Information | Analytics | Expertise

© 2014 IHS / ALL RIGHTS RESERVED

INTERNATIONAL LPG MARKETS AND LPG PRICING OUTLOOKGLP Forum MexicoHacienda GalindoQueretaro, Mexico

OCTOBER 2, 2014

Walter M. Hart, Ph.D, P.E., Senior Director+1 832 209 [email protected]

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 2

Agenda

World Supply

World Demand

World Trade

Prices

© 2014 IHS

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

3

Global LPG production is growing most rapidly in the US, the Middle East and in Asia

2000

2003

2006

2009

2012

2015

2018

0

50000

100000

150000

200000

250000

300000

350000

0.0

1,624,383.0

3,248,766.0

4,873,149.0

6,497,532.0

8,121,915.0

9,746,298.0

11,370,681.0

Global LPG Production by Region

Europe/CISLatin AmericaAfricaAsia/PacificMiddle EastNorth AmericaM

illi

on

Bar

rels

Per

Day

© 2014 IHS 4

LPG production from the Middle East has some uncertainty

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

10000

20000

30000

40000

50000

60000

70000

0.0

324,876.0

649,752.0

974,628.0

1,299,504.0

1,624,380.0

1,949,256.0

2,274,132.0

Middle East LPG Production by Country

OtherIraqIranUAEQatarSaudi ArabiaM

illi

on

Bar

rels

Per

Day

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 5

Asia LPG production will be driven by refinery additions in China

2000

2003

2006

2009

2012

2015

2018

0

10000

20000

30000

40000

50000

60000

70000

0.0

324,876.0

649,752.0

974,628.0

1,299,504.0

1,624,380.0

1,949,256.0

2,274,132.0

Asia LPG Production

Indian SubcontinentSoutheast AsiaNortheast Asia

Mil

lio

n B

arre

ls P

er D

ay

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 6

The US / Canada LPG production increase is driven by shale-sourced gas processing

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

-0.2

0.3

0.8

1.3

1.8

2.3

2.8

3.3

US/Canada LPG Production

SecAxisGas ProcessingRefining/ Upgrading

Mil

lio

n B

arre

ls p

er D

ay

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 7

Latin America has some promising developments to increase LPG production

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

5000

10000

15000

20000

25000

30000

0.0

324,876.0

649,752.0

974,628.0

Latin America LPG Production by Country

OtherVenezuelaPeruMexicoBrazilArgentina

Mil

lio

n B

arre

ls P

er D

ay

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 8

Agenda

World Supply

World Demand

World Trade

Prices

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 9

Global LPG demand growth will continue to be driven by Asia and the Middle East

0

50000

100000

150000

200000

250000

300000

350000

0.0

1,624,383.0

3,248,766.0

4,873,149.0

6,497,532.0

8,121,915.0

9,746,298.0

11,370,681.0

Global LPG Demand by Region

Europe/CIS

North America

Latin America

Africa

Middle East

Asia/Pacific

Mill

ion

Bar

rels

Pe

r D

ay

Asia/Pacific

Middle East

Africa

Latin America

North America

Europe/CIS

World

0.0% 5.0% 10.0%

LPG Demand Growth (CAGR)

