Lenhardt & Colton, LLC

Process-Based ManagementProcess-Based Management

City XXX Public Utilities

February 22, 2001

Lenhardt & Colton, LLC Slide 2

February 22, 2001

Today’s ObjectiveToday’s Objective

To Reaffirm:– The Need for Change in the Way XPU

Manages Its Business– The Preference of XPU for

• Process-Based Management• Process-Based Information Tools

– A Path & Timetable That Has Initial Process-Based Solutions Implemented in 2002

Lenhardt & Colton, LLC Slide 3

February 22, 2001

Today’s AgendaToday’s Agenda

The Case for Change at XPU

Why Process-Based?

Insights from a Real Life Project

XPU’s Roadmap

Lenhardt & Colton, LLC Slide 4

February 22, 2001

The Starting Point:The Starting Point:XPU Decides It Must XPU Decides It Must

Change Change 1996 Annual Report: “...an internal transition

designed to prepare staff and the Utility Board to operate the electric utility in an environment of increasing options for our electric customers.”

1997 Annual Report: “XPU’s efforts in the coming years will be to prepare for operating in a competitive market.”

1999 Strategic Plan: “Focus on FINANCIAL AWARENESS at a departmental level to drive us toward competitive rates.”

Lenhardt & Colton, LLC Slide 5

February 22, 2001

Then how do you decide?Then how do you decide?

……what to change?what to change?

. . . what to do differently?. . . what to do differently?

Lenhardt & Colton, LLC Slide 6

February 22, 2001

One Useful ModelOne Useful Model

BusinessIssues

BusinessDecisions

Informationfor

Decisions

InformationTools

BusinessIssues

BusinessDecisions

Informationfor

Decisions

InformationTools

What Needs Changed?

Lenhardt & Colton, LLC Slide 7

February 22, 2001

Identifying Needed ChangesIdentifying Needed Changes

BusinessIssues

BusinessDecisions

Informationfor

Decisions

InformationTools

Changing Business Issues are a Given; the Cause of

XPU’s Dilemma

XPU Wants More Business Decisions To

Be Made by Managers

XPU Needs New & Different Decision

Support Information

XPU Needs New & Different Tools to

Provide That Information

We’ll Look at Each of These in Turn

Lenhardt & Colton, LLC Slide 8

February 22, 2001

Engaging XPU’s ManagersEngaging XPU’s Managers

Role of an XPU Manager ChangeDo Functional Work

Manage the Department• Supervise Work

(Organize,Plan, Monitor, etc.)

• Manage People(Motivate, Discipline, etc.)

• Manage Resources(Workload, Operating Budget)

Participate in XPU Business Mgmt(Collaborative & Communicate Financial Impacts)

