Legacy Max

Keep Success in the Right Hands

Ras

Changing Financial Objectives

Estate planning goals can shift from accumulation to conservation

Your concern may have shifted from cash withdrawals for yourself to preserving a legacy

Annuities & IRAs may not meet your asset protection and transfer goals.

Tax Efficient Retirement SavingsAnnuities and IRAs are very tax-efficient ways to save for retirement

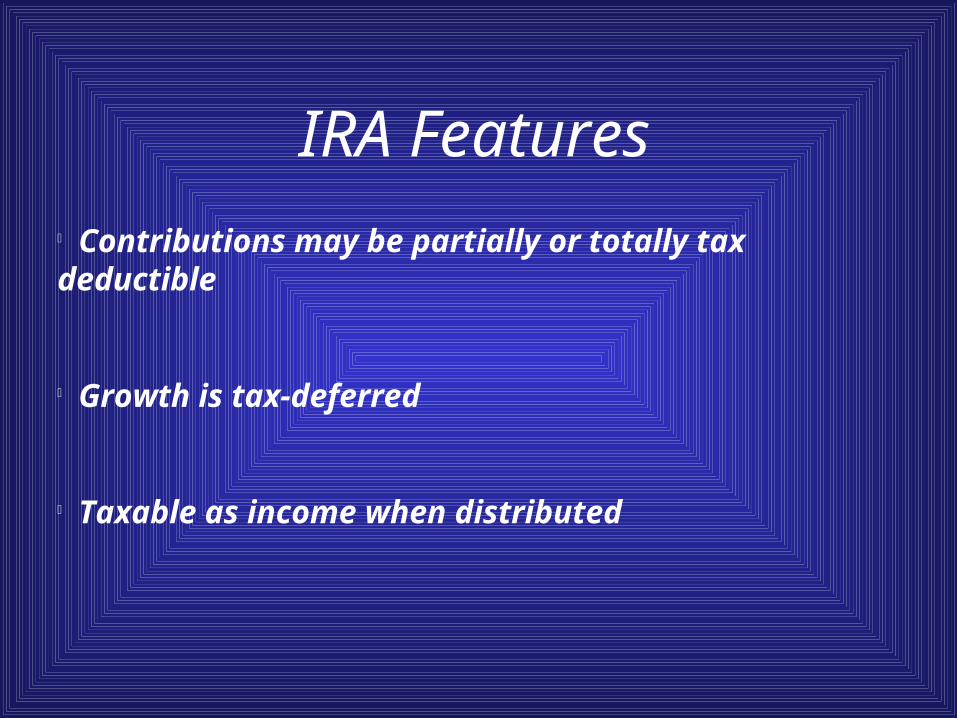

