KONECRANES INVESTOR PRESENTATION

Main production sitesSales and Service locations

Key figures in 2008:• Sales: MEUR 2,103• Employees: ~9,900• EBIT: MEUR 247• EBIT-%: 11.8 %• ROCE: 56.3%

Konecranes at a glance

#1 in the world in• Crane Maintenance Services• Standard Lifting Equipment• Industrial Process Cranes• #3-4 in lifting equipment for Ports

Production in 12 countries on three continents

Service depots and sales offices in 43 countries

© 2009 Konecranes Plc. All rights reserved. 2

Share basics

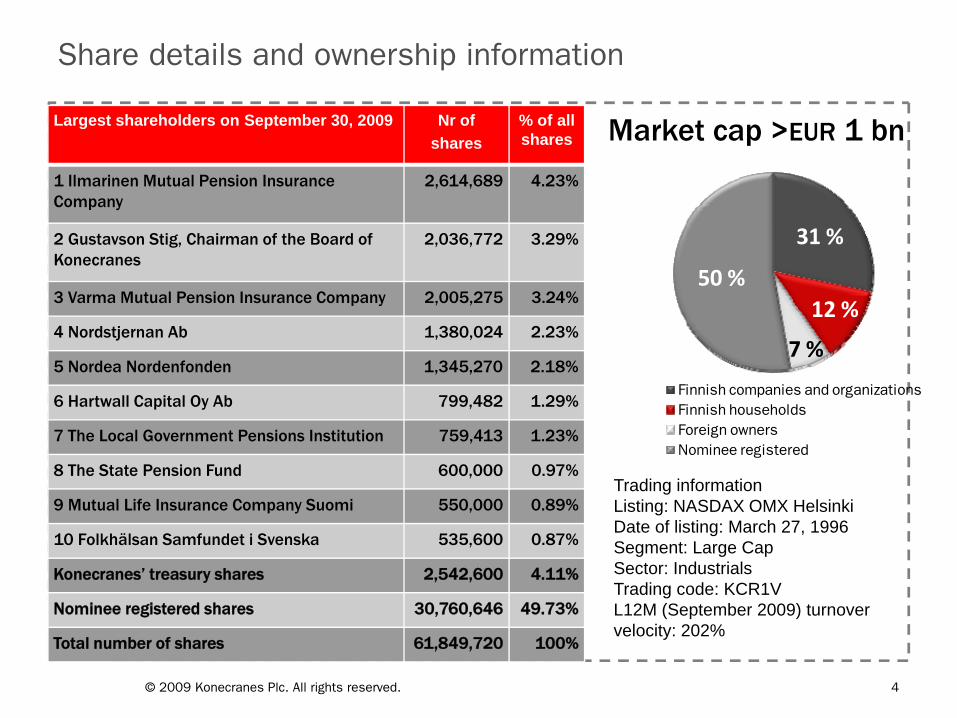

31 %

12 %

7 %

50 %

Finnish companies and organizationsFinnish householdsForeign ownersNominee registered

Share details and ownership information

Trading informationListing: NASDAX OMX HelsinkiDate of listing: March 27, 1996Segment: Large CapSector: IndustrialsTrading code: KCR1VL12M (September 2009) turnover velocity: 202%

Largest shareholders on September 30, 2009 Nr of shares

% of all shares

1 Ilmarinen Mutual Pension Insurance Company

2,614,689 4.23%

2 Gustavson Stig, Chairman of the Board of Konecranes

2,036,772 3.29%

3 Varma Mutual Pension Insurance Company 2,005,275 3.24%

4 Nordstjernan Ab 1,380,024 2.23%

5 Nordea Nordenfonden 1,345,270 2.18%

6 Hartwall Capital Oy Ab 799,482 1.29%

7 The Local Government Pensions Institution 759,413 1.23%

8 The State Pension Fund 600,000 0.97%

9 Mutual Life Insurance Company Suomi 550,000 0.89%

10 Folkhälsan Samfundet i Svenska 535,600 0.87%

Konecranes’ treasury shares 2,542,600 4.11%

Nominee registered shares 30,760,646 49.73%

Total number of shares 61,849,720 100%

Market cap >EUR 1 bn

© 2009 Konecranes Plc. All rights reserved. 4

Investment Case

Productivity enhancing • lifting equipment to various industries as

well as to ports and terminals• maintenance services to diverse industrial

customers and ports through the global sales network.