Other

Lenhardt & Colton, LLC Slide 9

February 22, 2001

Another Useful ModelAnother Useful Model

Three Time Perspectives of Business

YesterdayResults Perspective

TodayOperations Perspective

TomorrowStrategic Perspective

Lenhardt & Colton, LLC Slide 10

February 22, 2001

TodayOperations Perspective

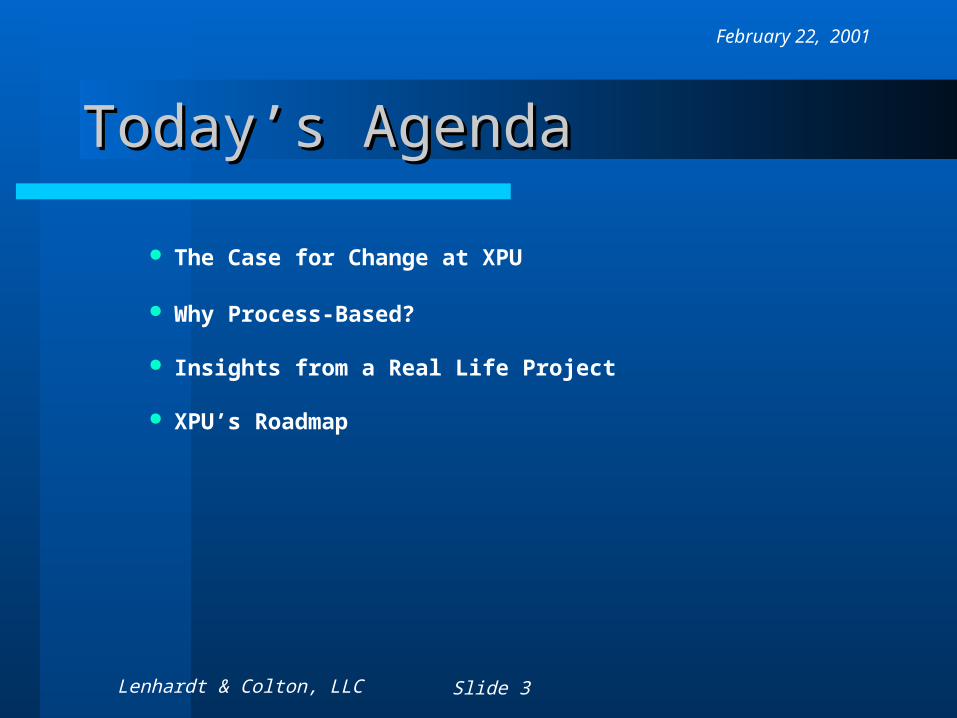

Three Kinds of Issues & DecisionsThree Kinds of Issues & Decisions

How is XPU doing “today”?Should I invest in

this XPU bond?What should I charge for this new service?

These Require Three Different Kinds of Information

YesterdayResults Perspective

TomorrowStrategic Perspective

How did XPU do

“yesterday”?

How will XPU do “tomorrow”?Where is the best opportunity to

improve our process?

Lenhardt & Colton, LLC Slide 11

February 22, 2001

Three Kinds of Information ToolsThree Kinds of Information Tools

YesterdayResults Perspective Today

Operations Perspective

TomorrowStrategic Perspective

What Tools Does XPU Have in Place Today?

Lenhardt & Colton, LLC Slide 12

February 22, 2001

XPU’s Existing Information ToolsXPU’s Existing Information Tools

YesterdayResults Perspective Today

Operations Perspective

TomorrowStrategic Perspective

SAP Financials

Little or NoInformation Available

Even LessInformation Available

Lenhardt & Colton, LLC Slide 13

February 22, 2001

Review Needed ChangesReview Needed Changes

BusinessIssues

BusinessDecisions

Informationfor

Decisions

InformationTools

XPU Wants More Business Decisions To

Be Made by Managers

XPU Needs New & Different Decision

Support Information

XPU Needs New & Different Tools to

Provide That Information

Lenhardt & Colton, LLC Slide 14

February 22, 2001

Today’s AgendaToday’s Agenda

The Case for Change at XPU

Why Process-Based?

Insights from a Real Life Project

XPU’s Roadmap

Lenhardt & Colton, LLC Slide 15

February 22, 2001

L&C’s Process-Based ApproachL&C’s Process-Based Approach

Promote “Process Thinking” in All Aspects of Business Management

Explicitly Use the Process Model of Business for:– Process-Based Management Techniques– Process-Based Information Tools

Lenhardt & Colton, LLC Slide 16

February 22, 2001

What is the Process Model?What is the Process Model?

Any endeavor can be described in terms of input, activity & output.

Input OutputActivity

Tangible inputs are converted (via the endeavor) to tangible outputs.

Lenhardt & Colton, LLC Slide 17

February 22, 2001

The Process Model & ResourcesThe Process Model & Resources

The cost of people, supplies and assets are viewed as organizational resources that are consumed by the activity.

Resources (Budget)People’s Time ($)

