IAS 17 - Leases

Academic Resource Center

Leases Page 2

Typical coverage of US GAAP

► General

► Scope

► Terminology and definitions

► Lease classification

► Lessee accounting

► Capitalization criteria

► Capital lease

► Operating lease

► Lessor accounting

► Capitalization criteria

► Capital lease

► Operating lease

► Sale and leaseback arrangements

► Definition

► Lease classification and capitalization criteria

► Accounting treatment

► Other lease considerations

► Disclosures

Academic Resource Center

Leases Page 3

Executive summary

► Overall accounting for leases under IFRS and US GAAP is similar, although IFRS has fewer specific rules than US GAAP.

► Both IFRS and US GAAP separately discuss lessee and lessor accounting.

► Both IFRS and US GAAP focus on classifying leases as either operating or capital. IFRS uses the term “finance” lease, whereas US GAAP uses “capital” lease.

► IFRS uses more general criterion based on the substance of the lease to determine lease capitalization whereas US GAAP uses “bright line” criteria.

Academic Resource Center

Leases Page 4

Primary pronouncements

US GAAP

► ASC 840, Leases

IFRS

► IAS 17, Leases

► SIC 15, Operating Leases – Incentives

Academic Resource Center

Leases Page 5

Progress on convergence

► A discussion paper on leases was released in March 2009 with comments due in July 2009. In the discussion paper, the FASB and IASB proposed a possible new model for lease accounting based on the principle that all leases give rise to liabilities for future rental payments and assets (the right to use the leased asset) and should be recognized in an entity’s balance sheet.

► An exposure draft on leases is expected to be issued in 2010.

► A final pronouncement on leases is expected in mid-2011.

Academic Resource Center

Leases Page 6

GeneralScope

ASC 840 applies to leases for PP&E while excluding leases to exploit or explore natural resources and certain licensing arrangements.

IAS 17 is similar.

IFRSUS GAAP

Academic Resource Center

Leases Page 7

GeneralScope

IFRS

► IAS 17 applies to all leases broadly.

► IAS 17 also specifically excludes leases for investment property (covered under IAS 40) and biological assets (covered under IAS 41).

US GAAP

► ASC 840 applies only to leases for PP&E.

Academic Resource Center

Leases Page 8

Terminology and definitions

A lease is defined as an agreement whereby the lessor conveys a right to use an asset to a lessee for a certain period of time in return for payment.

A BPO is defined as an option that allows the lessee to buy the leased asset at a price significantly lower than the asset’s fair value at the end of the lease term so that the exercise of the option is reasonably assured. The assessment as to whether a BPO exists is judgmental and requires a review of facts and circumstances.

IFRSUS GAAP

Similar

Similar

Academic Resource Center

Leases Page 9

Terminology and definitions

MLPs are defined as payments to be made over the lease term that a lessee is or can be required to make plus any amounts guaranteed by the lessee or by a party related to the lessee (such as a guaranteed RV), as well as a BPO.

MLPs exclude contingent rent, costs for services and taxes to be paid by and reimbursed to the lessor.

Similar

Similar

IFRSUS GAAP

The RV is the fair value of the leased asset at the end of the lease term and can be guaranteed or unguaranteed by the lessee or a party related to the lessee.

Academic Resource Center

Leases Page 10

Terminology and definitions

A lease term is the non-cancelable term of a lease, including any additional periods when the lease can be continued that seem reasonably certain to occur at the inception of the lease.

Similar

Similar

IFRSUS GAAP

Initial direct costs are incremental costs incurred by a lessor in acquiring a lease.

Academic Resource Center

Leases Page 11

Terminology and definitions

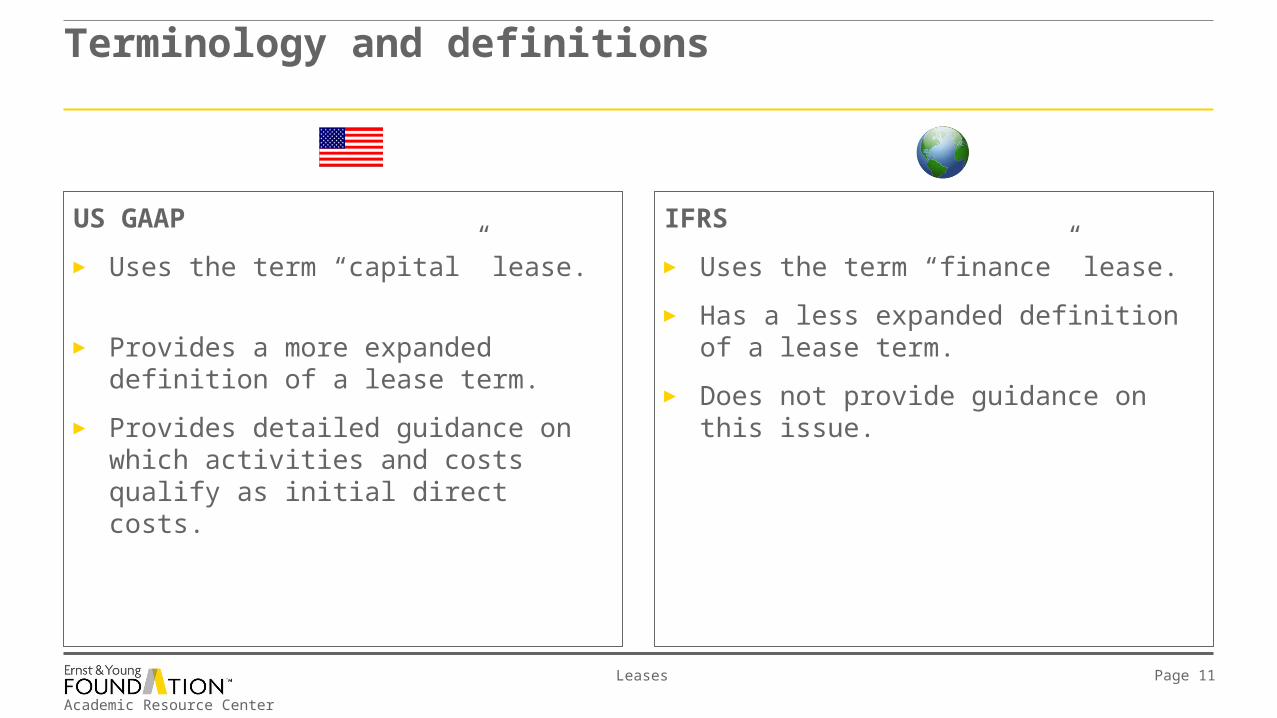

IFRS

► Uses the term “finance” lease.

► Has a less expanded definition of a lease term.

► Does not provide guidance on this issue.

US GAAP

► Uses the term “capital” lease.

► Provides a more expanded definition of a lease term.

► Provides detailed guidance on which activities and costs qualify as initial direct costs.

Academic Resource Center

Leases Page 12

Lease classification

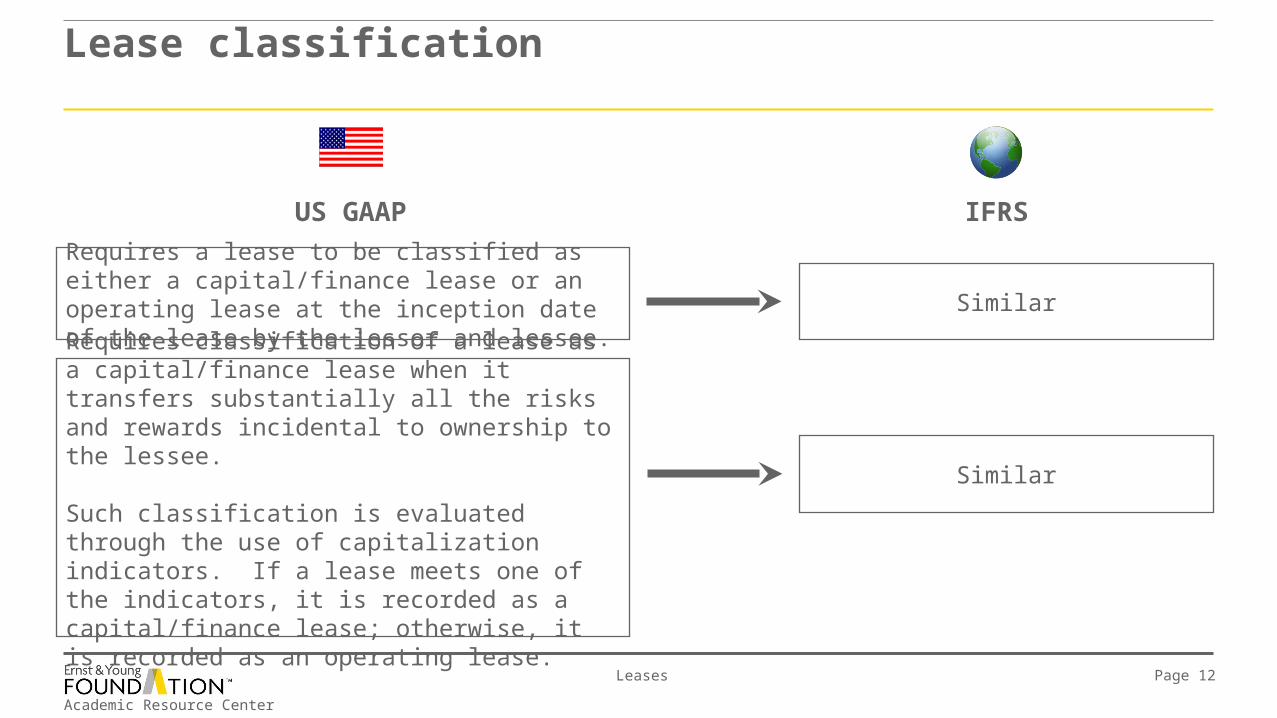

Requires a lease to be classified as either a capital/finance lease or an operating lease at the inception date of the lease by the lessor and lessee.

Requires classification of a lease as a capital/finance lease when it transfers substantially all the risks and rewards incidental to ownership to the lessee.

Such classification is evaluated through the use of capitalization indicators. If a lease meets one of the indicators, it is recorded as a capital/finance lease; otherwise, it is recorded as an operating lease.

IFRSUS GAAP

Similar

Similar

Academic Resource Center

Leases Page 13

Lease classificationFor both lessors and lessees

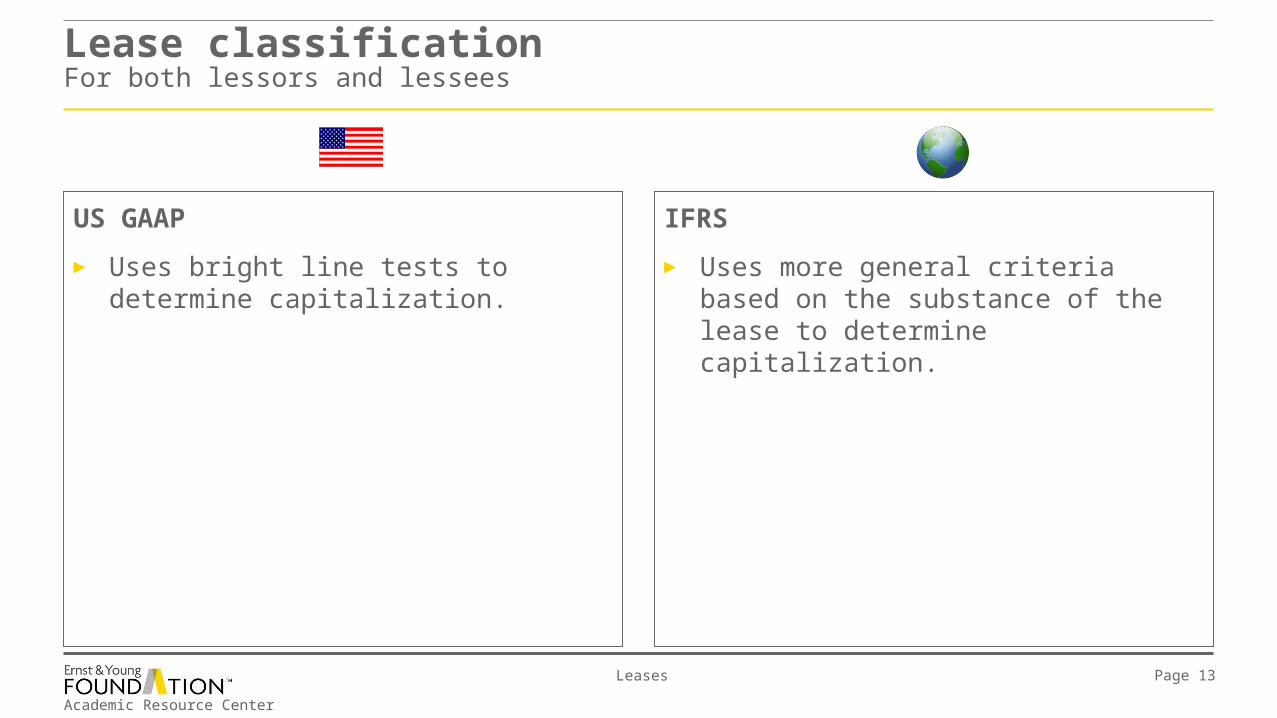

IFRS

► Uses more general criteria based on the substance of the lease to determine capitalization.

US GAAP

► Uses bright line tests to determine capitalization.

Academic Resource Center

Leases Page 14

Lease classificationFor lessors

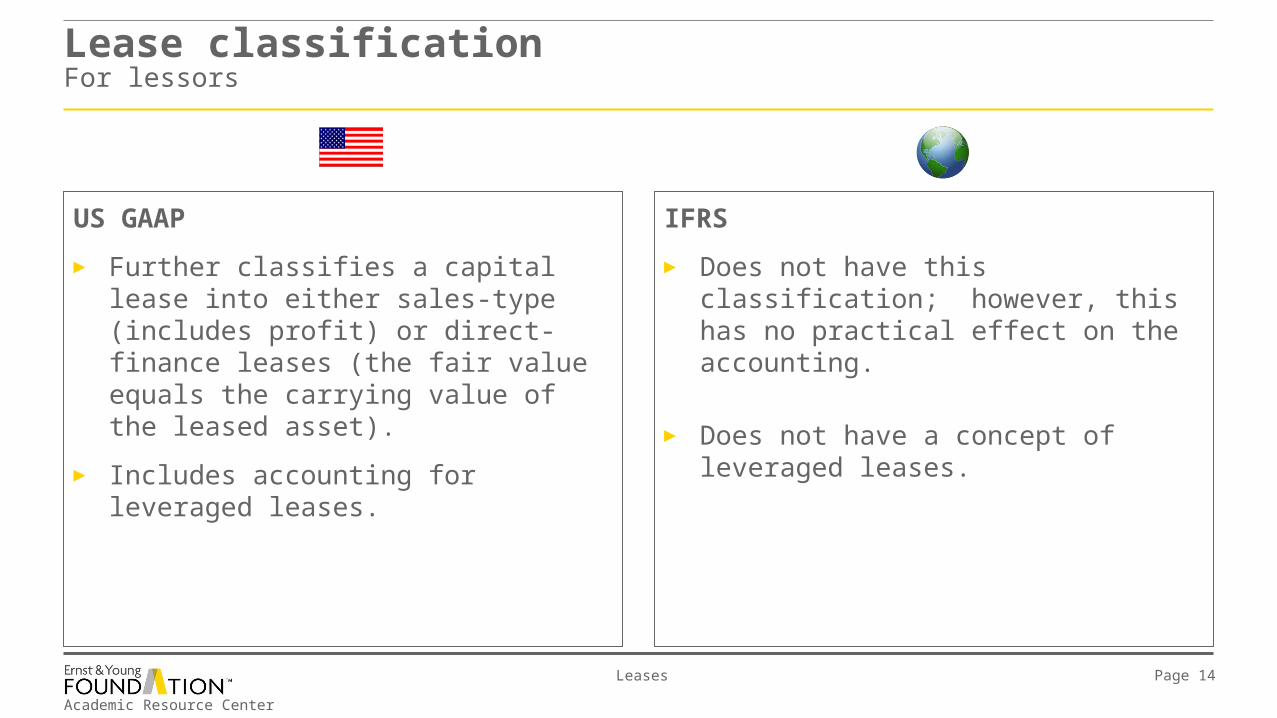

IFRS

► Does not have this classification; however, this has no practical effect on the accounting.

► Does not have a concept of leveraged leases.

US GAAP

► Further classifies a capital lease into either sales-type (includes profit) or direct-finance leases (the fair value equals the carrying value of the leased asset).

► Includes accounting for leveraged leases.

Academic Resource Center

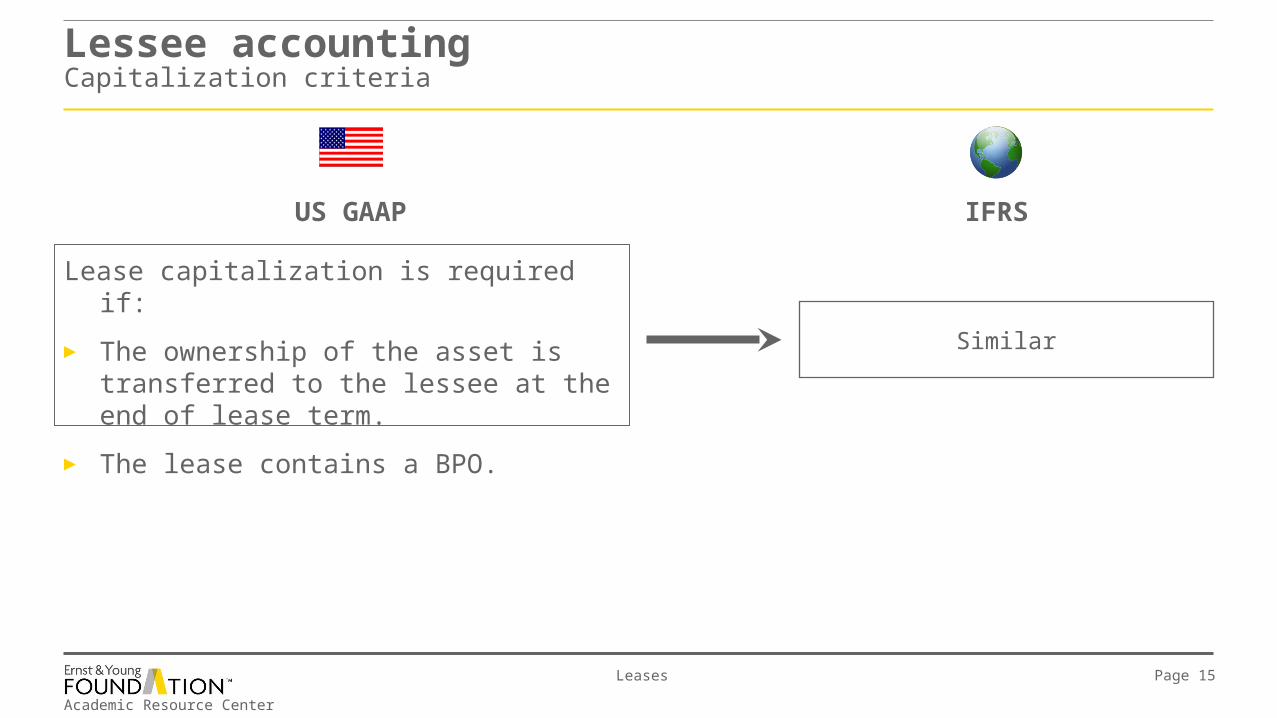

Leases Page 15

Lessee accountingCapitalization criteria

IFRSUS GAAP

Similar

Lease capitalization is required if:

► The ownership of the asset is transferred to the lessee at the end of lease term.

► The lease contains a BPO.

