ITS, UC Irvine

INDUSTRIES IN TRANSTION:FREIGHT TRANSPORTATION

INTERMEDIARIES IN THE INFORMATION AGE

Jiong Songand

Amelia C. Regan

Metrans 2nd Annual Transportation ConferenceFeb. 2, 2001

ITS, UC Irvine

Outline

Traditional Freight Transportation Intermediary

Section IISection IISection IISection II Current State and Evolution of the Industry

Niche Markets -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection ISection ISection I

Section IIISection IIISection IIISection III

Section IVSection IVSection IVSection IV

Section VSection VSection VSection V

ITS, UC Irvine

Traditional Freight Transportation Intermediary

Section IISection II Current State and Evolution of the Industry

Niche Market -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection I

Section IIISection III

Section IVSection IV

Section VSection V

ITS, UC Irvine

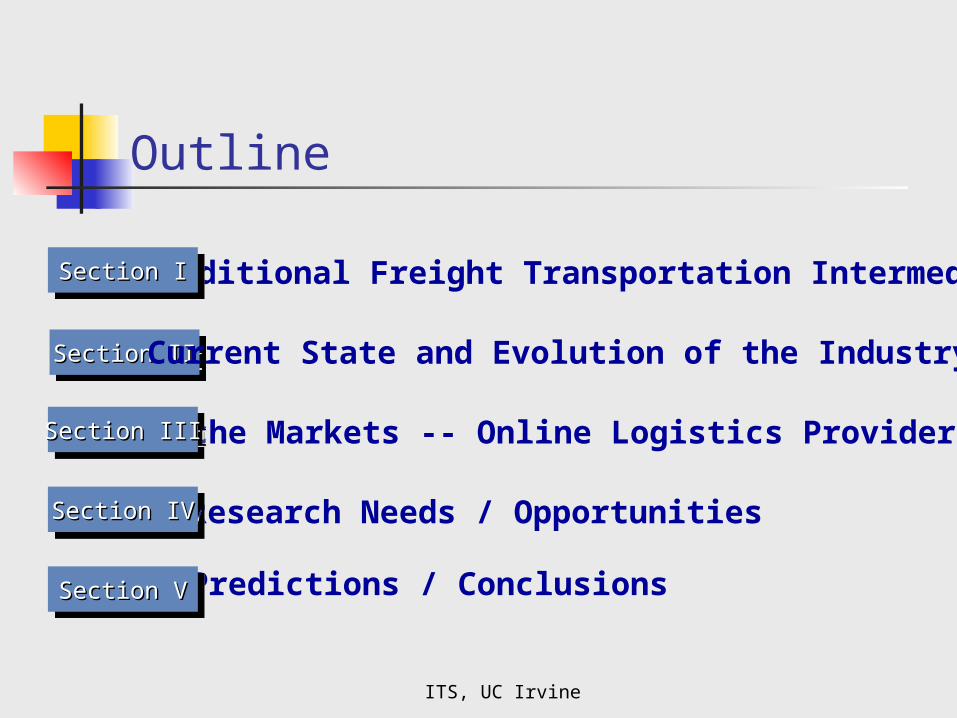

Third Party Logistics

“Third-party Logistics is simply the use of an outside company to perform all or part of the firm’s materials management and product distribution function.”

-- Simchi-Levi (2000)

“A relationship between a shipper and third party which, compared with the basic services, has more customized offerings, encompasses a broad number of service functions and is characterized by a long-term, more mutually beneficial relationship”

-- Murphy & Poist (1998)

Third Party Logistics

In-house Logistics Department

Shipper

Transportation

IT support

Warehousing

Others

In-house Operation

Outsourced Operation

3PL

Shipper

Shipper

Shipper

Transportation

Warehousing

IT support

SC integration

Others

ITS, UC Irvine

Characteristics of 3PL

Perform outsourced logistics activities Process management / Multiple activities More customized services Mutually beneficial and risk-sharing

relationship Long-term commitments (1~ 3 years)

