MASTER DRILLING GROUP

International Raise Drilling Experts

November 2012

Private & Confidential

Page 2

DISCLAIMER

IMPORTANT NOTICE

This document has been compiled from information provided by the Directors of Master Drilling Group Limited (“Master Drilling”, “Master Drilling Group” or the “Company”) and

from publicly available sources, and involves elements of subjective judgment and analysis, which may or may not be correct, and have not been independently verified.

Accordingly, Master Drilling and its Advisors accept no responsibility for the correctness or otherwise of the content set out herein and no representation or warranty, express or

implied, is being made or given as to the accuracy or completeness of the information set out herein. The information contained in this document is subject to completion,

revision, verification and amendment without prior notice and without liability to compensate or reimburse any party.

No representation or warranty, express or implied is, or will be, given by Master Drilling or its Directors, Partners, Employees or Advisors or any other person as to the

accuracy, completeness or fairness of this document and, so far as permitted by law and except in the case of fraud by the party concerned, no responsibility or liability

whatsoever is accepted for the accuracy or sufficiency thereof or for any errors, omissions or misstatements negligent or otherwise relating thereto.

Master Drilling shall only be bound by those particular representations and warranties set forth in definitive written transaction documents, when and if such transaction

documents are executed and subject to such restrictions and limitations as may be contained therein.

This document may include certain statements, estimates, targets, forecasts and projections provided by Master Drilling. Such statements, estimates, targets, forecasts and

projections reflect significant assumptions and subjective judgments and analysis by Master Drilling’s management concerning anticipated future events which may or may not

prove to be correct and there can be no assurance that any estimates, targets, forecasts or projections are attainable or wil l be realised. Nothing contained in this document is,

or shall be relied upon as, a promise or representation, whether as to the past or the future. Accordingly, (subject as aforesaid) neither Master Drilling nor its Directors,

Partners, Employees or Advisors nor any other person, shall be liable for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on

any statement in or omission from this document and any such liability is expressly disclaimed. In particular, but without l imitation, no representation or warranty is given as to

the achievement or reasonableness of, and no reliance should be placed on, any estimates, targets, forecasts or projections contained in this document (or otherwise provided

by or on behalf of Master Drilling with respect to the subject matter of this document). In all cases, interested parties should conduct their own investigation and analysis of

Master Drilling and the information contained in this document before making any decisions.

This presentation and the documents provided with this presentation are confidential and may not be disclosed to any third party without the prior written consent of Master

Drilling.

Page 3

MASTER DRILLING GROUP

1. MASTER DRILLING GROUP OVERVIEW................................................................................................................... 4

2. INVESTMENT HIGHLIGHTS........................................................................................................................................ 11

3. CORPORATE STRATEGY............................................................................................................................................ 14

4. MAJOR CLIENTS AND COMMODITIES..................................................................................................................... 19

5. OPERATIONS............................................................................................................................................................... 23

6. HISTORICAL FINANCIALS.......................................................................................................................................... 28

7. OUTLOOK ON DRILLING SERVICES MARKET......................................................................................................... 32

Page 4

Master Drilling Group Overview

Page 5

1. MASTER DRILLING GROUP OVERVIEW

Company Overview

Master Drilling Background and Organogram:

Master Drilling was founded by Mr. Daniel Coenraad Pretorius

in 1986 and commenced raise-boring operations in South Africa

during the same year with two raisebore machines

Today, Master Drilling is one of the global leaders in the

raiseboring market, also providing other specialised drilling

services for mineral exploration and mining companies

Master Drilling currently operates 154 drilling rigs of various

sizes globally, in countries including South Africa, Zambia,

DRC, Burkina Faso, Mexico, Peru, Brazil and Chile

Master Drilling has 94 machines (84 raise borers, 5 drilling

related rigs and 5 blast hole / sampling rigs) active across its

operations in Africa and South America. This is one of the

largest fleets of raisebore machines globally

Master Drilling expanded into exploration drilling during 2005 by

acquiring a controlling stake in Drillcorp Africa (Pty) Ltd

(“Drillcorp”)

Drillcorp has a total of 60 exploration drilling rigs in operation

across numerous countries in sub-Saharan Africa, including

Burkina Faso, Zambia and DRC. These rigs include both

surface and underground diamond drill and reverse circulation

rigs

Master Drilling’s head office is located in Fochville, South

Africa. An engineering facility, which manufactures most of the

consumables and parts for the world fleet, is housed within the

same complex

Master Drilling International

Limited (“MDI”)

Master Drilling Group Limited 100%

MDI Exco

Limited

Kala SA

(Chile)

Master Drilling

do Brasil Ltda

(Brazil)

Master Drilling

Peru SAC

(Peru)

Master Drilling

Mexico SA

(Mexico)

Master Drilling

Zambia Limited

(Zambia)

Master Drilling

Australia (Pty)

Limited

(Australia)

Drillcorp

Burkina Faso

SA

(Burkina Faso)

Drillcorp Cote

d’Ivoire SA

(Cote d’Ivoire)

Master Drilling

South Africa

(Pty) Limited

(“MDSA”)

Drilling

Technical

Services (Pty)

