Christof Rühl, Group Chief Economist

January 2013

© BP 2013

Contents

Introduction

Global energy trends

Outlook 2030: Fuel by fuel

Implications

Energy Outlook 2030

© BP 2013

Introduction

Global energy trends

Outlook 2030: Fuel by fuel

Implications

Energy Outlook 2030

© BP 2013

0

3

6

9

12

1990 2010 2030

OECD non-OECD

0

2

4

6

8

1990 2010 2030

OECD Non-OECD

0

25

50

75

100

1990 2010 2030

OECD Non-OECD

Population, income and energy growth

Energy Outlook 2030

Billion

Population GDP

Trillion $2011 PPP Billion toe

Primary energy

© BP 2013

0

3

6

9

12

15

18

1990 2010 2030

Industrialisation drives energy growth

Billion toe

Energy Outlook 2030

OECD

0

3

6

9

12

15

18

1990 2010 2030

Other

Power generation

Transport

By primary use By fuel By region

Oil

Coal

Gas

Billion toe Billion toe

Industry

0

3

6

9

12

15

18

1990 2010 2030

Hydro Nuclear

Renew.*

Oil

Coal

Gas

*Includes biofuels

Other non-OECD India

© BP 2013

The power sector leads primary energy growth

Growth by sector and fuel, 2011-2030 Growth by sector and region, 2011-2030

-1

0

1

2

3

Transport

Industry

Other

Power

Hydro

Nuclear

Renew.

Electricity

Gas

Biofuels

Oil

Coal

Final energy use Inputs to power

Billion toe

-1

0

1

2

3

Transport

Industry

Other

Power

RoW

Middle East

India

China

OECD

Final energy use Inputs to power

Billion toe

Energy Outlook 2030

© BP 2013

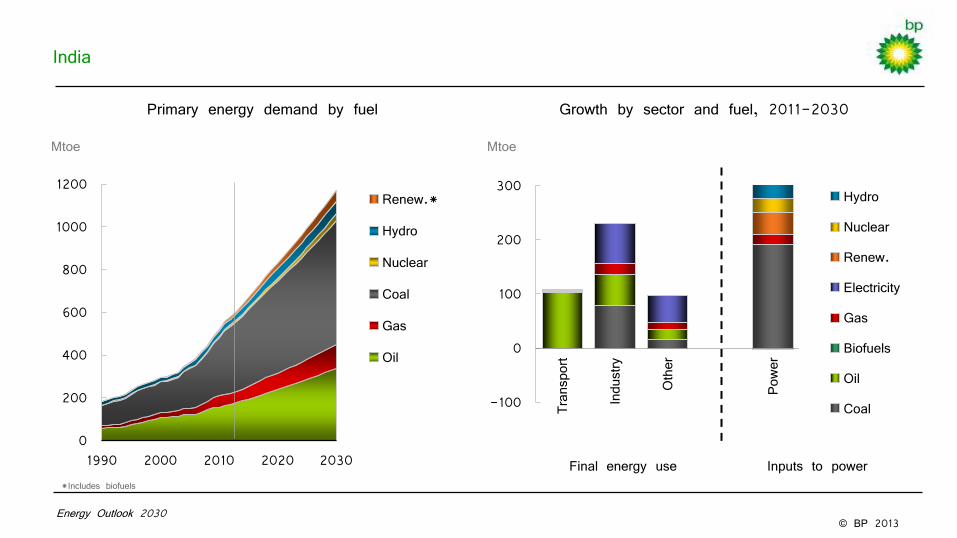

India

Mtoe

Energy Outlook 2030

Growth by sector and fuel, 2011-2030 Primary energy demand by fuel

Oil

Coal

Gas

0

200

400

600

800

1000

1200

1990 2000 2010 2020 2030

Renew.*

Hydro

Nuclear

Coal

Gas

Oil

*Includes biofuels

-100

0

100

200

300

Transport

Industry

Other

Power

Hydro

Nuclear

Renew.

