Map xxxx

▪

▪ University of OxfordEnergy Colloquium

Tidal lagoons as a cornerstone of the UK energy sectorOctober 2016

1850 : Locations of active UK tidal mills

2016 Images of these permanent assets

Felin Wen, Anglesey

Carew Castle, Pembrokeshire, 1542-1937

Three Mills, London, 1776-1817

Woodbridge, Ipswich, 1170-2016

24

Our island nation

! The best tidal range resource in Europe and 2nd best worldwide

! A 1,400 year history of tapping it! Shallow waters, suitable bathymetry,

population and grid proximity! Variance in tide times offering the

potential for 24-hour generation, a total potential for up to 40GW

Why do we have such a large tidal range?

‘Shoaling’

‘Funnelling’

Security and predictability

Vive la France!Opening of La Rance by General de Gaulle 26 November 1966

14

! World’s first tidal power station, opened November 1966

! Fruit of three decades of research into tidal power in salt water in the Breton-Normand Gulf

! 97% availability during nearly 50 years of operation

La Rance tidal power station

1914

La Rance Tidal Barrage, France49 years of field data

! Built and operated by EDF! 240MW installed capacity! 540,000 MWh/year! Operating smoothly! 97% availability in 49 years! 93% efficiency on the ebb! 75% efficiency on the flood! Year 47 – first overhaul of turbines, 5 turbines received

replacement parts! Year 48 – control system to be replaced! Year 50 - €200m refurbishment for another 50 years of

output

Tidal range is a proven technology

Year 47

Year 1

The UK energy gap

Source: Bircham Dyson Bell

The UK has a requirement to provide security of supply in the face of:

• Increasing demand through the electrification of heat and transport

• A requirement to decarbonise the electricity system by 2050

• Power station closures out to 2025 representing 30% of existing generation capacity

• Continuing focus on value for money and lowest cost solutions

24

Wall length: 9.5km Area: 11.5km2

Installed capacity: 320MWDaily generating time: 14 hoursAnnual output (net): 530GWhAnnual CO2 savings: 236,000 t

Design life: 120yrs Height of wall: 5-20mWall above low water: 12.0m Wall above high water: 3.5m Tidal range Neaps: 4.1mTidal range Springs: 8.5m

Swansea Bay Tidal Lagoon: a blueprint

We generate on the ebb & flood of each tide, sluicing & pumping at the end of eachtide to maximize head difference ready for the next tide

Flexible and predictable generation

Cardiff

Lancashire

Colwyn

Portfolio A: Cardiff, Colwyn, Lancashire

Portfolio A: Cardiff, Colwyn, Lancashire

Cardiff

Colwyn

Lancashire

Portfolio A: Flexible generation

CCGT behaviour change

24

Tidal Lagoon Swansea Bay

Technical drawings:Bund wall cross sections

Temporary bund wall (cofferdam)

