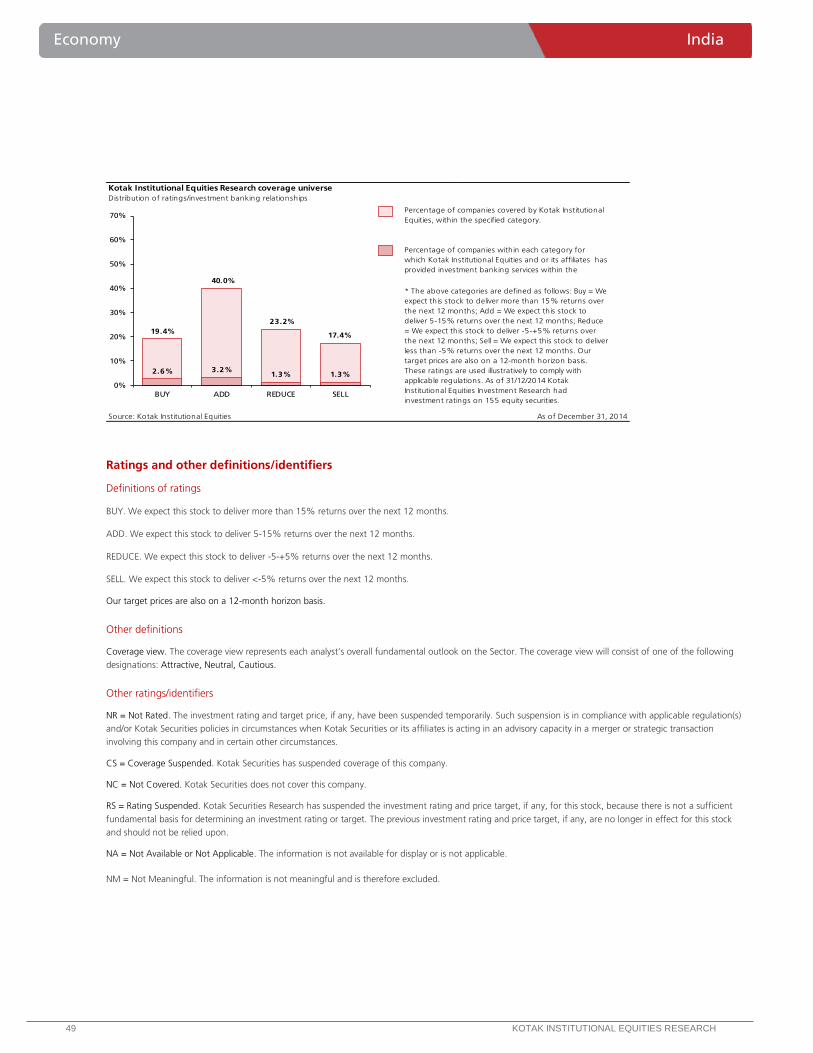

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Daily Alerts

Company alerts

Bajaj Corp.: Management meet notes - on a strong footing

Sector alerts

Technology: Accenture - another strong broad-based growth quarter

Telecom: Auction outcome details - largely in line, with some customary surprises

Infrastructure: Indian AC industry - bring on the heat

INDIA DAILY March 27, 2015 India 26-Mar 1-day 1-mo 3-mo

Sensex 27,458 (2.3) (6.0) 0.8

Nifty 8,342 (2.2) (5.7) 1.7

Global/Regional indices

Dow Jones 17,678 (0.2) (2.5) (2.1)

Nasdaq Composite 4,863 (0.3) (2.0) 1.2

FTSE 6,895 (1.4) (0.7) 4.3

Nikkei 19,491 0.1 3.7 9.4

Hang Seng 24,541 0.2 (1.1) 5.1

KOSPI 2,023 0.0 1.9 3.9

Value traded – India

Cash (NSE+BSE) 267 226 209

Derivatives (NSE) 5,785 5,816 1,093

Deri. open interest 2,812 2,777 1,585

Forex/money market

Change, basis points

26-Mar 1-day 1-mo 3-mo

Rs/US$ 62.8 (10) 123 (84)

10yr govt bond, % 7.9 1 9 (22)

Net investment (US$ mn)

25-Mar MTD CYTD

FIIs 99 3,678 16,162

MFs (63) (632) 4,802

Top movers

Change, %

Best performers 26-Mar 1-day 1-mo 3-mo

SIEM IN Equity 1355.2 (0.7) 2.1 58.5

HDIL IN Equity 101.3 1.0 (15.2) 49.6

LPC IN Equity 1973.0 (1.8) 13.6 40.2

AL IN Equity 68.5 1.6 2.3 37.6

RBXY IN Equity 819.3 (1.4) 19.1 33.3

Worst performers

BOI IN Equity 197.4 (2.7) (16.2) (34.5)

PNB IN Equity 148.2 (4.7) (10.8) (33.3)

UNBK IN Equity 162.0 (2.4) (7.6) (32.8)

RCOM IN Equity 60.1 (1.9) (13.9) (25.3)

BOB IN Equity 161.0 (2.9) (11.0) (24.6)

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

LHO growth accelerates a tad; however, overall consumer demand weak

Management highlighted that while LHO market growth, as per Nielsen, has picked up from -

1% in December 2014 to 1% in January 2015 and 2.5% in February, overall consumer demand

still remains weak. Cooling oils growth has come under pressure in 4QFY15 due to weaker off-

take, especially in North due to unseasonal rains and relatively cooler temperatures.

ADHO continues to grow ahead of market; several other growth drivers in place

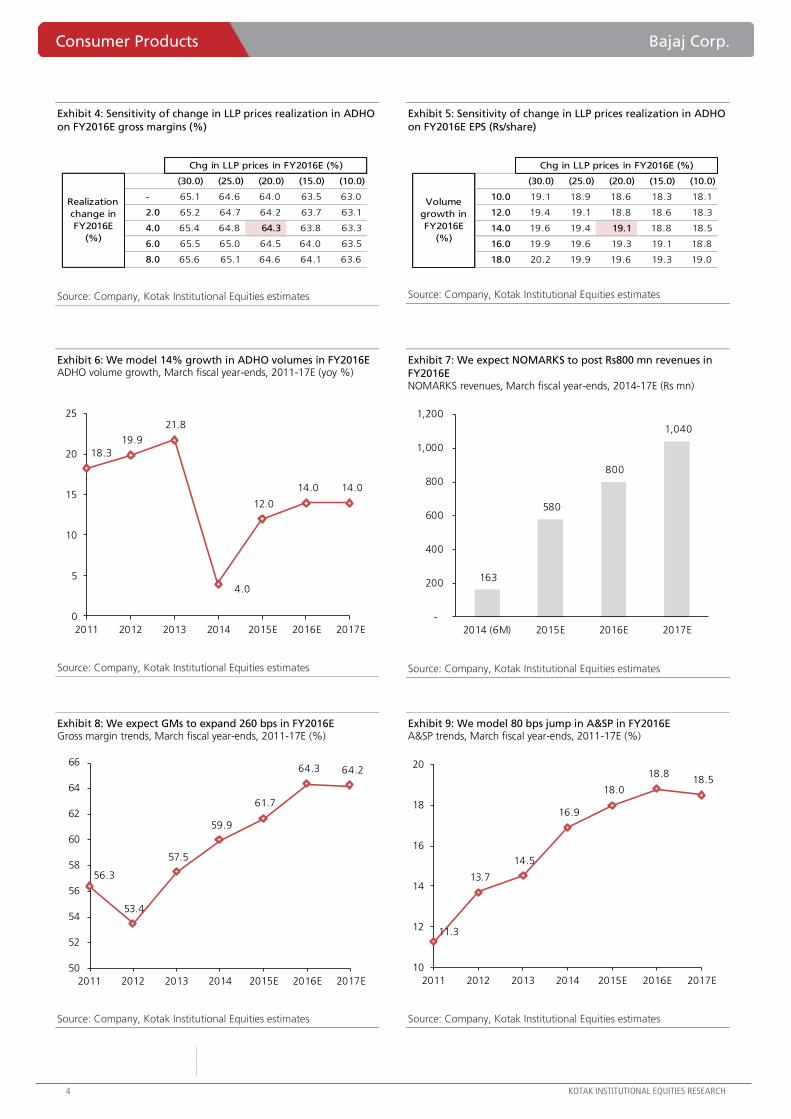

While we model 14% volume growth in ADHO in FY2016E driven by low base (in 1HFY16E)

and market share gains, our interaction with the management suggests several other growth

drivers – (1) NOMARKS continues to post good growth driven by better traction in both creams

and facewash and distribution expansion; we model NOMARKS to post `800 mn revenues in

FY2016E (+40% yoy), (2) BJCOR has recently launched a new low-cost Amla brand in five states

– Bajaj Amla with Almond and Rosemary oil positioned against Shanti Amla at `20 for 80 ml;

we note Marico has cut prices of Shanti Amla 80 ml SKU from `23 to `20 (in response,

perhaps), and (3) BJCOR is planning to increase its focus on international markets such as

Nepal, Bangladesh, the UAE and Africa; we note BJCOR has four dedicated country managers

across key geographies and is planning to set up a manufacturing (third-party) facility in the

UAE.

We remain positive; retain BUY and raise TP to `510 (from `495)

We model 27.7% yoy growth in PAT in FY2016E aided by – (1) 18% yoy growth in ADHO

revenues (14% volume growth and ~4% weighted average price hike) and (2) 260 bps jump in

GMs to 64.3% aided by 20% dip in LLP prices; we note BJCOR has locked in LLP for six months

at `60.5/kg (current LLP prices stand at `62.5/kg and FY2015E average for BJCOR stood at

`77.6/kg). While we expect A&SP to jump 80 bps yoy to 18.8%, we expect bulk of the increase

to be driven by higher promotional expenses (especially at consumer levels in the form of

freebies).

We remain bullish on BJCOR driven by – (1) volume growth pick-up, (2) strong earnings growth

visibility and (3) modest valuations (P/E of 20X FY2017E EPS; at ~40% discount to sector

multiples ex-ITC). BJCOR remains our preferred pick among small-cap consumer names; retain

BUY rating with a revised target price of `510 (from `495) as we roll over to March 2017E

estimates (based on P/E multiple of 23X; ~30% discount to sector multiples ex-ITC).

Bajaj Corp. (BJCOR) Consumer Products

Management meet notes – on a strong footing. Our recent interaction reinforces

our confidence in BJCOR – (1) LHO growth has accelerated a tad and ADHO continues

to grow significantly ahead of market, (2) LLP prices remain benign and (3) NOMARKS,

international business and new low-cost Amla brand to emerge as additional growth

drivers. Modest valuations at P/E of 20X FY2017E lend additional comfort. Retain BUY

rating with a revised TP of `510 (from `495) based on P/E of 23X March 2017E.

BUY

MARCH 27, 2015

UPDATE

Coverage view: Attractive

Price (`): 443

Target price (`): 510

BSE-30: 27,458

Bajaj Corp.

Stock data Forecasts/Valuations 2015 2016E 2017E

52-week range (Rs) (high,low) EPS (Rs) 15.0 19.1 22.3

Market Cap. (Rs bn) EPS growth (%) 24.3 27.7 16.6

Shareholding pattern (%) P/E (X) 29.6 23.2 19.9

Promoters 66.9 Sales (Rs bn) 8.3 9.9 12.0

FIIs 23.5 Net profits (Rs bn) 2.2 2.8 3.3

MFs 2.0 EBITDA (Rs bn) 2.4 3.1 3.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 26.1 19.9 16.0

Absolute 3.6 30.5 102.8 ROE (%) 43.5 52.9 53.1

Rel. to BSE-30 8.5 29.5 63.2 Div. Yield (%) 2.6 2.0 2.7

Company data and valuation summary

500-203

65.4

Bajaj Corp. Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

Exhibit 1: We have broadly retained our estimates Key changes to earnings model, Bajaj Corp, March fiscal year-ends, 2015-17E

Source: Company, Kotak Institutional Equities estimates

Exhibit 2: BJCOR has recently launched ‘Bajaj Amla with Almond and Rosemary oil’ – a low-cost Amla

brand positioned versus Shanti Amla (this is the 160 ml variant)

Source: Company, Kotak Institutional Equities

Exhibit 3: LLP prices have corrected sharply from peak of Rs85/kg a year ago to Rs62.5/kg BJCOR’s quarterly average purchase price for LLP (Rs/kg)

Source: Company, Kotak Institutional Equities

2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

Revenues (Rs mn) 8,266 9,896 11,964 8,262 9,947 12,098 0.0 (0.5) (1.1)

EBITDA (Rs mn) 2,390 3,084 3,768 2,376 3,068 3,778 0.6 0.5 (0.3)

EBITDA (%) 28.9 31.2 31.5 28.8 30.8 31.2

PAT (Rs mn) 2,206 2,817 3,283 2,194 2,795 3,291 0.5 0.8 (0.2)

EPS (Rs/share) 15.0 19.1 22.3 14.9 19.0 22.3 0.5 0.8 (0.2)

Revised Earlier Change (%)

50

55

60

65

70

75

80

85

90

1Q

FY1

1

2Q

FY1

1

3Q

FY1

1

4Q

FY1

1

1Q

FY1

1

2Q

FY1

2

3Q

FY1

2

4Q

FY1

2

1Q

FY1

3

2Q

FY1

3

3Q

FY1

3

4Q

FY1

3

1Q

FY1

4

2Q

FY1

4

3Q

FY1

4

4Q

FY1

4

1Q

FY1

5

2Q

FY1

5

3Q

FY1

5

4Q

FY1

5E

Consumer Products Bajaj Corp.