Electricity

Gas

Biofuels

Oil

Coal

Final energy use Inputs to power

Mtoe

© BP 2013

0

3

6

9

12

15

18

1990 2000 2010 2020 2030

FSU

S&C America

N. America

Middle East

Europe

India

Asia P. ex India

Africa

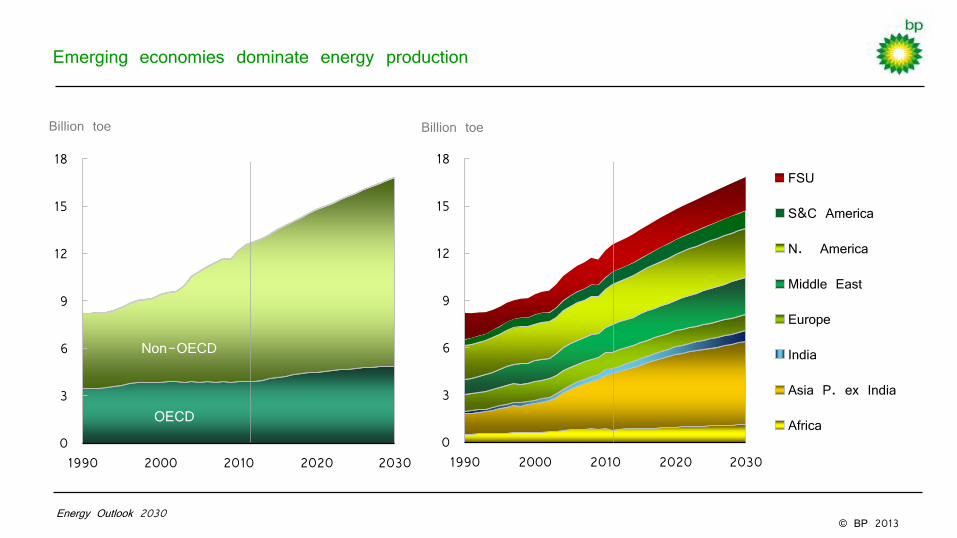

Emerging economies dominate energy production

OECD

Non-OECD

Billion toe

Energy Outlook 2030

0

3

6

9

12

15

18

1990 2000 2010 2020 2030

OECD

Non-OECD

Billion toe

© BP 2013 Energy Outlook 2030

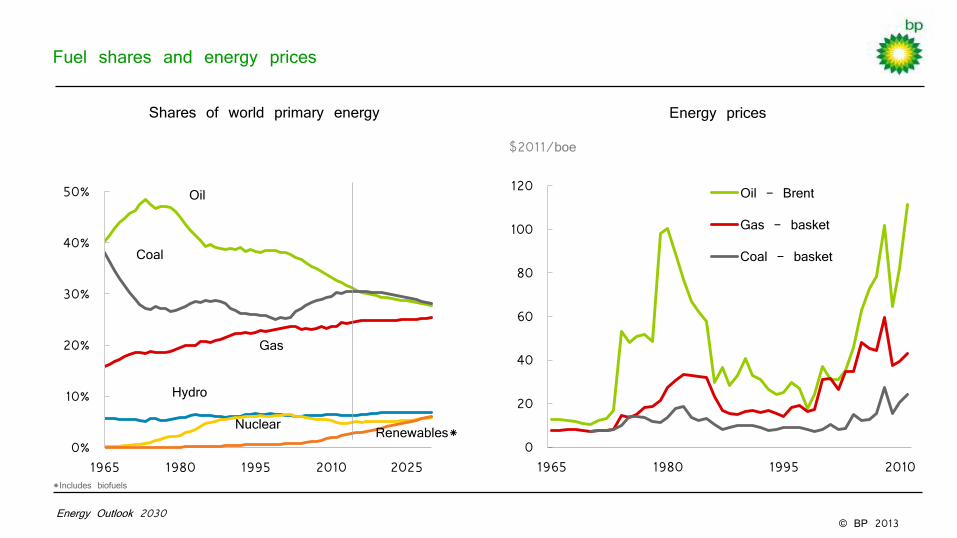

Shares of world primary energy

0%

10%

20%

30%

40%

50%

1965 1980 1995 2010 2025

Oil

Coal

Gas

Hydro

Nuclear Renewables*

*Includes biofuels

Fuel shares and energy prices

0

20

40

60

80

100

120

1965 1980 1995 2010

Oil - Brent

Gas - basket

Coal - basket

Energy prices

$2011/boe

© BP 2013 Energy Outlook 2030

0.0

0.1

0.2

0.3

0.4

0.5

1870 1890 1910 1930 1950 1970 1990 2010 2030

Energy intensity by region

Toe per thousand $2011 GDP (PPP)

China

US

World EU*

0

50

100

150

200

0

10

20

30

40

50

1970 1990 2010 2030

GDP (RHS)

Energy

Energy and GDP

Billion toe Trillion $2011 (PPP)

Energy efficiency improvements

*Euro4 (France, Italy, Germany, UK) pre-1970

© BP 2013 Energy Outlook 2030

0.0

0.1

0.2

0.3

0.4

0.5

1870 1890 1910 1930 1950 1970 1990 2010 2030

Energy intensity by region

Toe per thousand $2011 GDP (PPP)

China

US

World

EU*

0

50

100

150

200

0

10

20

30

40

50

1970 1990 2010 2030

GDP (RHS)

Energy

Energy and GDP

Billion toe Trillion $2011 (PPP)

Energy efficiency improvements

*Euro4 (France, Italy, Germany, UK) pre-1970

India

© BP 2013

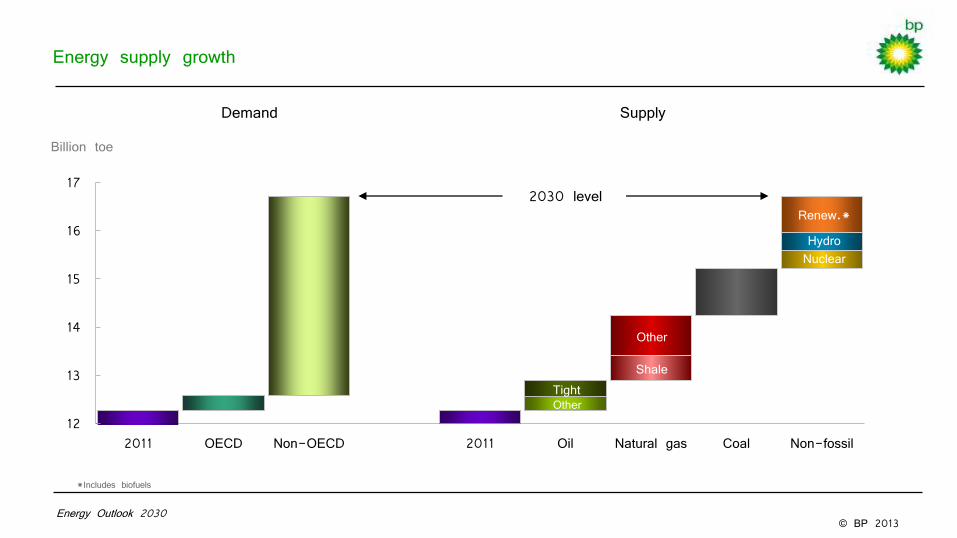

Energy supply growth

12

13

14

15

16

17

2011 OECD Non-OECD 2011 Oil Natural gas Coal Non-fossil

Demand Supply

Energy Outlook 2030

Tight Other

Shale

Other

Nuclear Hydro

Renew.*

Billion toe

2030 level

*Includes biofuels

© BP 2013

0

20

40

60

Asia Pacific

N. America

S. &

C. Am

erica

Africa

Europe &

Eurasia

Middle East

Gas Oil

Shale gas and tight oil: resources and production

Billion toe

Current resources Production in 2030

Energy Outlook 2030

0.0

0.3

0.6

0.9

Asia Pacific

N. America

S. &

C. Am

erica

Africa

Europe &

Eurasia

Middle East

Billion toe

Resources data © OECD/IEA 2012

© BP 2013

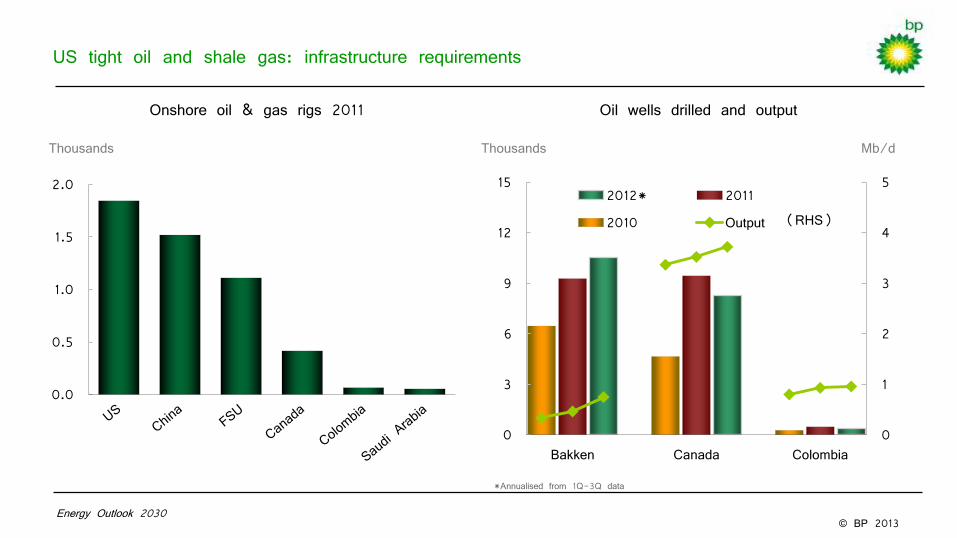

US tight oil and shale gas: infrastructure requirements

Onshore oil & gas rigs 2011

Thousands

Oil wells drilled and output

0

1

2

3

4

5

0

3

6

9

12

15

Bakken Canada Colombia

2012* 2011

2010 Output

Mb/d

Energy Outlook 2030

(RHS)