ITS, UC Irvine

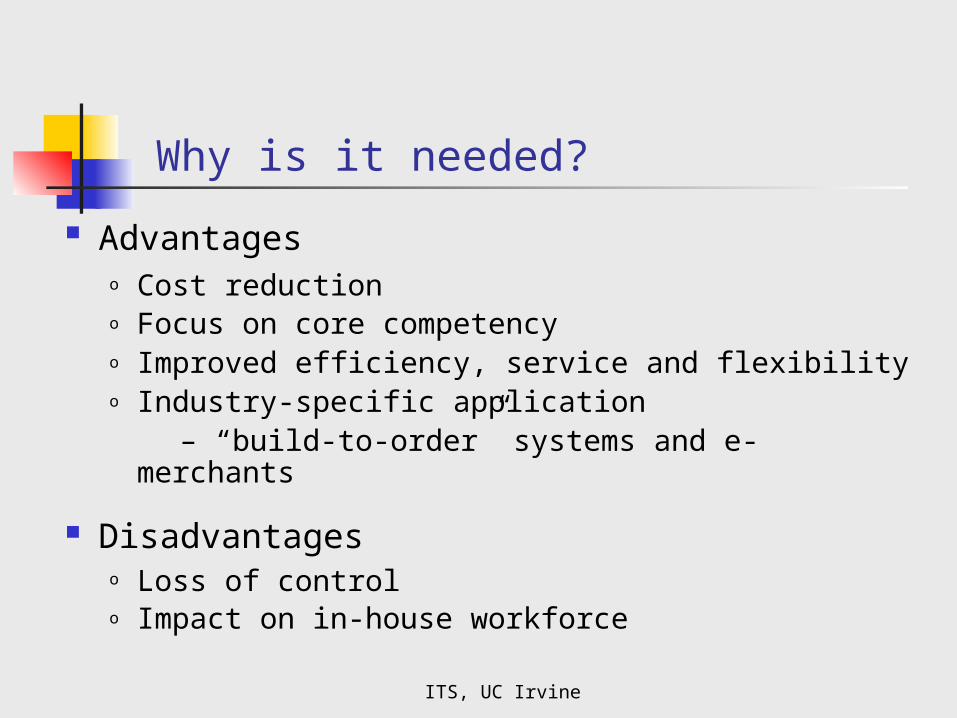

Why is it needed?

Advantageso Cost reductiono Focus on core competencyo Improved efficiency, service and flexibilityo Industry-specific application – “build-to-order” systems and e-merchants