Academic Resource Center

Leases Page 16

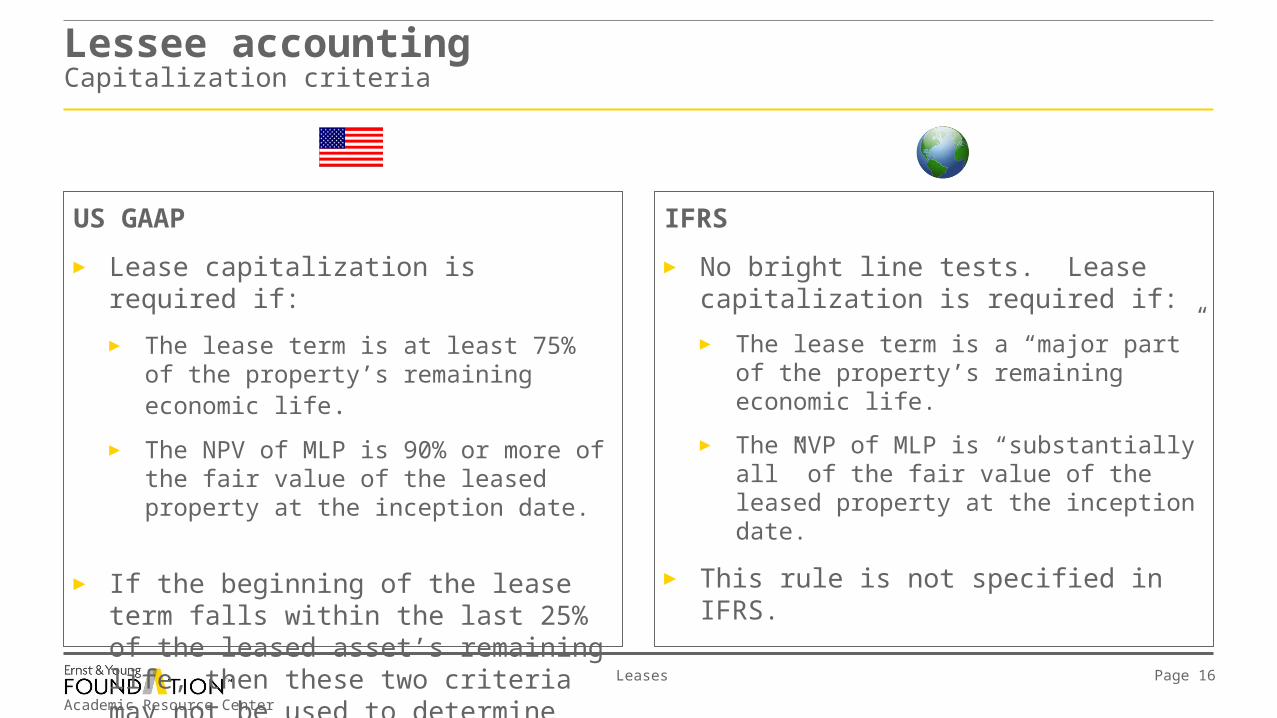

Lessee accountingCapitalization criteria

IFRS

► No bright line tests. Lease capitalization is required if:

► The lease term is a “major part” of the property’s remaining economic life.

► The NVP of MLP is “substantially all” of the fair value of the leased property at the inception date.

► This rule is not specified in IFRS.

US GAAP

► Lease capitalization is required if:

► The lease term is at least 75% of the property’s remaining economic life.

► The NPV of MLP is 90% or more of the fair value of the leased property at the inception date.

► If the beginning of the lease term falls within the last 25% of the leased asset’s remaining life, then these two criteria may not be used to determine capitalization.

Academic Resource Center

Leases Page 17

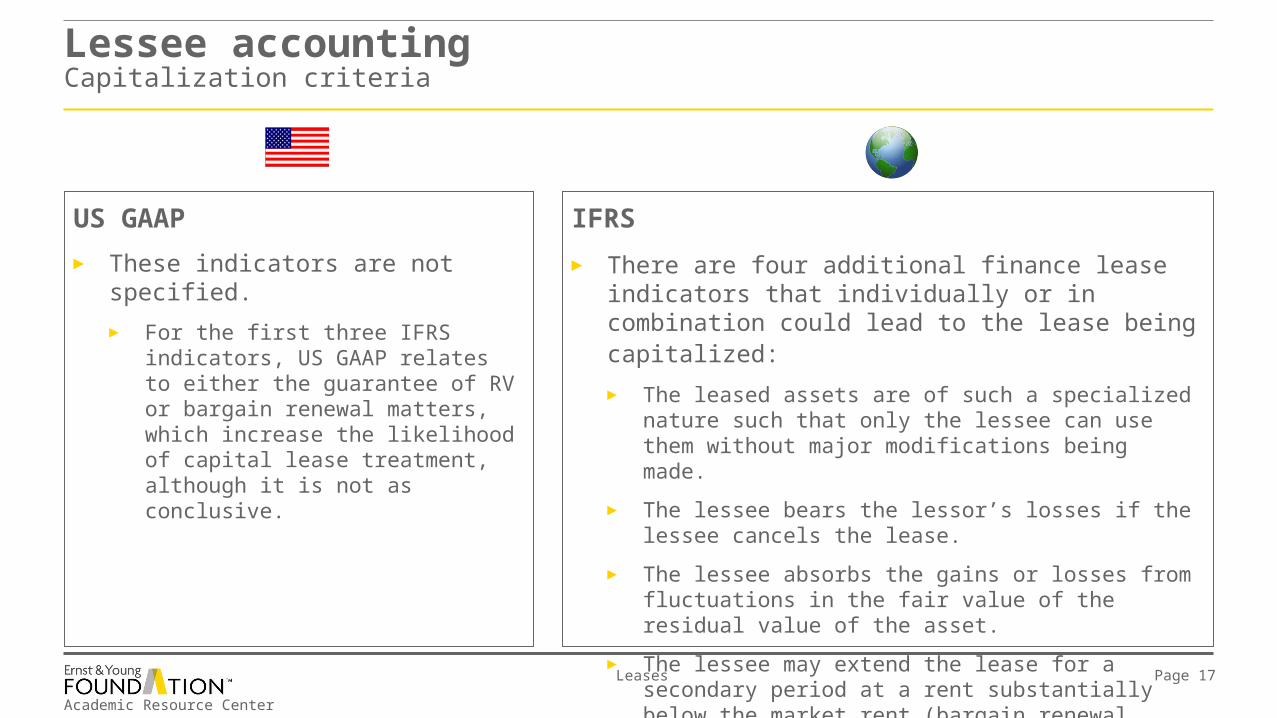

Lessee accountingCapitalization criteria

IFRS

► There are four additional finance lease indicators that individually or in combination could lead to the lease being capitalized: ► The leased assets are of such a specialized nature such

that only the lessee can use them without major modifications being made.

► The lessee bears the lessor’s losses if the lessee cancels the lease.

► The lessee absorbs the gains or losses from fluctuations in the fair value of the residual value of the asset.

► The lessee may extend the lease for a secondary period at a rent substantially below the market rent (bargain renewal option).

US GAAP

► These indicators are not specified.

► For the first three IFRS indicators, US GAAP relates to either the guarantee of RV or bargain renewal matters, which increase the likelihood of capital lease treatment, although it is not as conclusive.

Academic Resource Center

Leases Page 18

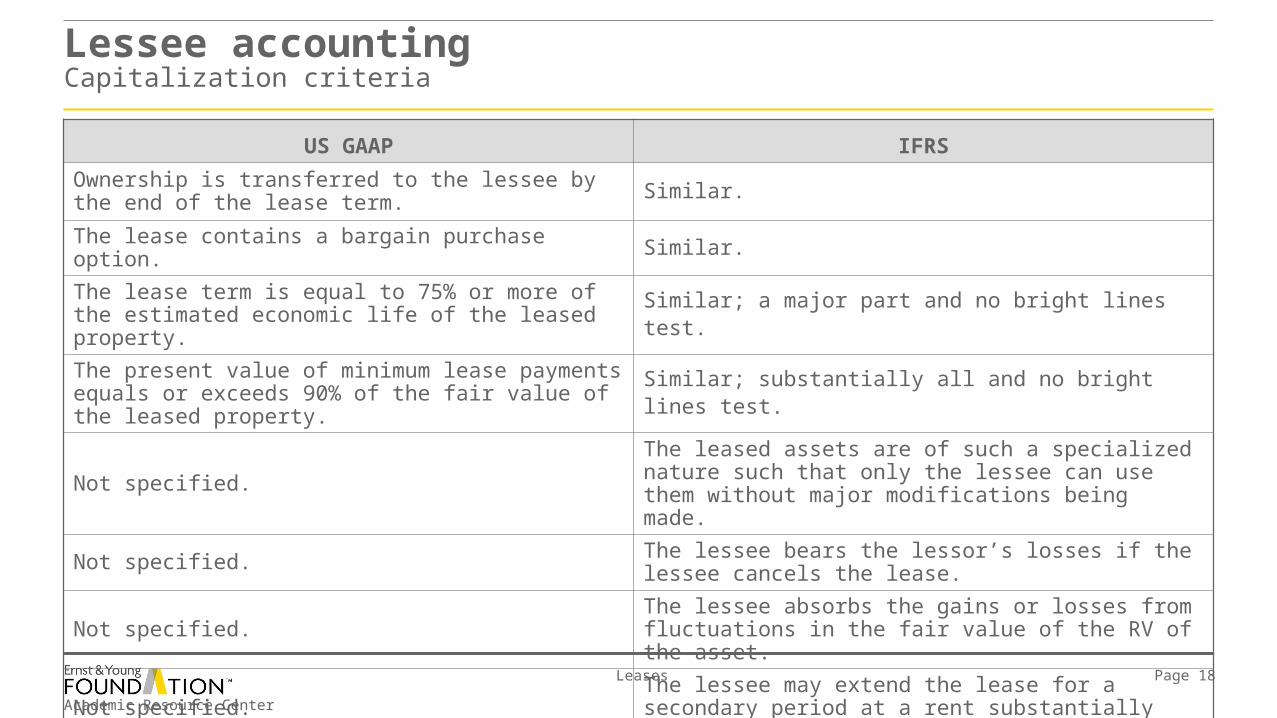

Lessee accountingCapitalization criteria

US GAAP IFRS

Ownership is transferred to the lessee by the end of the lease term. Similar.

The lease contains a bargain purchase option. Similar.

The lease term is equal to 75% or more of the estimated economic life of the leased property. Similar; a major part and no bright lines test.

The present value of minimum lease payments equals or exceeds 90% of the fair value of the leased property. Similar; substantially all and no bright lines test.

Not specified.The leased assets are of such a specialized nature such that only the lessee can use them without major modifications being made.

Not specified. The lessee bears the lessor’s losses if the lessee cancels the lease.

Not specified. The lessee absorbs the gains or losses from fluctuations in the fair value of the RV of the asset.

Not specified. The lessee may extend the lease for a secondary period at a rent substantially below the market rent.

Academic Resource Center

Leases Page 19

Example 1 – Lease classification for lessee

RRI entered into a lease on January 1, 2010, with Magical Mobile Transport (MMT) for a customized carriage. MMT will provide a carriage to RRI that has RRI’s logo molded into the iron work of the frame, carved into various areas of the woodwork and painted on the side of the doors. Additionally, MMT is providing custom-made pulling devices on the carriage to accommodate RRI’s Clydesdale horses.

See next slide for terms of the lease arrangement.

Lease classification for lessee example

► Determine if RRI should record this lease as an operating or capital lease, using US GAAP.

► Determine if RRI should record this lease as an operating or finance lease, using IFRS.

Academic Resource Center

Leases Page 20

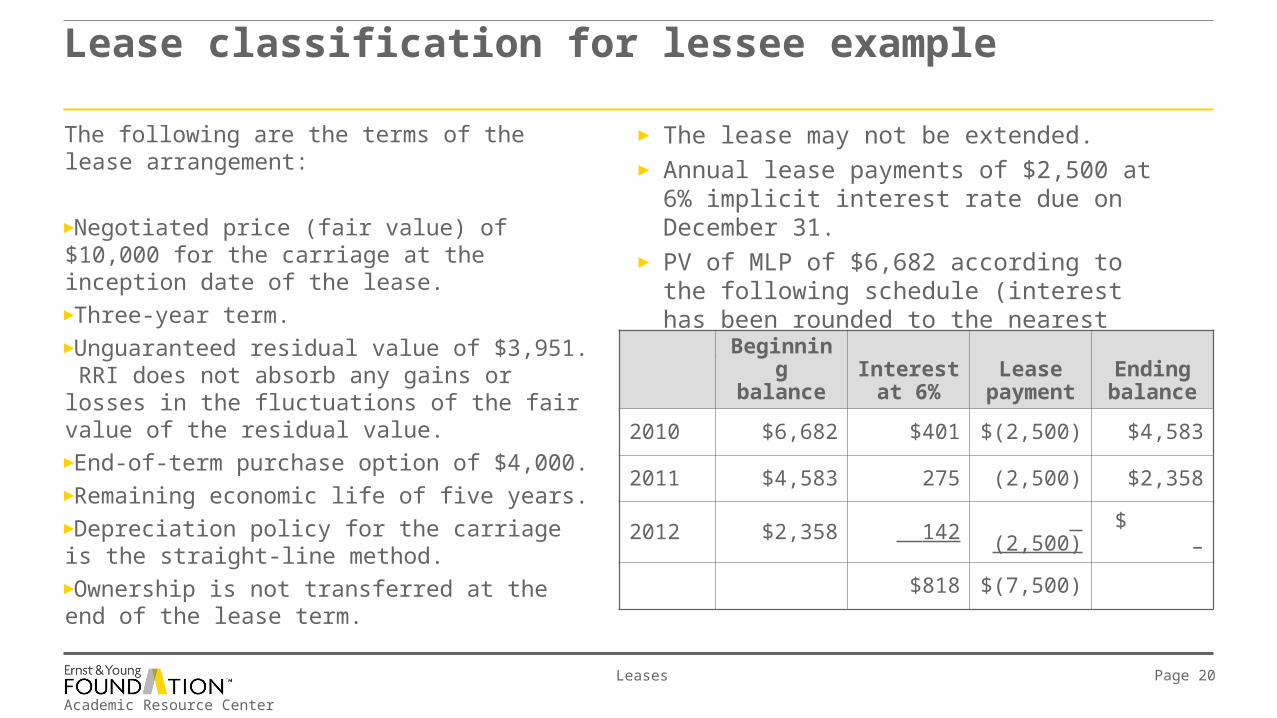

The following are the terms of the lease arrangement:

►Negotiated price (fair value) of $10,000 for the carriage at the inception date of the lease.►Three-year term.►Unguaranteed residual value of $3,951. RRI does not absorb any gains or losses in the fluctuations of the fair value of the residual value.►End-of-term purchase option of $4,000.►Remaining economic life of five years.►Depreciation policy for the carriage is the straight-line method.►Ownership is not transferred at the end of the lease term.

Lease classification for lessee example

► The lease may not be extended.► Annual lease payments of $2,500 at 6% implicit

interest rate due on December 31. ► PV of MLP of $6,682 according to the following

schedule (interest has been rounded to the nearest dollar):

Beginning balance

Interest at 6%

Lease payment

Ending balance

2010 $6,682 $401 $(2,500) $4,583

2011 $4,583 275 (2,500) $2,358

2012 $2,358 142 (2,500) $ –

$818 $(7,500)

Academic Resource Center

Leases Page 21

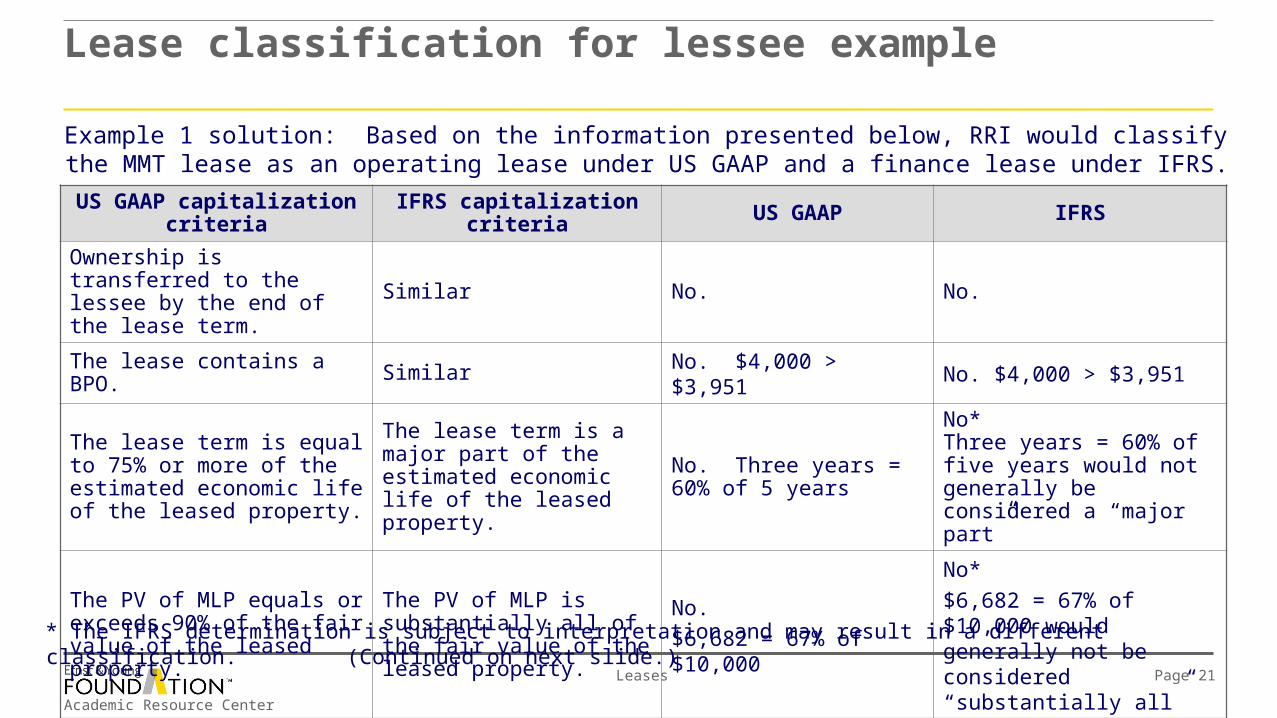

Example 1 solution: Based on the information presented below, RRI would classify the MMT lease as an operating lease under US GAAP and a finance lease under IFRS.

Lease classification for lessee example

US GAAP capitalization criteria IFRS capitalization criteria US GAAP IFRS

Ownership is transferred to the lessee by the end of the lease term.

Similar No. No.

The lease contains a BPO. Similar No. $4,000 > $3,951 No. $4,000 > $3,951

The lease term is equal to 75% or more of the estimated economic life of the leased property.

The lease term is a major part of the estimated economic life of the leased property.

No. Three years = 60% of 5 years

No*Three years = 60% of five years would not generally be considered a “major part”

The PV of MLP equals or exceeds 90% of the fair value of the leased property.

The PV of MLP is substantially all of the fair value of the leased property.

No.

$6,682 = 67% of $10,000

No*

$6,682 = 67% of $10,000 would generally not be considered “substantially all”

* The IFRS determination is subject to interpretation and may result in a different classification. (Continued on next slide.)