0.0

0.5

1.0

1.5

2.0

Thousands

*Annualised from 1Q-3Q data

© BP 2013

Introduction

Global energy trends

Outlook 2030: Fuel by fuel

Implications

Energy Outlook 2030

© BP 2013

0%

2%

4%

6%

8%

10%

0%

20%

40%

60%

1965 1978 1991 2004 2017 2030

Oil as % of primary energy Oil cost as % of GDP (RHS)

High oil prices are reducing oil’s share of primary energy

0%

25%

50%

75%

100%

1965 1978 1991 2004 2017 2030

Power

Other

Industry

Transport

% of energy

Oil share in sector Oil share of energy and GDP

% of GDP

Energy Outlook 2030

© BP 2013

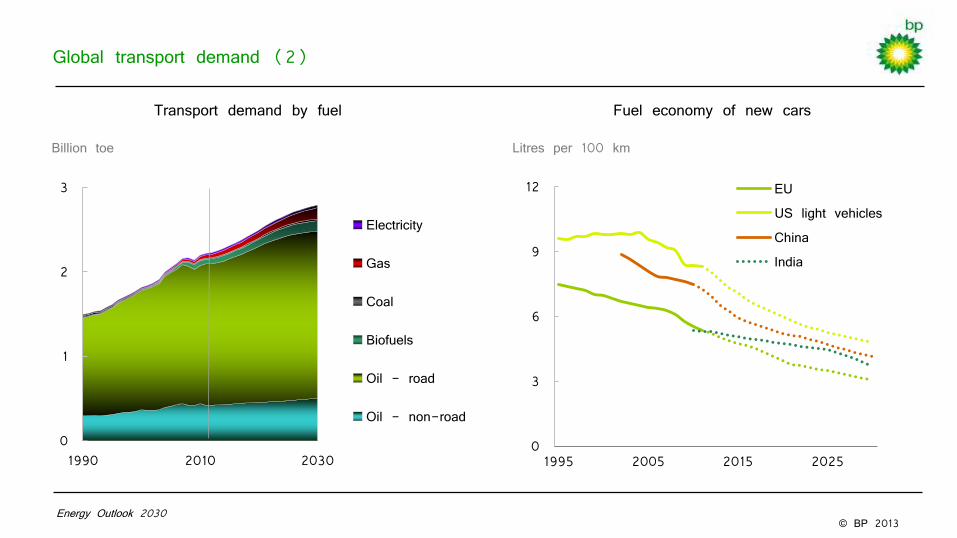

0

1

2

3

1990 2010 2030

Electricity

Gas

Coal

Biofuels

Oil - road

Oil - non-road

0

3

6

9

12

1995 2005 2015 2025

EU

US light vehicles

China

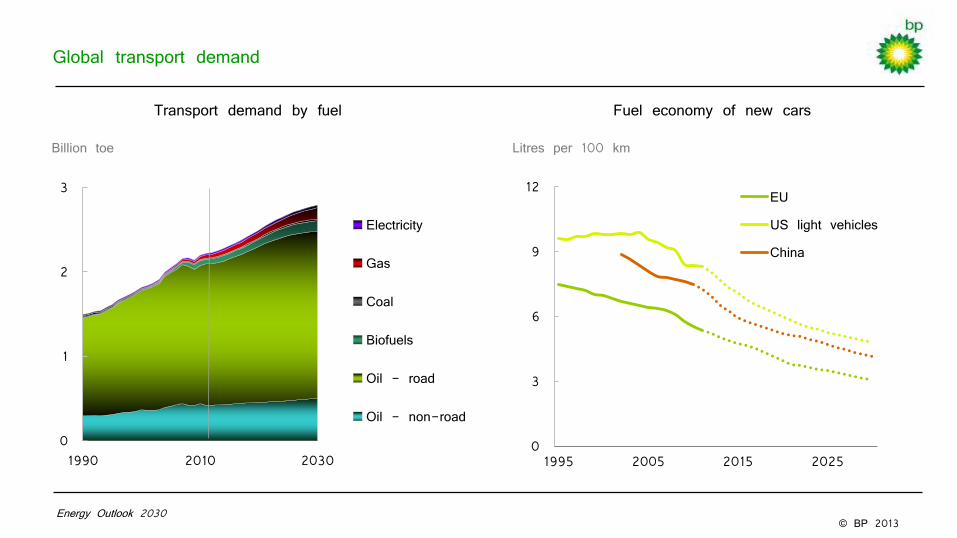

Global transport demand

Transport demand by fuel

Billion toe

Fuel economy of new cars

Litres per 100 km

Energy Outlook 2030

© BP 2013

0

1

2

3

1990 2010 2030

Electricity

Gas

Coal

Biofuels

Oil - road

Oil - non-road

0

3

6

9

12

1995 2005 2015 2025

EU US light vehicles China India

Global transport demand (2)