Disadvantageso Loss of controlo Impact on in-house workforce

ITS, UC Irvine

Traditional Freight Transportation Intermediary

Section IISection II Current State and Evolution of the Industry

Niche Markets -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection I

Section IIISection III

Section IVSection IV

Section VSection V

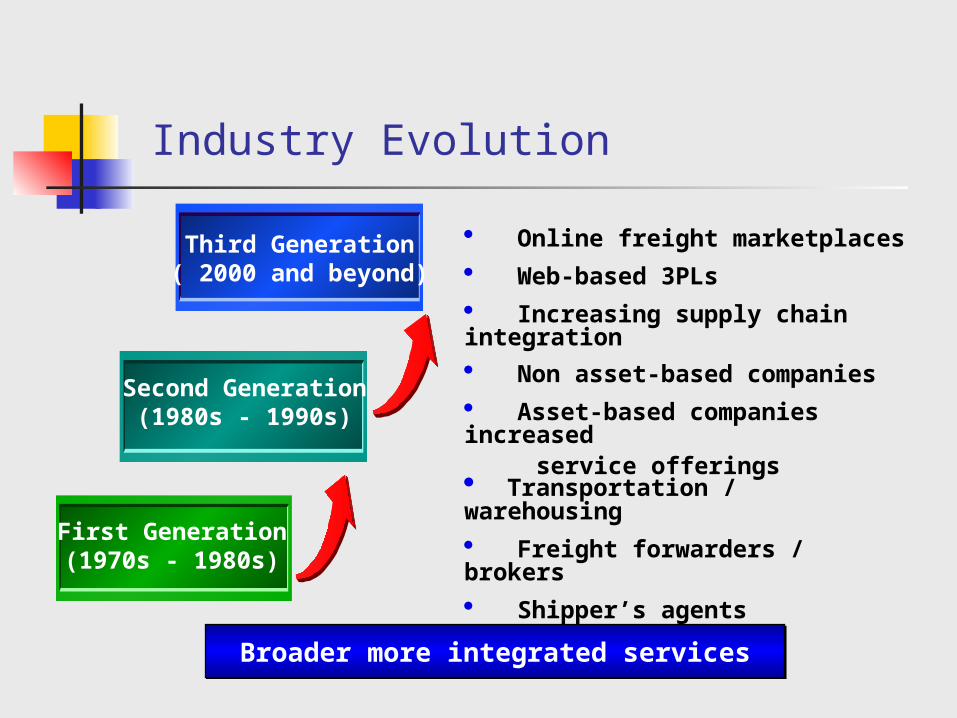

Industry Evolution

Third Generation( 2000 and beyond)

First Generation(1970s - 1980s)

Second Generation(1980s - 1990s)

Broader more integrated services

Transportation / warehousing Freight forwarders / brokers Shipper’s agents

Non asset-based companies Asset-based companies increased service offerings

Online freight marketplaces Web-based 3PLs Increasing supply chain integration

ITS, UC Irvine

Current State -- Service Offerings

Dedicated Contract Transportation / Transportation Procurement

Inventory Management Logistics Management and Consulting Freight Audit and Bill Payment Customs Services Shipment Tracking and Tracing Reverse Logistics and Value-added

Services

ITS, UC Irvine

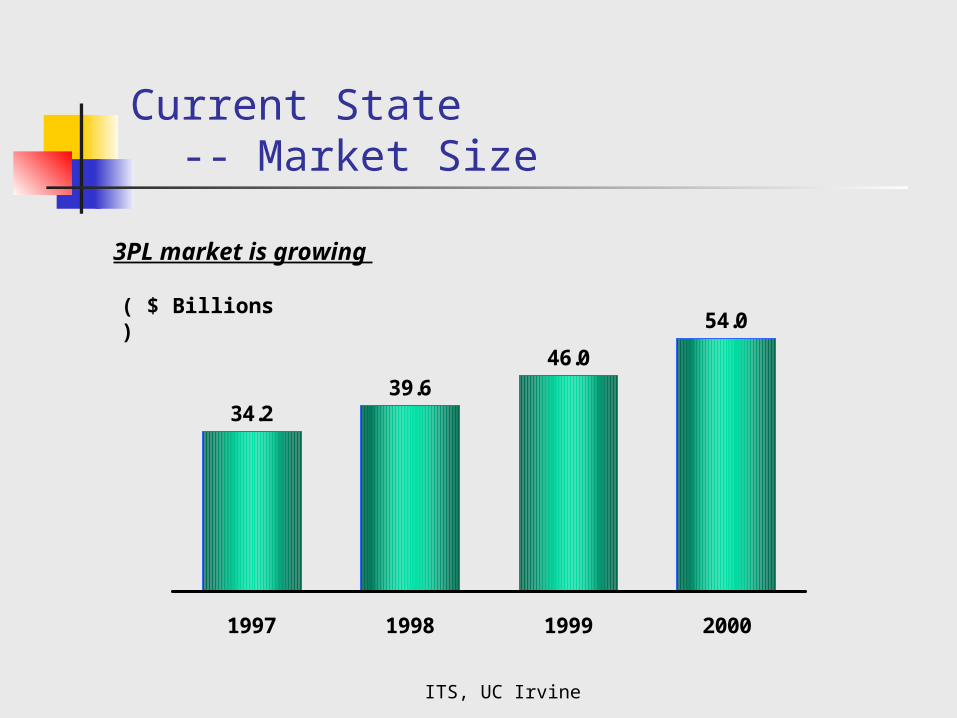

Current State -- Market Size

34.239.6

46.0

54.0

1997 1998 1999 2000

3PL market is growing

( $ Billions )