Academic Resource Center

Leases Page 22

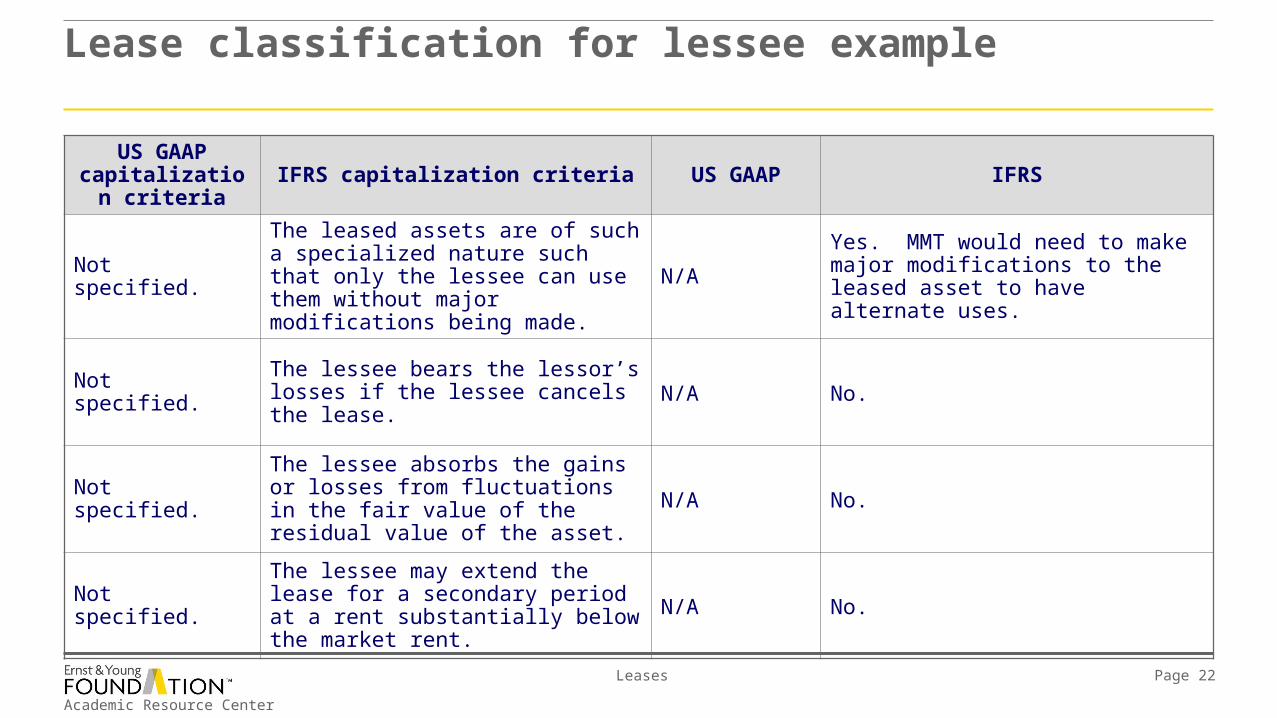

Lease classification for lessee example

US GAAP capitalization

criteriaIFRS capitalization criteria US GAAP IFRS

Not specified.

The leased assets are of such a specialized nature such that only the lessee can use them without major modifications being made.

N/AYes. MMT would need to make major modifications to the leased asset to have alternate uses.

Not specified. The lessee bears the lessor’s losses if the lessee cancels the lease. N/A No.

Not specified. The lessee absorbs the gains or losses from fluctuations in the fair value of the residual value of the asset.

N/A No.

Not specified. The lessee may extend the lease for a secondary period at a rent substantially below the market rent.

N/A No.

Academic Resource Center

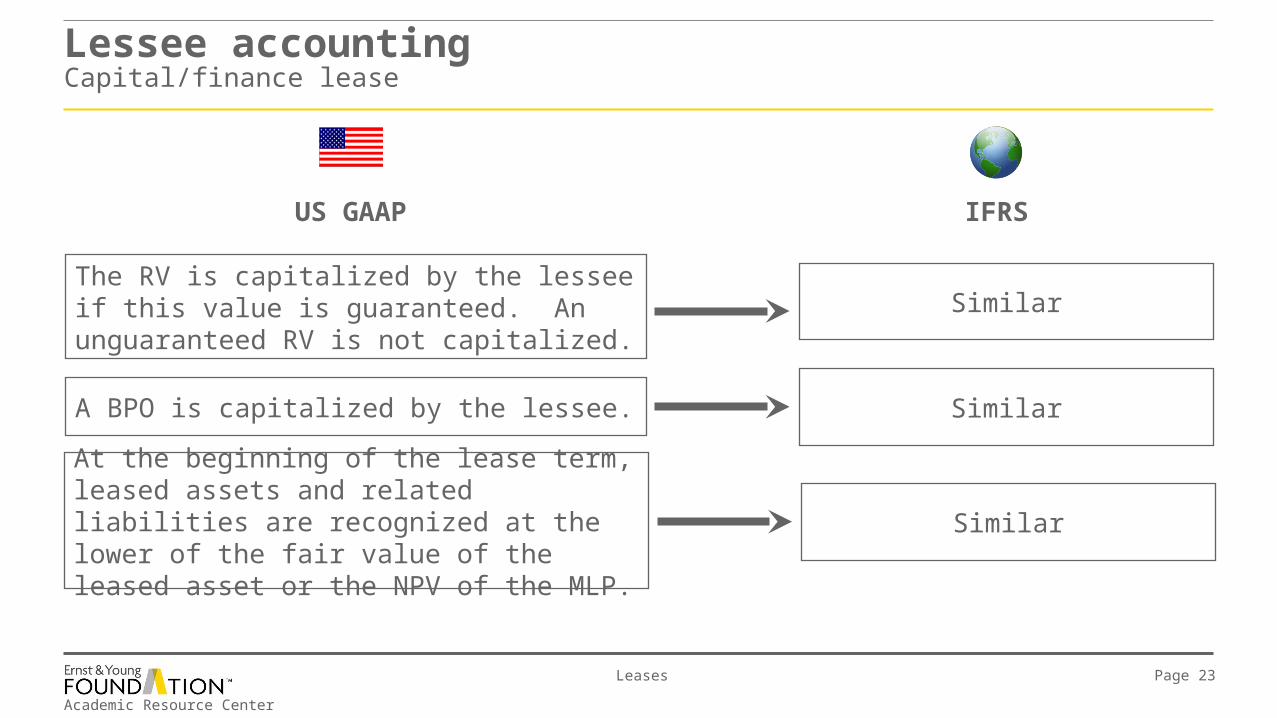

Leases Page 23

Lessee accountingCapital/finance lease

The RV is capitalized by the lessee if this value is guaranteed. An unguaranteed RV is not capitalized.

A BPO is capitalized by the lessee.

Similar

Similar

IFRSUS GAAP

At the beginning of the lease term, leased assets and related liabilities are recognized at the lower of the fair value of the leased asset or the NPV of the MLP.

Similar

Academic Resource Center

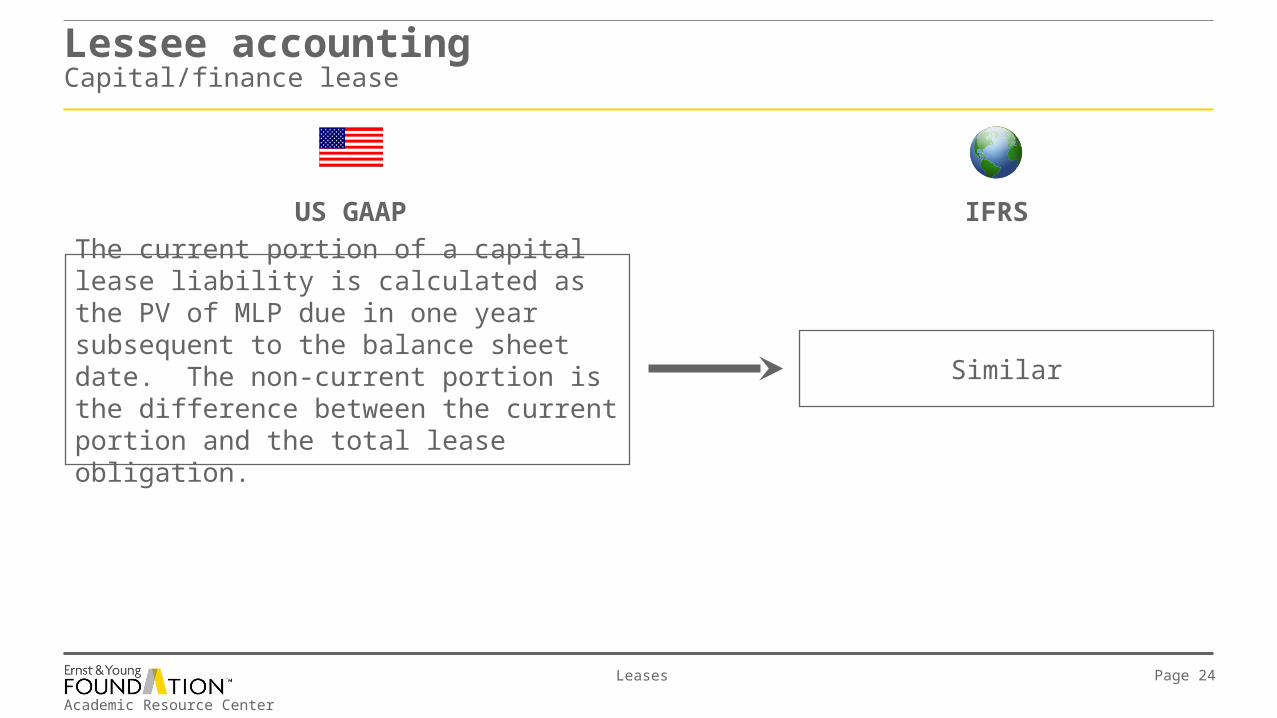

Leases Page 24

Lessee accountingCapital/finance lease

The current portion of a capital lease liability is calculated as the PV of MLP due in one year subsequent to the balance sheet date. The non-current portion is the difference between the current portion and the total lease obligation.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 25

Lessee accountingCapital/finance lease

IFRS

► The rate implicit in the lease is used to discount MLP, if practicable to determine (this is not common in practice because it is a key factor in the lessor’s business model to determine profitability); otherwise, the incremental borrowing rate should be used. No evaluation is made regarding which rate is lower.

US GAAP

► To calculate the NPV of MLP, the lessee’s incremental borrowing rate is used, unless the lessor’s implicit rate can be determined and is less.

Academic Resource Center

Leases Page 26

Example 2 – interest rate determination

On January 1, 2010, RRI entered into a lease with Bob’s Antique Cars (BAC) for an antique roadster with the following terms:

► Negotiated price (fair value) of $20,000 for the antique roadster at the inception date of the lease.► Term of seven years.► Unguaranteed residual value of $5,124. RRI does not absorb any gains or losses in the fluctuations of

the fair value of the residual value.► End-of-term purchase option of $12,000.► Implicit annual interest rate (disclosed to RRI by BAC) of 5%.► Incremental annual borrowing rate of 5.25%.► Payments of $3,000 per year due on December 31.► Remaining economic life of 10 years.► Depreciation policy for the auto is the straight-line method.► Ownership is not transferred at the end of the lease term.► The lease may not be extended.

Lease classification for lessee including interest rate determination example

Academic Resource Center

Leases Page 27

Lease classification for lessee including interest rate determination example

Part I:

► Determine if RRI should record this lease as an operating or capital lease using US GAAP.

► Determine if RRI should record this lease as an operating or finance lease using IFRS.

Part II:

► Assume RRI had an incremental borrowing rate of 4%. Would this change the results of the lease classification, using US GAAP or IFRS?

Note: Round dollar amounts to the nearest dollar when calculating the PV of MLP.

Academic Resource Center

Leases Page 28

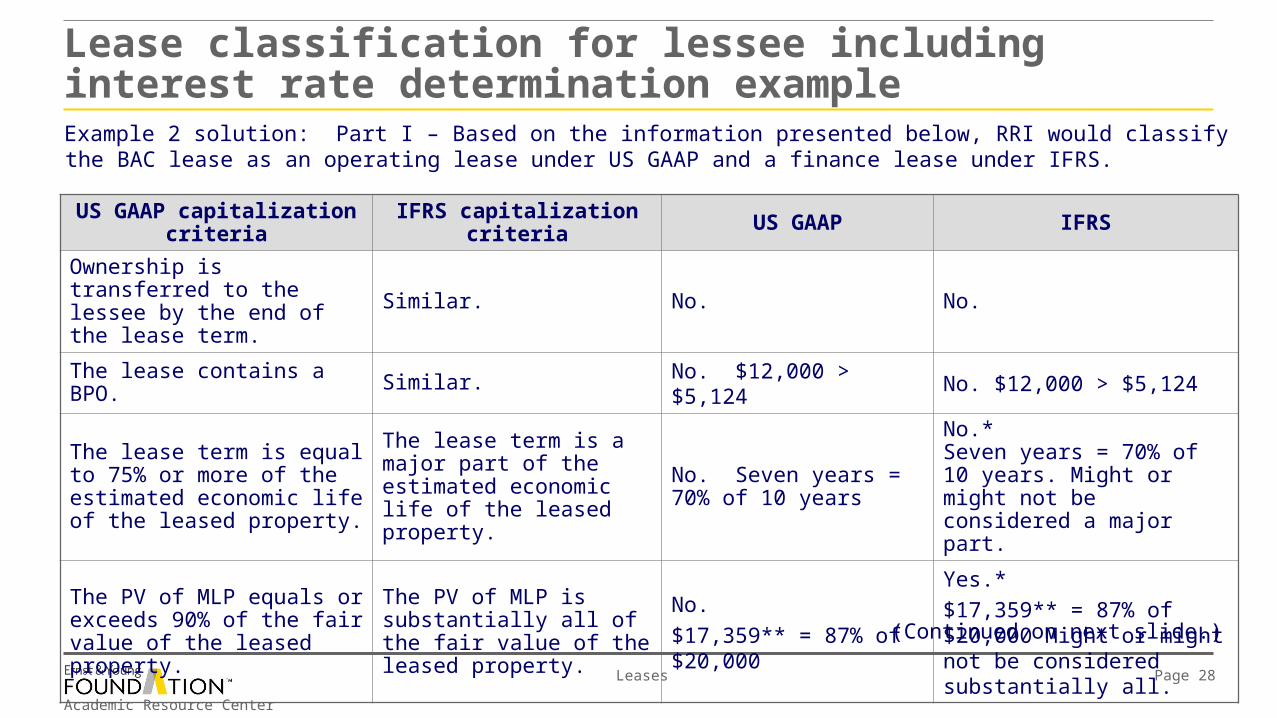

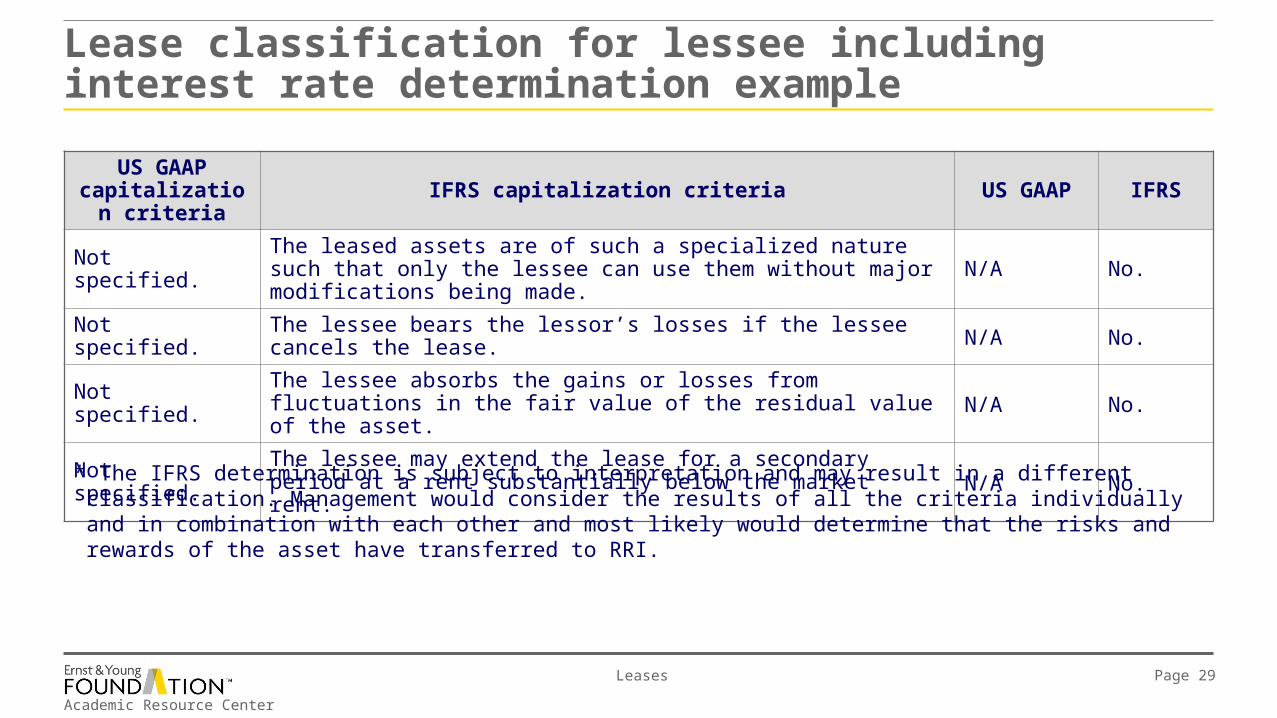

Example 2 solution: Part I – Based on the information presented below, RRI would classify the BAC lease as an operating lease under US GAAP and a finance lease under IFRS.

Lease classification for lessee including interest rate determination example

US GAAP capitalization criteria IFRS capitalization criteria US GAAP IFRS

Ownership is transferred to the lessee by the end of the lease term.

Similar. No. No.

The lease contains a BPO. Similar. No. $12,000 > $5,124 No. $12,000 > $5,124

The lease term is equal to 75% or more of the estimated economic life of the leased property.

The lease term is a major part of the estimated economic life of the leased property.

No. Seven years = 70% of 10 years

No.*Seven years = 70% of 10 years. Might or might not be considered a major part.

The PV of MLP equals or exceeds 90% of the fair value of the leased property.

The PV of MLP is substantially all of the fair value of the leased property.

No.

$17,359** = 87% of $20,000

Yes.*

$17,359** = 87% of $20,000 Might or might not be considered substantially all.

(Continued on next slide.)

Academic Resource Center

Leases Page 29

Lease classification for lessee including interest rate determination example

US GAAP capitalization

criteriaIFRS capitalization criteria US GAAP IFRS

Not specified. The leased assets are of such a specialized nature such that only the lessee can use them without major modifications being made. N/A No.

Not specified. The lessee bears the lessor’s losses if the lessee cancels the lease. N/A No.

Not specified. The lessee absorbs the gains or losses from fluctuations in the fair value of the residual value of the asset. N/A No.

Not specified. The lessee may extend the lease for a secondary period at a rent substantially below the market rent. N/A No.

* The IFRS determination is subject to interpretation and may result in a different classification. Management would consider the results of all the criteria individually and in combination with each other and most likely would determine that the risks and rewards of the asset have transferred to RRI.