2010-20202000-2010

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 10

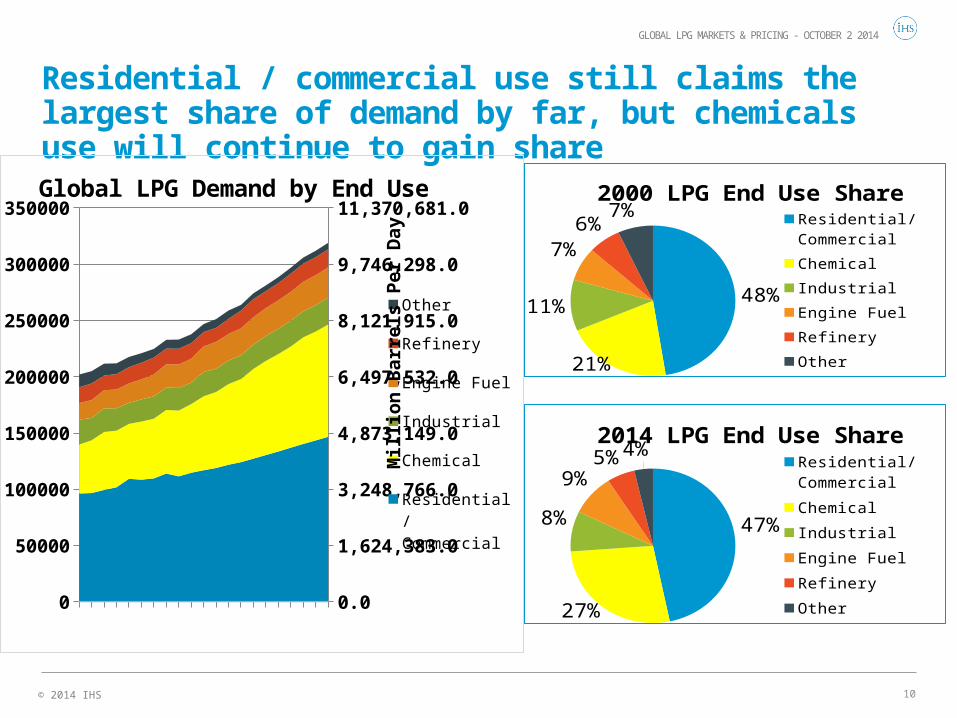

Residential / commercial use still claims the largest share of demand by far, but chemicals use will continue to gain share

0

50000

100000

150000

200000

250000

300000

350000

0.0

1,624,383.0

3,248,766.0

4,873,149.0

6,497,532.0

8,121,915.0

9,746,298.0

11,370,681.0Global LPG Demand by End Use

Other

Refinery

Engine Fuel

Industrial

Chemical

Residential/ Commercial

Mill

ion

Ba

rre

ls P

er

Da

y

47%

27%

8%

9%5% 4%2014 LPG End Use Share

Residential/ Commercial

Chemical

Industrial

Engine Fuel

Refinery

Other

48%

21%

11%

7%6%

7%2000 LPG End Use Share

Residential/ Commercial

Chemical

Industrial

Engine Fuel

Refinery

Other

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 11

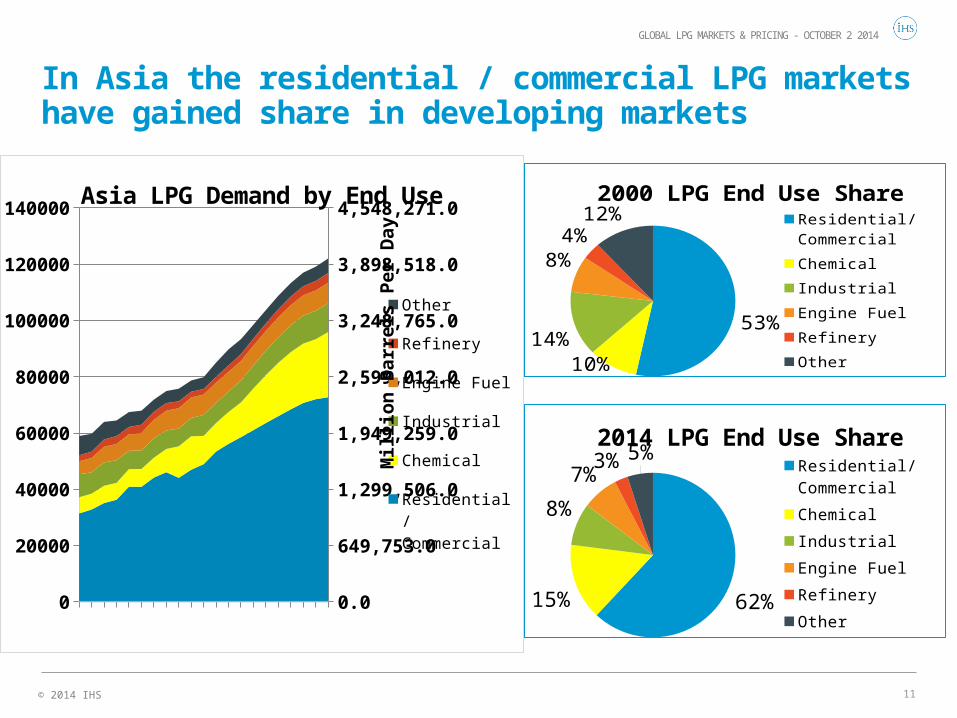

In Asia the residential / commercial LPG markets have gained share in developing markets

