Investor Presentation

January 2018

“Full cycle, fully engaged”

Ken Woolner, P.Eng.President & CEO

ADVISORY REGARDING FORWARD‐LOOKING STATEMENTS

2

This presentation contains certain forward‐looking information and statements with respect to Velvet Energy Ltd. (“Velvet” or the “Company”), includingexpectations, beliefs, plans, goals, objectives, assumptions, information and statements about future events, conditions, results of operations,performance, Velvet’s planned capital expenditure program and the nature of the expenditures, drilling plans, expected drilling and completion costs,expected average production, the expected splits among crude oil, NGLs and natural gas, forecasted commodity prices and factors affecting natural gasprices, forecasted general and administrative expenses, interest expenses, revenue, operating income, operating netbacks, funds from operations andyear‐end bank debt, management’s assessment of future potential, including years of drilling inventory and expectations with respect to natural gasdemand and supply in North America.. These forward‐looking statements are based on assumptions and are subject to numerous risks and uncertainties,certain of which are beyond the Company’s control, including the impact of general economic conditions; industry conditions; volatility of commodityprices; currency exchange rates; imprecision of reserve estimates; environmental risks; competition from other explorers; stock market volatility; oil andnatural gas development and transportation; actions by governmental authorities, including changes in government regulation, royalties and taxation;dependence upon compressors, gathering lines, pipelines and other facilities, certain of which the Company does not control; shortage or lack ofavailable of pipeline capacity or other transportation facilities; weather conditions, natural disasters and fires; and ability to access sufficient capital. Wecaution that the foregoing list of risks and uncertainties is not exhaustive. The use of any of the words “anticipate”, “continue”, “estimate”, “expect”,“may”, “will”, “should”, “believe”, “plans”, and similar expressions are intended to identify forward‐looking information or statements

Statements relating to “reserves” or “resources” are deemed to be forward‐looking statements as they involve the implied assessment, based on currentestimates and assumptions that the reserves and resources can be profitably produced in the future. Readers are cautioned that disclosure of any welltest results is not necessarily indicative of long‐term performance.

Velvet’s actual results, performance or achievement could differ materially from those expressed or implied by these forward‐looking statements. Noassurance can be given that any events anticipated herein will transpire or occur and such forward‐looking statements included in this presentationshould not be unduly relied upon.

In addition, the reader is cautioned that historical results are not necessarily indicative of future performance. The forward‐looking statementscontained herein are made as of the date of this presentation and the Company does not intend, and does not assume any obligation, to update orrevise any forward‐looking statements, whether as a result of new information, future events or otherwise, unless expressly required by applicablesecurities laws.

Certain information set out herein may be considered as “financial outlook” within the meaning of applicable securities laws. The purpose of thisfinancial outlook is to provide readers with disclosure regarding Velvet’s reasonable expectations as to the anticipated results of its proposed businessactivities for the periods indicated. Readers are cautioned that the financial outlook may not be appropriate for other purposes.

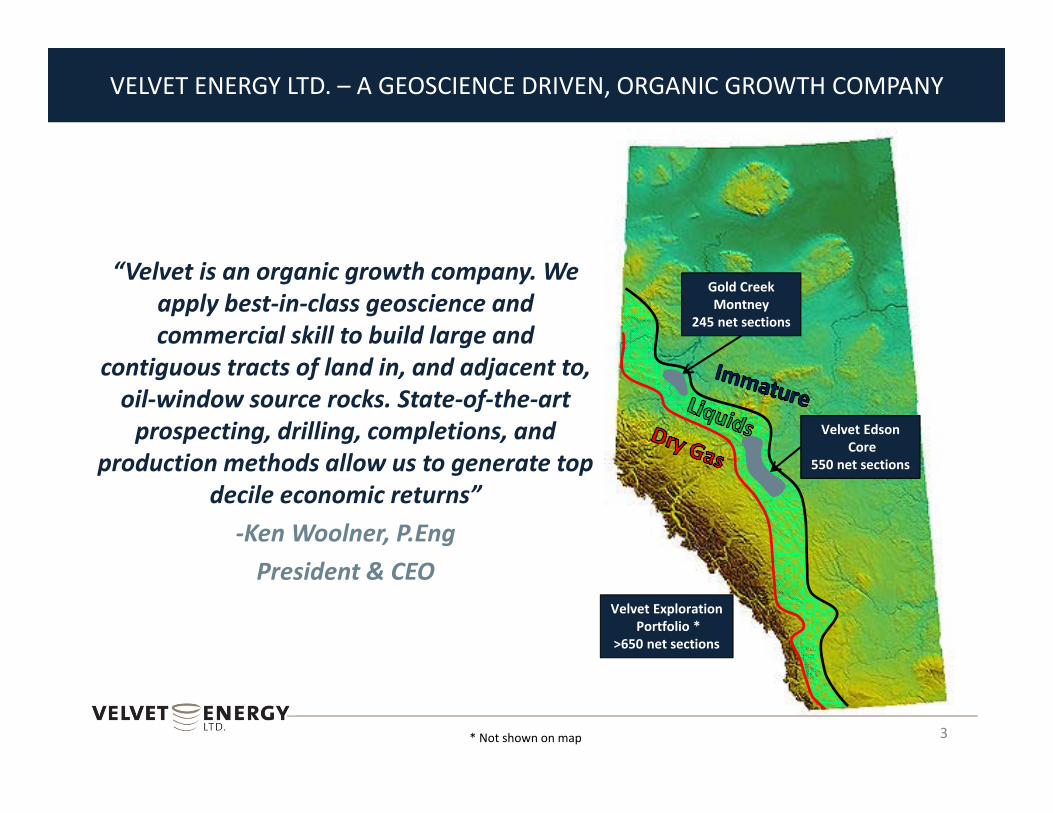

VELVET ENERGY LTD. – A GEOSCIENCE DRIVEN, ORGANIC GROWTH COMPANY

3

“Velvet is an organic growth company. We apply best‐in‐class geoscience and commercial skill to build large and

contiguous tracts of land in, and adjacent to, oil‐window source rocks. State‐of‐the‐art prospecting, drilling, completions, and

production methods allow us to generate top decile economic returns”

‐Ken Woolner, P.EngPresident & CEO

Velvet EdsonCore

550 net sections

Gold CreekMontney

245 net sections

Velvet ExplorationPortfolio *

>650 net sections

* Not shown on map

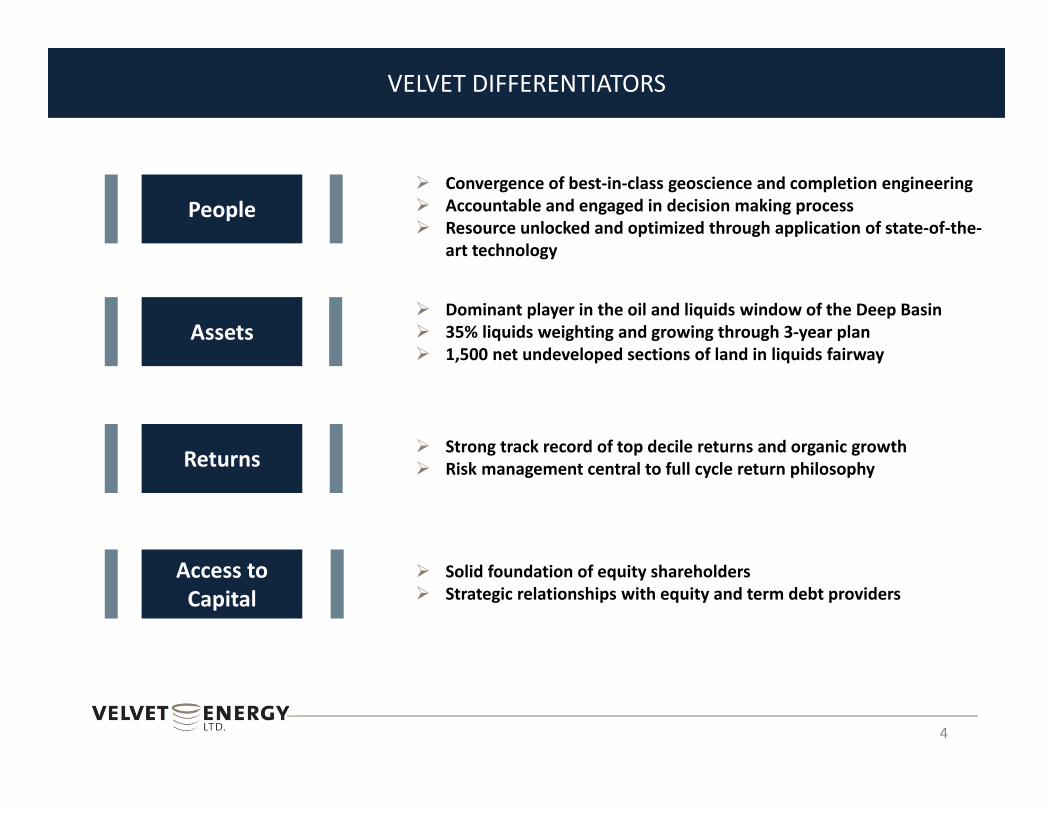

VELVET DIFFERENTIATORS

4

Convergence of best‐in‐class geoscience and completion engineering Accountable and engaged in decision making process Resource unlocked and optimized through application of state‐of‐the‐

art technology

People

Assets

Returns

Access to Capital

Dominant player in the oil and liquids window of the Deep Basin 35% liquids weighting and growing through 3‐year plan 1,500 net undeveloped sections of land in liquids fairway