Academic Resource Center

Leases Page 30

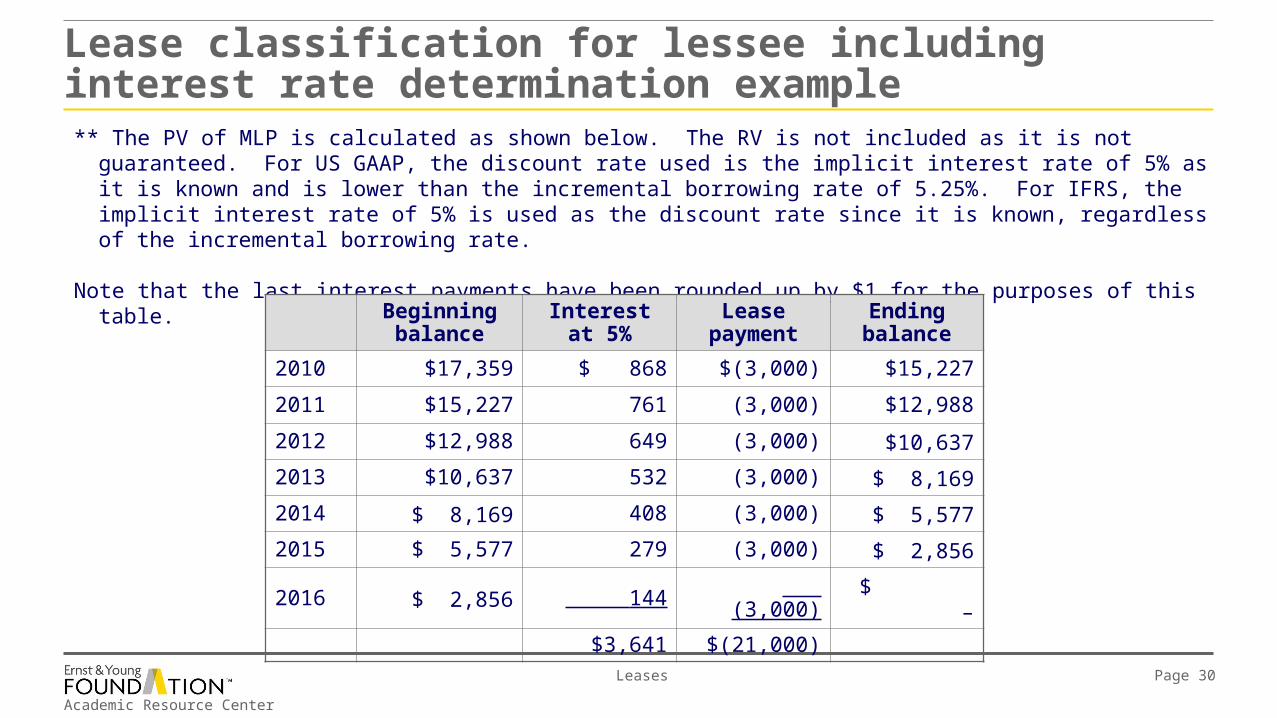

Lease classification for lessee including interest rate determination example** The PV of MLP is calculated as shown below. The RV is not included as it is not guaranteed. For US GAAP, the

discount rate used is the implicit interest rate of 5% as it is known and is lower than the incremental borrowing rate of 5.25%. For IFRS, the implicit interest rate of 5% is used as the discount rate since it is known, regardless of the incremental borrowing rate.

Note that the last interest payments have been rounded up by $1 for the purposes of this table.

Beginning balance

Interest at 5%

Lease payment

Ending balance

2010 $17,359 $ 868 $(3,000) $15,227

2011 $15,227 761 (3,000) $12,988

2012 $12,988 649 (3,000) $10,637

2013 $10,637 532 (3,000) $ 8,169

2014 $ 8,169 408 (3,000) $ 5,577

2015 $ 5,577 279 (3,000) $ 2,856

2016 $ 2,856 144 (3,000) $ –

$3,641 $(21,000)

Academic Resource Center

Leases Page 31

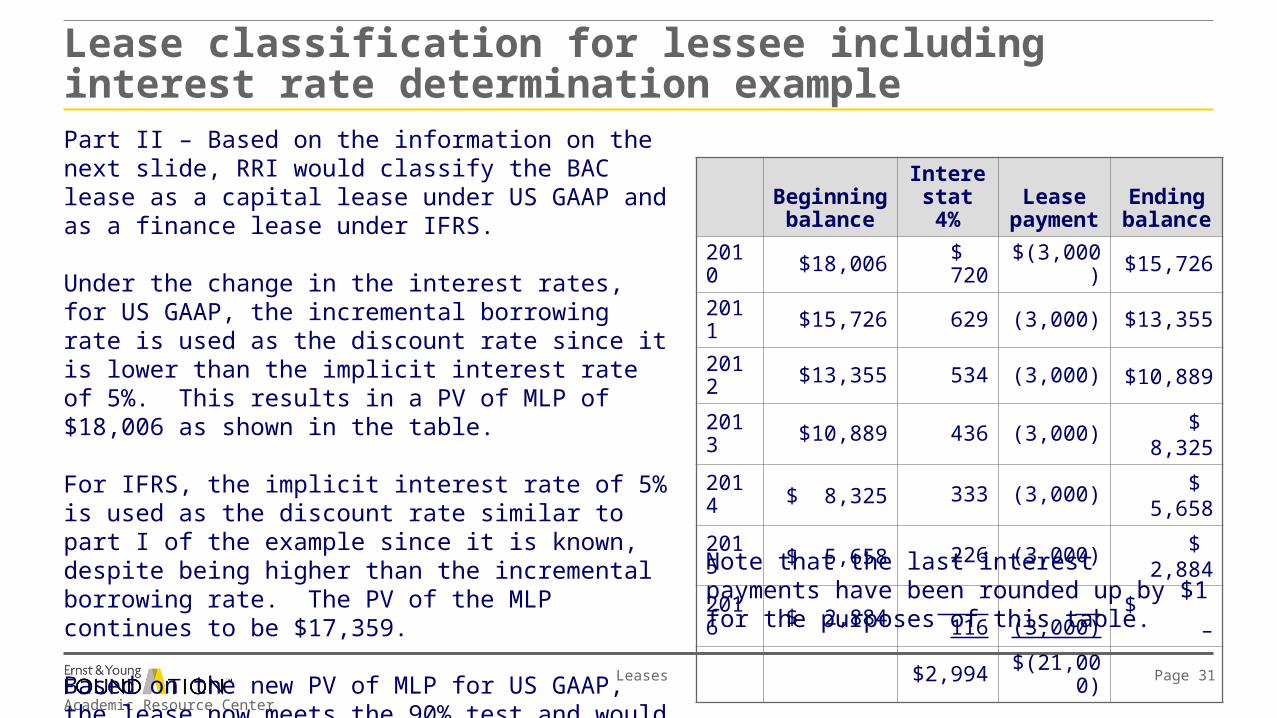

Lease classification for lessee including interest rate determination examplePart II – Based on the information on the next slide, RRI would classify the BAC lease as a capital lease under US GAAP and as a finance lease under IFRS.

Under the change in the interest rates, for US GAAP, the incremental borrowing rate is used as the discount rate since it is lower than the implicit interest rate of 5%. This results in a PV of MLP of $18,006 as shown in the table.

For IFRS, the implicit interest rate of 5% is used as the discount rate similar to part I of the example since it is known, despite being higher than the incremental borrowing rate. The PV of the MLP continues to be $17,359.

Based on the new PV of MLP for US GAAP, the lease now meets the 90% test and would be classified as a capital lease.

Beginning balance

Interestat 4%

Lease payment

Ending balance

2010 $18,006 $ 720 $(3,000) $15,726

2011 $15,726 629 (3,000) $13,355

2012 $13,355 534 (3,000) $10,889

2013 $10,889 436 (3,000) $ 8,325

2014 $ 8,325 333 (3,000) $ 5,658

2015 $ 5,658 226 (3,000) $ 2,884

2016 $ 2,884 116 (3,000) $ –

$2,994 $(21,000)

Note that the last interest payments have been rounded up by $1 for the purposes of this table.

Academic Resource Center

Leases Page 32

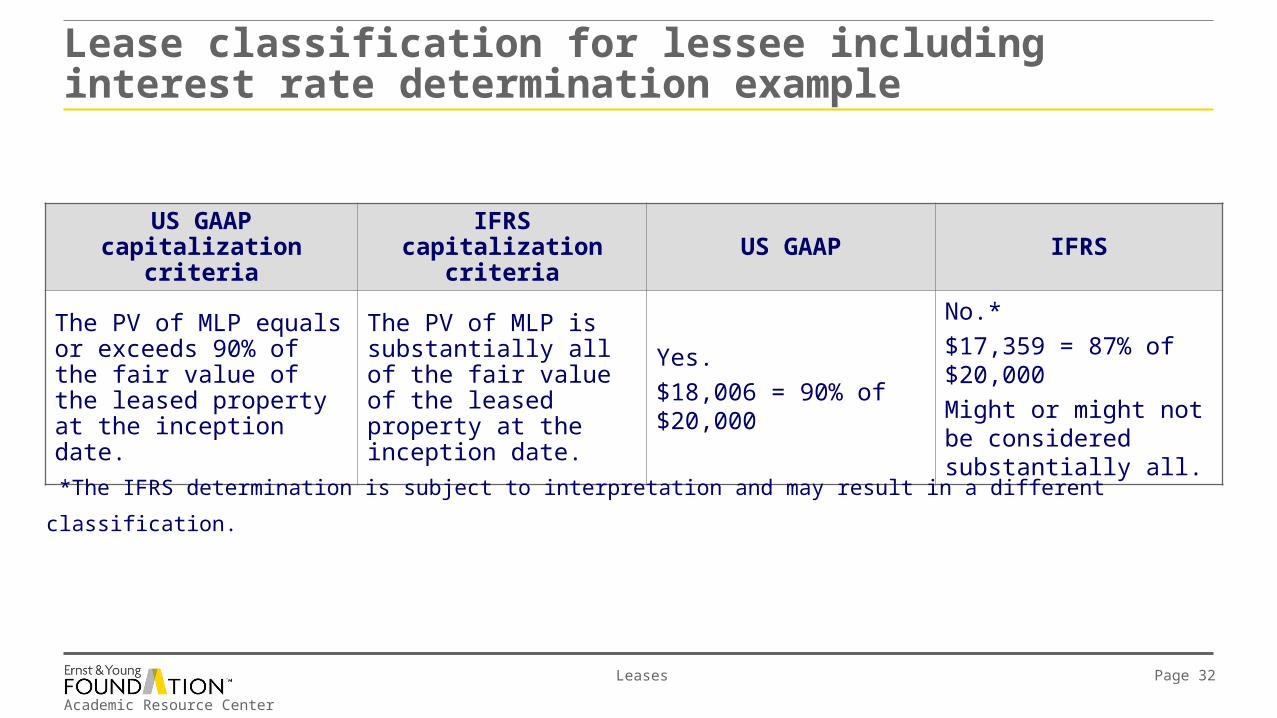

Lease classification for lessee including interest rate determination example

US GAAP capitalization criteria

IFRS capitalization criteria US GAAP IFRS

The PV of MLP equals or exceeds 90% of the fair value of the leased property at the inception date.

The PV of MLP is substantially all of the fair value of the leased property at the inception date.

Yes.

$18,006 = 90% of $20,000

No.*

$17,359 = 87% of $20,000

Might or might not be considered substantially all.

*The IFRS determination is subject to interpretation and may result in a different classification.

Academic Resource Center

Leases Page 33

Lessee accountingCapital/finance lease – depreciation of a leased asset

Amounts capitalized for a leased asset are depreciated according to the method of the underlying asset.

The depreciation term is based on the capitalization indicators and the certainty of ownership.

Due to the reasonable certainty of ownership for the lease ownership transfer and BPO indicators, the life of the asset is used as the depreciation term if these indicators are met.

Similar

IFRSUS GAAP

Similar

Academic Resource Center

Leases Page 34

Lessee accountingCapital/finance lease – depreciation of a leased asset

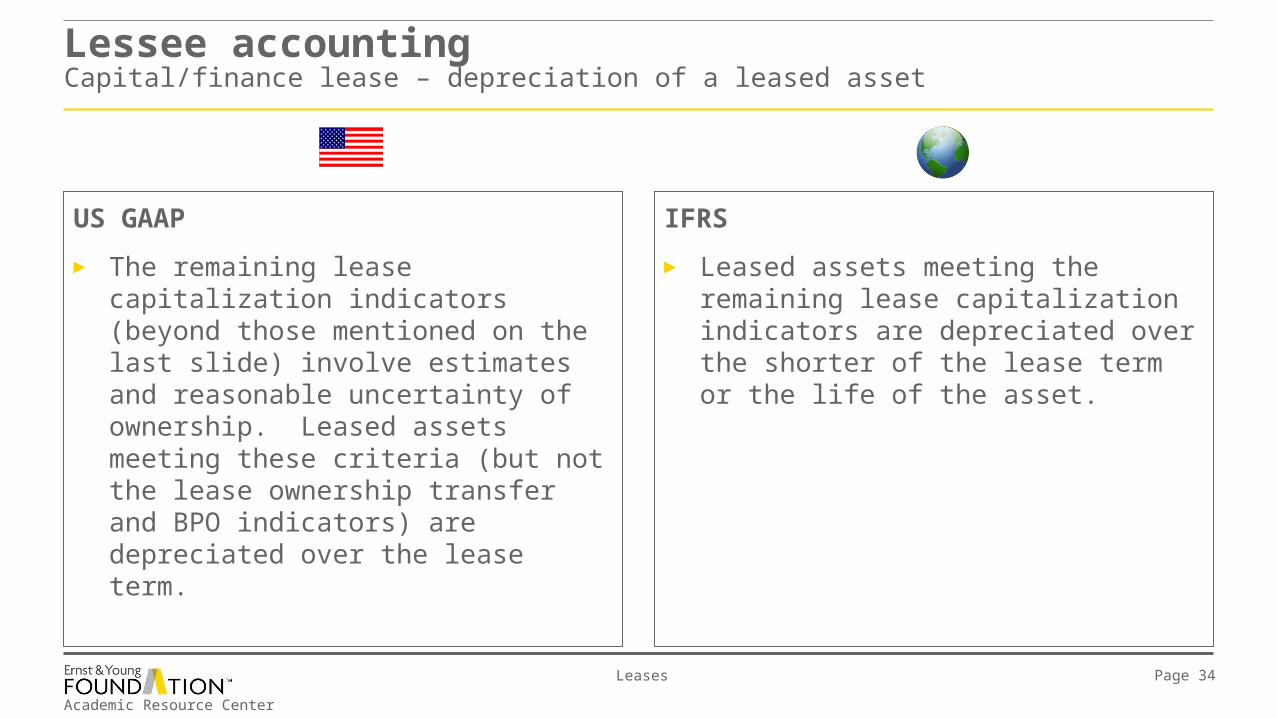

IFRS

► Leased assets meeting the remaining lease capitalization indicators are depreciated over the shorter of the lease term or the life of the asset.

US GAAP

► The remaining lease capitalization indicators (beyond those mentioned on the last slide) involve estimates and reasonable uncertainty of ownership. Leased assets meeting these criteria (but not the lease ownership transfer and BPO indicators) are depreciated over the lease term.

Academic Resource Center

Leases Page 35

Lessee accountingOperating lease

Lease payments are recorded as an expense when due.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 36

Lease accounting example

Example 3 – lease accounting

► Based on the information and lease classification determined in examples 1 and 2 (part I), prepare the journal entries for RRI for 2010, using US GAAP.

► Based on the information and lease classification determined in examples 1 and 2 (part I), prepare the journal entries for RRI for 2010, using IFRS.

Academic Resource Center

Leases Page 37

Lease accounting example

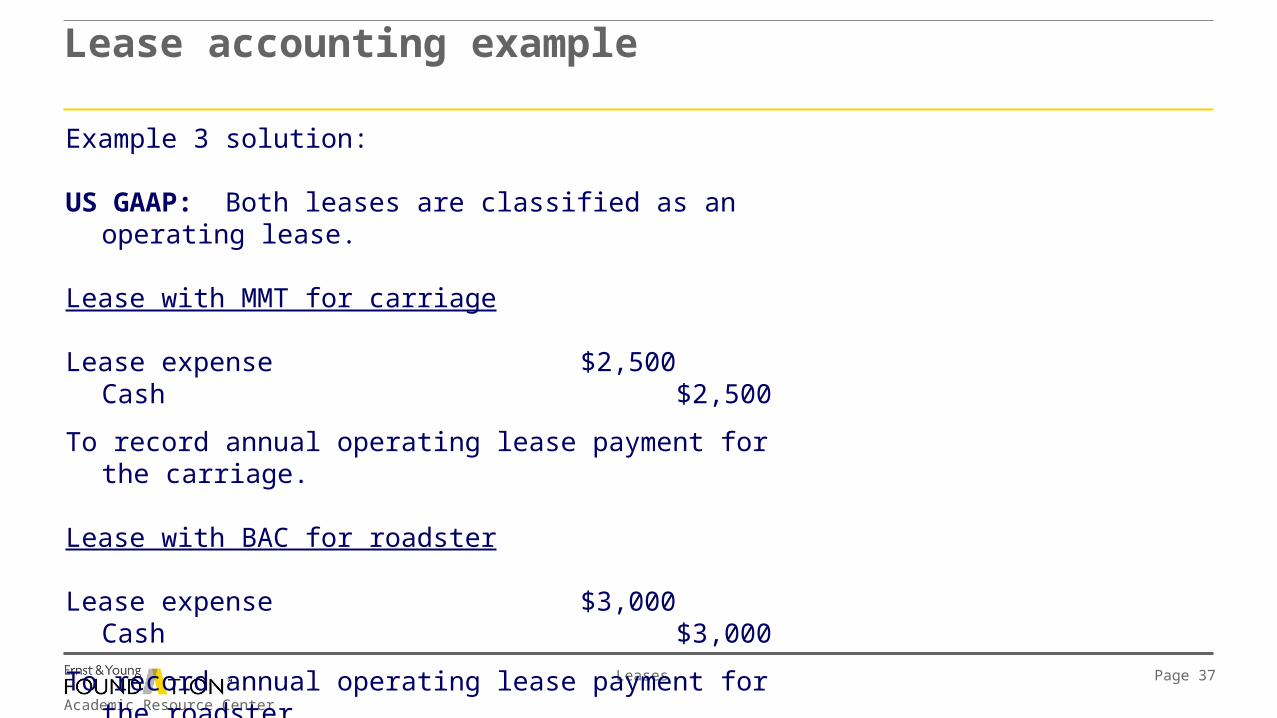

Example 3 solution:

US GAAP: Both leases are classified as an operating lease.

Lease with MMT for carriage

Lease expense $2,500Cash $2,500

To record annual operating lease payment for the carriage.

Lease with BAC for roadster

Lease expense $3,000Cash $3,000

To record annual operating lease payment for the roadster.

Academic Resource Center

Leases Page 38

Lease accounting example

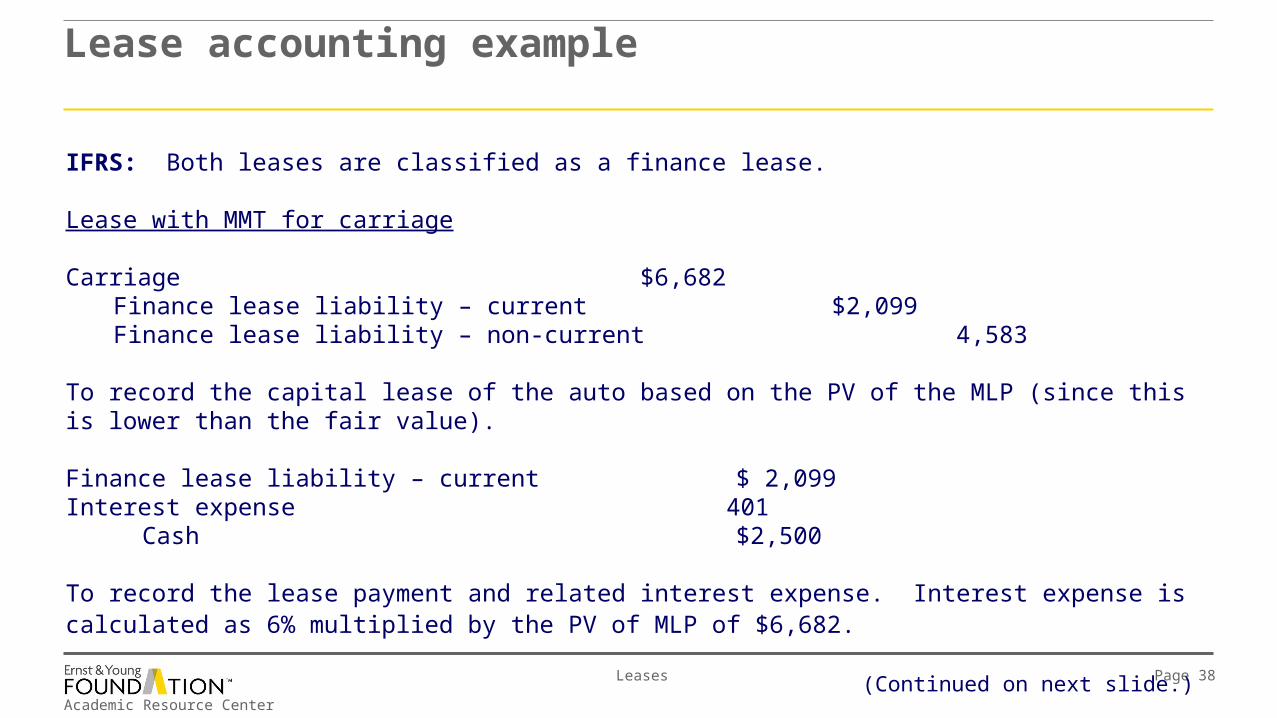

IFRS: Both leases are classified as a finance lease.