Limited

Drillcorp Africa

(Pty) Limited

15%

85% 74%1 74%2 74%1

100%

100%

100%

100%

100%

100%

80%3

80%3 International Operations

SA Operations

1 – Remaining 26% held by Mosima Drilling (Pty) Limited

2 – Remaining 26% held by Epha Drilling (Pty) Limited

3 – Remaining 20% held by Moussa Kone

Page 6

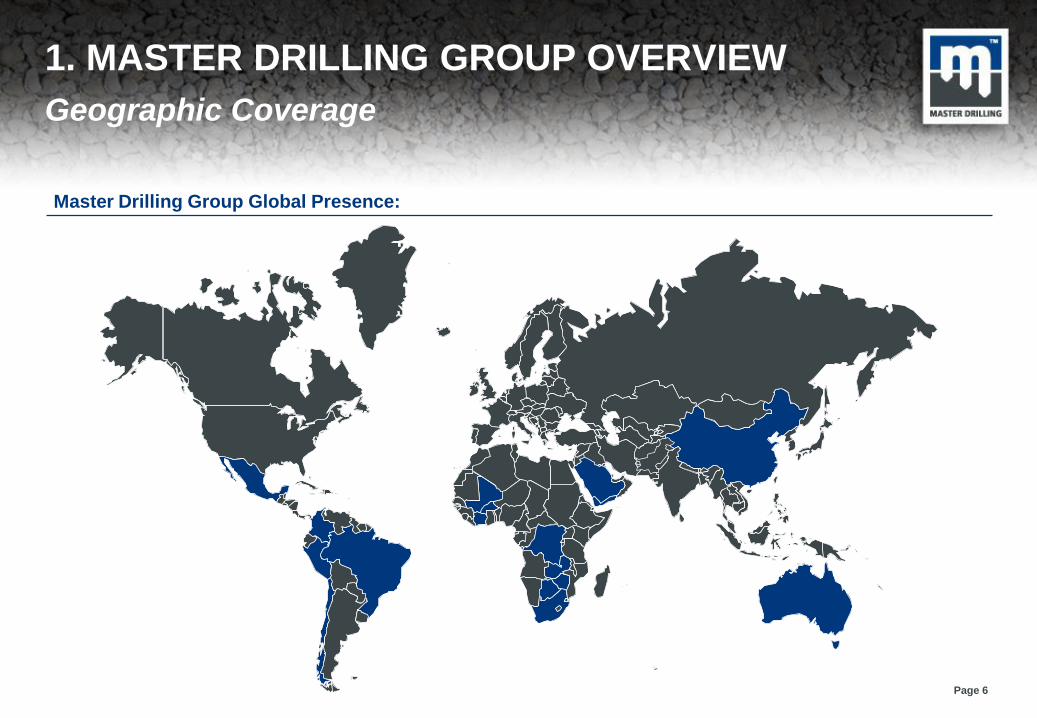

1. MASTER DRILLING GROUP OVERVIEW

Geographic Coverage

Master Drilling Group Global Presence:

Page 7

1. MASTER DRILLING GROUP OVERVIEW

Operational Milestones

Regional associates are established in Brazil and Zambia

First self designed, low profile blindhole / raiseborer (BHB200) was added to the fleet

Key Operational Milestones Since 2000:

2000

2001

2002

2003

2008

2004

2005

2006

2007

2009

2010

2011

Acquired the largest raisedrill ever built (HG380)

First stope long hole drilling contract commenced at Beatrix mine

First hole for the HG380 commenced at Anglo Platinum’s Amandelbult mine (501m x 4.5m diameter)

Acquired total fleet of boxhole machines from RUC

HG380 machine completed a 4.5m diameter and 500m in length hole at Amandelbult Platinum mine

Introduced a stope long hole drilling project at Mponeng mine

Designed and built a remote operated shot-crete application machine

Obtained coveted ISO9001:2000 accreditation

World’s fastest completion with HG380 machine at Tara Mines, Ireland (692m x 4.5m in 90 days)

Drilled Europe’s deepest 4m hole with HG380 machine at Tara Mines, Ireland (839m)

New cutter design implemented and stope drill mono rail system purposely built for Goldfield’s Kloof 3

Addition of new machines to the fleet

Design of the auto spanner

Shaft Support division. Training division introduced with virtual learning

Design of the gripper machine

Largest hole drilled to date with HG380 (7.3m diameter)

Designed first ever low profile Blind Hole borer (LP 150)

2012 Longest and most accurate raisebore hole ever drilled

Page 8

1. MASTER DRILLING GROUP OVERVIEW

Operational Photos

HG380 Raiseborer underground on site in Peru HG380 Raiseborer on surface at site in South Africa Blasthole drilling on site in Peru

Core drilling at site in Yemen Underground reamer head Underground holing of piloting process

Page 9

1. MASTER DRILLING GROUP OVERVIEW

Raisebore Drilling Overview

Raisebore Drilling – The Safer, Faster and More Accurate Method of Drilling:

Raisebore drilling is a method used to drill ore passes and

ventilation shafts required for production in an underground

mine, without the use of explosives

The raisebore drilling machine is set up on the upper level of

the two levels to be connected. A small pilot hole (c. 300mm in

diameter) is drilled to the level required. The pilot hole is then

reamed to a larger diameter (up to 6m in diameter) by attaching

a reamer head to the drillrods at the lower shaft and pulling it

back towards the drilling unit in a circular motion

The reamer head has a series of tungsten carbide cutters which

cut the rock during the circular motion. The drill cuttings from

the reamer head fall to the floor of the lower level and are

removed by a standard LHD loader

The boring principle is attractive because it offers the following

advantages over conventional drilling and blasting methods:

–Safer working conditions

–Speed of completion

–A hole which has a more stable structural shape

–A hole which has smooth sidewalls which has low

frictional loss in ventilation airways, and reduces the

likelihood of blockages in the ore-passes

HG380 Raisebore Machine

Reamer Head

Page 10

Fred G. Dixon GM, Drillcorp Africa

Mr. Fred G. Dixon is the

General Manager of

Drillcorp Africa Limited, a

position he has held for 6

years

Prior to joining Master

Drilling, Mr. Dixon was

employed in various

management roles over a

20 year career with Mittal

Steel in South Africa.

Specific roles include Plant

Manager, Project Manager

and Senior Draughtsman

In his work at Mittal Steel,

Mr. Dixon was responsible

for management of the

company’s heavy earth

moving equipment and

locomotives

Mr. Dixon holds an MBA

from Potchefstroom

University and a degree in

civil engineering from Vaal

Triangle Technicon

1. MASTER DRILLING GROUP OVERVIEW

Key Management Team

Daniël C. Pretorius Chief Executive Officer, MDG

Mr. Daniel (Danie) C.

Pretorius is the Founder

and Chief Executive

Officer of Master Drilling

Group Limited

Mr. Pretorius originally

founded Master Drilling in

1986 and has been

actively involved in

building the company for

over 25 years.

Mr. Pretorius is widely

considered a pioneer in

the field of raisebore

drilling, having helped

design the company’s

drilling fleet to meet the

needs of its clients

Prior to founding Master

Drilling, Mr. Pretorius was

an Engineer with Kuruman

Consolidated Asbestos,

Elandsrand Gold Mine,

Western Deep Levels Gold

Mine and RUC Mining

(now a division of Murray

& Roberts)

André J. Van Deventer Chief Financial Officer, MDG

Mr. André van Deventer is

the Chief Financial Officer

of Master Drilling Group

Limited, a position he has

held for the past 10 years

Joined Master Drilling as a

Financial Manager in 2001

and was appointed to

Board of Directors in 2002

Prior to joining Master

Drilling, Mr. Van Deventer

was a Financial Manager

at Beefmaster (Pty) Ltd, an

integrated beef business in

Kimberley, South Africa.

Before this, he was an

Accountant at Gericke,

Rademeyer & Newton

Walker in Klerksdorp,

South Africa

Mr. Van Deventer is a

member of the South

African Institute of

Chartered Accountants

Barend J. Jordaan Technical Director, MDG

Mr. Barend (Koos) J.

Jordaan is the Technical

Director of Master Drilling

Group Limited, a position

he has held for the past 11

years

Prior to joining Master

Drilling, Mr. Jordaan was a

Design and Project

Engineer for Joy Mining

Machinery in South Africa.

