserve, Bloomberg, Mercer

© MERCER 2016 15

C R E D I T L E S S AT T R A C T I V E

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

(%)

Investment-Grade Corporate BondCredit Spread

OAS

Median OAS

Quality Adjusted Median OAS

Source: Barclays, Mercer

2

4

6

8

10

12

14

16

18

20

22

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep-

14N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5Se

p-15

Nov

-15

Jan-

16M

ar-1

6M

ay-1

6

(%)

High Yield BondOption Adjusted Credit Spread

HY Energy

HY ex. Energy

Source: Barclays

© MERCER 2016 16

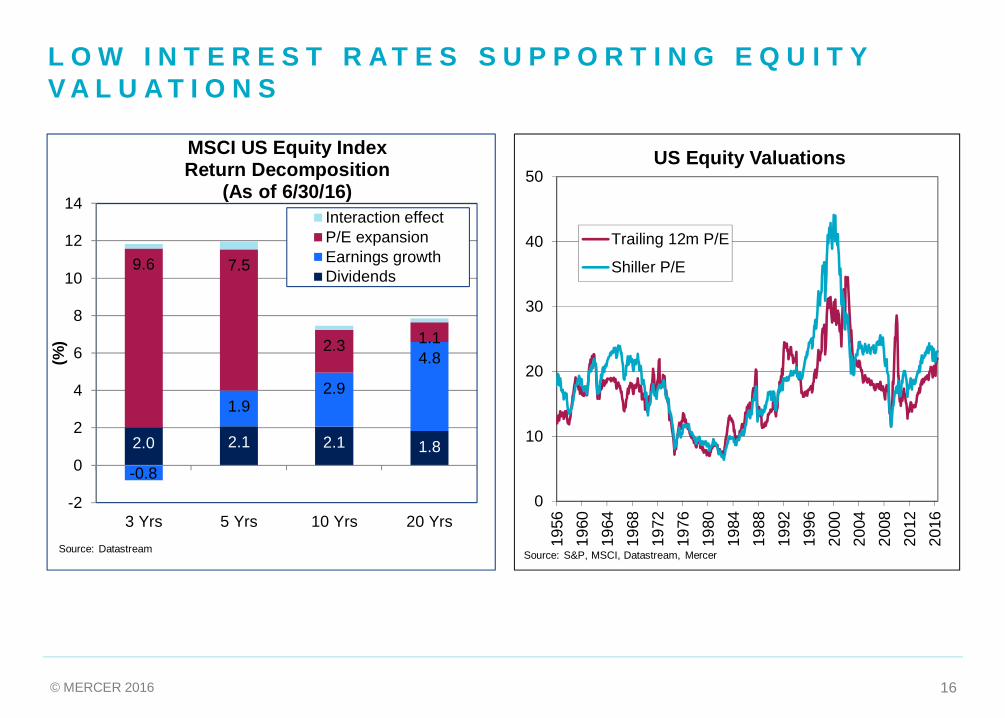

L O W I N T E R E S T R A T E S S U P P O R T I N G E Q U I T YV A L U A T I O N S

2.0 2.1 2.1 1.8-0.8

1.92.9

4.8

9.6 7.5

2.3 1.1

-2

0

2

4

6

8

10

12

14

3 Yrs 5 Yrs 10 Yrs 20 Yrs

(%)

MSCI US Equity IndexReturn Decomposition

(As of 6/30/16)Interaction effectP/E expansionEarnings growthDividends

Source: Datastream

0

10

20

30

40

50

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

US Equity Valuations

Trailing 12m P/E

Shiller P/E

Source: S&P, MSCI, Datastream, Mercer

© MERCER 2016 17

R I S I N G W A G E S A N D W E A K P R O D U C T I V I T YG R O W T H P R E S S U R I N G P R O F I T M A R G I N S

-3

-2

-1

0

1

2

3

4

5

6

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

(%)