Lease with MMT for carriage

Carriage $6,682Finance lease liability – current $2,099Finance lease liability – non-current 4,583

To record the capital lease of the auto based on the PV of the MLP (since this is lower than the fair value).

Finance lease liability – current $ 2,099Interest expense 401

Cash $2,500

To record the lease payment and related interest expense. Interest expense is calculated as 6% multiplied by the PV of MLP of $6,682.

(Continued on next slide.)

Academic Resource Center

Leases Page 39

Lease accounting example

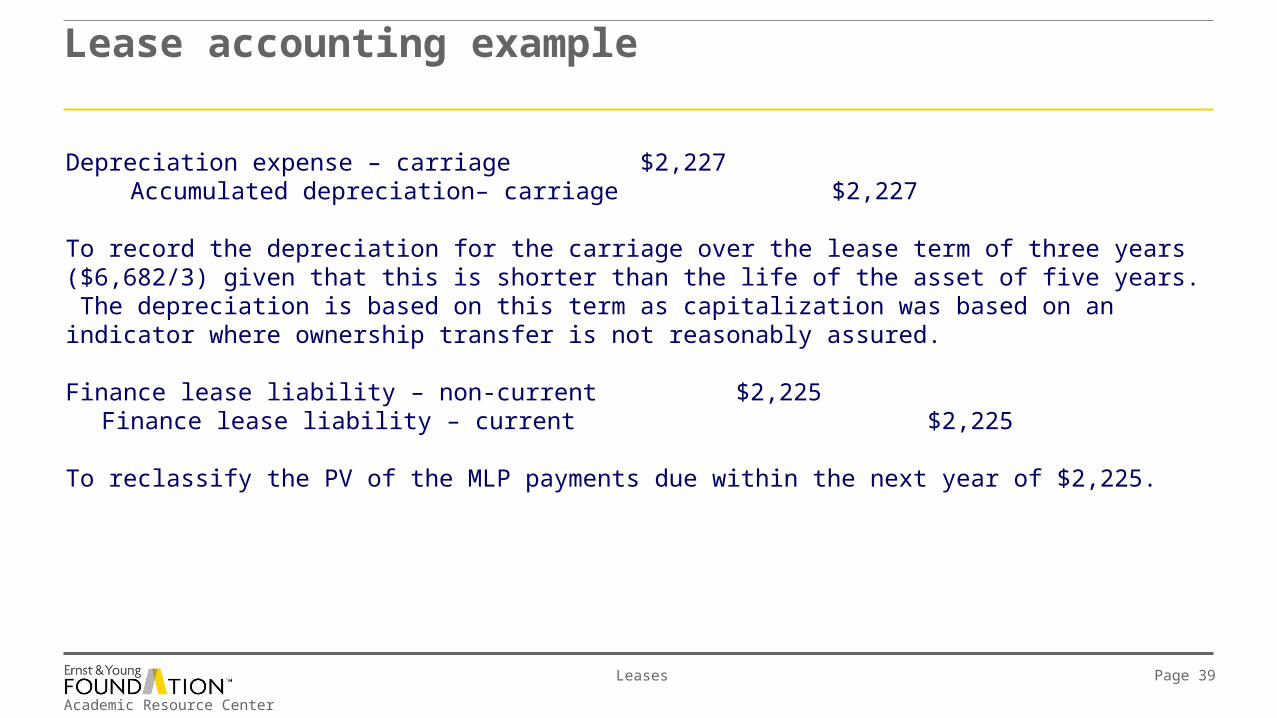

Depreciation expense – carriage $2,227 Accumulated depreciation– carriage $2,227

To record the depreciation for the carriage over the lease term of three years ($6,682/3) given that this is shorter than the life of the asset of five years. The depreciation is based on this term as capitalization was based on an indicator where ownership transfer is not reasonably assured.

Finance lease liability – non-current $2,225Finance lease liability – current $2,225

To reclassify the PV of the MLP payments due within the next year of $2,225.

Academic Resource Center

Leases Page 40

Lease accounting example

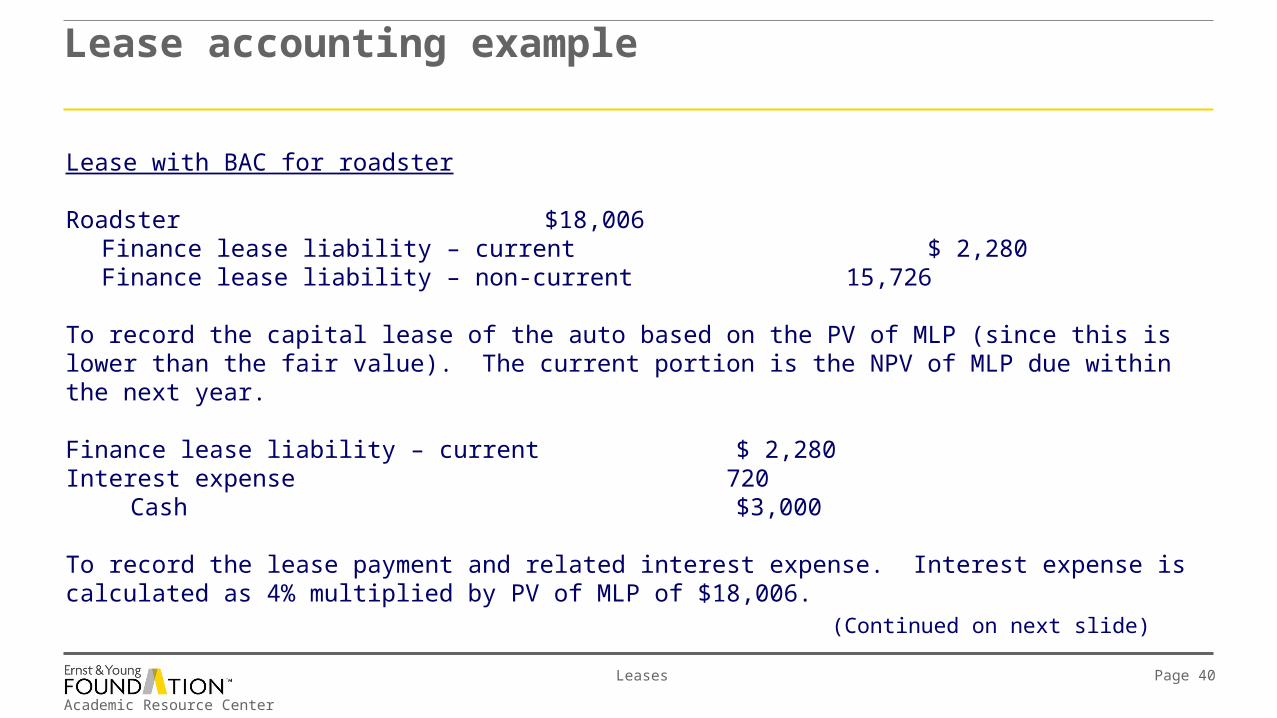

Lease with BAC for roadster

Roadster $18,006Finance lease liability – current $ 2,280Finance lease liability – non-current 15,726

To record the capital lease of the auto based on the PV of MLP (since this is lower than the fair value). The current portion is the NPV of MLP due within the next year.

Finance lease liability – current $ 2,280Interest expense 720

Cash $3,000

To record the lease payment and related interest expense. Interest expense is calculated as 4% multiplied by PV of MLP of $18,006.

(Continued on next slide)

Academic Resource Center

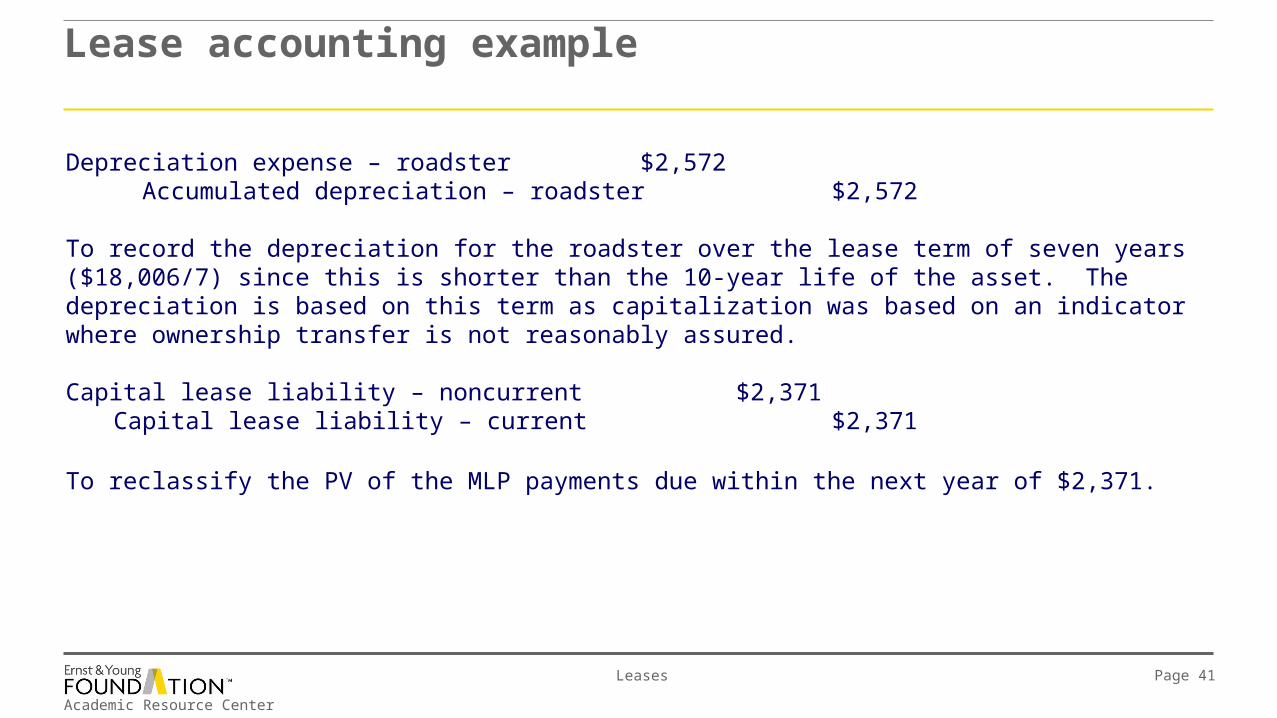

Leases Page 41

Lease accounting example

Depreciation expense – roadster $2,572 Accumulated depreciation – roadster $2,572

To record the depreciation for the roadster over the lease term of seven years ($18,006/7) since this is shorter than the 10-year life of the asset. The depreciation is based on this term as capitalization was based on an indicator where ownership transfer is not reasonably assured.

Capital lease liability – noncurrent $2,371Capital lease liability – current $2,371

To reclassify the PV of the MLP payments due within the next year of $2,371.

Academic Resource Center

Leases Page 42

Lessor accountingCapitalization criteria

Lessors apply the same criteria as lessees except that MLPs are viewed from the perspective of the lessor.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 43

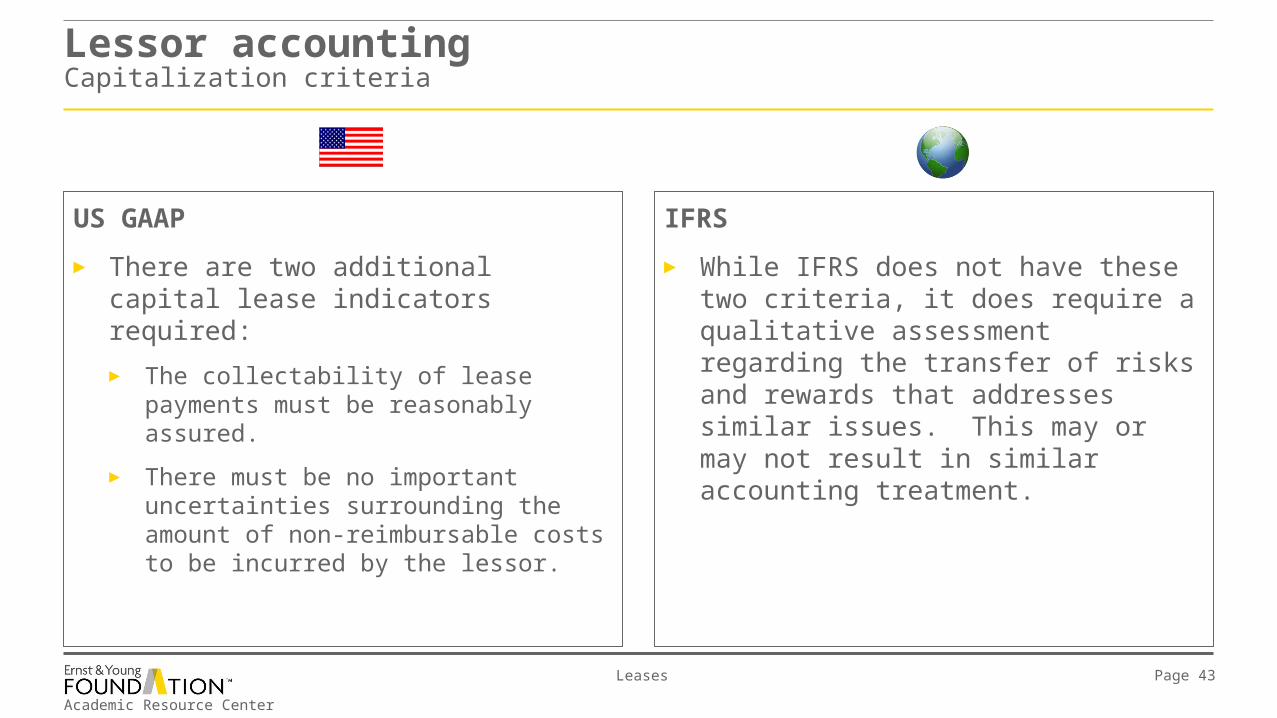

Lessor accountingCapitalization criteria

IFRS

► While IFRS does not have these two criteria, it does require a qualitative assessment regarding the transfer of risks and rewards that addresses similar issues. This may or may not result in similar accounting treatment.

US GAAP

► There are two additional capital lease indicators required:

► The collectability of lease payments must be reasonably assured.

► There must be no important uncertainties surrounding the amount of non-reimbursable costs to be incurred by the lessor.

Academic Resource Center

Leases Page 44

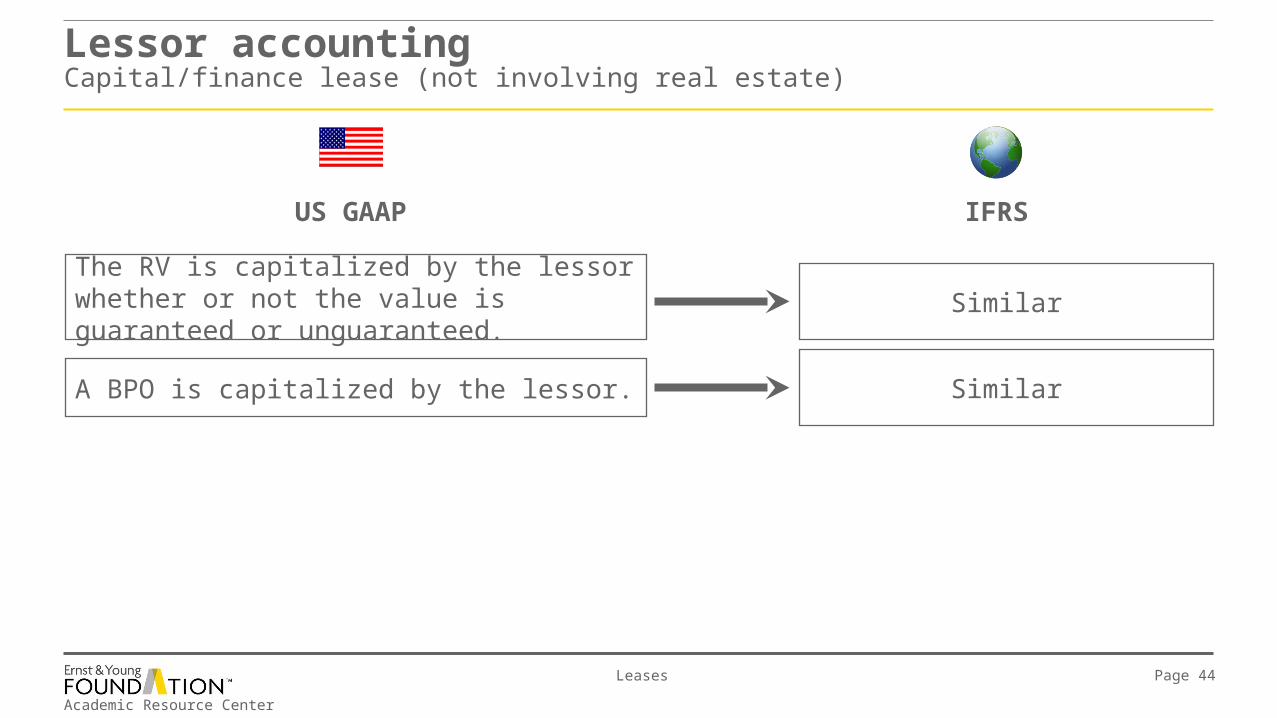

Lessor accountingCapital/finance lease (not involving real estate)

The RV is capitalized by the lessor whether or not the value is guaranteed or unguaranteed.

A BPO is capitalized by the lessor.

Similar

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 45

Lessor accountingCapital/finance lease (not involving real estate)

Initial direct costs include costs to initiate the lease such as credit checks, commissions, legal fees, agent fees, etc.

For direct-financing leases, these costs are capitalized as part of the net investment in the lease and amortized over the lease term to produce a constant periodic rate of return on the net investment (effective-interest method).

For sales-type leases, these costs are expensed in the same period as the recognition of the gain.

Similar, but for direct financing leases, these costs are first capitalized to the carrying value of the leased asset rather than being capitalized directly to the net investment in the lease, but this results in the same net investment in the lease and unearned income under both standards.

IFRS does not classify finance leases as sales-type, but the guidance directs manufacturers or dealer lessors (generally transacting sales-type leases) to expense these costs.

IFRSUS GAAP

Academic Resource Center

Leases Page 46

Lessor accountingCapital/finance lease (not involving real estate) – lease receivable

The interest rate implicit in a lease is the discount rate that, at the inception of the lease, causes the aggregate of the PV of the MLP and the residual value to be equal to the fair value of the asset, including any initial direct costs of the lessor.