ITS, UC Irvine

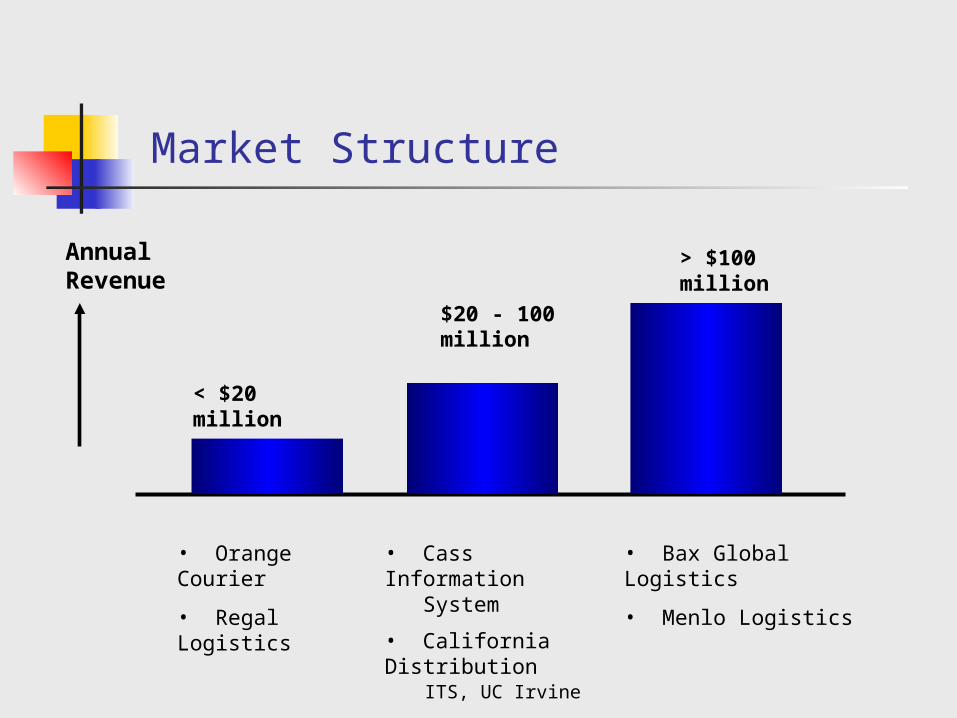

Market Structure

< $20 million

$20 - 100 million

> $100 million

Annual Revenue

• Orange Courier

• Regal Logistics

• Cass Information System

• California Distribution

• Bax Global Logistics

• Menlo Logistics

ITS, UC Irvine

Current use of 3PL by industry

75.9

71.1

61.4

56.2

53.8

82.2

Percentage of 3PL use in different industries Industry

Computer

Consumer

Retail

Chemical

Medical

Auto

Source "What's ahead for 3PLs“ Modern Materials Handling, April, 2000