Transport demand by fuel

Billion toe

Fuel economy of new cars

Litres per 100 km

Energy Outlook 2030

© BP 2013

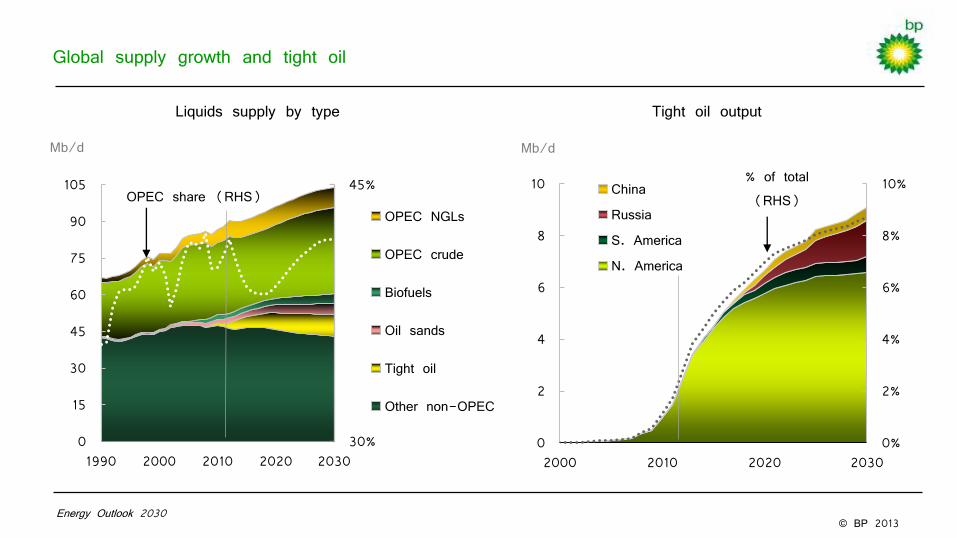

0%

2%

4%

6%

8%

10%

0

2

4

6

8

10

2000 2010 2020 2030

China

Russia

S. America

N. America

Liquids supply by type

30%

45%

0

15

30

45

60

75

90

105

1990 2000 2010 2020 2030

OPEC NGLs

OPEC crude

Biofuels

Oil sands

Tight oil

Other non-OPEC

Mb/d

NGLs

OPEC share (RHS)

Global supply growth and tight oil

Energy Outlook 2030

Tight oil output

% of total (RHS)

Mb/d

© BP 2013

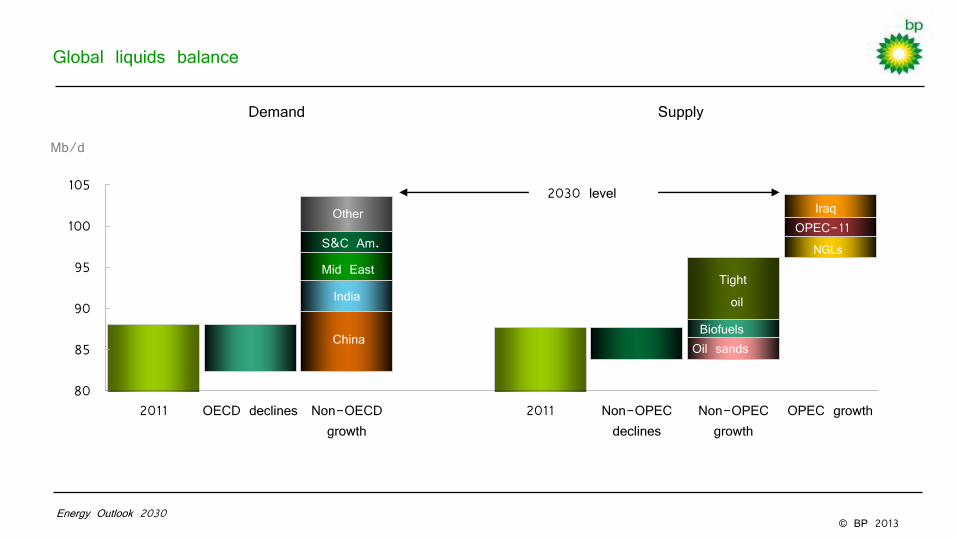

Global liquids balance

80

85

90

95

100

105

2011 OECD declines Non-OECD growth

2011 Non-OPEC declines

Non-OPEC growth

OPEC growth

Mb/d

Demand Supply

India

Mid East

China

NGLs OPEC-11

Other

S&C Am.

NGLs

Iraq 2030 level

Energy Outlook 2030

Tight oil

Biofuels Oil sands

© BP 2013

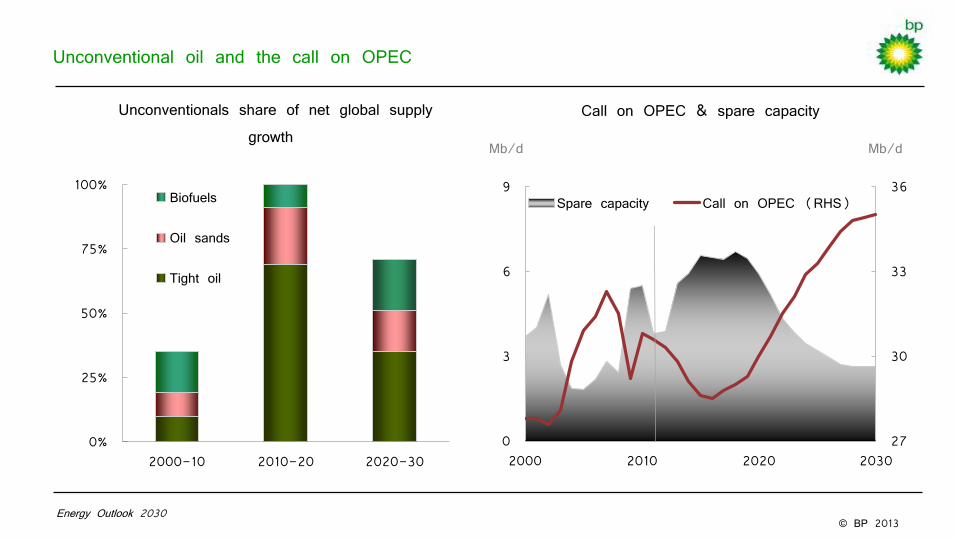

27

30

33

36

0

3

6

9

2000 2010 2020 2030

Spare capacity Call on OPEC (RHS)

Unconventional oil and the call on OPEC

Mb/d

Call on OPEC & spare capacity

Mb/d

Unconventionals share of net global supply growth

0%

25%

50%

75%

100%

2000-10 2010-20 2020-30

Biofuels

Oil sands

Tight oil

Energy Outlook 2030

© BP 2013

Shale gas and global supply growth

Energy Outlook 2030

Bcf/d

Gas production by type and region

0

100

200

300

400

500

1990 2000 2010 2020 2030

Non-OECD other

Non-OECD shale

OECD shale

OECD other

0%

6%

12%

18%

0

20

40

60

80

1990 2000 2010 2020 2030

RoW China

Europe & Eurasia Canada & Mexico

US

Shale gas production

Bcf/d

% of total (RHS)

