Tradi&onalDataWarehousesolu&onhelpscustomersinstoringvaluablebusinessdataandinextrac&ngstrategicinforma&onfromthedatacluBer

Order Sales Marketing Accounting

Company Operational Data Sources 1

Servers, Storage...

Data Warehouse Databases

Oracle, Microsoft, IBM, Netezza, Teradata

Business Intelligence/ Analytical Applications

COGNOS, Oracle, SAS, Microsoft,

Business Users

2

3 Customer value proposition

Stores and retrieves large amount of important daily and historical data

Helps users create complex queries to retrieve data in a user friendly way

Provides security for sensitive data

Assists decision makers to get meaningful information form large piles of data by performing complex analyses

Data is the most valuable business asset and analytical information helps business stay competitive in the market

Data Warehouse is a ~$9 Billion global industry, out of which US market contributes 50%

$-

$2,000.00

$4,000.00

$6,000.00

$8,000.00

$10,000.00

$12,000.00

DataWarehouseRevenue

DataWarehouseRevenue

11% CAGR

50%

35%

15%

Global DW Market Shares 2010

America EMEA Asia/Pacific

Which is growing at an impressive double digit annual rate

A highly consolidated industry with ~90% market controlled by top 4 players

Source: IDC report

Highlyconcentratedindustrywherecompe&&onisbasedonpriceandproduct/serviceporPoliocoverage

Barriers to Entry

(Medium)

Suppliers Power (Low)

Substitutes (Low)

Buyers Power

(Medium)

Industry Competitors

(High)

Bargaining power of suppliers

Threat of new entrants

Threat of substitutes

Bargaining power of buyers

- Need large investments to setup

- IP protection

- Incumbents will retaliate or acquire the new entrants

- High switching cost

- Price sensitive and often demand upgrade to new technology

- Open source technologies

- Large numbers of firms are backward integrating

- Cost advantage is diminishing with the outsourced suppliers - Competition is based on price and

product and service portfolio coverage

- Consolidation is on the rise; big players are acquiring smaller or niche players

- Growth driven by M&A

- Competition is also based on differentiation of product and service Adapted form Porter’s Five Force Framework

SystemsIntegratorandServiceProvider

StorageDeviceandAppliancesManufacturer

DataWarehouseIndustryValueChainandProfitPool

DatabaseandDWSoRwareVendor

SupportandMaintenance

ThirdpartyApplica&onandAnaly&csSoRwareVendor

Prof

itabi

lity

Market Size

Oracle, Microsoft, IBM

Oracle, Microsoft, IBM, SAP and Teradata

Net

ezza

, Exa

data

3P

AR

Oracle, Microsoft, IBM, Accenture, Deloitte and Teradata

IBM, Accenture, Deloitte, EDS, Infosys and other Outsourcing Firms

Adapted from Profit Pool Framework by Gadiesh & Gilbert, 1998

54321

1

23

4

5

Businesses are planning to store more data than ever to compete successfully

Resulting in a massive growth in data storage requirements (According to Netezza)

According to TDWI report According to Netezza report

Businessesarefacingchallengeswithuncontrollablegrowthindata

FromdatacluBertointelligentinsight,drama&cshiRindatausageistransformingDataWarehouseindustry

Data Warehouse Appliance and the New Customer Value

A New Value with DW

Appliances

Reduce

Eliminate Create

Raise

- Solutions Complexity - Overall Cost (Capex and Opex) - Time to Readiness - Multi-Vendor Dependencies

- Need for redundant data warehouse solutions

- One stop solution for advanced DW with DW Appliance - Provide high capacity DW with storage up to 1.5 petabyte - Provide highly efficient Business Analytics solutions with MPP processing - Provide power to end users with industry specific analytics solutions like Retail, Biotech and Financial industries - High ROI at low cost

- Ability to store large amount of data in Data Warehouse and Data Mart format - Ability to process large amount of data at the maximum - Ease in customer usability

Changeincustomerdemandforadvancedanaly&csandeverevolvingtechnologiesins&tutedDataWarehouseApplianceindustrysub‐segment

Blue Ocean Strategy for Data Warehouse Industry

Riseofthemachine;TheDataWarehouseApplianceisaonestopsolu&onthatcanstoreenormousamountofdata,processatlightspeedandcapableofrunningadvancedanaly&cs