Before this, he was a

Technician for Orsmond

Aviation and a Design

Engineer for FEV

Motorentechnik

Mr. Jordaan holds a

degrees in Mechanical

Engineering from Pretoria

Technicon (now Tshwane

University of Technology)

and International

Technology Management

from University of

Gronigen, Netherland

MBA from Bond University,

Australia

Gareth R. Sheppard Director of Operations (Int.), MDG

Mr. Gareth R. Sheppard is

the Director for

International Operations of

Master Drilling Group

Limited, a position he has

held for the past 10 years

Mr. Sheppard joined

Master Drilling in 2001 as

Director of Master Drilling

Peru S.A.C. and Master

Drilling International Ltd

Joined the Board of

Directors of Master Drilling

Mexico SA de CV in 2005

and Master Drilling

Australia (Pty) Ltd in 2011

Mr. Sheppard holds a

degree in Mining

Engineering from Wits

University and an MBA

from Wits Business School

in South Africa

Member of Instituto de

Ingenieros de Minas del

Peru

Page 11

Investment Highlights

Page 12

2. INVESTMENT HIGHLIGHTS

Key Highlights

GLOBAL RAISEBORE DRILLING

SPECIALIST WITH

SUBSTANTIAL GROWTH

UPSIDE

STRONG PIPELINE OF ORDERS

FROM TOP-TIER MINING

CLIENTS

PREFERRED EMERGING

MARKET EXPOSURE WITH

BENEFIT OF COUNTRY AND

COMMODITY DIVERSIFICATION

SUPPORTIVE MARKET

CONDITIONS UNDERPINNED BY

ROBUST COMMODITY PRICES

WORLD CLASS MANAGEMENT

EXPERTISE

1

2 5

4 3

Page 13

2. INVESTMENT HIGHLIGHTS

Global Raiseboring Drilling Specialist Growth

GLOBAL LEADER

IN RAISE BORE

DRILLING

SERVICES

Niche drilling segment used extensively in on-mine development

(ventilation shafts and ore passes) by exiting producers

Raise bore drilling is highly differentiated to exploration drilling; it is

insulated from mining capital cycle (customers are major miners in

production not explorers), benefits from rising safety standards (increased

ventilation shafts) and increasing mining capital intensity (customers

seeking to extend existing operations rather than build new mines)

EXISTING CASH

FLOW

GENERATIVE

BUSINESS

Solid cash flow generative business, operating since 1986 with significant

growth history

FULLY

INTEGRATED

BUSINESS MODEL

Integrated business model including design, manufacture, service and

operation of rigs (including manufacture of bespoke rigs for customer

demands)

GOOD VISIBILITY

ON FUTURE

EARNINGS

Strong pipeline of orders from top-tier mining houses

WORLDWIDE

OPERATIONS 154 total rigs across 7 countries

WORLD CLASS

MANAGEMENT

EXPERTISE

Built business from start-up to global leader

OPERATIONAL

DIVERSIFICATION

Diversified exposure to mix of commodities and multiple emerging

markets

Historical Revenue:

Historical EBITDA:

0

10

20

30

40

50

60

70

80

90

100

2009FY 2010FY 2011FY 2012H1

US

$m

0

5

10

15

20

25

2009FY 2010FY 2011FY 2012H1

US

$m

Page 14

Corporate Strategy

Page 15

3. CORPORATE STRATEGY

Vision & Mission

Our vision is to be the global preferred supplier of efficient and reliable, high quality

drilling services and technology in the mining and civil engineering sectors

OUR VISION:

Our mission is to remain at the forefront of technological advancement through ongoing

research and development and continuous interaction with our customers, contributing to

improved customer business performance, now and in the future. Our key business

principles are quality, safety and integrity

OUR MISSION:

Page 16

3. CORPORATE STRATEGY

Organisational Culture

1. The quality of Master Drilling’s service is achieved through excellent planning, which takes into consideration every step of drilling

operations, in order to mitigate any possibility of a mistake in advance

2. Preventing pollution and wastage

3. Satisfaction of clients is paramount

4. Providing a safe working environment

5. Master Drilling carefully chooses its suppliers and subcontractors by taking into consideration their quality consciousness

6. Trained and qualified staff shall be employed in all functions of the Company. The knowledge and the responsibility for quality of all

employees is fostered by means of continuous skills development

7. Identify measurable, functional objectives during management review meetings

8. In providing its drilling service to mines and the civil construction industries, the Company strives to be as environmentally friendly as

possible. This includes the efforts of its employees to use equipment with care, making use of the Company’s resources and energy in a

manner that is as economical as possible in order to minimise waste

9. The consequences of Master Drilling’s work and the effectiveness of the SHEQ Management System are controlled regularly by means of

internal audits and annual management reviews by management where objectives are assessed and reported

“DOING THINGS RIGHT THE FIRST TIME” – WHAT IT MEANS TO MASTER DRILLING:

Master Drilling’s organisational culture focuses on “Doing Things Right the First Time”

Master Drilling is committed to cultivating a culture of quality through on-going employee training & development,

responsible & direct communication with clients and continuous improvement in service quality

Page 17

Peter J. Ledger Non Executive Chairman

3. CORPORATE STRATEGY

Corporate Governance & Strategic Planning

The Board of Directors of Master Drilling is responsible

for providing strategic direction and effective oversight

of corporate governance for the Company on a global

basis

The Board meets for scheduled meetings at least once

per quarter and otherwise as needed

Key responsibilities of the Board of Directors include:

Establish and review the Company’s Vision,

Objectives, Values and Strategic Plan

Establish and monitor firm-wide policies and

procedures which provide a framework for

effective and responsible management of the

Company

Oversight of appropriate programmes and

services offered in order to meet the needs of

clients and remain ahead of the competition

On an annual basis, establish specific business

objectives and identify key performance areas

for all major functions of the Company

Appoint senior management and efficiently

delegate responsibility for execution of key

objectives

Daniël C. Pretorius Chief Executive Officer

André J. Van Deventer Chief Financial Officer

Gareth R. Sheppard Executive Director

Barend J. Jordaan Executive Director

Shane Ferguson Non Executive Director

Roger Davey Non Executive Director

Jacques de Wet Non Executive Director

Corporate Governance & Strategic Planning:

Akhter A. Deshmukh Non Executive Director

Page 18

3. CORPORATE STRATEGY

SWOT Analysis

S Established client base among blue chip mining companies

Pioneer and market leader in technically specialised raisebore

drilling – creates competitive advantage vs. competitors

Primary focus on production-stage drilling – less influenced by

commodity price swings and/or capital market uncertainty

Contracts signed up to 1-2 years in advance of service delivery,

enabling high degree of future earnings visibility

Large fleet of specialised drill rigs, including one of the world’s

largest raisebore machines (HG380)