© BP 2013 Energy Outlook 2030

-20

0

20

40

60

80

100

120

1990 2010 2030

Net pipeline imports

Net LNG imports

Shale gas production

Other domestic production

Energy Outlook 2030

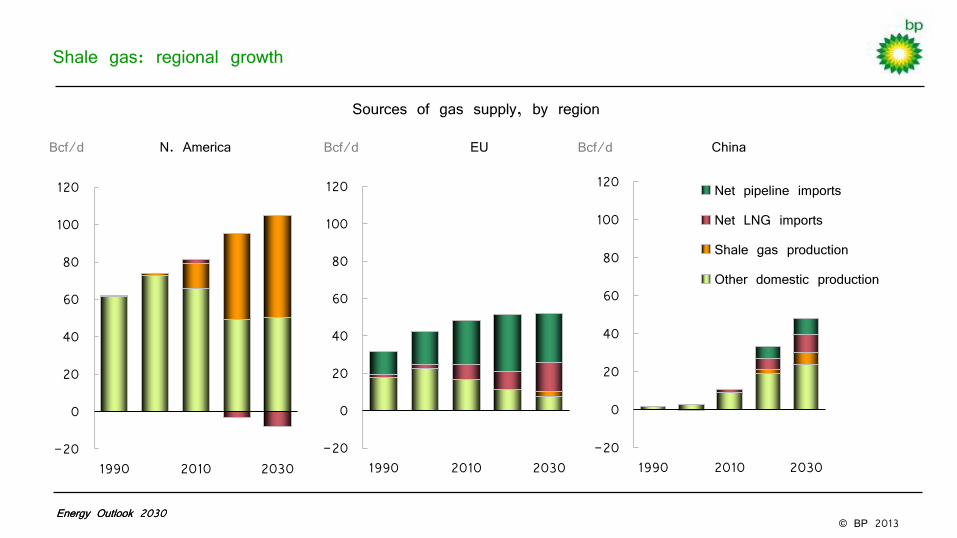

Shale gas: regional growth

Bcf/d China Bcf/d N. America Bcf/d EU

Sources of gas supply, by region

-20

0

20

40

60

80

100

120

1990 2010 2030 -20

0

20

40

60

80

100

120

1990 2010 2030

© BP 2013

0

10

20

30

40

50

60

1990 2010 2030

Energy Outlook 2030

0

10

20

30

40

50

60

1990 2010 2030

Net pipeline imports

Net LNG imports

Shale gas production

Other domestic production

Energy Outlook 2030

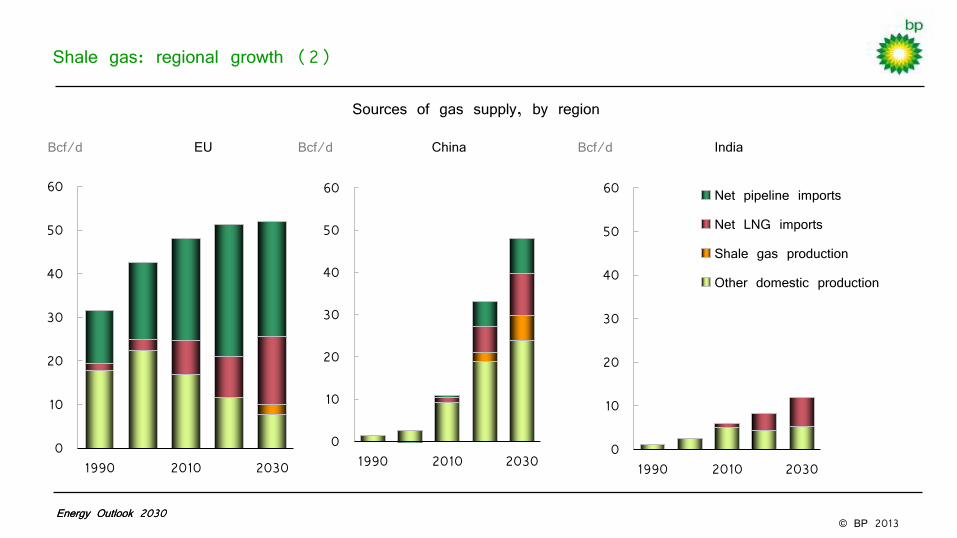

Shale gas: regional growth (2)

Bcf/d India Bcf/d EU

Sources of gas supply, by region

0

10

20

30

40

50

60

1990 2010 2030

Bcf/d China

© BP 2013

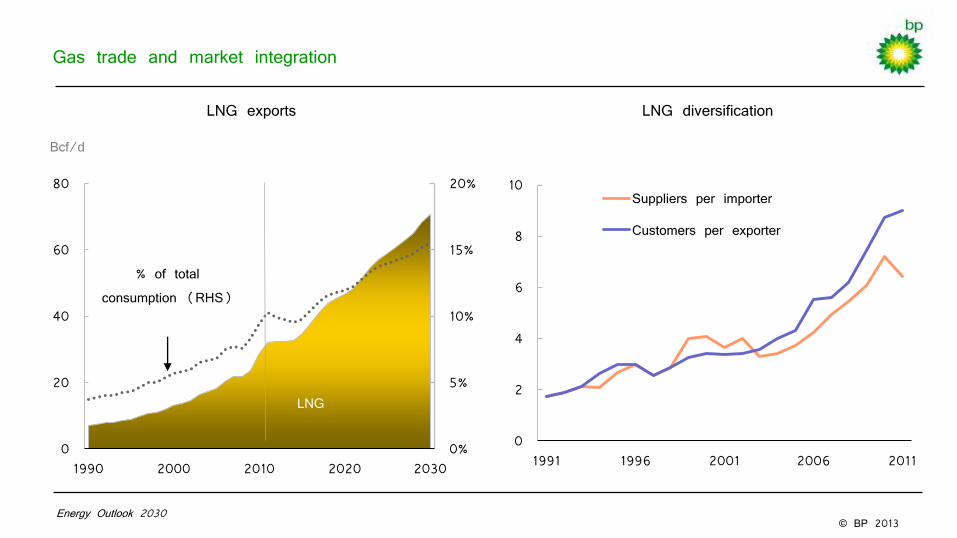

Gas trade and market integration

Energy Outlook 2030

0%

5%

10%

15%

20%

0

20

40

60

80

1990 2000 2010 2020 2030

LNG

Bcf/d

LNG exports

% of total consumption (RHS)

