STRONG FUTURE.IMPROVING CAPITAL EFFICIENCIES.SOLID BALANCE SHEET.

MULTI-YEAR INVENTORY.

HIGHLIGHTS 04LETTER TO SHAREHOLDERS 08

RESERVES SUMMARY 12MANAGEMENT’S DISCUSSION AND ANALYSIS 19

INDEPENDENT AUDITORS’ REPORT 47FINANCIAL STATEMENTS 48

NOTES TO THE FINANCIAL STATEMENTS 52CORPORATE INFORMATION 76

DeeThree’s improved capital and operating efficiencies, strong balance sheet and massive inventory of

multi-zone drilling opportunities solidly position the Company to navigate through the current

commodity price weakness. DeeThree’s $160 million 2015 capital program will

increase average production to approximately 13,300 boe per day

while conserving the balance sheet and maintaining

financial flexibility.

ANNUAL REPORT2014

STRONG FUTURE.IMPROVING CAPITAL EFFICIENCIES.SOLID BALANCE SHEET.

MULTI-YEAR INVENTORY.

HIGHLIGHTS 04LETTER TO SHAREHOLDERS 08

RESERVES SUMMARY 12MANAGEMENT’S DISCUSSION AND ANALYSIS 19

INDEPENDENT AUDITORS’ REPORT 47FINANCIAL STATEMENTS 48

NOTES TO THE FINANCIAL STATEMENTS 52CORPORATE INFORMATION 76

DeeThree’s improved capital and operating efficiencies, strong balance sheet and massive inventory of

multi-zone drilling opportunities solidly position the Company to navigate through the current

commodity price weakness. DeeThree’s $160 million 2015 capital program will

increase average production to approximately 13,300 boe per day

while conserving the balance sheet and maintaining

financial flexibility.

ANNUAL REPORT2014

13Consecutive quarters of production growth through Q4 2014

39.4 Proved + probable reserves at year-end 2013

M I L L I O N B O E

51.8 FERGUSONProved + probable reserves at year-end 2014

M I L L I O N B O E

Gas injection EOR scheme mitigates declines and increases oil recoveries

Focused horizontal drilling in DeeThree Exploration Ltd.’s two core areas drove 58 percent year-over-year growth in average daily production, to 11,325 boe per day (80 percent oil and natural gas liquids) in 2014. Reducing technical risks and further refining our well drilling and completions processes improved per-well results and lifted operating netbacks. In 2014, DeeThree again recorded some of the best on-stream results for new oil wells drilled in western Canada. The average netback increased by over 12 percent, from $40.50 per boe in 2013 to $45.16 per boe in 2014, despite softening commodity prices toward year-end.

IMPROVING CAPITAL EFFICIENCIES

ALBERTA BAKKEN GAS INJECTION EOR SCHEME MODEL AREA

Oil Production (bbls/d) Gas Injection (mcf/d)

5,000 35

4,500

4,000

3,500

0 0

5005

1,000

101,500

152,000

20

Wel

l Cou

nt

2,500

25

3,000

30

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q4 2014Q3 2014 Q1 2015

1415

1617

1819

2021

2223

24

25

2627

28

29 29

13Consecutive quarters of production growth through Q4 2014

39.4 Proved + probable reserves at year-end 2013

M I L L I O N B O E

51.8 FERGUSONProved + probable reserves at year-end 2014

M I L L I O N B O E

Gas injection EOR scheme mitigates declines and increases oil recoveries

Focused horizontal drilling in DeeThree Exploration Ltd.’s two core areas drove 58 percent year-over-year growth in average daily production, to 11,325 boe per day (80 percent oil and natural gas liquids) in 2014. Reducing technical risks and further refining our well drilling and completions processes improved per-well results and lifted operating netbacks. In 2014, DeeThree again recorded some of the best on-stream results for new oil wells drilled in western Canada. The average netback increased by over 12 percent, from $40.50 per boe in 2013 to $45.16 per boe in 2014, despite softening commodity prices toward year-end.

IMPROVING CAPITAL EFFICIENCIES

ALBERTA BAKKEN GAS INJECTION EOR SCHEME MODEL AREA

Oil Production (bbls/d) Gas Injection (mcf/d)

5,000 35

4,500

4,000

3,500

0 0

5005

1,000

101,500

152,000

20

Wel

l Cou

nt

2,500

25

3,000

30

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q4 2014Q3 2014 Q1 2015

1415

1617

1819

2021

2223

24

25

2627

28

29 29

1

BRAZEAUSignificant pool extensions in the prolific Belly River C and D zones at Brazeau

New 12,000 bbl/d central oil battery improves operating efficiency

DTX .TO ANNUAL REPORT

2014

BRAZEAU BELLY RIVER – IMPROVING CAPITAL EFFICIENCIES

Drilling & Completion Costs ($ per boe/d of new production added*)

* Excludes tie-in costs

Average per well IP365 (boe/d)

50,000$

40,000

45,000

35,000

2012 2014 2015 Target2013

30,000

25,000

20,000

15,000

5,000

10,000

0

250

200

150

100

50

0

DTX .TO ANNUAL REPORT2014

2

A V E R A G E W E L L D R I L L E D A T B R A Z E A U I N 2 0 1 4 ( B O E / D )

B E S T W E L L A T B R A Z E A U I N 2 0 1 4 ( B O E / D )

672 30-day IP

1,24930-day IP

557 60-day IP

1,01460-day IP

90-day IP500

90-day IP900

HOW WE HAVE IMPROVED CAPITAL EFFICIENCIESImproved Per-Well Results: the Key to Capital and Operating EfficienciesDEETHREE MADE CAPITAL EFFICIENCIES A HIGH PRIORITY LONG BEFORE COMMODITY PRICES SOFTENED.

Seeking to build shareholder value for the long term, we worked hard to increase the reserves and production impact of each dollar of capital invested at both core areas. Many separate measures contributed. Longer-leg horizontal wells with more fracturing stages and heavier tonnage. Lowering geological risk as pool areas became delineated. State-of-the-art drilling tools to stay in the target reservoir and maximize the length of horizontal reservoir pay. Drilling multiple wells per pad to exploit common infrastructure.

THE RESULTS ARE CLEAR: HIGHER AVERAGE INITIAL PRODUCTIVITY PER WELL AND LOWER COST PER BOE OF DAILY PRODUCTION ADDED.

Brazeau Belly River SandsAt Brazeau, we completed numerous two-mile-long (or >10,000-foot) horizontal well legs in 2014, placing up to 950 tonnes of sand over 30 fracturing stages. We focused on increasing vertical fracture development to access geological

sub-units within the reservoir. To improve operating efficiency, we enlarged the central oil battery to 12,000 bbls per day capacity and completed a network of 8” gathering lines across the play.

We also found success through “exploration by development”, a low-risk tactic of pushing pool boundaries outward in small increments by drilling a long-leg horizontal well through a length of known pool area, then outward into an area without well control. DeeThree will pursue further capital and operating efficiencies in 2015, such as testing down-space drilling to eight wells per section of pool area, plus potentially drilling up to eight wells from a common pad.

Ferguson Upper Bakken SiltstoneIn Ferguson, a discovery well in 2014 extended the Upper Bakken pool by 7 miles to the southwest, setting up a new 30-section exploration area with minimal reserves booked at year-end 2014. Our primary focus at Ferguson in 2014 was to maximize the pool’s profitability and long-term resource recovery. The gas injection pressure maintenance scheme initiated in 2013 showed with very promising initial results, so in 2014 we expanded the program to three gas injection wells, high-pressure injection compression and flow lines.

BRAZEAU

DTX .TO ANNUAL REPORT

20143

25%Reduction in average per well

costs at Ferguson in 2014

FERGUSON

AlbertaBakken

Banff

BakkenSiltstone

ExshawShale

ProducerGas InjectorWater Injector

1,250 m

14 m

5.6 km25 km

R 16R 17

ALBERTA BAKKEN EOR PROCESS

DTX .TO ANNUAL REPORT2014

4

FINANCIAL AND OPERATING HIGHLIGHTSYears Ended December 31, 2014 2013 Change

Financial(000s, except per share amounts) ($) ($) (%)

Oil and natural gas revenues 303,348 177,991 70Funds from operations (1) 173,196 93,295 86 Per share – basic 2.01 1.23 63 Per share – diluted 1.95 1.18 65Cash flow from operating activities 184,239 97,448 89Net income 76,233 18,048 322 Per share – basic 0.89 0.24 271 Per share – diluted 0.86 0.23 274Capital expenditures (2) 296,549 211,885 40Working capital deficit (at year-end)(3) 171,347 119,787 43Bank debt (at year-end) 139,234 88,404 57Shareholders’ equity (at year-end) 463,509 311,070 49

Share Data(000s) (#) (#) (%)

At period-end 88,974 81,560 9Weighted average – basic 86,088 76,009 13Weighted average – diluted 88,763 78,892 13

Operating (4)

Production

Natural gas (mcf/d) 13,823 9,881 40 Crude oil (bbls/d) 8,353 5,205 60 NGLs (bbls/d) 668 332 101 Total (boe/d) 11,325 7,184 58Average wellhead prices Natural gas ($/mcf) 4.73 3.42 38 Crude oil and NGLs ($/bbl) 84.84 81.81 4 Combined average ($/boe) 73.38 67.88 8Netbacks Operating netback ($/boe) 45.16 40.50 12 Funds flow netback ($/boe) 41.86 35.51 18Reserves Proved (mboe) 35,354 26,285 35 Proved plus probable (mboe) 51,833 39,413 32 Total net present value – proved plus probable (10% discount, before taxes) ($000s) 893,934 703,716 27Undeveloped land Gross (acres) 466,554 334,252 40 Net (acres) 437,728 311,268 41Gross (net) wells drilled Gas (#) 1 (1.00) – (–) – (–) Oil (#) 43 (42.93) 32 (31.19) 34 (38) Dry and abandoned (#) 3 (3.00) 3 (2.97) – (1)

Total (#) 47 (46.93) 35 (34.15) 34 (37) Average working interest (%) 100 98 2

(1) Funds from operations and funds from operations per share are not recognized measures under International Financial Reporting Standards (IFRS). Refer to the commentary in the Management’s Discussion and Analysis under “Non-GAAP Measurements” for further discussion.