IRA Features Contributions may be partially or totally tax deductible

Growth is tax-deferred

Taxable as income when distributed

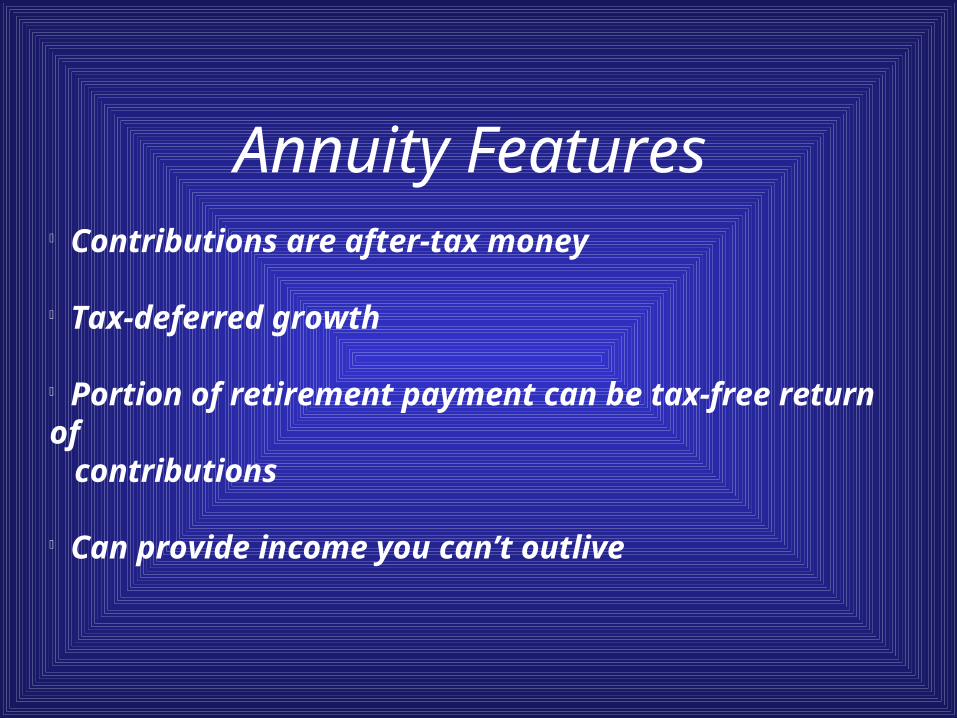

Annuity Features Contributions are after-tax money

Tax-deferred growth

Portion of retirement payment can be tax-free return of contributions

Can provide income you can’t outlive

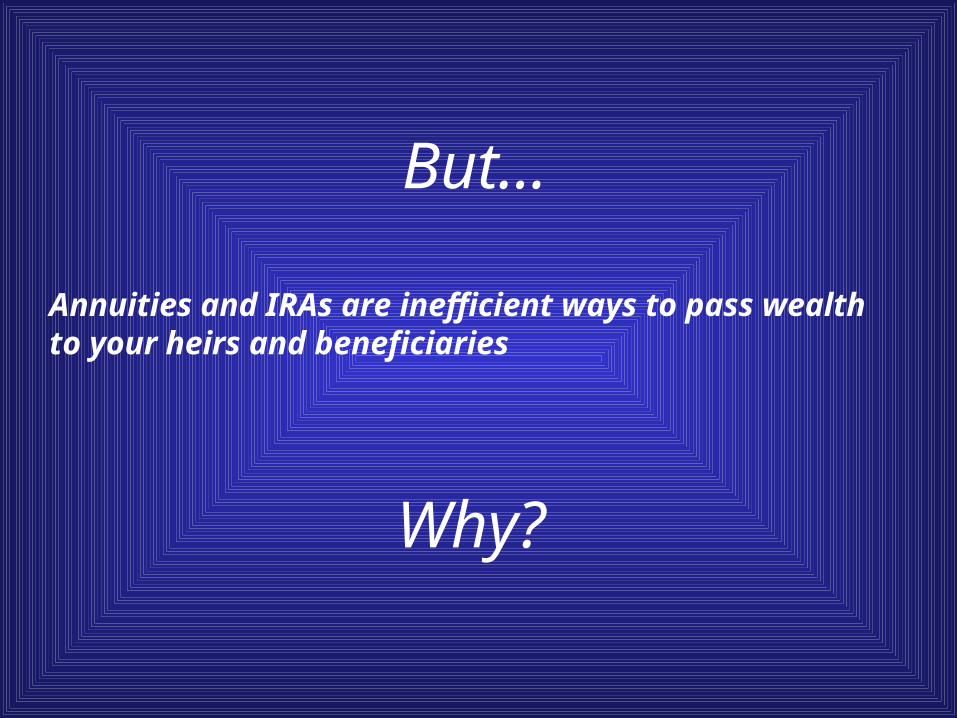

But…

Annuities and IRAs are inefficient ways to pass wealth to your heirs and beneficiaries

Why?