Strong track record of top decile returns and organic growth Risk management central to full cycle return philosophy

Solid foundation of equity shareholders Strategic relationships with equity and term debt providers

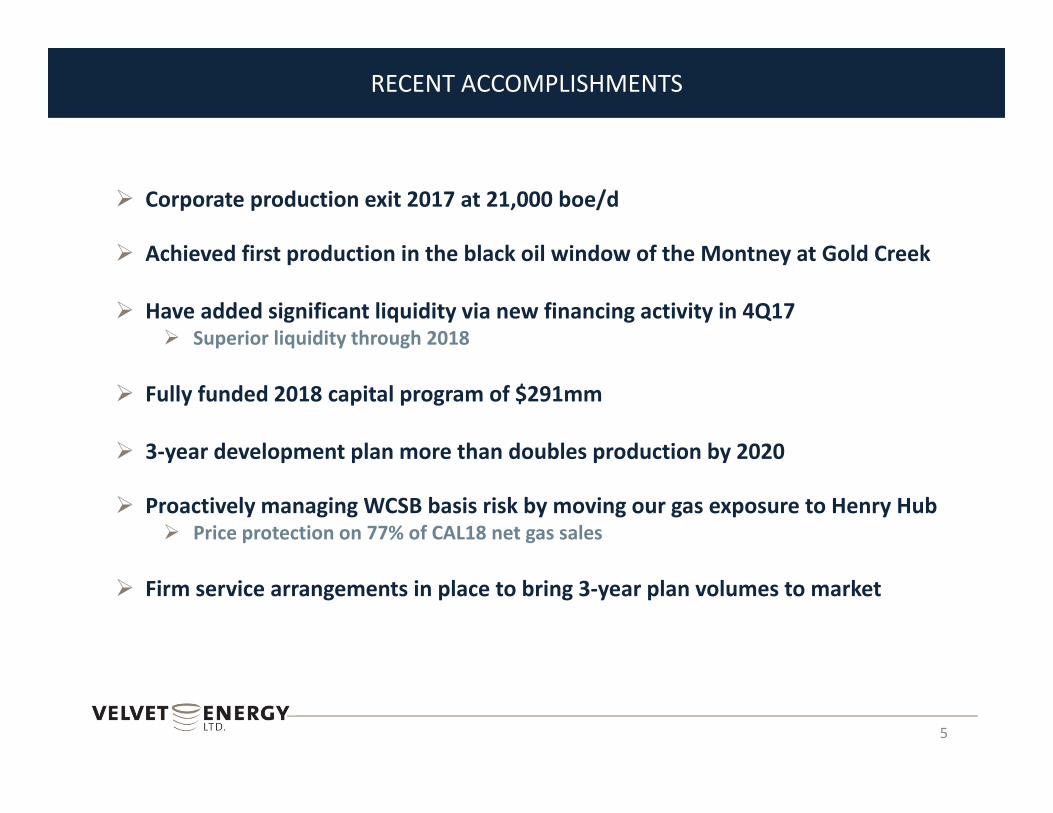

RECENT ACCOMPLISHMENTS

5

Corporate production exit 2017 at 21,000 boe/d

Achieved first production in the black oil window of the Montney at Gold Creek

Have added significant liquidity via new financing activity in 4Q17 Superior liquidity through 2018

Fully funded 2018 capital program of $291mm

3‐year development plan more than doubles production by 2020

Proactively managing WCSB basis risk by moving our gas exposure to Henry Hub Price protection on 77% of CAL18 net gas sales