0

20000

40000

60000

80000

100000

120000

140000

0.0

649,753.0

1,299,506.0

1,949,259.0

2,599,012.0

3,248,765.0

3,898,518.0

4,548,271.0Asia LPG Demand by End Use

Other

Refinery

Engine Fuel

Industrial

Chemical

Residential/ Commercial

Mill

ion

Ba

rre

ls P

er

Da

y

62%15%

8%

7%3% 5%2014 LPG End Use Share

Residential/ Commercial

Chemical

Industrial

Engine Fuel

Refinery

Other

53%

10%

14%

8%4%

12%2000 LPG End Use Share

Residential/ Commercial

Chemical

Industrial

Engine Fuel

Refinery

Other

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 12

In the Middle East the impressive growth in residential / commercial LPG markets is eclipsed by dramatic petrochemical feedstocks market growth

0

10000

20000

30000

40000

0.0

324,876.0

649,752.0

974,628.0

1,299,504.0

Middle East LPG Demand by End Use

Refinery/ Indus-trial

Engine Fuel

Chemical

Residential/ Commercial

Mill

ion

Ba

rre

ls P

er

Da

y57%

38%

3% 3%2000 LPG End Use Share

Residential/ Commercial

Chemical

Engine Fuel

Refinery/ Industrial

35%

63%

1% 1%2014 LPG End Use Share

Residential/ Commercial

Chemical

Engine Fuel

Refinery/ Industrial

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 13

Residential / Commercial LPG demand is declining in the US/ Canada - LPG demand growth will be driven by USGC PDH units

0

10000

20000

30000

40000

50000

60000

70000

80000

0.0

500,000.0

1,000,000.0

1,500,000.0

2,000,000.0

2,500,000.0

North America LPG Demand by End Use

Other

Refinery

Chemical

Residential/ Commercial

Mill

ion

Ba

rre

ls P

er

Da

y 26%

40%

14%

20%

2000 LPG End Use Share

Residential/ Commercial

Chemical

Refinery

Other

21%

44%

18%

17%

2014 LPG End Use Share

Residential/ Commercial

Chemical

Refinery

Other

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 14

US domestic propane demand is not increasing except for the PDH units, so surplus propane must be exported

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

US Propane demand

Res/Com Base Chemical-Ethylene Price Sensitive Chemical

Chemical-Ref. Propylene Chemical-PDH Industrial

Farm Other Exports

Th

ou

san

d

bar

rels

per

day

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 15

Increased gas-sourced isobutane production will reduce the demand for isomerization; increased exports will be needed

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0

100

200

300

400

500

600US isobutane demand

Refining Chemicals Other Exports

Th

ou

sa

nd

ba

rre

ls p

er

da

y2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

0

100

200

300

400

500

600US normal butane demand

Refining IsomerizationChemical-Base Demand Price Sensitive ChemicalIndustrial OtherExports

Th

ou

sa

nd

ba

rre

ls p

er

da

yGLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 16

The Latin America LPG demand growth rate is limited because the dominant end use is residential / commercial

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

5000

10000

15000

20000

25000

30000

35000

40000

0.0

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

Latin America LPG Demand by Country

OtherVenezuelaPeruMexicoBrazilArgentinaM

illi

on

Bar

rels

Per

Day

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 17

Agenda

World Supply

World Demand

World Trade

Prices

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 18

The United States now rivals the world’s largest LPG exporters

2005 2009 2011 2013 2014 Ann.