Fuel $Depreciation $

Lenhardt & Colton, LLC Slide 18

February 22, 2001

The Process Model & OutputsThe Process Model & Outputs

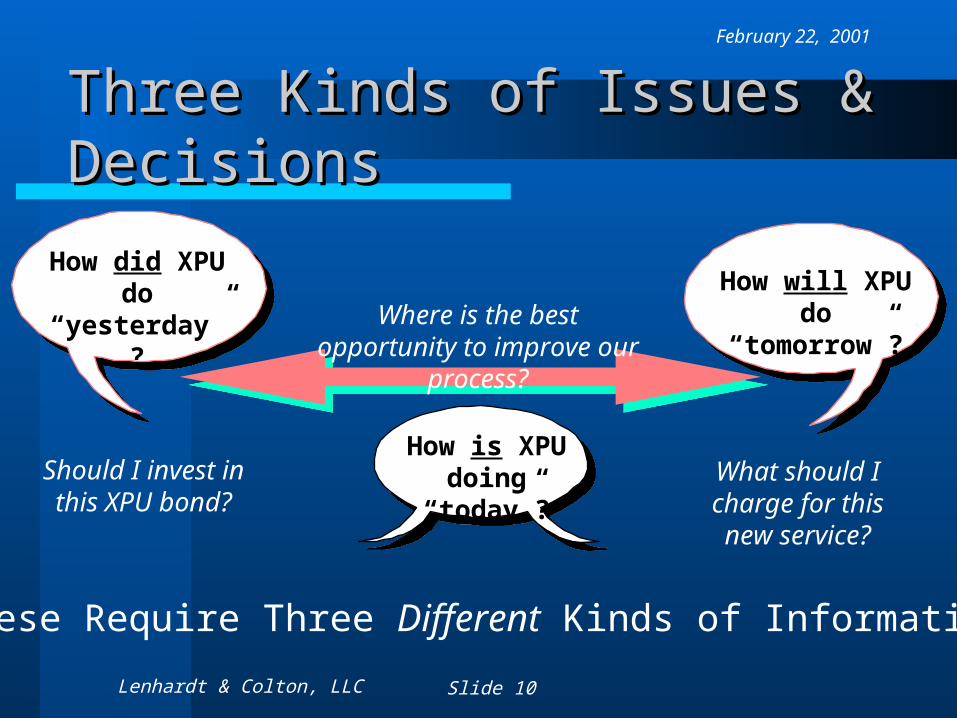

Output is expressed in terms of measurable units: – KiloWatt Hours (kWh’s) of electricity

The cost of a measurable unit is the ratio of it’s activity cost and the quantity of the measurable units completed:– Cost per kWh of electricity

Outputs are consumed by products & services, market segments, and so on...

Lenhardt & Colton, LLC Slide 19

February 22, 2001

Process Model SummaryProcess Model Summary

Input OutputActivity

Resource $

CustomersOfferings Segments

End Cost Objectives

Lenhardt & Colton, LLC Slide 20

February 22, 2001

Why “Process-Based”?Why “Process-Based”? The Process Model, Its Tools & Techniques

– Enable Cost Management to be Practiced Throughout the Organization and That’s Good!

• They Describe the Organization in the Language of People Who Do the Work

• They Establish a Real-Life Causal Relationship Between the Work People Do and Cost

– Systematically Integrate Seemingly Independent Functions and Activities and That’s Good!

• They “…remind employees that the activities of disparate departments are interdependent, even if organizational charts… suggest otherwise.”

No Other Cost Management Model Does This

Lenhardt & Colton, LLC Slide 21

February 22, 2001

Today’s AgendaToday’s Agenda

The Case for Change at XPU

Why Process-Based?

Insights from a Real Life Project

XPU’s Roadmap

Lenhardt & Colton, LLC Slide 22

February 22, 2001

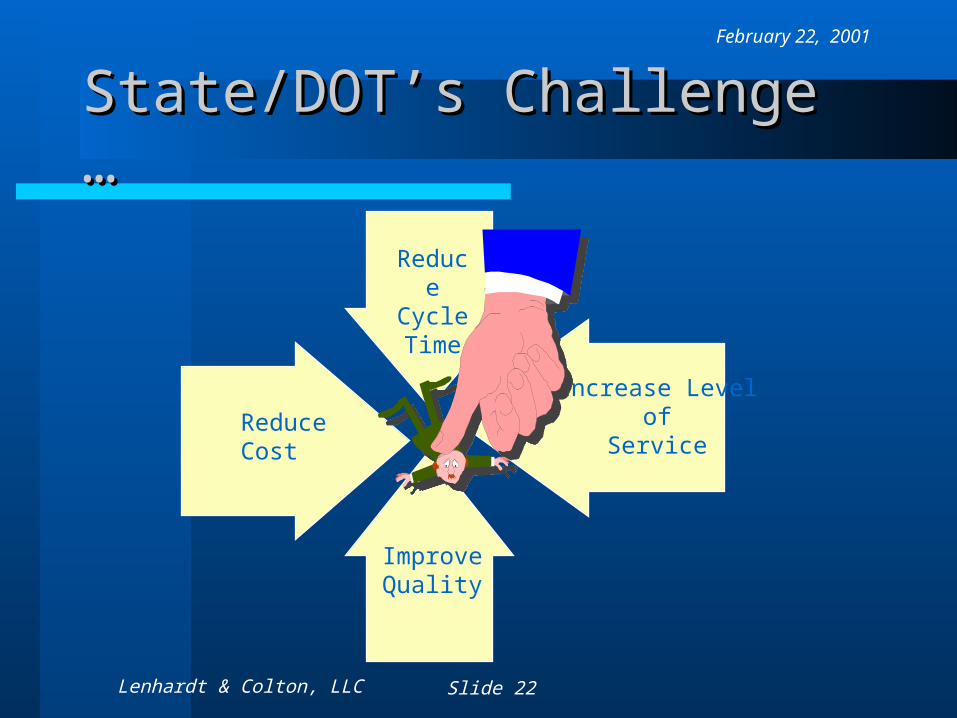

Reduce Cycle Time

ReduceCost

ImproveQuality

Increase Levelof

Service

State/DOT’s Challenge … State/DOT’s Challenge …

Lenhardt & Colton, LLC Slide 23

February 22, 2001

The Gov’s Challenge Pool . . .The Gov’s Challenge Pool . . .