Product offering based on• a unique service business concept • world’s most extensive crane service

network• industry-leading technology• global modular product platforms• extensive own and third-party distribution

coverage

Business proposition

© 2009 Konecranes Plc. All rights reserved.6

0%

2%

4%

6%

8%

10%

12%

14%

0

250

500

750

1000

1250

1500

1750

2000

2250

© 2009 Konecranes Plc. All rights reserved.

Solid profitable growth during the past few years

MEUR

7

Sales by business area 1998 - 2008

0

500

1000

1500

2000

2500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

SERVICE STANDARD LIFTING HEAVY LIFTINGMEUR

29%

37%

34%

© 2009 Konecranes Plc. All rights reserved. 8

Sales by region MEUR 1998 - 2008

0

250

500

750

1000

1250

1500

1750

2000

2250

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

EMEA AME APAC

15%

28%

57%

© 2009 Konecranes Plc. All rights reserved. 9

10,8

13,7

17,2

29,5

46,2*56,3

0 10 20 30 40 50 60

2003

2004

2005

2006

2007

2008

Recent development in ROCE

• Vision to increase the current 17-percent market share and achieve a 30-percent global market share

Focus on profitable growth

• Optimal long-term gearing ratio in the range of 50 – 80% - may be under/above in the short term

• Group EBIT-margin 10% over the cycle

* The 2007 ROCE including capital gain was 50.4 %

© 2009 Konecranes Plc. All rights reserved. 10

Payout history

0.220.33

0.43

1.17

2.17*

2.83

0.50

0.26 0.280.45

0.800.90

00,20,40,60,8

11,21,41,61,8

22,22,42,62,8

3

2003 2004 2005 2006 2007 2008

EPS DIVIDEND

* 2007 EPS excluding capital gain: EUR 1.95

© 2009 Konecranes Plc. All rights reserved. 11

Strategy

Strategic cornerstones

GROUP STRATEGY

BUSINESS AREAServiceStandard Lifting Heavy Lifting

REGIONEMEAAMEAPAC

SEGMENTSAutomotive General manufacturingIntermodal & RailMiningOil & GasPaperPortsPowerSteel