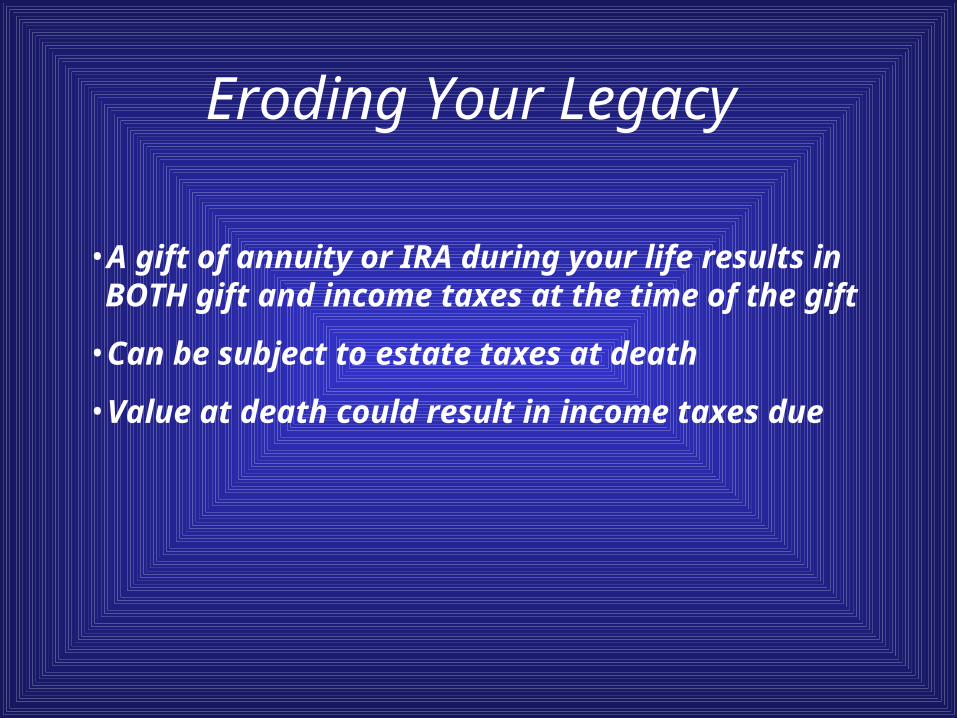

Eroding Your Legacy

• A gift of annuity or IRA during your life results in BOTH gift and income taxes at the time of the gift

• Can be subject to estate taxes at death

• Value at death could result in income taxes due

Eroding Your Legacy

Combined gift and income taxes

or Combined estate and income taxes could result in...

Loss of up to 70% or more to taxes

An Example

Gross value of non-qualified annuity at life expectancy = $1.6 M based on 20 years of growth, tables 5 & 6, 6% net rate.

Harry is 65. His estate is worth $5M at his death

Included in Harry’s estate - a non-qualified annuity that has grown to a value of about $1.6 million