LAGOON SIDE

SEA SIDE

La Rance – cofferdam construction

Shiwa – cofferdam construction

Shiwa – cofferdam construction

Shiwa – cofferdam construction

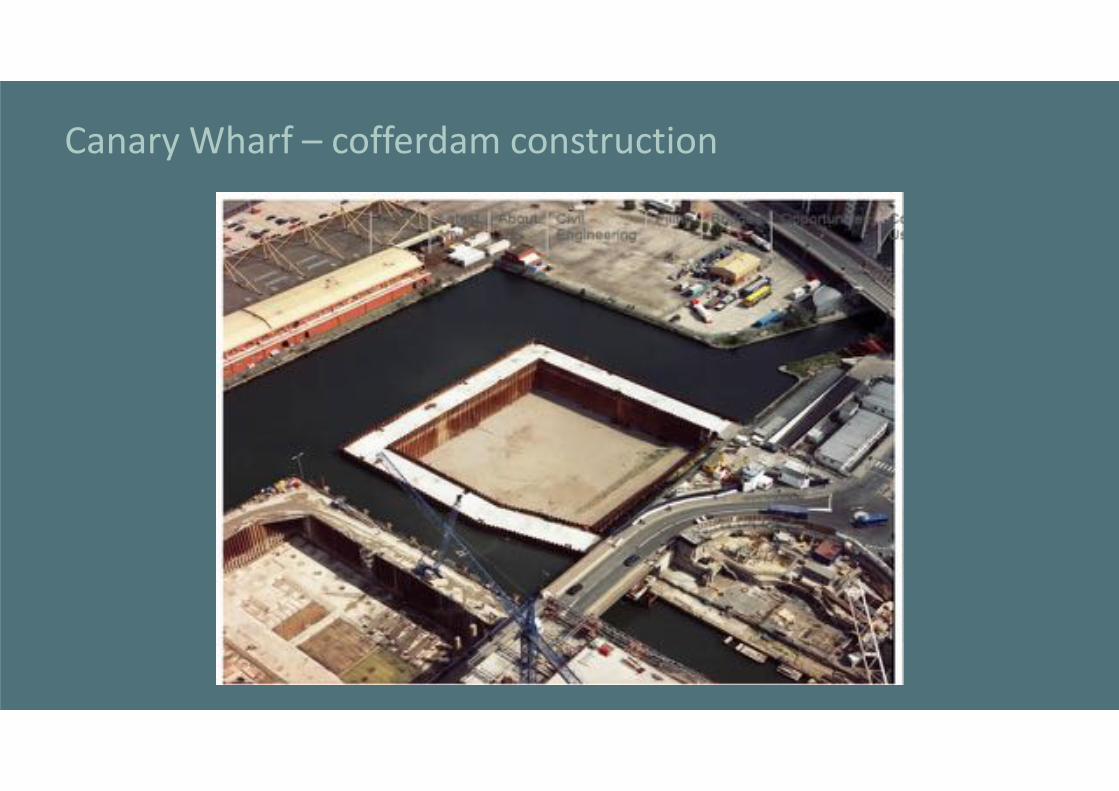

Canary Wharf – cofferdam construction

Technical drawings:Turbine and sluice gate structures

Technical drawings:Turbine house cross section

Technical drawings:Sluice gate cross section

Construction sequence – Year 1

Construction sequence – Year 2 & 3

Construction sequence – Year 4

Turbine house

Draft Tube40 tonnes

Turbine Housing90 tonnes

Bulb Nose20 tonnes

Hatch Cover30 tonnes

Shaft40 tonnes

Runner

Runner blade18 tonne

Runner hub45 tonnes

Distributor90 tonnes

Discharge ring

Generator

Turbine components

CACW heat exchangers

Stator end plate

Stator frame

Stator copper

Stator laminationsRotor

laminations

Rotorbars

Terminal box

Rotor spider

Rotor end rings

Rotor pressure plates

Stator compression

plates

Converter

Generator components

TLSB turbine tender

! 2 stage competitive process

! 18 month duration including 9 months of homologous model testing

! 3 global leaders in hydro turbine design and manufacture: GE-Andritz, Voith, Alstom

! 3 different variable speed solutions

! Winner-GE Andritz-triple regulated varspeed bulb

24

Tidal Lagoon Swansea Bay

IEC60193 homologous model testing – guaranteed performance

Our Preferred Contractor (AndritzHydro) has supplied 455 similar design bulb turbines around the world with an installed capacity of over 10GW

Low head hydro bulb turbine – 7.2m runner

Distributor and runner installation

Bulb nose installation

Runner inspection

Andritz Hydro turbine performance data

Tidal Lagoon Swansea Bay:UK supply chain locations

Swansea Bay Tidal Lagoon - direct construction demand

Swansea Bay Tidal Lagoon - direct construction employment

UK contentOffshore Wind Programme Board/BVG Associates methodologyTidal lagoons have 84% UK content throughout their lifetime

• Tidal lagoons have significantly higher UK content across development, capital and operational expenditure• This translates into improved GVA, skills and expertise, taxation and regeneration in deprived areas

Balance of paymentsTidal lagoons divert more spending into the UK across all stages84p of every £1 spent stays in the UK

• Under a CfD, payments from UK consumers to tidal lagoons are recycled back into the UK economy, contributing to GDP and keeping value in the country

• The most recent offshore wind farm to secure a CfD sends most of its subsidy overseas – 57p of every £1

South Wales industrial potential:

Pembroke Docks: Heavy fabrication

Port Talbot Docks: Pre-cast/caisson yard

Newport: Manufacturing logistics centre/Turbine Manufacturing Plant/Generator Manufacturing Plant

Swansea Docks: Turbine Manufacturing Plant

Milford Haven: Caisson yard

Tidal Lagoon Cardiff

Indicative design:Average tide: 9.21mArea: 70km2

Length: 22km Turbines: 90-110Installed cap: 3,240MWOutput: 6TWh p/a

Comfortably enough low carbon electricity to power every home in Wales **Average annual electricity consumption per Welsh household = 3,928 kWh. 1.319m Welsh households

Figures are based on a single indicative design iteration and are not necessary representative of any scheme that may be developed

SWANSEAMATERIAL QUANTITY

CARDIFFMATERIAL QUANTITY

Scaling up from TLSB in a single step

52

CARDIFF

SWANSEA20m

27m

98m

130m

Cardiff cofferdam modification

53

Turbine blocks are based on a scaled-up version of the Swansea Bay design to accommodate a larger 8m turbine and increased tides