Firm service arrangements in place to bring 3‐year plan volumes to market

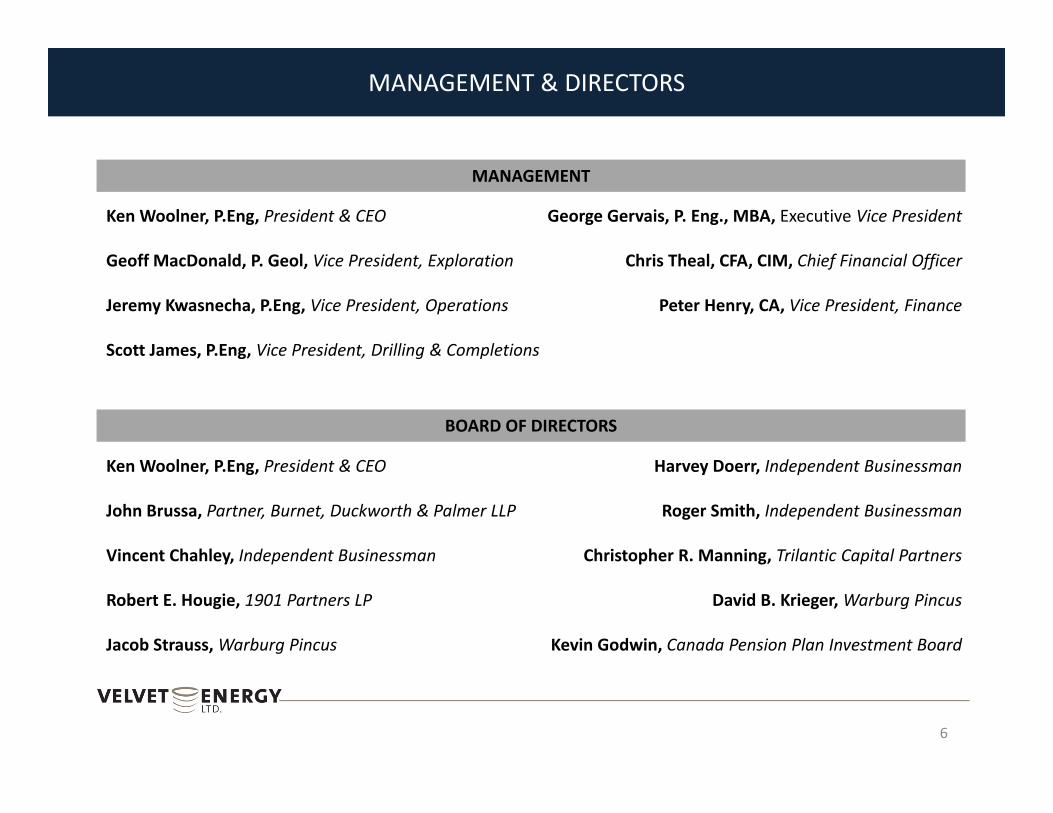

MANAGEMENT & DIRECTORS

6

Ken Woolner, P.Eng, President & CEO

Geoff MacDonald, P. Geol, Vice President, Exploration

Jeremy Kwasnecha, P.Eng, Vice President, Operations

Scott James, P.Eng, Vice President, Drilling & Completions

George Gervais, P. Eng., MBA, Executive Vice President

Chris Theal, CFA, CIM, Chief Financial Officer

Peter Henry, CA, Vice President, Finance

Ken Woolner, P.Eng, President & CEO

John Brussa, Partner, Burnet, Duckworth & Palmer LLP

Vincent Chahley, Independent Businessman

Robert E. Hougie, 1901 Partners LP

Jacob Strauss, Warburg Pincus

Harvey Doerr, Independent Businessman

Roger Smith, Independent Businessman

Christopher R. Manning, Trilantic Capital Partners

David B. Krieger, Warburg Pincus

Kevin Godwin, Canada Pension Plan Investment Board

MANAGEMENT

BOARD OF DIRECTORS

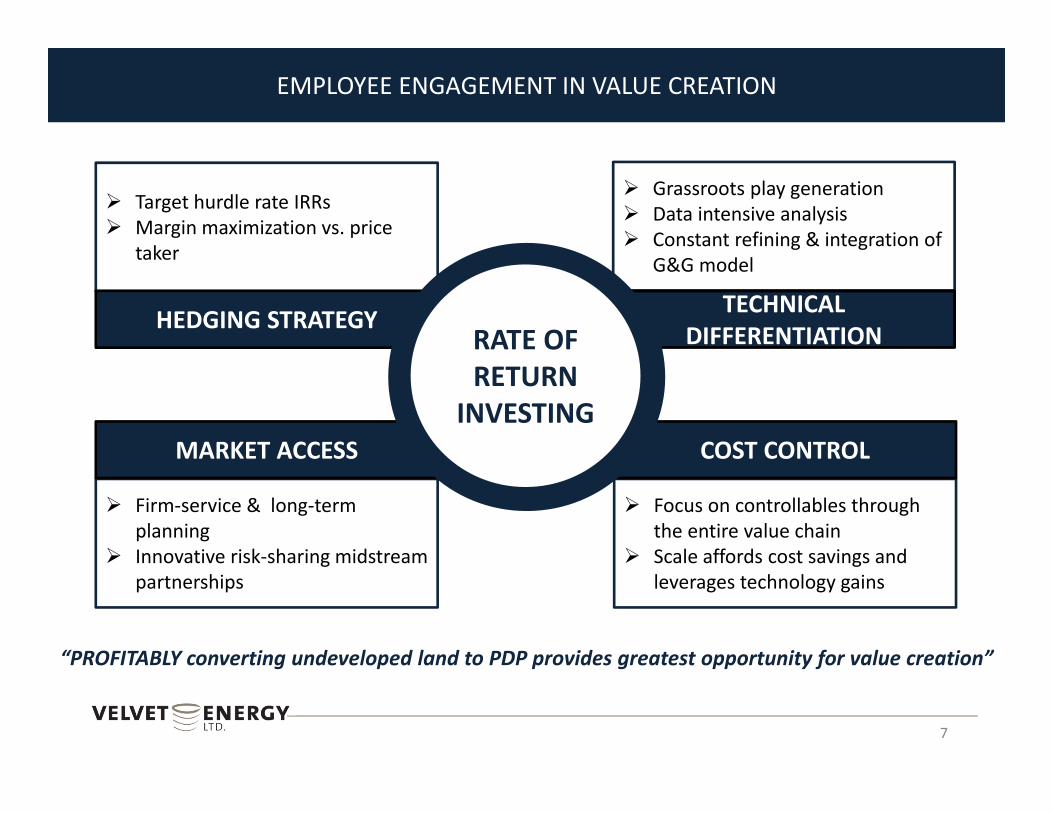

Firm‐service & long‐term planning

Innovative risk‐sharing midstream partnerships

Focus on controllables through the entire value chain

Scale affords cost savings and leverages technology gains

Grassroots play generation Data intensive analysis Constant refining & integration of

G&G model

Target hurdle rate IRRs Margin maximization vs. price

taker

EMPLOYEE ENGAGEMENT IN VALUE CREATION

7

“PROFITABLY converting undeveloped land to PDP provides greatest opportunity for value creation”

TECHNICAL DIFFERENTIATION

MARKET ACCESS COST CONTROL

HEDGING STRATEGYRATE OF RETURN

INVESTING

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

‐ 10.00 20.00 30.00 40.00 50.00 60.00 70.00 80.00 90.00 100.00

CFRO

I (%)

Average Annual WTI Oil Price (US$/bbl)

Velvet CFROI vs. WTI Oil Price

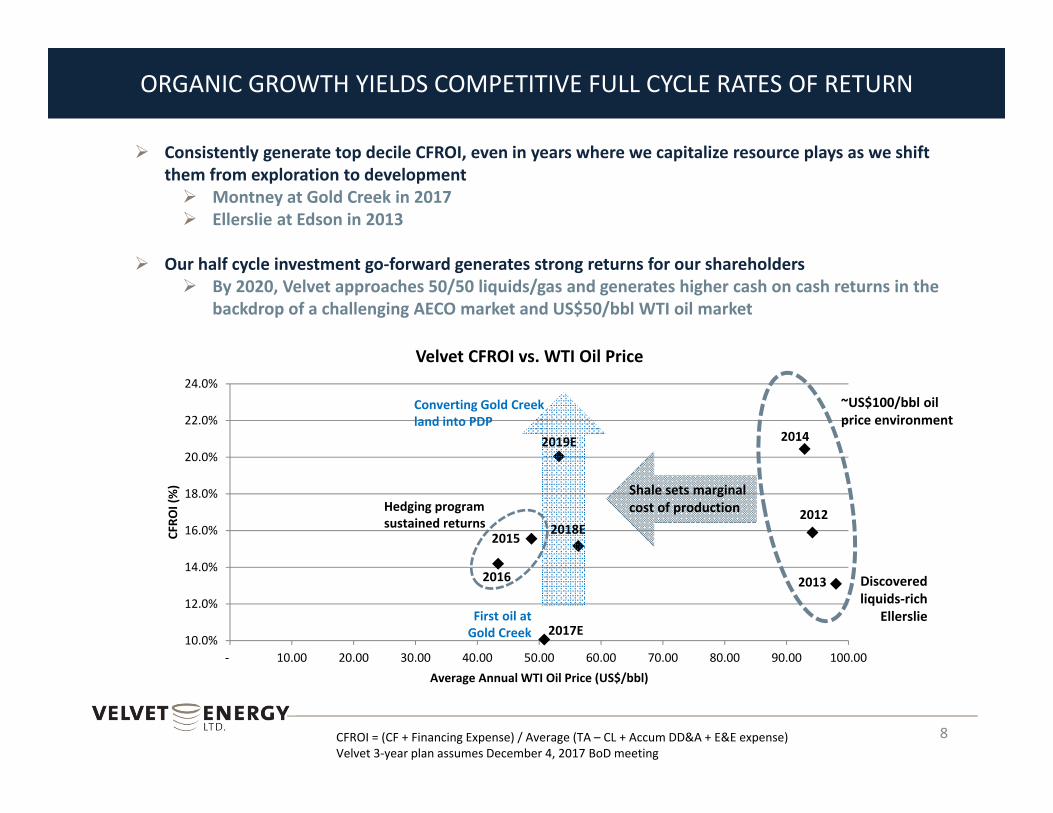

ORGANIC GROWTH YIELDS COMPETITIVE FULL CYCLE RATES OF RETURN

8

Consistently generate top decile CFROI, even in years where we capitalize resource plays as we shift them from exploration to development Montney at Gold Creek in 2017 Ellerslie at Edson in 2013

Our half cycle investment go‐forward generates strong returns for our shareholders By 2020, Velvet approaches 50/50 liquids/gas and generates higher cash on cash returns in the

backdrop of a challenging AECO market and US$50/bbl WTI oil market

2014

2012

20132016

2019E

2018E2015

2017E

~US$100/bbl oil price environment

CFROI = (CF + Financing Expense) / Average (TA – CL + Accum DD&A + E&E expense)Velvet 3‐year plan assumes December 4, 2017 BoD meeting

Shale sets marginalcost of productionHedging program

sustained returns

Converting Gold Creekland into PDP

Discovered liquids‐rich

EllerslieFirst oil at Gold Creek

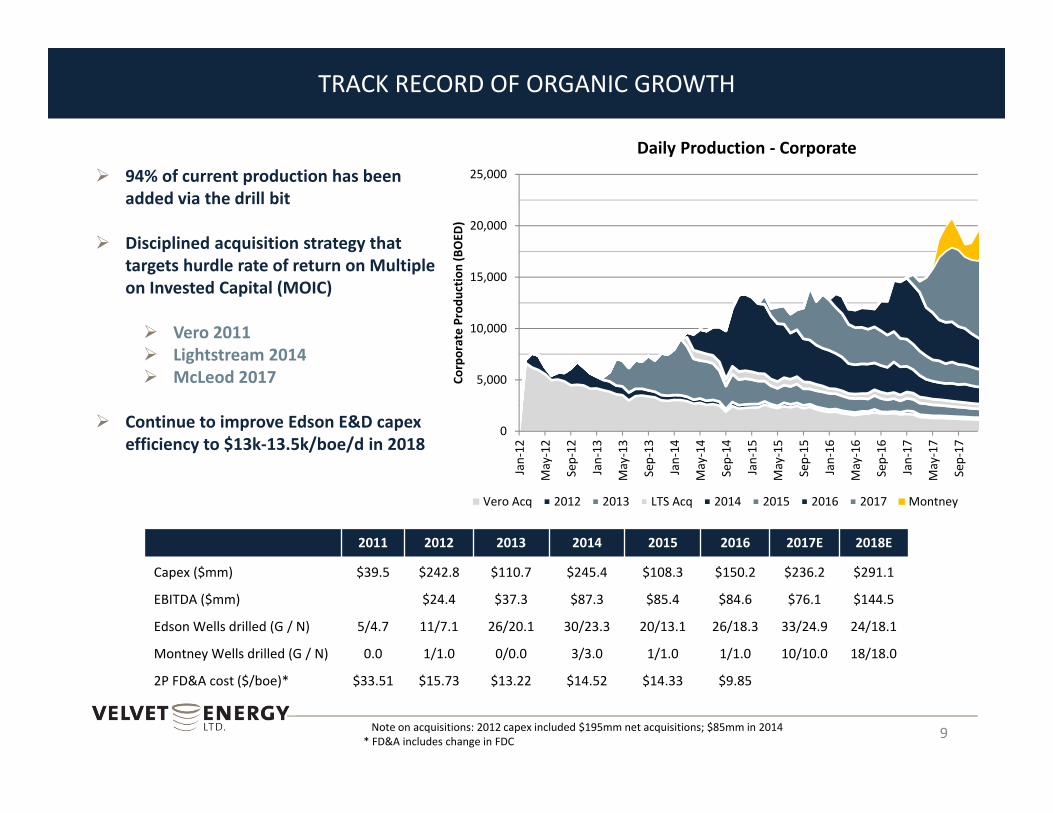

TRACK RECORD OF ORGANIC GROWTH

9

94% of current production has been added via the drill bit

Disciplined acquisition strategy that targets hurdle rate of return on Multiple on Invested Capital (MOIC)