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 4: Sensitivity of change in LLP prices realization in ADHO

on FY2016E gross margins (%)

Source: Company, Kotak Institutional Equities estimates

Exhibit 5: Sensitivity of change in LLP prices realization in ADHO

on FY2016E EPS (Rs/share)

Source: Company, Kotak Institutional Equities estimates

Exhibit 6: We model 14% growth in ADHO volumes in FY2016E ADHO volume growth, March fiscal year-ends, 2011-17E (yoy %)

Source: Company, Kotak Institutional Equities estimates

Exhibit 7: We expect NOMARKS to post Rs800 mn revenues in

FY2016E NOMARKS revenues, March fiscal year-ends, 2014-17E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

Exhibit 8: We expect GMs to expand 260 bps in FY2016E Gross margin trends, March fiscal year-ends, 2011-17E (%)

Source: Company, Kotak Institutional Equities estimates

Exhibit 9: We model 80 bps jump in A&SP in FY2016E A&SP trends, March fiscal year-ends, 2011-17E (%)

Source: Company, Kotak Institutional Equities estimates

64.3 (30.0) (25.0) (20.0) (15.0) (10.0)

- 65.1 64.6 64.0 63.5 63.0

2.0 65.2 64.7 64.2 63.7 63.1

4.0 65.4 64.8 64.3 63.8 63.3

6.0 65.5 65.0 64.5 64.0 63.5

8.0 65.6 65.1 64.6 64.1 63.6

Chg in LLP prices in FY2016E (%)

Realization

change in

FY2016E

(%)

19.1 (30.0) (25.0) (20.0) (15.0) (10.0)

10.0 19.1 18.9 18.6 18.3 18.1

12.0 19.4 19.1 18.8 18.6 18.3

14.0 19.6 19.4 19.1 18.8 18.5

16.0 19.9 19.6 19.3 19.1 18.8

18.0 20.2 19.9 19.6 19.3 19.0

Chg in LLP prices in FY2016E (%)

Volume

growth in

FY2016E

(%)

18.3

19.9

21.8

4.0

12.0

14.0 14.0

0

5

10

15

20

25

2011 2012 2013 2014 2015E 2016E 2017E

163

580

800

1,040

-

200

400

600

800

1,000

1,200

2014 (6M) 2015E 2016E 2017E

56.3

53.4

57.5

59.9

61.7

64.3 64.2

50

52

54

56

58

60

62

64

66

2011 2012 2013 2014 2015E 2016E 2017E

11.3

13.7

14.5

16.9

18.0

18.8 18.5

10

12

14

16

18

20

2011 2012 2013 2014 2015E 2016E 2017E

Bajaj Corp. Consumer Products

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Exhibit 10: Profit model, balance sheet, cash model of Bajaj Corp, March fiscal year-ends, 2011-17E

Source: Company, Kotak Institutional Equities estimates

2011 2012 2013 2014 2015E 2016E 2017E

Profit model

Net revenues 3,587 4,722 6,057 6,707 8,266 9,896 11,964

EBITDA 1,081 1,154 1,714 1,849 2,390 3,084 3,768

Other income 178 385 411 412 336 416 510

Interest expense — (1) (1) (59) (2) (2) (2)

Depreciation (18) (26) (40) (43) (50) (57) (67)

Pretax profits 1,240 1,512 2,085 2,159 2,674 3,440 4,209

Tax (210) (311) (423) (384) (468) (624) (926)

Net income 1,031 1,201 1,662 1,775 2,206 2,817 3,283

Extraordinary items (190) — — (286) (470) (470) (184)

Reported profit 841 1,201 1,662 1,489 1,736 2,347 3,100

Recurring Earnings per share (Rs) 7.0 8.1 11.3 12.0 15.0 19.1 22.3

Balance sheet

Total shareholder's equity 3,763 4,278 4,826 5,192 4,944 5,698 6,673

Total borrowings — — — — — — —

Deferred tax liability 0 10 15 4 4 4 4

Total liabilities and equity 3,764 4,288 4,840 5,196 4,948 5,702 6,677

Net fixed assets 220 389 791 812 886 1,126 1,238

Investments 3,301 3,135 1,845 1,575 1,575 1,575 1,575

Cash 813 275 1,892 1,292 1,471 2,487 3,577

Net current assets (571) 59 (118) (37) (68) (100) (144)

Miscellaneous expenditure 1 — — — — — —

Goodwill/intangibles — 430 430 1553 1084 614 430

Total assets 3,764 4,288 4,840 5,196 4,948 5,702 6,677

Free cash flow

Operating cash flow, excl. working capital 875 868 1,300 1,408 1,922 2,460 2,842

Working capital changes 140 28 (70) (150) 31 32 44

Capital expenditure (62) (196) (111) (1,467) (124) (297) (179)

Free cash flow 953 700 1,118 (208) 1,829 2,195 2,707

Ratios (%)

Revenue growth 21.8 31.7 28.3 10.7 23.3 19.7 20.9

Gross margin 56.3 53.4 57.5 59.9 61.7 64.3 64.2

EBITDA margin 30.1 24.4 28.3 27.6 28.9 31.2 31.5

EPS growth 22.8 16.5 38.4 6.8 24.3 27.7 16.6

RoE 41.5 25.6 26.4 33.2 35.0 41.5 45.5

RoCE 47.7 26.4 24.7 33.4 35.6 43.9 48.9

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Accenture delivers yet again; 10% growth in 2QFY15, FY2015 revenue growth outlook raised

Accenture reported local currency (l/c) revenue growth of 12% in the February 2015 (2QFY15)

quarter. Growth was strong in both consulting (+11% yoy in l/c) and outsourcing (+13% yoy in

l/c) segments. Digital, contributing 20% to overall revenues, grew 20% and forms the bedrock

of ACN’s growth; part of the growth is aided by a number of acquisitions in the past 12

months. From a vertical standpoint, communications, media and tech grew 15% and products

segment grew by 13%. Accenture reported second-highest bookings of US$9.4 bn in the

quarter.

ACN raised FY2015 (Aug year-end) revenue growth guidance to 8-10% from 5-8% in l/c. The

management indicated continuation of strong growth in 2HFY15, while attributing the growth

to significant market share gains across all streams of businesses. Accenture targets gross

addition of 90,000 employees in FY2015.

Currency impacts reported USD growth and EPS

Fx impacted ACN‘s reported USD revenue growth by 6.5%. We note that ACN derives 36% of

revenues from Europe, which has suffered from currency depreciation against USD. ACN, as a

result, cut FY2015 (Aug year-end) EPS guidance by 1%. An interesting aspect of the

performance was 140 bps yoy decline in gross margin in the Feb 2015 quarter, presumably due

to currency movements. However, 170 bps decline in SG&A expenses resulted in overall 30 bps

yoy increase in EBIT margin.

Read-through—the difficult part but positive overall

Accenture’s result read-through is always open to contradicting interpretations. Strong

outsourcing-based growth for Accenture can be a reflection of a strong demand environment

(positive for Indian IT) or alternately led by market share gains (negative for Indian IT). The

management’s statement of growth led by market share gains across all key segments stirs up

the plot even more. Yet we believe that the overall read-through is a positive. We based this on

Growth in consulting business indicates a solid discretionary spending environment.

ACN indicated that growth in consulting business was across all segments, digital,

management, strategy and operations. Strong growth in consulting is a useful indicator of

discretionary spending even after making concessions of market share gains.

Another quarter of double-digit yoy growth in outsourcing segment. Solid growth in

outsourcing indicates that Accenture is participating in and winning deals as much as any

other offshore IT pure-plays. What makes this growth creditable is that ACN does not have

high exposure to IMS, the primary growth driver of other IT companies. The performance of

ACN demonstrates that growth is still possible in apps portfolio provided vendors are capable

to structure and deliver multi-service lines deals in an outcome-based format. ACN’s

outsourcing business comprises application services, business process management and

relatively low exposure to infra.

Technology India

Accenture—another strong broad-based growth quarter. Accenture reported an

outstanding local currency (l/c) revenue growth of 12% yoy and raised l/c revenue

growth guidance to 8-10% for FY2015E (August year-end) from 5-8% earlier. Growth

was strong across consulting and outsourcing segments. Read-through of ACN’s

results, tricky as it may be, is a positive for Indian IT based on strong growth in the

consulting business. Infosys and Tech Mahindra are our key picks in the sector.

NEUTRAL

MARCH 27, 2015

UPDATE

BSE-30: 27,458

Technology India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Maintain constructive view, recent correction is an opportunity to buy

We believe that demand in FY2016 will be similar to FY2015. Several US indicators such as

the Consumer Confidence Index, PMI and unemployment rate have been robust for the past

few quarters and point towards a healthy US economy. IT spends are likely to pick up in

banking and financial services. Indian IT companies are seeing significant market share gains

as large deals come up for re-bid. Demand is Europe is robust led by higher outsourcing. We

see recent correction in the stock prices as an opportunity to buy.

Exhibit 1: Accenture interim results, August fiscal year-ends (US$ mn)

Source: Company, Kotak Institutional Equities

Exhibit 2: Kotak Institutional Equities: valuation summary of key Indian technology companies

Source: Companies, Kotak Institutional Equities estimates

2QFY14 1QFY15 2QFY15 % qoq % yoy

Revenues 7,131 7,896 7,493 (5.1) 5.1

Cost of revenues 4,901 5,356 5,253 (1.9) 7.2

SG&A expenses 1,279 1,352 1,220 (9.8) (4.6)

EBIT 951 1,188 1,021 (14.0) 7.3

Other income (1) 4 (16)

PBT 950 1,192 1,005 (15.7) 5.8

Provision for taxes 228 300 262

PAT 722 892 743 (16.7) 2.9

Minority interest 51 61 52 (13.6) 2.8

PAT after minority interest 671 832 691 (16.9) 2.9

Margins (%)

EBIT 13.3 15.0 13.6

Net income 10.1 11.3 9.9

26-Mar-15 EPS (Rs) P/E (X) EV/EBITDA (X) RoE (%)

Company Price (Rs) Rating (Rs m) (US$ m) 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

HCL Technologies 987 REDUCE 1,387,984 22,141 53.8 56.2 62.2 18.4 17.6 15.9 13.6 12.2 10.5 32.7 27.4 24.9

Hexaware Technologies 289 SELL 87,160 1,390 10.8 14.1 16.0 26.7 20.5 18.1 17.2 14.4 12.5 26.2 31.5 32.6

Infosys 2,146 ADD 2,465,024 39,322 108.4 123.1 146.0 19.8 17.4 14.7 14.2 12.0 9.8 25.7 25.0 25.3

Mindtree 1,361 REDUCE 113,903 1,817 64.8 75.1 88.3 21.0 18.1 15.4 14.8 12.2 10.0 29.8 28.2 27.3

Mphasis 376 SELL 78,908 1,259 31.5 33.9 37.3 11.9 11.1 10.1 6.5 5.8 5.0 12.6 12.9 13.4

TCS 2,513 ADD 4,922,479 78,524 107.8 122.9 145.5 23.3 20.5 17.3 17.2 14.4 12.0 35.8 35.0 34.6

Tech Mahindra 651 ADD 625,525 9,978 32.6 38.9 45.8 20.0 16.7 14.2 14.5 11.8 9.9 26.9 25.4 24.0

Wipro 632 ADD 1,560,175 24,888 34.4 38.4 44.8 18.3 16.5 14.1 12.4 10.7 8.8 22.7 21.5 21.4

Technology Attractive 11,241,158 179,321 20.8 18.5 15.8 15.0 12.7 10.6 26.8 25.4 25.0

KIE universe 74,544,416 1,189,143 19.1 16.0 13.5 11.5 9.6 8.1 13.8 14.8 15.7

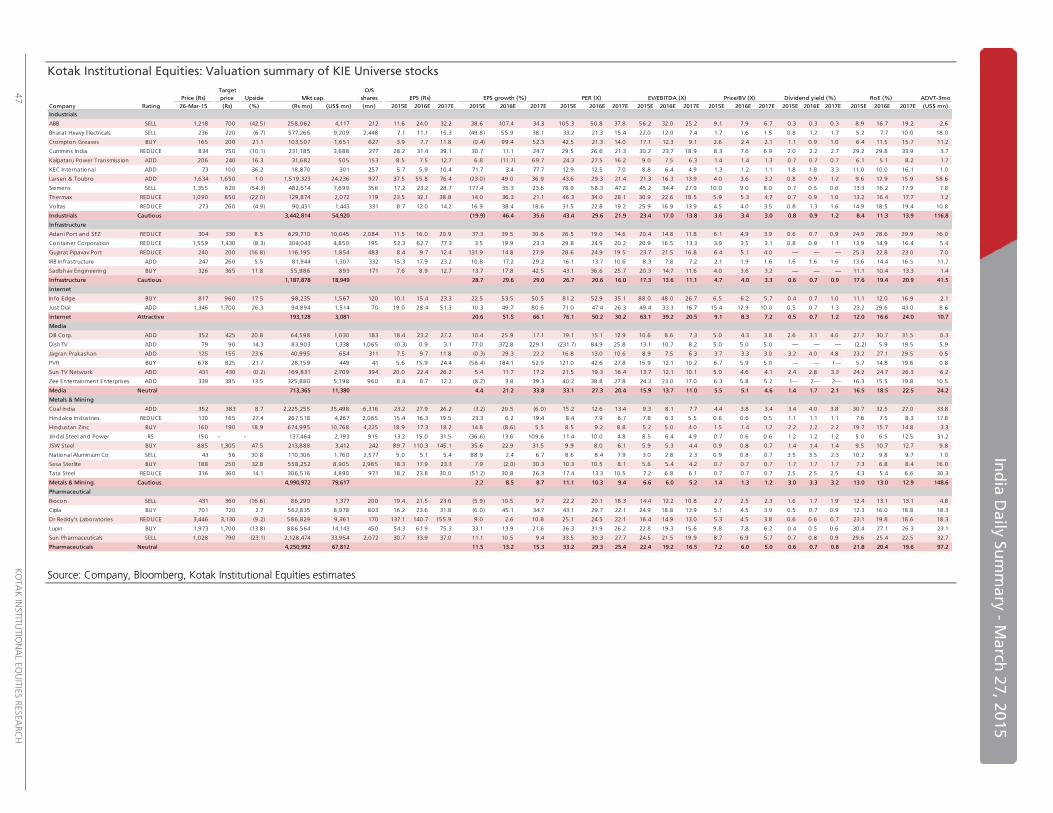

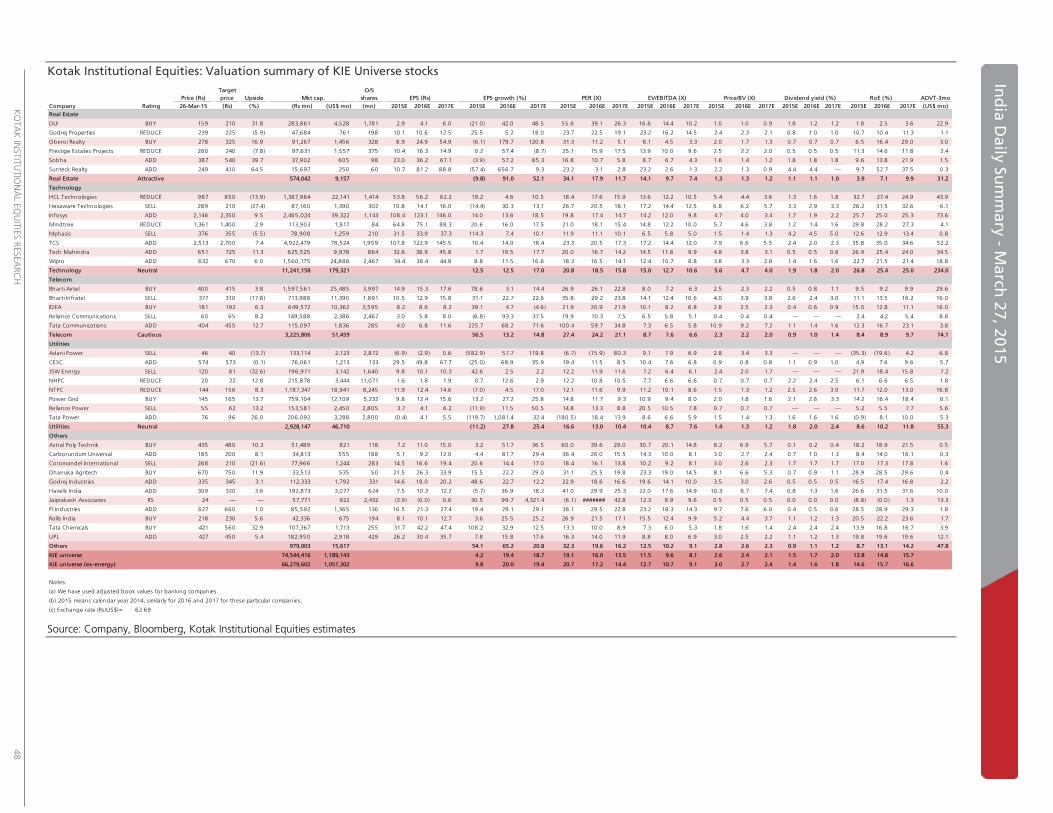

Target O/S shares EPS CAGR (%) Net Profit (Rs mn) EBITDA (Rs mn) Sales (Rs mn)

Company Price (Rs) (mn) 2014-17E 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

HCL Technologies 850 1,414 (11.7) 19.2 4.6 10.5 76,026 79,530 88,033 92,179 99,008 109,574 373,409 424,690 483,651

Hexaware Technologies 210 302 8.1 (14.4) 30.3 13.1 3,265 4,255 4,814 4,776 5,688 6,507 25,817 31,079 35,607

Infosys 2,350 1,143 (8.4) 14.0 13.6 18.5 123,923 140,730 166,802 151,530 175,693 208,274 537,630 611,997 716,247

Mindtree 1,400 84 18.0 20.6 16.0 17.5 5,452 6,324 7,431 7,140 8,462 10,060 35,601 41,818 49,573

Mphasis 355 210 36.3 114.3 7.4 10.1 6,625 7,112 7,828 8,874 9,625 10,516 58,502 62,083 66,382

TCS 2,700 1,959 14.2 10.4 14.0 18.4 211,120 240,700 285,082 273,451 321,887 377,750 950,462 1,109,160 1,303,154

Tech Mahindra 725 864 (29.0) 1.7 19.5 17.7 28,123 33,621 39,586 42,384 51,041 59,445 223,161 277,731 321,838

Wipro 670 2,467 12.2 8.8 11.5 16.6 84,989 94,750 110,440 109,738 121,764 140,490 472,513 521,492 598,704

Technology 12.5 12.5 17.0 539,522 607,023 710,016 690,073 793,169 922,616 2,677,096 3,080,050 3,575,156

KIE universe 4.2 19.4 18.7

Notes:

(a) HCL Technologies is June fiscal year-ending.