Cardiff Swansea Bay

Cardiff powerhouse design modification

SWANSEAVOLUME OF LAGOON

70,000,000 M

CARDIFFVOLUME OF LAGOON

810,000,000 M

Scaling up from TLSB in a single step

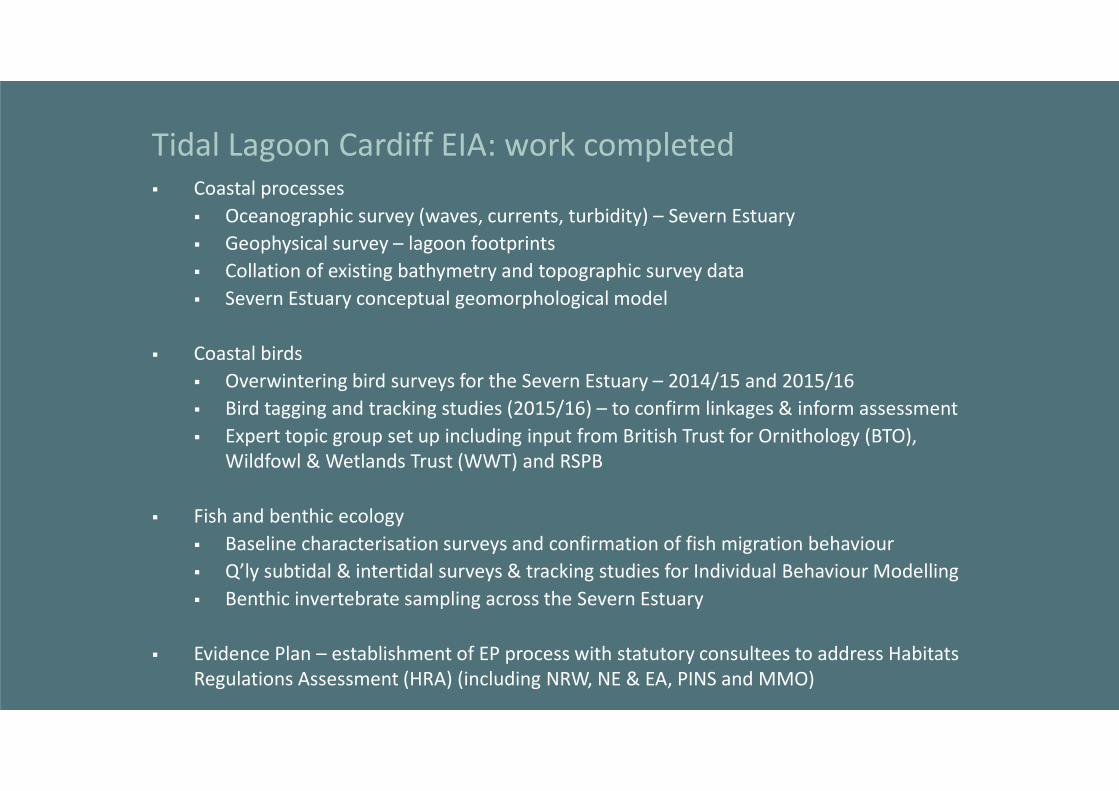

! Coastal processes! Oceanographic survey (waves, currents, turbidity) – Severn Estuary! Geophysical survey – lagoon footprints! Collation of existing bathymetry and topographic survey data! Severn Estuary conceptual geomorphological model

! Coastal birds! Overwintering bird surveys for the Severn Estuary – 2014/15 and 2015/16! Bird tagging and tracking studies (2015/16) – to confirm linkages & inform assessment! Expert topic group set up including input from British Trust for Ornithology (BTO),

Wildfowl & Wetlands Trust (WWT) and RSPB

! Fish and benthic ecology! Baseline characterisation surveys and confirmation of fish migration behaviour! Q’ly subtidal & intertidal surveys & tracking studies for Individual Behaviour Modelling! Benthic invertebrate sampling across the Severn Estuary

! Evidence Plan – establishment of EP process with statutory consultees to address Habitats Regulations Assessment (HRA) (including NRW, NE & EA, PINS and MMO)

Tidal Lagoon Cardiff EIA: work completed

! Steering Group set up – comprised of TLP, NRW, Natural England and Environment Agency. PINS and MMO have a watching brief

! Six Expert Topic Groups (ETGs) set up and meetings held (TLP specialist consultants identified below)! Coastal processes (ABPmer + Intertek re water quality &

JBA on flooding)! Coastal birds (BTO, WWT)! Marine mammals (Natural Power)! Intertidal and subtidal benthic ecology (APEM and Ocean

Ecology)! Fish (APEM and THA)! HRA/WFD/MCZ/Compensation

Evidence Plan process: established

Environmental Enhancement Programme – EEP

! Compensation for lost intertidal areas! Cardiff: potential compensation up to 2,200 ha! Reduced lay-out option for lagoon to reduce this compensation area! Importance for pumping to reduce intertidal loss within the lagoon

footprint! Better operation of the lagoon to reduce intertidal losses

58

Wallasea Island (Alfleets Marsh) Managed Realignment

Stanford Wharf Nature Reserve (London Gateway compensation) Fish migration highway and Fish pass (Rhine west)