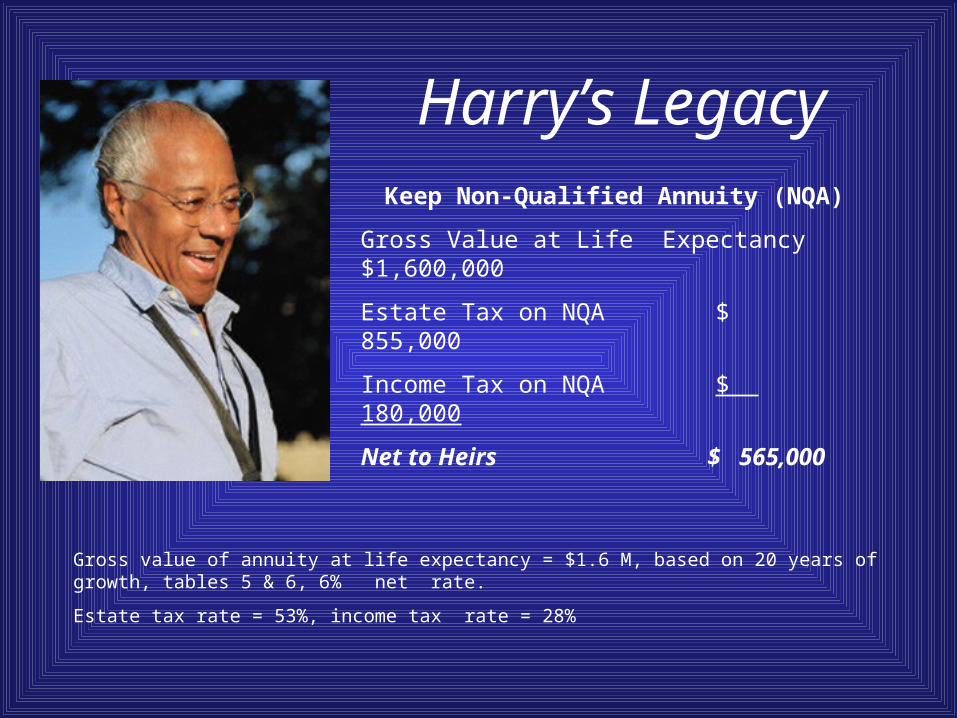

Harry’s LegacyKeep Non-Qualified Annuity (NQA)

Gross Value at Life Expectancy $1,600,000

Estate Tax on NQA $ 855,000

Income Tax on NQA $ 180,000

Net to Heirs $ 565,000

Gross value of annuity at life expectancy = $1.6 M, based on 20 years of growth, tables 5 & 6, 6% net rate.

Estate tax rate = 53%, income tax rate = 28%

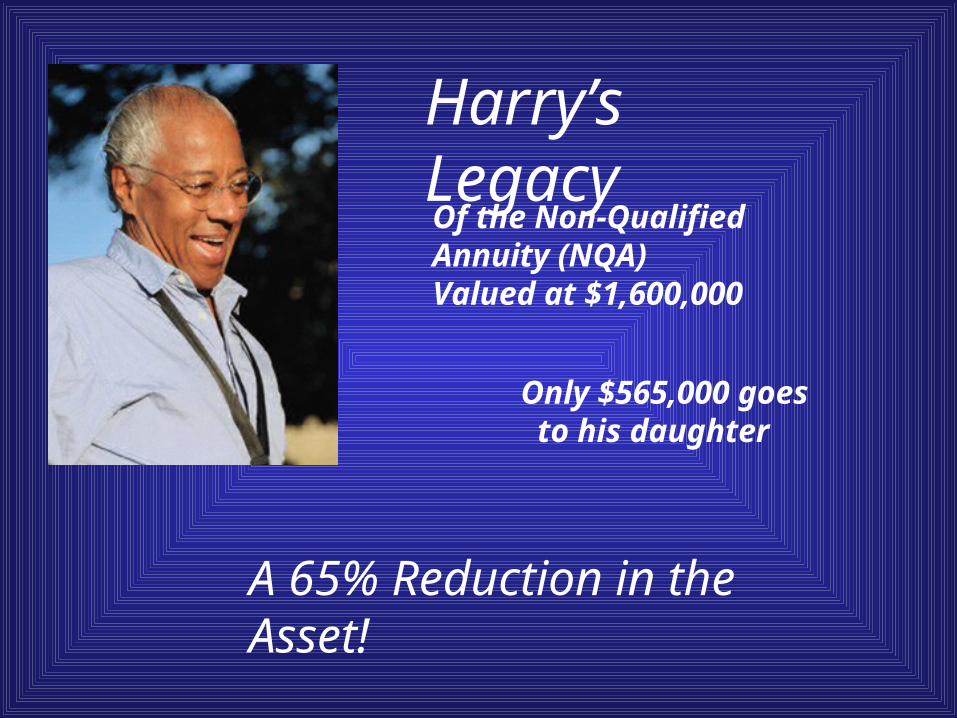

Harry’s Legacy

Of the Non-Qualified Annuity (NQA) Valued at $1,600,000

Only $565,000 goes to his daughter

A 65% Reduction in the Asset!