(b) Hexaware Technologies is December year-ending.

Mkt cap.

EPS growth (%)

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

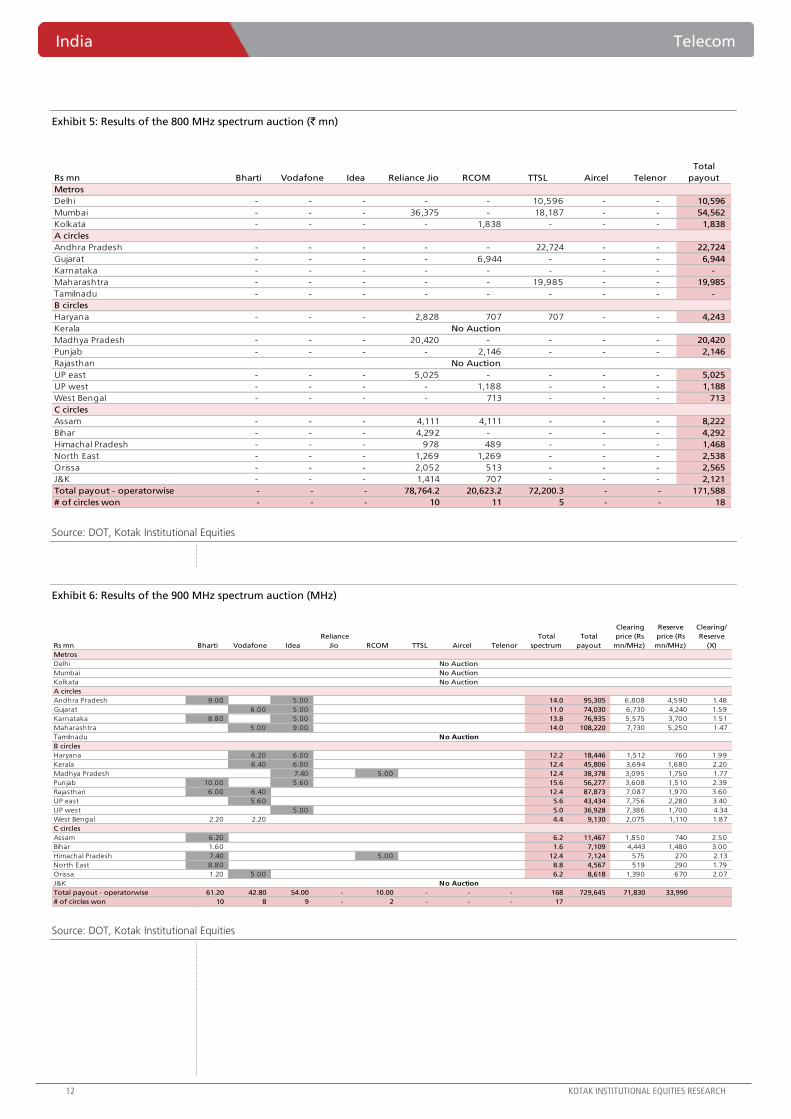

Auction details out; some surprises as always even as broad results are on expected lines

Some quick top-down highlights first, before we jump into the details –

Total aggregate payout of `1.1 tn, of which upfront payment would be `290 bn.

Aggregate payouts for various players—Idea – `303 bn, Vodafone `260 bn, Bharti – `291

bn, RJio – `101 bn, RCOM – `43 bn, TTSL – `79 bn, and Aircel – `23 bn. Telenor did not win

any spectrum.

Bharti, Vodafone, and Idea renewed a minimum of 5 MHz of 900 MHz spectrum in all of

their renewal circles. In fact, Bharti enhanced its 900 MHz holdings in five out of its six

renewal circles.

RCOM could not renew 900 MHz spectrum in five out of its seven circles, but did buy

alternate 1800 spectrum in two circles. The company faces the reality of having to shut

down its 2G GSM operations in three circles (Assam, Bihar, and West Bengal; GSM

operations in these circles contribute roughly 13% of its overall wireless revenues).

Bharti and Vodafone made good strides in terms of buying fresh spectrum for enhancing

data spectrum footprint. Idea could not do much on this front given that the company’s

primary focus was ensuring that it renews 900 MHz spectrum in its nine renewal circles.

R-Jio largely focused on completing its FD-LTE spectrum footprint and managed to expand

this to 20 circles from 14 before the auctions. The only two circles where RJio does not have

FD-LTE spectrum (either 1800 or 800; it bought substantial 800 MHz spectrum in these

auctions and we are assuming it is for FD-LTE) are Punjab and UP (West).

What do these results mean for the sector/ listed incumbents? A lot…

We believe that the incumbents met their two key objectives—(1) renew a minimum 5 MHz of

900-band spectrum in their respective 900 circles, and (2) enhance data spectrum footprint

wherever possible. On the second aspect, Bharti did better than Vodafone and Idea; however,

we believe that all three are well-positioned from a hi-speed data spectrum standpoint in their

respective leadership circles (more on this later). From a renewal pressure standpoint,

incumbents can now look forward to a long phase where they do not need to worry about

‘business continuity risks’ emerging from the unique spectrum renewal approach that the

government adopted. To sum up, we believe the positives just about balance out the negatives

in the form of financial pressure arising from massive payouts. We stay positive on both Bharti

and Idea.

Telecom India

Auction outcome details—largely in line, with some customary surprises. Circle-

wise spectrum won (and lost, RCOM in particular) by various players was largely in line

with our expectations in terms of renewals. In fresh spectrum buyouts, the top-3 players

(Bharti, Vodafone and Idea) and R-Jio bought to enhance data-spectrum breadth and

depth while players such as TTSL and Aircel bought spectrum to de-risk some of their

key renewals (due in the next 3-4 years). Auction outcome may lead to some cuts in our

near-term estimates, but does not change out medium-term positive view on the two

listed incumbents—Bharti and Idea.

CAUTIOUS

MARCH 26, 2015

UPDATE

BSE-30: 27,458

Telecom India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

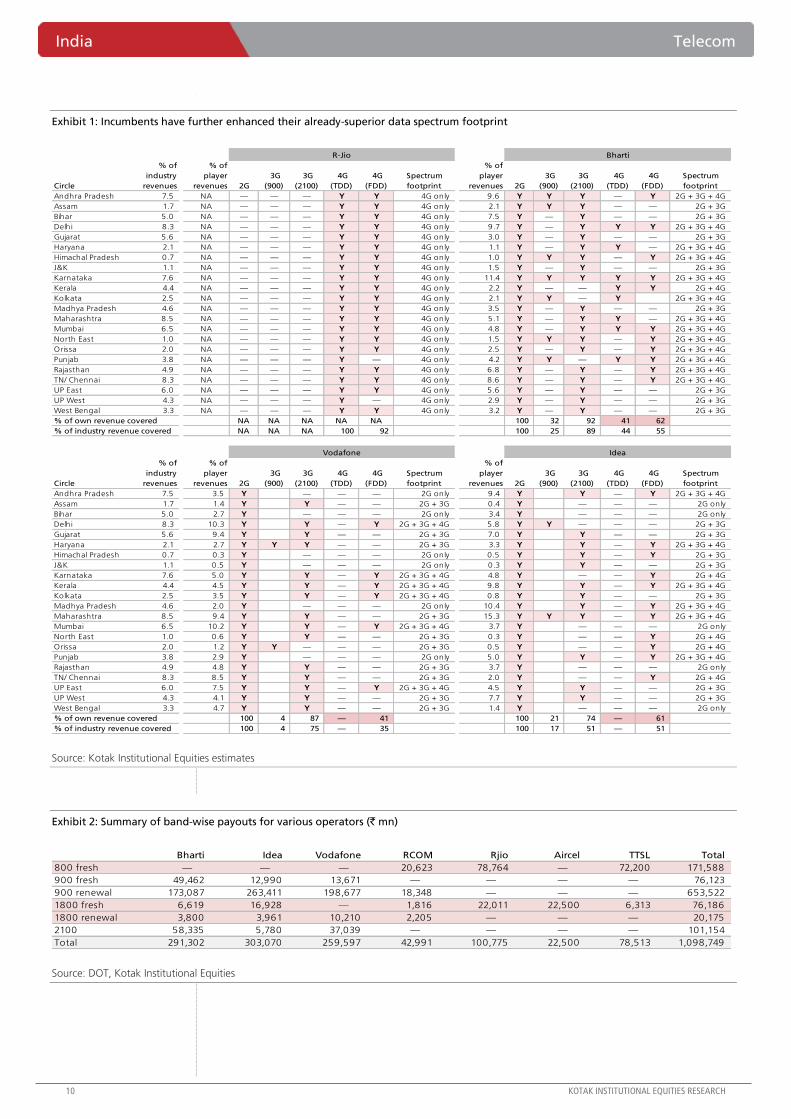

Incumbents now even better placed, spectrum-wise, to capture upside from

data (3G and 4G) growth

Exhibits 1 and 2 depict the spectrum footprint of R-Jio, Bharti, Vodafone, and Idea after

these auctions. While R-Jio has now broadly completed its pan-India FD-LTE footprint to add

to its 2300 MHz TD-LTE footprint, we believe that the incumbents’ combination of 2G + 3G

+ 4G spectrums (different combinations in different circles for different incumbents) is

superior to R-Jio’s, and that incumbents are not likely to lose to R-Jio on this count. More

specifically:

Bharti’s 3G footprint (commercially launched + circles with the requisite spectrum) now

covers 98% of its revenues and its 4G (LTE) footprint covers 71%. The company does not

have any ‘2G only’ circles anymore and can offer mobile broadband in all its circles.

Idea: 3G footprint 80%, 4G footprint 61%; 5 2G-only circles contributing 13% to its

revenues.

Vodafone: 3G footprint 88%, 4G footprint 41%; six ‘2G-only circles’ contributing 12%

to its revenues.

Even as there are gaps in Vodafone’s and Idea’s footprint, what matters is data spectrum in

their leadership circles and on that count, we see almost no gaps. Bharti is placed extremely

well on this aspect.

We shall publish more thoughts and earnings revisions, if any, after hearing the

managements’ views on implications of these auctions

Our auction payout estimates were amongst the highest on the Street and the actual

outcome has turned out to be broadly in line with our expectations. Bharti’s auction payout

(aggregate) is about 30% higher than our estimate, but the company has achieved (almost)

pan-India 3G footprint and enhanced its 4G footprint; we were building in payouts towards

this in later years and to that extent, the additional payout only has a time-value impact.

Idea is hosting a call to discuss auction results and implications on Monday, March 30, 2015;

we expect to get Bharti’s views too and shall have a relook at our estimates after these

discussions.

We remain constructive on both Bharti and Idea and negative on RCOM. From a Bharti

Infratel standpoint, data footprint expansion will lead to higher loading revenues in the

future; however, (1) these are in our numbers, and (2) loading does not create material

value.

We have refrained from detailing auction results in words; a lot of charts follow that largely

convey the story.

India Telecom

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 1: Incumbents have further enhanced their already-superior data spectrum footprint

Source: Kotak Institutional Equities estimates

Exhibit 2: Summary of band-wise payouts for various operators (` mn)

Source: DOT, Kotak Institutional Equities

Circle

% of

industry

revenues

% of

player

revenues 2G

3G

(900)

3G

(2100)

4G

(TDD)

4G

(FDD)

Spectrum

footprint

% of

player

revenues 2G

3G

(900)

3G

(2100)

4G

(TDD)

4G

(FDD)

Spectrum

footprint

Andhra Pradesh 7.5 NA — — — Y Y 4G only 9.6 Y Y Y — Y 2G + 3G + 4G

Assam 1.7 NA — — — Y Y 4G only 2.1 Y Y Y — — 2G + 3G

Bihar 5.0 NA — — — Y Y 4G only 7.5 Y — Y — — 2G + 3G

Delhi 8.3 NA — — — Y Y 4G only 9.7 Y — Y Y Y 2G + 3G + 4G

Gujarat 5.6 NA — — — Y Y 4G only 3.0 Y — Y — — 2G + 3G

Haryana 2.1 NA — — — Y Y 4G only 1.1 Y — Y Y — 2G + 3G + 4G

Himachal Pradesh 0.7 NA — — — Y Y 4G only 1.0 Y Y Y — Y 2G + 3G + 4G

J&K 1.1 NA — — — Y Y 4G only 1.5 Y — Y — — 2G + 3G

Karnataka 7.6 NA — — — Y Y 4G only 11.4 Y Y Y Y Y 2G + 3G + 4G

Kerala 4.4 NA — — — Y Y 4G only 2.2 Y — — Y Y 2G + 4G

Kolkata 2.5 NA — — — Y Y 4G only 2.1 Y Y — Y 2G + 3G + 4G

Madhya Pradesh 4.6 NA — — — Y Y 4G only 3.5 Y — Y — — 2G + 3G

Maharashtra 8.5 NA — — — Y Y 4G only 5.1 Y — Y Y — 2G + 3G + 4G

Mumbai 6.5 NA — — — Y Y 4G only 4.8 Y — Y Y Y 2G + 3G + 4G

North East 1.0 NA — — — Y Y 4G only 1.5 Y Y Y — Y 2G + 3G + 4G

Orissa 2.0 NA — — — Y Y 4G only 2.5 Y — Y — Y 2G + 3G + 4G

Punjab 3.8 NA — — — Y — 4G only 4.2 Y Y — Y Y 2G + 3G + 4G

Rajasthan 4.9 NA — — — Y Y 4G only 6.8 Y — Y — Y 2G + 3G + 4G

TN/ Chennai 8.3 NA — — — Y Y 4G only 8.6 Y — Y — Y 2G + 3G + 4G

UP East 6.0 NA — — — Y Y 4G only 5.6 Y — Y — — 2G + 3G

UP West 4.3 NA — — — Y — 4G only 2.9 Y — Y — — 2G + 3G

West Bengal 3.3 NA — — — Y Y 4G only 3.2 Y — Y — — 2G + 3G

% of own revenue covered NA NA NA NA NA 100 32 92 41 62

% of industry revenue covered NA NA NA 100 92 100 25 89 44 55

Circle

% of

industry

revenues

% of

player

revenues 2G

3G

(900)

3G

(2100)

4G

(TDD)

4G

(FDD)

Spectrum

footprint

% of

player

revenues 2G

3G

(900)

3G

(2100)

4G

(TDD)

4G

(FDD)