Vero 2011 Lightstream 2014 McLeod 2017

Continue to improve Edson E&D capex efficiency to $13k‐13.5k/boe/d in 2018

Daily Production ‐ Corporate

2011 2012 2013 2014 2015 2016 2017E 2018E

Capex ($mm) $39.5 $242.8 $110.7 $245.4 $108.3 $150.2 $236.2 $291.1

EBITDA ($mm) $24.4 $37.3 $87.3 $85.4 $84.6 $76.1 $144.5

Edson Wells drilled (G / N) 5/4.7 11/7.1 26/20.1 30/23.3 20/13.1 26/18.3 33/24.9 24/18.1

Montney Wells drilled (G / N) 0.0 1/1.0 0/0.0 3/3.0 1/1.0 1/1.0 10/10.0 18/18.0

2P FD&A cost ($/boe)* $33.51 $15.73 $13.22 $14.52 $14.33 $9.85

Note on acquisitions: 2012 capex included $195mm net acquisitions; $85mm in 2014* FD&A includes change in FDC

0

5,000

10,000

15,000

20,000

25,000

Jan‐12

May‐12

Sep‐12

Jan‐13

May‐13

Sep‐13

Jan‐14

May‐14

Sep‐14

Jan‐15

May‐15

Sep‐15

Jan‐16

May‐16

Sep‐16

Jan‐17

May‐17

Sep‐17

Corporate Prod

uctio

n (BOED

)

Vero Acq 2012 2013 LTS Acq 2014 2015 2016 2017 Montney

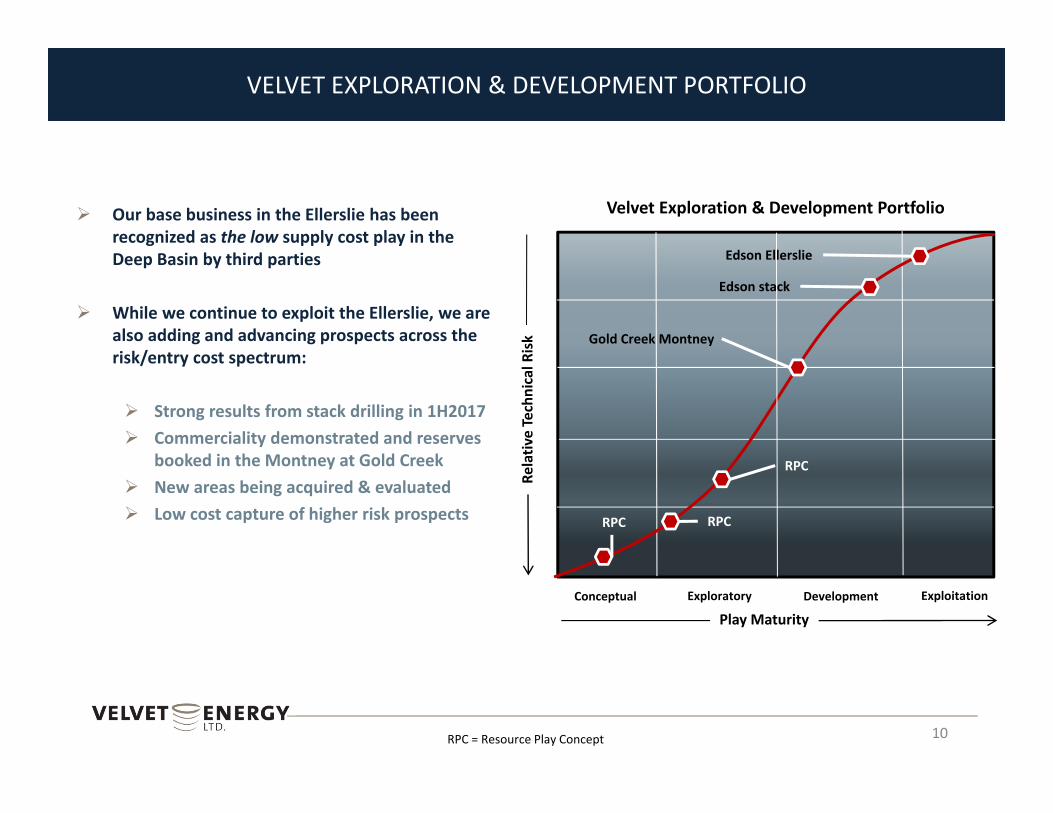

VELVET EXPLORATION & DEVELOPMENT PORTFOLIO

Our base business in the Ellerslie has been recognized as the low supply cost play in the Deep Basin by third parties

While we continue to exploit the Ellerslie, we are also adding and advancing prospects across the risk/entry cost spectrum:

Strong results from stack drilling in 1H2017 Commerciality demonstrated and reserves

booked in the Montney at Gold Creek New areas being acquired & evaluated Low cost capture of higher risk prospects

10

Velvet Exploration & Development Portfolio

Conceptual Exploratory Development Exploitation

Play Maturity

Edson Ellerslie

Relativ

e Technical R

isk Gold Creek Montney

RPC

RPC

RPC

RPC = Resource Play Concept

Edson stack

Gold Creek Montney ‐Unlocking the Light Oil Window

11

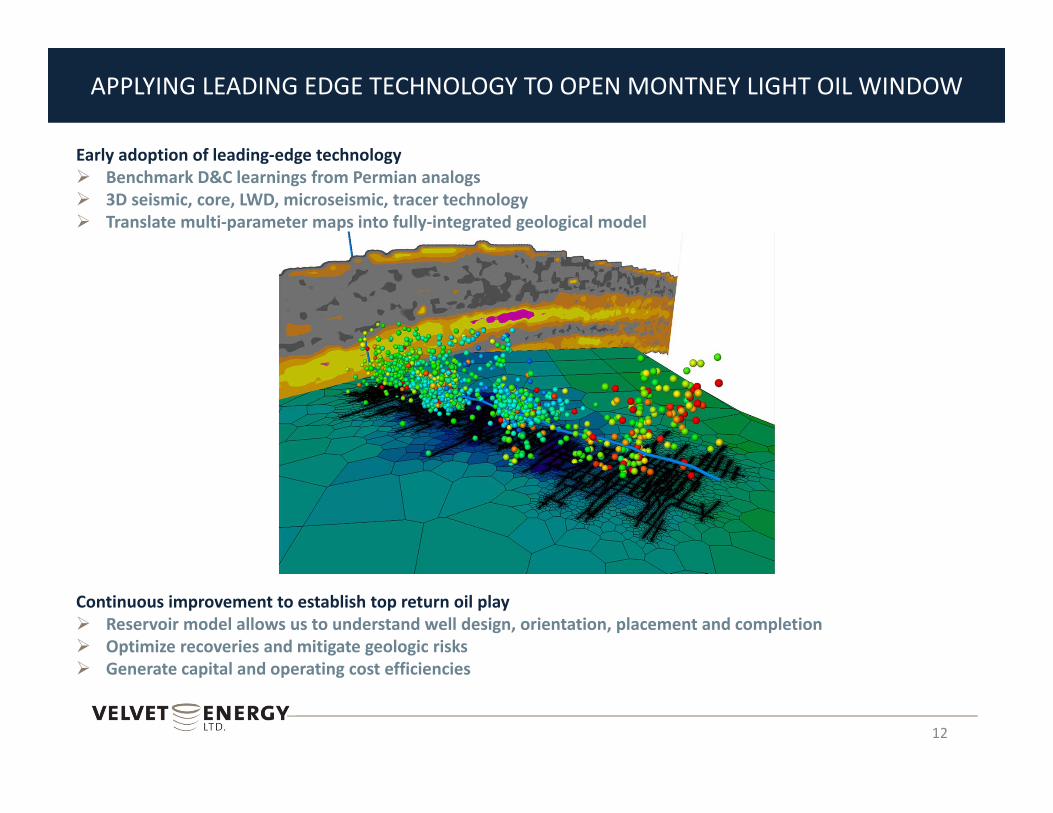

APPLYING LEADING EDGE TECHNOLOGY TO OPEN MONTNEY LIGHT OIL WINDOW

12

Early adoption of leading‐edge technology Benchmark D&C learnings from Permian analogs 3D seismic, core, LWD, microseismic, tracer technology Translate multi‐parameter maps into fully‐integrated geological model

Continuous improvement to establish top return oil play Reservoir model allows us to understand well design, orientation, placement and completion Optimize recoveries and mitigate geologic risks Generate capital and operating cost efficiencies