Harry’s LegacyOf the Non-Qualified Annuity (NQA) Valued at $1,600,000

Only $565,000 goes to his daughter

The rest goes to IRS

It could get worse….

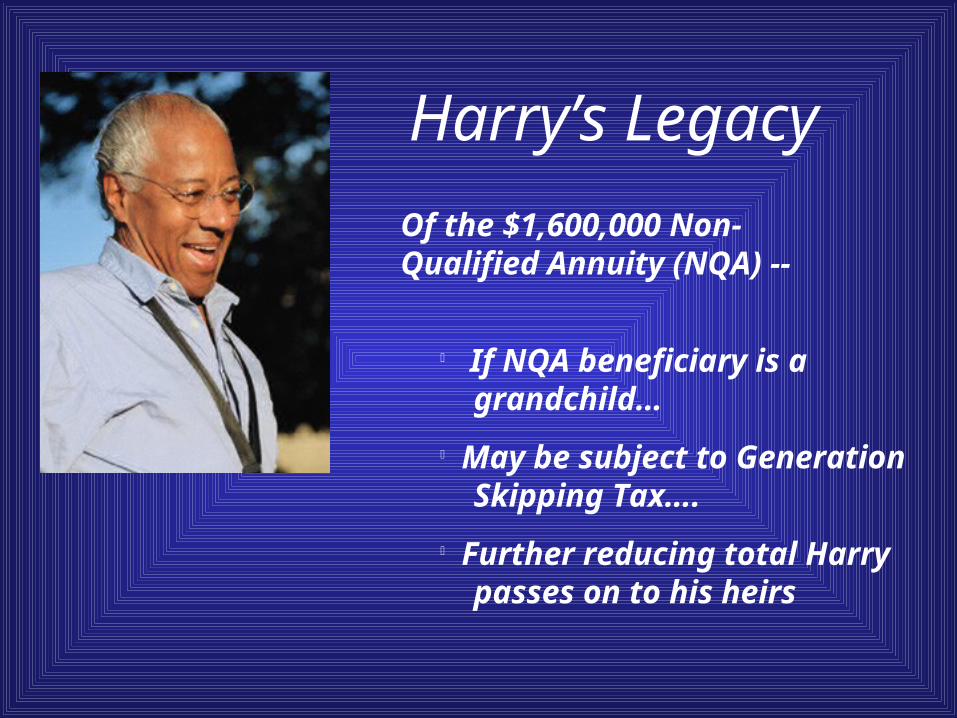

Harry’s Legacy

Of the $1,600,000 Non-Qualified Annuity (NQA) --

If NQA beneficiary is a grandchild…

May be subject to Generation Skipping Tax….