Customer value proposition Affordable cost

– Lox CAPEX and OPEX

Faster time to value – Plug in and go – Save time

Breakneck processing power – 100 times faster than traditional Data Warehouse system – Save time

Massive data storage capacity – Capable of storing 1.5 petabyte data

And customers faced many challenges Extremely complex system

– Many products from different vendors – Dependency on IT department – Slow performance

Data clutter – Valuable information lost – Lost ROI

Limitation in data storage

Expensive – SMB companies can’t afford

Traditional Data Warehouse system was complex and was a nightmare to manage

MarketPenetra*on 5‐20%

Maturity EarlyMainstream

CustomerAdapta*on Increasing

Withonly20%currentmarketpenetra&on,DataWarehouseApplianceisapoten&algrowthmarket

Source: Gartner Hype Cycle for Data Management Industry, 2010

Growing customer confidence on the DW Appliance is boosting the product visibility…

and is also improving the technology adoption of the Appliance products

SystemsIntegratorandServiceProvider

StorageDeviceandApplianceManufacturer

DatabaseandDWSoRwareVendor

SupportandMaintenance

ThirdpartyApplica&onandAnaly&csSoRwareVendor

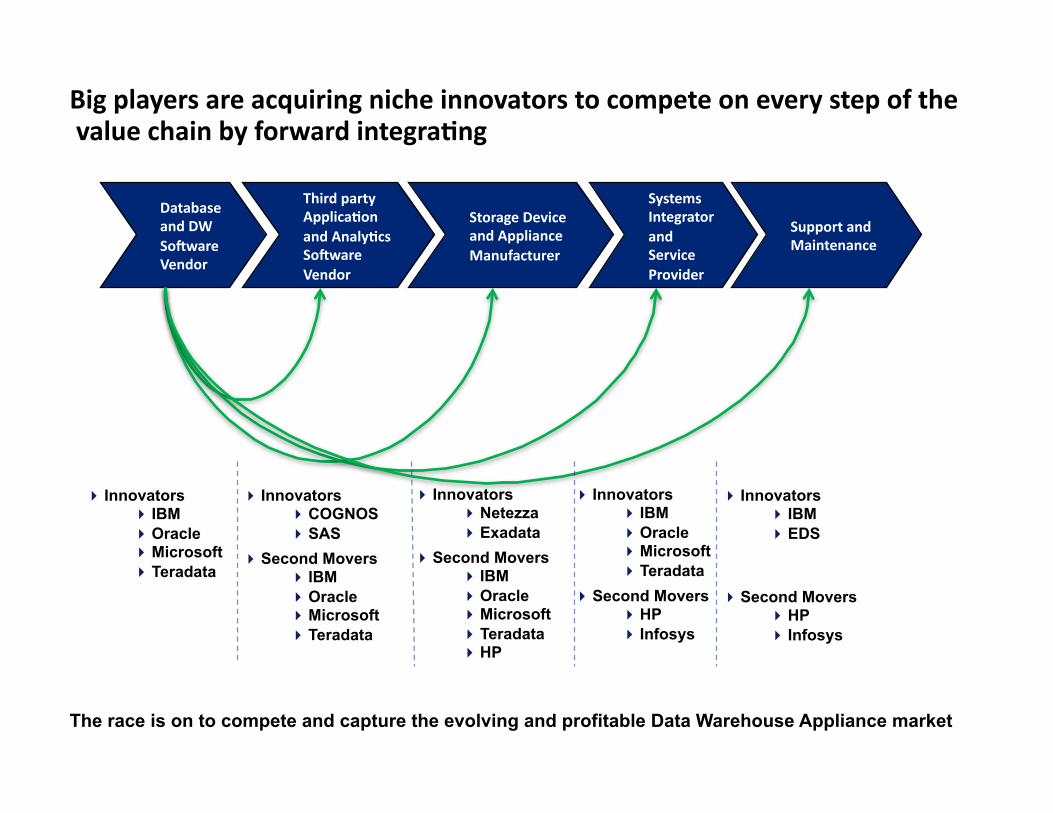

Bigplayersareacquiringnicheinnovatorstocompeteoneverystepofthevaluechainbyforwardintegra&ng