(2) Total capital expenditures, including acquisitions and excluding non-cash transactions. Refer to commentary in the Management’s Discussion and Analysis under “Capital Expenditures and Acquisitions” for further information.

(3) Working capital deficit, which is calculated as current liabilities (excluding derivative financial instruments) and bank debt less current assets (excluding derivative financial instruments), is not a recognized measure under IFRS. Please refer to the commentary under “Non-GAAP Measurements” for further discussion.

(4) For a description of the boe conversion ratio, refer to the commentary in the Management’s Discussion and Analysis under “Other Measurements”.

DTX .TO ANNUAL REPORT

20145

DEETHREE’S FOCUS ON HIGH PERFORMANCE AT THE FIELD LEVEL plus a disciplined financial approach have given the Company financial strength and flexibility. We are not sugar-coating the commodity price situation in 2015: DeeThree’s financial strength will be put to the test. Reduced capital spending – only slightly exceeding cash flow in the first half – will enable us to continue growing production while carefully managing our debt levels and ratios.

SOLID BALANCE SHEET

Much of what DeeThree talks about on the technical side – better results per well, higher IPs, improved type curves, more efficient infrastructure – is crystallized in this metric. We’re proud of our multi-year growth record, to some of the highest company-wide netbacks in western Canada’s producing sector. Last year’s Company-record netback provides a substantial cushion for this year’s more difficult conditions.

Operating costs are typically higher for oil-focused producers than for gas-weighted companies, especially as oil pools move into secondary or enhanced recovery. DeeThree has worked hard to maximize operating efficiencies – building centralized oil batteries and connecting wells via flow lines rather than trucking fluids. The results are clear in our record of declining operating costs per boe. This creates another strong advantage for navigating through lower commodity prices.

DeeThree’s bank lines provided overall borrowing capacity of $310 million at year-end 2014, of which $170.8 million remained available. Our reduced 2015 capital program will be over 90 percent directed to drilling and completing wells, focused on adding production to maximize the year’s cash flow. DeeThree expects to exit 2015 with a debt to funds from operations ratio of 1.1:1.

Growing production from the successful exploration and development of our liquids-producing plays at Brazeau and Ferguson, along with greater operating efficiencies, have delivered successive years of cash flow growth. The high quality of these two plays will support DeeThree in getting the most production and cash flow out of each dollar invested in 2015.

Funds from Operations($ millions, $/share)

Operating Netback($/boe)

Operating Costs($/boe)

Net Debt($ millions)

200

250 2.50

2.00

1.50

1.00

0.50

0.00

150

100

50

0

$ M

illio

ns

$/Sh

are

11 12 13 14

$23.

41 $32.

66 $40.

50

$45.

16

30

40

50

60

20

10

011 12 13 14

$14.

32

$10.

53

$9.9

1

$9.4

4

9

12

15

18

6

3

011 12 13 14

200 2.0

1.5

1.0

0.5

0

150

100

50

0

Net D

ebt (

$ M

illio

ns)

Debt

to F

unds

Flo

w Ra

tio

11 12 13 14

DTX .TO ANNUAL REPORT2014

6

338

2%

440Number of confirmed, de-risked horizontal drilling locations at Brazeau at year-end 2013

Estimated overall resource base booked as 2P reserves at both core areas, year-end 2014

Number of confirmed, de-risked horizontal drilling locations at Brazeau at year-end 2014

80 30Long-leg horizontal drilling locations in delineated Upper Bakken pool area at Ferguson

Sections of new development lands at Ferguson

MULTI-YEAR INVENTORYDeeThree has a Strong Future Our focus on “getting the most oil out” with each well – i.e., maximizing our capital efficiencies – while operating more efficiently through greater scale and dedicated new infrastructure will help DeeThree weather the current market weakness. Quite simply, moving up the performance ladder has pushed down our break-even commodity price. That gives us the confidence to continue investing this year, at a conservative rate tailored to today’s financial constraints.

High-Quality, Multi-Zone OpportunitiesThe quality of DeeThree’s resource base – reflected in the 44° API light oil produced from multiple stacked zones at Brazeau, the lower-decline production at Ferguson, and the high average IP we’re achieving at both plays – is enabling DeeThree to continue drilling this year. We are aiming for modest production growth in 2015, while remaining financially and operationally strong and flexible.

DTX .TO ANNUAL REPORT

20147

STRONG FUTURE

Ferguson Operations

Land (net)

Average working interest (earned lands)

Geology

Horizontal wells drilled in 2014

Production at year-end 2014

407,183 acres

99%

Upper Bakken Siltstone

18

3,540 boe per day

Brazeau Operations

Land (net)

Average working interest (earned lands)

Geology

Horizontal wells drilled in 2014

Production at year-end 2014

95,485 acres

97%

28

9,086 boe per day

With modern, high-capacity infrastructure in place at both plays, thanks to concerted investments over the previous two years, DeeThree is now able to focus almost entirely on adding production by drilling and completing wells. With two rigs running in 2015, we are drilling 13 net horizontal wells in the first half of 2015 and plan a further 16 net wells in the second half. Levering our years spent de-risking both plays, we are aiming to set new records in per-well results and capital efficiencies. This will maximize the production impact – and cash flow impact – of each dollar of capital invested.

The majority of our new wells drilled in 2015 will be in the highly productive, light-oil-producing Belly River sands at Brazeau. At Ferguson, substantially all of the solution gas produced will be reinjected and DeeThree expects this

program to materially reduce the asset’s overall production decline. With an estimated 500 million barrels of oil-in-place in the Upper Bakken, every 1 percent increase in the recovery factor represents 5 million barrels of oil, approximately 10 percent of DeeThree’s current booked reserves. With limited drilling required in 2015, Ferguson is expected to generate free cash flow even at current commodity prices.

DeeThree’s large inventory of high-working-interest wells at our two well-understood, largely de-risked core areas of Brazeau and Ferguson will support many years of more robust activity and faster production growth under appropriate commodity prices.

Land held at year-end 2014 Gas pipeline Oil pipelineDTX oil battery Keyera West Pembina gas plant Hz well

Belly River Cretaceous stacked sands 10 productive zones and

sub-zones established

ALBERTA

Ferguson

Brazeau

DTX .TO ANNUAL REPORT2014

8

LETTER TO SHAREHOLDERS

DeeThree had another highly successful year in 2014, increasing average daily production by 58 percent and funds from operations by 86 percent year-over-year, and adding over 12 million boe in proved plus probable reserves at year-end. All of our growth was achieved through successful drilling, complemented by minimal working interest acquisitions, with lower overall risks than in 2013.

With the severe reduction in oil and natural gas prices towards the end of 2014, we are fully cognizant that investors are concerned about the ongoing effects of commodity price weakness and volatility on exploration and production companies. Balance sheet health, production profiles, decline rates under reduced drilling programs and overall sustainability are key areas of focus.

Last year at this time, we talked about moving our drilling program into “manufacturing mode”, with a focus on improving per-well results and capital efficiencies – and we did so, as the graphics on the previous pages illustrate. We are generating greater production from each dollar of capital invested, a critical advantage in capital-constrained times. Additionally, we have reduced operating and G&A expenses per unit of production and are generating greater operating netbacks and funds from operations at a given commodity price, making the most of each boe produced. By remaining conservative with our balance sheet as we grew production, we entered 2015 with manageable debt and substantial unutilized borrowing capacity.

In sum, we are sustainable at current commodity prices and prepared on multiple levels to weather low commodity prices. We have reduced 2015’s capital spending in order to maintain our balance sheet. We are drilling fewer wells in 2015, all at high-graded locations, in order to achieve the greatest capital efficiency.

We are confident that DeeThree has a strong future despite this down phase in the commodity price cycle. The high quality of our resource base, the large size of our drilling inventory – now at 520 horizontal locations, enough to keep five drilling rigs busy for at least 10 years – and our record of drilling success over multiple years position DeeThree to resume its fast rate of growth to exploit a recovery in commodity prices.