VELVET

INCEPTION

IRON BRIDGE

HAMMERHEAD

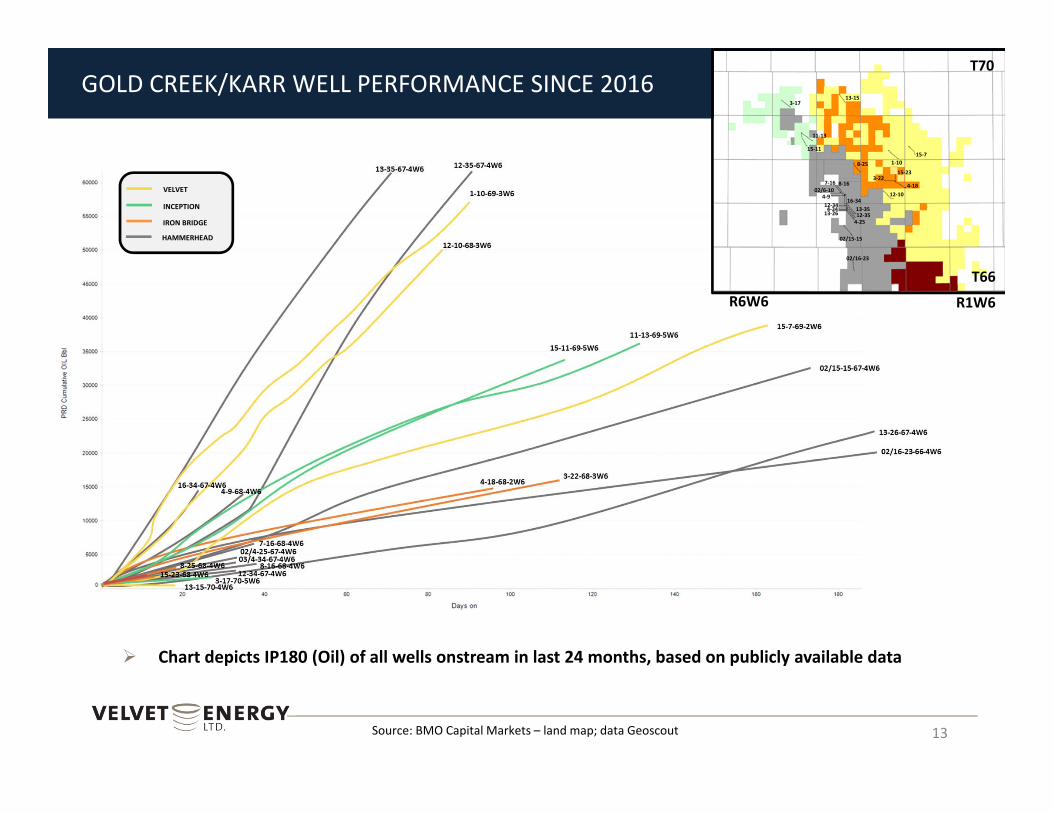

GOLD CREEK/KARR WELL PERFORMANCE SINCE 2016

Chart depicts IP180 (Oil) of all wells onstream in last 24 months, based on publicly available data

13

02/15‐15

12‐10

15‐71‐10

13‐15

11‐13

15‐11

3‐17

8‐25

4‐183‐22

8‐167‐16

4‐9

13‐26

15‐23

02/16‐23

02/6‐10

12‐344‐34 13‐35

12‐354‐25

16‐34

T66

T70

R1W6R6W6

Source: BMO Capital Markets – land map; data Geoscout

MONTNEY LIGHT OIL WINDOW AT GOLD CREEK

14

First production from three wells in June 2017

Drilled and completed four well pad in fall 2017 (photo below)

18 gross / net wells planned in 2018

11‐2 Pad Completion, October 2017

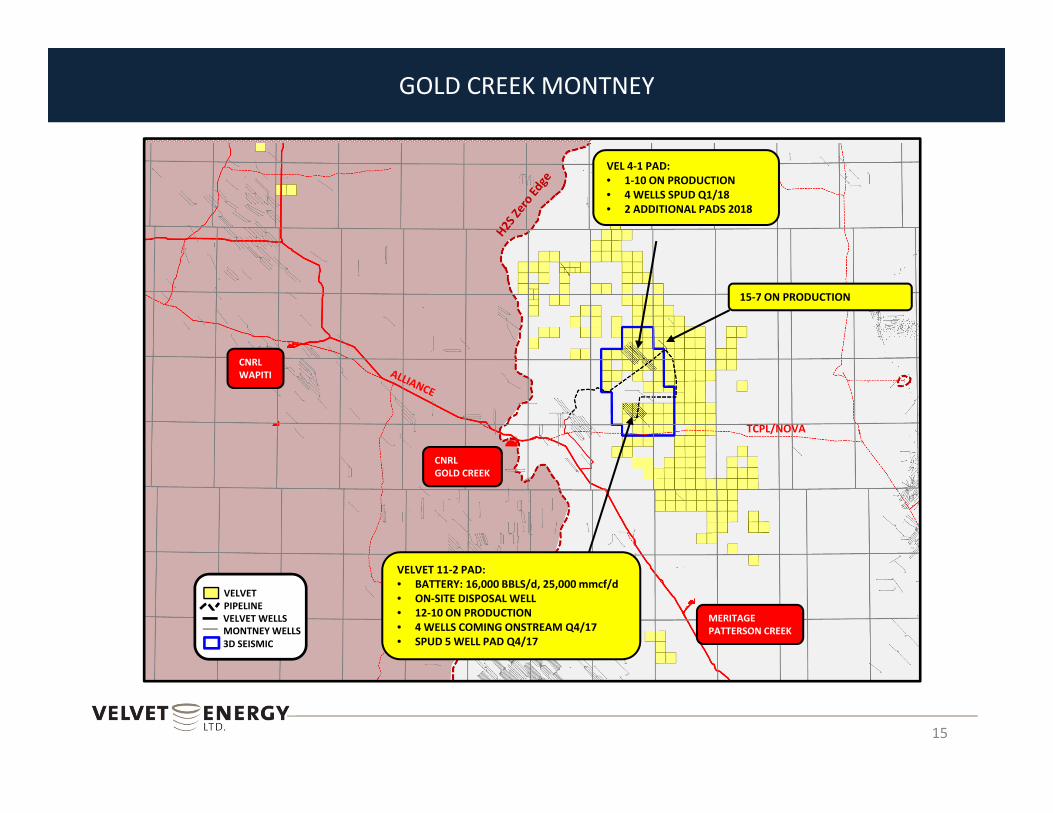

GOLD CREEK MONTNEY

15

TCPL/NOVA

MERITAGEPATTERSON CREEK

VELVET 11‐2 PAD:• BATTERY: 16,000 BBLS/d, 25,000 mmcf/d• ON‐SITE DISPOSAL WELL• 12‐10 ON PRODUCTION• 4 WELLS COMING ONSTREAM Q4/17• SPUD 5 WELL PAD Q4/17

VEL 4‐1 PAD:• 1‐10 ON PRODUCTION• 4 WELLS SPUD Q1/18• 2 ADDITIONAL PADS 2018

15‐7 ON PRODUCTION

CNRL GOLD CREEK

CNRL WAPITI

VELVET

3D SEISMIC

PIPELINEVELVET WELLSMONTNEY WELLS

Edson Ellerslie Hybrid Resource Play –Transitioning our High Return Base Business to FCF Generator

16

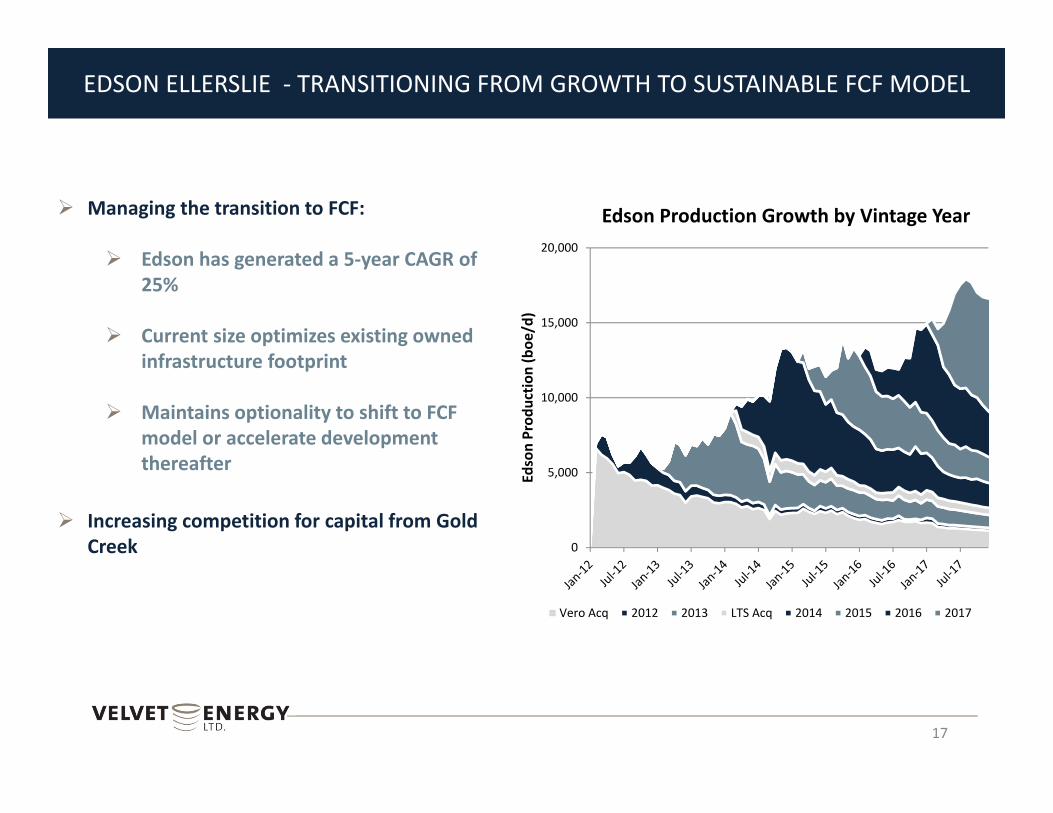

EDSON ELLERSLIE ‐ TRANSITIONING FROM GROWTH TO SUSTAINABLE FCF MODEL

17

Managing the transition to FCF:

Edson has generated a 5‐year CAGR of 25%

Current size optimizes existing owned infrastructure footprint

Maintains optionality to shift to FCF model or accelerate development thereafter

Increasing competition for capital from Gold Creek

Edson Production Growth by Vintage Year

0

5,000

10,000

15,000

20,000

Edson Prod

uctio

n (boe

/d)

Vero Acq 2012 2013 LTS Acq 2014 2015 2016 2017

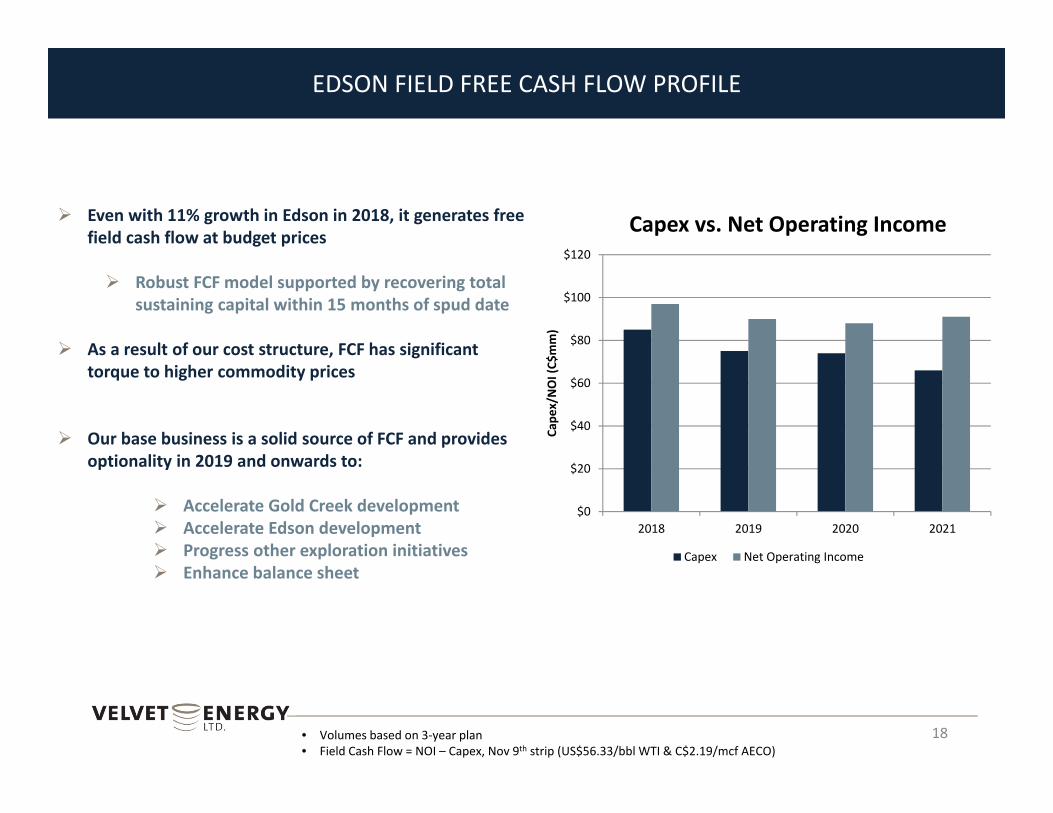

EDSON FIELD FREE CASH FLOW PROFILE

18

Even with 11% growth in Edson in 2018, it generates free field cash flow at budget prices

Robust FCF model supported by recovering total sustaining capital within 15 months of spud date

As a result of our cost structure, FCF has significant torque to higher commodity prices

Our base business is a solid source of FCF and provides optionality in 2019 and onwards to:

Accelerate Gold Creek development Accelerate Edson development Progress other exploration initiatives Enhance balance sheet

• Volumes based on 3‐year plan• Field Cash Flow = NOI – Capex, Nov 9th strip (US$56.33/bbl WTI & C$2.19/mcf AECO)

$0

$20

$40

$60

$80

$100

$120

2018 2019 2020 2021

Cape

x/NOI (C$

mm)

Capex vs. Net Operating Income

Capex Net Operating Income

0.0%

25.0%

50.0%

75.0%

100.0%

125.0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

% of D

CET Ca

pital R

ecovered

Time from Spud (months)

$3,150

$3,370

$2,366

$142 $861

$‐

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

DCET Revenue Royalties OperatingCosts

Year 1 NetOperatingIncome

C$mm

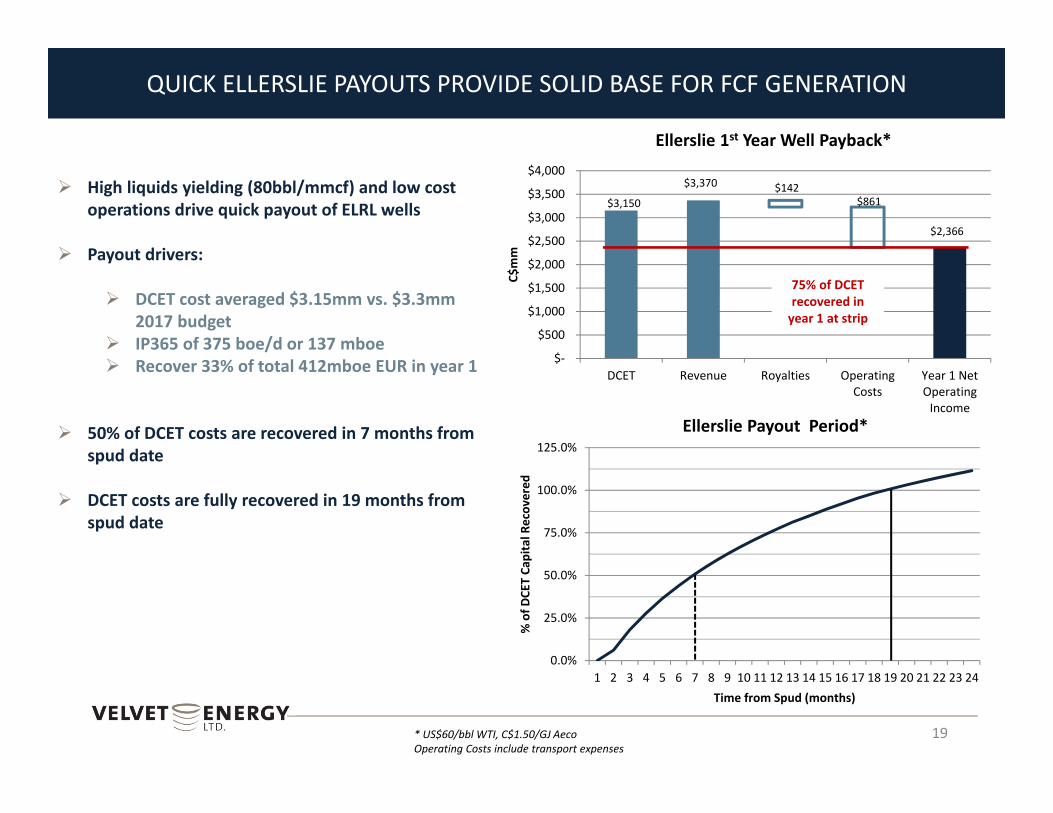

QUICK ELLERSLIE PAYOUTS PROVIDE SOLID BASE FOR FCF GENERATION

19

High liquids yielding (80bbl/mmcf) and low cost operations drive quick payout of ELRL wells

Payout drivers:

DCET cost averaged $3.15mm vs. $3.3mm 2017 budget

IP365 of 375 boe/d or 137 mboe Recover 33% of total 412mboe EUR in year 1

50% of DCET costs are recovered in 7 months from spud date

DCET costs are fully recovered in 19 months from spud date

Ellerslie 1st Year Well Payback*

* US$60/bbl WTI, C$1.50/GJ AecoOperating Costs include transport expenses

Ellerslie Payout Period*

75% of DCET recovered in year 1 at strip

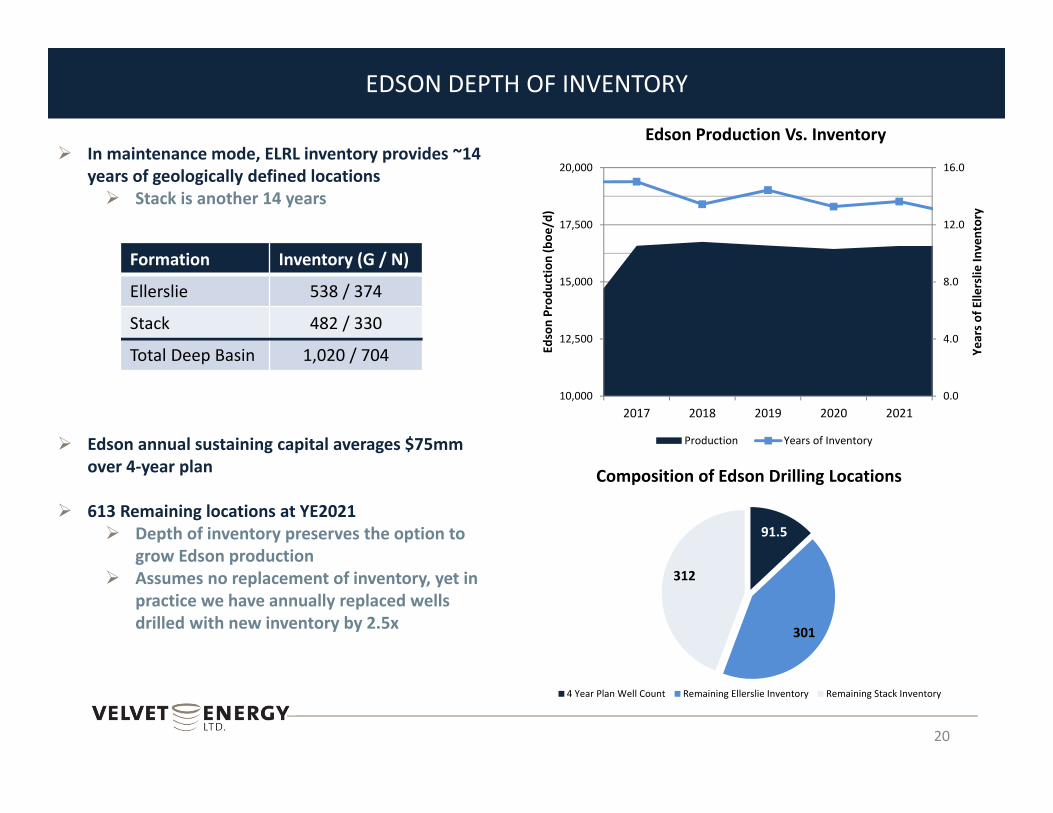

EDSON DEPTH OF INVENTORY

20

In maintenance mode, ELRL inventory provides ~14 years of geologically defined locations Stack is another 14 years

Edson annual sustaining capital averages $75mm over 4‐year plan

613 Remaining locations at YE2021 Depth of inventory preserves the option to

grow Edson production Assumes no replacement of inventory, yet in

practice we have annually replaced wells drilled with new inventory by 2.5x

Formation Inventory (G / N)

Ellerslie 538 / 374

Stack 482 / 330

Total Deep Basin 1,020 / 704

Edson Production Vs. Inventory

91.5

301

312

4 Year Plan Well Count Remaining Ellerslie Inventory Remaining Stack Inventory

0.0

4.0

8.0

12.0

16.0

10,000

12,500

15,000

17,500

20,000

2017 2018 2019 2020 2021

Years o

f Ellerslie

Inventory

Edson Prod

uctio

n (boe

/d)

Production Years of Inventory

Composition of Edson Drilling Locations

Corporate highlights

21

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

‐

5.00

10.00

15.00

20.00

25.00

PEY

AAV

TOU

PONY

BIR

BNP

SRX CR VEL

ARX

PNE

ERF

IKM VII

TVE

RMP

TVL

CQE

VET

WCP BTE

ATU

RRX

NVA LXE

KEL

BNE

POU

JOY

TOG

DEE

CPG

SGY

OBE GXE

MQX

SPE CJ

Liqu

ids W

eight (%)

2018

E Ope

x + Tp

ort ($/bo

e)

Opex + Tport ($/boe) Liquids (%)

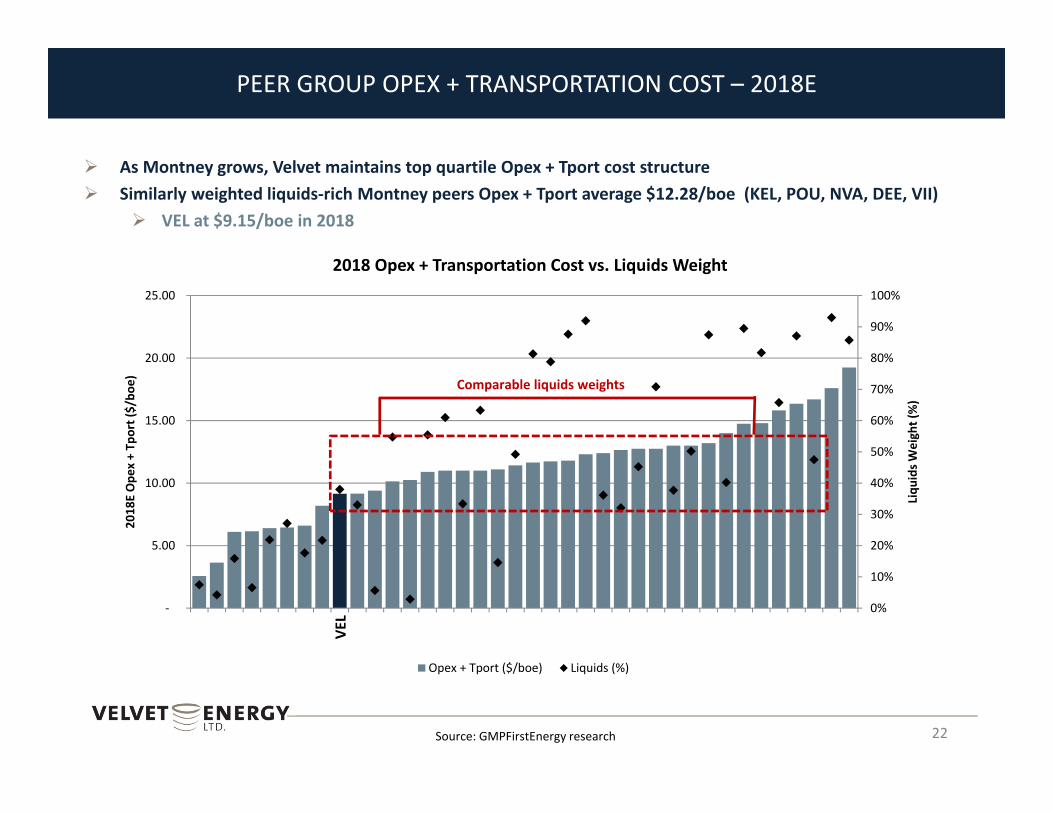

PEER GROUP OPEX + TRANSPORTATION COST – 2018E

As Montney grows, Velvet maintains top quartile Opex + Tport cost structure Similarly weighted liquids‐rich Montney peers Opex + Tport average $12.28/boe (KEL, POU, NVA, DEE, VII)