The capital/finance lease receivable is recorded as the net investment in the lease, which is the carrying value of the leased asset including initial direct costs for non-sales-type leases. Alternatively, this net investment is calculated as the gross investment in the lease (the minimum lease payments and RV (whether guaranteed or unguaranteed)) less unearned interest income plus initial direct costs for non-sales-type leases.

Similar

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 47

Lessor accountingCapital/finance lease (not involving real estate) – lease receivable

The current portion of the capital lease receivable is receivable in one year subsequent to the balance sheet date. The non-current portion is the difference between the current portion and the total lease receivable.

Selling profit is recognized immediately in income.

Similar

Similar

IFRSUS GAAP

Interest income is recognized over the lease term using a constant rate of return.

Similar

Academic Resource Center

Leases Page 48

Lessor accountingOperating lease

Lease receipts are recognized as lease income on a straight-line basis over the period of the lease or another systematic basis.

Another systematic basis is used if it is more representative of the time pattern of the benefits from the leased asset’s use.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 49

Lessor accountingOperating lease

IFRS

► Initial direct costs are added to the carrying value of the leased assets and depreciated over the lease term on the same basis as the rental income, unless they are manufacturer or dealer lessors, in which case they must be expensed immediately. Although the deferral is recorded in different accounts, the result on income is the same.

US GAAP

► Initial direct costs are deferred and allocated over the lease term in proportion to the recognition of rental income.

Academic Resource Center

Leases Page 50

– The collectability of the lease payments from RRI are reasonably assured, and no uncertainties exist regarding non-reimbursable costs to be incurred by MMT or BAC.

– MMT’s carrying value of the carriage ($8,000) is less than the fair value of the carriage ($10,000).– MMT is a manufacturer lessor and market rates are the same as its implicit rate.– MMT incurred $500 of initial costs for credit checks in executing the lease.– BAC’s carrying value of the roadster is equal to the fair value of the roadster ($20,000).– BAC incurred $1,000 of initial costs for legal fees and credit checks in executing the lease.– BAC is neither a manufacturer or dealer lessor.

Lessor accounting example

► Based on this information, prepare the journal entries for MMT for 2010, using US GAAP and IFRS. Round to the nearest dollar.

► Based on this information, prepare the journal entries for BAC for 2010, using US GAAP and IFRS. Round to the nearest dollar.

Example 4 – lessor accounting

The same terms of the lease arrangements between MMT and BAC with RRI apply to this example, while also considering the additional information below:

Academic Resource Center

Leases Page 51

Lessor accounting example

Example 4 solution:

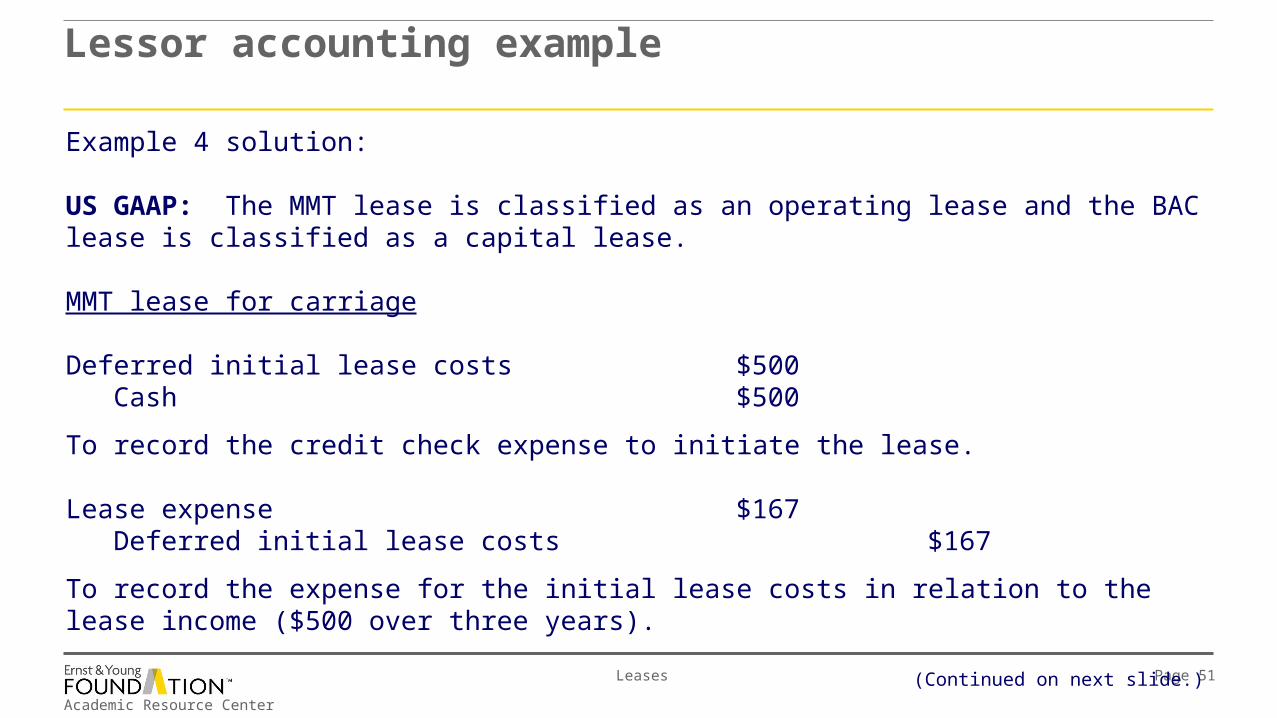

US GAAP: The MMT lease is classified as an operating lease and the BAC lease is classified as a capital lease.

MMT lease for carriage

Deferred initial lease costs $500Cash $500

To record the credit check expense to initiate the lease.

Lease expense $167Deferred initial lease costs $167

To record the expense for the initial lease costs in relation to the lease income ($500 over three years).

(Continued on next slide.)

Academic Resource Center

Leases Page 52

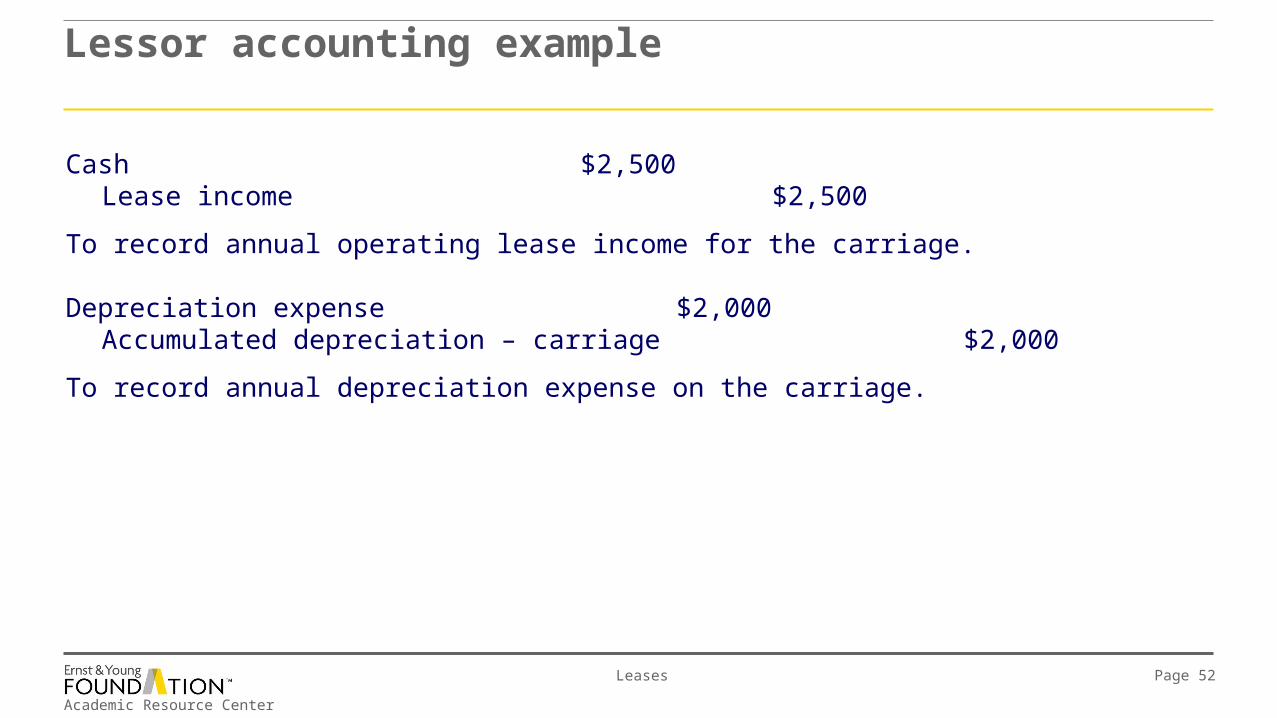

Lessor accounting example

Cash $2,500Lease income $2,500

To record annual operating lease income for the carriage.

Depreciation expense $2,000Accumulated depreciation – carriage $2,000

To record annual depreciation expense on the carriage.

Academic Resource Center

Leases Page 53

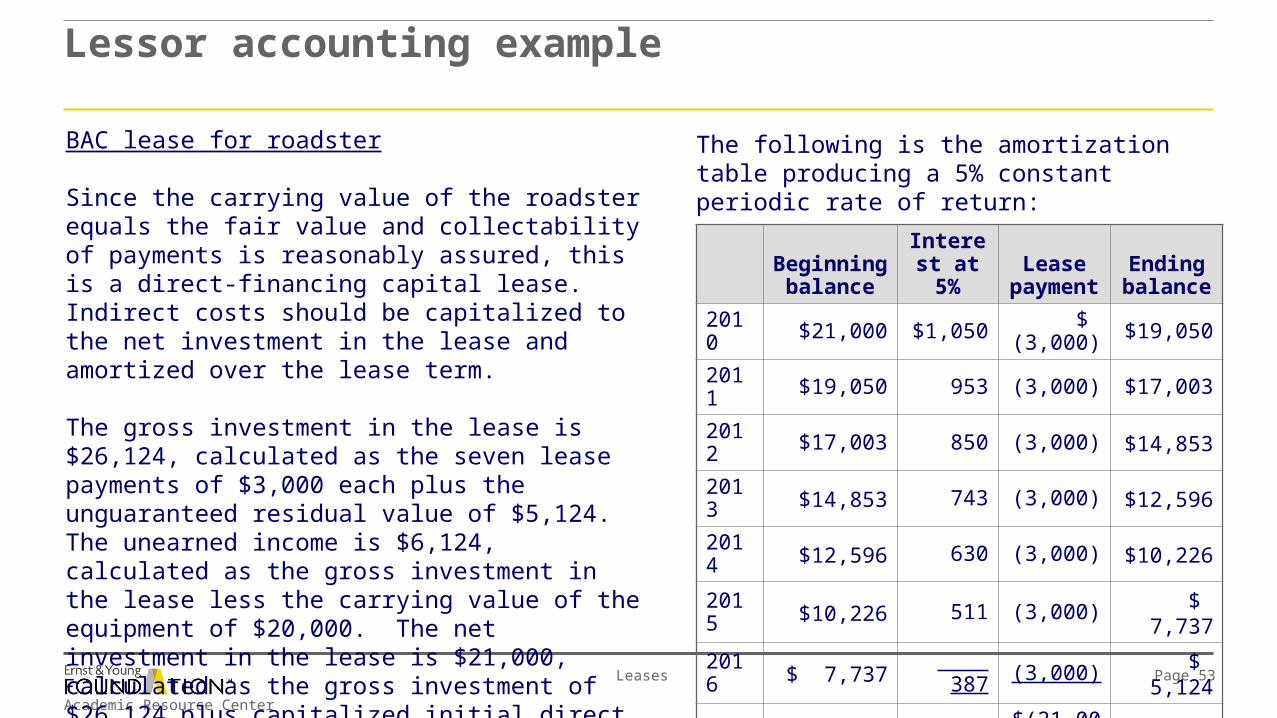

Lessor accounting example

BAC lease for roadster

Since the carrying value of the roadster equals the fair value and collectability of payments is reasonably assured, this is a direct-financing capital lease. Indirect costs should be capitalized to the net investment in the lease and amortized over the lease term.

The gross investment in the lease is $26,124, calculated as the seven lease payments of $3,000 each plus the unguaranteed residual value of $5,124. The unearned income is $6,124, calculated as the gross investment in the lease less the carrying value of the equipment of $20,000. The net investment in the lease is $21,000, calculated as the gross investment of $26,124 plus capitalized initial direct costs of $1,000 and less unearned income of $6,124.

The following is the amortization table producing a 5% constant periodic rate of return:

Beginning balance

Interest at 5%

Lease payment

Ending balance

2010 $21,000 $1,050 $ (3,000) $19,050

2011 $19,050 953 (3,000) $17,003

2012 $17,003 850 (3,000) $14,853

2013 $14,853 743 (3,000) $12,596

2014 $12,596 630 (3,000) $10,226

2015 $10,226 511 (3,000) $ 7,737

2016 $ 7,737 387 (3,000) $ 5,124

$5,124 $(21,000)

Academic Resource Center

Leases Page 54

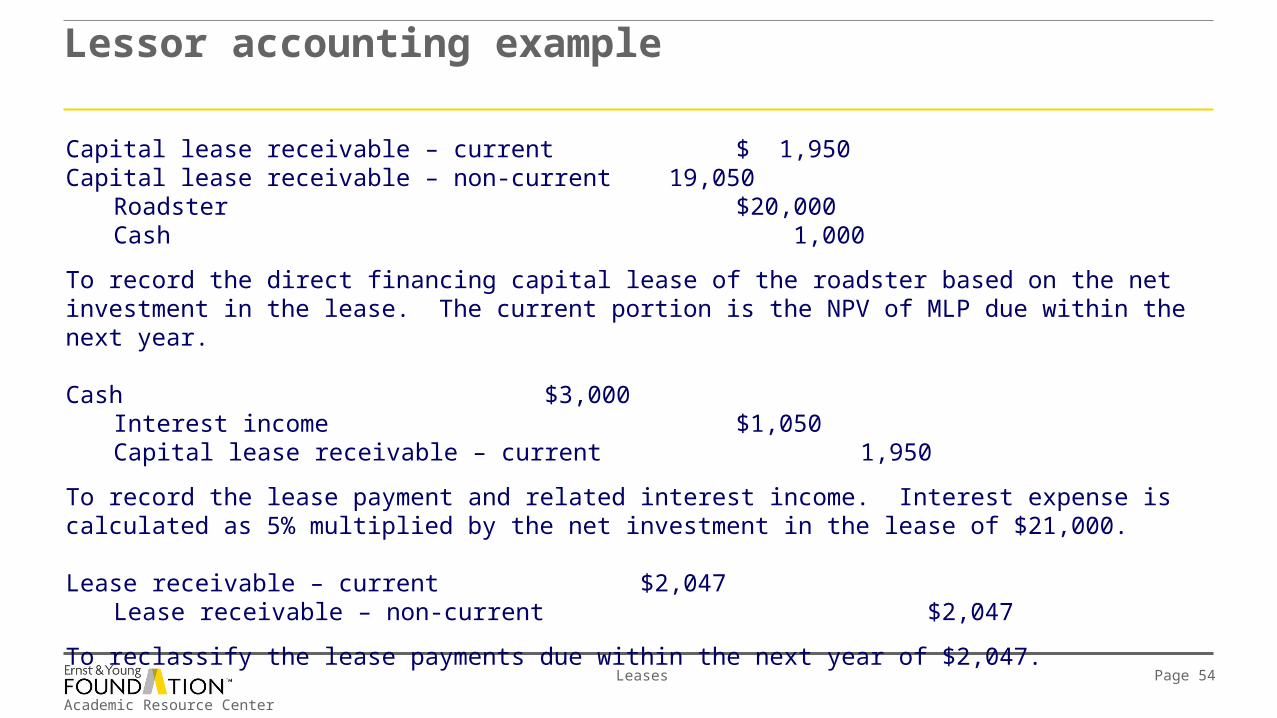

Lessor accounting example

Capital lease receivable – current $ 1,950Capital lease receivable – non-current 19,050

Roadster $20,000Cash 1,000

To record the direct financing capital lease of the roadster based on the net investment in the lease. The current portion is the NPV of MLP due within the next year.

Cash $3,000Interest income $1,050Capital lease receivable – current 1,950

To record the lease payment and related interest income. Interest expense is calculated as 5% multiplied by the net investment in the lease of $21,000.

Lease receivable – current $2,047Lease receivable – non-current $2,047

To reclassify the lease payments due within the next year of $2,047.

Academic Resource Center

Leases Page 55

Lessor accounting example

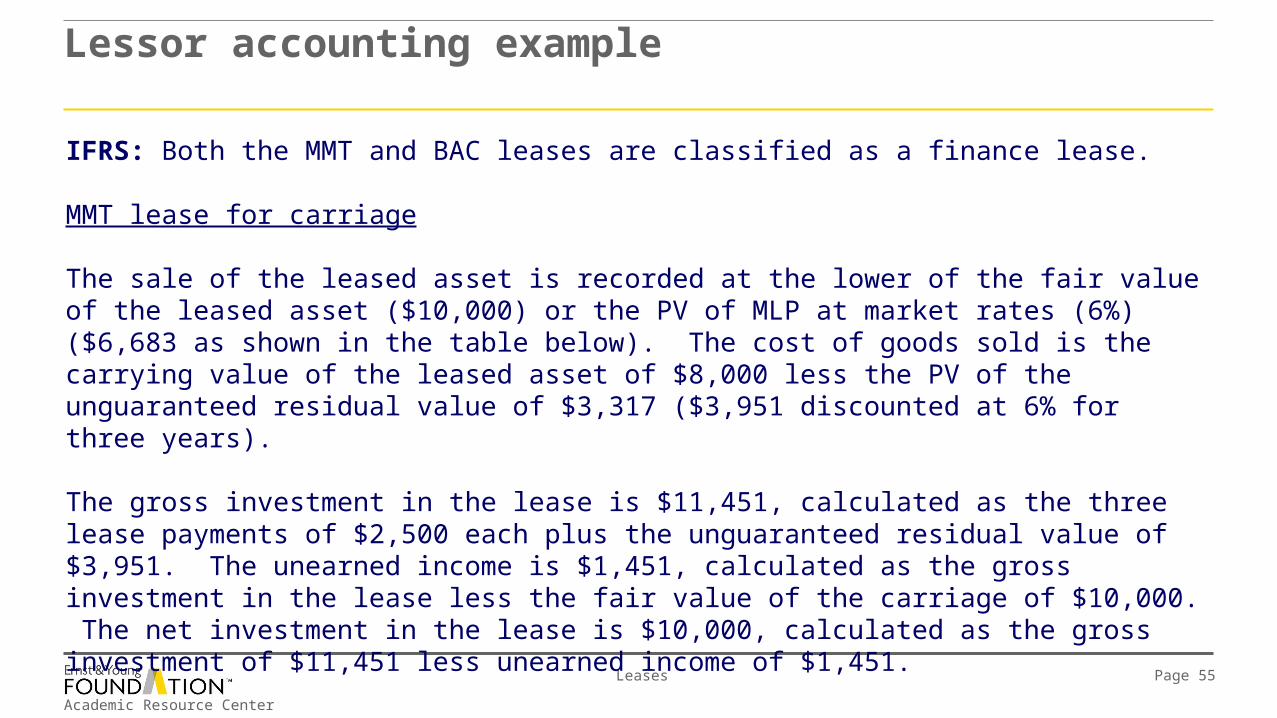

IFRS: Both the MMT and BAC leases are classified as a finance lease.

MMT lease for carriage

The sale of the leased asset is recorded at the lower of the fair value of the leased asset ($10,000) or the PV of MLP at market rates (6%) ($6,683 as shown in the table below). The cost of goods sold is the carrying value of the leased asset of $8,000 less the PV of the unguaranteed residual value of $3,317 ($3,951 discounted at 6% for three years).