Innovators IBM Oracle Microsoft Teradata

Innovators COGNOS SAS

Second Movers IBM Oracle Microsoft Teradata

Innovators Netezza Exadata

Second Movers IBM Oracle Microsoft Teradata HP

The race is on to compete and capture the evolving and profitable Data Warehouse Appliance market

Second Movers HP Infosys

Innovators IBM Oracle Microsoft Teradata

Second Movers HP Infosys

Innovators IBM EDS

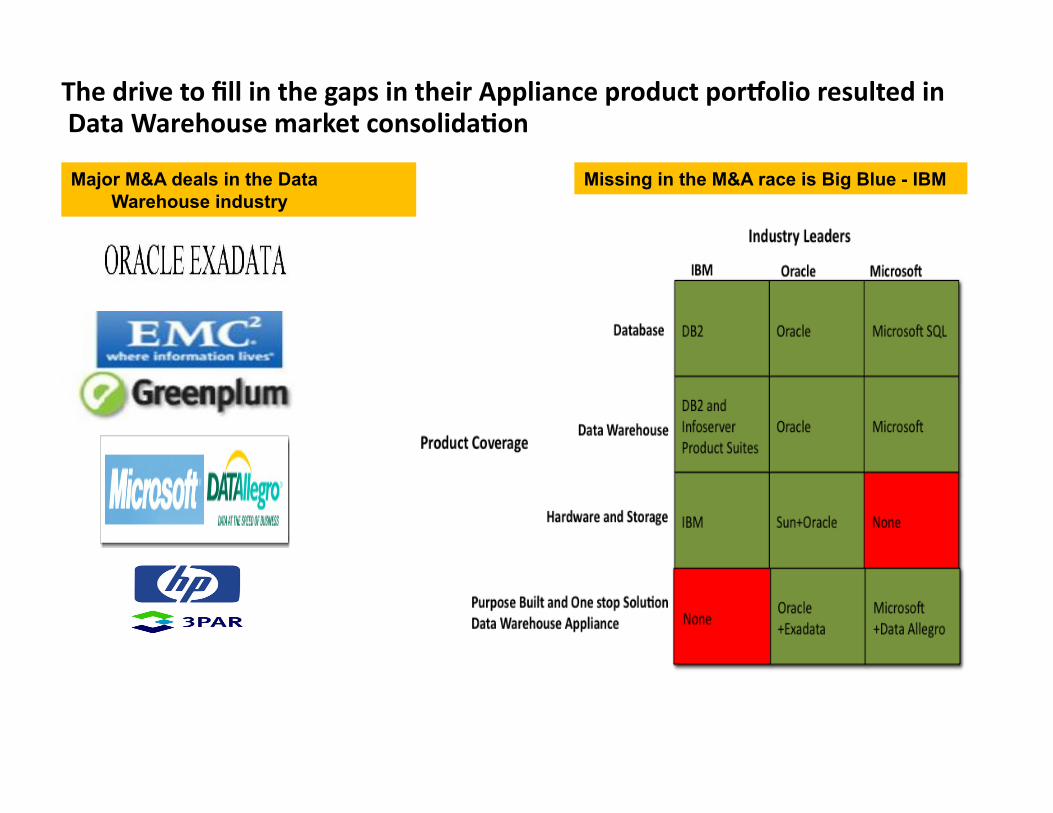

ThedrivetofillinthegapsintheirApplianceproductporPolioresultedinDataWarehousemarketconsolida&on

Major M&A deals in the Data Warehouse industry

Missing in the M&A race is Big Blue - IBM

PenetratedMarket

ServedMarket

MissedMarket

‐ SmallandMediumBusinessesLookingforAffordableAnaly&csSolu&on‐ Purposedbuiltandonestopsolu&onapplianceataffordableprice(NetezzaandExadata)

‐ LargeenterpriseswithbothDatabaseandDataWarehouseneeds(Transac&onalsystems)‐ Clientswithexpensiveandmul&‐&erIBMdatabaseanddatawarehouseproductsuites(DB2,Bladeservers,ISASorInfoServerandCOGNOS)‐ Longandcomplicatedimplementa&onlifecycle

‐ Largeormediumenterpriseswithsomeanaly&csneeds‐ Mediumbudgetanaly&cssolu&ons‐ DisparatesoRwareandhardwaresolu&onsfromcompe&ngvendors