2014 HighlightsSignificant achievements in 2014 included:

• Increased annual average production to 11,325 boe per day, a gain of 58 percent over 2013. Fourth quarter average production rose to a new three-month high of 12,842 boe per day, up by 49 percent from the same period in 2013. DeeThree’s crude oil and liquids weighting was 80 percent in 2014 compared to 77 percent in 2013;

• Increased oil and gas revenues by 70 percent from $178 million in 2013 to $303 million in 2014;

• Grew funds from operations from $93 million ($1.23 per basic share) in 2013 to $173 million ($2.01 per basic share) in 2014, an 86 percent increase;

• Reduced year-over-year net G&A costs per unit of production by 19 percent, from $2.48 per boe in 2013 to $2.01 per boe in 2014;

DTX .TO ANNUAL REPORT

20149

• Reduced operating costs year-over-year, showing particular improvement in the fourth quarter, with operating costs declining by 26 percent from $10.03 per boe in the fourth quarter of 2013 to $7.45 per boe in the fourth quarter of 2014;

• Improved the average operating netback by 12 percent to $45.16 per boe in 2014 from $40.50 per boe in 2013;

• Increased total proved plus probable reserves by 31 percent to 51.8 million boe as at December 31, 2014 from 39.4 million boe at year-end 2013;

• Increased the Company’s estimated net asset value, on a net present value, before tax, 10 percent discounted basis, to $8.75 per fully diluted share at December 31, 2014;

• Achieved all-in finding, development and acquisition costs, including the change in future development capital, of $21.51 per boe on proved plus probable reserve additions and $27.89 per boe on total proved reserve additions; and

• Increased the Company’s availability under its credit facility by 88 percent during the year to $310 million, exiting 2014 with net debt of $171 million.

Operations In 2014, we executed the largest exploration and development capital program in our history. The Company invested $297 million to drill a total of 47 gross (46.93 net) wells with a 94 percent success rate. Drilling activity was concentrated in

our two core areas, with 18 gross wells drilled in the Upper Bakken at Ferguson, 28 gross wells drilled in the multi-zone Belly River stacked sands at Brazeau and one gross well drilled on our non-core property in the Peace River Arch.

The Company achieved material improvements in operating and capital costs. On the operating cost side, previous investments in infrastructure, plus an additional $18 million invested in 2014 to enlarge the Brazeau oil battery to 12,000 bbls per day capacity, add gas compression and lay additional 8” flow lines, resulted in meaningfully lower operating costs. On the capital spending side, a combination of lower service costs, improved processes and careful execution of our program enabled DeeThree to materially improve capital efficiencies.

FERGUSON – UPPER BAKKEN SILTSTONE

DeeThree’s primary focus at its 100 percent working interest Ferguson property last year was further testing and development of the gas reinjection enhanced oil recovery (EOR) scheme. This program’s success was a major highlight for 2014. We initiated a pressure maintenance and resource conservation program in July 2013, reinjecting some of the solution gas produced along with the Bakken oil, using one converted producing well.

Last year we invested $7 million and enlarged the EOR scheme, adding two further injector wells and a built-for-purpose gas compressor plus high-pressure injection lines. This enabled the Company to reinject 100 percent of its produced gas into an EOR area covering 14 sections in the heart of the Ferguson pool. Production from the field averaged 4,284 boe per day in 2014, with producing wells experiencing an average decline rate of 40 percent.

We previously stated that sound reservoir management aimed at maximizing the long-term recovery of this reservoir’s large volume of oil-in-place should be our highest priority. DeeThree’s EOR scheme demonstrates this commitment, and the initial results suggest we are on the right path. The Upper Bakken reservoir is oil-saturated but shallow, naturally under-pressured and lacking in natural water drive. The reservoir pressure and production results demonstrate that the gas flood mitigates decline rates on offsetting producing wells, as the graph and illustration on the previous pages indicate.

FOURTH QUARTER AVERAGE PRODUCTION ROSE TO A NEW THREE-MONTH HIGH OF 12,842 BOE PER DAY, UP BY 49 PERCENT FROM THE SAME PERIOD IN 2013.

DTX .TO ANNUAL REPORT2014

10

Recent well results in the EOR injection area show very strong production results, with one well testing at up to 1,800 bbls per day and as of early March producing 370 bbls per day plus 450 mscf of gas per day. The results have encouraged us to accelerate the transition to full implementation of the EOR scheme. The scheme’s first water injection well and two more gas injection wells are planned in 2015.Initial results from a third-party computer simulation of the Ferguson pool suggest that the EOR scheme could triple the recovery factor (or percentage of the reservoir’s oil-in-place that can be ultimately produced) relative to primary production alone.

Going forward, we plan to increase production at Ferguson at a pace matching the growth of our EOR scheme. Lower decline rates along with improved drilling techniques, such as monobore drilling, which have reduced per-well capital costs by 25-30 percent in initial tests, should each help to further improve capital efficiencies at Ferguson.

Another significant event in 2014 was a discovery well confirming a 7-mile, 30-section western extension of our Upper Bakken play. This year we will drill one delineation well to follow-up on last year’s well, which could add materially to the current inventory of 80 long-leg horizontal drilling locations, giving DeeThree a 30-mile-long Upper Bakken fairway, all held at 100 percent working interest.

BRAZEAU – BELLY RIVER MULTI-ZONE STACKED SANDS

Last year, DeeThree drilled 28 of its 47 wells at Brazeau, where results continue to demonstrate the quality and scale of the multi-zone play. Drilling activity last year at Brazeau was generally on lower-risk locations than in 2013, focusing less on pool extensions and testing new zones, and more on improving per-well results. Capital efficiencies in Brazeau have improved from $41,000 per boe per day added in 2012 to $29,000 in 2013 and $24,000 in 2014, while average first-year per-well productivity improved from 114 boe per day in 2012 to 172 boe per day in 2013 and to 220 boe per day last year. Our best well in 2014 was better than the best well in 2013, and the average 2014 well was better than the average 2013 well.

These results came about through a number of technical refinements, including drilling two-mile-long horizontal well legs, increasing to 30 fracturing stages per well and up to 40 tonnes per stage, improved placement of the horizontal well leg within the pay zone through the use of rotary steerable bits, and greater use of multi-well pads to exploit existing infrastructure.

To date in 2015, the Company has drilled three 100 percent working interest, multi-stage fractured horizontal wells at Brazeau, all of which have met or exceeded expectations. Our results so far include a Belly River D zone well which tested at a final flowing rate of 1,700 bbls per day of crude oil and 1.9 mmscf per day of natural gas at 260 psi wellhead pressure after a four- day test. As such, DeeThree will be able to meet its production targets for the first quarter with fewer wells than originally planned. Capital cost reductions achieved to date are in-line with the 10 percent year-over-year cost reduction provided for in our 2015 budget.

Brazeau remains a growth play over the long term. The play now extends over 40 miles of multi-zone fairway held at nearly 100 percent average working interest, with a current inventory of 440 horizontal locations. Brazeau offers 70 sections of pool area, with up to 10 commercial zones, several of which have only been tested and remain essentially undeveloped. Brazeau is a critical part of DeeThree’s strong future.

CAPITAL EFFICIENCIES IN BRAZEAU HAVE IMPROVED FROM $41,000 PER BOE PER DAY ADDED IN 2012 TO $29,000 IN 2013 AND $24,000 IN 2014.

DTX .TO ANNUAL REPORT

201411

Risk ManagementDeeThree has secured several commodity contracts to protect its cash flow and support its 2015 capital budget. Prior to the decline in world oil prices last fall, the Company had 2,000 bbls per day of crude oil contracted for 2015 with 500 bbls per day in a U.S. dollar collar (US$85.00 per bbl floor and US$100.80 per bbl ceiling). The remaining 1,500 bbls per day are hedged at a fixed price in Canadian dollars ranging from $99.00 per bbl to $100.00 per bbl. Subsequent to year-end, the Company hedged an additional 500 bbls per day, 250 bbls per day for March 2015 to June 2016 at a fixed price of Cdn$72.92 per barrel and 250 bbls per day for 2016 at a fixed price of Cdn$78.00 per bbl.

In addition, the Company has one foreign exchange contract and one interest rate contract in place (please see the following Management’s Discussion and Analysis for further details).

OutlookAs we announced in mid-January, our 2015 capital program includes planned expenditures of up to $160 million. With 93 percent of 2015 capital spending focused on drilling and completing wells, we anticipate delivering production growth of 18 percent year-over-year, to 13,300 boe per day in 2015. We are prudently managing our capital expenditures and production levels in combination with our debt. At present, we are on-track to meet these targets. We will be focused throughout the year on meeting operational guidance while maintaining maximum financial and operational flexibility. As such, DeeThree will continue to re-evaluate its capital spending in the context of commodity prices.

The Company remains focused on improving capital costs through further service cost reductions and added improvements to well drilling and completion processes, including infill drilling with up to eight wells per common pad targeting multiple zones at Brazeau.

With a slower pace of activity in 2015, along with the EOR scheme on our Alberta Bakken property, we expect our production decline rate to improve by as much as 10 percent from the 40 percent corporate decline experienced in 2014. As we announced in early March, per-well results to date in 2015 have been so strong that we were able to reduce the planned number of first-half 2015 wells from 10 to six, conserving additional capital without affecting planned production. The combination of lower declines, improved capital efficiencies and reduced spending will enhance DeeThree’s sustainability.

Many thanks to our office staff, the management team and all our shareholders for their continued support and their trust in all of us at DeeThree.