Further reducing total Harry passes on to his heirs

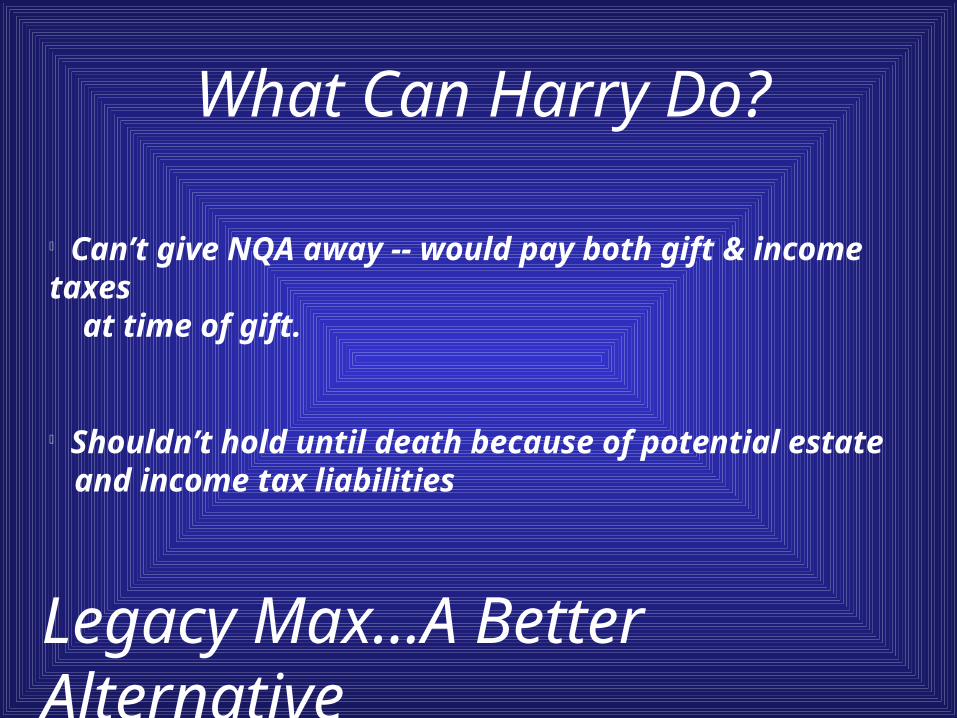

What Can Harry Do?

Can’t give NQA away -- would pay both gift & income taxes at time of gift.

Shouldn’t hold until death because of potential estate and income tax liabilities