• Extensive product offering• Broad customer base• Global reach

• Footprint expansion• New products• Acquisitions

© 2009 Konecranes Plc. All rights reserved. 13

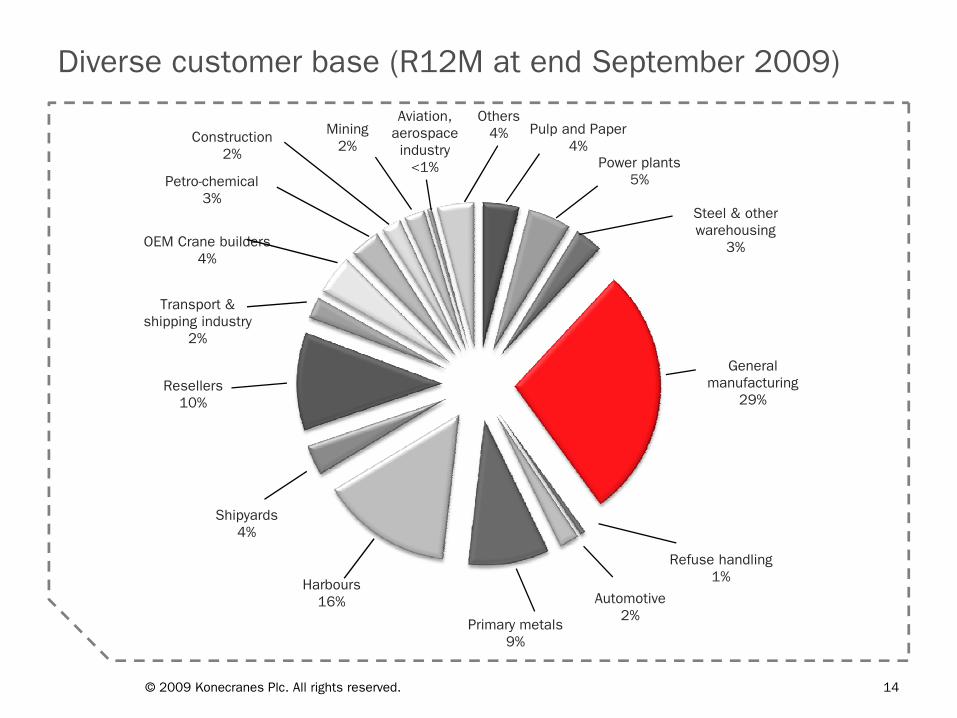

Diverse customer base (R12M at end September 2009)

© 2009 Konecranes Plc. All rights reserved. 14

Pulp and Paper4%

Power plants5%

Steel & other warehousing

3%

General manufacturing

29%

Refuse handling1%

Automotive2%

Primary metals9%

Harbours16%

Shipyards4%

Resellers10%

Transport & shipping industry

2%

OEM Crane builders4%

Petro-chemical3%

Construction2%

Mining2%

Aviation, aerospace industry

<1%

Others4%

Interlinked business model

STANDARD LIFTING

• Prominent position as the world’s largest supplier of industrial cranes and wire rope hoistsEfficient modularized product platformScale benefits both in production and sales via global supply chain and distribution channels

HEAVY LIFTING

• Prominent position as one of the world’s largest suppliers of heavy-duty cranes and container handling equipmentHigh-level expertise on customers ‘production processesFlexibility through cost baseGlobal supply chain

The business model offers a substantial potential for cross selling between new equipment and services

SERVICE

• A unique business conceptOne step ahead of a traditional after-sales only serviceMaintenance to all, including competitors’ crane makesMore value-added for customers through performance-based agreements

© 2009 Konecranes Plc. All rights reserved. 15

Business strategies are implemented through three regions

EMEAEurope, Middle East,

Africa

Mature markets

• High technology equipment for efficiency enhancing material handling• Higher level service contractsFast growing markets

• Capacity upgrading and expansions• Opportunity for service contracts

AMENorth and South

Americas

North America

• Utilizing the willingness for maintenance outsourcing and higher level service contracts

• High technology equipment for efficiency enhancing material handlingSouthern America

• Fast growing market with lots of opportunities both in new equipment and services

APACNortheast Asia,

South Asia-Pacific

A mix of mature markets in Australia and Southeast Asia and the fast growing economies of China and India

•Exploiting the market leader position for service in Australia•Exploiting the market leader position for high-end equipment market in China•Increasing market share and introducing the concept for outsourced maintenance

© 2009 Konecranes Plc. All rights reserved. 16

Two-folded sales and distribution strategy

GROUP STRATEGY

BUSINESS AREAServiceStandard Lifting Heavy Lifting

• Sales directly to end users under the Konecranes brand

• Sales to crane makers and resellers under the freestanding power brands

© 2009 Konecranes Plc. All rights reserved. 17

Main production sitesSales and Service locations

Production and supplying partners on three continents

USA• wire rope hoists• chain hoists• gear reducers• winches• control systems• crane factories

Finland• wire rope hoists &

winches• gear redurcers• control systems• automation/software

Sweden

• lift trucks

UK• crane factories

France• chain hoists

Germany• wire rope hoists• chain hoists• crane factory

Ukraine

• mechanical crane components and heavy steel structures

China

• RTG-crane assemblies

• wire rope hoists

• chain hoists

• winches

• control systems

• lift trucks

© 2009 Konecranes Plc. All rights reserved. 18

Opportunities for growth

Heavy Lifting Demag Cranes AG, GermanyProcess cranes ZPMC, China~ 2 BEUR ~ 14% Kalmar (part of Cargotec Corporation), FinlandCont. handling & other port equip. Fantuzzi Group, Italy (part of Terex, USA)~ 5 BEUR ~ 8% Liebherr, Germany (private company)

Various smaller private companies

Market size and market share

Market Size KC market share* Other companies in the sector

*Konecranes estimates

Standard Lifting Demag Cranes AG, Germany> 4 BEUR ~ 20% Columbus McKinnon Corporation, U.S.A.