A precedent: Wallasea Island

A partnership project between the Environment Agency, the RSPB and CrossRail

Objectives:

! Coastal squeeze compensation! Creation of a major new visitor attraction: quiet enjoyment of nature and open space that will reconnect

people with their coastal heritage, display rich biodiversity and provide a safe haven for birds

! The largest conservation and habitat engineering project of its type in Europe (688ha)! Habitat creation:

! 320ha of mudflats! 160ha of saltmarsh! 96ha shallow saline lagoons! 64ha of brackish grazing marsh! 129ha of pasture

! Completion expected 2025! £100-150m overall project cost (£130-195k/ha)! £5.8m land purchase estimate (£3k/ha)

59

A precedent: Medmerry

An Environment Agency flood defence project that has created a 500ha RSPB reserve.

Project objectives:1. Sustainable flood risk management2. Creation of intertidal habitat to help offset losses elsewhere

in the Solent3. Community involvement in the scheme

development (the Medmerry Stakeholder Advisory Group was established in 2009)

Achievements:• Constructed in 2 years (£35M project cost)• 13 industry awards in 2014 alone, including The Prime

Minister’s Better Public Building Award (previous winners include the Tate Modern)

• Species success: in 2015, avocet, dunlin, wigeon, knot and grey plover have all be seen using the reserve, along with redshank, oystercatcher, lapwing and little ternAnd now sharks!

60

Coastal processes – geophysical & oceanographic surveys complete

Terrain model from aerial LiDAR & bathymetry surveys

Seabed relief and magnetometer surveys

Rockhead depth

Oceanographic surveys – Severn Estuary

Surveys to inform coastal processes modelling

! Waves! Currents! Turbidity

Bathymetry & topographic data collated from multiple sources

Data collated from: TLP Survey work; Ports; UKHO; NRW; EA

! Fundamental initial step for the TLP team and ETG is to agree the use of a model with appropriate boundaries to ensure robust assessment of both project and cumulative effects.

! Coastal processes model will also form the basis of the water quality and flooding assessments and support other assessments.

! Coastal processes model proposed was that used for the DECC (2010) STP SEA.

! Key project specific surveys undertaken and ongoing to assist in this process and refinement of the model grid.

Coastal processes model overview

Model boundaries

67

Coastal processes – TLC flow speed changes

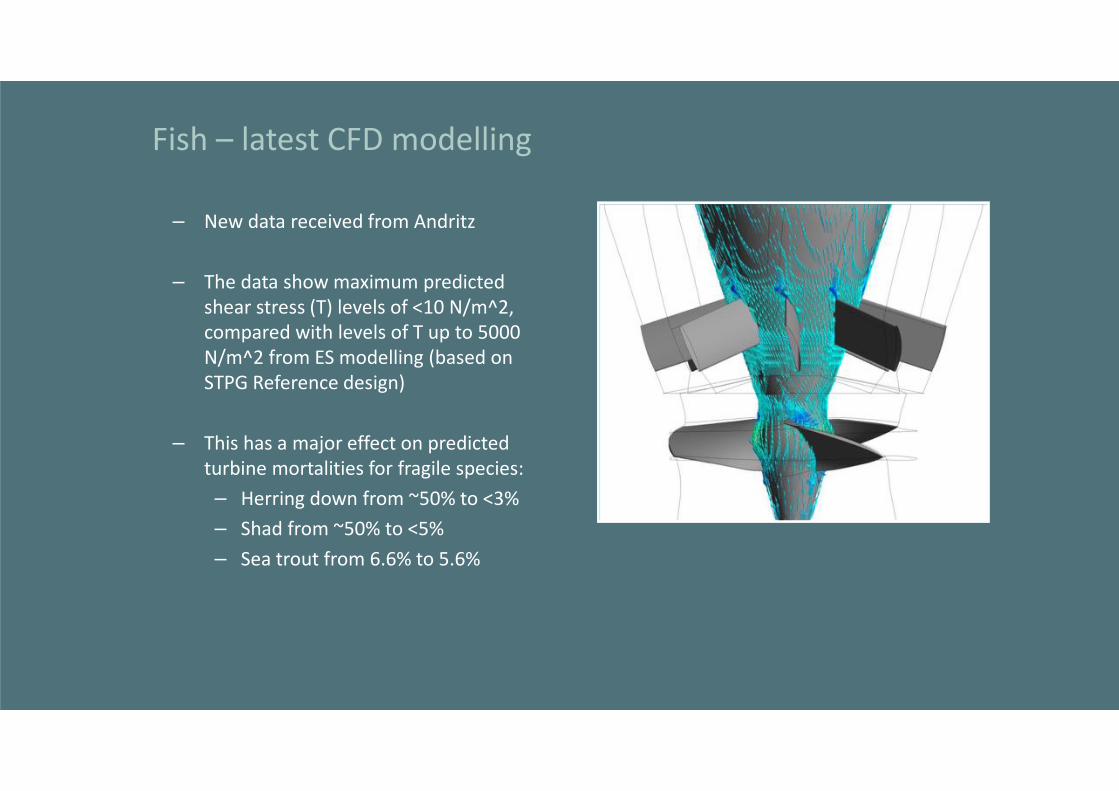

Fish – latest CFD modelling

– New data received from Andritz

– The data show maximum predicted shear stress (Τ) levels of <10 N/m^2, compared with levels of Τ up to 5000 N/m^2 from ES modelling (based on STPG Reference design)

