Indian Media Scenario

December 2011

Content

India - In 2010

India at a glance

The Magnitude of Indian M&E Industry

Growth of the media industry

Growth of advertising revenue

India Outlook-Projection 2015

A closer look at

Television Media

Print Industry

Radio Industry

Internet Industry

Film Industry

Music Industry

OOH Industry

Data sources

Google.com

Census of India

The Economist

Telecom Regulatory Authority of India (TRAI)

Television Audience Measurement (TAM)

Price Water House Cooper (PWC Entertainment & Media Outlook)

Radio Audience Measurement (RAM)

ComScore Media Matrix

Indian Readership Survey (IRS)

Radio Establishment Survey

Indian Market Research Bureau (IMRB)

Central Intelligence Agency World Fact Book (CIA)

India – In 2010

India – a diverse country

More than 1 billion people

Urban: Rural ratio 31:69

29 States

7 Union Territories

22 Official Languages

More than 1600 local dialects

Key Parameters

Parameters Statistics

Population 1210.2 Million

Population Under 15 years of age 29.7%

Literacy Rate 74%

Exchange Rates 51.96 (Rs per US$)

No. of Households 241 Million

Average no. of people per household

5.0

Source: TRAI| The Economist| CIA World Fact Book | TAM | PWC

The Economic Construct

Source: Govt. of India | The Economist | CIA World Fact Book

Parameters Statistics

GDP $1.53 trillion

Origins of GDP % of total

Agriculture 18.5%

Industry 26.3%

Services 55.2%

Structure of Employment % of total

Agriculture 52%

Industry 14%

Services 34%

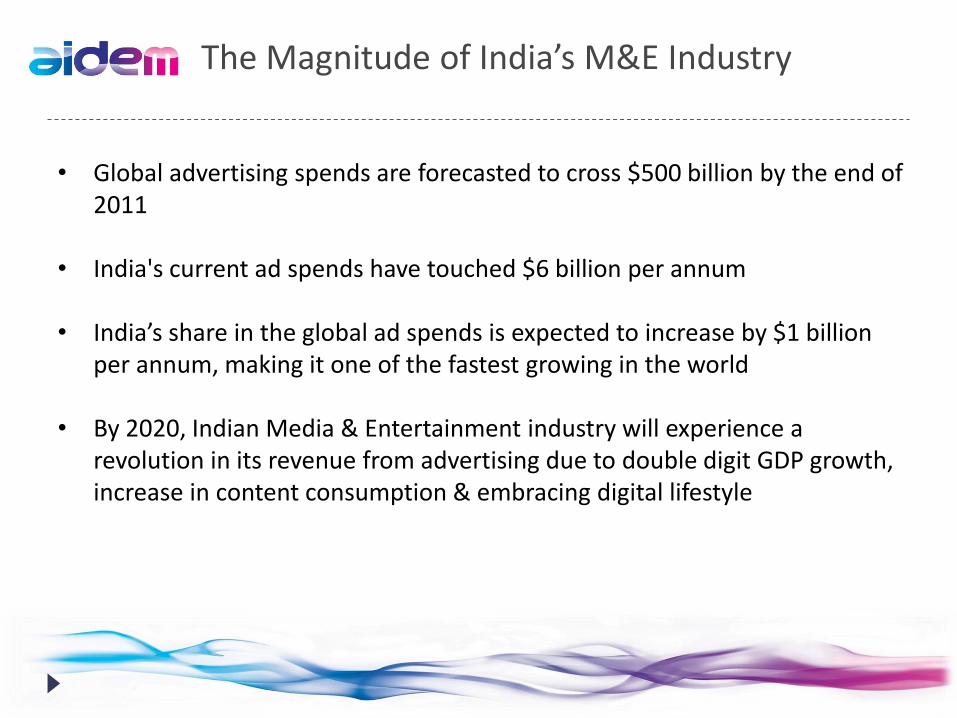

The Magnitude of India’s M&E Industry

• Global advertising spends are forecasted to cross $500 billion by the end of 2011

• India's current ad spends have touched $6 billion per annum

• India’s share in the global ad spends is expected to increase by $1 billion per annum, making it one of the fastest growing in the world

• By 2020, Indian Media & Entertainment industry will experience a revolution in its revenue from advertising due to double digit GDP growth, increase in content consumption & embracing digital lifestyle

Indian Media – Industry overview

2010 – The economy on track

Source: PWC | Industry Estimates

2010 saw the global economy begin to recover after the steep decline in 2009

In M&E sector, India recorded one of the highest growth in the world growing at 11.2% in 2010

The M&E industry in 2010 stood at INR 646 Bn. as compared to INR 580 Bn. in 2009

Two key industrial segments television & print have shown commendable growth

India – Growth of the Media Industry

Source: PWC | Industry Estimates

Growth of the Industry

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Television 192.2 223.9 244.7 265.5 306.5 12.5

% Change 17.1 9.3 8.5 15.4

Print 128.0 149.0 162.0 161.5 178.7 8.7

% Change 16.4 8.7 (0.3) 10.7

Film 84.5 96.0 107.0 95.0 87.5 0.9

% Change 13.6 11.5 (11.2) (7.9)