STRENGTHS:

OPPORTUNITIES:

O Expand geographical footprint to new target markets (Colombia,

DRC, Mali, Australia)

New technology development (Gripper – horizontal drilling)

Diversification into new market segments, including hydro

schemes (well drilling) and civil engineering

Improved brand recognition, both within mining industry and

amongst institutional capital market participants

Strategic and opportunistic acquisitions in new markets

W High quality, specialised raisebore services charged at premium

price point relative to competitors

High average fleet age

Lack of enterprise-wide IT platform (currently being addressed)

Low BBBEE score of local South African business – reduces

competitiveness when tendering for South African government

contracts

WEAKNESSES:

THREATS:

T Shortage of skilled labour inhibits rate of expansion (mineral

drilling more technically advanced skill than oil/gas, requiring

approx. 3 – 4 years to train supervisory/lead driller)

Exchange rate fluctuations for international operations

Closure of client mines caused by commodity price weakness,

capital shortage or other factors

Cash flow constraints inhibit ability to deliver on contracts

Deterioration in government relations in key markets

Sustained long-term capital market weakness

Page 19

Major Clients and Commodities

Page 20

2012 H1

4. MAJOR CLIENTS & COMMODITIES

Commodity Focus

Overview of MD Group Commodity Focus: MD Group Revenues by Commodity (2011 / 2012H1):

Master Drilling enjoys a degree of diversification through its

relative balance between precious and base metals exposure:

Gold & Silver: increasingly driven by investment demand

as safe haven and hedge against US dollar inflation

PGMs: remain subject to developed market demand,

particularly EU automobile consumption

Base Metals: remain vital to urbanisation and

industrialisation of BRICs and other emerging markets

In light of recent commodity price volatility, the Company’s

management has identified commodity diversification as a high

priority short-term focus area

In particular, Master Drilling is targeting revenue growth and

diversification in the coal, iron ore and ferroalloys (chrome,

manganese) sectors in South Africa

Iron ore and ferroalloys exposure will provide cyclical

diversification, as steel is an early-cycle industry vs. precious

metals and PGMs (typically late-cycle)

Additionally, the Company seeks to expand service offering in

the civil engineering sector, particularly for underground

development at large hydro-electric projects

PRECIOUS & BASE METALS ANCHOR PORTFOLIO, BUT AIM TO EXPAND IN COAL, FERROALLOYS & CIVIL ENGINEERING

26%

17%

20%

11%

8%

7% 2%

2% 1% 6% Gold

Copper

PGM

Silver/Lead/ Zinc & Copper

Gold/Silver

Coal

Silver

Zinc/Lead

Chrome

Other

2011

26%

15%

24%

12%

5%

12%

1% 2% 1% 2%

Gold

Copper

PGM

Silver/Lead/ Zinc & Copper

Gold/Silver

Coal

Silver

Zinc/Lead

Chrome

Other

Page 21

20%

0%

10%

25% 9%

5%

-19%

8% 4% 12%

3%

8%

28%

6%

8%

-19%

8%

8%

-6

-4

-2

0

2

4

6

8

10

12

14

16

H1 2012 2011 2010 2009

US

$m

MD Zambia

MD Peru

MD Brazil

MD Mexico

Kala

MDI

Drillcorp Africa

Drilling Technical Services

MDSA

4. MAJOR CLIENTS & COMMODITIES

Geographical Focus

Overview of MD Group Geographical Focus: MD Profit for the Year by Geography (2009 – 2012H1):

Master Drilling is capable of offering specialised drilling services

virtually anywhere in the world and is not limited to specific

countries or regions. Contracts can be effectively mobilised as a

self-contained business unit on a temporary basis

Principal focus on the drilling services markets in Africa and

Latin America, including continuing operations in South Africa,

Peru, Chile, Brazil, Mexico and Zambia

In addition to continuing operations, Master Drilling carries our

projects in various other countries, including Burkina Faso,

Zimbabwe, Botswana and Saudi Arabia

Master Drilling recently registered a subsidiary in China, where

it engages in manufacturing and trading. The Chinese drilling

market is a target for future revenue expansion

Established brand name and market leader in raisebore drilling

amongst major South African mining companies

Rapid revenue growth in Latin American markets, where Master

Drilling is often the monopoly supplier of raisebore technology

Other expansion opportunities exist in Colombia, DRC, Mali,

Australia and other high opportunity markets

ESTABLISHED BRAND IN SOUTH AFRICA, WITH RAPID REVENUE GROWTH IN LATIN AMERICA & OTHER AFRICA

2011 2012 H1

1Positive values excludes loss from MD Brazil

1 1 1

Page 22

4. MAJOR CLIENTS & COMMODITIES

Selected Existing Client Base

AFRICA: LATIN AMERICA:

CLIENT BASE PRIMARILY COMPRISED OF BLUE-CHIP MAJOR & MID-TIER MINING COMPANIES

Page 23

Operations

Page 24

5. OPERATIONS

Service Offering

Master Drilling’s Specialised Service Offering:

Master Drilling provides both primary and secondary services to

its clients, depending on the terms of each individual contract

Primary services offered by Master Drilling include:

− Raisebore drilling

− Box hole & slot riser boring/drilling

− Drain hole drilling

− Drop raising

− Shaft support

− Surface blast hole drilling

Primary services offered by Drillcorp Africa include:

− Core drilling

− Percussion drilling

− Reverse circulation drilling

Secondary services are offered in contracts where the scope

of services exceeds the core, primary services on offer. These

are either offered directly by Master Drilling or alternatively sub-

contracted to third party providers

− Earthworks, piling & foundation construction

− Directional drilling & wedging

− Core logging & cutting

Equipment supply services are offered to the MD Group

companies by Drilling Technical Services and MD China

RAISEBORE

DRILLING

Used to drill smooth ore passes and

ventilation shafts in underground mines,

without the use of explosives

Further applications in civil engineering,

particularly underground hydro schemes

Significant advantages including no

blasting (ie. no fracturing), safety, speed,

accuracy and depth capability

Requires stable ground conditions

SLOT & DROP

RAISING

Raise excavation which is completely pre-

drilled over full length and blasted from

bottom at appropriate lengths

Advantages of safety and low cost

BLAST HOLE

DRILLING

Used to drill consistent blast patterns in

time-effective manner for open pit mines

Typically used in large surface operations

with high production rates (coal & bulks)

EXPLORATION

DRILLING

Core drilling, percussion drilling and

reverse circulation drilling used in

discovery of new mineral deposits and

determination of grade & continuity

Page 25

5. OPERATIONS

Key Performance Metrics

Key Operational Performance Metrics:

Master Drilling’s management team uses a variety of Key Performance Indicators (KPIs) to monitor the Company’s performance against

targeted objectives:

− Rig Availability (%)

− Rig Utilisation (%)

− Achieved Drilling Hours (hours drilled per day)

− Achieved Penetration Rates (metres driller per hour)

− Revenue Contribution per Rig (US$ per machine)

Achieved and targeted performance metrics are reviewed by senior management on a quarterly basis

Key Performance Indicators Summary:

2009 2010 2011 2012a

Total Capital Project and Production Stage Rigs 68 73 78 87

Utilisation Percentage 65% 80% 80% 74%

ARPOR (US$) 54,386 66,235 78,502 73,401

Total Exploration Stage Rigs 40 43 54 60

Utilisation Percentage 39% 23% 58% 67%

ARPOR (US$) 16,859 16,531 29,989 22,724

Source: Master Drilling Group Limited a As at 30 June

Page 26

Maintain sufficient working capital and balance sheet

strength to weather economic downturns

RISK MANAGEMENT & MITIGANTS:

Focus on diversification across key commodity groups,

including early, mid and late-cycle commodities

Geographical diversification and active relationship

management with local government authorities

Cultivate future senior managers from within through

continual investment in employee training and development

Core raiseboring business is a specialised, niche market in

which Master Drilling is a leading recognised provider

Aim to match currency of revenues, costs and liabilities;

utilise FX hedging instruments where possible

Management expertise and prudence in accepting contracts;

DTS subsidiary ensures availability of custom supplies

5. OPERATIONS

Risks & Mitigants

MACROECONOMIC RISK:

Global economic downturn & capital market weakness

SELECTED KEY RISKS TO MASTER DRILLING:

COMMODITY MARKET RISK:

Exposure to fluctuations in commodity prices

GEOPOLITICAL RISK:

Heightened risk in high opportunity emerging markets

PERSONNEL RISK:

Loss of key managers & inability to recruit/retain skilled personnel

COMPETITION RISK:

Competition from alternative suppliers of drilling services

FOREIGN EXCHANGE RISK:

Exposure to fluctuations in foreign exchange rates

OPERATIONAL RISK:

Management failure to successfully execute on contracts

Page 27

0

20

40

60

80

100

120

140

160

180

2009 2010 2011 Aug 2012

Nu

mb

er

of

Dri

ll R

igs

XXL Raisebore

X Large Raisebore

Large Raisebore

Medium Raisebore

Small Raisebore

Other Specialised Rigs

Blast Hole

Drain / Slot Hole

Blind Hole

Exploration Rigs

33

46

63

27

11

12

10

9

9

9

21

10

0

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012H1

Rev

en

ues (

US

$ m

illio

n)

Exploration Stage

Capital Project Stage

Production Stage

5. OPERATIONS

Group Operational Drill Rigs

Group Revenues by Drilling Type, 2009 – 2012H1: Group Total Drill Rigs by Machine Type, 2009 – 2012:

Total:

110

Total:

120

Total:

138

Total:

154

Computational reconciliation of totals may not be possible due to independent rounding

Source: Master Drilling Group Limited

Total:

$53m

Total:

$67m

Total:

$95m

Total:

$46m

Page 28

Historical Financials

Page 29

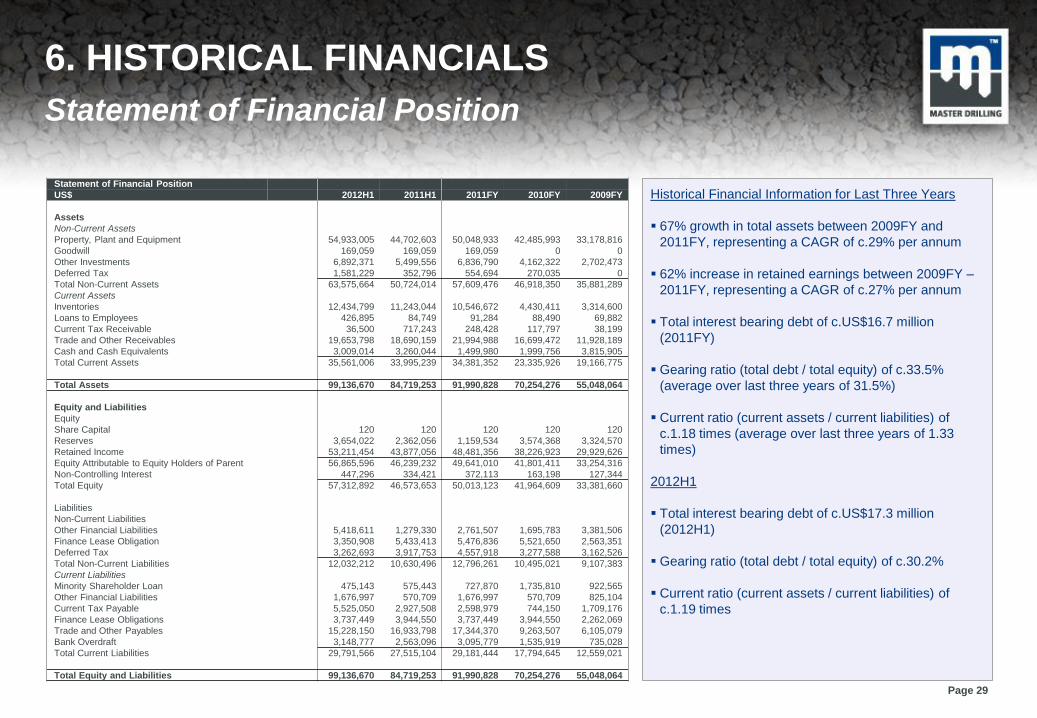

6. HISTORICAL FINANCIALS

Statement of Financial Position

Statement of Financial Position

US$ 2012H1 2011H1 2011FY 2010FY 2009FY

Assets

Non-Current Assets

Property, Plant and Equipment 54,933,005 44,702,603 50,048,933 42,485,993 33,178,816

Goodwill 169,059 169,059 169,059 0 0

Other Investments 6,892,371 5,499,556 6,836,790 4,162,322 2,702,473

Deferred Tax 1,581,229 352,796 554,694 270,035 0

Total Non-Current Assets 63,575,664 50,724,014 57,609,476 46,918,350 35,881,289

Current Assets

Inventories 12,434,799 11,243,044 10,546,672 4,430,411 3,314,600

Loans to Employees 426,895 84,749 91,284 88,490 69,882

Current Tax Receivable 36,500 717,243 248,428 117,797 38,199

Trade and Other Receivables 19,653,798 18,690,159 21,994,988 16,699,472 11,928,189