ITS, UC Irvine

Current Industry Status

• No commonly accepted terminology

• Technologies increase visibility, efficiency and integration

• The service menu is rapidly changing

• New breed of companies are emerging

ITS, UC Irvine

Traditional Freight Transportation Intermediary

Section IISection II Current State and Evolution of the Industry

Niche Markets -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection I

Section IIISection III

Section IVSection IV

Section VSection V

ITS, UC Irvine

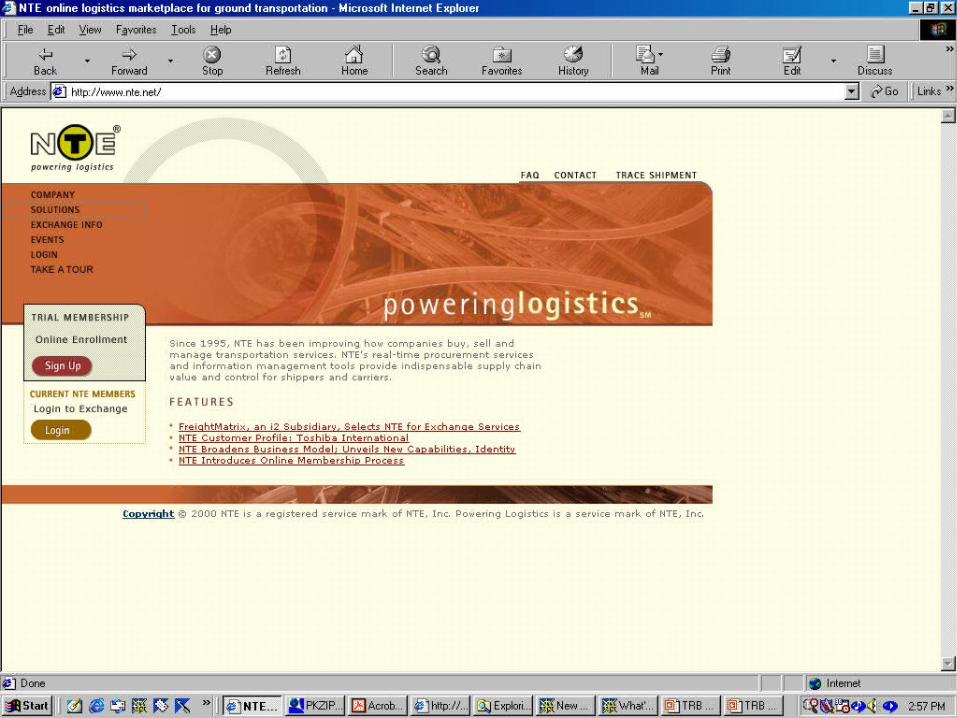