Radio 5.0 6.9 8.3 9.0 10.8 21.2

% Change 38.0 20.3 8.4 20.0

Internet 1.6 2.7 5.0 6.0 7.7 48.1

% Change 68.8 85.2 20.0 28.3

OOH 10.0 12.5 15.0 12.5 14.0 8.8

% Change 25.0 20.0 (16.7) 12.0

Animation Etc. 12.6 15.7 19.6 23.8 31.3 25.6

% Change 24.6 24.6 21.8 31.4

Music 7.3 7.6 6.9 7.5 9.5 6.8

% Change 3.3 (8.2) 8.5 25.7

Total 440.2 514.3 568.5 580.8 646.0 10.1

% Change 16.8 10.5 2.2 11.2

Television - Key Issues & trends

Source: PWC | Industry Estimates

• Growth in Ad revenues gives a boost to the television industry

• DTH platforms have given an impetus to the distribution levels

• Regional players have started focusing on Kids Channels

• With the IPL, four to five India series and some ICC tournaments taking place every year, Sports has become a significant genre

Trends

• Slow growth of digitization

• High cost of content production

• Low ARPUs to increase payback time

Issues

• The industry has shown a growth of 15.4% over 2009

• Digitization is emerging as a key success factor for the M&E industry

• Television advertising witnessed a double digit growth in 2010

Conclusion

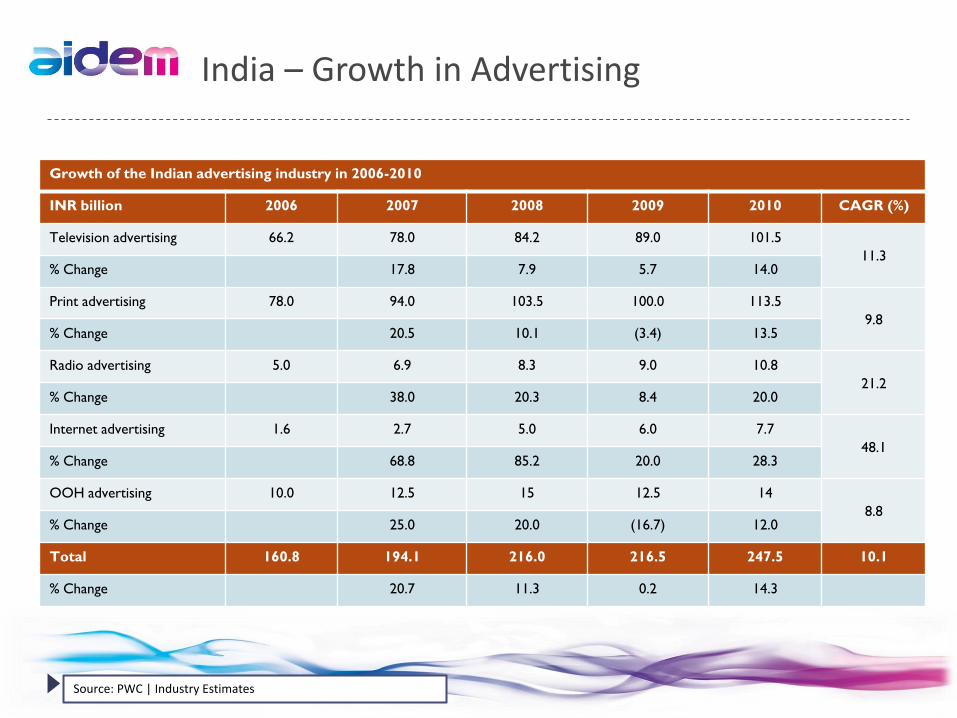

India – Growth in Advertising

Source: PWC | Industry Estimates

Growth of the Indian advertising industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Television advertising 66.2 78.0 84.2 89.0 101.5

11.3 % Change 17.8 7.9 5.7 14.0

Print advertising 78.0 94.0 103.5 100.0 113.5

9.8 % Change 20.5 10.1 (3.4) 13.5

Radio advertising 5.0 6.9 8.3 9.0 10.8

21.2 % Change 38.0 20.3 8.4 20.0

Internet advertising 1.6 2.7 5.0 6.0 7.7

48.1 % Change 68.8 85.2 20.0 28.3

OOH advertising 10.0 12.5 15 12.5 14

8.8 % Change 25.0 20.0 (16.7) 12.0

Total 160.8 194.1 216.0 216.5 247.5 10.1

% Change 20.7 11.3 0.2 14.3

2015: India Outlook

Source: PWC | Industry Estimates

• The India M&E industry is estimated to grow from INR 646 Bn. in 2010, at a CAGR of 13.2% for the next five years to reach INR 1199 Bn. in 2015

• The television industry is projected to continue to be the major contributor to the overall industry revenue pie & is estimated to grow at a healthy rate of 14.5% over the next five years

Television

• Indian print media is projected to grow by 9.6% over the period of 2010-15, reaching INR 282 Bn. in 2015 from present INR 178.7 Bn. in 2010

• The magazine industry is projected to grow at 5% approx. over the next five years

• The Indian film industry has had two consecutive bad years in 2009 & 2010 and shown considerable decline

• The industry depends heavily on big films and worthwhile content.