Kito, JapanAbus Kransysteme GmbH, Germany (private company)Various smaller private companies

Service Customers’ in-house maintenanceOpen: > 3 BEUR > 20% Demag Cranes AG, GermanyTotal: > 10 BEUR > 7% Various smaller private companies

© 2009 Konecranes Plc. All rights reserved. 20

Rising requirement for increasing productivity, byoutsourcing and High-class equipment

Increasing environmentalconsciousness through investments in ecological solutions Increasing need for energy

investments

Increasing global tradeWestern players transferring production to lower cost areas

Economic growth driven industrial capacity build up

Need for new technology/Software applications

Global megatrends

© 2009 Konecranes Plc. All rights reserved. 21

Every new nuclear reactor offers a large potential for cranes and services

© 2009 Konecranes Plc. All rights reserved. 22

What makes Konecranes tick

•Actively seeking profitable growth– Aggressive organic growth

– Acquisitions

•Being alert to global megatrends

•Responding innovatively to customer needs

• R&D

• Value-adding service concepts

•Enhancing efficiency of own business model

Main drivers for Konecranes’ success

© 2009 Konecranes Plc. All rights reserved. 24

Management agenda

• Top-line defense– footprint expansion, new products

and services, bolt-on acquisitions• Actions to adjust capacity • Rationalization

– manufacturing, purchases, operative and legal structures

• Balance sheet management– low gearing– NWC in focus

• Risk management– order book quality – monitoring

postponements and cancellation risks

– counterparties – diverse customer and supplier base

© 2009 Konecranes Plc. All rights reserved. 25

Flexible material and subcontracting costs account for some 60% of total operating expenses in 2008

Depreciation/ amortisation

1%

Total personnel expenses25%

Other operating expenses14%

Subcontracting13 %

Material and supplies47%

Flexibility directly linked to volume development

Actions case by case and unit by unit

Flexibility somewhat more restricted

Total operating expenses in 2008 EUR 1.9 bn

© 2009 Konecranes Plc. All rights reserved. 26

Service

Services is a genuine growth market benefiting from the outsourcing trend

© 2009 Konecranes Plc. All rights reserved.

• Outsourcing driven by productivity, opex, safety & competence.

• Customers increasingly prefer globally scalable suppliers.

27 %

66% Konecranes

Outsourced Market

“In-house”Maintenance

Case Study of North American Market 2007 (> 3.5 BUSD)