• Commissioners “Contribute” to the Commissioners “Contribute” to the Pool via targeted cuts to least valuable Pool via targeted cuts to least valuable programs/servicesprograms/services• Participation in Challenge Pool earns Participation in Challenge Pool earns them the opportunity to obtain NEW them the opportunity to obtain NEW funding, greater than their “pool funding, greater than their “pool contributions”, to add or improve contributions”, to add or improve existing servicesexisting services•Election not to participate in pool Election not to participate in pool earns them automatic budget reductionearns them automatic budget reduction

What to Change?

How?

Lenhardt & Colton, LLC Slide 24

February 22, 2001

Information isData

Endowed withRelevance

andPurpose.

Peter Drucker, 1990

Requirement for “Good” InformationRequirement for “Good” Information

Lenhardt & Colton, LLC Slide 25

February 22, 2001

State/DOT: Start with the End in State/DOT: Start with the End in MindMindState/DOT’s “Purpose”

– Identify CQT– Manage CQT

• Improve Competitiveness• Focus on Continuous Improvement• Deploy Resources Effectively

– Measure CQT

Lenhardt & Colton, LLC Slide 26

February 22, 2001

Q - What’s ABC Used For?

A - Get Relevant Info. To

support strategic decisions,

such as:

– Are we competitive, OR not?

– Are our resources deployed

effectively, OR not?

– Should we invest in ABM to

support the Challenge Pool

requirements, OR not?

What is the annual cost of Construction Management?

What is the cost of a “typical” bridge design?

How much does it cost to prepare a “complex” PS&E package?

Activity Based ManagementActivity Based Management

How well are we meeting our objectives?

Activity Based Performance

Measures

How can we institutionalize improvements?

Activity Based Budgeting

How do we know what to improve?

Activity Based Continuous

Improvement

How can we better manage

capital projects?

Activity Based Project/Resource

Management

Activity Based SolutionsActivity Based SolutionsProblem? Solution!

How much does it really cost?

Activity Based Costing

ActivitiesActivities

Activities Outputs

Resources

Activity Analysis

Inputs

Lenhardt & Colton, LLC Slide 27

February 22, 2001

Program SupportProgram Support

I. Develop Activity-based ModelsII. Institutionalize the Process III. Roll-out Additional Activity-based

Tools• Focus on Activity-based Continuous

Improvement, and• Integrate with Business Planning

Lenhardt & Colton, LLC Slide 28

February 22, 2001

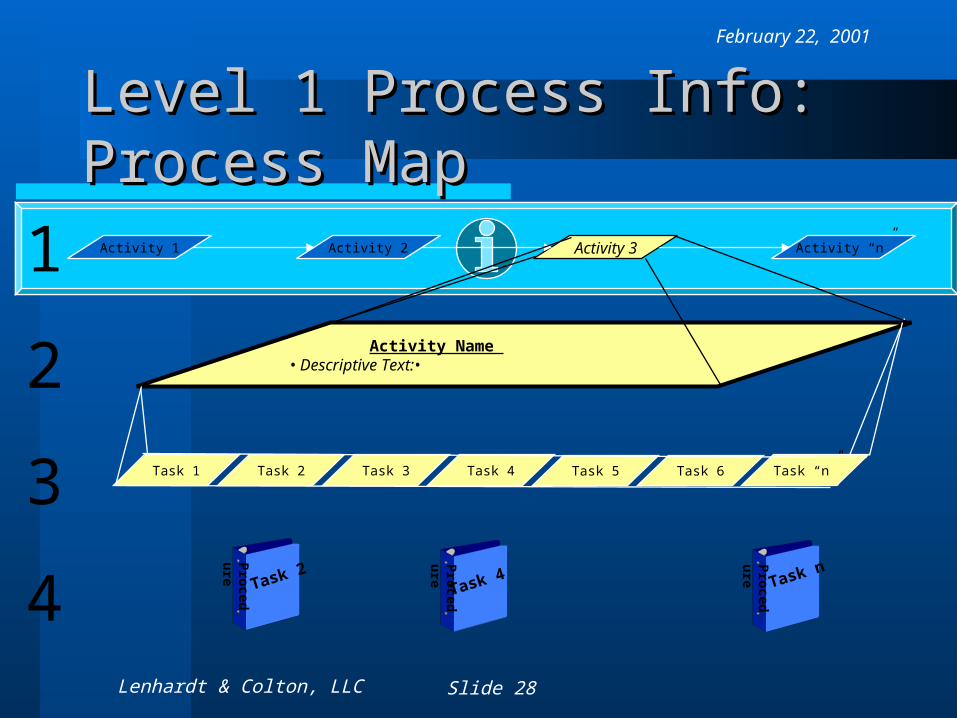

Level 1 Process Info: Process MapLevel 1 Process Info: Process Map

Activity 1 Activity 2 Activity 3 Activity “n”