VEL at $9.15/boe in 2018

22

2018 Opex + Transportation Cost vs. Liquids Weight

Source: GMPFirstEnergy research

Comparable liquids weights

VEL

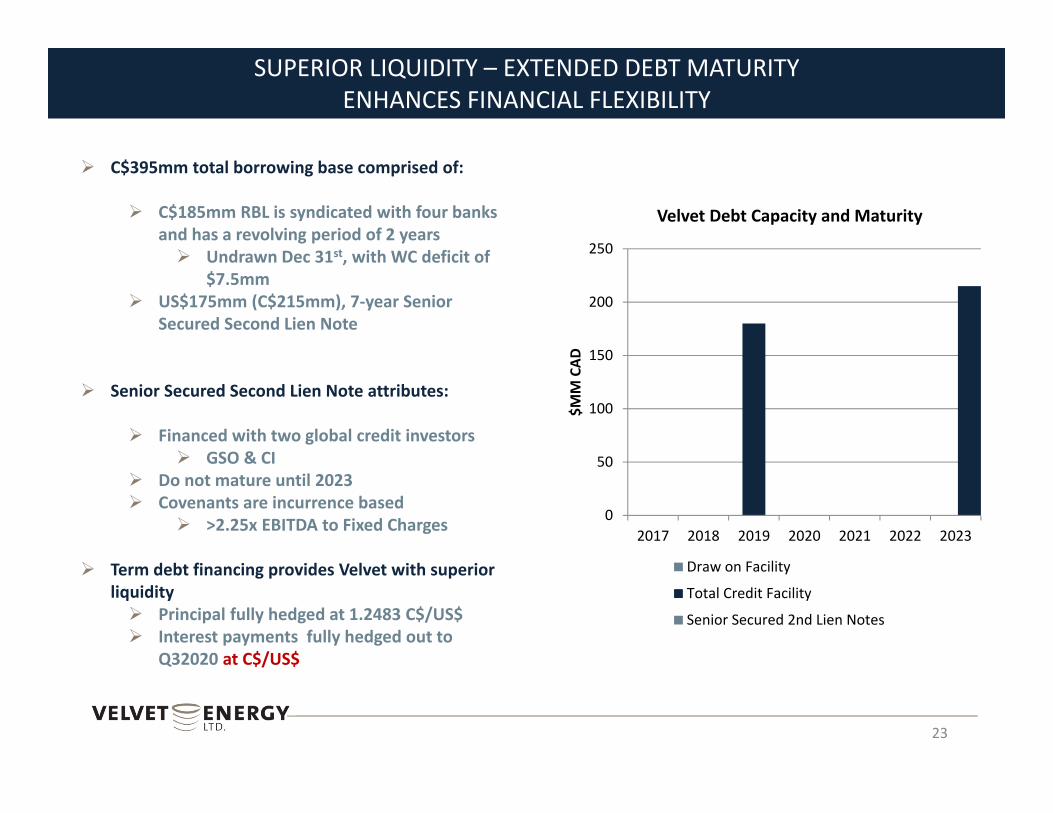

SUPERIOR LIQUIDITY – EXTENDED DEBT MATURITY ENHANCES FINANCIAL FLEXIBILITY

23

C$395mm total borrowing base comprised of:

C$185mm RBL is syndicated with four banks and has a revolving period of 2 years Undrawn Dec 31st, with WC deficit of

$7.5mm US$175mm (C$215mm), 7‐year Senior

Secured Second Lien Note

Senior Secured Second Lien Note attributes:

Financed with two global credit investors GSO & CI

Do not mature until 2023 Covenants are incurrence based

>2.25x EBITDA to Fixed Charges

Term debt financing provides Velvet with superior liquidity Principal fully hedged at 1.2483 C$/US$ Interest payments fully hedged out to

Q32020 at C$/US$

Velvet Debt Capacity and Maturity

0

50

100

150

200

250

2017 2018 2019 2020 2021 2022 2023

$MM CAD

Draw on Facility

Total Credit Facility

Senior Secured 2nd Lien Notes

RISK MANAGEMENT OVERVIEW: POLICY AND MANDATE

24

HEDGING PHILOSOPHY AND MANDATE:

The financial risk management mandate is to enable the effective execution of business and financing activities in the interest of Velvet’s stakeholders and partners by managing an active hedging program to mitigate price risks that achieves the following objectives

1) Protecting value and returns Protect PDP lending value Support rate of return thresholds

2) Supporting the execution of the business Near term budgets and long‐term plans Execution of top tier profitable growth Acquisitions and development commitments

3) Protect against adverse price movements and constraints Be adaptive to changing business and market conditions Diversify exposure in the interest of reducing risk

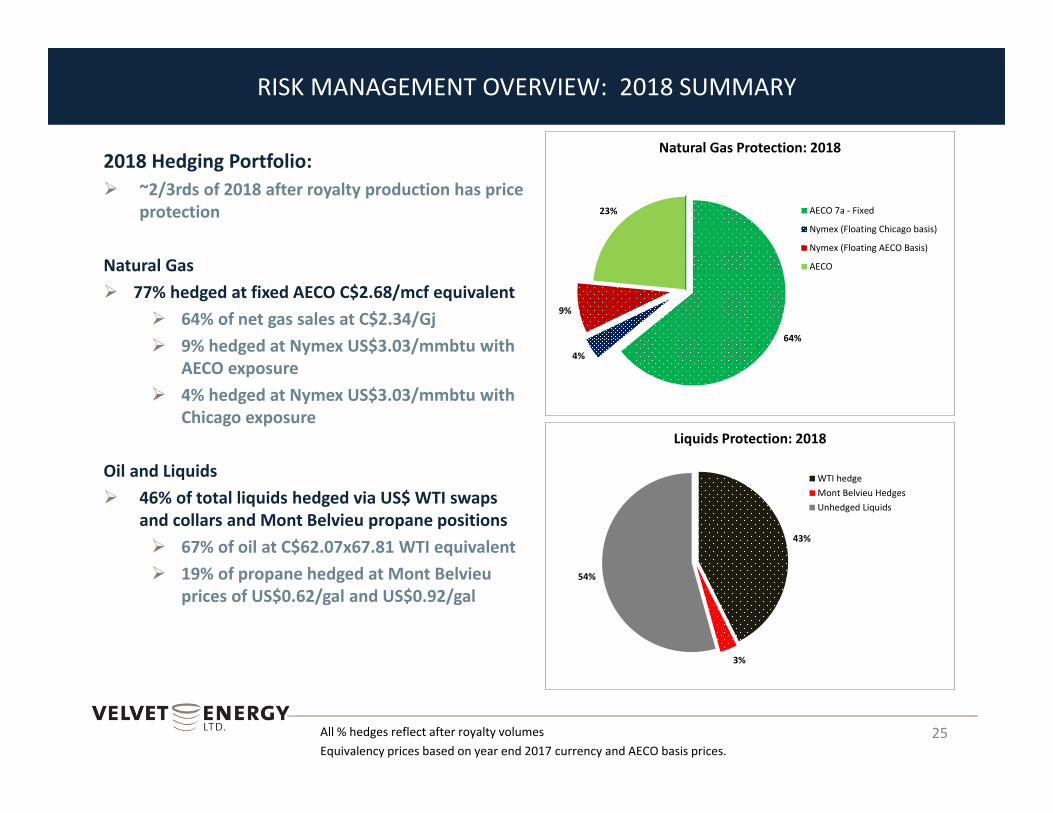

RISK MANAGEMENT OVERVIEW: 2018 SUMMARY

25All % hedges reflect after royalty volumesEquivalency prices based on year end 2017 currency and AECO basis prices.

64%

4%

9%

23%

Natural Gas Protection: 2018

AECO 7a ‐ Fixed

Nymex (Floating Chicago basis)

Nymex (Floating AECO Basis)

AECO

43%

3%

54%

Liquids Protection: 2018

WTI hedgeMont Belvieu HedgesUnhedged Liquids

2018 Hedging Portfolio: ~2/3rds of 2018 after royalty production has price

protection

Natural Gas 77% hedged at fixed AECO C$2.68/mcf equivalent

64% of net gas sales at C$2.34/Gj 9% hedged at Nymex US$3.03/mmbtu with

AECO exposure 4% hedged at Nymex US$3.03/mmbtu with

Chicago exposure

Oil and Liquids 46% of total liquids hedged via US$ WTI swaps

and collars and Mont Belvieu propane positions 67% of oil at C$62.07x67.81 WTI equivalent 19% of propane hedged at Mont Belvieu

prices of US$0.62/gal and US$0.92/gal

CORPORATE INFORMATION

26

AuditorsPricewaterhouseCoopers, LLPReservoir EngineersGLJ Petroleum ConsultantsMcDaniel & Associates Consultants Ltd.BankersCanadian Imperial Bank of CommerceRoyal Bank of CanadaBank of MontrealThe Toronto‐Dominion BankSolicitorsBurnet, Duckworth & Palmer LLP

Velvet Energy Ltd.1500, 308 4th Avenue SWCalgary, AB T2P 0H7

P: 403.781.9125

Investor contacts:

Ken Woolner, President & CEO403.781.9134

Chris Theal, Chief Financial Officer403.781.9162

www.velvetenergy.ca

![AkzoNobel Dulux Velvet Touch Emulsion€¦ · Dulux Dulux Dulux h Velvet TOUCh Velvet Touch DIAMOND PLATINUM GLO FINISH PEARL GLO FIN] NEW& IMPROVED rÅkZON0bel Dulux Velvet Touch](https://static.cupdf.com/doc/110x72/61481ebecee6357ef92525b0/akzonobel-dulux-velvet-touch-emulsion-dulux-dulux-dulux-h-velvet-touch-velvet-touch.jpg)

![AkzoNobel Dulux Velvet Touch Emulsion… · PEARL GLO FIN] NEW& IMPROVED rÅkZON0bel Dulux Velvet Touch zoNobel DUIux Velvet PEARL GLO FINISH _ NEW&. IMPROVED Dulux Velvet Touch DIAMOND](https://static.cupdf.com/doc/110x72/60a4cc2c64ba681d2238fa1f/akzonobel-dulux-velvet-touch-emulsion-pearl-glo-fin-new-improved-rkzon0bel.jpg)