Cash and Cash Equivalents 3,009,014 3,260,044 1,499,980 1,999,756 3,815,905

Total Current Assets 35,561,006 33,995,239 34,381,352 23,335,926 19,166,775

Total Assets 99,136,670 84,719,253 91,990,828 70,254,276 55,048,064

Equity and Liabilities

Equity

Share Capital 120 120 120 120 120

Reserves 3,654,022 2,362,056 1,159,534 3,574,368 3,324,570

Retained Income 53,211,454 43,877,056 48,481,356 38,226,923 29,929,626

Equity Attributable to Equity Holders of Parent 56,865,596 46,239,232 49,641,010 41,801,411 33,254,316

Non-Controlling Interest 447,296 334,421 372,113 163,198 127,344

Total Equity 57,312,892 46,573,653 50,013,123 41,964,609 33,381,660

Liabilities

Non-Current Liabilities

Other Financial Liabilities 5,418,611 1,279,330 2,761,507 1,695,783 3,381,506

Finance Lease Obligation 3,350,908 5,433,413 5,476,836 5,521,650 2,563,351

Deferred Tax 3,262,693 3,917,753 4,557,918 3,277,588 3,162,526

Total Non-Current Liabilities 12,032,212 10,630,496 12,796,261 10,495,021 9,107,383

Current Liabilities

Minority Shareholder Loan 475,143 575,443 727,870 1,735,810 922,565

Other Financial Liabilities 1,676,997 570,709 1,676,997 570,709 825,104

Current Tax Payable 5,525,050 2,927,508 2,598,979 744,150 1,709,176

Finance Lease Obligations 3,737,449 3,944,550 3,737,449 3,944,550 2,262,069

Trade and Other Payables 15,228,150 16,933,798 17,344,370 9,263,507 6,105,079

Bank Overdraft 3,148,777 2,563,096 3,095,779 1,535,919 735,028

Total Current Liabilities 29,791,566 27,515,104 29,181,444 17,794,645 12,559,021

Total Equity and Liabilities 99,136,670 84,719,253 91,990,828 70,254,276 55,048,064

Historical Financial Information for Last Three Years

67% growth in total assets between 2009FY and

2011FY, representing a CAGR of c.29% per annum

62% increase in retained earnings between 2009FY –

2011FY, representing a CAGR of c.27% per annum

Total interest bearing debt of c.US$16.7 million

(2011FY)

Gearing ratio (total debt / total equity) of c.33.5%

(average over last three years of 31.5%)

Current ratio (current assets / current liabilities) of

c.1.18 times (average over last three years of 1.33

times)

2012H1

Total interest bearing debt of c.US$17.3 million

(2012H1)

Gearing ratio (total debt / total equity) of c.30.2%

Current ratio (current assets / current liabilities) of

c.1.19 times

Page 30

Statement of Comprehensive Income

US$ 2012H1 2011H1 2011FY 2010FY 2009FY

Continuing Operations

Revenue 45,713,505 46,197,088 94,631,187 66,694,491 52,982,060

Cost of Sales (30,930,366) (28,019,592) (66,164,018) (46,013,406) (35,211,863)

Gross Profit 14,783,139 18,177,496 28,467,169 20,681,085 17,770,197

Other Income 1,138,576 1,001,011 1,263,783 2,688,485 567,939

Operating Expenses (9,138,283) (10,252,488) (12,382,027) (11,108,114) (8,896,831)

Operating Profit 6,783,432 8,926,019 17,348,925 12,261,456 9,441,305

Investment Revenue 170,809 149,548 223,795 90,767 65,813

Finance Costs (1,131,762) (894,211) (1,997,265) (1,291,916) (887,213)

Profit Before Taxation 5,822,479 8,181,356 15,575,455 11,060,307 8,619,905

Taxation (1,017,198) (2,360,000) (3,900,547) (2,074,509) (2,700,975)

Profit From Continuing Operations 4,805,281 5,821,356 11,674,908 8,985,798 5,918,930

Discontinued Operations

Loss from Discontinued Operations (630,249)

Profit For The Year 4,805,281 5,821,356 11,044,659 8,985,798 5,918,930

Other Comprehensive Income

Exchange Differences on Translating Foreign

Operations 2,471,216 (1,301,133) (2,122,348) 83,721 1,897,048

Gains and Losses on Property Revaluation 23,272 (46,014) (292,486) 166,077 298,607

Other Comprehensive (Loss) Income for the

Year 2,494,488 (1,347,147) (2,414,834) 249,798 2,195,655

Total Comprehensive Income 7,299,769 4,609,043 8,629,825 9,235,596 8,114,585

Net Profit Attributable To:

Owners Of The Parent:

Profit for the Year from Continuing Operations 4,730,098 5,650,133 11,465,993 8,949,944 5,855,181

Loss for the Year from Discontinuing Operations (630,249)

Profit for the Year Attributable to Owners of the

Parent 4,730,098 5,650,133 10,835,744 8,949,944 5,855,181

Non-Controlling Interest:

Profit for the Year from Continuing Operations 75,183 171,223 208,915 35,854 63,749

Total Comprehensive Income Attributable To:

Owners of the Parent 7,224,586 4,437,820 8,420,910 9,199,742 8,050,836

Non-Controlling Interest 75,183 171,223 208,915 35,854 63,749

Total Comprehensive Income 7,299,769 4,609,043 8,629,825 9,235,596 8,114,585

6. HISTORICAL FINANCIALS

Statement of Comprehensive Income

Historical Financial Information for Last Three Years

Top-line revenue growth of 79% between 2009FY and

2011FY, representing a CAGR of c.34% per annum

Gross margin of 30% in 2011FY (average over last

three years of c.32%)

Operating margin of 18% in 2011FY (average over last

three years of 18%)

Net profit margin of 12% in 2011FY (average over last

three years of 12%)

Adjusted EBITDA US$11.5m, US$13.7m & US$19.2m

(2009FY, 2010FY & 2011FY)

Net profit from continuing operations increased 97%

between 2009FY and 2011FY, representing a CAGR of

c.40% per annum

Loss from discontinued operations represents the

Company’s decision to discontinue its exploration

operations in Brazil. The assets from this operation

have been transferred to other operating entities in the

Group

2012H1

Adjusted EBITDA US$11.2m & US$8.2m (2011H1 &

2012H1)

Page 31

Statement of Cash Flows

US$ 2012H1 2011H1 2011FY 2010FY 2009FY

Cash Flows from Operating Activities

Cash Generated from Operations 6,484,069 10,390,757 14,752,818 8,755,460 6,345,569

Interest Income 170,809 149,548 223,795 479,303 514,187

Finance Costs (1,131,762) (894,211) (1,997,265) (1,220,383) (719,871)

Tax Paid 2,120,801 (135,923) (896,289) (3,004,071) (1,505,253)