7%

27%

28

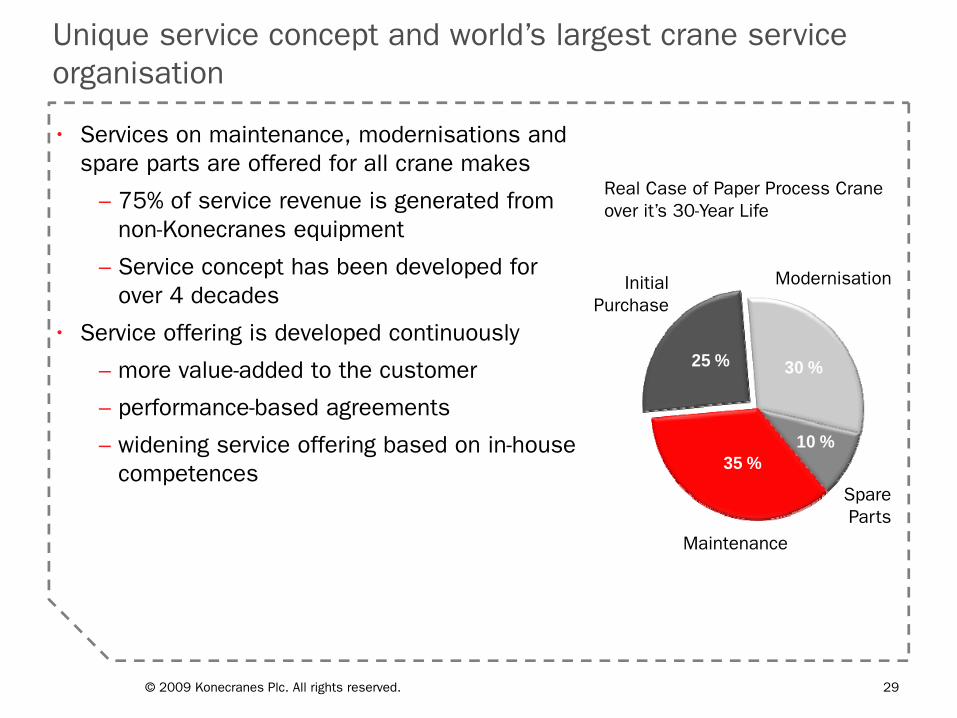

• Services on maintenance, modernisations and spare parts are offered for all crane makes

– 75% of service revenue is generated from non-Konecranes equipment

– Service concept has been developed for over 4 decades

• Service offering is developed continuously

– more value-added to the customer

– performance-based agreements

– widening service offering based on in-house competences

25 % 30 %

10 %35 %

Initial Purchase

Maintenance

Spare Parts

Modernisation

Real Case of Paper Process Crane over it’s 30-Year Life

Unique service concept and world’s largest crane serviceorganisation

© 2009 Konecranes Plc. All rights reserved. 29

Five Levels of Service

1 CONTACT- One-off repairs, spare parts, inspections, modernizations, emergency on-call

- Contract on periodic and scheduled inspections- Maintenance action recommendations

- Preventive maintenance contract

-Full scope maintenance outsourcing- Tied to customers KPI’s

- Fully outsourced material handling

2 CONDITION

3 CARE

4 COMMITMENT

5 COMPLETE

Full scope contract

One-off transactions

Full scope outsourcing

© 2009 Konecranes Plc. All rights reserved. 30

Standard Lifting

Light lifting and chain hoists

• Workstation Cranes

up to 2000kg

• Jib Cranes up to 5000kg

• XN Chain Hoists 60 – 7500kg

• Monorail Systems 125 – 2000kg

Jib Crane Chain Hoist Monorail systems

© 2009 Konecranes Plc. All rights reserved. 32

Industrial cranes

• Single Girder Cranes up to 12.5 tons

• Double Girder Cranes up to 80 tons

• Underslung Cranes up to 12.5 tons

• Explosion Proof Cranes up to 80 tons

Electric Overhead Traveling Crane

© 2009 Konecranes Plc. All rights reserved. 33

Customer industries

• General Manufacturing• Automotive• Cement and Concrete• Entertainment• Glass• Mining• Petrochemical• Plastic• Power Plants• Pulp and Paper• Steel• Stone and Marble• Water Treatment Plants