Task “n”Task 1 Task 2 Task 3

Activity Name • Descriptive Text:•

Task 4 Task 5 Task 6

Procedu

re

Task 2

Procedu

re

Task 4

Procedu

re

Task n

1

2

3

4

Lenhardt & Colton, LLC Slide 29

February 22, 2001

Level 2 Process Info: Activity DictionaryLevel 2 Process Info: Activity Dictionary

Activity 1 Activity 2 CLICK HERE! Activity “n”

Task “n”Task 1 Task 2 Task 3

Activity Name • Descriptive Text:•

Task 4 Task 5 Task 6

Procedu

re

Task 2

Procedu

re

Task 4

Procedu

re

Task n

1

2

3

4

Lenhardt & Colton, LLC Slide 30

February 22, 2001

More Level 2 Info: Resource UsageMore Level 2 Info: Resource Usage

Activity 1 Activity 2 CLICK HERE! Activity “n”

Task “n”Task 1 Task 2 Task 3

Activity Name • Descriptive Text:•

Task 4 Task 5 Task 6

Procedu

re

Task 2

Procedu

re

Task 4

Procedu

re

Task n

1

2

3

4

Lenhardt & Colton, LLC Slide 31

February 22, 2001

Example of Results: An “80/20” AnalysisExample of Results: An “80/20” Analysis

Lenhardt & Colton, LLC Slide 32

February 22, 2001

Example: Cost/Unit of Primary OutputsExample: Cost/Unit of Primary Outputs

Lenhardt & Colton, LLC Slide 33

February 22, 2001

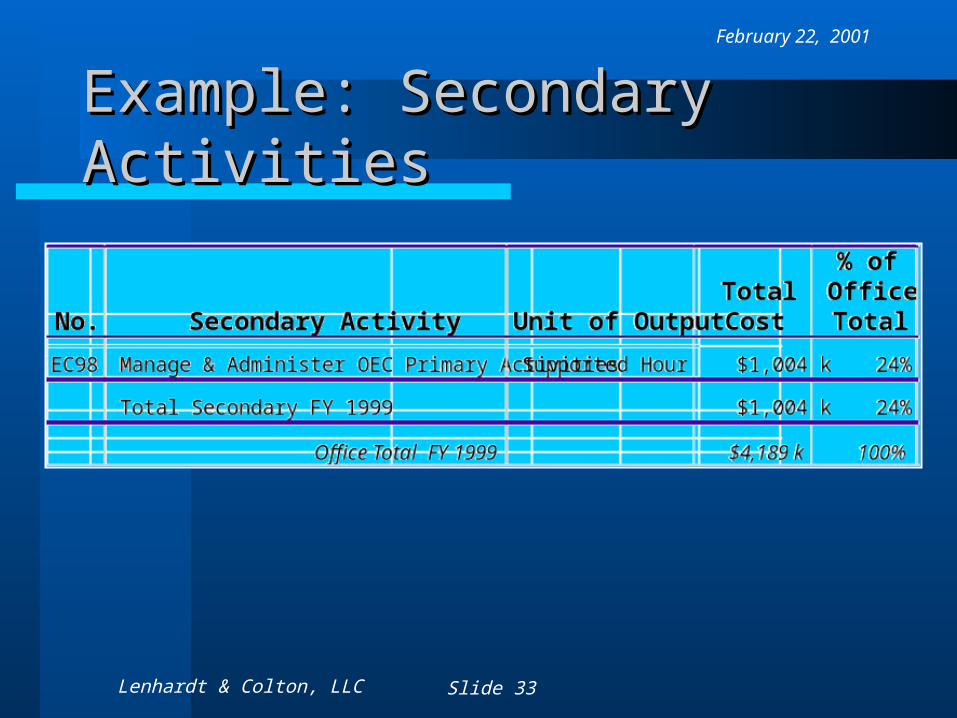

Example: Secondary ActivitiesExample: Secondary Activities

Lenhardt & Colton, LLC Slide 34

February 22, 2001

Example: Hours/UnitExample: Hours/Unit

Lenhardt & Colton, LLC Slide 35