• Radio industry projected to show healthy growth at CAGR of 19.2% over 2010-15, reaching INR 26 Bn. in 2015 from the present INR 10.8 Bn. in 2010

Film & Radio

2015: India Outlook

Source: PWC | Industry Estimates

Projected growth of the Indian E&M industry in 2010-15

INR billion 2010 2011 2012 2013 2014 2015 CAGR (%)

Television 306.5 353.0 404.0 465.0 532.5 602.5 14.5

% Change 15.2 14.4 15.1 14.5 13.1

Print 178.7 196.2 214.4 235.6 256.5 282.0 9.6

% Change 9.8 9.3 9.9 8.9 9.9

Film 87.5 96.5 104.5 115.3 125.0 136.5 9.3

% Change 10.3 8.3 10.3 8.4 9.2

Radio 10.8 13.5 16.5 19.0 22.0 26.0 19.2

% Change 25.0 22.2 15.2 15.8 18.2

Internet 7.7 10.0 12.5 15.5 19.5 24.0 25.5

% Change 29.9 25.0 24.0 25.8 23.1

OOH 14.0 15.5 17.0 19.0 21.5 24.0 11.4

% Change 10.7 9.7 11.8 13.2 11.6

Animation Etc. 31.3 38.6 47.8 57.7 69.4 82.6 21.4

% Change 23.4 23.8 20.6 20.3 19.0

Music 9.5 11.9 13.9 16.1 18.4 21.4 17.6

% Change 25.0 17.5 15.6 14.2 16.0

Total 646.0 735.2 830.7 943.2 1064.8 1198.9 13.2

% Change 13.8 13.0 13.5 12.9 12.6

Television Industry - At a glance

Television Industry - Total Revenue

Source: PWC | Industry Estimates

Television market segmentation 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Television distribution 117.0 136.5 150.0 165.0 192.0 13.2

% Change 20.6 16.7 9.9 10.0 16.4

Television advertising 66.2 78.0 84.2 89.0 101.5 11.3

% Change 21.5 17.8 7.9 5.7 14.0

Television content 8.0 9.4 10.5 11.5 13 16.7

% Change 14.3 17.5 11.7 9.5 13.0

Total 191.2 223.9 244.7 265.5 306.5 12.5

• Television Distribution grew by 16.4 % this year aided by high growth of DTH industry & advances in digitization

• Sectors such as FMCG, telecom & financial services have led to growth in Television Advertising

• Revenues from Television content were driven by the rise in non-fiction shows & growth in regional markets

Television Industry - Distribution

Source: PWC | Industry Estimates

Television distribution market 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Television distribution 117.0 136.5 150.0 165.0 192.0 13.2

% Change 20.6 16.7 9.9 10.0 16.4

% of Total 61 61 61 62 63

• Distribution forms a large part of the television industry & contributes to about 63% of the television industry revenue

• The distribution industry revenues are a function of pay TV households & ARPU generated for each pay TV households

Television Industry - TV households

Source: TAM | PWC | Industry Estimates

Television households in India 2006-2010

Million 2006 2007 2008 2009 2010

Total households 190.0 195.5 197.0 207.0 213.0

% Change 7.0 3.0 3.0 5.0 3.0

TV households 112.0 115.0 118.0 124.0 130.0

% Change 7.0 3.0 3.0 5.0 5.0

% TV Penetration 59.0 59.0 60.0 60.0 61.0

• TV households in India increased at the rate of 5% since 2009 • The TV penetration in India still remains relatively low at 61% as compared to developed

countries like the US & UK where TV penetration is around 95% & 93% respectively • With the GDP rising, the number of TV owning households is expected to rise

Television Industry-Pay TV households in India

Source: PWC | Industry Estimates

Pay TV households in India 2006-2010

Million 2006 2007 2008 2009 2010

Cable TV households 68.0 70.0 71.0 72.0 74.0

% Change 11.0 3.0 1.0 1.0 2.8

DTH households 2.0 3.5 9.0 14.0 26.0

% Change 100.0 75.0 157.0 56.0 86.0

Total Pay TV households 70.0 73.5 80.0 86.0 100.0

% Change 13.0 5.0 9.0 8.0 16.0

• The no. of Pay TV owning households increased at the rate of 16% since 2009 • This growth was largely led by the increasing no. of DTH households

Television Industry-TV households ARPU in India

Source: PWC | Industry Estimates

TV household ARPU in India

INR 2006 2007 2008 2009 2010

Pay TV ARPU 139.0 155.0 156.0 160.0 160.0

% Change 6.9 11.5 1.0 3.0 0.0

• Pay TV ARPU owning households haven’t witnessed any growth over 2009

Television Industry - Advertising revenue

Source: PWC | Industry Estimates

Television advertising growth for 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

TV advertising 66.2 78.0 84.2 89.0 101.5 11.3

% Change 21.5 17.8 7.9 5.7 14.0

% of total TV industry 35 35 34 34 33

% of total advertising industry 41 40 39 41 41

• With a contribution of 41%, TV advertising accounts for the largest slice in the total advertising pie in India

• In 2010, the TV advertising registered a growth of 14% over 2009

Television Industry - Advertisers in 2010

Source: TAM Adex

Top sectors advertising on television

2009 % share 2010 % share

Toilet soaps 4 Toilet soaps 4

Cellular phone service 4 Cellular phone services 3

Social advertisements 3 Social advertisements 3

Aerated soft drinks 2 Shampoos 3

Shampoo 2 Cellular phones 2

DTH service provider 2 Aerated soft drinks 2

Two-wheelers 2 Toothpastes 2

Toothpastes 2 Corporate/brand image 2

Cars/jeeps 2 Fairness cream 2

Life insurance 2 DTH service providers 2

• The food & beverages sector’s contribution to TV advertising went up by 27% during 2010 • Coca Cola India Ltd was the top advertiser from the food & beverages sector • Personal care /hygiene saw a 55% rise in TV advertisement volume during 2010 as compared to 2009 • The personal care category was led by Toilet Soaps • HUL contributed the higher share among all advertisers of the personal care category