On behalf of the Board of Directors,

Martin Cheyne President & Chief Executive Officer

March 25, 2015

DTX .TO ANNUAL REPORT2014

12

> RESERVES SUMMARY AND ADDITIONAL INFORMATIONSALES SUMMARY

Three Months Ended December 31, Years Ended December 31,

2014 2013 2014 2013

Natural gas (mcf/d) 16,510 10,251 13,823 9,881

Crude oil (bbls/d) 9,275 6,547 8,353 5,205

NGLs (bbls/d) 815 369 668 332

Total (boe/d) 12,842 8,625 11,325 7,184

LAND SUMMARY

Undeveloped Developed Total

Gross Net Gross Net Gross Net

(acres) (acres) (acres) (acres) (acres) (acres)

2014

Lethbridge 357,114 355,365 54,112 51,818 411,226 407,183Brazeau 76,960 63,072 47,400 32,413 124,360 95,485Peace River Arch 29,600 17,589 48,082 24,453 77,682 42,042Other 2,880 1,702 6,880 4,337 9,760 6,039

Total 466,554 437,728 156,474 113,021 623,028 550,749

2013

Lethbridge 254,412 253,223 50,890 48,773 305,302 301,996

Brazeau 33,600 27,066 26,720 22,746 60,320 49,812

Peace River Arch 42,560 28,837 51,612 25,290 94,172 54,127

Other 3,680 2,142 7,040 4,474 10,720 6,616

Total 334,252 311,268 136,262 101,283 470,514 412,551

As at December 31, 2014, DeeThree controlled petroleum and natural gas leases covering 437,728 net acres of

undeveloped land, a 41 percent increase from the 311,268 net acres held at the end of 2013.

During 2014, DeeThree invested $8.2 million for the acquisition of 131,666 net acres of petroleum and natural gas rights

in the Lethbridge area at an average cost of $61.92 per acre and $7.5 million for the acquisition of 29,356 net acres of

petroleum and natural gas rights in the Brazeau area at an average cost of $256.38 per acre.

DTX .TO ANNUAL REPORT

201413

RESERVES

Sproule Associates Limited (“Sproule”), an independent petroleum engineering firm, evaluated the natural gas, crude oil and NGLs reserves of the Company as at December 31, 2014 and 2013. Sproule based their evaluation on land data, well and geological information, reservoir studies, estimates of on-stream dates, contract information, current hydrocarbon product prices, operating cost data, capital budget forecasts and future operating plans provided by DeeThree, and prepared their report in accordance with the Canadian Securities Administrators’ National Instrument NI 51-101, “Standards of Disclosure for Oil and Gas Activities”. The required disclosure of the reserves estimates and future net revenue of the Company as at December 31, 2014, based on forecast prices and costs, is outlined below along with the economic assumptions used in preparing those estimates. For purposes of computing such units, natural gas is converted to equivalent barrels of oil using a conversion factor of six thousand cubic feet of gas to one barrel of oil. This conversion ratio of 6:1 is based on an energy-equivalent conversion for the individual products at the burner tip and does not represent a value equivalency at the wellhead. Such disclosure of boes may be misleading, particularly if used in isolation. Also refer to the disclosure under “Statement of Reserves Data and Other Oil and Gas Information” included in the Company’s Annual Information Form for the year ended December 31, 2014.

SUMMARY OF OIL AND GAS RESERVES

The following table outlines the oil and gas reserves of the Company by product type on a gross (before royalties) and net (after royalties) basis:

Crude Oil Natural Gas NGLs Total

Gross Net Gross Net Gross Net Gross Net

(mbbls) (mbbls) (mmcf) (mmcf) (mbbls) (mbbls) (mboe) (mboe)

Proved Developed producing 10,837 8,375 24,815 22,336 1,059 712 16,032 12,810 Developed non-producing 192 155 7,809 5,604 287 196 1,780 1,285 Undeveloped 12,388 10,248 23,053 20,915 1,312 982 17,542 14,716

Total proved 23,417 18,778 55,677 48,856 2,657 1,890 35,354 28,810Probable 11,830 8,674 21,735 18,528 1,027 685 16,479 12,447

Total proved plus probable 35,247 27,452 77,412 67,384 3,684 2,574 51,833 41,257

Note: Table may not be additive due to rounding.

NET PRESENT VALUES OF FUTURE NET REVENUE

The net present values of future net revenue of the Company’s reserves at various discount rates on a before-tax basis are outlined below.

Before Income Taxes Discounted At

0% 5% 10% 15% 20%

($000s)

Proved Developed producing 542,053 433,604 363,181 314,207 278,336 Developed non-producing 56,697 25,884 14,291 9,372 6,970 Undeveloped 508,124 343,569 245,083 180,754 135,908

Total proved 1,106,874 803,056 622,556 504,334 421,214Probable 599,905 381,846 271,378 207,168 165,832

Total proved plus probable 1,706,779 1,184,902 893,934 711,501 587,047

Note: Table may not be additive due to rounding.

DTX .TO ANNUAL REPORT2014

14

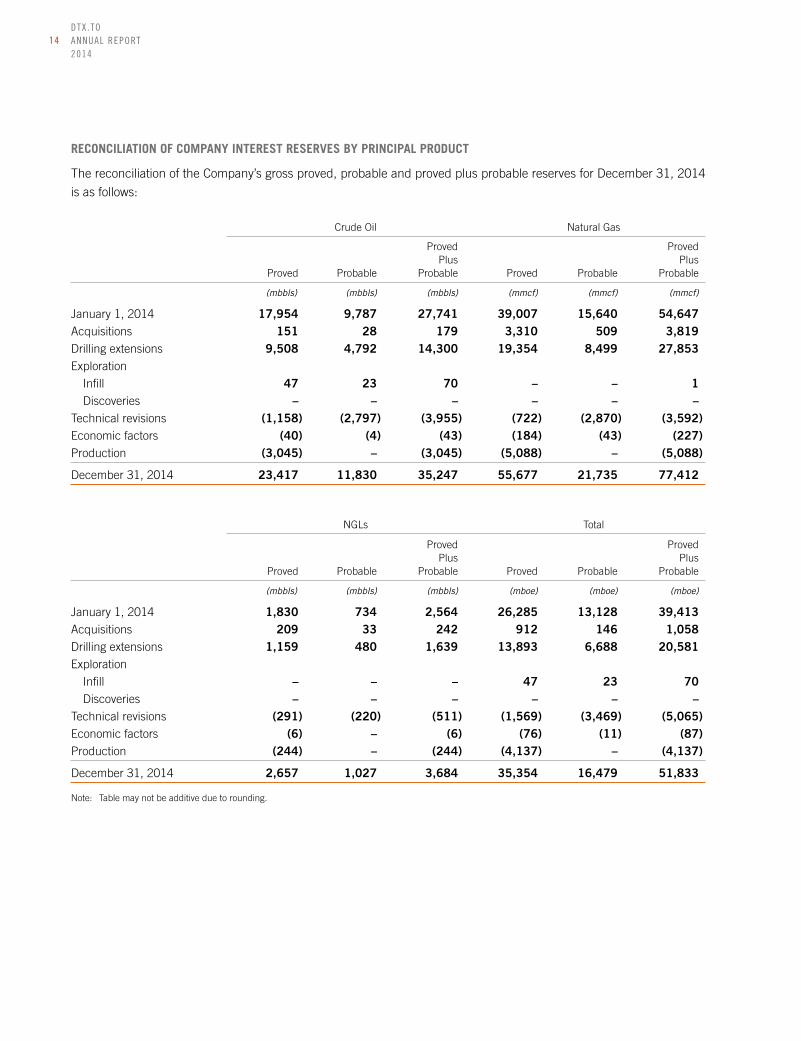

RECONCILIATION OF COMPANY INTEREST RESERVES BY PRINCIPAL PRODUCT

The reconciliation of the Company’s gross proved, probable and proved plus probable reserves for December 31, 2014

is as follows:

Crude Oil Natural Gas

Proved Proved Plus Plus Proved Probable Probable Proved Probable Probable

(mbbls) (mbbls) (mbbls) (mmcf) (mmcf) (mmcf)

January 1, 2014 17,954 9,787 27,741 39,007 15,640 54,647Acquisitions 151 28 179 3,310 509 3,819Drilling extensions 9,508 4,792 14,300 19,354 8,499 27,853Exploration

Infill 47 23 70 – – 1 Discoveries – – – – – –Technical revisions (1,158) (2,797) (3,955) (722) (2,870) (3,592)Economic factors (40) (4) (43) (184) (43) (227)Production (3,045) – (3,045) (5,088) – (5,088)

December 31, 2014 23,417 11,830 35,247 55,677 21,735 77,412

NGLs Total

Proved Proved Plus Plus Proved Probable Probable Proved Probable Probable

(mbbls) (mbbls) (mbbls) (mboe) (mboe) (mboe)

January 1, 2014 1,830 734 2,564 26,285 13,128 39,413Acquisitions 209 33 242 912 146 1,058Drilling extensions 1,159 480 1,639 13,893 6,688 20,581Exploration

Infill – – – 47 23 70 Discoveries – – – – – –Technical revisions (291) (220) (511) (1,569) (3,469) (5,065)Economic factors (6) – (6) (76) (11) (87)Production (244) – (244) (4,137) – (4,137)

December 31, 2014 2,657 1,027 3,684 35,354 16,479 51,833

Note: Table may not be additive due to rounding.