February 22, 2001

Activity “5”—A Closer LookActivity “5”—A Closer Look

Lenhardt & Colton, LLC Slide 36

February 22, 2001

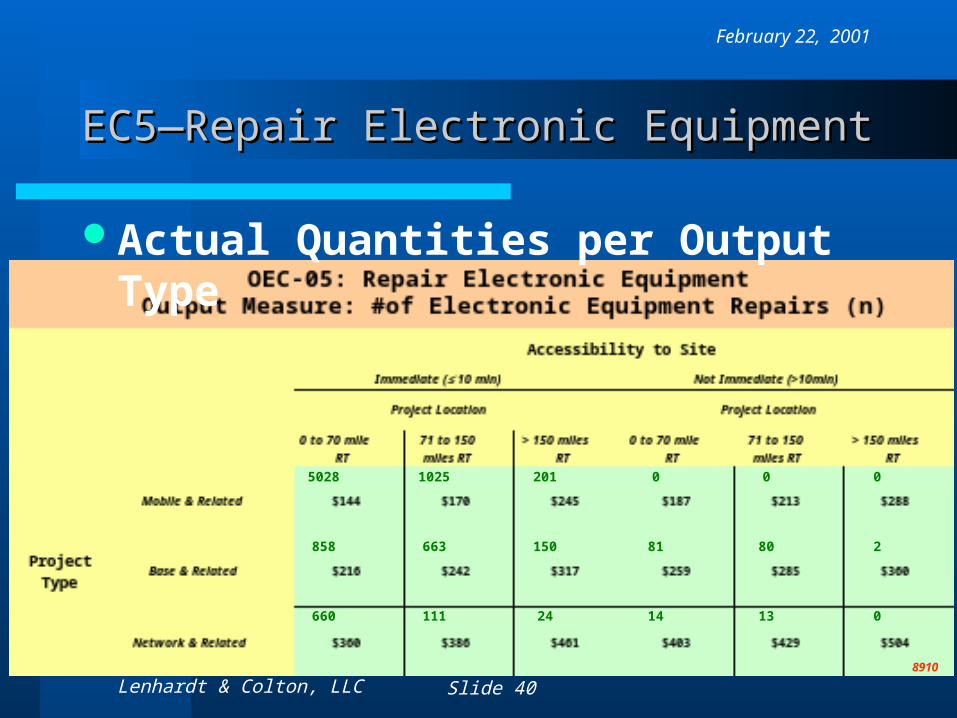

EC5—Repair Electronic EquipmentEC5—Repair Electronic Equipment

Normalization Criteria

Lenhardt & Colton, LLC Slide 37

February 22, 2001

Normalization Factors X = 2.8

EC5—Repair Electronic EquipmentEC5—Repair Electronic Equipment

Lenhardt & Colton, LLC Slide 38

February 22, 2001

Hours Per Output Type

EC5—Repair Electronic EquipmentEC5—Repair Electronic Equipment

1.0X

1.0 FactorX

2.8 hrs./ (n) unit

Lenhardt & Colton, LLC Slide 39

February 22, 2001

Dollars Per Output Type

EC5—Repair Electronic EquipmentEC5—Repair Electronic Equipment

1.0X

Lenhardt & Colton, LLC Slide 40

February 22, 2001

EC5—Repair Electronic EquipmentEC5—Repair Electronic Equipment

Actual Quantities per Output Type

5028 1025 201 0 0 0

858 663 150 81 80 2

660 111 24 14 13 0

8910

Lenhardt & Colton, LLC Slide 41

February 22, 2001

Projected Quantities per Output Type

EC5—What if Demand Increases?EC5—What if Demand Increases?

5028 1025 201 0 0 0

858 663 150 > 250 81 80 2

660 111 24 14 13 0

Suppose projected demand is for +100 more Repairs of the variety indicated above, in red. Assuming no other changes, resource requirements would increase by approximately (100 qty * $317/ea = $32 K).