Television Industry - New brands in 2010

Source: TAM Adex

Top new brands on TV during 2010

Rank New brands

1 Colgate Total Clean Mint

2 Airtel 3G

3 Cadbury Perk Glucose

4 L’Oreal Total Repair 5

5 Nokia 5233

6 Knorr Soupy Noodles

7 Lux Purple Lotus & Cream

8 Sure Dry Shield Deodorants

9 Superia Lemon Fresh Soap

10 Minute Maid Nimbu Fresh

• The top three advertisers on TV i.e. HUL, Reckitt Benkiser Ltd & Cadbury India Ltd accounted for 13% of the overall advertisement share

Top 10 advertisers on TV on the basis of spend

Rank Advertisers

1 HUL

2 Reckitt Benkiser (India) Ltd

3 Cadbury India Ltd

4 ITC Ltd

5 Procter & Gamble

6 Coca Cola India Ltd

7 Colgate Palmolive Ltd

8 Ponds India

9 Glaxo Smithkline

10 L'Oreal's India Pvt. Ltd

Television Industry - TV Channels

Source: TAM

Total channels on television in 2010

Active Channels in 2010 New Channels in 2010 Total Channels in 2010

Regional 225 25 269

Hindi 88 2 104

English 65 11 76

Others 39 4 123

Total 417 42 572

• 42 new channels were introduced in 2010 • Regional channels’ genre witnessed the maximum increase in the number of new channels • There are in all more than 264 new TV channels licenses pending with the Ministry & with TRAI, this

number is bound to increase • Al Jazeera also got a nod from the Information & Broadcasting Ministry for its news channel

Television Industry - New TV channels in 2010

Source: TAM

New channels in 2010

Sr. No. Network Channel Name Category

1 Astro Group Food Food Food

2 Zee Khana Khazana Food

3 BIG-CBS Prime English GEC

4 BIG-CBS Spark Youth Channel

5 BIG-CBS Love Female Centric

6 FOX FX, FOX Crime, Nat Geo Music, Nat Geo Adventure, Nat Geo Wild, Nat Geo HD, Baby TV -

7 Discovery Discovery Science, Discovery Turbo -

8 Times Group Movies Now English Movies

• The year 2010 are witnessed for more fragmentation of TV genre, ZEEL launched first of its kind food channel Zee Khana Khazana

• ADAG group tied up with global media house CBS Studio & launched three new channels in the English GEC space

Television Industry - Viewership Share (%)

Source: TAM Adex

31.7

22.9

12

6.5 6

3.4 3.6 3.8 2.8

1.9 2.5 2.9

26.2

24.2

11.7

7.9

5.5 4 3.7 3.4 2.8 2.4

1.7

6.5

0

5

10

15

20

25

30

0

5

10

15

20

25

30

35

Hindi

GEC

Regional

GEC

Hindi

Movies

Cable Kids Regional

Movies

Regional

News

Hindi

News

Sports Regional

Music

Music Others

Vie

wers

hip

Shar

e (

%)

2009

Vie

wers

hip

Shar

e (

%)

2010

2010 2009

• Hindi GEC is the largest & only shown distinct viewership growth in 2010 as compared to period 2009 • Regional GEC which was running neck to neck Hindi GEC in 2009, has fallen behind in 2010 • Remaining all categories are showing more or less same performance in 2010

Television Industry - The Hindi GEC Space

Source: TAM, CS4+ YRS, All India 2010

Number of Weeks channel remained No.1

Channel Weeks 2010

Star Plus 42

Colors 10

• Entry of Colors in 2009 changed the game in the Hindi GEC space, especially impacted the top three players

• Innovative programming, differentiated content & well thought of distribution process made Colors strong contender in Hindi GEC space

• Star underwent rebranding exercise to connect with younger audience- “Rishta wahi, soch nayi” • Sony invested in newer & fresher content

Television - Top Rated TV programs in 2010

Source: TAM

Top rated TV programs in 2010

Sr. No. Show Channel Average Prime Time Rating (%)

1 Pavitra Rishta Zee TV 5.36

2 Yeh Rishta Kya Kehlata Hai Star Plus 5.00

3 Uttaran Colors 4.90

4 Bidayi Star Plus 4.55

5 Jhalak Dhikhla Ja-VI Sony 4.43

6 Pratigya Star Plus 4.42

7 Balika Vadhu Colors 4.33

8 Na Ana Is desh Laado Colors 4.09

9 DID Lil Masters Zee TV 3.92

• Fiction remained the most watched genre in 2010 • However, Jhalak Dhikhla Ja-IV & DID Lil Masters, Reality shows marked their presence in top ten list

Television - Reality Shows on Hindi GEC

Source: TAM | PWC Research

Reality Shows on Hindi GEC

Sr. No. Genre Shows Channel

1 Celeb reality Rakhi Ka Insaaf Imagine TV

2 Game show KBC Sony TV

3 Talent hunts Jhalak Dikhla Ja, Indian Idol, Master Chef India, DID,

India's Got Talent, Sa re Ga Ma Pa, The Great India

Laughter Challenge, Boogie Woogie

Sony TV, Star Plus, Zee TV, Star One

4 Matchmaking Rahul Dulhaniya Le Jayega Imagine TV

5 Social Experiment Bigg Boss, Emotional Atyachar Colors, UTV Bindass

6 Adventure-based show Khatron Ke Khiladi, MTV Roadies Colors, MTV

• The year 2010 saw the non-fiction genre rise in popularity • Many high profile reality shows yielded good results for the broadcaster