The gross investment in the lease is $11,451, calculated as the three lease payments of $2,500 each plus the unguaranteed residual value of $3,951. The unearned income is $1,451, calculated as the gross investment in the lease less the fair value of the carriage of $10,000. The net investment in the lease is $10,000, calculated as the gross investment of $11,451 less unearned income of $1,451.

Academic Resource Center

Leases Page 56

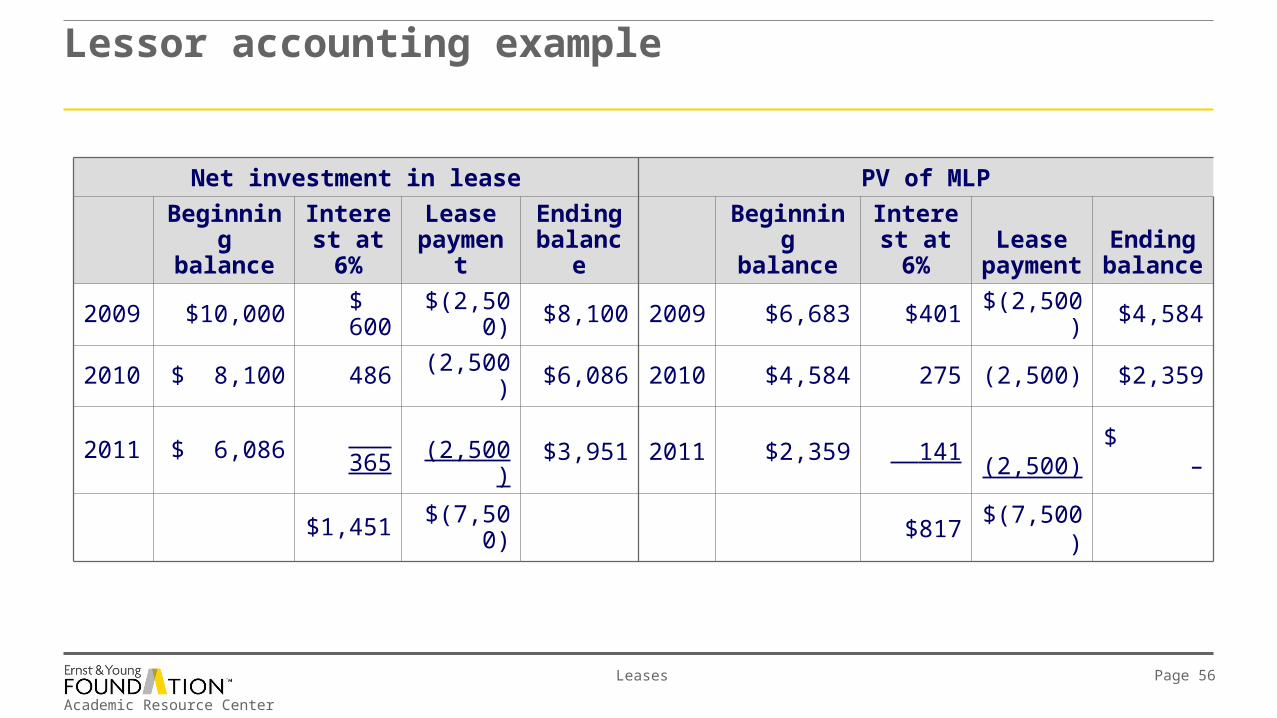

Lessor accounting example

Net investment in lease PV of MLP

Beginning balance

Interest at 6%

Lease payment

Ending balance

Beginning balance

Interest at 6%

Lease payment

Ending balance

2009 $10,000 $ 600 $(2,500) $8,100 2009 $6,683 $401 $(2,500) $4,584

2010 $ 8,100 486 (2,500) $6,086 2010 $4,584 275 (2,500) $2,359

2011 $ 6,086 365 (2,500) $3,951 2011 $2,359 141 (2,500) $ –

$1,451 $(7,500) $817 $(7,500)

Academic Resource Center

Leases Page 57

Lessor accounting example

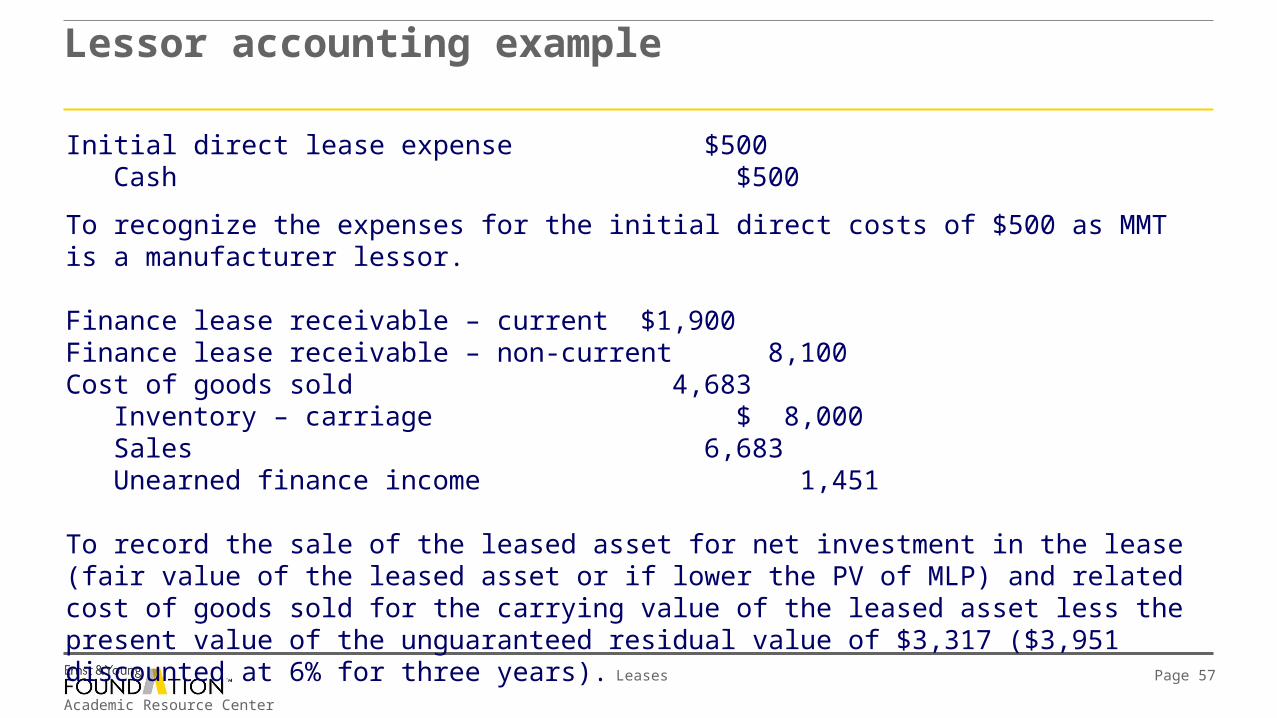

Initial direct lease expense $500Cash $500

To recognize the expenses for the initial direct costs of $500 as MMT is a manufacturer lessor.

Finance lease receivable – current $1,900Finance lease receivable – non-current 8,100Cost of goods sold 4,683

Inventory – carriage $ 8,000Sales 6,683Unearned finance income 1,451

To record the sale of the leased asset for net investment in the lease (fair value of the leased asset or if lower the PV of MLP) and related cost of goods sold for the carrying value of the leased asset less the present value of the unguaranteed residual value of $3,317 ($3,951 discounted at 6% for three years).

Academic Resource Center

Leases Page 58

Lessor accounting example

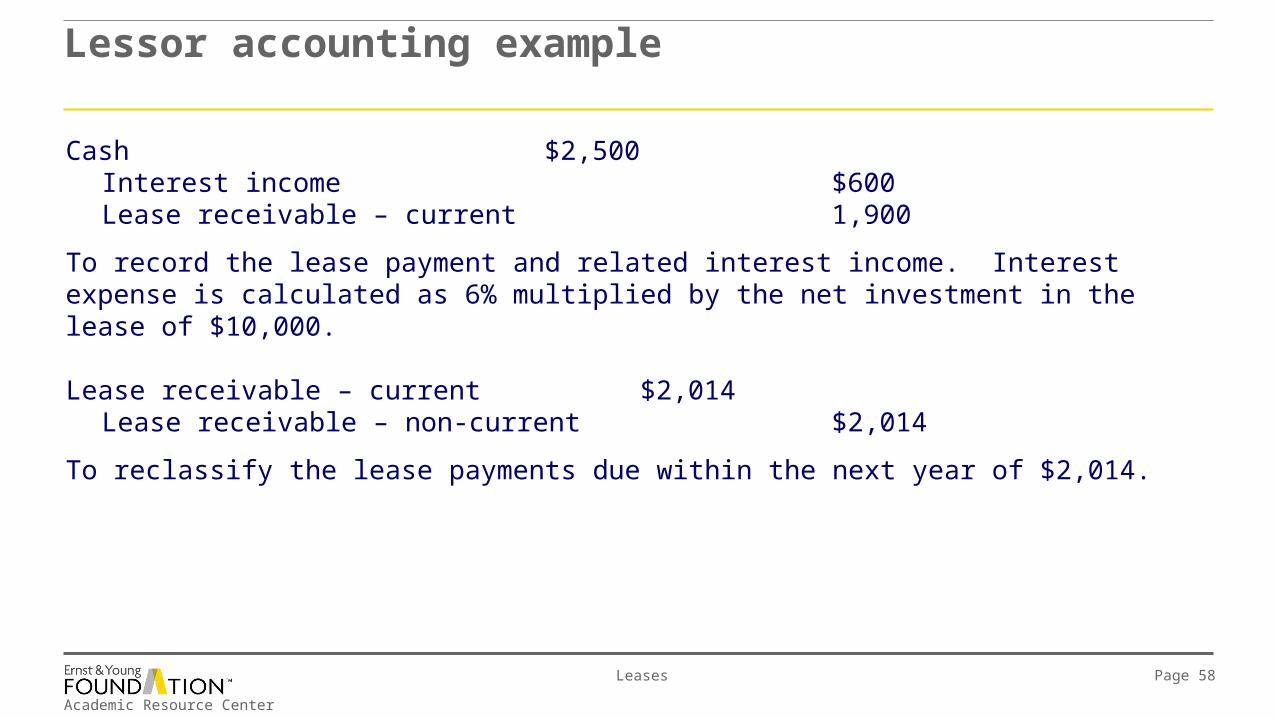

Cash $2,500Interest income $600Lease receivable – current 1,900

To record the lease payment and related interest income. Interest expense is calculated as 6% multiplied by the net investment in the lease of $10,000.

Lease receivable – current $2,014Lease receivable – non-current $2,014

To reclassify the lease payments due within the next year of $2,014.

Academic Resource Center

Leases Page 59

Lessor accounting example

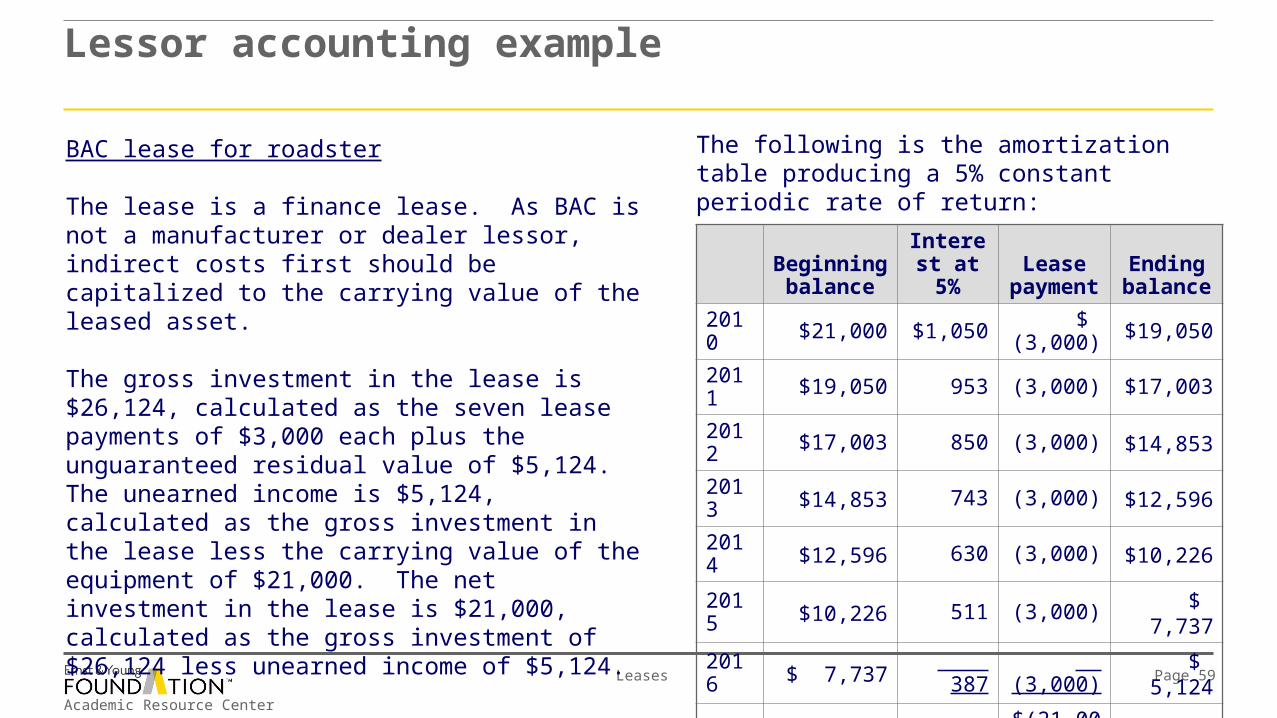

BAC lease for roadster

The lease is a finance lease. As BAC is not a manufacturer or dealer lessor, indirect costs first should be capitalized to the carrying value of the leased asset.

The gross investment in the lease is $26,124, calculated as the seven lease payments of $3,000 each plus the unguaranteed residual value of $5,124. The unearned income is $5,124, calculated as the gross investment in the lease less the carrying value of the equipment of $21,000. The net investment in the lease is $21,000, calculated as the gross investment of $26,124 less unearned income of $5,124.

The following is the amortization table producing a 5% constant periodic rate of return:

Beginning balance

Interest at 5%

Lease payment

Ending balance

2010 $21,000 $1,050 $ (3,000) $19,050

2011 $19,050 953 (3,000) $17,003

2012 $17,003 850 (3,000) $14,853

2013 $14,853 743 (3,000) $12,596

2014 $12,596 630 (3,000) $10,226

2015 $10,226 511 (3,000) $ 7,737

2016 $ 7,737 387 (3,000) $ 5,124

$5,124 $(21,000)

Academic Resource Center

Leases Page 60

Lessor accounting example

Roadster $1,000Cash $1,000

To capitalize the indirect costs to the carrying amount of the leased asset.

Finance lease receivable – current $ 1,950Finance lease receivable – non-current 19,050

Roadster $21,000

To record the direct financing capital lease of the roadster based on the net investment in the lease. The current portion is the NPV of MLP due within the next year.

Cash $3,000Interest income $1,050Finance lease receivable – current 1,950

To record the lease payment and related interest income. Interest expense is calculated as 5% multiplied by the net investment in the lease of $21,000.

(Continued on next slide.)

Academic Resource Center

Leases Page 61

Lessor accounting example

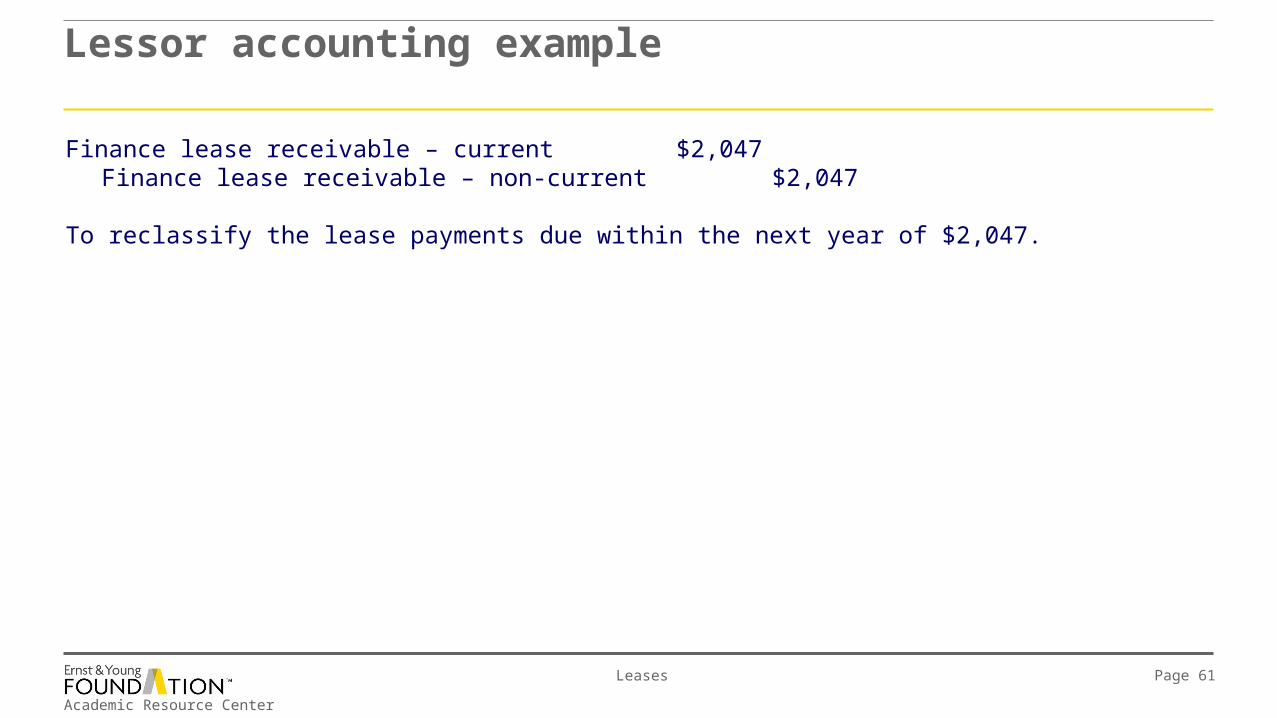

Finance lease receivable – current $2,047Finance lease receivable – non-current $2,047

To reclassify the lease payments due within the next year of $2,047.

Academic Resource Center

Leases Page 62

Sales leaseback arrangementsDefinition

An SLB arrangement is a transaction in which the owner of an asset sells the asset and then leases it back.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 63

Sale and leaseback arrangementsLease classification and capitalization criteria

The same classification and capitalization criteria must be met as defined previously. Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 64

Sale and leaseback arrangements Accounting treatment

For a capital/finance SLB, if the seller does not relinquish more than a minor part (>10%) of the use of the leased asset, the gain or loss is deferred and amortized ratably over the lease term.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 65

Sale and leaseback arrangementsAccounting treatment

IFRSUS GAAP

► The accounting treatment is the same for both a capital and operating SLB arrangement.

► US GAAP generally tries to capture the substance of the leaseback, and the accounting follows whether or not the seller relinquishes substantially all of the use of the asset, more than a minor part of the asset or less than a minor part of the asset.

► Details on next slide.