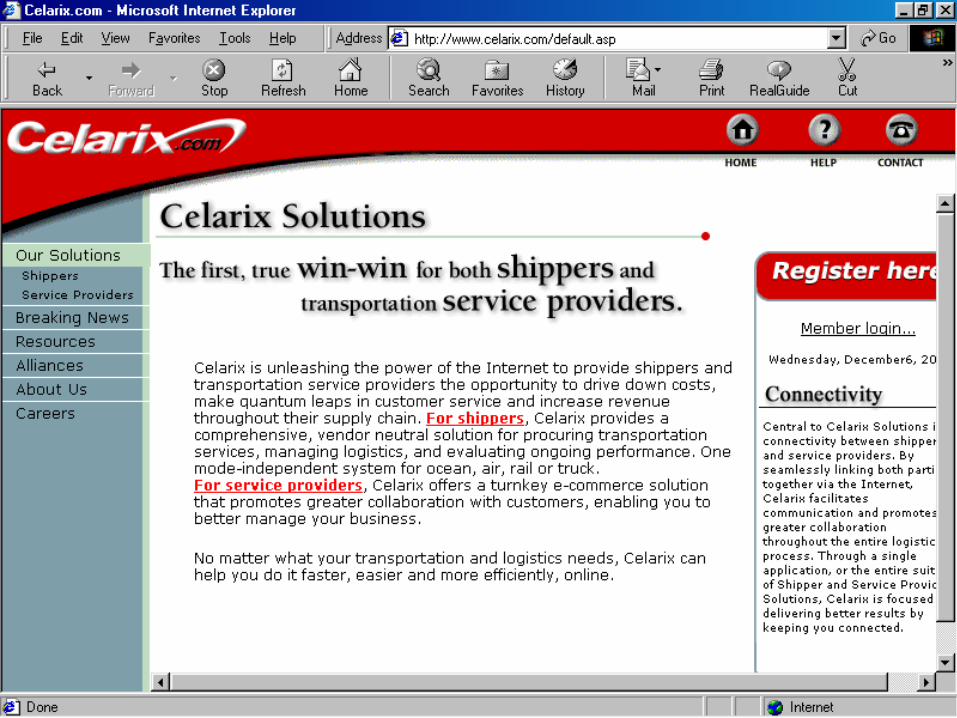

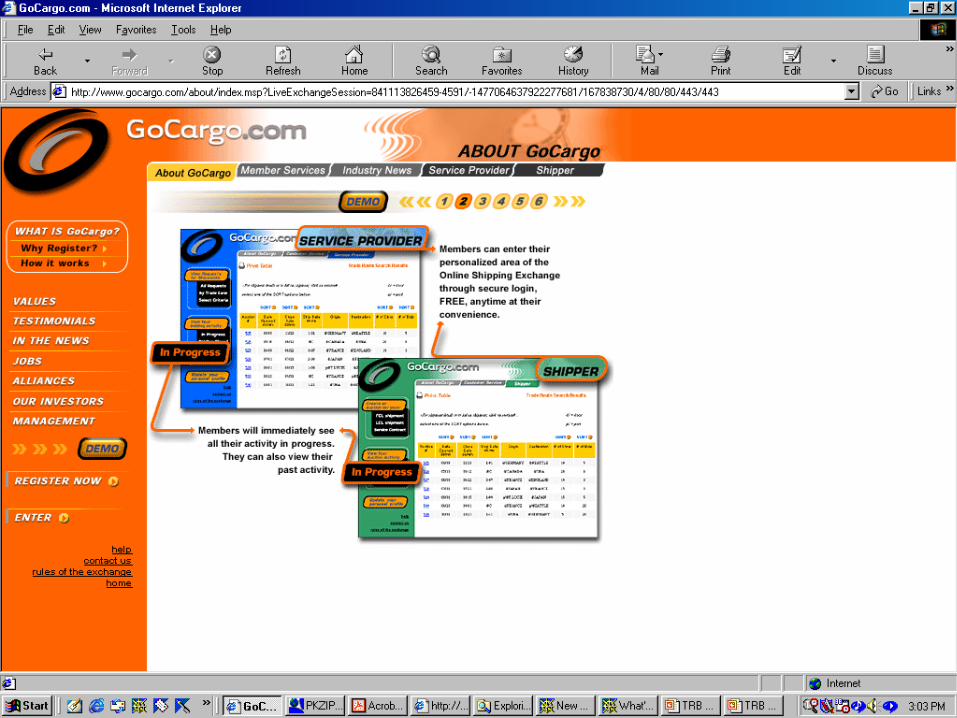

Niche Markets – Online Logistics Providers

Online Freight Marketplaces Spot market Auction and RFQ Exchange Meta-marketplaces

Application Service Providers (ASPs) Purchasing Consolidation Market Infomediaries

ITS, UC Irvine

The Freight Transportation Industry is Ideally Suited e-commerce High Fragmentation of Shippers and Carriers Many Intermediaries Complex Supply Chains High Search Costs Significant Opportunities for Economies of