© 2009 Konecranes Plc. All rights reserved. 34

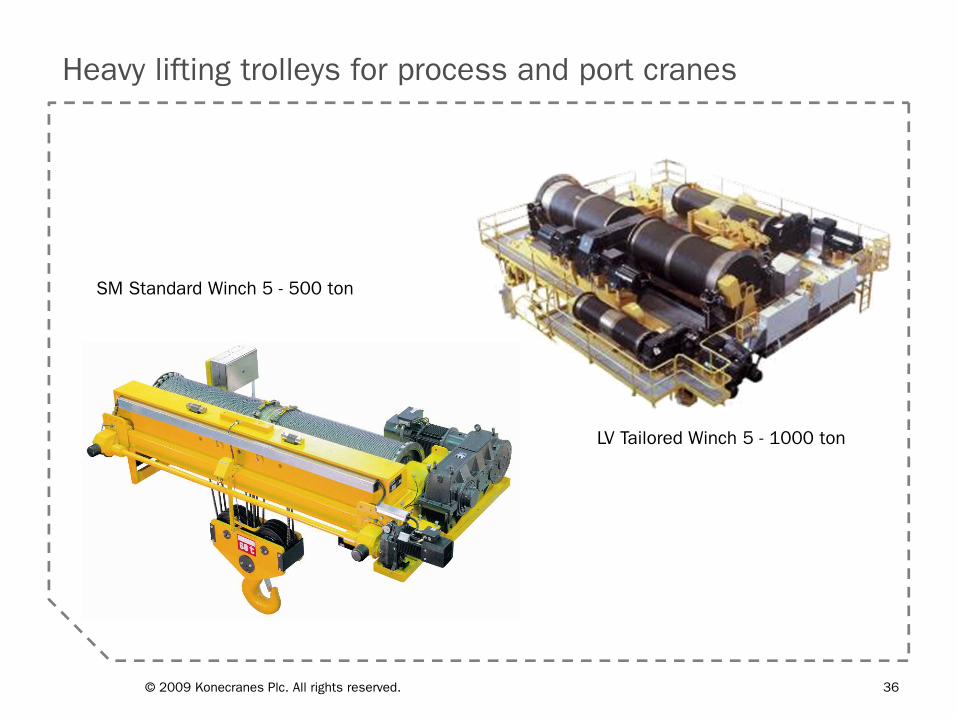

Heavy Lifting

Heavy lifting trolleys for process and port cranes

LV Tailored Winch 5 - 1000 ton

SM Standard Winch 5 - 500 ton

© 2009 Konecranes Plc. All rights reserved. 36

Steel industry

• Solutions in EOT Cranes and Lift Trucks for All Process Phases

• From the Scrapyard through the melt-shop to the storage area

• Slabs, blooms, billets, format plates, coils, tubes and wires

© 2009 Konecranes Plc. All rights reserved. 37

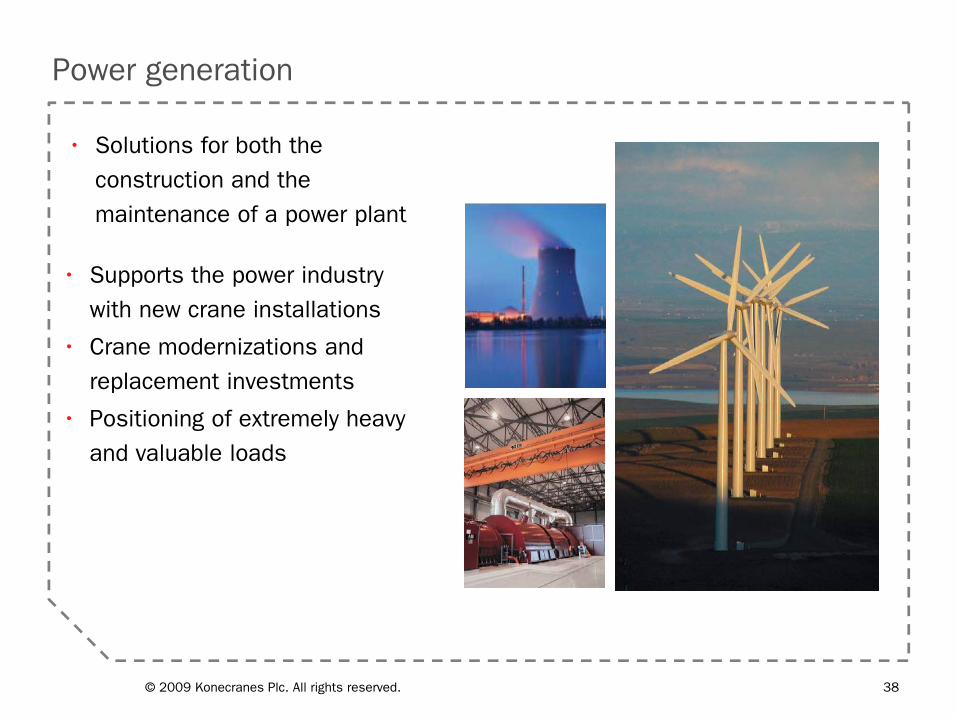

Power generation

• Supports the power industry with new crane installations

• Crane modernizations and replacement investments

• Positioning of extremely heavy and valuable loads

• Solutions for both the construction and the maintenance of a power plant

© 2009 Konecranes Plc. All rights reserved. 38

Paper industry

• Applications in the pulp and paper production

• Process duty and service cranes for all phases

• Clamp & Bale trucks for Loading and Unloading of trucks, rail cars or ships and handling of rolls in storage