– This has a major effect on predicted turbine mortalities for fragile species:– Herring down from ~50% to <3%– Shad from ~50% to <5%– Sea trout from 6.6% to 5.6%

Fish – subtidal surveys

! Annual volume of deposition: 4 to 10 million tons! Needs to be removed by maintenance dredging

Tides in the estuary are reduced due to the presence of the lagoon

Coastal birds – work completed

72

• Overwintering Bird Surveys – Cardiff/Newport footprints & full survey of Severn Estuary SPA (2014/16)

• Bird GPS tagging & tracking studies – to confirm how birds currently use the estuary & associated freshwater habitats (2015/16)

• Benthic Invertebrate Surveys – sampling to inform Individual Based Modelling (IBM) for birds – 200 locations throughout the estuary

Fish – work completed

73

• Quarterly subtidal & intertidal surveys – baseline characterisation surveys since 2015 – Welsh & English waters

• Migratory fish tagging & tracking studies – work in Swansea to inform future modelling & impact assessment work

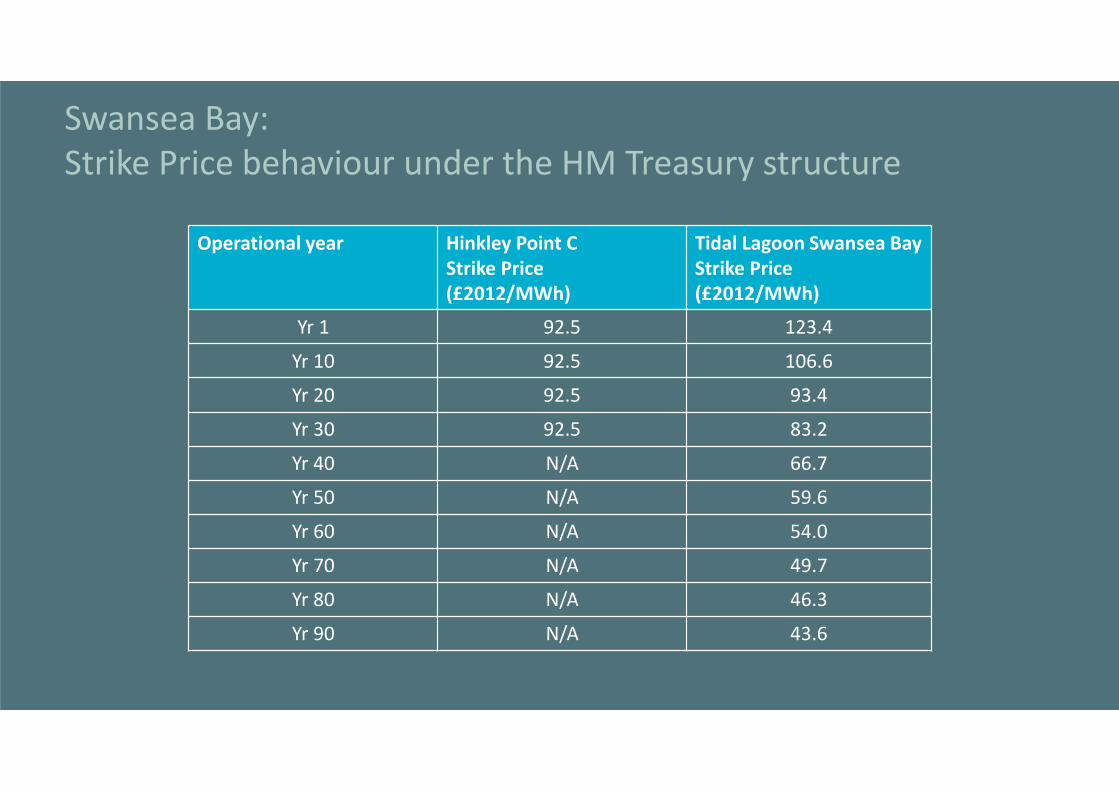

Swansea Bay:Strike Price behaviour under the HM Treasury structure

[SERIES NAME]

[SERIES NAME]

[SERIES NAME]

[SERIES NAME]

[SERIES NAME]