Net Cash from Operating Activities 7,643,917 9,510,171 12,083,059 5,010,309 4,634,632

Cash Flows from Investing Activities

Purchase of Property, Plant and Equipment (7,670,022) (6,083,529) (9,476,837) (10,737,468) (11,650,315)

Sale of Property, Plant and Equipment 1,473,490 1,242,503 843,991 2,207,621 2,570,003

Increase in Goodwill (169,059)

Sale of Financial Assets (1,026,535) 82,761 (284,659) (270,035) 0

Net Cash from Investing Activities (7,223,067) (4,927,324) (8,917,505) (8,799,882) (9,080,312)

Cash Flows from Financing Activites

Proceeds / (Repayment) of Financial Liabilities 2,657,104 (416,453) 2,172,012 (1,632,039) 4,206,610

Movement in Loans to Employees (335,611) 3,741 (2,794) (18,608) (69,882)

Proceeds from Shareholders Loan 1,427,917

Repayment of Shareholders Loan (55,581) (1,337,234) (2,674,471) (1,459,849)

Repayment of / (Proceeds on) Minority Shareholder Loan (252,727) (1,160,367) (1,007,940) 813,245 922,565

Acquisition of Additional Shares in Subsidiary (1,302,377)

Finance Lease Payments (1,988,683) (1,186,062) (1,932,560) 4,569,247 1,738,027

Dividends Paid (581,311) (652,647) (375,818)

Net Cash from Financing Activities 24,502 (4,096,375) (4,321,501) 498,025 6,926,854

Total Cash Movement for the Year 445,352 320,950 (2,163,887) (2,478,303) 3,403,739

Cash at the Beginning of the Year (595,799) 463,837 463,837 3,080,877 (352,244)

Effect of Exchange Rate Movement on Cash Balances 10,684 (87,839) 104,251 (138,737) 0

Total Cash at End of the Year (139,763) 696,948 (1,595,799) 463,837 3,080,877

6. HISTORICAL FINANCIALS

Statement of Cash Flows

Historical Financial Information for Last Three Years

Cash generated from operations increased by 132%

between 2009FY and 2011FY, representing a CAGR of

c.52% per annum

Increase in net cash from operating activities of 161%

between 2009FY and 2011FY, representing a CAGR of

c.61% per annum

Historically, the majority of Master Drilling’s operating

cash flow has been reinvested into the business to

pursue expansion opportunities

In 2011FY, purchases of PP&E represented c.78% of

net cash generated from operating activities (average

over last three years of c.181%)

Page 32

Outlook on Drilling Services Market

Page 33

7. OUTLOOK ON DRILLING SERVICES MARKET

Overview of Drilling Services Industry

Market correlated to commodity prices & capital markets:

Exploration and development drilling are highly correlated to

commodity prices, mining company equity financings, mining

acquisitions and mine site activity

Drilling services demand for production-stage clients is considerably

less volatile than exploration/development clients due to lower

dependence on commodity prices and equity market financing

Exploration budgets of both senior and early-stage exploration

companies are key leading indicators of global demand for drilling

services

In 2008, high commodity prices drove exploration activity to record

highs with global exploration spending approaching US$14 billion

During the global economic slowdown of 2009, mineral exploration

expenditures fell by over 40%, but have since recovered

Funding for junior miners dried up during financial crisis, resulting in

delay or cancellation of many pre-production mining projects globally

Current outlook for gold and base metal exploration is positive, as

emerging markets continue to drive global demand for commodities

Mineral reserves of both precious and base metals have been

increasingly depleted during the past decade

Reduction in both mine lives and mined grade likely to lead to an

extended recovery in exploration and development activity

EXPLORATION

DRILLING

SERVICES

MINE

DEVELOPMENT

DRILLING

SERVICES

PRODUCTION

DRILLING

SERVICES

Focussed on discovery of new

mineral deposits and to determine

whether reserves are sufficient to

justify project development

High volatility due to dependence

on junior miners, commodity

cycles and availability of financing

Initial establishment of mine

infrastructure, including tunnels,

ventilation shafts, dewatering

systems and ore passes

Continued core drilling for accurate

definition of geological conditions

Tends to be high margin

Multiple purposes, including

establishment or expansion or

ventilation shafts and ore passes

Typically undertaken for majors

and established mining

companies, resulting in greater

contract frequency and reliability

Page 34

-25%

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

Jan 0

9

Ap

r 0

9

Ju

l 0

9

Oct 0

9

Ja

n 1

0

Apr

10

Ju

l 1

0

Oct 1

0

Ja

n 1

1

Apr

11

Ju

l 1

1

Oct 1

1

Ja

n 1

2

Ap

r 1

2

Ju

l 1

2

Pri

ce P

erf

orm

an

ce

(2

00

9 =

0%

) Gold Spot (US$/oz)

Copper Spot (US$/lb)

-100%

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

1000%

1100%

Ja

n 0

9

Ap

r 0

9

Ju

l 0

9

Oct 0

9

Jan 1

0

Ap

r 1

0

Ju

l 1

0

Oct 1

0

Ja

n 1

1

Ap

r 1

1

Ju

l 1

1

Oct 1

1

Ja

n 1

2

Ap

r 1

2

Ju

l 1

2

Boart Longyear Ltd

Major Drilling Group Int.

Ausdrill Ltd

Foraco International

Energold Drilling Corp

MSCI M&M Index

7. OUTLOOK ON DRILLING SERVICES MARKET

Performance of Key Commodities & Drilling Equities

Rising gold & copper prices benefit drillers: Drilling equities outperformed mining index since ‘09:

Source: Bloomberg Finance L.P. Source: Bloomberg Finance L.P.

-6%

57%

179%

250% 304%

580%

101%

175%

Page 35

9

22

33

19

54

34

38

0

10

20

30

40

50

60

2005

2006

2007

2008

2009

2010

2011

Eq

uit

y C

ap

ital R

ais

ed

* (

US

$b

n)

*Includes IPO, follow-on equity

and convertible bonds across

ASX, TSX, TSX-V, London,

London AIM and JSE markets

7. OUTLOOK ON DRILLING SERVICES MARKET

Mining Capital Raising & Exploration Spending

Large increase in mining capital raised since ‘05: Robust recovery in exploration spend post–GFC:

Source: Thomson Financial Source: Metals Economics Group, 2012

2.7

4.4

6.0

8.8

12.2

15.1

8.5

12.4

16.3

19.0

20.4

19.3

17.1

18.0

20.8

0

5

10

15

20

25

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012e

2013e

2014e

2015e

2016e

2017e

No

n-F

err

ou

s E

xp

lora

tio

n S

pen

din

g (

US

$b

)