Productivity and Hourly Wage GrowthRolling 4 Quarters

Real Compensation Per Hour

Non Farm Business Output

Source: Bloomberg

0%

2%

4%

6%

8%

10%

12%

14%

16%

52%

54%

56%

58%

60%

62%

64%

66%

68%

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Afte

r-Ta

xPr

ofits

Com

pens

atio

nof

Empl

oyee

s

Employee Compensation and ProfitsShare of Non-financial Corporate GDP

Employee Compensation (LS)Corporate Profits (RS)

Source: Bureau of Economic Analysis

© MERCER 2016 18

I N T E R N A T I O N A L V A L U A T I O N S R E L A T I V E L YA T T R A C T I V E , B U T U N C E R T A I N E A R N I N G S O U T L O O K

22.0

20.0

13.813.8

23.2

14.2

17.6

10.8

13.2

9.6

7.0 8.2

2.8 1.7 1.1 1.52.1

3.7

2.4 2.8

0

5

10

15

20

25

30

MSCI US MSCI Europe MSCI Japan MSCI EM

Global Valuations

P/E Trailing Shiller's P/E

P/CF P/B

Dividend Yield

Source: Bloomberg, Datastream, Mercer

-5

0

5

10

15

20

25

1990

1993

1996

1999

2002

2005

2008

2011

2014

(%)

Return-On-Equity for Global Markets

MSCI Europe MSCI Japan MSCI US

Source: Bloomberg, Datastream, MSCI

© MERCER 2016 19

C O N C L U S I O N S

• Base case of low, stable economic growth most likely, but the downside risks are increasing– Contagion risk from Brexit– Growing popularity of populism– Chinese growth

• The Fed could surprise the bond market

• Recovery in credit reduced relative attractiveness

• Equities offer an attractive return relative to bonds in the base case, but little margin for error

• Continue to seek alpha and other alternative sources of return

© MERCER 2016 20

Q U E S T I O N S ?

QUESTIONSPlease type your questions in the Q&A section of the toolbarand we will do our best to answer as many questions as wehave time for.

To submit a question while in full screen mode, use the Q&Abutton, on the floating panel, on the top of your screen.

CLICK HERE TO ASK A QUESTIONTO “ALL PANELISTS”

FEEDBACKPlease take the time to fill out thefeedback form at the end of this webcastso we can continue to improve. Thefeedback form will pop-up in a newwindow when the session ends.

Anthony Brown Lucy TusaSt. Louis London+1 314 982 5741 +44 (0)20 7178 [email protected] [email protected]

© MERCER 2016 21

Important NoticesReferences to Mercer shall be construed to include Mercer LLC and/or its associated companies.

© 2016 Mercer LLC. All rights reserved.

Information contained herein has been obtained from a range of third party sources. While the information is believed to be reliable, Mercer has not sought to verify it independently. As such,Mercer makes no representations or warranties as to the accuracy of the information presented and takes no responsibility or liability (including for indirect, consequential or incidental damages)for any error, omission or inaccuracy in the data supplied by any third party.

No investment decision should be made based on this information without first obtaining appropriate professional legal, tax and accounting advice and considering your circumstances.

Investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money.

Mercer Investment Management, Inc. and Mercer Investment Consulting LLC are federally registered investment advisers under the Investment Advisers Act of 1940, as amended. Registrationas an investment adviser does not imply a certain level of skill or training. Mercer’s Form ADV Part 2A & 2B can be obtained by written request directed to: Compliance Department, MercerInvestments, 701 Market Street, Suite 1100, St. Louis, MO 63101.

MMC Securities LLC is a registered broker dealer and an SEC registered investment adviser. Securities offered through MMC Securities; member FINRA/SIPC, main office: 1166 Avenue of theAmericas, New York, New York 10036. Variable insurance products distributed through Marsh Insurance & Investments LLC; and Marsh Insurance Agency & Investments in New York. Mercer,Mercer Investment Consulting, LLC, Mercer Investment Management, Inc., Guy Carpenter, Oliver Wyman, Marsh and Marsh & McLennan Companies are affiliates of MMC Securities.

Download a guide on key index definitions.

© MERCER 2016 2222