Television - IPL

Source: TAM

Effects of IPL Season IV on various channel genre GRP

Genre Pre IPL Season IV IPL Season IV Difference (%)

ENGLISH BUSINESS NEWS 39 30 -22

ENGLISH MOVIES 228 243 7

English GEC 47.19 45.63 3

ENGLISH NEWS 90 79 -13

HINDI BUSINESS NEWS 37 28 -24

HINDI GEC 7364 6899 -6

HINDI MNEWS 1083 968 -11

HINDI MOVIES EXCEPT MAX 1996 2177 9

HINDI MUSIC GENRE 601 611 2

INFOTAINMENT 304 283 -7

KIDS 1632 1955 20

LIFESTYLE 38 41 7

MAX 743 2376 220

REGIONAL 8515 8671 2

• Today IPL is the most sought-after property on Indian television • The average TVR for IPL season IV was 3.91, much lower than 5.51 for IPL season III • IPL IV highly impacted the News category, didn’t affect Hindi & English GECs much

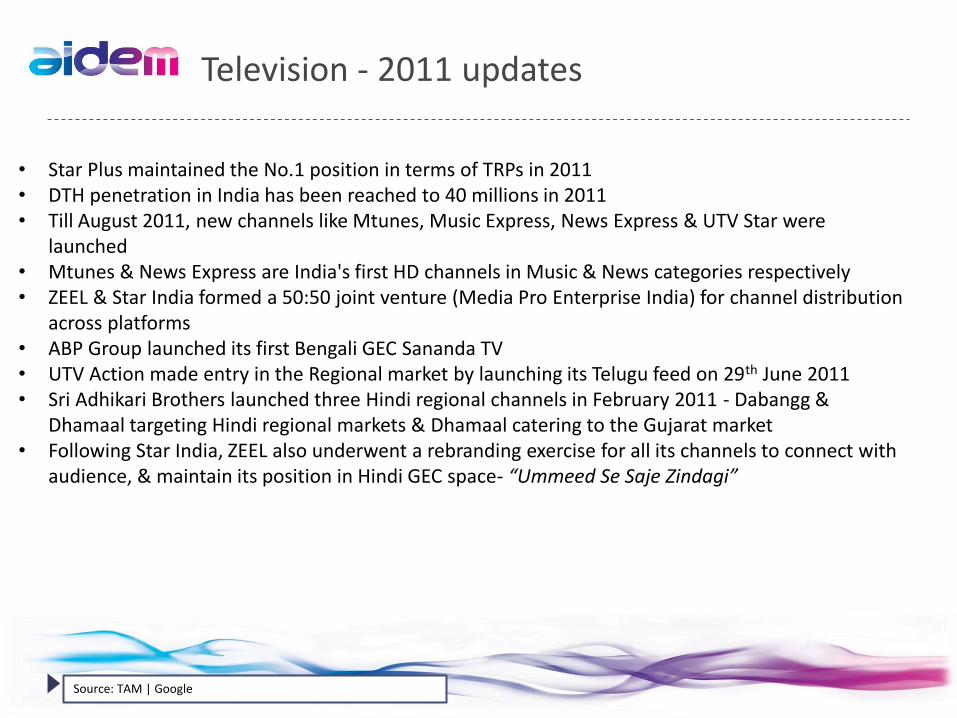

Television - 2011 updates

Source: TAM | Google

• Star Plus maintained the No.1 position in terms of TRPs in 2011 • DTH penetration in India has been reached to 40 millions in 2011 • Till August 2011, new channels like Mtunes, Music Express, News Express & UTV Star were

launched • Mtunes & News Express are India's first HD channels in Music & News categories respectively • ZEEL & Star India formed a 50:50 joint venture (Media Pro Enterprise India) for channel distribution

across platforms • ABP Group launched its first Bengali GEC Sananda TV • UTV Action made entry in the Regional market by launching its Telugu feed on 29th June 2011 • Sri Adhikari Brothers launched three Hindi regional channels in February 2011 - Dabangg &

Dhamaal targeting Hindi regional markets & Dhamaal catering to the Gujarat market • Following Star India, ZEEL also underwent a rebranding exercise for all its channels to connect with

audience, & maintain its position in Hindi GEC space- “Ummeed Se Saje Zindagi”

The Print Industry-At a glance

Print media industry - Revenue

Source: PWC | Industry Estimates

Growth of the print media industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Newspaper 121.1 131.5 140.7 142.8 159.5 9.2

% change 17.3 7.0 1.5 11.7

Magazine 16.5 19.0 21.0 18.6 19.2 3.8

% change 14.9 10.6 (11.5) 3.1

Total 128.0 149.0 162.0 161.5 178.7 8.6

% change 16.4 8.7 (0.3) 10.7

• It was a poor year for the Magazine industry with a marginal growth in advertising & almost no change in circulation

Print media industry - Revenue segmentation

Source: PWC | Industry Estimates

Growth of the print media industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Advertisement 78.0 94.0 103.5 100.0 113.5 9.8