[SERIES NAME]

0

20

40

60

80

100

120

140

160

2017

2020

2023

2026

2029

2032

2035

2038

2041

2044

2047

2050

2053

2056

2059

2062

2065

2068

2071

2074

2077

2080

2083

2086

2089

2092

2095

2098

2101

2104

2107

2110

2113

£201

2/M

Wh

2012 real Strike Price

Swansea Bay:Strike Price behaviour under the HM Treasury structure

Operational year Hinkley Point CStrike Price(£2012/MWh)

Tidal Lagoon Swansea BayStrike Price(£2012/MWh)

Yr 1 92.5 123.4

Yr 10 92.5 106.6

Yr 20 92.5 93.4

Yr 30 92.5 83.2

Yr 40 N/A 66.7

Yr 50 N/A 59.6

Yr 60 N/A 54.0

Yr 70 N/A 49.7

Yr 80 N/A 46.3

Yr 90 N/A 43.6

Debt amortization – 35 year structureRelative to technology lifetime, short term CfD structures force inefficient debt amortisation

- x

0.50x

1.00x

1.50x

2.00x

2.50x

3.00x

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2015 2019 2023 2027 2031 2035 2039 2043 2047 2051 2055 2059 2063 2067 2071 2075 2079 2083 2087 2091 2095 2099 2103 2107

£m

Refinancing - nominal debt Bond Index Linked Debt - Real Bank Debt

Mezz Private Placement EIB Refinancing - index linked debt

Index-Linked Debt - Nominal Avg DSCR

Debt amortization – 90 year structureStructuring debt amortisation to complement the longevity of the technology dramatically improves efficiency, reducing overall subsidy requirements by 50%

- x

0.50x

1.00x

1.50x

2.00x

2.50x

-200

0

200

400

600

800

1,000

1,200

1,400

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 2070 2075 2080 2085 2090 2095 2100 2105

£m

Refinancing - nominal debt Bank Debt Index-Linked Debt - Nominal

Avg DSCR Backward Looking ADSCR - Total Debt

HM Treasury structure:Optimisation mechanisms

Mechanism Rationale

Partial indexation of Strike Price High capex, low opex project – efficient financing, reduces overall subsidy

CfD term Allows long term debt – efficient financing

Capex protections None. Equity take construction risk

Cost of debt mechanism Minimised refinancing risk during operations

Refinancing risk £50m refinance gain assumed in the base case – at Equity risk

HMG grant Reduces overall subsidy requirement

HMG sharing mechanisms Reduces overall subsidy requirement

Cardiff payment Reduces overall subsidy requirement

Annual take of LCFPartially indexed strike prices mean the tidal lagoon take of the LCF decreases year on year

LCF assumed to remain at 2020/21 level of £7.6bn annually, in 2012 terms

If LCF is larger in reality, percentages will be lower

At a level of £10bn, all tidal lagoon figures would be under 2%

Power station Year 1 Year 5 Year 10 Year 35

Tidal Lagoon Swansea Bay 0.41% 0.36% 0.32% 0.14%

Tidal Lagoon Cardiff 2.06% 1.83% 1.33% -0.10%

Swansea & Cardiff 2.47% 2.19% 1.65% 0.04%

Hinkley Point C 9.67% 10.22% 9.87% 11.70%

Impact on consumer billsTidal lagoons have a low overall impact on bills – less so year on year

Project Technology Capacity Annual cost per household Impact on unit rateMW £2016/yr p2016/kWh

Tidal Lagoon Swansea Bay (30 yr average) Tidal lagoon 320 0.31 0.008

Tidal Lagoon Cardiff (30 yr average) Tidal lagoon 2,700 1.20 0.030

Hinkley Point C (CfD average) New nuclear 3,200 12.06 0.305

Burbo Bank Ex. (CfD average) Offshore wind 258 1.16 0.029

East Anglia 1 (CfD average) Offshore wind 714 2.18 0.055

Drax Unit 1 (CfD average) Biomass conversion 600 2.63 0.066

New CCGT (lifetime average) CCGT 880 2.18 0.055

Project Technology Capacity Annual cost per household Impact on unit rate

MW £2016/yr p2016/kWh

Tidal Lagoon Swansea Bay (60 yr average) Tidal lagoon 320 0.18 0.005

Tidal Lagoon Cardiff (60 yr average) Tidal lagoon 2,700 0.31 0.008

Hinkley Point C (60 yr average) New nuclear 3,200 7.03 0.178

Burbo Bank Ex. (60 yr average) Offshore wind 258 0.44 0.011

East Anglia 1 (60 yr average) Offshore wind 714 0.96 0.024

New CCGT (60 yr average) CCGT 880 2.23 0.057

CfD term or 30 year average

60 year average*

*Assumes new power stations are built to replace retired ones if required, at a reduced cost for offshore wind (£85/MWh, 2012prices), CCGT case is based on an LCOE of £80/MWh, 2012 prices