Spectrum

footprint

Andhra Pradesh 7.5 3.5 Y — — — 2G only 9.4 Y Y — Y 2G + 3G + 4G

Assam 1.7 1.4 Y Y — — 2G + 3G 0.4 Y — — — 2G only

Bihar 5.0 2.7 Y — — — 2G only 3.4 Y — — — 2G only

Delhi 8.3 10.3 Y Y — Y 2G + 3G + 4G 5.8 Y Y — — — 2G + 3G

Gujarat 5.6 9.4 Y Y — — 2G + 3G 7.0 Y Y — — 2G + 3G

Haryana 2.1 2.7 Y Y Y — — 2G + 3G 3.3 Y Y — Y 2G + 3G + 4G

Himachal Pradesh 0.7 0.3 Y — — — 2G only 0.5 Y Y — Y 2G + 3G

J&K 1.1 0.5 Y — — — 2G only 0.3 Y Y — — 2G + 3G

Karnataka 7.6 5.0 Y Y — Y 2G + 3G + 4G 4.8 Y — — Y 2G + 4G

Kerala 4.4 4.5 Y Y — Y 2G + 3G + 4G 9.8 Y Y — Y 2G + 3G + 4G

Kolkata 2.5 3.5 Y Y — Y 2G + 3G + 4G 0.8 Y Y — — 2G + 3G

Madhya Pradesh 4.6 2.0 Y — — — 2G only 10.4 Y Y — Y 2G + 3G + 4G

Maharashtra 8.5 9.4 Y Y — — 2G + 3G 15.3 Y Y Y — Y 2G + 3G + 4G

Mumbai 6.5 10.2 Y Y — Y 2G + 3G + 4G 3.7 Y — — — 2G only

North East 1.0 0.6 Y Y — — 2G + 3G 0.3 Y — — Y 2G + 4G

Orissa 2.0 1.2 Y Y — — — 2G + 3G 0.5 Y — — Y 2G + 4G

Punjab 3.8 2.9 Y — — — 2G only 5.0 Y Y — Y 2G + 3G + 4G

Rajasthan 4.9 4.8 Y Y — — 2G + 3G 3.7 Y — — — 2G only

TN/ Chennai 8.3 8.5 Y Y — — 2G + 3G 2.0 Y — — Y 2G + 4G

UP East 6.0 7.5 Y Y — Y 2G + 3G + 4G 4.5 Y Y — — 2G + 3G

UP West 4.3 4.1 Y Y — — 2G + 3G 7.7 Y Y — — 2G + 3G

West Bengal 3.3 4.7 Y Y — — 2G + 3G 1.4 Y — — — 2G only

% of own revenue covered 100 4 87 — 41 100 21 74 — 61

% of industry revenue covered 100 4 75 — 35 100 17 51 — 51

R-Jio Bharti

Vodafone Idea

Bharti Idea Vodafone RCOM Rjio Aircel TTSL Total

800 fresh — — — 20,623 78,764 — 72,200 171,588

900 fresh 49,462 12,990 13,671 — — — — 76,123

900 renewal 173,087 263,411 198,677 18,348 — — — 653,522

1800 fresh 6,619 16,928 — 1,816 22,011 22,500 6,313 76,186

1800 renewal 3,800 3,961 10,210 2,205 — — — 20,175

2100 58,335 5,780 37,039 — — — — 101,154

Total 291,302 303,070 259,597 42,991 100,775 22,500 78,513 1,098,749

Telecom India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Exhibit 3: 900 MHz spectrum renewal summary

Source: DOT, Kotak Institutional Equities

Exhibit 4: Results of the 800 MHz spectrum auction (MHz)

Source: DOT, Kotak Institutional Equities

Up for renewal (MHz) Post auction holding (MHz)

Bharti

Andhra Pradesh 7.8 9.0

Himachal Pradesh 6.2 7.4

Karnataka 7.8 8.8

North East 4.4 8.8

Punjab 7.8 10.0

Rajasthan 6.2 6.0

Idea

Andhra Pradesh 6.2 5.0

Gujarat 6.2 5.0

Haryana 6.2 6.0

Karnataka 6.2 5.0

Kerala 6.2 6.0

Madhya Pradesh 6.2 7.4

Maharashtra 7.8 9.0

Punjab 7.8 5.6

UP (West) 6.2 5.0

Vodafone

Gujarat 7.8 6.0

Haryana 6.2 6.2

Kerala 6.2 6.4

Maharashtra 6.2 5.0

Rajasthan 6.2 6.4

UP (East) 6.2 5.6

RCOM

Assam 6.2 —

Bihar 6.2 —

Himachal Pradesh 6.2 5.0

Madhya Pradesh 6.2 5.0

North East 4.4 —

Orissa 6.2 —

West Bengal 4.4 —

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

spectrum

Total

payout

Clearing

price (Rs

mn/MHz)

Reserve

price (Rs

mn/MHz)

Clearing/

Reserve

(X)

Metros

Delhi 1.25 1.25 10,596 8,477 6,170 1.37

Mumbai 5.00 2.50 7.50 54,562 7,275 4,390 1.66

Kolkata 1.25 1.25 1,838 1,470 1,470 1.00

A circles

Andhra Pradesh 3.75 3.75 22,724 6,060 2,340 2.59

Gujarat 2.50 2.50 6,944 2,777 2,750 1.01

Karnataka - - 3,030 3,030 1.00

Maharashtra 2.50 2.50 19,985 7,994 3,390 2.36

Tamilnadu - - 3,600 3,600 1.00

B circles

Haryana 5.00 1.25 1.25 7.50 4,243 566 380 1.49

Kerala

Madhya Pradesh 5.00 5.00 20,420 4,084 910 4.49

Punjab 2.50 2.50 2,146 858 850 1.01

Rajasthan

UP east 3.75 3.75 5,025 1,340 1,340 1.00

UP west 1.25 1.25 1,188 950 950 1.00

West Bengal 1.25 1.25 713 570 570 1.00

C circles

Assam 5.00 5.00 10.00 8,222 822 280 2.94

Bihar 5.00 5.00 4,292 858 850 1.01

Himachal Pradesh 5.00 2.50 7.50 1,468 196 190 1.03

North East 5.00 5.00 10.00 2,538 254 110 2.31

Orissa 5.00 1.25 6.25 2,565 410 380 1.08

J&K 5.00 2.50 7.50 2,121 283 280 1.01

Total quantum operatorwise - - - 48.75 26.25 11.25 - - 86 171,588 51,875 34,230 1.52

# of circles won - - - 10 11 5 - - 18

No Auction

No Auction

India Telecom

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 5: Results of the 800 MHz spectrum auction (` mn)

Source: DOT, Kotak Institutional Equities

Exhibit 6: Results of the 900 MHz spectrum auction (MHz)

Source: DOT, Kotak Institutional Equities

Rs mn Bharti Vodafone Idea Reliance Jio RCOM TTSL Aircel Telenor

Total

payout

Metros

Delhi - - - - - 10,596 - - 10,596

Mumbai - - - 36,375 - 18,187 - - 54,562

Kolkata - - - - 1,838 - - - 1,838

A circles

Andhra Pradesh - - - - - 22,724 - - 22,724

Gujarat - - - - 6,944 - - - 6,944

Karnataka - - - - - - - - -

Maharashtra - - - - - 19,985 - - 19,985

Tamilnadu - - - - - - - - -

B circles

Haryana - - - 2,828 707 707 - - 4,243

Kerala

Madhya Pradesh - - - 20,420 - - - - 20,420

Punjab - - - - 2,146 - - - 2,146

Rajasthan

UP east - - - 5,025 - - - - 5,025

UP west - - - - 1,188 - - - 1,188

West Bengal - - - - 713 - - - 713

C circles

Assam - - - 4,111 4,111 - - - 8,222

Bihar - - - 4,292 - - - - 4,292

Himachal Pradesh - - - 978 489 - - - 1,468

North East - - - 1,269 1,269 - - - 2,538

Orissa - - - 2,052 513 - - - 2,565

J&K - - - 1,414 707 - - - 2,121

Total payout - operatorwise - - - 78,764.2 20,623.2 72,200.3 - - 171,588

# of circles won - - - 10 11 5 - - 18

No Auction

No Auction

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

spectrum

Total

payout

Clearing

price (Rs

mn/MHz)

Reserve

price (Rs

mn/MHz)

Clearing/

Reserve

(X)

Metros

Delhi

Mumbai

Kolkata

A circles

Andhra Pradesh 9.00 5.00 14.0 95,305 6,808 4,590 1.48

Gujarat 6.00 5.00 11.0 74,030 6,730 4,240 1.59

Karnataka 8.80 5.00 13.8 76,935 5,575 3,700 1.51

Maharashtra 5.00 9.00 14.0 108,220 7,730 5,250 1.47

Tamilnadu

B circles

Haryana 6.20 6.00 12.2 18,446 1,512 760 1.99

Kerala 6.40 6.00 12.4 45,806 3,694 1,680 2.20

Madhya Pradesh 7.40 5.00 12.4 38,378 3,095 1,750 1.77

Punjab 10.00 5.60 15.6 56,277 3,608 1,510 2.39

Rajasthan 6.00 6.40 12.4 87,873 7,087 1,970 3.60

UP east 5.60 5.6 43,434 7,756 2,280 3.40

UP west 5.00 5.0 36,928 7,386 1,700 4.34

West Bengal 2.20 2.20 4.4 9,130 2,075 1,110 1.87

C circles

Assam 6.20 6.2 11,467 1,850 740 2.50

Bihar 1.60 1.6 7,109 4,443 1,480 3.00

Himachal Pradesh 7.40 5.00 12.4 7,124 575 270 2.13

North East 8.80 8.8 4,567 519 290 1.79

Orissa 1.20 5.00 6.2 8,618 1,390 670 2.07

J&K

Total payout - operatorwise 61.20 42.80 54.00 - 10.00 - - - 168 729,645 71,830 33,990

# of circles won 10 8 9 - 2 - - - 17

No Auction

No Auction

No Auction

No Auction

No Auction

Telecom India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

Exhibit 7: Results of the 900 MHz spectrum auction (` mn)

Source: DOT, Kotak Institutional Equities

Exhibit 8: Results of the 1800 MHz spectrum auction (MHz)

Source: DOT, Kotak Institutional Equities

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

payout

Metros

Delhi

Mumbai

Kolkata

A circles

Andhra Pradesh 61,268 - 34,038 - - - - - 95,305

Gujarat - 40,380 33,650 - - - - - 74,030

Karnataka 49,060 - 27,875 - - - - - 76,935

Maharashtra - 38,650 69,570 - - - - - 108,220

Tamilnadu

B circles

Haryana - 9,374 9,072 - - - - - 18,446

Kerala - 23,642 22,164 - - - - - 45,806

Madhya Pradesh - - 22,903 - 15,475 - - - 38,378

Punjab 36,075 - 20,202 - - - - - 56,277

Rajasthan 42,519 45,354 - - - - - - 87,873

UP east - 43,434 - - - - - - 43,434

UP west - - 36,928 - - - - - 36,928

West Bengal 4,565 4,565 - - - - - - 9,130

C circles

Assam 11,467 - - - - - - - 11,467

Bihar 7,109 - - - - - - - 7,109

Himachal Pradesh 4,251 - - - 2,873 - - - 7,124

North East 4,567 - - - - - - - 4,567

Orissa 1,668 6,950 - - - - - - 8,618

J&K

Total payout - operatorwise 222,549 212,348 276,401 - 18,348 - - - 729,645

# of circles won 10 8 9 - 2 - - - 17

No Auction

No Auction

No Auction

No Auction

No Auction

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

spectrum

Total

payout

Clearing

price (Rs

mn/MHz)

Reserve

price (Rs

mn/MHz)

Clearing/

Reserve

(X)

Metros

Delhi

Mumbai

Kolkata 2.00 5.00 7.0 10,437 1,491 730 2.04

A circles

Andhra Pradesh 1.20 2.60 3.8 9,226 2,428 1,690 1.44

Gujarat 3.40 3.4 8,092 2,380 2,380 1.00

Karnataka 1.00 0.60 1.6 2,960 1,850 1,850 1.00

Maharashtra

Tamilnadu 6.40 0.60 10 17.0 38,250 2,250 2,250 1.00

B circles

Haryana 3.40 4.00 0.60 8.0 3,728 466 320 1.46

Kerala 1.00 1.0 835 835 750 1.11

Madhya Pradesh

Punjab 1.00 0.60 1.6 1,136 710 710 1.00

Rajasthan 10.00 10.0 7,275 728 600 1.21

UP east 1.20 3.00 4.2 4,492 1,070 970 1.10

UP west 2.20 2.2 2,111 960 950 1.01

West Bengal

C circles

Assam

Bihar - - 620 620 1.00

Himachal Pradesh 4.80 5.40 10.2 1,622 159 90 1.77

North East 1.60 1.00 5.00 7.6 836 110 110 1.00

Orissa 6.20 5.00 5.00 16.2 5,362 331 230 1.44

J&K

Total payout - operatorwise 15.40 5.60 20.40 28.00 11.80 2.60 10 - 93.8 96,362 16,386 14,250

# of circles won 6 3 6 6 5 1 1 - 14.0

No Auction

No Auction

No Auction

No Auction

No Auction

No Auction

No Auction

India Telecom

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 9: Results of the 1800 MHz spectrum auction (` mn)

Source: DOT, Kotak Institutional Equities

Exhibit 10: Results of the 2100 MHz spectrum auction (MHz)

Source: DOT, Kotak Institutional Equities

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total # of

blocks

Metros

Delhi

Mumbai

Kolkata 2,982 - - 7,455 - - - - 10,437

A circles

Andhra Pradesh 2,914 - - - - 6,313 - - 9,226

Gujarat - 8,092 - - - - - - 8,092

Karnataka - - 1,850 - 1,110 - - - 2,960

Maharashtra

Tamilnadu - - 14,400 1,350 - - 22,500 - 38,250

B circles

Haryana 1,584 - - 1,864 280 - - - 3,728

Kerala - 835 - - - - - - 835

Madhya Pradesh

Punjab 710 - - - 426 - - - 1,136

Rajasthan - - - 7,275 - - - - 7,275

UP east - 1,283 - 3,209 - - - - 4,492

UP west - - 2,111 - - - - - 2,111

West Bengal

C circles

Assam

Bihar - - - - - - - - -

Himachal Pradesh - - 763 859 - - - - 1,622

North East 176 - 110 - 550 - - - 836

Orissa 2,052 - 1,655 - 1,655 - - - 5,362

J&K

Total payout - operatorwise 10,418.20 10,209.90 20,889.10 22,011.10 4,020.60 6,312.80 22,500 - 96,362

# of circles won 6 3 6 6 5 1 1 - 14

No Auction

No Auction

No Auction

No Auction

No Auction

No Auction

No Auction

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

spectrum

Total

payout

Clearing

price (Rs

mn/MHz)

Reserve

price (Rs

mn/MHz)

Clearing/

Reserve

(X)

Metros

Delhi - - 6,630 6,630 1.00

Mumbai - - 6,490 6,490 1.00

Kolkata 5.0 5.0 5,780 1,156 1,090 1.06

A circles

Andhra Pradesh - - 2,750 2,750 1.00

Gujarat 5.0 5.0 12,900 2,580 2,580 1.00

Karnataka 5.0 5.0 16,424 3,285 3,220 1.02

Maharashtra 5.0 5.0 15,050 3,010 3,010 1.00

Tamilnadu 5.0 5.0 17,200 3,440 3,440 1.00

B circles

Haryana 5.0 5.0 2,300 460 460 1.00

Kerala 5.0 5.0 5,886 1,177 1,110 1.06

Madhya Pradesh 5.0 5.0 4,568 914 870 1.05

Punjab

Rajasthan 5.0 5.0 6,991 1,398 870 1.61

UP east 5.0 5.0 4,515 903 860 1.05

UP west 5.0 5.0 5,254 1,051 1,030 1.02

West Bengal

C circles

Assam 5.0 5.0 1,932 386 290 1.33

Bihar

Himachal Pradesh

North East 5.0 5.0 554 111 80 1.38

Orissa 5.0 5.0 1,803 361 330 1.09

J&K

Total payout - operatorwise 35.00 30.00 5.00 - - - - - 70.0 101,154 36,101 35,110