% change 20.5 10.1 (3.0) 13.5

Circulation 50.7 56.5 58.3 61.5 65.2 6.5

% change 12.0 3.0 5.0 6.2

Total 128.0 149.0 162.0 161.5 178.7 9.6

% change 16.4 8.7 (0.3) 10.7

• Print advertising contributes to 63% of the industry’s revenue • The growth in circulation was largely contributed by players expanding into newer geographic

markets

Sector & Category wise share in print advertising

Source: TAM Adex

Sector-wise share in print advertising in 2010

Top sectors Share %

Services 12

Banking/Finance/Investments 11

Education 10

Auto 7

Retail 5

Personnel Accessories 4

Durables 4

Personnel Healthcare 3

Corporate/Brand Image 3

Media 2

• Print ad volumes of the Services sector grew by 43% during 2010 as compared to 2009 • Print ad volumes of the BSFI sector grew by 50% during 2010 compared to 2009 • Educational institutions , social ads & properties/real estates were the top three categories constituted

39% share of overall Print ad pie

Share of top categories in print advertising in 2010

Top categories Share %

Educational Institutions 9

Social Advertisements 7

Properties/Real Estates 4

Independent Retailors 4

Cars/Jeeps 3

Corporate/Brand Image 3

Hospital/Clinics 2

Events 2

Cellular Phones 2

Coaching Centers/Competitive Exams 2

Key Advertisers in print advertising

Source: TAM Adex

Key advertisers in print in 2010

Sr. No. Top Advertisers

1 Naaptol.com

2 Tata Motors Ltd

3 Maruti Udyog Ltd

4 Pantaloons Retail India Ltd

5 LG Electronics India Ltd

6 Dell Computers Corporation

7 SBI

8 General Motors India Ltd

9 Torque Pharmaceuticals

10 Videocon Industries Ltd

• Naaptol.com, operating in the Internet service domain, broke into the Top Advertisers category and was the largest advertiser in Print followed by Tata Motors & Maruti Udyog

The Radio Industry - At a glance

Radio media industry - Revenue

Source: PWC | Industry Estimates

Growth of the radio media industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Radio Advertising 5.0 6.9 8.3 9.0 10.8 21.20

% change 38.0 20.3 8.4 20.0

Radio share in ad pie % 3.1 3.6 3.8 4.2 4.4

• Radio advertising witnessed a healthy growth in 2010 • Radio advertising currently constitutes about 4.4% of the Total Advertising industry

Sector & Category wise share in radio advertising

Source: RAM Adex | PWC Research

Sector-wise share in radio advertising in 2010

Top sectors Rank in 2009

Properties/real estate 5

Cellular phone service 2

TV channel promotion 1

Independent retailors 4

Social advertisements 3

Cellular phones New

Jewellery 10

Educational Institutes 6

Corporate/brand image New

Automobiles New

• Properties/real estates was the Top advertiser category on radio • Vodafone was the top advertiser as telecom players increased their spends on radio • Star TV increased its promotion on radio during its Rebranding exercise

Share of top categories in radio advertising in 2010

Top categories Rank in 2009

Vodafone Essar Ltd 2

Bharti Airtel Ltd 10

Star TV Network 6

Pantaloons Retail India Ltd 5

Nokia Corporation New

Tata Teleservices 3

Min of Health & Family Welfare 9

Coca Cola India Ltd New

Idea Cellular Ltd New

HUL 1

FM penetration 2007 vs. 2011

Source: Radio Establishment Survey |RAM| PWC Research

51%

59%

71%

63% 59%

70%

88% 87%

64%

77%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mumbai Delhi Banglore Kolkata Overall

FM

Penetr

atio

n 2

011 (

%)

FM

Penetr

atio

n 2

007 (

%)

2007 2011

• Delhi has observed the greatest increase in FM penetration among RAM markets

Preferred mode of listening to radio

Source: IRS 2010 Q4 | PWC Research

71%

21%

2% 1% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Radio/Music System Mobile/Portable

Device

TV Car/Stereo Others

FM

Penetr

atio

n 2

007 (

%)

%

• Radio handsets & Music systems remain the most used device for radio listening • This is probably because radio listening habits haven’t yet developed fully in the smaller towns of India