Academic Resource Center

Leases Page 66

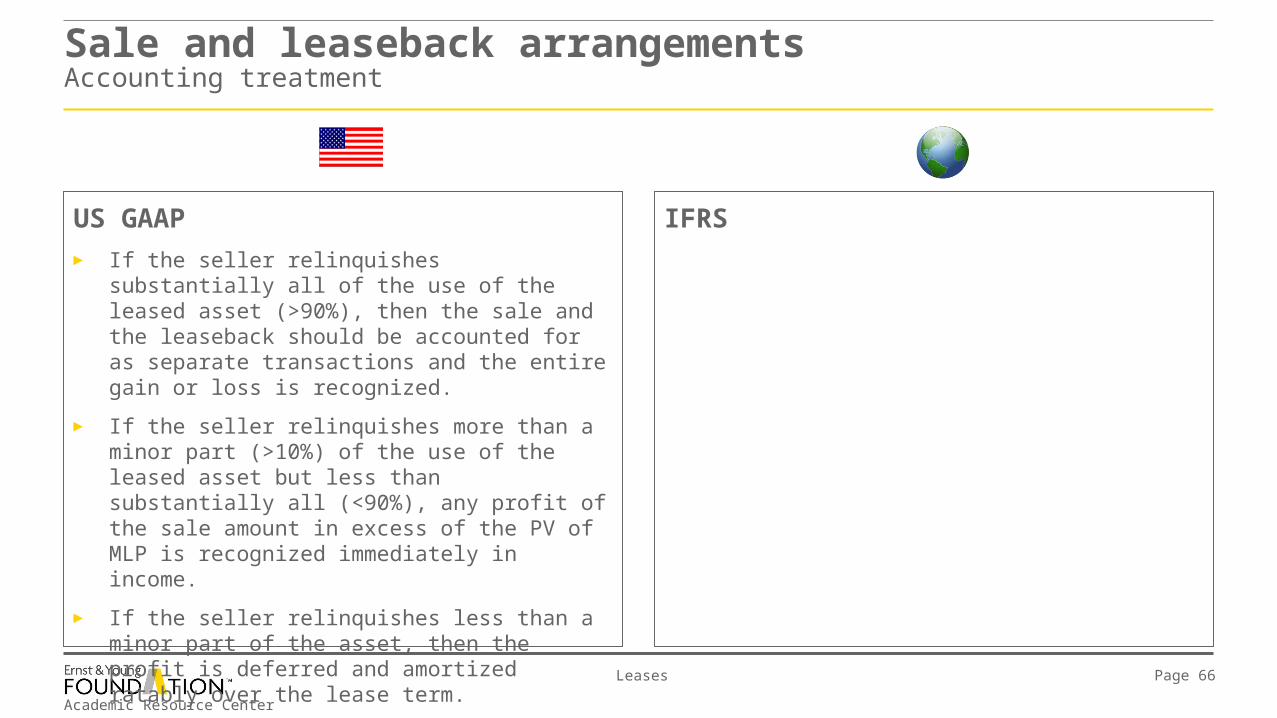

Sale and leaseback arrangements Accounting treatment

IFRSUS GAAP► If the seller relinquishes substantially all of the use of

the leased asset (>90%), then the sale and the leaseback should be accounted for as separate transactions and the entire gain or loss is recognized.

► If the seller relinquishes more than a minor part (>10%) of the use of the leased asset but less than substantially all (<90%), any profit of the sale amount in excess of the PV of MLP is recognized immediately in income.

► If the seller relinquishes less than a minor part of the asset, then the profit is deferred and amortized ratably over the lease term.

► If the transaction results in a loss, it is recognized immediately.

Academic Resource Center

Leases Page 67

Sale and leaseback arrangements Accounting treatment

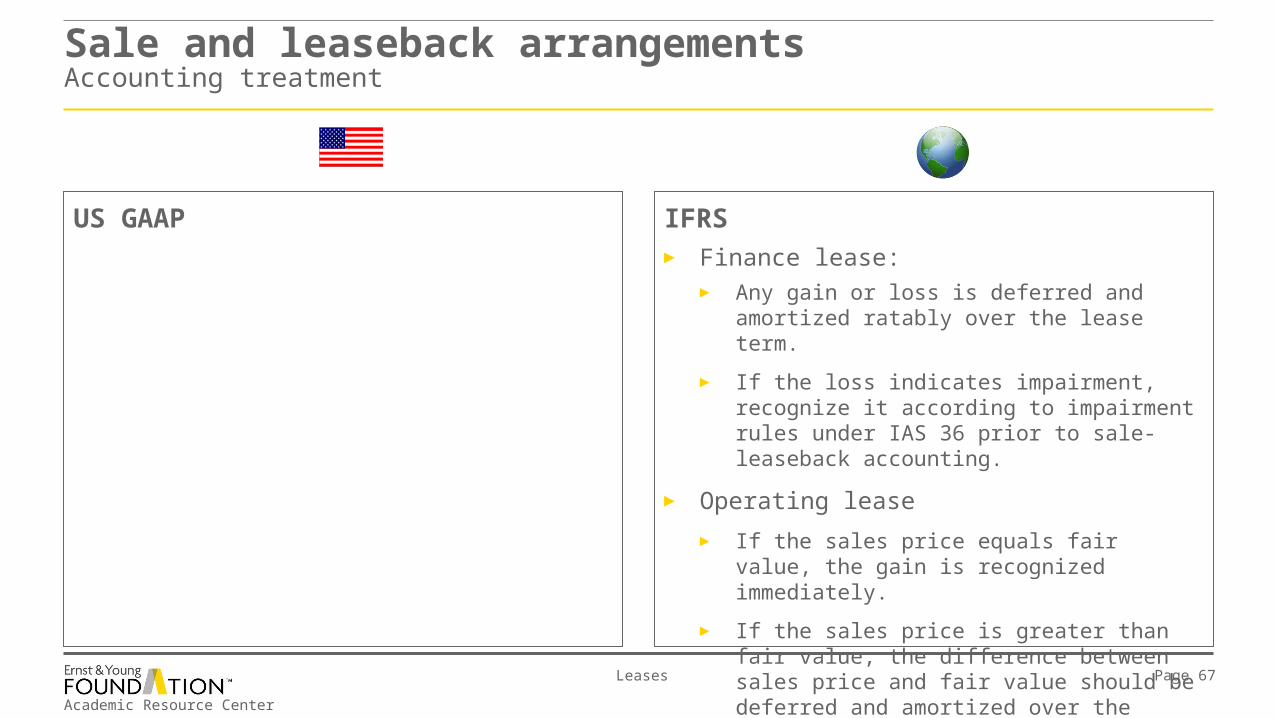

IFRS► Finance lease:

► Any gain or loss is deferred and amortized ratably over the lease term.

► If the loss indicates impairment, recognize it according to impairment rules under IAS 36 prior to sale-leaseback accounting.

► Operating lease

► If the sales price equals fair value, the gain is recognized immediately.

► If the sales price is greater than fair value, the difference between sales price and fair value should be deferred and amortized over the period for which the asset is expected to be used.

US GAAP

Academic Resource Center

Leases Page 68

Sale and leaseback arrangementsAccounting treatment

IFRS

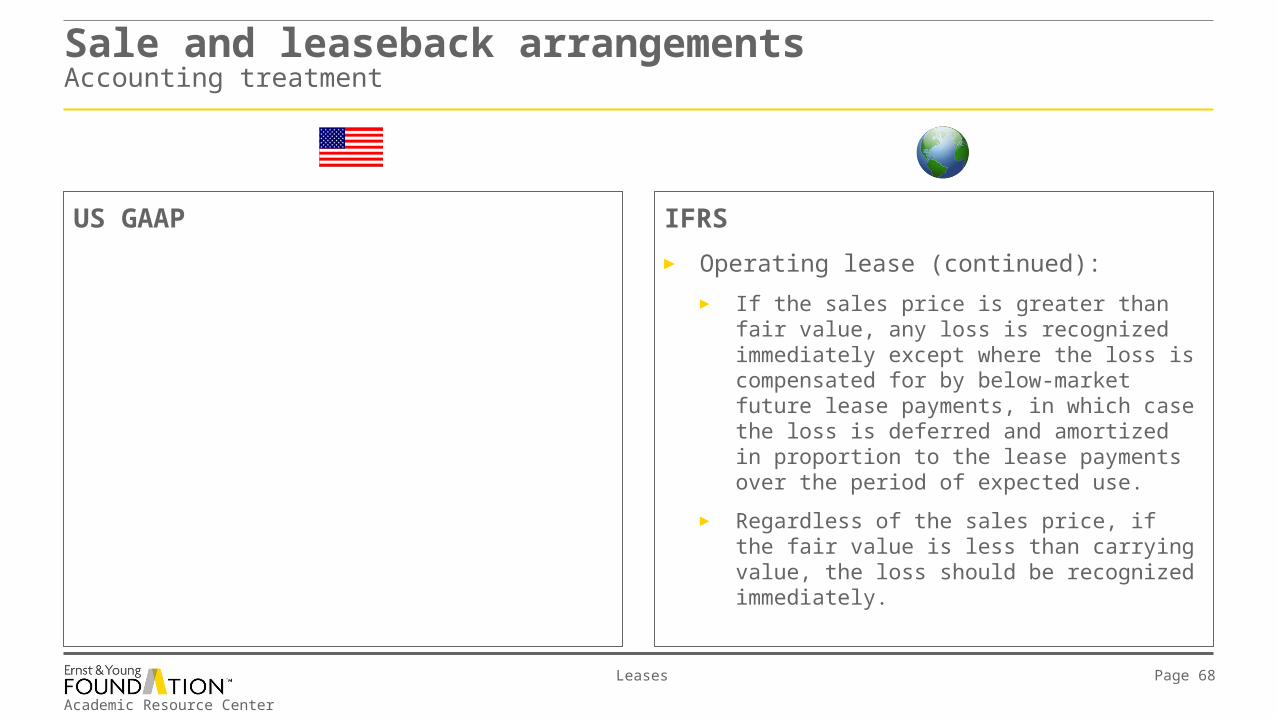

► Operating lease (continued):

► If the sales price is greater than fair value, any loss is recognized immediately except where the loss is compensated for by below-market future lease payments, in which case the loss is deferred and amortized in proportion to the lease payments over the period of expected use.

► Regardless of the sales price, if the fair value is less than carrying value, the loss should be recognized immediately.

US GAAP

Academic Resource Center

Leases Page 69

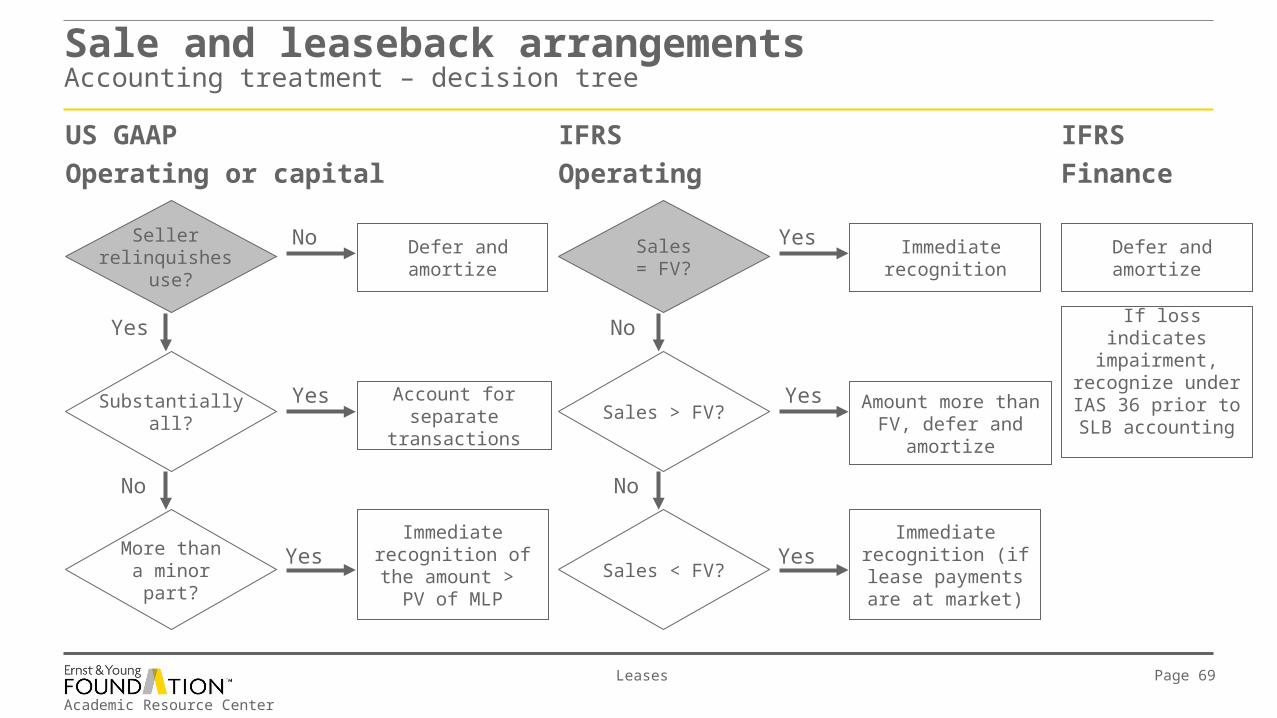

US GAAP

Operating or capital

Immediate recognition of the amount >

PV of MLP

Account for separate transactions

Defer and amortize

Substantiallyall?

No

Yes

No

Yes

Yes

Seller relinquishes

use?

More thana minorpart?

IFRS

Operating

Immediate recognition (if lease payments are

at market)

Amount more than FV, defer and amortize

Immediate recognition

Sales > FV?

Yes

Yes

No

Yes

No

Sales= FV?

Sales < FV?

Defer and amortize

IFRS

Finance

If loss indicates impairment, recognize under IAS 36 prior to

SLB accounting

Sale and leaseback arrangements Accounting treatment – decision tree

Academic Resource Center

Leases Page 70

Example 5 – sale and leaseback

Part I:

RRI sells a sports car to the Hot Rod Company (HRC) and then leases it back under an operating lease for a period of three years. The leaseback is estimated to be approximately 9% of the fair value of the sports car. The sales price of the sports car is $100,000 and the net book value is $80,000. The lease payments are reasonable in view of the current market conditions, and the sales price approximates the fair value of the sports car.

Sale and leaseback example

► Determine how RRI would account for the leaseback using US GAAP and IFRS.

Academic Resource Center

Leases Page 71

Example 5 solution:

Part I :

US GAAP:

RRI is retaining only a minor portion of the remaining use of the sports car (9% of the fair value); therefore, RRI would record the sale and lease as separate transactions. RRI would record the sale and recognize the gain of $20,000 as the difference in the sales price of $100,000 and the carrying value of $80,000.

IFRS:

The accounting treatment would be the same as US GAAP since the sales price approximates fair value.

Sale and leaseback example

Academic Resource Center

Leases Page 72

Example 5 – sale and leaseback

Part II:

RRI sells a sports car to HRC and then leases it back under an operating lease for a period of three years. The sales price of the sports car is $100,000, and the net book value is $50,000. The lease payments are reasonable in view of the current market conditions. The PV of MLP is $30,000. The fair value of the sports car is $90,000.

Sale and leaseback example

► Determine how RRI would account for the leaseback, using US GAAP and IFRS.

Academic Resource Center

Leases Page 73

Example 5 solution:

Part II :

US GAAP:

RRI is retaining more than a minor portion of the remaining use of the sports car but less than substantially all. This is determined by comparing the PV of the MLP of $30,000 to the fair value of the asset of $90,000 or 30%. RRI would calculate the profit as the sales price of $100,000 less the carrying value of $50,000. A gain of $20,000 would be recognized immediately since this is the amount of the profit above the PV of MLP. The PV of MLP of $30,000 would be deferred and amortized ratably over the term of the lease.

IFRS:

Since the sales price of $100,000 is above the fair value of the sports car of $90,000, the excess of $10,000 would be deferred and amortized ratably over the term of the lease period (the period for which the asset is expected to be used). The remaining gain of $40,000 would be recognized immediately.

Sale and leaseback example

Academic Resource Center

Leases Page 74

Example 5 – sale and leaseback

Part III:

RRI sells a sports car to HRC and then leases it back under a capital/finance lease for a period of three years. The sales price of the sports car is $100,000, which is determined to be fair value. The net book value is $50,000. The lease payments are reasonable in view of current market conditions. The PV of MLP is $95,000.

Sale and leaseback example

► Determine how RRI would account for the leaseback, using US GAAP and IFRS.

Academic Resource Center

Leases Page 75

Example 5, part III solution (continued):

US GAAP:

RRI is retaining a substantial portion of the remaining use of the sports car. This is determined by comparing the PV of MLP of $95,000 to the fair value of the asset of $100,000 or 95%. RRI would defer the gain of $50,000, calculated as the sales price of $100,000 less the carrying value of $50,000 and amortize the amount over the term of the lease.

IFRS:

The accounting treatment would be the same as US GAAP.

Sale and leaseback example

Academic Resource Center

Leases Page 76

Other lease considerations

IFRSUS GAAP

Similar

Lease incentives are deferred and amortized on a straight-line basis, unless a more systematic basis is more representative of the time pattern of the lessee’s benefit from the use of the leased asset:

► Leasehold improvements are amortized over the shorter of the lease term or their estimated useful life when there is no reasonable uncertainty that ownership will transfer by the end of the lease term.

► Rent holidays or rent-free periods are amortized over the lease term.

Academic Resource Center

Leases Page 77

Example 6 – leasehold improvements

The Retail Company (TRC) enters into an operating lease with a lessor, Main Street Mall Inc. (MSM), for a five-year term at a monthly rental of $110. In order to induce TRC into the lease, MSM agrees to provide funding of up to $600 for leasehold improvements. TRC spends $720 on leasehold improvements having an estimated useful life of six years.

Leasehold improvements example

► What journal entries should TRC prepare during its first month of the lease, using US GAAP and IFRS?

Academic Resource Center

Leases Page 78

Example 6 solution:

The entries are the same for both US GAAP and IFRS:

Cash $600

Lease incentive obligation $600

To record the receipt of the lease incentive.

Leasehold improvements $720

Cash $720

To record the expenditure of the funds (including the $600 of funds supplied by MSM) on leasehold improvements.(Continued on next slide.)

Leasehold improvements example

Academic Resource Center

Leases Page 79

Example 6 solution (continued):

Operating lease expense $100

Lease incentive obligation 10

Cash $110

To record monthly lease payments. The lease expense is reduced by the amortization of the lease incentive ($600) over the term of the lease of 60 months.

Amortization expense $12

Accumulated leasehold improvements $12

To record monthly amortization of leasehold improvements ($720/60) over the shorter of the lease term (60 months) or estimated useful life (72 months).

Leasehold improvements example

Academic Resource Center

Leases Page 80

Example 7 – rent-free periods

Catherine’s Internet Café (CIC) enters into a new operating lease for a 10-year term at a monthly rental of $500. To induce CIC into the lease, the lessor agreed to a free-rent period for the first year.

Rent-free periods example

► How would lease expense for CIC differ, using US GAAP compared to IFRS in years one and two?

Academic Resource Center

Leases Page 81

Example 7 solution:

The annual lease expense is the same under US GAAP and IFRS. Total consideration for rent over the lease term is $54,000 ($500 for 108 months). This consideration must be recognized on a straight-line basis (unless another systematic basis is more representative of the time pattern of the lessee’s benefit from using the leased asset) over the entire lease period of 10 years, resulting in annual lease expense of $5,400.

Lease expense $5,400

Deferred rent payable $5,400

To record lease expense in year one.

Rent-free periods example

Academic Resource Center

Leases Page 82

Disclosures

Generally, the disclosures vary based on the type of lease (capital/finance or operating) and whether the disclosure is for a lessee or lessor.

Similar

IFRSUS GAAP

Academic Resource Center

Leases Page 83

Disclosures

IFRS

► Future rent is disclosed for the first year, years two through five inclusive and the aggregate amount thereafter.

US GAAP

► Future rent disclosures are by individual year for the first five years and the aggregate amount thereafter.

Academic Resource Center

Leases Page 84

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 144,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global and of Ernst & Young Americas operating in the US.

© 2010 Ernst & Young Foundation (US). All Rights Reserved.SCORE No. MM4050C.