DTX .TO ANNUAL REPORT

201415

TOTAL FUTURE NET REVENUE

The following table provides a breakdown of the various components of total future net revenue on an undiscounted

basis for proved and proved plus probable reserves:

Future Net Revenue Well Before Operating Development Abandonment Income Revenue Royalties Costs Costs Costs Taxes

($000s)

Proved2015 258,485 51,018 45,913 137,500 – 24,054

2016 327,107 60,724 50,455 112,164 – 103,764

2017 313,129 58,083 48,921 42,366 – 163,759

2018 227,946 49,196 42,295 3,872 – 132,583

2019 183,228 42,168 38,760 – – 102,300

2020 154,523 35,363 36,400 – – 82,760

2021 131,831 28,474 34,135 – 197 69,025

2022 114,981 23,329 32,570 – – 59,082

2023 101,111 19,187 31,079 – 142 50,703

2024 89,879 16,118 29,802 – – 43,959

2025 80,383 13,681 28,979 – – 37,723

2026 72,102 11,791 27,920 – 56 32,335

Remainder 593,263 88,442 292,383 673 6,931 204,834

Total proved 2,647,968 497,577 739,612 296,575 7,326 1,106,874

Proved plus probable2015 316,774 64,711 52,578 176,025 – 23,460

2016 443,697 88,835 62,050 146,089 – 146,723

2017 435,033 97,571 60,986 56,849 – 219,627

2018 319,212 83,365 52,312 8,296 – 175,239

2019 261,810 68,337 48,055 – – 145,418

2020 223,681 57,999 44,811 – – 120,871

2021 193,467 48,696 42,579 – – 102,192

2022 170,131 40,773 40,633 – – 88,725

2023 151,053 33,818 38,986 – 255 77,994

2024 135,531 28,519 37,431 – – 69,851

2025 122,068 24,213 36,325 – 147 61,383

2026 110,795 20,891 35,301 – – 54,603

Remainder 1,159,620 183,688 543,779 792 10,448 420,913

Total proved plus probable 4,042,872 841,419 1,095,828 388,050 10,850 1,706,779

Note: Table may not be additive due to rounding.

DTX .TO ANNUAL REPORT2014

16

SUMMARY OF PRICING AND INFLATION RATE ASSUMPTIONS

The economic parameters, as determined by Sproule, assumed in preparing the forecast prices and costs reserves

report are outlined below.

Price Forecast – Effective December 31, 2014

Currency WTI Edmonton Henry Alberta Exchange Cushing, Light Hub, AECO-C Year Rate Oklahoma Par Louisiana Spot

(US$/Cdn$) (US$/bbl) (Cdn$/bbl) (US$/mmbtu) (Cdn$/GJ)

Historical2010 0.971 79.43 77.80 4.39 4.16

2011 1.012 95.00 95.16 4.04 3.72

2012 1.001 94.19 86.57 2.79 2.43

2013 0.971 97.98 93.24 3.68 3.13

2014 0.905 93.00 94.18 4.28 4.50

Forecast2015 0.850 65.00 70.35 3.25 3.32

2016 0.870 80.00 87.36 3.75 3.71

2017 0.870 90.00 92.28 4.00 3.90

2018 0.870 91.35 99.75 4.50 4.47

2019 0.870 92.72 101.25 5.00 5.05

2020 0.870 94.11 103.85 5.08 5.13

2021 0.870 95.52 105.40 5.15 5.22

2022 0.870 96.96 106.99 5.23 5.31

2023 0.870 98.41 108.59 5.31 5.40

2024 0.870 99.89 110.22 5.39 5.49

2025 0.870 101.38 111.87 5.47 5.58

Remainder +1.5%/yr +1.5%/yr +1.5%/yr +1.5%/yr +1.5%/yr

RESERVE LIFE INDEX

The reserve life index of DeeThree has been calculated using 2015 estimated gross production volumes and gross

proved and proved plus probable reserves using forecast prices and costs, all of which were taken from the December

31, 2014 Sproule reserves report. The reserve life index of the Company as at December 31, 2014, on a boe basis, was

7.8 years for total proved reserves and 6.7 years for total proved plus probable reserves.

Proved Plus Proved Probable Proved Expected Expected Proved Plus 2015 2015 Plus Proved Probable Production Production Proved Probable

(years) (years)

Natural gas (mmcf) 55,677 77,412 6,488 20,488 8.6 3.8Crude oil and NGLs (mbbls) 26,075 38,931 3,448 4,274 6.8 8.2

Total (mboe) 35,354 51,834 4,529 7,688 7.8 6.7

DTX .TO ANNUAL REPORT

201417

FINDING AND DEVELOPMENT COSTS AND RECYCLE RATIO

The recycle ratio is a measure for evaluating the effectiveness of a company’s re-investment program. The ratio measures

the efficiency of capital investment, which is accomplished by comparing the operating netback per boe to that year’s

reserves’ finding and development (F&D) cost per boe. For the year ended December 31, 2014, DeeThree’s recycle

ratio was 1.6 times on a proved basis and 2.1 times on a proved plus probable basis, while the Company achieved an

average F&D cost, including future development costs, of $27.89 per boe on a proved basis and $21.51 per boe on a

proved plus probable basis.

The table below provides detailed calculations relating to F&D costs and recycle ratios for the Company’s proved and

proved plus probable reserves for the years ended December 31, 2014 and 2013.

Years Ended December 31, 2014 2013

Proved ReservesCapital expenditures ($000s) 296,549 211,885

Change in future capital ($000s) 71,640 73,146

Total capital costs ($000s) 368,189 285,031

Reserve additions (mboe) 13,203 14,549

F&D costs, excluding future development costs ($/boe) 22.46 14.56

F&D costs, including future development costs ($/boe) 27.89 19.59

Operating netback ($/boe) 45.16 40.50

Recycle ratio 1.6 2.1

Proved Plus Probable ReservesCapital expenditures ($000s) 296,549 211,885

Change in future capital ($000s) 59,561 169,543

Total capital costs ($000s) 356,110 381,428

Reserve additions (mboe) 16,554 21,847

F&D costs, excluding future development costs ($/boe) 17.91 9.70

F&D costs, including future development costs ($/boe) 21.51 17.46

Operating netback ($/boe) 45.16 40.50

Recycle ratio 2.1 2.3

(1) For a description of the boe conversion ratio, refer to the commentary at the end of the Management’s Discussion and Analysis.(2) The aggregate of the exploration and development costs incurred in 2014 and 2013 and the change during the year in estimated future development costs

may not reflect total F&D costs related to reserve additions for the year.

DTX .TO ANNUAL REPORT2014

18

NET ASSET VALUE

Years Ended December 31, 2014 2013

(000s, except per share amounts) ($) ($)

Present value of petroleum and natural gas reserves (1) 893,934 373,009

Net undeveloped land (2) 77,954 62,483

Working capital deficit (171,347) (77,586)

Proceeds from stock options (3) 14,048 18,193

Net asset value 814,589 376,099

Diluted shares outstanding (#) (4) 93,137,688 76,779,805

Net asset value per share 8.75 4.90

(1) Total proved plus probable, discounted at 10%, before tax per the Sproule December 31 reserves evaluations.(2) Based on a third-party evaluation as at December 31, 2014 and 2013.(3) Calculated proceeds from in-the-money options using a 2014 year-end closing common share price of $5.11 per share (2013 – $9.57 per share).(4) Calculated as basic shares outstanding at December 31 plus in-the-money options.

DTX .TO ANNUAL REPORT

201419

> MANAGEMENT’S DISCUSSION AND ANALYSISThe following Management’s Discussion and Analysis (MD&A) of the financial condition and results of operations for

DeeThree Exploration Ltd. (“DeeThree” or “the Company”) is dated March 25, 2015 and should be read in conjunction

with the Company’s audited financial statements and related notes for the years ended December 31, 2014 and 2013

and with the MD&A and unaudited interim financial statements for the periods ended March 31, 2014, June 30, 2014

and September 30, 2014. All financial information is reported in Canadian dollars, unless otherwise noted.

This MD&A contains additional measures under generally accepted accounting principles (GAAP), non-GAAP measures

and forward-looking statements. Readers are cautioned that the MD&A should be read in conjunction with the Company’s

disclosure under “Non-GAAP Measures” and “Forward-looking Information and Statements” included at the end of

this MD&A.

ABOUT DEETHREE EXPLORATION LTD.

DeeThree is a Canadian company actively engaged in crude oil and natural gas exploration, development and production

in key areas of the Western Canada Sedimentary Basin. DeeThree is focused on creating long-term shareholder value

through a successful drilling program, growth-oriented field operations and prudent financial management.

DeeThree’s strategic platform for growth includes low-risk development and higher-risk exploration as well as strategic

acquisitions. The Company has two core operating areas: the Brazeau area of west central Alberta, which features crude

oil, natural gas and natural gas liquids (NGLs), and the Ferguson area of southern Alberta, which features Bakken oil

and shallow natural gas. These two core areas have provided the Company with a balanced and diverse production base.

The Company’s experienced technical team has a proven track record of driving quarter-over-quarter organic growth

with these assets.

DeeThree commenced operations in 2007 as a private company focused on development and production of natural

gas in southern Alberta. In late 2008, DeeThree completed its first significant acquisition from a major oil and natural

gas producer comprised of properties in the Lethbridge area of southern Alberta, which became known as the Ferguson

area. Ferguson was the Company’s primary focus until late in the first quarter of 2011, when DeeThree closed a

transformational acquisition of properties in the Brazeau and Peace River Arch areas. Since 2012, the Company has

been successful in exploration and development activities in the Brazeau and Ferguson areas and continues to achieve

growth in production, reserves and net asset value.

DeeThree is headquartered in Calgary, Alberta and the common shares of DeeThree are listed for trading on the Toronto

Stock Exchange under the symbol DTX and on the United States OTCQX under the symbol DTHRF.