ProductCoverage

Strong

SoRware‐DB2,InfoServer/ISAS,COGNOSandotherspecializedanaly&csapplica&ons

Hardware–BladeServer

Services–6000trainedconsultants

Missing

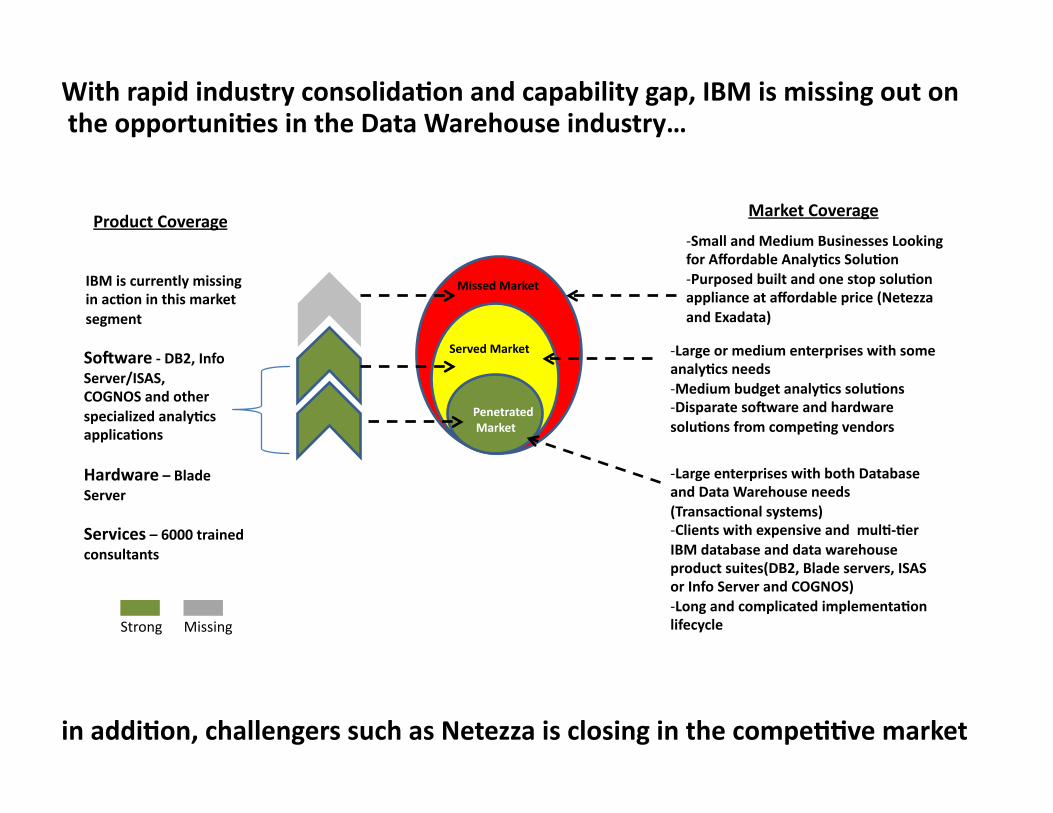

IBMiscurrentlymissinginac&oninthismarketsegment

Withrapidindustryconsolida&onandcapabilitygap,IBMismissingoutontheopportuni&esintheDataWarehouseindustry…