LNG diversification

0

2

4

6

8

10

1991 1996 2001 2006 2011

Suppliers per importer

Customers per exporter

© BP 2013 Energy Outlook 2030

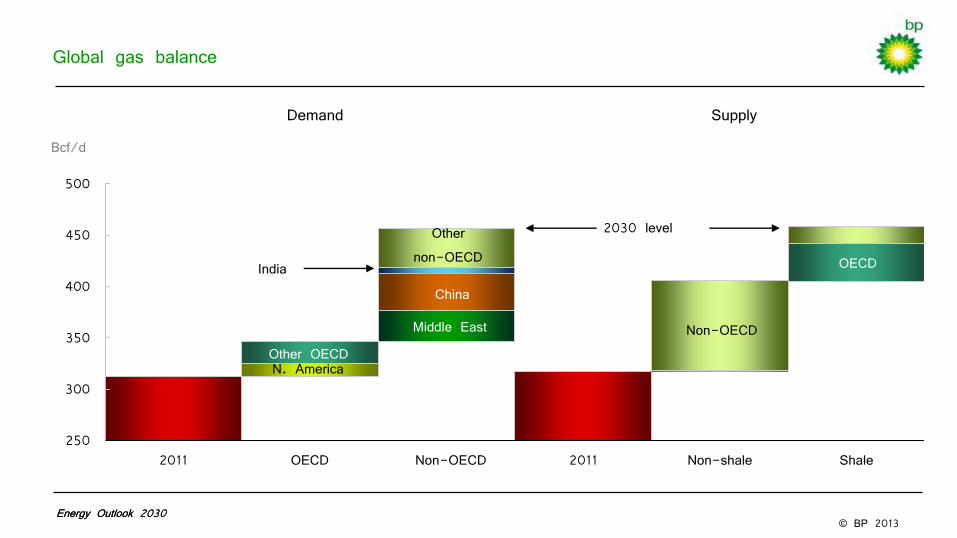

250

300

350

400

450

500

2011 OECD Non-OECD 2011 Non-shale Shale

N. America Other OECD

Middle East

China

Other non-OECD

Non-OECD

Energy Outlook 2030

Global gas balance

Bcf/d

Demand Supply

2030 level

OECD India

© BP 2013

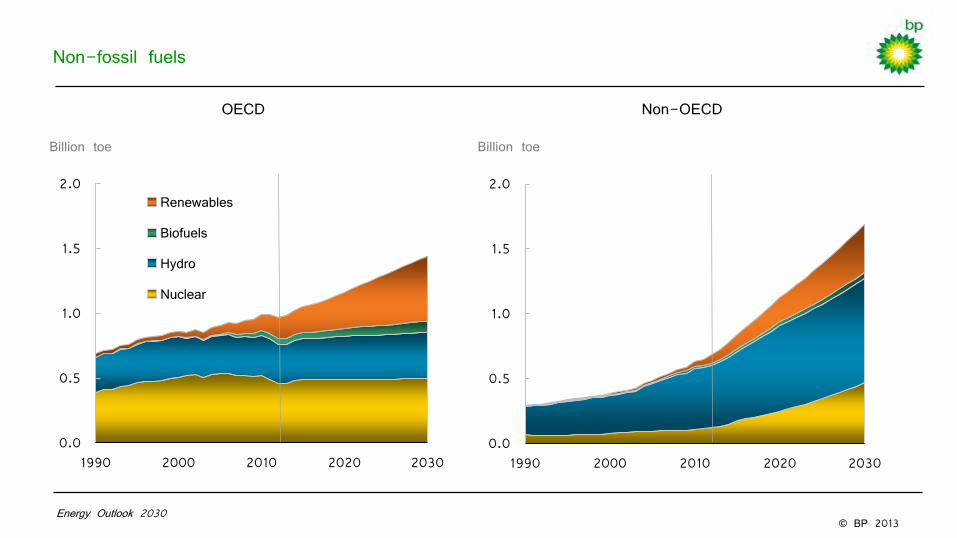

Non-fossil fuels

0.0

0.5

1.0

1.5

2.0

1990 2000 2010 2020 2030

Renewables

Biofuels

Hydro

Nuclear

Billion toe

Renewables in power

Biofuels

OECD

0.0

0.5

1.0

1.5

2.0

1990 2000 2010 2020 2030

Non-OECD

Billion toe

Energy Outlook 2030

© BP 2013

Growth of renewables in power

OECD

Non-OECD

0%

5%

10%

15%

20%

2000 2010 2020 2030

Nuclear 1970-2000

Renewables 2000-2030

1970 1980 1990 2000 0%

3%

6%

9%

12%

15%

0%

5%

10%

15%

20%

25%

OECD Europe Other OECD Non-OECD

Growth (RHS)

Share 2011

Share 2030

Renewable power

% p.a. % share

Share of power generation

Energy Outlook 2030

Growth 2011-30, and share of power

© BP 2013

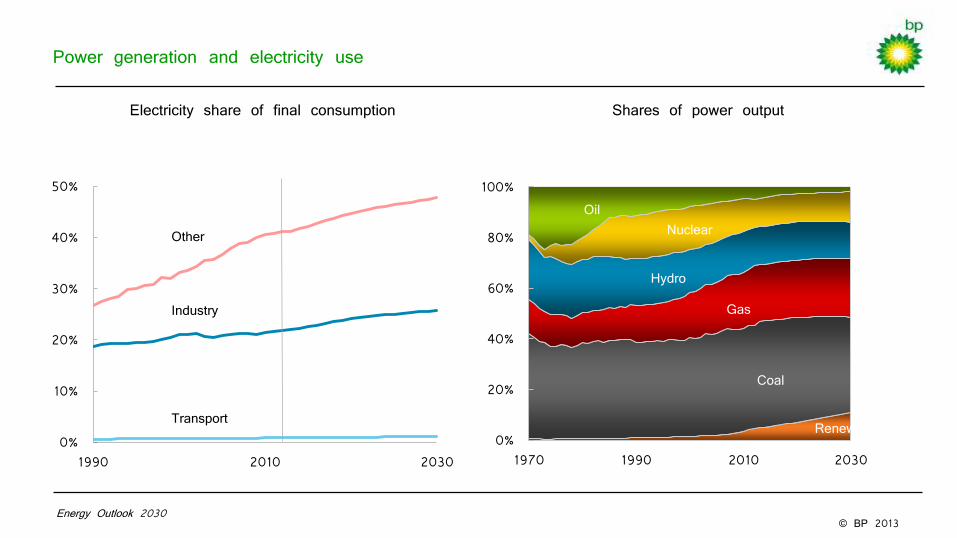

Electricity share of final consumption

Energy Outlook 2030

0%

10%

20%

30%

40%

50%

1990 2010 2030

Other

Industry

Transport

Power generation and electricity use

Shares of power output

0%

20%

40%

60%

80%

100%

1970 1990 2010 2030

Renew.