2014 FINANCIAL AND OPERATING HIGHLIGHTS

DeeThree’s average annual production of 11,325 boe/d for 2014 reflects strong operating performance from existing

wells in the Ferguson and Brazeau areas as well as strong production from new wells drilled during the year.

For the year ended December 31, 2014, DeeThree realized a combined average sales price of $73.38/boe, an 8 percent

increase over the prior year. This was primarily due to increased market prices for crude oil for the majority of the

DTX .TO ANNUAL REPORT2014

20

year. With average operating costs of $9.44/boe, transportation costs of $2.18/boe and average royalties of 23 percent,

DeeThree achieved an operating netback of $45.16/boe, a 12 percent increase over the prior year.

DeeThree incurred $296.5 million of capital expenditures in 2014, with a capital program that focused on the drilling

of 47 gross (46.93 net) wells, with 18 gross (18.0 net) in the Ferguson area, 28 gross (27.93 net) in the Brazeau area,

and 1 gross (1.0 net) in the Peace River Arch area. The capital program also included approximately $22.6 million of

minor acquisitions, $8.9 million on land and $31.0 million related to upgrading of existing facilities as well as facility and

pipeline construction to handle the Company’s growing production.

During the year, DeeThree increased its proved plus probable reserves by 32 percent to 51.8 million boe (75 percent oil

and NGLs) at December 31, 2014 from 39.4 million boe (77 percent oil and NGLs) in the prior year. DeeThree’s reserve

additions were predominately a result of the successful 2014 drilling program in the Company’s Brazeau and Ferguson

areas, which continue to demonstrate their high quality and generate strong returns through the Company’s rapid pace

of development.

During 2014, DeeThree issued a total of 5,714,200 common shares and 752,000 flow-through shares for net proceeds

of approximately $69.4 million, and issued common shares on the exercise of options for $2.4 million, for total cash

proceeds of $71.8 million. This allowed the Company to reduce debt and free up borrowing capacity, which was redrawn

to fund the Company’s 2014 capital program.

DTX .TO ANNUAL REPORT

201421

FUNDS FROM OPERATIONS (1)

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

($000s)

Net income 28,312 3,305 76,233 18,048

Non-cash items:

Depletion and depreciation (D&D) expense 23,785 15,984 80,799 51,309

Deferred income tax expense 10,285 1,974 28,331 9,253

Share-based compensation (2) 785 573 3,069 2,238

Accretion 229 188 850 497

Unrealized loss (gain) on financial instruments (22,572) (524) (25,494) 3,074

Loss on disposition 90 – 90 –

Exploration and evaluation (E&E) expense 859 3,160 9,318 8,876

Funds from operations (1) 41,773 24,660 173,196 93,295

(1) Funds from operations and funds from operations per share are not recognized measures under International Financial Reporting Standards (IFRS). Refer to “Non-GAAP Measurements” for further discussion.

(2) The share-based compensation amount included in the calculation of funds from operations was adjusted for the non-cash portion related to certain field employees that was reclassified to operating expenses for presentation in the statement of operations and comprehensive income.

During the three months ended December 31, 2014, the Company generated funds from operations totalling

$41.8 million ($0.47 per basic share and $0.46 per diluted share) compared to $24.7 million ($0.32 per basic share

and $0.31 per diluted share) in the comparative period of 2013 and $52.7 million ($0.59 per basic share and $0.57 per

diluted share) in the third quarter of 2014. The year-over-year increase is primarily attributable to increased revenue,

stemming from increased production and a higher realized price for the majority of the year. The quarter-over-quarter

decrease reflects decreased revenue associated with decreased commodity prices, partially offset by lower operating

and transportation costs.

Funds from operations totalled $173.2 million ($2.01 per basic share and $1.95 per diluted share) for the year ended

December 31, 2014 compared to $93.3 million ($1.23 per basic share and $1.18 per diluted share) recorded in 2013.

NET INCOME

For the three months ended December 31, 2014, the Company recorded net income of $28.3 million ($0.32 per basic

share and $0.31 per diluted share) compared to $3.3 million ($0.04 per basic and diluted share) in the same period

of 2013 and net income of $21.1 million ($0.24 per basic share and $0.23 per diluted share) in the third quarter of

2014. The Company’s increased net income for the year was primarily due to the impact of unrealized mark-to-market

gains recognized mostly in the fourth quarter of the year. The quarter-over-quarter increase was also primarily due to

the impact of the unrealized and realized gains relating to the Company’s mark-to-market assets and decreased E&E

expense, partially offset by decreased revenue from lower commodity prices.

Net income for the year ended December 31, 2014 was $76.2 million ($0.89 per basic share and $0.86 per diluted

share) compared to $18.0 million ($0.24 per basic share and $0.23 per diluted share) in 2013.

DTX .TO ANNUAL REPORT2014

22

FINANCIAL AND OPERATING RESULTS

SALES VOLUMES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

SalesNatural gas (mcf/d) 16,510 10,251 13,823 9,881

Crude oil (bbls/d) 9,275 6,547 8,353 5,205

NGLs (bbls/d) 815 369 668 332

Total sales (boe/d) 12,842 8,625 11,325 7,184

(%) (%)

Production SplitNatural gas 22 20 20 23

Crude oil 72 76 74 72

NGLs 6 4 6 5

Total 100 100 100 100

For the fourth quarter of 2014, the Company’s production averaged 12,842 boe/d compared to 8,625 boe/d in the

same period of 2013 and 12,294 boe/d in the third quarter of 2014. This represents a 49 percent year-over-year and a

4 percent quarter-over-quarter increase and reflects new production from the tie-in of wells drilled during 2014.

For the year ended December 31, 2014, DeeThree’s production averaged 11,325 boe/d compared to 7,184 boe/d in

the previous year, representing a 58 percent increase. During 2014, production was comprised of 13,823 mcf/d of gas,

8,353 bbls/d of crude oil and 668 bbls/d of NGLs, thereby increasing the Company’s crude oil and NGL production to

80 percent of total corporate production from 77 percent a year earlier.

REVENUE

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

($000s)

Natural gas 5,833 3,777 23,848 12,347

Crude oil 61,530 46,747 267,527 159,555

NGLs and other 2,594 1,341 11,973 6,089

Total oil and natural gas revenue 69,957 51,865 303,348 177,991

During the three months ended December 31, 2014, revenue increased by 35 percent to $70.0 million from

$51.9 million in the comparative period of 2013. The year-over-year increase was a result of increased production. When

compared to the third quarter of 2014, revenue decreased by 20 percent to $70.0 million from $87.2 million due to

decreased commodity prices.

During 2014, revenue totalled $303.3 million compared to $178.0 million a year earlier. Total revenue increased by

70 percent over 2013 primarily as a result of the increase in sales volumes as well as higher crude oil market prices for

the year as a whole.

DTX .TO ANNUAL REPORT

201423

Pricing for both the three and 12-month periods ended December 31, 2014 is discussed in further detail in “Commodity

Prices and Foreign Exchange” below.

COMMODITY PRICES AND FOREIGN EXCHANGE

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Benchmark PricesCrude oil

WTI (US$/bbl) 73.15 97.46 93.00 97.97

Edmonton Light (MSW) (Cdn$/boe) 75.55 86.41 94.44 93.03

Differential – MSW/WTI (US$/bbl) (6.36) (14.93) (7.17) (7.57)

Hardisty Bow River (Cdn$/boe) 77.38 69.51 91.60 76.16

Differential – Bow River/WTI (US$/bbl) (13.65) (31.07) (18.95) (24.02)

Natural gas

NYMEX (US$/mmbtu) (1) 4.00 3.62 4.41 3.67

AECO (Cdn$/GJ) (2) 3.41 3.35 4.27 3.01

Average Realized PricesNatural gas ($/mcf) 3.84 4.00 4.73 3.42

Crude oil ($/bbl) 72.11 77.62 87.74 83.98

NGLs ($/bbl) 34.13 38.87 48.60 47.80

Combined average ($/boe) 59.21 65.37 73.38 67.88

Foreign ExchangeCdn$/US$ 1.14 1.05 1.10 1.03

US$/Cdn$ 0.88 0.95 0.91 0.97

(1) Mmbtu is the abbreviation for millions of British thermal units. One mcf of natural gas is approximately 1.02 mmbtu.(2) GJ is the abbreviation for gigajoule. One mcf of natural gas is approximately 1.05 GJ.

CRUDE OIL PRICING

The average realized price of DeeThree’s crude oil was $72.11/bbl for the fourth quarter of 2014 compared to $77.62/bbl

in the fourth quarter of 2013 and $91.60/bbl in the third quarter of 2014. DeeThree’s realized oil price decreased by

7 percent from the prior year’s fourth quarter and by 21 percent from the third quarter of 2014, due to a combination of a

decrease in the US$ WTI benchmark oil price, offset by the change in the differentials and a weakened Canadian dollar.

For the year ended December 31, 2014, the Company’s average realized crude oil price was $87.74/bbl compared

to $83.98/bbl during 2013, a 4 percent increase driven by higher average benchmark prices and a weakened

Canadian dollar.

NATURAL GAS PRICING

DeeThree receives a premium to the AECO gas index price due to the heat content of its sales gas. DeeThree’s average

realized natural gas price was $3.84/mcf in the fourth quarter of 2014 versus $4.00/mcf in the fourth quarter of 2013

and $4.39/mcf in the third quarter of 2014. The Company’s realized gas price decreased by 4 percent from the same

period of 2013 and 13 percent from the third quarter of 2014.