MarketCoverage

inaddi&on,challengerssuchasNetezzaisclosinginthecompe&&vemarket

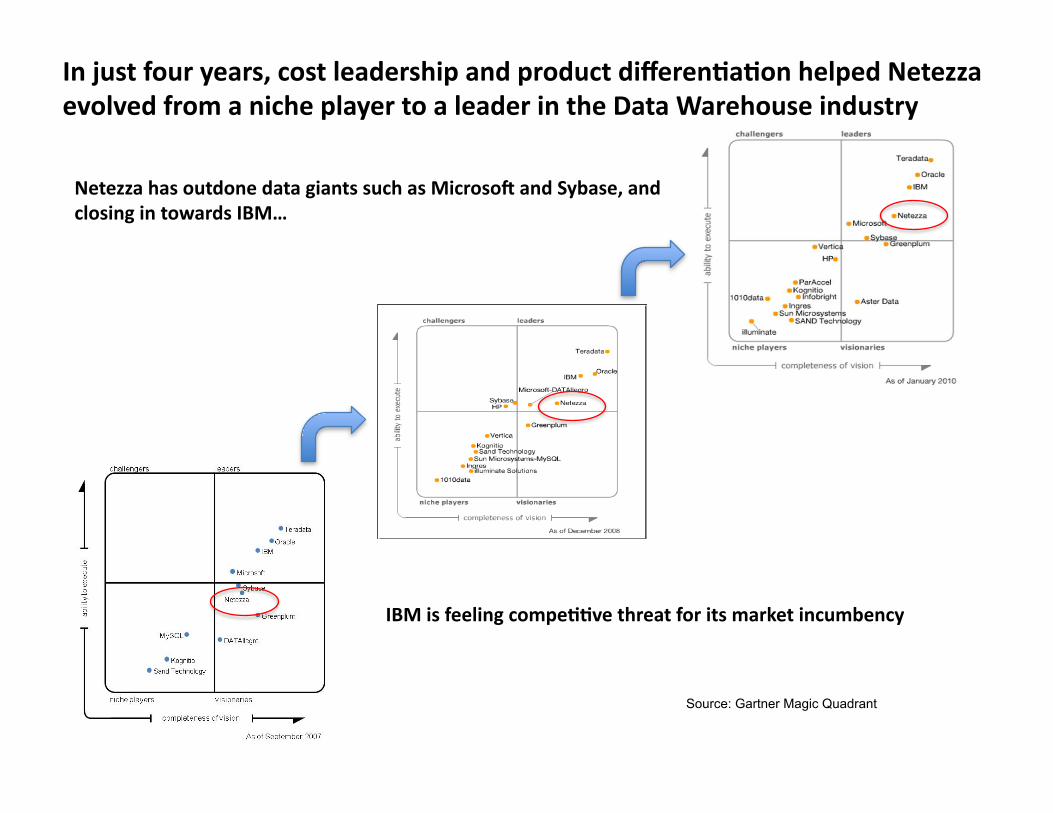

Injustfouryears,costleadershipandproductdifferen&a&onhelpedNetezzaevolvedfromanicheplayertoaleaderintheDataWarehouseindustry

NetezzahasoutdonedatagiantssuchasMicrosoRandSybase,andclosingintowardsIBM…

IBMisfeelingcompe&&vethreatforitsmarketincumbency

Source: Gartner Magic Quadrant

Strategy Opportunities

Leaders

Growth by acquisition Deter competition

Capture evolving market Increase market share Increase customer and

geographical foot print Increase customer dependencies

and life-cycle by cross selling

Challengers

Collaboration with industry leaders

Create niche and differentiation

Merge with leaders Continuous innovation

and patent portfolio

Premium pricing because of differentiation

Become a supplier or integrator for the leaders

Increase the sale-off value

M&Aisthenaturalcourseofac&onwhenchallengersarethreateningtheincumbencyofmarketleaders

FactorsdroveIBMtoacquireNetezza

Compe&&vePressure

TechnologyPatents

CompleteProductPorPolio

GlobalGrowthinAnaly&cs

MarketforcescompelledIBMtojointhepurposebuiltDataWarehouseAppliancerace

IBMacquiredNetezzatoenterthepurposedbuiltDataWarehouseAppliancemarketandtogeneratesustainablevalue

Netezza’sacquisi&onpriceof$1.7B(6.5xsalesmul&ple)isinlinewiththerecenthighgrowthdataindustrytake‐outmul&ples