Page 36

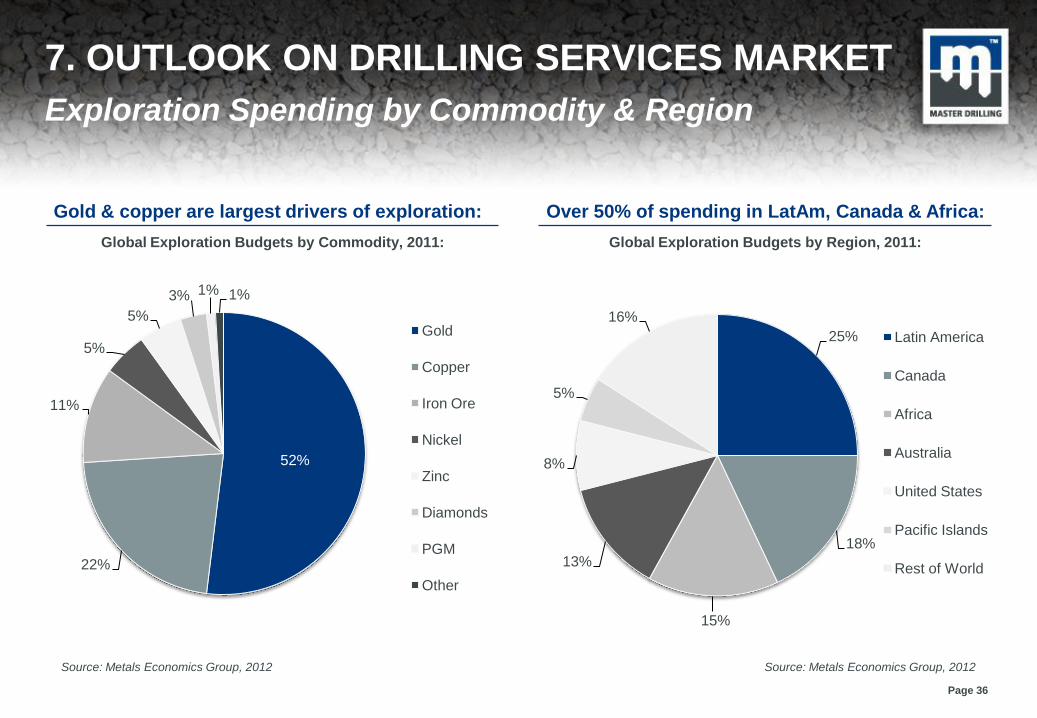

52%

22%

11%

5%

5%

3% 1% 1%

Gold

Copper

Iron Ore

Nickel

Zinc

Diamonds

PGM

Other

7. OUTLOOK ON DRILLING SERVICES MARKET

Exploration Spending by Commodity & Region

Gold & copper are largest drivers of exploration: Over 50% of spending in LatAm, Canada & Africa:

Source: Metals Economics Group, 2012 Source: Metals Economics Group, 2012

Global Exploration Budgets by Commodity, 2011: Global Exploration Budgets by Region, 2011:

25%

18%

15%

13%

8%

5%

16%

Latin America

Canada

Africa

Australia

United States

Pacific Islands

Rest of World

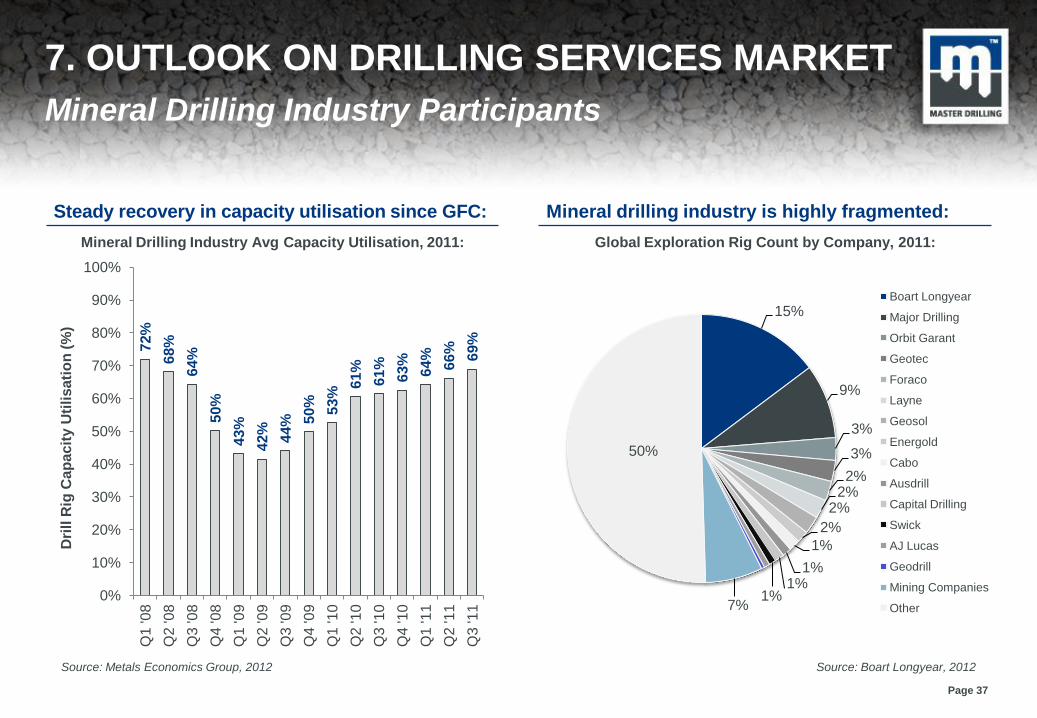

Page 37

72%

68%

64%

50%

43%

42%

44%

50%

53%

61%

61%

63

%

64%

66%

69%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 '0

8

Q2

'08

Q3

'08

Q4

'08

Q1

'09

Q2

'09

Q3

'09

Q4

'09

Q1

'10

Q2 '1

0

Q3

'10

Q4

'10

Q1

'11

Q2

'11

Q3

'11

Dri

ll R

ig C

ap

acit

y U

tili

sati

on

(%

) 7. OUTLOOK ON DRILLING SERVICES MARKET

Mineral Drilling Industry Participants

Steady recovery in capacity utilisation since GFC: Mineral drilling industry is highly fragmented:

Source: Metals Economics Group, 2012 Source: Boart Longyear, 2012

Mineral Drilling Industry Avg Capacity Utilisation, 2011: Global Exploration Rig Count by Company, 2011:

15%

9%

3%

3%

2% 2%

2%

2%

1%

1% 1%

1% 7%

50%

Boart Longyear

Major Drilling

Orbit Garant

Geotec

Foraco

Layne

Geosol

Energold

Cabo

Ausdrill

Capital Drilling

Swick

AJ Lucas

Geodrill

Mining Companies

Other