DTX .TO ANNUAL REPORT2014

24

For the year ended December 31, 2014, the Company’s average realized price for natural gas increased by 38 percent

to $4.73/mcf from $3.42/mcf in 2013, driven by a 42 percent increase in the AECO gas index price.

PRICE RISK & MITIGATION

Ongoing commodity price volatility may affect DeeThree’s funds from operations and rates of return on capital programs.

As continued volatility is expected in 2015, DeeThree will take steps to mitigate these risks and protect its financial

position, as it was doing in 2014. For example, in the first half of 2014, the Company was moving a portion of its crude oil

out of the Ferguson area via rail cars. The Company was able to attract better pricing on those volumes and will continue

to explore options to move its crude oil by rail when market conditions are favourable.

The Company’s financial results are significantly influenced by fluctuations in commodity prices, including price

differentials and foreign exchange rates. As a means of managing commodity price volatility and its impact on cash

flows, the Company seeks to protect itself from fluctuations in prices and exchange rates by maintaining an appropriate

hedging strategy. As at the date of this MD&A, DeeThree had six crude oil hedges (refer to “Risk Management” below

for details). Most commodity prices are based on US dollar benchmarks, which result in the Company’s realized prices

being influenced by the Canadian/US exchange rates. The Company does not sell or transact in foreign currency, but

is affected by foreign currency exchange rate changes related to commodity prices as outlined above. As at the date of

this MD&A, DeeThree had one foreign currency exchange risk management contract in place to mitigate these risks (see

“Risk Management” below for contract details).

ROYALTIES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Oil and natural gas revenues ($000s) 69,957 51,865 303,348 177,991

Total royalties ($000s) 16,277 12,858 68,613 40,349

Total royalties ($/boe) 13.78 16.21 16.60 15.39

Percent of revenue (%) 23 25 23 23

The Ferguson property is primarily subject to freehold royalties, which work on a sliding-scale determined monthly

on a well-by-well basis using a calculation based on the new royalty regulation implemented in 2009 with a cap of

30 percent. The sliding scale provides varying rates based on productivity (a higher royalty is payable from wells with

higher production rates) and commodity prices (a higher royalty is payable in times of higher natural gas and crude

oil prices). This area is also subject to freehold mineral taxes (which are included as royalties for financial reporting

purposes) and overriding royalties related to farm-in arrangements.

The Brazeau property is primarily subject to Crown royalties payable to the provincial government and overriding royalties

on oil, natural gas and NGL production. These types of royalties are also sensitive to production levels and commodity

prices; therefore, the Company’s royalties will continue to fluctuate with commodity prices, well production rates,

production declines of existing wells along with the performance and location of new wells drilled.

For the fourth quarter of 2014, royalties totalled $16.3 million or 23 percent of revenue compared to $12.9 million or

25 percent of revenue for the same quarter in 2013 and $18.1 million or 21 percent of revenue in the third quarter of

2014. The year-over-year royalty rate decrease was due to new production from the Company’s wells brought on-stream

during the past few quarters, some of which qualify for the 5 percent royalty holiday under the Government of Alberta’s

royalty framework.

DTX .TO ANNUAL REPORT

201425

During the year ended December 31, 2014, royalties totalled $68.6 million or 23 percent of revenue compared to

$40.3 million or 23 percent of revenue for 2013.

OPERATING AND TRANSPORTATION EXPENSES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Operating expenses ($000s) 8,798 7,962 39,032 25,998

Transportation expenses ($000s) 3,507 1,391 9,016 5,448

Total operating and transportation expenses ($000s) 12,305 9,353 48,048 31,446

Operating expenses ($/boe) 7.45 10.03 9.44 9.91

Transportation expenses ($/boe) 2.97 1.75 2.18 2.08

Total operating and transportation expenses ($/boe) 10.42 11.78 11.62 11.99

Operating costs include all costs associated with the production of crude oil and natural gas. The major components

of operating costs include charges for contract operating, processing fees, lease rentals, property and pipeline taxes,

utilities and well maintenance charges.

Operating expenses for the fourth quarter of 2014 totalled $8.8 million or $7.45/boe compared to $8.0 million or

$10.03/boe in the same period of 2013 and $10.9 million or $9.63/boe in the third quarter of 2014. The year-over year

decrease was driven by the Company ceasing to have any wells on extended flow-back until being tied into a pipeline

(which had contributed to higher operating costs for the past few quarters) as well as the effects of an over-estimation of

operating expenses in the third quarter of 2014.

Transportation expenses for the three months ended December 31, 2014 were $3.5 million or $2.97/boe compared to

$1.4 million or $1.75/boe in the fourth quarter of 2013 and $2.2 million or $1.95/boe in the third quarter of 2014. Over

the past year, the Company has increased production of crude oil and NGLs, and the transportation costs associated

with those products consist primarily of pipeline tariffs, terminal charges and trucking (crude oil and NGLs incur a higher

cost per boe for transportation than natural gas). When the Company experiences pipeline capacity constraints, it must

use alternative means of transportation to move production volumes to market. In particular, the Company saw a large

increase in the cost per barrel for clean oil trucking during the fourth quarter of 2014 and expects this to continue into

early 2015.

For the year ended December 31, 2014, the Company incurred operating expenses of $39.0 million or $9.44/boe compared

to $26.0 million or $9.91/boe in 2013. Transportation expenses for the year totalled $9.0 million or $2.18/boe versus

$5.4 million or $2.08/boe last year.

RISK MANAGEMENT

DeeThree maintains a risk management program to reduce the volatility of revenues and to increase the certainty of

funds from operations. DeeThree considers all of its risk management contracts to be effective economic hedges of

the underlying business transactions. The Company had the following crude oil, foreign exchange and interest rate risk

management contracts, with a short-term mark-to-market asset of $23.3 million at December 31, 2014 (September 30,

2014 – short-term asset of $0.6 million and $0.1 million long-term asset and December 31, 2013 – short-term liability of

$2.2 million):

DTX .TO ANNUAL REPORT2014

26

CRUDE OIL CONTRACTS

Period Commodity Type of Contract Quantity Pricing Point Contract Price

Jan.1/15 – Dec.31/15 Crude Oil Collar 500 bbls/d WTI-NYMEX US$85.00/bbl (floor) – US$100.80/bbl (cap)

Jan.1/15 – Dec.31/15 Crude Oil Fixed 500 bbls/d WTI-NYMEX Cdn$99.00/bbl

Jan.1/15 – Dec.31/15 Crude Oil Fixed 500 bbls/d WTI-NYMEX Cdn$99.39/bbl

Jan.1/15 – Dec.31/15 Crude Oil Fixed 500 bbls/d WTI-NYMEX Cdn$100.00/bbl

FOREIGN EXCHANGE CONTRACT

Pricing Point Period Currency Type of Contract Quantity (Cdn$/US$)

Jan. 1/15 – Dec. 31/15 US$ Average Rate Range Forward US$1,300,000 Trigger – 1.1300 Cdn$/US$ Floor – 1.100 Cdn$/US$ Ceiling – 1.1110 Cdn$/US$

INTEREST RATE CONTRACT

Term Amount Fixed Rate Index

Feb. 18 /14 – Feb. 18/16 Cdn$40 million 1.44% CDOR

Subsequent to December 31, 2014, DeeThree entered into the following crude oil risk management contracts:

CRUDE OIL CONTRACTS

Period Commodity Type of Contract Quantity Pricing Point Contract Price

March 1/15 – June 30/16 Crude Oil Fixed 250 bbls/d WTI-NYMEX Cdn$72.92/bbl

Jan.1/16 – Dec. 31/16 Crude Oil Fixed 250 bbls/d WTI-NYMEX Cdn$78.00/bbl

Gains and losses on risk management contracts are composed both of unrealized gains or losses that represent the

change in the mark-to-market position of those contracts throughout the period and of realized gains and losses

representing the portion of the contracts that have settled in cash during the period. The Company has elected not to

use hedge accounting for its current risk management contracts.

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Unrealized loss (gain) on financial instruments ($000s) (22,572) (524) (25,494) 3,074

Unrealized loss (gain) on financial instruments ($/boe) (19.11) (0.66) (6.17) 1.17

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Realized loss (gain) on financial instruments ($000s) (4,661) 548 426 2,226

Realized loss (gain) on financial instruments ($/boe) (3.95) 0.69 0.10 0.85

DTX .TO ANNUAL REPORT

201427

During the fourth quarter of 2014, the Company recorded an unrealized gain on financial instruments of $22.6 million

and a realized gain of $4.7 million. In the same period of the prior year, the Company recorded an unrealized gain of

$0.5 million and a realized loss of $0.5 million. In the previous quarter, the Company recorded an unrealized gain of

$6.1 million and a realized loss of $0.7 million. The unrealized gain resulted from the mark-to-market of financial risk

management contracts at the period end. These non-cash unrealized derivative gains are generated by the change

over the reporting period in the mark-to-market valuation of DeeThree’s risk management contracts, which fluctuated

significantly in the fourth quarter of 2014 due to the change in the forward price curves for crude oil. The realized

gains or losses represent actual cash settlements under the respective commodity, foreign exchange and interest rate

contracts in the respective periods.