# of circles won 7 6 1 - - - - - 14

No Auction

No Auction

No Auction

No Auction

No Auction

Telecom India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Exhibit 11: Results of the 2100 MHz spectrum auction (` mn)

Source: DOT, Kotak Institutional Equities

Exhibit 12: Bharti - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

Rs mn Bharti Vodafone Idea

Reliance

Jio RCOM TTSL Aircel Telenor

Total

payout

Metros

Delhi - - - - - - - - -

Mumbai - - - - - - - - -

Kolkata - - 5,780 - - - - - 5,780

A circles

Andhra Pradesh - - - - - - - - -

Gujarat 12,900 - - - - - - - 12,900

Karnataka - 16,424 - - - - - - 16,424

Maharashtra 15,050 - - - - - - - 15,050

Tamilnadu 17,200 - - - - - - - 17,200

B circles

Haryana 2,300 - - - - - - - 2,300

Kerala - 5,886 - - - - - - 5,886

Madhya Pradesh 4,568 - - - - - - - 4,568

Punjab

Rajasthan - 6,991 - - - - - - 6,991

UP east 4,515 - - - - - - - 4,515

UP west - 5,254 - - - - - - 5,254

West Bengal

C circles

Assam - 1,932 - - - - - - 1,932

Bihar

Himachal Pradesh

North East - 554 - - - - - - 554

Orissa 1,803 - - - - - - - 1,803

J&K

Total payout - operatorwise 58,335 37,039 5,780 - - - - - 101,154

# of circles won 7 6 1 - - - - - 14

No Auction

No Auction

No Auction

No Auction

No Auction

900 MHz

1800

administered

1800

auctioned 2100 MHz 2300 MHz

900 MHz

administered

900 MHz

auctioned

1800

administered 1800 auctioned 2100 MHz 2300 MHz

Renewed circles

Delhi 6.0 — 7.0 5.0 20.0 — 6.0 — 7.0 5.0 20.0

Kolkata 7.0 — 5.0 — 20.0 — 7.0 — 7.0 — 20.0

Renewal circles

Andhra Pradesh 7.8 2.2 8.8 5.0 — — 9.0 — 10.0 5.0 —

Himachal Pradesh 6.2 — 10.2 5.0 — — 7.4 — 10.2 5.0 —

Karnataka 7.8 2.2 8.8 5.0 20.0 — 8.8 — 8.8 5.0 20.0

North East 4.4 1.8 7.0 5.0 — — 8.8 — 8.6 5.0 —

Punjab 7.8 — 8.2 — 20.0 — 10.0 — 9.2 — 20.0

Rajasthan 6.2 2.0 8.2 5.0 — — 6.0 — 8.2 5.0 —

Non-renewal circles

Assam 1.8 4.4 1.3 5.0 — 1.8 6.2 4.4 1.3 5.0 —

Bihar 6.2 3.0 — 5.0 — 6.2 1.6 3.0 — 5.0 —

Chennai/ TN — 9.2 5.0 5.0 — — — 9.2 5.0 10.0 —

Gujarat — 6.2 — — — — — 6.2 — 5.0 —

Haryana — 6.2 — — 20.0 — — 6.2 3.4 5.0 20.0

J&K 6.2 — 2.6 5.0 — 6.2 — — 2.6 5.0 —

Kerala — 6.2 5.0 — 20.0 — — 6.2 5.0 — 20.0

Madhya Pradesh — 8.0 5.8 — — — — 8.0 5.8 5.0 —

Maharashtra — 8.2 — — 20.0 — — 8.2 — 5.0 20.0

Mumbai 5.0 9.2 6.0 5.0 20.0 5.0 — 9.2 6.0 5.0 20.0

Orissa 6.2 1.8 5.0 — — 6.2 1.2 1.8 11.2 5.0 —

UP (East) 6.2 1.0 — — — 6.2 — 1.0 — 5.0 —

UP (West) — 6.2 — 5.0 — — — 6.2 — 5.0 —

West Bengal 4.4 1.8 4.4 5.0 — 4.4 2.2 1.8 4.4 5.0 —

Pre-auction Post-auction

India Telecom

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

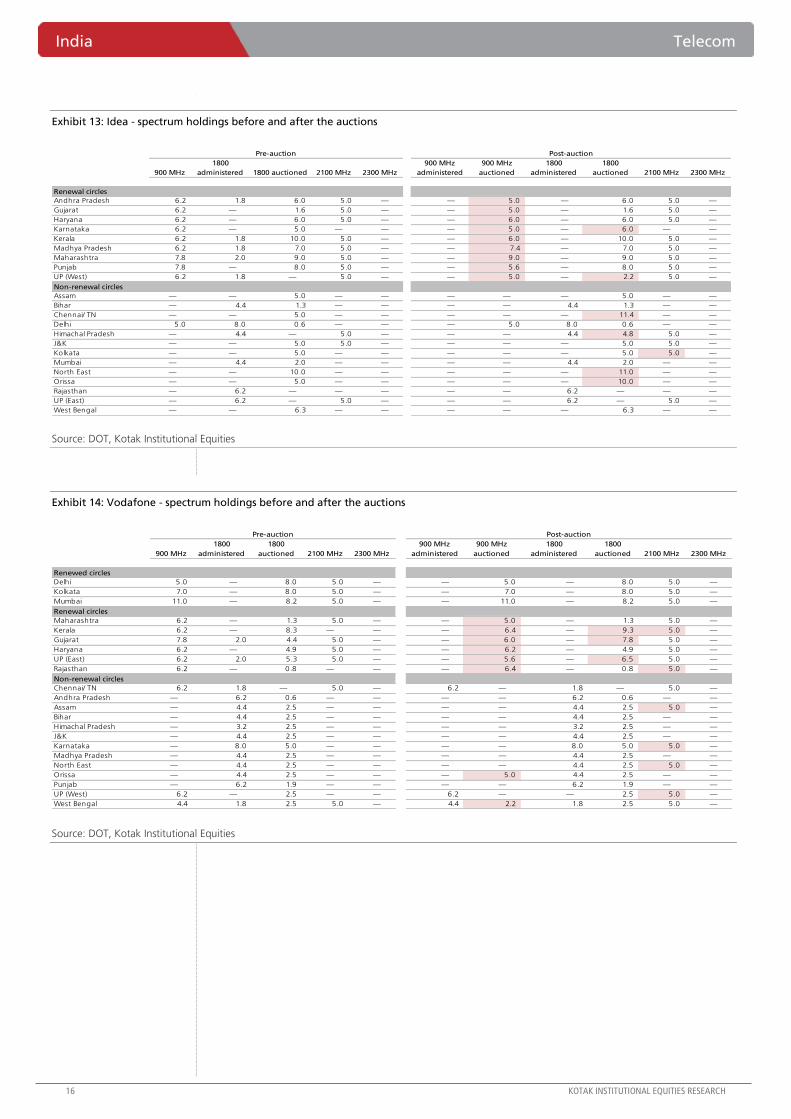

Exhibit 13: Idea - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

Exhibit 14: Vodafone - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

900 MHz

1800

administered 1800 auctioned 2100 MHz 2300 MHz

900 MHz

administered

900 MHz

auctioned

1800

administered

1800

auctioned 2100 MHz 2300 MHz

Renewal circles

Andhra Pradesh 6.2 1.8 6.0 5.0 — — 5.0 — 6.0 5.0 —

Gujarat 6.2 — 1.6 5.0 — — 5.0 — 1.6 5.0 —

Haryana 6.2 — 6.0 5.0 — — 6.0 — 6.0 5.0 —

Karnataka 6.2 — 5.0 — — — 5.0 — 6.0 — —

Kerala 6.2 1.8 10.0 5.0 — — 6.0 — 10.0 5.0 —

Madhya Pradesh 6.2 1.8 7.0 5.0 — — 7.4 — 7.0 5.0 —

Maharashtra 7.8 2.0 9.0 5.0 — — 9.0 — 9.0 5.0 —

Punjab 7.8 — 8.0 5.0 — — 5.6 — 8.0 5.0 —

UP (West) 6.2 1.8 — 5.0 — — 5.0 — 2.2 5.0 —

Non-renewal circles

Assam — — 5.0 — — — — — 5.0 — —

Bihar — 4.4 1.3 — — — — 4.4 1.3 — —

Chennai/ TN — — 5.0 — — — — — 11.4 — —

Delhi 5.0 8.0 0.6 — — — 5.0 8.0 0.6 — —

Himachal Pradesh — 4.4 — 5.0 — — — 4.4 4.8 5.0 —

J&K — — 5.0 5.0 — — — — 5.0 5.0 —

Kolkata — — 5.0 — — — — — 5.0 5.0 —

Mumbai — 4.4 2.0 — — — — 4.4 2.0 — —

North East — — 10.0 — — — — — 11.0 — —

Orissa — — 5.0 — — — — — 10.0 — —

Rajasthan — 6.2 — — — — — 6.2 — — —

UP (East) — 6.2 — 5.0 — — — 6.2 — 5.0 —

West Bengal — — 6.3 — — — — — 6.3 — —

Pre-auction Post-auction

900 MHz

1800

administered

1800

auctioned 2100 MHz 2300 MHz

900 MHz

administered

900 MHz

auctioned

1800

administered

1800

auctioned 2100 MHz 2300 MHz

Renewed circles

Delhi 5.0 — 8.0 5.0 — — 5.0 — 8.0 5.0 —

Kolkata 7.0 — 8.0 5.0 — — 7.0 — 8.0 5.0 —

Mumbai 11.0 — 8.2 5.0 — — 11.0 — 8.2 5.0 —

Renewal circles

Maharashtra 6.2 — 1.3 5.0 — — 5.0 — 1.3 5.0 —

Kerala 6.2 — 8.3 — — — 6.4 — 9.3 5.0 —

Gujarat 7.8 2.0 4.4 5.0 — — 6.0 — 7.8 5.0 —

Haryana 6.2 — 4.9 5.0 — — 6.2 — 4.9 5.0 —

UP (East) 6.2 2.0 5.3 5.0 — — 5.6 — 6.5 5.0 —

Rajasthan 6.2 — 0.8 — — — 6.4 — 0.8 5.0 —

Non-renewal circles

Chennai/ TN 6.2 1.8 — 5.0 — 6.2 — 1.8 — 5.0 —

Andhra Pradesh — 6.2 0.6 — — — — 6.2 0.6 — —

Assam — 4.4 2.5 — — — — 4.4 2.5 5.0 —

Bihar — 4.4 2.5 — — — — 4.4 2.5 — —

Himachal Pradesh — 3.2 2.5 — — — — 3.2 2.5 — —

J&K — 4.4 2.5 — — — — 4.4 2.5 — —

Karnataka — 8.0 5.0 — — — — 8.0 5.0 5.0 —

Madhya Pradesh — 4.4 2.5 — — — — 4.4 2.5 — —

North East — 4.4 2.5 — — — — 4.4 2.5 5.0 —

Orissa — 4.4 2.5 — — — 5.0 4.4 2.5 — —

Punjab — 6.2 1.9 — — — — 6.2 1.9 — —

UP (West) 6.2 — 2.5 — — 6.2 — — 2.5 5.0 —

West Bengal 4.4 1.8 2.5 5.0 — 4.4 2.2 1.8 2.5 5.0 —

Pre-auction Post-auction

Telecom India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

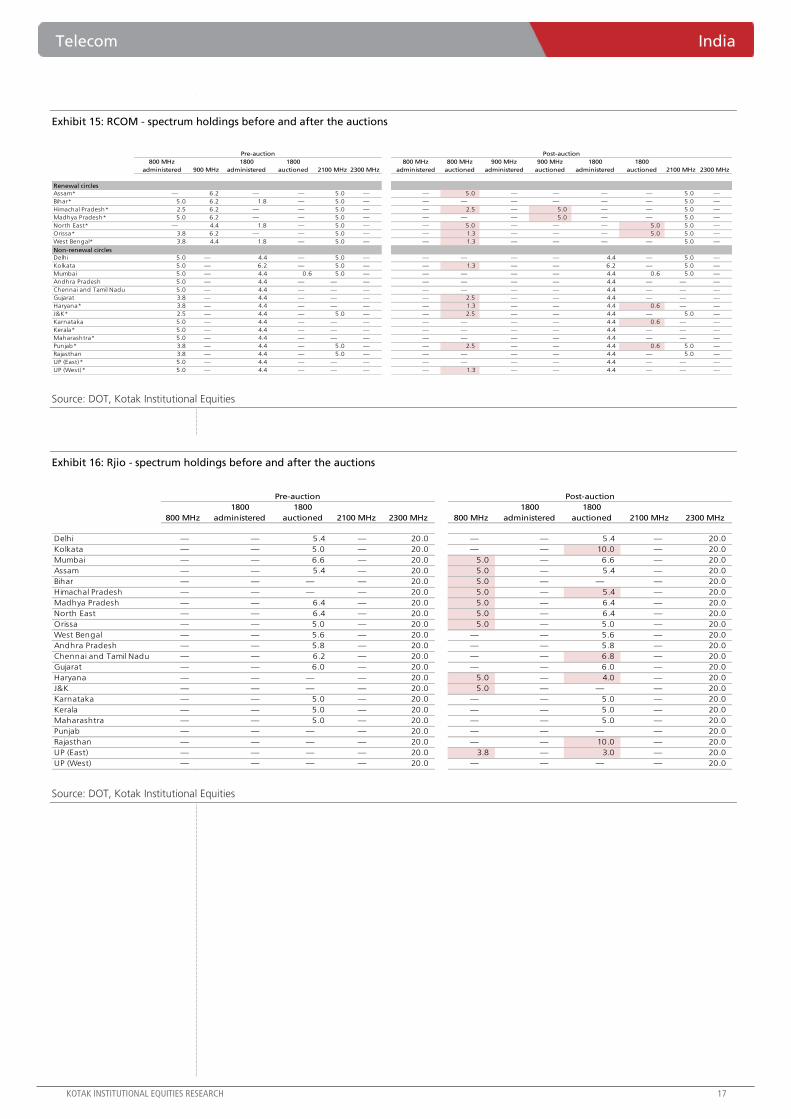

Exhibit 15: RCOM - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

Exhibit 16: Rjio - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

800 MHz

administered 900 MHz

1800

administered

1800

auctioned 2100 MHz 2300 MHz

800 MHz

administered

800 MHz

auctioned

900 MHz

administered

900 MHz

auctioned

1800

administered

1800

auctioned 2100 MHz 2300 MHz

Renewal circles

Assam* — 6.2 — — 5.0 — — 5.0 — — — — 5.0 —

Bihar* 5.0 6.2 1.8 — 5.0 — — — — — — — 5.0 —

Himachal Pradesh* 2.5 6.2 — — 5.0 — — 2.5 — 5.0 — — 5.0 —

Madhya Pradesh* 5.0 6.2 — — 5.0 — — — — 5.0 — — 5.0 —

North East* — 4.4 1.8 — 5.0 — — 5.0 — — — 5.0 5.0 —

Orissa* 3.8 6.2 — — 5.0 — — 1.3 — — — 5.0 5.0 —

West Bengal* 3.8 4.4 1.8 — 5.0 — — 1.3 — — — — 5.0 —

Non-renewal circles

Delhi 5.0 — 4.4 — 5.0 — — — — — 4.4 — 5.0 —

Kolkata 5.0 — 6.2 — 5.0 — — 1.3 — — 6.2 — 5.0 —

Mumbai 5.0 — 4.4 0.6 5.0 — — — — — 4.4 0.6 5.0 —

Andhra Pradesh 5.0 — 4.4 — — — — — — — 4.4 — — —

Chennai and Tamil Nadu 5.0 — 4.4 — — — — — — — 4.4 — — —

Gujarat 3.8 — 4.4 — — — — 2.5 — — 4.4 — — —

Haryana* 3.8 — 4.4 — — — — 1.3 — — 4.4 0.6 — —

J&K* 2.5 — 4.4 — 5.0 — — 2.5 — — 4.4 — 5.0 —

Karnataka 5.0 — 4.4 — — — — — — — 4.4 0.6 — —

Kerala* 5.0 — 4.4 — — — — — — — 4.4 — — —

Maharashtra* 5.0 — 4.4 — — — — — — — 4.4 — — —