Scale

Several Models Emerging

Online Logistics Providers-Opportunity

ITS, UC Irvine

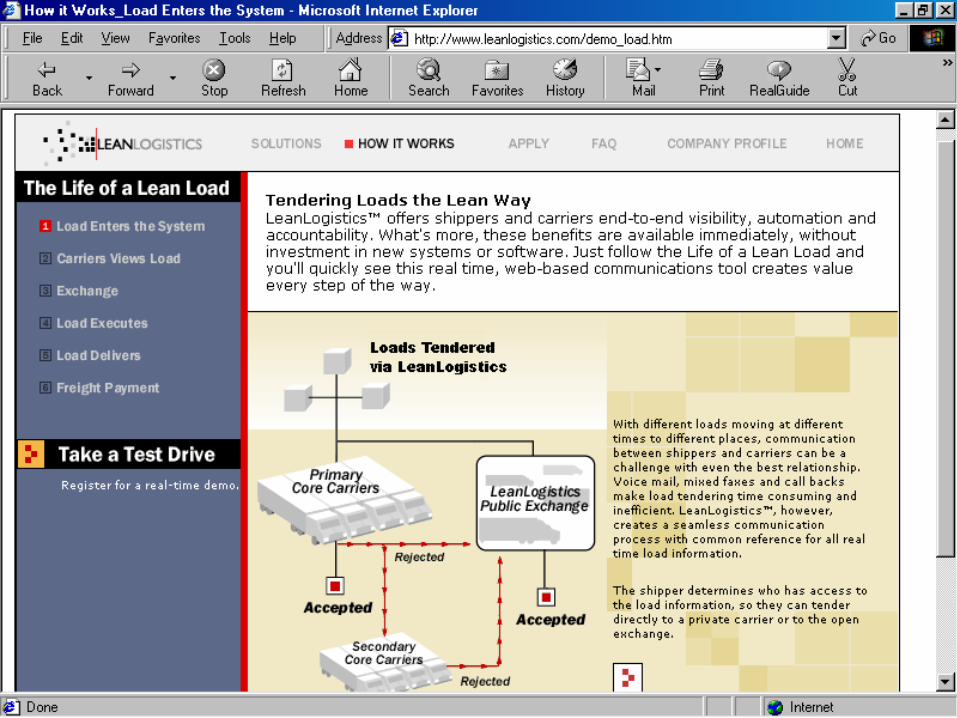

Spot market Auction and RFQ Exchange Meta-marketplaces Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

ITS, UC Irvine

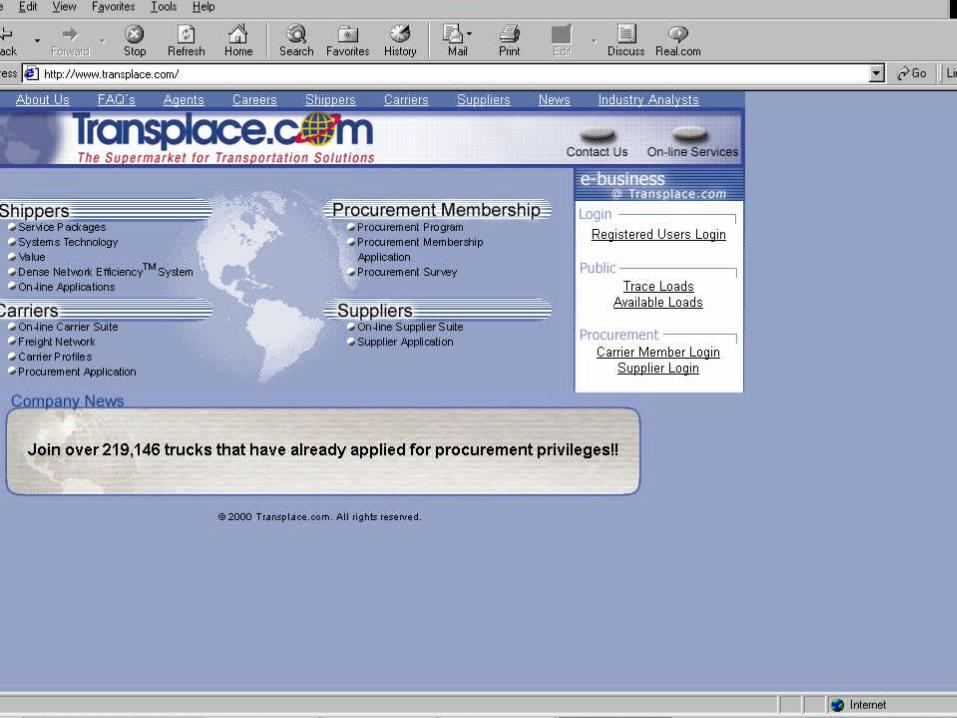

Spot market Auction and RFQ Exchange Meta-marketplaces Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