Nuclear

Coal

Oil

Hydro

Gas

© BP 2013

Introduction

Global energy trends

Outlook 2030: Fuel by fuel

Implications

Energy Outlook 2030

© BP 2013

0%

50%

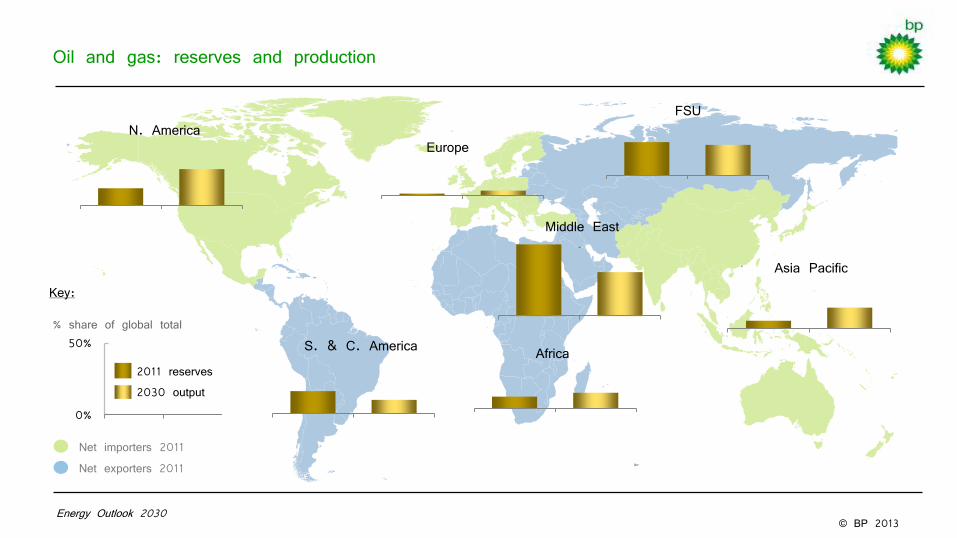

Oil and gas: reserves and production

2011 reserves 2030 output

% share of global total

Key:

Europe N. America

S. & C. America Africa

Middle East

FSU

Asia Pacific

Energy Outlook 2030

Net exporters 2011 Net importers 2011

© BP 2013

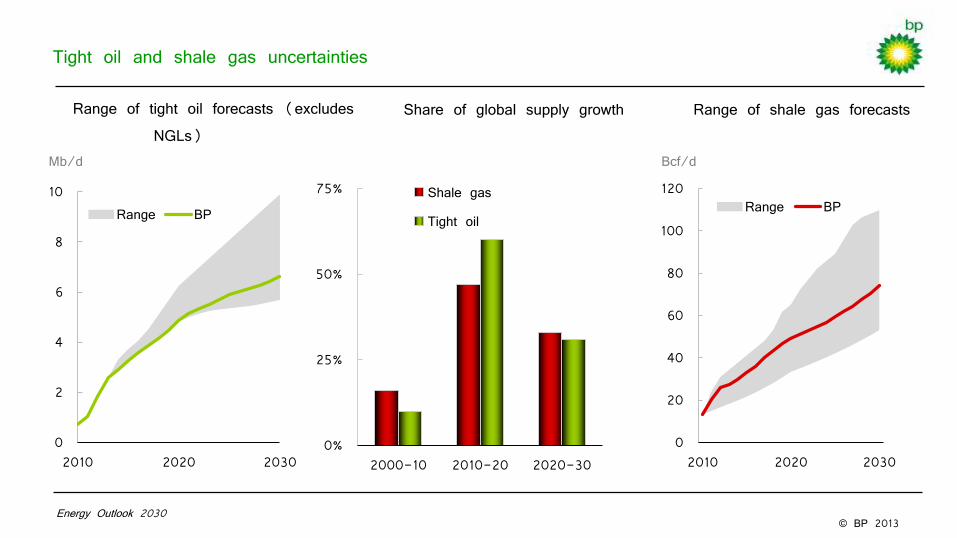

Tight oil and shale gas uncertainties

Share of global supply growth

0

2

4

6

8

10

2010 2020 2030

Range BP

Range of tight oil forecasts (excludes NGLs)

Mb/d

Energy Outlook 2030

0%

25%

50%

75%

2000-10 2010-20 2020-30

Shale gas

Tight oil

0

20

40

60

80

100

120

2010 2020 2030

Range BP

Bcf/d

Range of shale gas forecasts

© BP 2013

-80

-60

-40

-20

0

20

40

60

1990 2000 2010 2020 2030

China US

EU India

Energy imbalances to GDP ratio

Energy Outlook 2030

Energy imbalances

China EU US

-1,200

-900

-600

-300

0

300

1990

2010

2030

1990

2010

2030

1990

2010

2030

1990

2010

2030

Oil

Gas

Coal

Mtoe Toe per $Mln GDP PPP

Energy imbalances: import profiles

India

© BP 2013

0

200

400

600

800

1000

1200

1990 2000 2010 2020 2030

Saudi Arabia

Russia

Africa

Energy imbalances to GDP ratio

Energy Outlook 2030

Energy imbalances

Saudi Arabia Africa Russia

0

200

400

600

800

1990

2010

2030

1990

2010

2030

1990

2010

2030

Oil

Gas

Coal

Mtoe Toe per $Mln GDP PPP

Energy imbalances: export profiles

© BP 2013

Oil

Gas

CO2 emissions and primary energy

Billion tonnes CO2

Energy Outlook 2030

Growth of CO2 emissions

% p.a.

0

3

6

9

12

15

18

0

10

20

30

40

50

1970 1990 2010 2030

Emissions from energy use

Primary energy (RHS)

Billion toe

-2%

0%

2%

4%

6%

8%

China India EU US

1970-1990

1990-2010

2010-2030

Energy and carbon emissions

© BP 2013

Conclusion

0%

1%

2%

3%

4%

Population

Income per capita

Economic growth

Efficiency gains New supply

% p.a. Economic growth needs energy

Competition and innovation are the key to meeting this need

− energy efficiency

− new supplies

Energy security and climate change remain challenges

Energy Outlook 2030

January 2013

© BP 2013

0

30

60

90

120

150

180

1970 1990 2010 2030 0

1

2

3

4

5

6

7

8

9

1970 1990 2010 2030 0

3

6

9

12

15

18

1970 1990 2010 2030

Alternative for #4

Energy

Billion toe Trillion, $2011 PPP

GDP Population

Billion

Other non-OECD

India

OECD

Energy Outlook 2030 38

© BP 2013

India

Mtoe

Energy Outlook 2030

Growth by sector and fuel, 2011-2030 Primary energy demand by fuel

Oil

Coal

Gas

0

200

400

600

800

1000

1200

1990 2000 2010 2020 2030

Renew.*

Hydro

Nuclear

Coal

Gas

Oil

*Includes biofuels

-100

0

100

200

300

Transport

Industry

Other

Power

Hydro

Nuclear

Renew.