Legacy Max…A Better Alternative

Legacy Max Exchange for something that has “no value” for estate

taxation purposes

Remove Non-Qualified Annuity from estate WITHOUT gift taxes

Exchange NQA for Immediate Annuity

Step 1 Purchase immediate annuity with payments to Harry for his lifetime

Annuity payable for his life terminates without value at his death

Step 2Exchange NQA for Immediate Annuity

Annuity Payments to

Harry

Harry receives annuity payments and pays income taxes on each payment

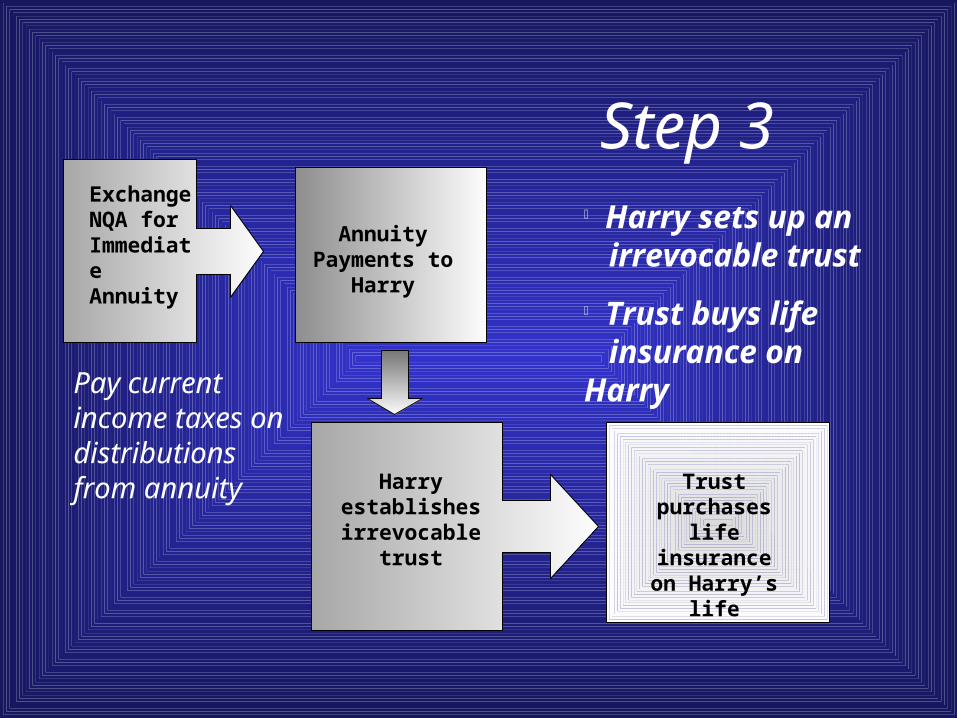

Step 3Exchange NQA for Immediate Annuity

Harry establishes irrevocable

trust

Annuity Payments to

Harry

Harry sets up an irrevocable trust

Trust buys life insurance on Harry

Trust purchases life insurance on Harry’s life

Pay current income taxes on distributions from annuity

Exchange NQA for Immediate Annuity

Harry establishes irrevocable

trust

Annuity Payments to

Harry

Trust purchases life insurance on Harry’s life

Harry uses annuity payments to pay premiums

During Harry’s Life

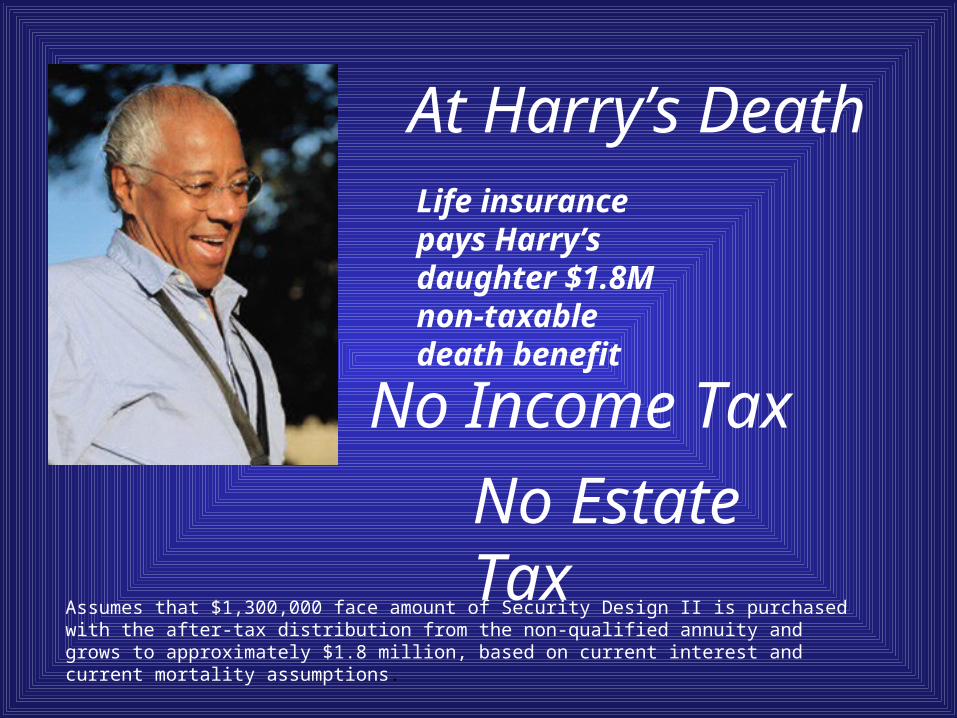

At Harry’s DeathLife insurance pays Harry’s daughter $1.8M non-taxable death benefit

No Income Tax

No Estate Tax

Assumes that $1,300,000 face amount of Security Design II is purchased with the after-tax distribution from the non-qualified annuity and grows to approximately $1.8 million, based on current interest and current mortality assumptions.

If Harry is married…. Annuity can pay income to Harry or his wife until second of

them dies

Life insurance can be designed to insure both spouses and payat second death

So What Did Legacy Max Accomplish?