ITS, UC Irvine

Spot market Auction and RFQ Exchange Meta-marketplaces Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

ITS, UC Irvine

ITS, UC Irvine

Spot market Auction and RFQ Exchange Meta-marketplaces Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

Spot market Auction and RFQ Exchange Meta-marketplaces Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

ITS, UC Irvine

Spot market Auction and RFQ Exchange Application Service Providers (ASPs) Purchasing Consolidation market Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

Spot market Auction and RFQ Exchange Application Service Providers (ASPs) Co-ops Infomediaries

Niche Markets – Online Service Providers

ITS, UC Irvine

ITS, UC Irvine

Traditional Freight Transportation Intermediary

Section IISection II Current State and Evolution of the Industry

Niche Markets -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection I

Section IIISection III

Section IVSection IV

Section VSection V

ITS, UC Irvine

Recent Research

General market examinationo Lieb and Randal (1999)o Lieb and Peluso (2000a, 2000b)

Contracts and relationshipso Leahy, Murphy & Poist (1995)o Sankaran & Charman (2000)

Decision-making processeso Menon, McGinnis & Ackerman (1998)o Lim (2000)

ITS, UC Irvine

Behavioral Models

Carrier and Shipper behavior modelso Carrier selectiono Contract design o Contract negotiation

3PL provider’s behavioro Service offeringso Carrier selectiono Contract design o Contract negotiation

ITS, UC Irvine

Online Freight Marketplaces

Integrated and Time Sensitive Optimization Problems

o Dynamic and stochastic routing and scheduling systemso Dynamic inventory management systemso Combined inventory-routing modelso Real-time bidding and freight matching algorithmso Optimal pricing strategies for intermediaries and carrierso Optimal bidding strategies for shippers

Simulation-based analysis of costs and benefits to shippers, carriers and 3PLs under competing business models

o Is it a zero sum game? Who wins? Who loses? How much?

ITS, UC Irvine

Section IISection II Evolution and Current State of the Industry

Niche Markets -- Online Logistics Providers

Research Needs / Opportunities

Predictions / Conclusions

Section ISection I

Section IIISection III

Section IVSection IV

Section VSection V

Traditional Freight Transportation Intermediary

ITS, UC Irvine

Predictions and Conclusions

The total market for freight transportation intermediaries is still growing with the boom of e-commerce;

The conventional 3PLs will not fade, but will face with the competition from the online logistics providers;

The companies have to combine the logistics expertise with advanced technology to evolve;

Strategic alliance and merge/acquisition will be important to obtain comprehensive and intergrated supply chain solution capability;

Small carriers and niche carriers will benefit from increased access to shippers and reduced search costs

Medium sized and Large carriers may resist and try to continue business as usual or simply become e-commerce enabled using current business models

The 120+ on-line freight marketplaces will be reduced to less than 10 leaders and a few successful niche players in near future.

ITS, UC Irvine

Predictions and Conclusions

The freight transportation industry has historically been slow to change

Personal relationships will continue to be important despite a growing acceptance of web based interactions

The potential benefits of IT are huge Major industry changes will come – the question is how

soon

ITS, UC Irvine

End

![Automated Container Transport System Between Inland …Imperial)/[6] 02 METRANS Final Report.pdf · Automated Container Transport System between Inland ... The scarcity of land at](https://static.cupdf.com/doc/110x72/5afdd52d7f8b9a864d8e17d8/automated-container-transport-system-between-inland-imperial6-02-metrans.jpg)