Lenhardt & Colton, LLC Slide 42

February 22, 2001

EC5—Kinds of Resources per (n) OutputEC5—Kinds of Resources per (n) Output

Lenhardt & Colton, LLC Slide 43

February 22, 2001

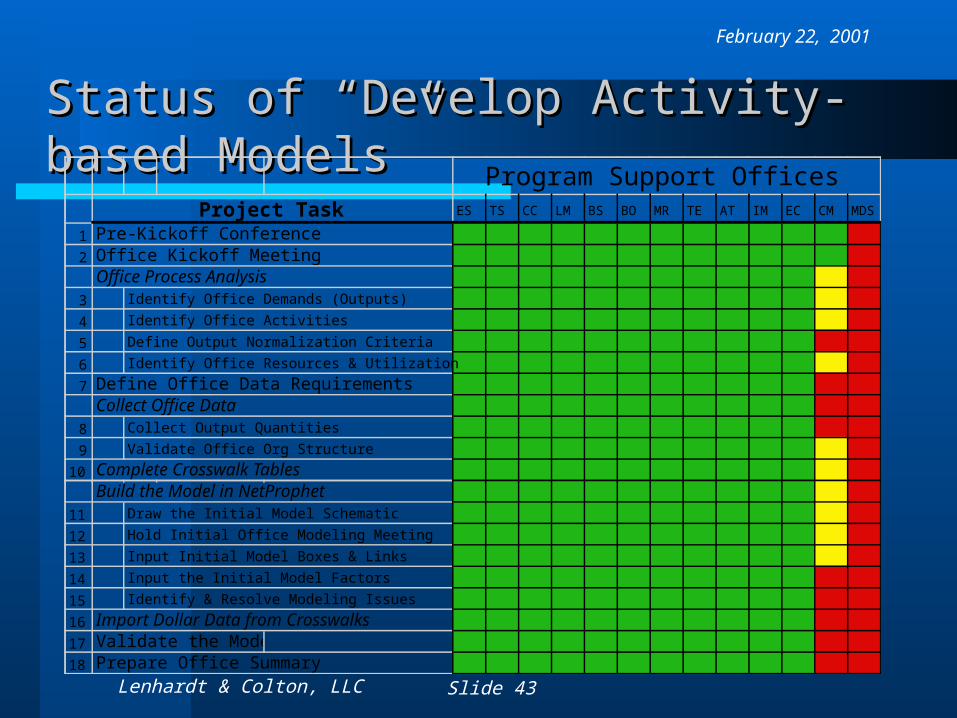

Status of “Develop Activity-based Models”Status of “Develop Activity-based Models”

ES TS CC LM BS BO MR TE AT IM EC CM MDS

1 Pre-Kickoff Conference2 Office Kickoff Meeting

Office Process Analysis3 Identify Office Demands (Outputs)

4 Identify Office Activities

5 Define Output Normalization Criteria

6 Identify Office Resources & Utilization

7 Define Office Data RequirementsCollect Office Data

8 Collect Output Quantities

9 Validate Office Org Structure

10 Complete Crosswalk Tables

Project Task

Program Support Offices

Build the Model in NetProphet11 Draw the Initial Model Schematic

12 Hold Initial Office Modeling Meeting

13 Input Initial Model Boxes & Links

14 Input the Initial Model Factors

15 Identify & Resolve Modeling Issues

16 Import Dollar Data from Crosswalks17 Validate the Model18 Prepare Office Summary

Lenhardt & Colton, LLC Slide 44

February 22, 2001

ABM Rollout in Program SupportABM Rollout in Program Support

Major Milestones

FOR MORE INFO...

State/DOT deployment of Activity-based models nearing completion. Institutionalization of model-building process and usage is ongoing. ABM Cycle 1 is in early planning stage.

Jan Feb Mar Apr May Jun July Aug Oct Nov Dec

Complete AB ModelsComplete AB Models

InstitutionalizeInstitutionalize

Do ABM Cycle 1Do ABM Cycle 1

Institutionalize ABMInstitutionalize ABM

Sep Jan Feb Mar Apr May Jun2001 2002

Lenhardt & Colton, LLC Slide 45

February 22, 2001

ABM - A Systematic Process ABM - A Systematic Process

Identify improvement opportunities

Develop action plans

Implement & Evaluate

Improve Processes

Cost, Quality, Time (CQT)

Evaluate Performance

Input OutputActivity

Resource $Assign Resources

to achieve Performance

Budgeting

PL

AN

DO

CH

EC

K

ACT

AC

T

Lenhardt & Colton, LLC Slide 46

February 22, 2001

A New A New FocusFocus

Lenhardt & Colton, LLC Slide 47

February 22, 2001

Today’s AgendaToday’s Agenda

The Case for Change at XPU

Why Process-Based?