• Automatic paper roll storage systems

© 2009 Konecranes Plc. All rights reserved. 39

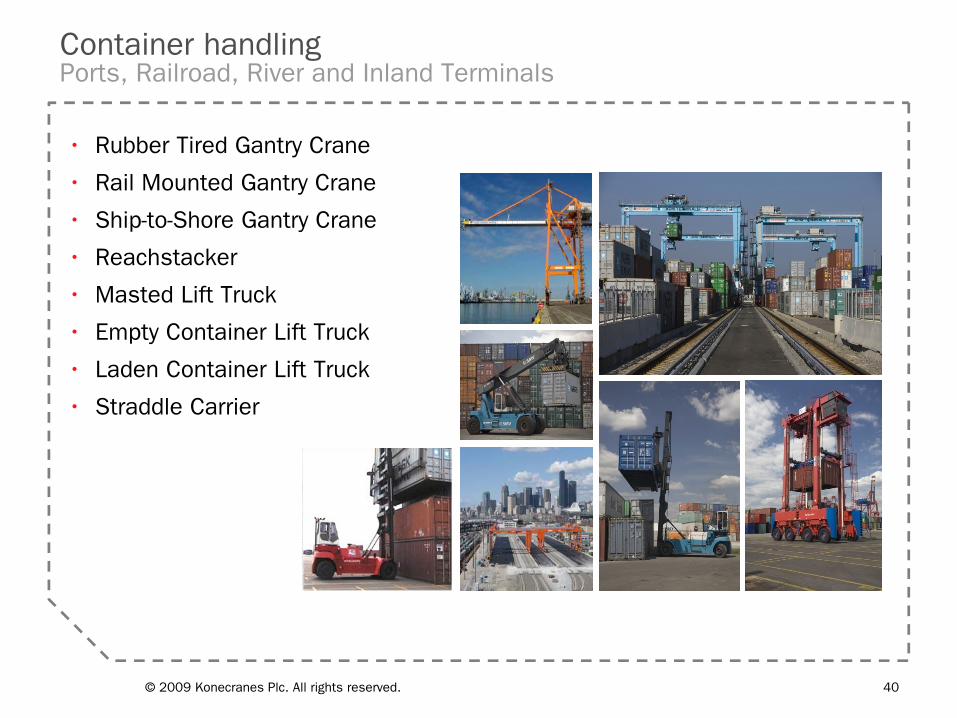

Container handlingPorts, Railroad, River and Inland Terminals

• Rubber Tired Gantry Crane

• Rail Mounted Gantry Crane

• Ship-to-Shore Gantry Crane

• Reachstacker

• Masted Lift Truck

• Empty Container Lift Truck

• Laden Container Lift Truck

• Straddle Carrier

© 2009 Konecranes Plc. All rights reserved. 40

Bulk handling & shipyards

• Bulk Handling Cranes

• Shipyard Cranes

• Shipboard Cranes

• Fork Lift Trucks

Slewing Ship-yard Crane

Munckloader Off Shore CraneHeavy Cargo Gantry Crane

Goliath GantryCrane

Fork Lift Truck

Grab Unloader

© 2009 Konecranes Plc. All rights reserved. 41

Contact information

• Pekka Lundmark, President and CEOtel. +358 (0)20 427 2000 [email protected]

• Teo Ottola, Chief Financial Officertel.+358 (0)20 427 2040 [email protected]

• Mikael Wegmüller, Director, Marketing and Communicationstel: +358 (0)20 427 [email protected]

www.konecranes.com

© 2009 Konecranes Plc. All rights reserved. 42

Thank you!Thank you!