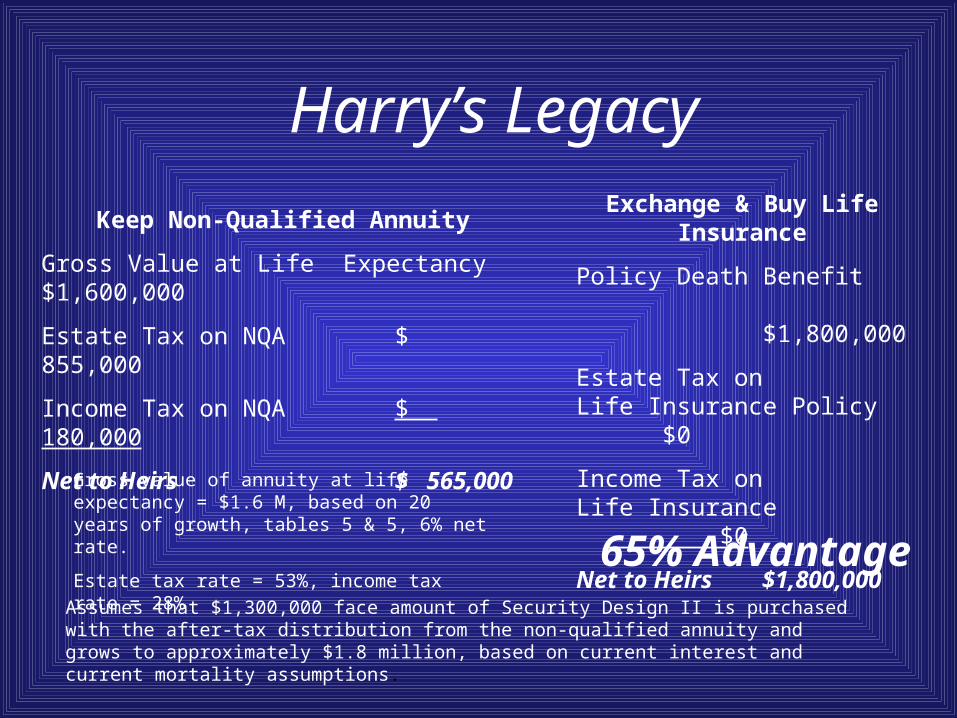

Harry’s Legacy

Keep Non-Qualified Annuity

Gross Value at Life Expectancy $1,600,000

Estate Tax on NQA $ 855,000

Income Tax on NQA $ 180,000

Net to Heirs $ 565,000

Exchange & Buy Life Insurance

Policy Death Benefit $1,800,000

Estate Tax onLife Insurance Policy $0

Income Tax onLife Insurance $0

Net to Heirs $1,800,000Gross value of annuity at life expectancy = $1.6 M, based on 20 years of growth, tables 5 & 5, 6% net rate.

Estate tax rate = 53%, income tax rate = 28% 65% AdvantageAssumes that $1,300,000 face amount of Security Design II is purchased with the after-tax distribution from the non-qualified annuity and grows to approximately $1.8 million, based on current interest and current mortality assumptions.

What Did Legacy Max Do? $1.8M vs. $565,000 for Harry’s daughter -- a 65% increase

With a survivorship policy, the increase could be even greater

Assumes that $1,300,000 face amount of Security Design II is purchased with the after-tax distribution from the non-qualified annuity and grows to approximately $1.8 million, based on current interest and current mortality assumptions.

Caveat

Not everyone will qualify for life insurance -- it will be based on current condition

Legacy Max Helps preserve your assets

Helps maximize the benefit to your heirs and beneficiaries

DisclaimersScenarios used the following assumptions: All figures used in this presentation are for illustrative purposes only

Net value of non-qualified annuity at life expectancy = $1.6M based on 20 years of growth, tables 5 & 6, 6% net rate of return. Rollover non-qualified annuity to immediate annuity - payments to ILIT to purchase life insurance, using Security Design II, Policy Form No. 11320 (#11330 in Montana), varies by state and is not available for sale in every state.

Estate tax on annuity = 53%

Income tax on annuity = 28%

Legacy Max concept designed for use with either Universal Life Insurance or Variable Universal Life Insurance products

Insurance and annuities issued by ReliaStar Life Insurance Company and Security-Connecticut Life Insurance Company. Securities offered through Washington Square Securities, Inc., 20 Washington Avenue South, Minneapolis, MN, 55401, (612) 372-5507. WSSI, ReliaStar Life and Security-Connecticut are wholly-owned subsidiaries of ReliaStar Financial Corp., a diversified holding company based in Minneapolis, MN.

Doc. #6176