Date Acquirer Target PremiumPaid OfferEnterpriseValue

EV/SalesMul*ples

09/20/2010 IBM Netezza 9.8% $1.7B 6.5x

09/02/2010 HP 3PAR 242.0% $2.4B 9.8x

07/08/2009 EMC DataDomain 92.2% $2.1B 5.4x

Source: Morgan Stanley Report

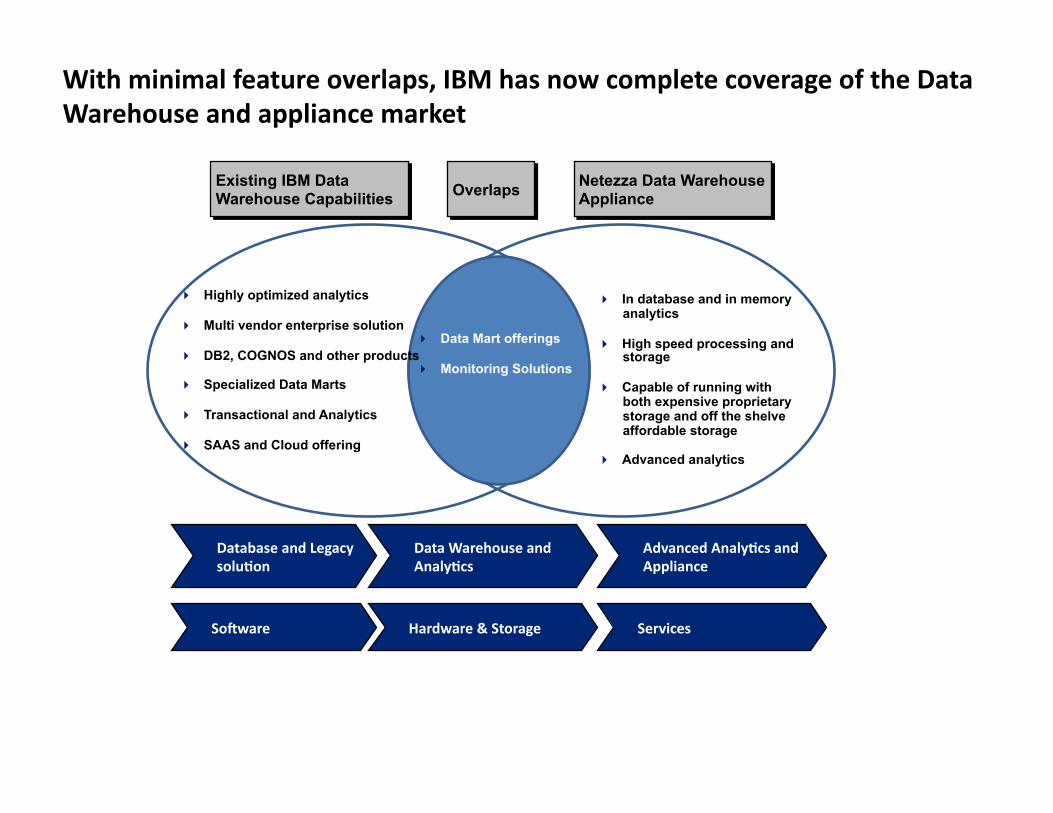

Highly optimized analytics

Multi vendor enterprise solution

DB2, COGNOS and other products

Specialized Data Marts

Transactional and Analytics

SAAS and Cloud offering

Existing IBM Data Warehouse Capabilities

Netezza Data Warehouse Appliance Overlaps

Data Mart offerings

Monitoring Solutions

In database and in memory analytics

High speed processing and storage

Capable of running with both expensive proprietary storage and off the shelve affordable storage

Advanced analytics

Withminimalfeatureoverlaps,IBMhasnowcompletecoverageoftheDataWarehouseandappliancemarket

DatabaseandLegacysolu&on

DataWarehouseandAnaly&cs

AdvancedAnaly&csandAppliance

SoRware Hardware&Storage Services

ImplementMarke&ng/Sales

IBMandNetezzaValueChainInterrela&onshipandValueCrea&on

R&D/Innova&on

MarketResearch

SoRwareDevelopment

BuildHardware

SupportandService

ImplementR&D/Innova&on

MarketResearch

SoRwareDevelopment

BuildHardware

SupportandService

IBM

Netezza

Marke&ng/Sales

IBMwillu&lizeitscapability

Sharedcapabili&es

ShadowedChevronNetezza’sredundantac&vi&eswillbeconsolidatedbyIBM

IBMandNetezzatogethercantrulycreatevaluefortheircustomersandshareholdersbyleveragingeachothers’competencies

Synergies Complementing product capabilities will help IBM cover the

complete market segment IBM’s deep pocket will help Netezza’s long term R&D and

product planning

Netezza’s patents will strengthen IBM’s market leadership

IBM’s global market reach will help Netezza enter new markets

IBM can leverage its consulting workforce to create Appliances related new service offerings – Capable of storing 1.5 petabyte data