Insights from a Real Life Project

XPU’s Roadmap

Lenhardt & Colton, LLC Slide 48

February 22, 2001

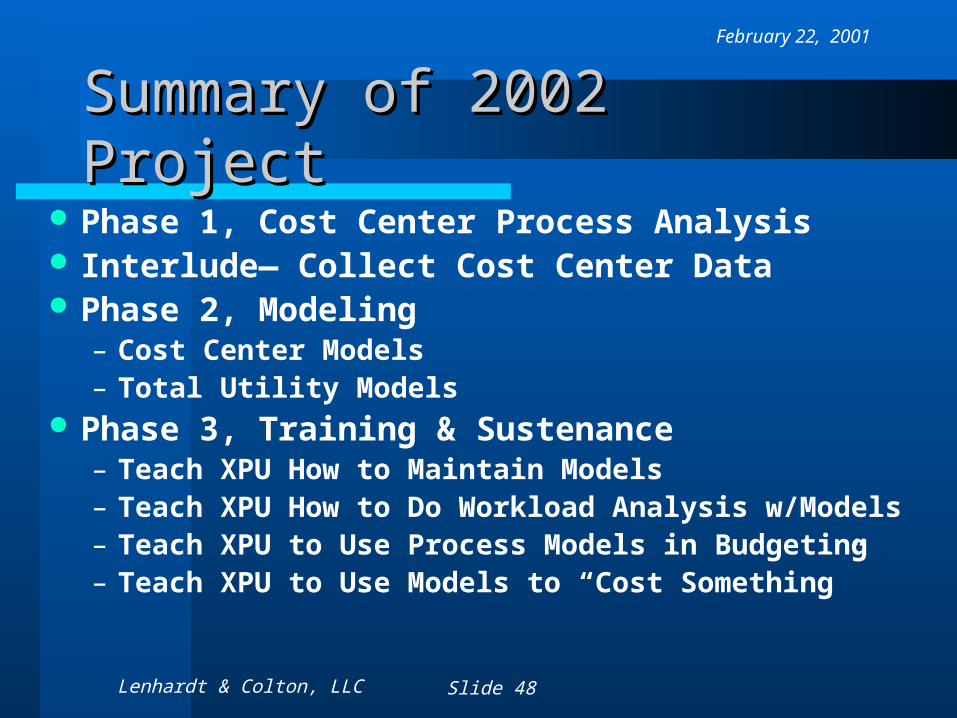

Summary of 2002 ProjectSummary of 2002 Project

Phase 1, Cost Center Process Analysis Interlude— Collect Cost Center Data Phase 2, Modeling

– Cost Center Models– Total Utility Models

Phase 3, Training & Sustenance– Teach XPU How to Maintain Models– Teach XPU How to Do Workload Analysis w/Models– Teach XPU to Use Process Models in Budgeting– Teach XPU to Use Models to “Cost Something”

Lenhardt & Colton, LLC Slide 49

February 22, 2001

The Overall RoadmapThe Overall Roadmap

Addressed to Date

Addressed By Project

Develop action plans

Identify improvement opportunities

Develop process controls

Non-financial process reports

ABC info for strategic decisions

Project Status Reports

Reduce NVA Improve VA

Identify Activities Identify

outputs and CPO

Trace costs

Process Controls

Strategic Information

Process Improvements

Resource Controls

Cost, Quality, Time (CQT)

Activity Based Planning &

Analysis

Evaluate Performance

Develop ABC Information

Lenhardt & Colton, LLC Slide 50

February 22, 2001

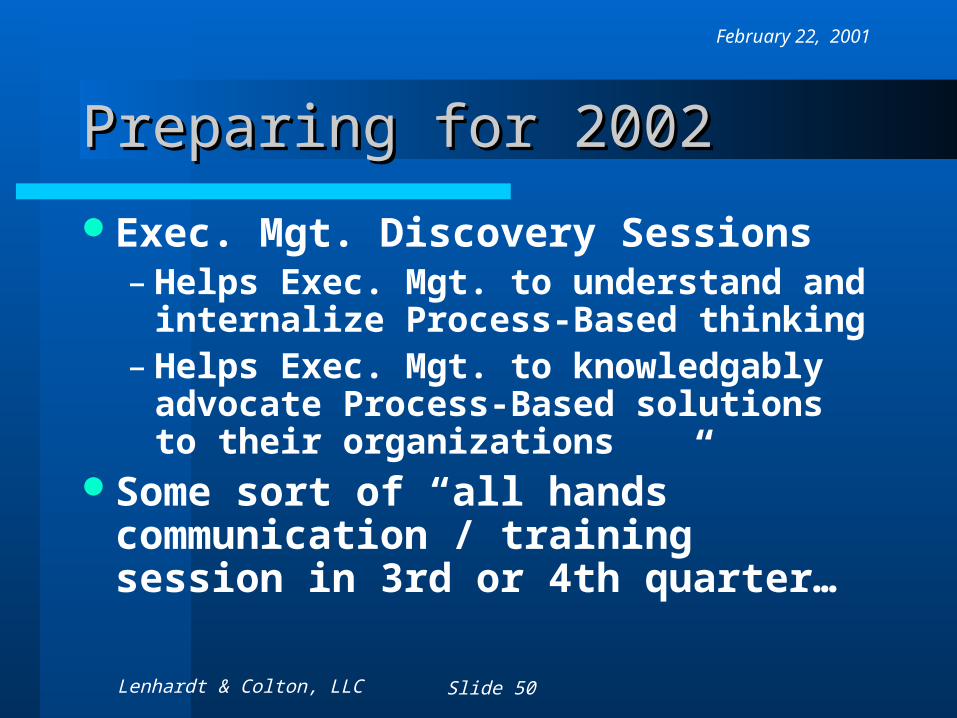

Preparing for 2002Preparing for 2002

Exec. Mgt. Discovery Sessions– Helps Exec. Mgt. to understand and

internalize Process-Based thinking– Helps Exec. Mgt. to knowledgably

advocate Process-Based solutions to their organizations

Some sort of “all hands” communication / training session in 3rd or 4th quarter…