• Partial indexation means the consumer impact of tidal lagoons diminishes over time, competitive over the short term, they can provide improving value for money over the long term

60 year regret – wind and nuclear scenariosTidal lagoons represent ‘no-regrets options’ even under aggressive cost reductions for wind and new nuclear together

60 year regret - net subsidy position per equivalent MW (£'000)

Aurora assumptions

40% 66.0 (607) (502) (377) (188)

30% 77.0 (972) (867) (741) (553)

20% 88.0 (1,336) (1,231) (1,106) (917)

10% 99.0 (1,701) (1,596) (1,470) (1,282)

0% 110.0 (2,065) (1,961) (1,835) (1,647)

95.0 92.5 89.5 85.0

New nuclear price (£2012/MWh)

Decline in offshore wind CfD

price 2025 (£2012/MWh)

Wind starting point uses Aurora Energy Research assumptionsCosts of a wind and nuclear MW are scaled to represent the same volume of MWh delivered over a 60 year periodWind price evolution from starting 2025 price is based on middle scenario of 30% cost reduction per 15 year cycle and convergence on £60/MWh

System impacts of tidal lagoons: Aurora Energy Research study• 25GW of tidal lagoons would require

£0.7bn of system spending• This provides over 10% of the UK’s

energy requirement• CO2 emissions would be reduced by

36% in 2036 – a 130MT saving on the system between 2020-2040

• 25GW of tidal lagoons provide £270m of savings in the balancing mechanism compared to wind

• Tidal lagoons have lower intermittency costs than wind and solar

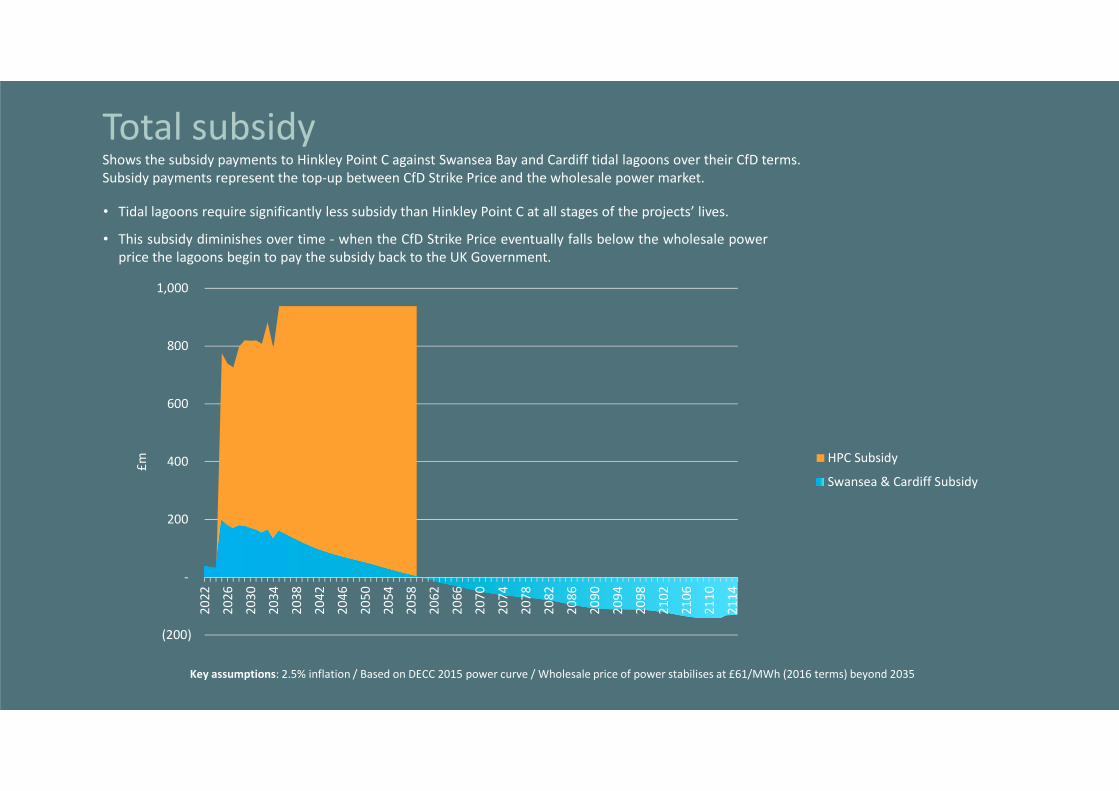

Total subsidyShows the subsidy payments to Hinkley Point C against Swansea Bay and Cardiff tidal lagoons over their CfD terms.Subsidy payments represent the top-up between CfD Strike Price and the wholesale power market.

• Tidal lagoons require significantly less subsidy than Hinkley Point C at all stages of the projects’ lives.