Punjab* 3.8 — 4.4 — 5.0 — — 2.5 — — 4.4 0.6 5.0 —

Rajasthan 3.8 — 4.4 — 5.0 — — — — — 4.4 — 5.0 —

UP (East)* 5.0 — 4.4 — — — — — — — 4.4 — — —

UP (West)* 5.0 — 4.4 — — — — 1.3 — — 4.4 — — —

Post-auctionPre-auction

800 MHz

1800

administered

1800

auctioned 2100 MHz 2300 MHz 800 MHz

1800

administered

1800

auctioned 2100 MHz 2300 MHz

Delhi — — 5.4 — 20.0 — — 5.4 — 20.0

Kolkata — — 5.0 — 20.0 — — 10.0 — 20.0

Mumbai — — 6.6 — 20.0 5.0 — 6.6 — 20.0

Assam — — 5.4 — 20.0 5.0 — 5.4 — 20.0

Bihar — — — — 20.0 5.0 — — — 20.0

Himachal Pradesh — — — — 20.0 5.0 — 5.4 — 20.0

Madhya Pradesh — — 6.4 — 20.0 5.0 — 6.4 — 20.0

North East — — 6.4 — 20.0 5.0 — 6.4 — 20.0

Orissa — — 5.0 — 20.0 5.0 — 5.0 — 20.0

West Bengal — — 5.6 — 20.0 — — 5.6 — 20.0

Andhra Pradesh — — 5.8 — 20.0 — — 5.8 — 20.0

Chennai and Tamil Nadu — — 6.2 — 20.0 — — 6.8 — 20.0

Gujarat — — 6.0 — 20.0 — — 6.0 — 20.0

Haryana — — — — 20.0 5.0 — 4.0 — 20.0

J&K — — — — 20.0 5.0 — — — 20.0

Karnataka — — 5.0 — 20.0 — — 5.0 — 20.0

Kerala — — 5.0 — 20.0 — — 5.0 — 20.0

Maharashtra — — 5.0 — 20.0 — — 5.0 — 20.0

Punjab — — — — 20.0 — — — — 20.0

Rajasthan — — — — 20.0 — — 10.0 — 20.0

UP (East) — — — — 20.0 3.8 — 3.0 — 20.0

UP (West) — — — — 20.0 — — — — 20.0

Pre-auction Post-auction

India Telecom

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

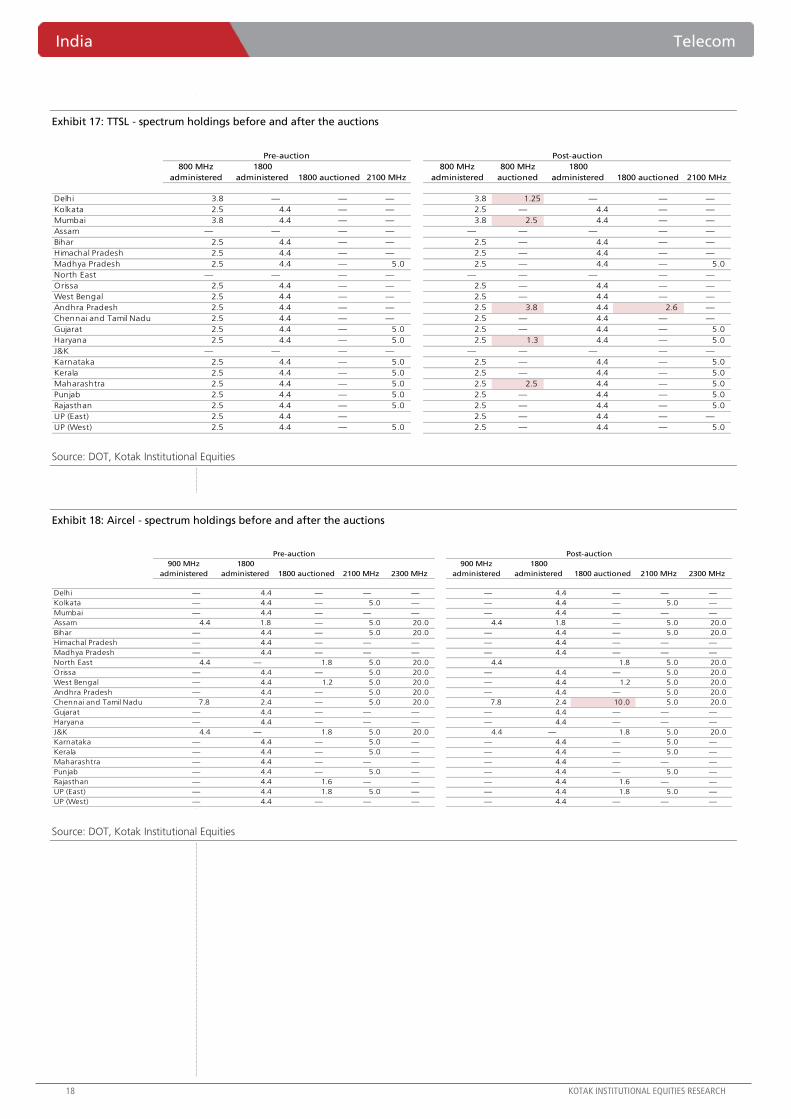

Exhibit 17: TTSL - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

Exhibit 18: Aircel - spectrum holdings before and after the auctions

Source: DOT, Kotak Institutional Equities

800 MHz

administered

1800

administered 1800 auctioned 2100 MHz

800 MHz

administered

800 MHz

auctioned

1800

administered 1800 auctioned 2100 MHz

Delhi 3.8 — — — 3.8 1.25 — — —

Kolkata 2.5 4.4 — — 2.5 — 4.4 — —

Mumbai 3.8 4.4 — — 3.8 2.5 4.4 — —

Assam — — — — — — — — —

Bihar 2.5 4.4 — — 2.5 — 4.4 — —

Himachal Pradesh 2.5 4.4 — — 2.5 — 4.4 — —

Madhya Pradesh 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

North East — — — — — — — — —

Orissa 2.5 4.4 — — 2.5 — 4.4 — —

West Bengal 2.5 4.4 — — 2.5 — 4.4 — —

Andhra Pradesh 2.5 4.4 — — 2.5 3.8 4.4 2.6 —

Chennai and Tamil Nadu 2.5 4.4 — — 2.5 — 4.4 — —

Gujarat 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

Haryana 2.5 4.4 — 5.0 2.5 1.3 4.4 — 5.0

J&K — — — — — — — — —

Karnataka 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

Kerala 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

Maharashtra 2.5 4.4 — 5.0 2.5 2.5 4.4 — 5.0

Punjab 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

Rajasthan 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

UP (East) 2.5 4.4 — 2.5 — 4.4 — —

UP (West) 2.5 4.4 — 5.0 2.5 — 4.4 — 5.0

Pre-auction Post-auction

900 MHz

administered

1800

administered 1800 auctioned 2100 MHz 2300 MHz

900 MHz

administered

1800

administered 1800 auctioned 2100 MHz 2300 MHz

Delhi — 4.4 — — — — 4.4 — — —

Kolkata — 4.4 — 5.0 — — 4.4 — 5.0 —

Mumbai — 4.4 — — — — 4.4 — — —

Assam 4.4 1.8 — 5.0 20.0 4.4 1.8 — 5.0 20.0

Bihar — 4.4 — 5.0 20.0 — 4.4 — 5.0 20.0

Himachal Pradesh — 4.4 — — — — 4.4 — — —

Madhya Pradesh — 4.4 — — — — 4.4 — — —

North East 4.4 — 1.8 5.0 20.0 4.4 1.8 5.0 20.0

Orissa — 4.4 — 5.0 20.0 — 4.4 — 5.0 20.0

West Bengal — 4.4 1.2 5.0 20.0 — 4.4 1.2 5.0 20.0

Andhra Pradesh — 4.4 — 5.0 20.0 — 4.4 — 5.0 20.0

Chennai and Tamil Nadu 7.8 2.4 — 5.0 20.0 7.8 2.4 10.0 5.0 20.0

Gujarat — 4.4 — — — — 4.4 — — —

Haryana — 4.4 — — — — 4.4 — — —

J&K 4.4 — 1.8 5.0 20.0 4.4 — 1.8 5.0 20.0

Karnataka — 4.4 — 5.0 — — 4.4 — 5.0 —

Kerala — 4.4 — 5.0 — — 4.4 — 5.0 —

Maharashtra — 4.4 — — — — 4.4 — — —

Punjab — 4.4 — 5.0 — — 4.4 — 5.0 —

Rajasthan — 4.4 1.6 — — — 4.4 1.6 — —

UP (East) — 4.4 1.8 5.0 — — 4.4 1.8 5.0 —

UP (West) — 4.4 — — — — 4.4 — — —

Pre-auction Post-auction

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Indian room air-conditioning industry is poised for steady growth

The Indian room air-conditioning (AC) industry is poised to grow steadily given (1) increasing push

towards higher urbanization, (2) a growing middle class and increase in discretionary spending,

(3) easy availability of financing schemes, (4) climate across several Indian states is conducive to AC

demand, and (5) lower penetration of ACs than other home appliances and versus Asian peer

countries. We estimate a 13-15% volume CAGR over FY2015-20, which will lead to a per-year

sales volume of 5.5-6.3 mn in FY2020 versus 3.1 mn in FY2015; value growth will be US$2.7-3.0

bn in FY2020 versus US$1.4 bn in FY2015.

Competition – top eight players control >85% of the market share

There are around 32 players in the Indian room-AC market (Appendix 2), which may sound

worrisome from a competition standpoint; however, the top-eight players control >85% of the

market (Exhibit 5). Several new players continue to enter the market and smaller existing players

try to gain market share with little or no success. For established players, higher market share

supported by large distribution networks (>50% of the sales for Voltas and Blue Star come from

Tier 2-4 cities), strong brand names and quality products form a virtuous circle and become an

enduring advantage. In Exhibit 5, we spell out recent efforts by top-eight players to increase

market share.

Air-conditioning purchase—first-hand experience

We recently visited several local multi-brand outlets and found that (1) the multi-brand stores

typically offer around 10-15 brands (top-eight companies’ brands mostly find a place in these

stores while remaining companies’ brands are unevenly scattered across stores), (2) there can be

a sharp variance between the MRP prices, store prices and final negotiated prices (explained on

page 10 through some examples), (3) online prices are not always cheaper than physical store

ones, as we found out while purchasing an LG inverter AC, and (4) to reduce barriers for first-

time buyers, there were several easy-financing schemes offered through credit cards and NBFCs.

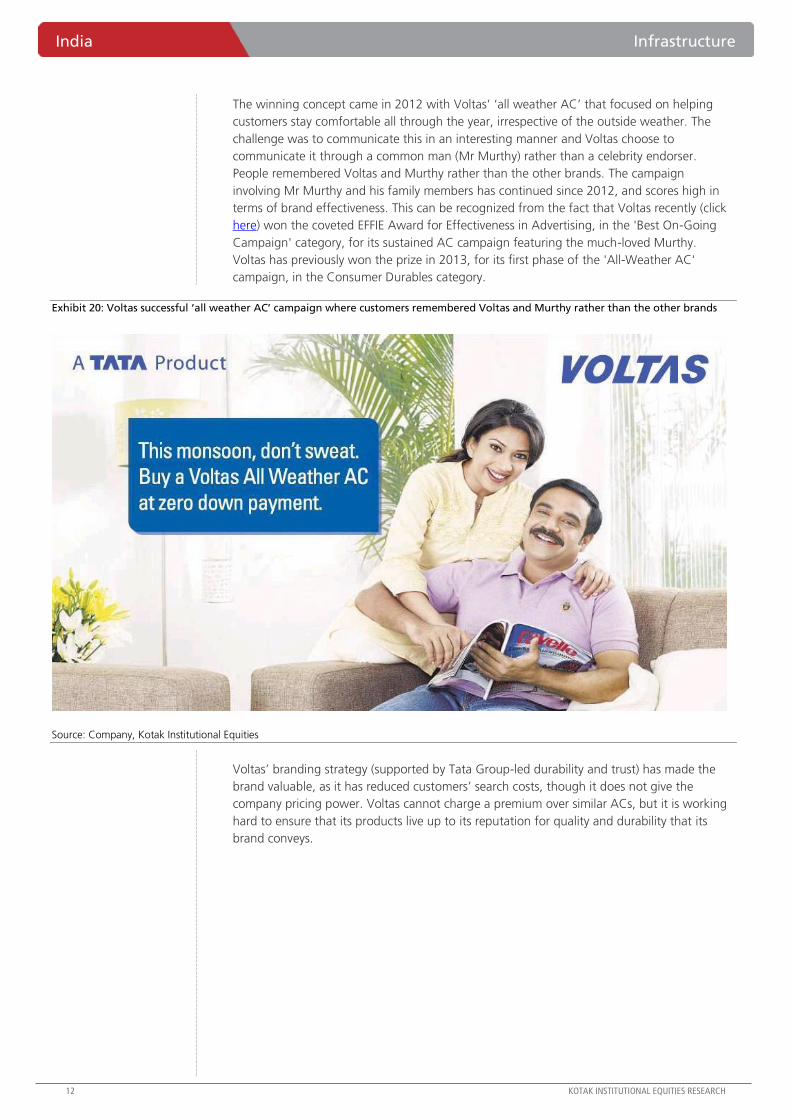

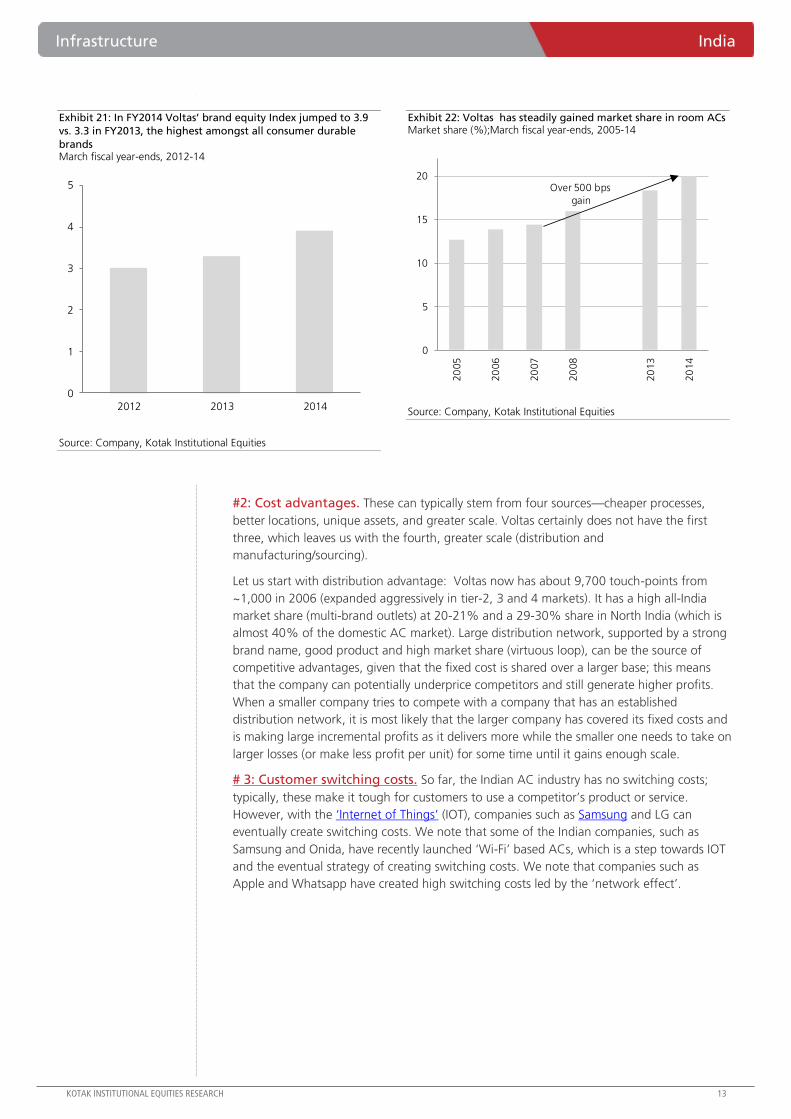

How Voltas gained market share in the past few years…

Voltas’ cooling products business gained market share (20-21% currently from lower double

digits in 2006) led by (1) its consumer-centric smart brand positioning and the trust factor that

comes from being a Tata brand, (2) its expanding distribution with about 9,700 touch-points

(highest reach in the category), and (3) its evolving model mix in terms of new technology,

features and price points.