Electricity

Gas

Biofuels

Oil

Coal

Final energy use Inputs to power

Mtoe

© BP 2013

0

1

2

3

1990 2010 2030

Electricity

Gas

Coal

Biofuels

Oil - road

Oil - non-road

0

3

6

9

12

1995 2005 2015 2025

EU US light vehicles China India

Global transport demand (with India forecast added, no history)

Transport demand by fuel

Billion toe

Fuel economy of new cars

Litres per 100 km

Energy Outlook 2030

© BP 2013

0

5

10

15

20

25

30

35

40

45

50

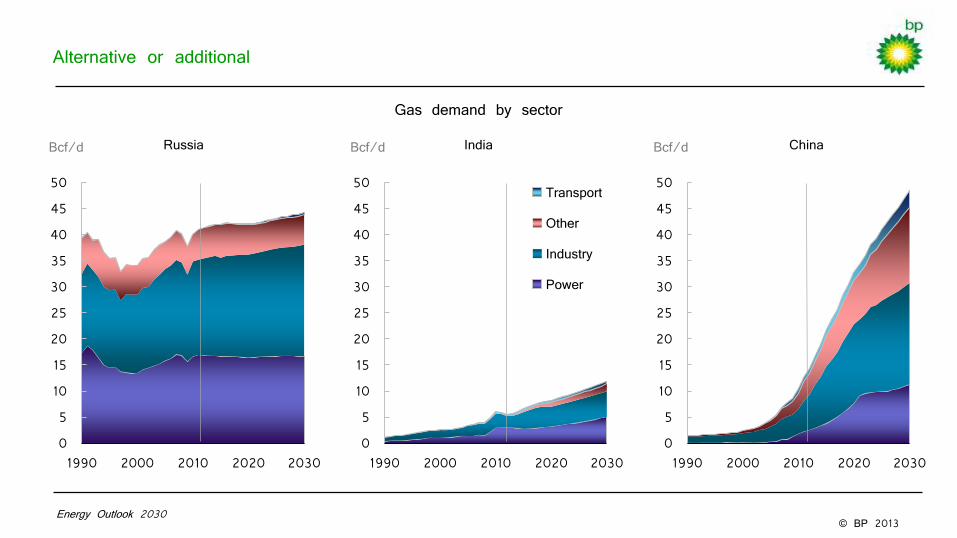

1990 2000 2010 2020 2030

Power

Oil

Industry

OECD

China

India

Energy Outlook 2030

China

India

OECD

China

India

China

India

OECD OECD

China

India

OECD

Bcf/d

Gas demand by sector

Power

Industry

0

5

10

15

20

25

30

35

40

45

50

1990 2000 2010 2020 2030

Transport

Other

Industry

Power

0

5

10

15

20

25

30

35

40

45

50

1990 2000 2010 2020 2030

Russia India China

Alternative or additional

Bcf/d Bcf/d

© BP 2013

0

10

20

30

40

50

60

1990 2010 2030

Energy Outlook 2030

0

10

20

30

40

50

60

1990 2010 2030

Net pipeline imports

Net LNG imports

Shale gas production

Other domestic production

Energy Outlook 2030

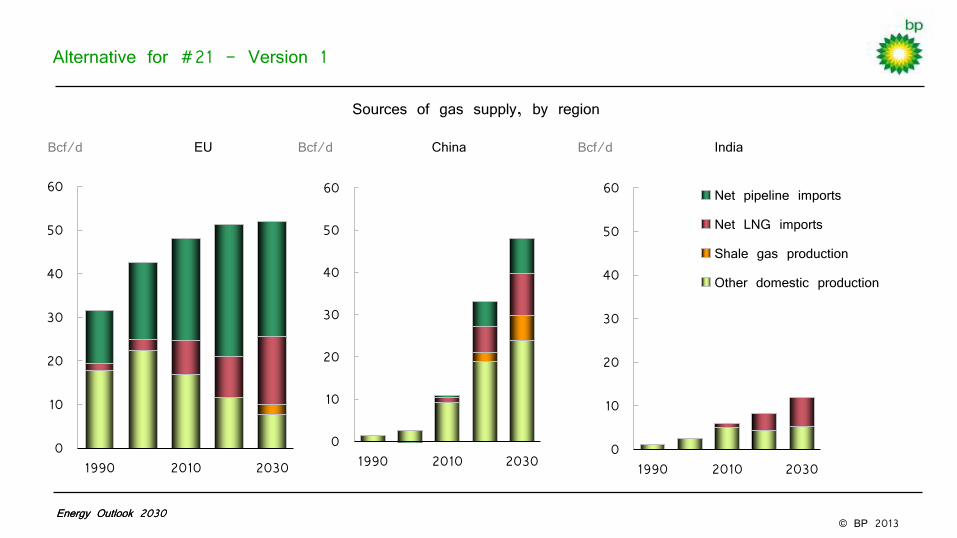

Alternative for #21 - Version 1

Bcf/d India Bcf/d EU

Sources of gas supply, by region

0

10

20

30

40

50

60

1990 2010 2030

Bcf/d China

© BP 2013 Energy Outlook 2030

-5

0

5

10

15

20

25

30

1990 2010 2030

Net pipeline imports

Net LNG imports

Shale gas production

Other domestic production

Energy Outlook 2030

Alternative for #21 - Version 2 (different scales)

Bcf/d India Bcf/d N. America Bcf/d EU

Sources of gas supply, by region

-20

0

20

40

60

80

100

120

1990 2010 2030 -20

0

20

40

60

80

100

120

1990 2010 2030

© BP 2013

High oil prices are reducing oil’s share of primary energy

0%

25%

50%

75%

100%

1965 1978 1991 2004 2017 2030

Power

Other

Industry

Transport

Oil share in sector

Energy Outlook 2030

0

2

4

6

8

10

12

1995 2005 2015 2025

EU

US light vehicles

China

Fuel economy of new cars

Litres per 100 km

© BP 2013

Coal consumption

Power

Oil

Industry

Coal demand by region

OECD

China

India

Billion toe

Energy Outlook 2030

China

India

OECD

China

Other Non-OECD

India

China

India

OECD

0

1

2

3

4

5

1990 2000 2010 2020 2030

OECD

China

Other non-OECD

India

China

India

OECD

Billion toe

Coal demand by sector

0

1

2

3

4

5

1990 2000 2010 2020 2030

Power

Industry

Other