• This subsidy diminishes over time - when the CfD Strike Price eventually falls below the wholesale powerprice the lagoons begin to pay the subsidy back to the UK Government.

Key assumptions: 2.5% inflation / Based on DECC 2015 power curve / Wholesale price of power stabilises at £61/MWh (2016 terms) beyond 2035

(200)

-

200

400

600

800

1,000

2022

2026

2030

2034

2038

2042

2046

2050

2054

2058

2062

2066

2070

2074

2078

2082

2086

2090

2094

2098

2102

2106

2110

2114

£m

HPC Subsidy

Swansea & Cardiff Subsidy

0

1

2

3

4

5

6

7

8

9

10

Output Subsidy

Ratio Hinkley Point C

Swansea & Cardiff tidal lagoons (blended)

Hinkley Point C vs. Swansea Bay and Cardiff tidal lagoonsHead-to-head relative comparison over their respective CfD terms:

Key assumptions: 2.5% inflation / Based on DECC 2015 power curve / Wholesale price of power stabilises at £61/MWh (2016 terms) beyond 2035

Chart illustrates the ratio of electricitygenerated and subsidy received over CfDterm between Swansea Bay and Cardifftidal lagoons (combined capacity of3,560MW with a 90 year CfD) and HinkleyPoint C nuclear power station (capacity of3,200MW with a 35 year CfD).

86

1914

Global potential – France, India, China & Canada:Large scope for exports from UK supply chain

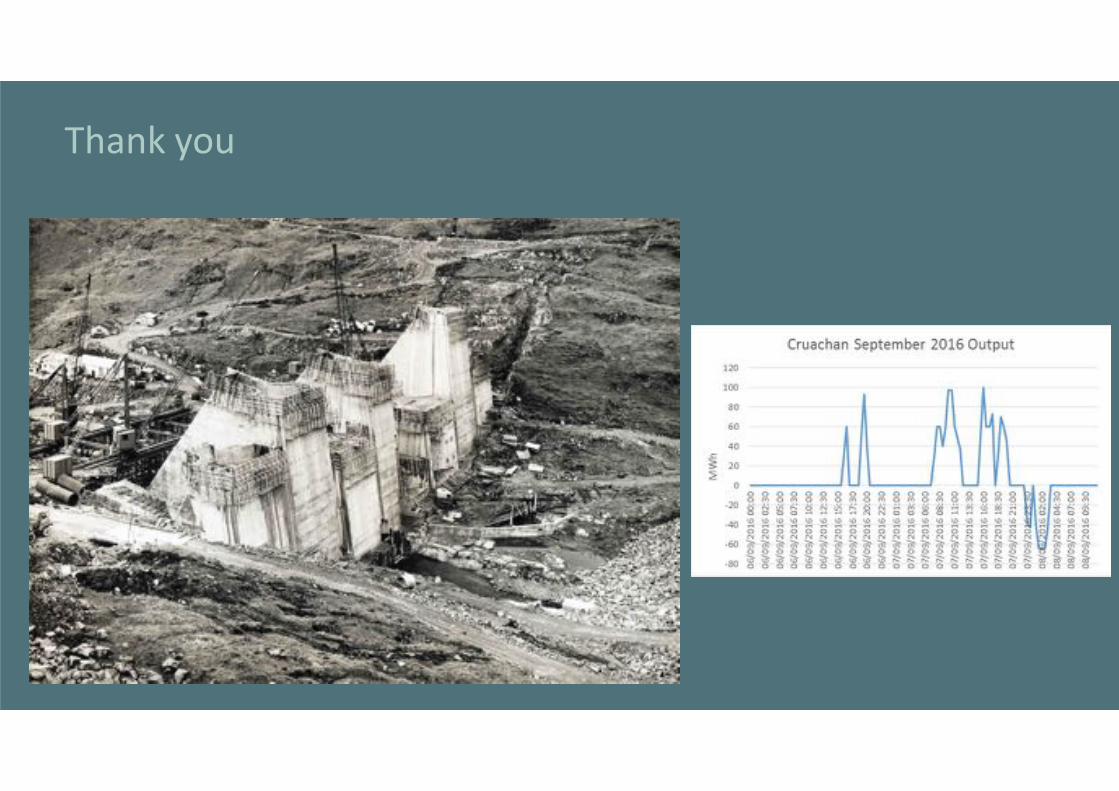

Thank you

![Esitys tarjouskilpailuun perustuvasta ... · Uusiutuvan energian pienyksikkö: vuosituotanto max 10 000 MWh [min. vuosituotanto 800 MWh] Tarjous Preemio €/MWh Vuosituotanto MWh](https://static.cupdf.com/doc/110x72/5f68f0e09636bc7f4a5fd91e/esitys-tarjouskilpailuun-perustuvasta-uusiutuvan-energian-pienyksikk-vuosituotanto.jpg)