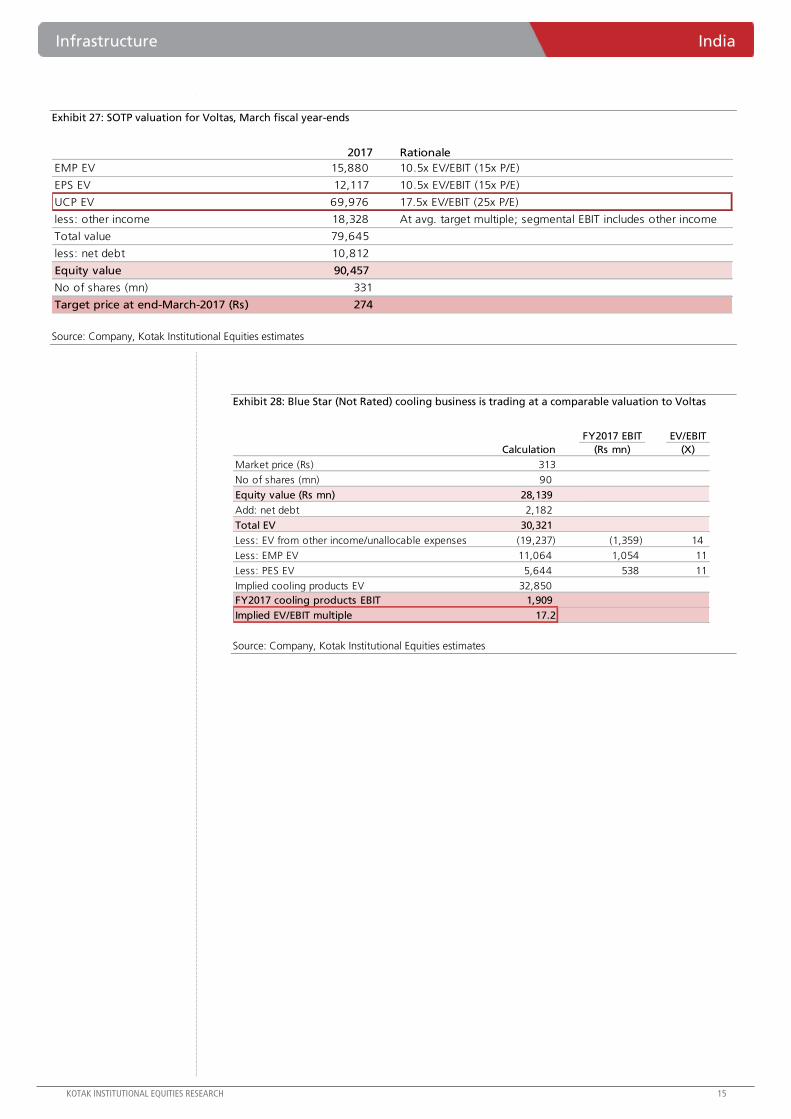

We increase Voltas’ target price to `275 (from `260 earlier) on rollover to March 2017

estimates. We have a REDUCE rating given little margin of safety at the CMP; implied

expectations factors (1) full recovery of its EMP business margin in FY2016-17 (we expect the

issue to persist longer than anticipated, as has been the case so far), and (2) cooling products

business trading at full valuations (Exhibit 27). If Voltas was a pure cooling-products business,

then we could have been more confident about the estimates and would have been

comfortable with slightly higher valuation than is reasonably warranted for higher longer-term

compounding.

Infrastructure India

Indian AC industry—bring on the heat. The Indian room AC industry is poised to

grow steadily—we estimate a 13-15% volume CAGR over FY2015-20. While 32 players

vying for the market share may sound worrisome from a competition standpoint, top

eight players controlling >85% of the market gives comfort. Voltas (REDUCE) and Blue

Star (Not Rated) are well known proxy plays for the sector’s growth, but fully valued at

their CMPs (Exhibits 27-28).

CAUTIOUS

MARCH 26, 2015

UPDATE

BSE-30: 28,112

India Infrastructure

2 KOTAK INSTITUTIONAL EQUITIES RESEARCH

INDIAN ROOM AIR CONDITIONING INDUSTRY: WELL-POISED FOR GROWTH

The Indian room AC industry is well-poised to grow steadily given (1) increasing push

towards higher urbanization (Exhibits 7-8), (2) a growing middle class and increase in

discretionary spending (Exhibit 9), (3) easy availability of financing schemes (Exhibits 10-11),

(4) climate across several Indian states conducive to AC demand, (5) lower penetration of

ACs relative to other home appliances (Exhibit 12), and (6) low penetration than in Asian

peer countries (Exhibit 13).

We estimate a 12.5-15.0% volume CAGR over FY2015-20, which will lead to per-year sales

volume of 5.5-6.3 mn in FY2020 versus 3.1 mn in FY2015 (Exhibit 1). Value growth will be

US$2.7-3 bn in FY2020 versus US$1.4 bn in FY2015 (Exhibit 2).

Exhibit 1: Air-conditioning volumes are likely to grow to >5 mn in FY2020 versus 3.1 mn in FY2015 Trend in volumes sales of air conditioners, March fiscal year-ends, 2000-2020E (mn units)

0.5

3.1

5.5

-10

0

10

20

30

40

0

1

2

3

4

5

6

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

Sales by volume (mn units) YoY growth (%)

12.5%

CAGR

12.5%

CAGR

15%

CAGR

6.3

10%

CAGR

Source: Industry, Kotak Institutional Equities estimates

Exhibit 2: Air-conditioning sales likely to grow to US$2.7-3 bn in FY2020 versus US$1.4 bn in FY2015 Trend in sales (by value of air conditioners, March fiscal year-ends, 2000-2020E (US$ mn)

-

500

1,000

1,500

2,000

2,500

3,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

Source: Industry, Kotak Institutional Equities estimates

Infrastructure India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

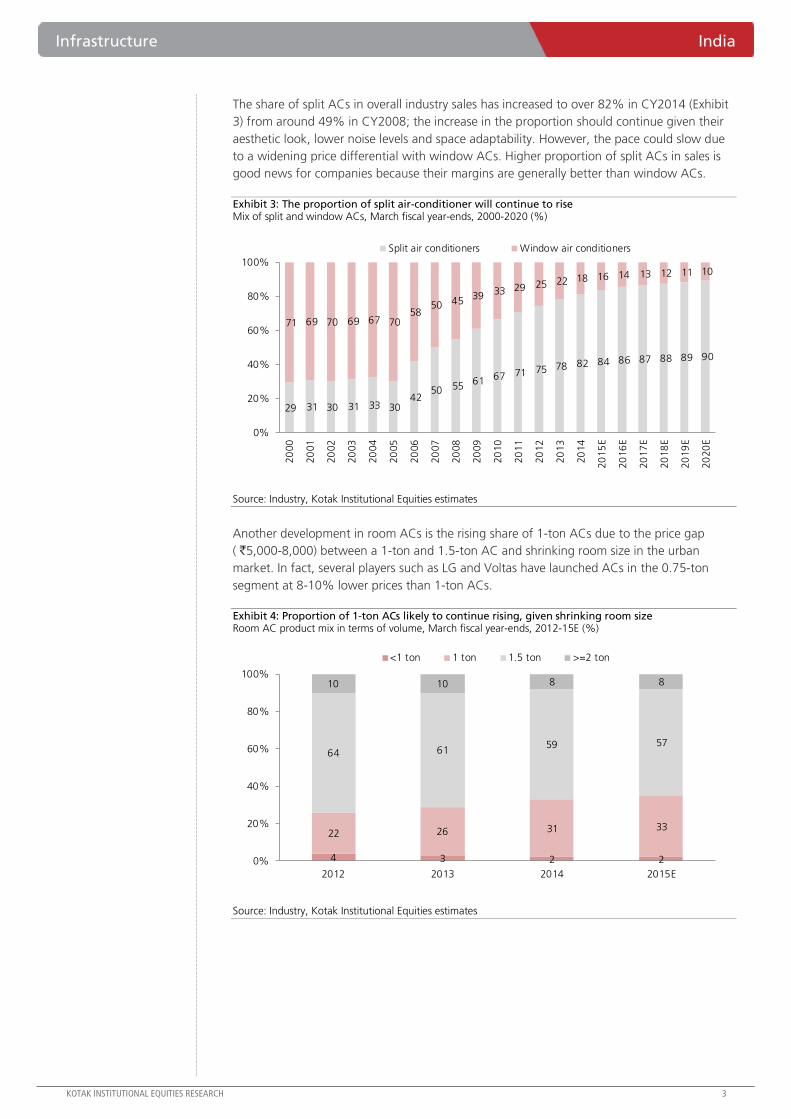

The share of split ACs in overall industry sales has increased to over 82% in CY2014 (Exhibit

3) from around 49% in CY2008; the increase in the proportion should continue given their

aesthetic look, lower noise levels and space adaptability. However, the pace could slow due

to a widening price differential with window ACs. Higher proportion of split ACs in sales is

good news for companies because their margins are generally better than window ACs.

Exhibit 3: The proportion of split air-conditioner will continue to rise Mix of split and window ACs, March fiscal year-ends, 2000-2020 (%)

29 31 30 31 33 30 42

50 55 61 67 71 75 78 82 84 86 87 88 89 90

71 69 70 69 67 70 58

50 45 39 33 29 25 22 18 16 14 13 12 11 10

0%

20%

40%

60%

80%

100%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

Split air conditioners Window air conditioners

Source: Industry, Kotak Institutional Equities estimates

Another development in room ACs is the rising share of 1-ton ACs due to the price gap

( `5,000-8,000) between a 1-ton and 1.5-ton AC and shrinking room size in the urban

market. In fact, several players such as LG and Voltas have launched ACs in the 0.75-ton

segment at 8-10% lower prices than 1-ton ACs.

Exhibit 4: Proportion of 1-ton ACs likely to continue rising, given shrinking room size Room AC product mix in terms of volume, March fiscal year-ends, 2012-15E (%)

4 3 2 2

22 26 31 33

64 6159 57

10 10 8 8

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015E

<1 ton 1 ton 1.5 ton >=2 ton

Source: Industry, Kotak Institutional Equities estimates

India Infrastructure

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Competition – top eight players control >85% of the market share

There are around 32 players in the Indian room AC market (Appendix 2), which may sound

worrisome from a competitive standpoint. However, the good part is that the top eight

players control >85% of the market share (Exhibit 5).

Several new players continue to enter the market and smaller existing players try to gain

market share with little or no success so far. This is because for established players large

distribution-led scale advantages support higher market share (>50% of the sales for Voltas

and Blue Star comes from Tier 2-4 cities); besides their strong brand names and quality

products form a virtuous circle and become a competitive advantage. As we explain below

(air-conditioning purchase – first-hand experience), this probably corroborates the thesis

that ‘nothing succeeds like success’ and implies that the smaller players have to work twice

as hard to gain share from larger players.

In Exhibit 5 details the top-eight players’ recent efforts to maintain or increase market share.

Exhibit 5: Top-eight players in the market have captured >85% market share AC players’ strategies to capture higher market share

Company Remarks Market share Dealers

Voltas # Recently introduced a ‘smart’ range of all-weather ACs, which allows users to keep track

of the amount of electricity guzzled by downloading an app called Voltas Remote

# Looking to diversify into new releated consumer product categories

# Export target of at least 100,000 units p.a over the next two years (10% of the annual

sales) vs. 25,000 to 30,000 units now

20-21% >6,500

LG India # Recently launched an innovative product; an inverter AC that can keep mosquitoes away!

It also has Himalaya cool and monsoon comfort technologies, geared for Indian

conditions

# Market share target of 25% in CY2015 with a turnover of Rs25bn, a growth of 25% yoy

(vs. 10-15% in last few years)

18-19% na

Samsung # Recently launched an innovative product; an inverter air conditioner that can also keep

mosquitoes away! It has also launched Himalaya cool and monsoon comfort

technologies, designed especially for Indian conditions

12-13% na

Hitachi # US-based Johnson Controls and Japanese Hitachi have entered into a global joint

venture (JV), which is going to have a bearing on the India business

# Hitachi Groups has increased its focus in India and plans to hire additonal 30%

employees to touch 13,000

9-10% 2,100

Daikin # Looking at setting up a second manufacturing plant to double its capacity as exisinting

plant at Neemrana running at >90% utilisation (further investment of Rs3.3 bn)

# Plan to sell 0.5mn ACs in FY16 vs. 0.425mn in FY15

# Moving from “prominence to dominance” in India by launching new technology;

looking for exports to Sri Lanka, Bangladesh

8-9% 2,650

Panasonic # Katrina Kaif is the brand ambassador. New campaign launched ( ‘need for more’),

positioning the product as a LifeConditioner

8-9% na

Videocon # Recently launched ‘Wi-Fi enabled’ AC range which can be controlled using a smartphone

app. Further investment planned at Rs1 bn.

# Wants to increase market share to 15% in an years' time from present ~8% and has

assigned Rs450 mn towards advertisment and Rs600mn towards R&D spends

7-8% 6,000

Blue Star # Looking at setting up an air-conditioner manufacturing facility in South India, having a

capacity of 500,000 units p.a (further investment of Rs1.5 bn)

# Targeting a market share of 10% in FY16 as compared to the current 8.5% in terms of

value; plans to spend Rs350mn of advertisment in the forthcoming summer season

7-8% 3,500

Source: Industry, media sources, Kotak Institutional Equities estimates

We note that of the 32 players offering ACs, only 17 offer window ACs while they all offer

split ACs (Appendix 2). LG is the leader in split ACs while Voltas is the market leader (by a

wide margin) in the window AC market. Hitachi has worked its way up in window ACs

while Samsung vacated the window AC market in FY2012.