The Internet Industry - At a glance

Internet media industry - Revenue

Source: PWC | Industry Estimates

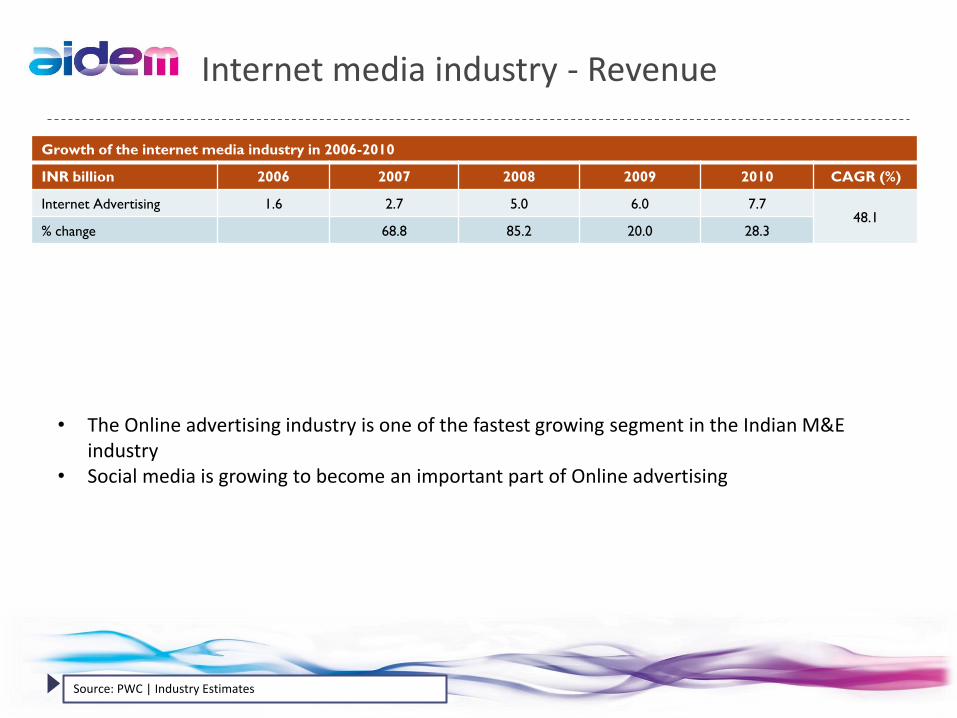

Growth of the internet media industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Internet Advertising 1.6 2.7 5.0 6.0 7.7 48.1

% change 68.8 85.2 20.0 28.3

• The Online advertising industry is one of the fastest growing segment in the Indian M&E industry

• Social media is growing to become an important part of Online advertising

Top social networking sites in India

Source: ComScore Media Matrix | PWC Research

Top social networking site in India

Total India: Age 15+, home & work location

India Total unique visitors (‘000s)

July-2009 July-2010 % change

Total Internet: Total audience 35028 39562 13

Social networking 23255 33158 43

Facebook.com 7472 20873 179

Orkut 17069 19871 16

Bharatstudent.com 4292 4432 3

Yahoo! Plus - 3507 -

Twitter.com 984 3341 239

LinkedIn.com - 3267 -

Zedge.net 1767 3206 81

Ibibo.com 1562 2960 89

• In India, Social Networking websites have shown a remarkable growth of 43% in total unique visitors over 2009

• Advertising on social media has witnessed a growth of 54% in 2010-11

Internet Usage Patterns

Source: IAMAI| PWC Research

41%

32%

25% 24%

6% 5% 3% 2% 2%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

% o

f purp

ose

of onlin

e a

ccess

• In terms of revenue, travel websites are growing at a very fast pace • Travel sites reached 37% of the online population in India in April 2010 • Entertainment & Communication continue to be the major reason for internet access, 73% of the

population access the net for this reason

Internet users: 50:50 splits in Metros-Non Metros

Source: IMRB iCube report 2010

Maximum online population growth has been coming from the Non Metro towns

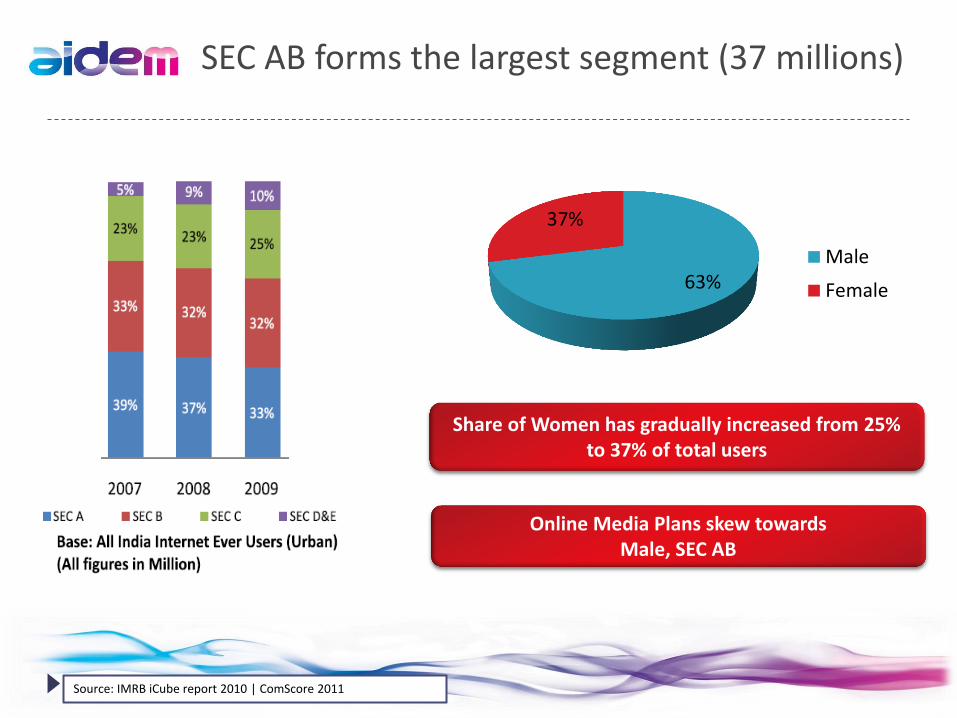

SEC AB forms the largest segment (37 millions)

63%

37%

Male

Female

Online Media Plans skew towards Male, SEC AB

Share of Women has gradually increased from 25% to 37% of total users

Source: IMRB iCube report 2010 | ComScore 2011

User profile on the Internet

35%

41%

16%

6% 2%

Age break up

15-24 25-34 35-44 45-55 55+

63%

37%

Gender

Male Female

Youth are the driving factor– More than 75% of them fall under the age bracket of 15 – 34

The Male populations constitutes a majority but the % growth of females on the internet is on an increase