0

20,000,000

40,000,000

60,000,000

80,000,000

0.0

500,000.0

1,000,000.0

1,500,000.0

2,000,000.0

2,500,000.0

Selected Waterborne LPG Exports

Second AxisAustraliaNigeriaKuwaitAlgeriaNorth SeaUnited StatesQatarUAESaudi Arabia

Source: IHS Energy - Waterborne

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 19

The US will be the world’s largest LPG exporter

0

10000

20000

30000

40000

50000

60000

70000

80000

0.0

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

1,400,000.0

1,600,000.0

1,800,000.0

Total LPG Exports by Selected Major Exporters

NigeriaAlgeriaNorth SeaUnited StatesQatarUAESaudi Arabia

Mil

lio

n B

arre

ls P

er D

ay

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 20

Most US LPG exports are going to Latin America, but the market is limited…

0.0

5000000.0

10000000.0

15000000.0

0

0.1

0.2

0.3

0.4

0.5

Destination of US LPG Exports

scndaxisOtherAsiaEuropeLatin AmericaM

illi

on

Bar

rels

per

Day

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

Source: IHS Energy - Waterborne

© 2014 IHS 21

Asia will have import growth in all sub-regions

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

-10000

0

10000

20000

30000

40000

50000

60000

-324,876.0

0.0

324,876.0

649,752.0

974,628.0

1,299,504.0

1,624,380.0

1,949,256.0Asia Net LPG Imports by Subregion

Indian SubcontinentNortheast AsiaSoutheast Asia

Mil

lio

n B

arre

ls P

er D

ay

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 22

Agenda

World Supply

World Demand

World Trade

Prices

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS

A glut of US ethane has ethane prices following natural gas, but the other US NGLs are still tracking refined products

0

5

10

15

20

25

30Henry Hub Natural Gas

Ethane

Propane

Normal Butane

Natural Gasoline

N o m i n a l d o l l a r s p e r M M B t u

USGC (Mont Belvieu) NGL natural gas prices

© 2014 IHSSource: IHS

23

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 24

Since about 2012, the last significant increment of US LPG exports has been moving to Asia

0.0

5000000.0

10000000.0

15000000.0

0

0.1

0.2

0.3

0.4

0.5

Destination of US LPG Exports

scndaxisOtherAsiaEuropeLatin AmericaM

illi

on

Bar

rels

per

Day

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

Source: IHS Energy - Waterborne

© 2014 IHS

WORLD LPG MARKET OVERVIEW/ MARCH 2014

25

LPG competes with refined products in the Asian markets

1995 2000 2005 2010 2015 2020 20250

2

4

6

8

10

12

14

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Propane to Dubai Crude OilPropane to Naphtha Ratio in Japan

$/t

on

pro

pa

ne

pe

r $

/Bb

l c

rud

e o

il

$/t

on

pro

pa

ne

pe

r $

/to

n o

f n

ap

hth

a

Weakening trend pre-recession

Volatile but flatter post-recession

Forecast

© 2014 IHS

The arbitrage between Asia and the United States must remain large enough to clear the US LPG markets

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

-600

-400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800Belv - Japan DifferentialForecast DifferentialPropane, Mont BelvieuPropane, MB FcstSpot Propane, Japan

Price ($/metric ton)

Differential($/metric ton)

Propane

© 2014 IHSSource: IHS

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

0

100

200

300

400

500

600

700

800

900

1,000

1,100

-600

-400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

Belv - NWE Differen-tialDifferential FcstN-Butane, Mont BelvieuN-Butane, MB Fcst

Price ($/metric ton)

Differential($/metric ton)

Butane

© 2014 IHSSource: IHS

26

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS 27

Thank You!

Walter M. Hart, Ph.D., P.E.

Senior Director, NGL Research & Consulting

1 (832) 209-4424

GLOBAL LPG MARKETS & PRICING - OCTOBER 2 2014

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.

Americas: +1.800.IHS.CARE (+1.800.447.273); [email protected]

Europe, Middle East, and Africa: +44.(0).1344.328.300; [email protected]

Asia and the Pacific Rim: +604.291.3600; [email protected]

Contact us

![#CiveItUp LPG (LPG a) IOCL Cl / BPCL D / HPCL C] LPG àà àa … · · 2018-02-28iocl cl / bpcl d / hpcl c] lpg àà àa-r/àkft lpg àž lpg t:- lpg dgcc (poi) lpg 17 lpg id"](https://static.cupdf.com/doc/110x72/5ae5ebd07f8b9acc268cac07/civeitup-lpg-lpg-a-iocl-cl-bpcl-d-hpcl-c-lpg-a-cl-bpcl-d-hpcl-c.jpg)