Infrastructure India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

In Exhibit 6, we highlight key financial parameters of companies’ home appliances segment.

The operating margin and pre-tax RoCE data indicate that a price war is not likely to capture

higher market share, especially from MNC players.

Exhibit 6: MNCs’ financials indicate price-war is unlikely to capture market share Financials for home appliances segments of various AC companies, March fiscal year-ends, 2011-14

2011 2012 2013 2014

Revenue (Rs mn)

Samsung India (a) 35,246 34,753 36,806 51,958

Hitachi Home & Life Solutions (b) 7,640 7,981 9,300 10,997

Daikin Airconditioning India 6,974 11,962 16,037 18,204

Blue Star (c) 7,889 9,326 9,652 10,755

Voltas (d) 15,608 15,388 18,356 20,524

Whirlpool India (e) 27,028 26,579 27,727 28,346

Operating profit (Rs mn)

Samsung India (a) (1,103) (142) (635) (184)

Hitachi Home & Life Solutions (b) 634 300 480 533

Daikin Airconditioning India (274) 429 (126) (36)

Blue Star (c) 902 875 804 948

Voltas (d) 1,599 1,298 1,655 2,567

Whirlpool India (e) 2,191 1,734 1,617 1,477

Operating profit margin (%)

Samsung India (a) (3.1) (0.4) (1.7) (0.4)

Hitachi Home & Life Solutions (b) 8.3 3.8 5.2 4.8

Daikin Airconditioning India (3.9) 3.6 (0.8) (0.2)

Blue Star (c) 11.4 9.4 8.3 8.8

Voltas (d) 10.2 8.4 9.0 12.5

Whirlpool India (e) 8.1 6.5 5.8 5.2

Capital Employed (Rs mn)

Samsung India 10,333 8,731 7,301 7,344

Hitachi Home & Life Solutions 2,353 2,390 3,040 3,154

Daikin Airconditioning India 2,781 3,399 6,446 7,955

Blue Star 1,390 2,068 2,195 2,513

Voltas 1,908 1,903 2,371 2,747

Whirlpool India 5,026 5,299 5,911 5,799

Pre-tax ROCE (%)

Samsung India (a) (11) (2) (9) (3)

Hitachi Home & Life Solutions (b) 27 13 16 17

Daikin Airconditioning India (10) 13 (2) (0)

Blue Star (c) 65 42 37 38

Voltas (d) 84 68 70 93

Whirlpool India (e) 44 33 27 25

Notes:

(a) Numbers pertain to home appliances segment (washing machines, air-conditioners, refrigerators and

microwave ovens).

(b) Includes air-conditioners and refrigerators.

(c) Numbers pertain to cooling products segment (room air-conditioners, commercial refrigeration products &

systems).

(d) Numbers pertain to unitary cooling products segment (room air-conditioners, commercial refrigeration

products & systems).

(e) Numbers pertain to home appliances segment (washing machines, air-conditioners, refrigerators and

microwave ovens).

Source: Companies, Kotak Institutional Equities

Many macro factors support the longevity and durability of the ACs business in

India

We explain through Exhibits 7-16 how a plethora of factors supports the longevity and

durability of the ACs business in India.

India Infrastructure

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

A rising share of manufacturing GDP (to 25% over the next 10-15 years from current 16%)

will entail higher urbanization (Exhibits 7-8), as seen in China. The corollary is a growing

middle class and increase in discretionary spending (Exhibit 9), adequately supported by easy

availability of financing schemes (Exhibits 10-11). The room AC industry will clearly benefit

from these factors, which will also be supported by (1) low penetration levels in India than

other home appliances (Exhibit 12) and versus Asian peer countries (Exhibit 13) and

(2) climate across several Indian states being conductive to AC demand (Exhibit 14).

Exhibit 7: Urban population at 31% in India versus 51% in China Share of urban population in India and China, calendar year-ends 1987-2011 (%)

25

31

24

51

15

20

25

30

35

40

45

50

55

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

India China

Source: World Bank, Kotak Institutional Equities

Exhibit 8: Indian cities likely to house 40% population by 2030 Share of urban population in India, March fiscal- year-ends 1971-2030 (%)

10

15

20

25

30

35

40

45

300

500

700

900

1,100

1,300

1,500

1,700

1971 1981 1991 2001 2011 2030

Total population (mn) Urbanisation rate (%)

Source: Ministry of Urban Development, Kotak Institutional Equities

Exhibit 9: India will see a massive uptick in affluent households Distribution of Indian households by consumption expenditure, March fiscal year-ends, 2011-25E

2011 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Rural households (mn)

Real-rich — — — — — — — — — — — — — — —

Upper-class — — — — — — — — — — — — — — —

Prospering — — 1 2 3 4 5 6 7 8 9 10 12 13 14

Evolving 11 18 18 18 21 23 26 29 31 34 38 43 47.1 51 57

Emerging 51 70 77 84 88 91 96 100 104 107 109 110 111 112 111

Surviving 106 82 77 71 64 58 52 46 40 35 30 25 20 16 12

Total 169 170 172 174 175 177 179 181 183 184 186 188 190 192 194

Urban households (mn)

Real-rich — — — — — — — — — — — — — — 1

Upper-class — — 0 1 1 2 2 3 3 4 5 6 6 7 7

Prospering 6 9 9 9 10 12 13 14 16 17 19 20 21 24 27

Evolving 19 25 28 31 33 35 38 40 42 46 49 52 55 57 60

Emerging 38 40 42 43 43 44 45 45 46 46 46 45 44 42 41

Surviving 18 10 9 8 7 6 5 3 2 1 — — — — —

Total 81 84 88 91 95 98 102 106 110 114 118 122 126 131 135

Total households (mn)

Real-rich — — — — — — — — — — — — — — 1

Upper-class — — 0 1 1 2 2 3 3 4 5 6 6 7 7

Prospering 6 9 10 11 13 15 18 20 23 25 28 30 33 37 41

Evolving 30 43 46 48 54 59 64 68 74 79 87 95 102 109 117

Emerging 89 111 118 126 131 135 140 145 150 154 155 155 155 154 152

Surviving 124 92 86 78 71 64 57 50 43 36 30 25 20 16 12

Total 249 254 260 265 270 275 281 287 292 298 304 310 316 323 329

Source: Kotak Institutional Equities estimate

Infrastructure India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

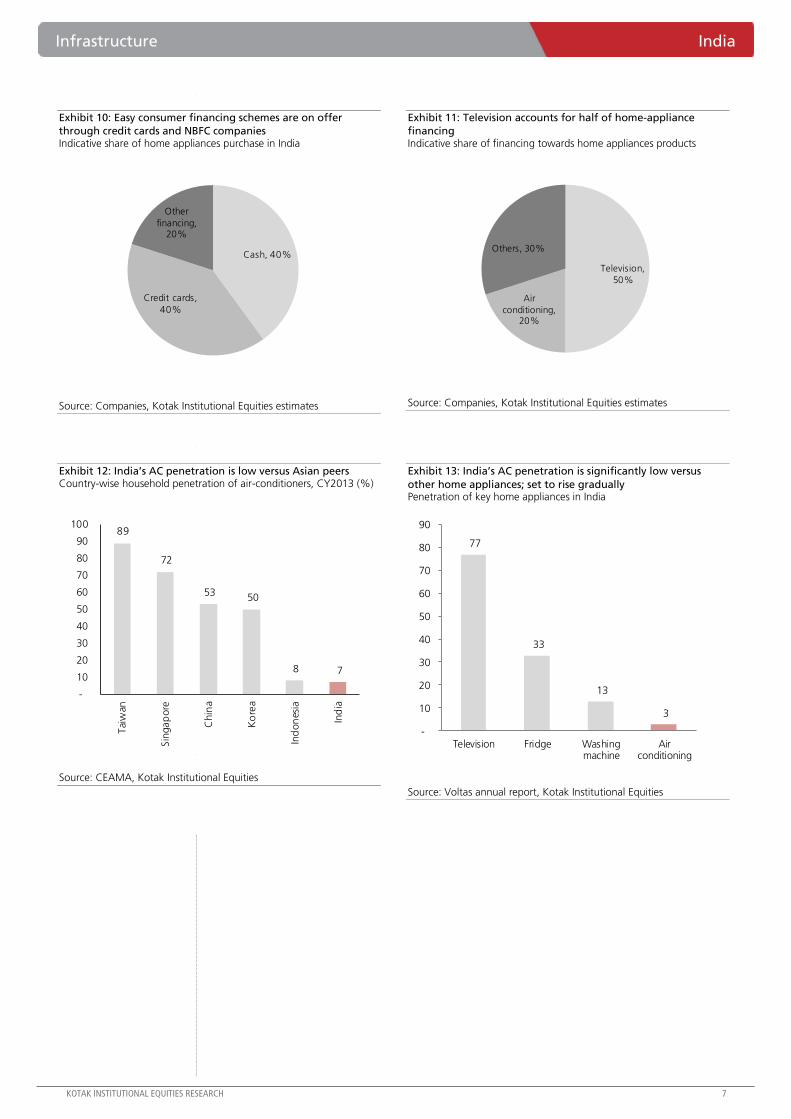

Exhibit 10: Easy consumer financing schemes are on offer

through credit cards and NBFC companies Indicative share of home appliances purchase in India

Cash, 40%

Credit cards,

40%

Other

financing, 20%

Source: Companies, Kotak Institutional Equities estimates

Exhibit 11: Television accounts for half of home-appliance

financing Indicative share of financing towards home appliances products

Television,

50%

Air

conditioning, 20%

Others, 30%

Source: Companies, Kotak Institutional Equities estimates

Exhibit 12: India’s AC penetration is low versus Asian peers Country-wise household penetration of air-conditioners, CY2013 (%)

89

72

53 50

8 7

-

10

20

30

40

50

60

70

80

90

100

Tai

wan

Sin

gap

ore

Chin

a

Ko

rea

Ind

on

esia

Ind

ia

Source: CEAMA, Kotak Institutional Equities

Exhibit 13: India’s AC penetration is significantly low versus

other home appliances; set to rise gradually Penetration of key home appliances in India

77

33

13

3

-

10

20

30

40

50

60

70

80

90

Television Fridge Washingmachine

Airconditioning

Source: Voltas annual report, Kotak Institutional Equities

India Infrastructure

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 14: A large part of India has temperatures that is suitable for AC installation Average annual temperatures and climatic zones in India

Source: Industry, Kotak Institutional Equities

Exhibit 15: ACs’ share among low versus other cooling products Cooling pyramid (Indian households in million)

Source: Symhony, Kotak Institutional Equities

Exhibit 16: Low penetration shows ample growth opportunity Penetration of air-conditioners versus other cooling products (%)

3

9

59

0

10

20

30

40

50

60

70

AC Air Cooler Fans

Source: Sympony, Kotak Institutional Equities

Air-coolers are appliances that can cool the room, but are not substitutes for air-conditioners

(Exhibit 17). Depending on the budget and preference, a person may opt to buy either a

cooler or an air-conditioner. Beyond initial capital cost, factors that may help in choosing the

right cooling product are recurring cost, cooling requirement, humidity level, space

constraint, impact of the appliance on the environment, etc.

AC 9.4

Air Cooler 24

No fans 82.6

Fans 164.1

Infrastructure India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

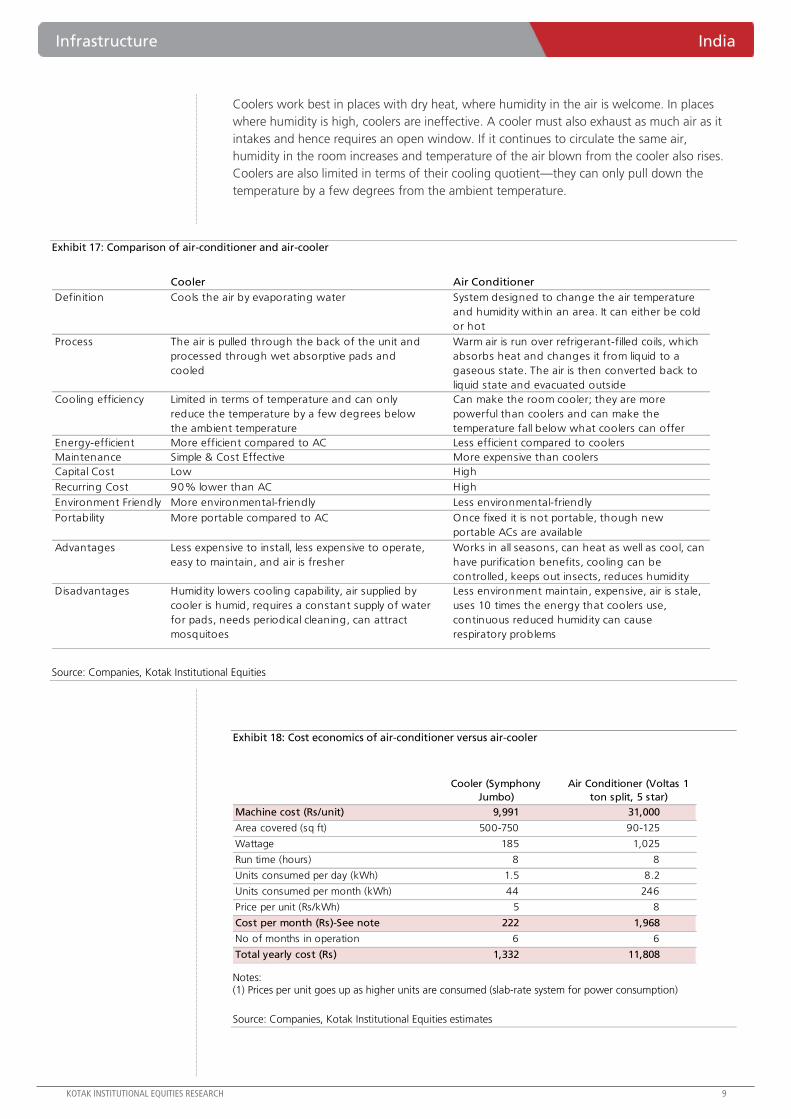

Coolers work best in places with dry heat, where humidity in the air is welcome. In places

where humidity is high, coolers are ineffective. A cooler must also exhaust as much air as it

intakes and hence requires an open window. If it continues to circulate the same air,

humidity in the room increases and temperature of the air blown from the cooler also rises.

Coolers are also limited in terms of their cooling quotient—they can only pull down the

temperature by a few degrees from the ambient temperature.

Exhibit 17: Comparison of air-conditioner and air-cooler

Cooler Air Conditioner

Definition Cools the air by evaporating water System designed to change the air temperature

and humidity within an area. It can either be cold

or hot

Process The air is pulled through the back of the unit and

processed through wet absorptive pads and

cooled

Warm air is run over refrigerant-filled coils, which

absorbs heat and changes it from liquid to a

gaseous state. The air is then converted back to

liquid state and evacuated outside

Cooling efficiency Limited in terms of temperature and can only

reduce the temperature by a few degrees below

the ambient temperature

Can make the room cooler; they are more

powerful than coolers and can make the

temperature fall below what coolers can offer

Energy-efficient More efficient compared to AC Less efficient compared to coolers

Maintenance Simple & Cost Effective More expensive than coolers

Capital Cost Low High

Recurring Cost 90% lower than AC High

Environment Friendly More environmental-friendly Less environmental-friendly

Portability More portable compared to AC Once fixed it is not portable, though new

portable ACs are available

Advantages Less expensive to install, less expensive to operate,

easy to maintain, and air is fresher

Works in all seasons, can heat as well as cool, can

have purification benefits, cooling can be