For the year ended December 31, 2014, the Company recorded an unrealized gain of $25.5 million and a realized loss

of $0.4 million compared to an unrealized loss of $3.1 million and a realized loss of $2.2 million, respectively, for 2013.

GENERAL AND ADMINISTRATIVE (G&A) EXPENSES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

($000s except per boe)

Gross G&A expense 3,923 3,303 11,343 9,171

Capitalized G&A (direct) (863) (848) (2,297) (2,012)

Overhead recoveries (163) (225) (735) (651)

G&A expense (net) 2,897 2,230 8,311 6,508

G&A expense (net) ($/boe) 2.45 2.81 2.01 2.48

Gross G&A expense totalled $3.9 million for the three-month period ended December 31, 2014 compared to

$3.3 million in the comparable period of 2013 and $2.2 million in the third quarter of 2014. Net G&A costs were

$2.9 million or $2.45/boe in the fourth quarter of 2014 compared to $2.2 million or $2.81/boe a year earlier and

$1.6 million or $1.41/boe in the third quarter of 2014. When compared to the same quarter of the prior year, gross G&A

costs increased on an absolute basis due to increased staffing costs (including salaries, bonuses, consulting and office

rent) required to manage DeeThree’s growing business. Additionally, $0.5 million in bad debt expense was recognized

during the fourth quarter of 2014, compared to $nil in the same period in 2013. In the fourth quarter of 2014, the

Company had an average of 37 full-time employees and three consultants versus 26 full-time employees and seven

consultants in the same period of 2013.

The Company capitalized direct G&A expenses amounting to $0.9 million and had overhead recoveries of $0.2 million

in the fourth quarter of 2014 versus $0.8 million and $0.2 million, respectively, in the comparative period of 2013, and

$0.4 million and $0.2 million, respectively, in the third quarter of 2014.

Net G&A expenses for the year ended December 31, 2014 totalled $8.3 million or $2.01/boe compared to $6.5 million

or $2.48/boe for 2013. During the year ended December 31, 2014, the Company capitalized $2.3 million in direct costs

related to its exploration and development efforts and $0.7 million of overhead recoveries compared to $2.0 million and

$0.7 million, respectively, in 2013.

DTX .TO ANNUAL REPORT2014

28

SHARE-BASED COMPENSATION

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

($000s except per boe)

Gross share-based compensation 1,346 948 5,036 3,613

Share-based compensation reclassified to operating costs (43) (43) (167) (188)

Capitalized share-based compensation (561) (375) (1,967) (1,375)

Share-based compensation expense (net) 742 530 2,902 2,050

Share-based compensation expense (net) ($/boe) 0.63 0.67 0.70 0.78

The Company has a stock option plan, which is described in note 10 to the financial statements for the years ended

December 31, 2014 and 2013. Options granted under the plan have a four-year vesting term and expire five years from

the grant date, with the fair value of options granted estimated at the grant date using the Black-Scholes option-pricing

model. At December 31, 2014, the Company had 7,676,328 options outstanding under this plan.

Share-based compensation expense is a non-cash expense that reflects the amortization over the vesting period of

the fair value of stock options granted to the Company’s employees, consultants and directors. For those stock options

granted to field employees, their portion of the share-based compensation is reclassified to operating expenses, in order

to be consistent with the recognition of their salaries on the statement of operations and comprehensive income.

For the quarter ended December 31, 2014, the Company incurred net share-based compensation expense of

$0.7 million or $0.63/boe versus $0.5 million or $0.67/boe in the same period of 2013 and $0.9 million or $0.80/boe in

the third quarter of 2014. The year-over-year absolute increase was directly attributable to grants issued during the year

and the resulting share-based compensation from those issuances.

During 2014, DeeThree incurred net share-based compensation expense of $2.9 million or $0.70/boe compared to

$2.1 million or $0.78/boe recorded in 2013.

DEPLETION AND DEPRECIATION (D&D) EXPENSE

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Depletion and depreciation expense ($000s) 23,785 15,984 80,799 51,309

Depletion and depreciation expense ($/boe) 20.14 20.15 19.55 19.57

DeeThree records D&D expense on its property and equipment over the individual useful lives of the assets, employing

the unit-of-production method using proved plus probable reserves and associated estimated future development capital

required for its oil and natural gas assets, the straight-line method for field facilities (20-year useful life) and the declining-

balance method on corporate assets (20 to 30 percent). Assets in the E&E phase are not amortized.

For the three months ended December 31, 2014, the Company recorded D&D expense of $23.8 million or $20.14/boe

compared to $16.0 million or $20.15/boe in the same period of 2013 and $21.8 million or $19.25/boe in the third

quarter of 2014. The absolute increase in D&D expense year-over-year is attributable to the 49 percent and 4 percent

respective increases in production volumes, slightly offset by lower costs related to finding and developing reserves.

During 2014, D&D expense was $80.8 million or $19.55/boe compared to $51.3 million or $19.57/boe in 2013.

DTX .TO ANNUAL REPORT

201429

LOSS ON DISPOSITIONS

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Loss on dispositions ($000s) 90 – 90 –

Loss on dispositions ($/boe) 0.08 – 0.02 –

For the three months ended December 31, 2014, the Company recorded a loss on dispositions of $0.09 million or

$0.08/boe. The loss was the result of the disposition of a minor property to the joint venture partner during the fourth

quarter. There were no such expenses during the same quarter of the prior year or in the third quarter of 2014.

During 2014, the loss on dispositions was $0.09 million or $0.02/boe.

IMPAIRMENT OF OIL AND GAS PROPERTIES

Impairment is recognized when the carrying value of an asset or group of assets (referred to as a cash-generating unit or

CGU) exceeds its recoverable amount, defined as the higher of its value in use and fair value less costs to sell. Any asset

impairment is recoverable to its original value less associated D&D expense should there be indicators that the asset’s

recoverable value has increased since the time of recording the initial impairment. Impairment testing is performed at

the CGU level and is required when there are indicators of impairment, such as a significant drop in commodity prices

or a write-down of proved or probable reserves. No impairment charges were recorded in 2014.

IMPAIRMENT OF FIELD FACILITIES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Impairment of field facilities ($000s) – 1,317 – 1,317

Impairment of field facilities ($/boe) – 1.66 – 0.50

During the fourth quarter of 2013, DeeThree expensed some costs related to an original facility in the Ferguson area. No

such expenses were incurred during the year ended December 31, 2014.

DTX .TO ANNUAL REPORT2014

30

EXPLORATION AND EVALUATION (E&E) EXPENSE

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Exploration and evaluation expense ($000s) 859 3,160 9,318 8,876

Exploration and evaluation expense ($/boe) 0.73 3.98 2.25 3.39

DeeThree accumulates costs related to its E&E assets in one pool pending determination of an asset’s technical feasibility

and commercial viability. E&E costs are primarily for seismic data, undeveloped land and drilling until the well in question

is complete and results have been evaluated. Costs related to wells determined to be uneconomical as well as costs of

undeveloped land lease expiries are expensed as they occur.

During the fourth quarter of 2014, the Company recorded E&E expense of $0.9 million or $0.73/boe, which included

$0.2 million of lease expiries in several of the Company’s areas, $0.7 million related to the write-off of preliminary drilling

costs, and a $0.2 million dollar recovery related to a dry and abandoned well that was written off during the third quarter

of 2014. This compares to $3.2 million or $3.98/boe in the same period of 2013. During the third quarter of 2014, E&E

expense consisted of $6.5 million or $5.75/boe of lease expiries and costs related to dry and abandoned wells.

During the year ended December 31, 2014, the Company recorded E&E expense of $9.3 million or $2.25/boe compared

to $8.9 million or $3.39/boe during 2013.

ACCRETION AND FINANCE EXPENSES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

($000s except per boe)

Accretion expense on decommissioning liabilities 228 188 850 497

Finance expense 1,410 942 4,921 3,038

Total accretion and finance expenses 1,638 1,130 5,771 3,535

Accretion expense on decommissioning liabilities ($/boe) 0.19 0.24 0.21 0.19

Finance expense ($/boe) 1.19 1.19 1.19 1.16

Total accretion and finance expenses ($/boe) 1.38 1.43 1.40 1.35

Accretion expense represents the increase in the present value of the Company’s decommissioning liabilities. In the

fourth quarter of 2014, the Company recorded accretion expense of $0.2 million or $0.19/boe compared to $0.2 million

or $0.24/boe in the same period of 2013 and $0.2 million or $0.19/boe in the third quarter of 2014.

During the three months ended December 31, 2014, the Company recorded interest and finance expenses of

$1.4 million or $1.19/boe compared to $0.9 million or $1.19/boe in the same period of 2013 and $1.0 million or

$0.92/boe in the previous quarter. The Company incurred interest charges and standby fees related to the $310 million

credit facility, which was drawn to $139.2 million at the end of the year (December 31, 2013 – $88.4 million; September

30, 2014 – $107.5 million).

For the year ended December 31, 2014, the Company recorded accretion expense of $0.9 million or $0.21/boe compared

to $0.5 million or $0.19/boe in 2013. The Company also recorded finance expense of $4.9 million or $1.19/boe in 2014

compared to $3.0 million or $1.16/boe in the prior year.

DTX .TO ANNUAL REPORT

201431

INCOME TAXES

Three Months Ended December 31, Year Ended December 31,

2014 2013 2014 2013

Deferred income tax expense ($000s) 10,285 1,974 28,331 9,253