Source: IMRB iCube report 2010 | ComScore 2011

User exploring the net more

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

ServicesPortals

Social Network

Search

News

Technology

Multimedia

Blogs

Retail

Finance

Travel

EducationCareer

Music

Sports

Movies

Games

Photos

Regional

TV

IM

B2b

Health

Automotive

Real Estate

May-11

Apr-10

Social networks are the new IM’s and Photo sharing platforms

Internet is the new TV, 100% growth for TV sites, more than 10mm users watching TV content

Moderate growth of about 35% for Retail, Travel & Finance

Health & coupon category seeing an upward trend

Internet grew by 13%, avg. growth for Categories 48% indicating more consumption by same users

Source: ComScore 2011

Change in age distribution

Source: ComScore 2011

34%

27%

41%

26%

16%

22%

6%

14%

2%

11%

15-24 25-34 35-44 45-54 55+

There’s has been a radical growth in the share of the 25-34 age group to the total online population

2010

2011

Internet ‘Routine’

Source: Microsoft 2011

Internet - 2011

Source: IIMRB iCube Report | ComScore May 2011 | PWC

• 100 Million active users by 2012 • Average of 16 hours being spent online every week • 100% increase in time spent in last three years • 85% of internet users are in the age group of 19-40 years • 100% growth for TV sites, more than 10 million users watching TV content • The online advertising industry is estimated to march ahead from INR 7.7 billion in 2010 to INR 24 billion

in 2015 a CAGR of 25% over the next five years • In January 2011, Groupon entered the Indian market with the acquisition of SoSasta.com • As the national broadband policy formulated & implemented over the next three to five years, internet

subscription will increase

• Highlights of 2011 o Bazee.com Pvt. Ltd. invested INR 164.8 Mn. in Ebay India Pvt. Ltd. o As 3G becomes more affordable, it will give a boost to mobile advertising

The Film & Music Industry - At a glance

Film industry - Revenue

Source: PWC | Industry Estimates

Growth of the film industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

Box office-domestic 64.0 71.5 81.3 70.0 61.1 (1.2)

% change 11.7 13.6 (13.8) (12.7)

Box office-overseas 7.0 8.5 10.0 8.0 7.7 2.4

% change 21.4 17.6 (20.0) (3.8)

Home Video 6.4 7.4 5.9 6.5 5.2 (5.3)

% change 15.3 (20.9) 11.3 (16.1)

Ancillary right 7.0 8.5 10.0 10.5 13.5 17.8

% change 21.4 17.6 5.0 28.6

Total 84.4 95.9 107.1 95.0 87.5 0.9

• The industry showed a de-growth for the second consecutive year • There were 215 Hindi releases in 2010 as compared to 235 in 2009 and 1059 regional releases

in 2010 as compared to 1053 in 2009

Film industry - Multiples players

Source: PWC | Industry Estimates

Snapshots of key multiplex players- Total number of screens in 2009 vs. 2010

Players 2009 2010 Proposed addition in 2011

Cinemax 94 114 30

Big Cinema 253 260 -

Fame 95 97 10

Inox 119 144 40

PVR 148 175 50

• Despite the lack of good quality content in films, multiplexes registered a double digit growth • Multiplexes have been experimenting with schemes to increase the footfalls (For e.g. giving

heavy discount on morning shows) • Newer players like Cinepolis, Mexican multiplex chain announced their entry in Indian market

in 2009

Music industry – A Snapshot

Source: PWC | Industry Estimates

• The music industry earns its revenue from five major streams 1. Physical Sales:- Revenue from cassettes, CDs, etc.. 2. Mobile VAS:- Ring tones, caller tunes etc. 3. Radio broadcast:- Royalties from radio stations etc. 4. Online download:- Sale of music through Internet Downloads 5. Public performance royalty:- Royalty from events & other functions

• Major portion of the music revenue in India comes from film music • Share of independent music albums is very small • The industry is currently estimated to be INR 9.5 Bn. in 2010 as compared to INR 7.5 Bn. in

2009, growth of 25.7% • Mobile is expected to be a major growth driver for the music industry • Mobile VAS is projected to contribute around 75% to the total industry revenue in 2015 • Physical sales are expected to decline in the coming years

OOH industry - A Snapshot

Source: PWC | Industry Estimates

• Telecom, BFSI, E&M & FMCG were among the top advertisers for 2010 • Digital OOH is the next growth medium for the industry • Focus is shifting from the number of screens to the quality and quantity of audience • OOH players are offering innovative & customized solutions to advertisers for specific target

audience • OOH players are focusing on ROI rather than on increasing the number of properties

Growth of the Indian OOH industry in 2006-2010

INR billion 2006 2007 2008 2009 2010 CAGR (%)

OOH Advertising 10.0 12.5 15.0 12.5 14.0 8.8

% change 25.0 20.0 (16.7) 12.0

OOH share in ad pie (%) 6.2 6.4 6.9 5.8 5.7

For enquiries, please contact

Aidem Ventures Pvt Ltd.

1/A Kaledonia,

Andheri Sahar Road,

Andheri (East),

Mumbai – 400069,

India.

Ph. no. +91. 2266665000

www.aidem.in

![arXiv:1608.05148v2 [cs.CV] 7 Jul 2017 · Nick Johnston nickj@google.com Sung Jin Hwang sjhwang@google.com David Minnen dminnen@google.com Joel Shor joelshor@google.com Michele Covell](https://static.cupdf.com/doc/110x72/5ee12c7aad6a402d666c2605/arxiv160805148v2-cscv-7-jul-2017-nick-johnston-nickj-sung-jin-hwang-sjhwang.jpg)