GST Valuation

Issues

Virtual Certificate Course on GST

By IDTC-ICAI

CA Vasant K. Bhatt

1

Consideration versus Sole Consideration

Supply Includes

Sec 7 (1)(a) For consideration(for business)

sale, transfer, barter, exchange, licence, rental, lease or disposal etc

Sec 7 (1)(b) For consideration(for business or not)

Import of service

Schedule I Without consideration

•Permanent transfer/disposal of business assets where ITC availed

•Supply of goods or services between related persons, or distinct persons , when made in the course or furtherance of Business

•Supply between agent and principal•Import of service from a related person .

CA Vasant K. Bhat2

Consideration versus Sole Consideration Contd..

Supply Includes Schedule II Whether or not for consideration

• Transfer or disposal of business asset• Business assets put to private or other than

business purpose

Value of Taxable Supply:

Section 15 : Value of supply shall be the transaction value, where;(a) Supplier and recipient are not related, and (b) price is the sole consideration

Consideration is relevant to determine ‘supply’

Sole consideration is relevant to determine ‘value of taxable supply’

CA Vasant K. Bhat3

Consideration

Sec 2(31) of CGST Act: Consideration includes;

(a) any payment made or to be made, whether in money or otherwise…..whether by

the recipient or by any other person (excluding govt subsidies)

(b) the monetary value of any act or forbearance, … whether by the recipient or by any

other person (excluding govt subsidies)

CA Vasant K. Bhat4

Sole Consideration

CCE Mumbai v. Fiat India Pvt Ltd. [2012(283) ELT 161 (SC)];

“When word ‘consideration’ is qualified by word ‘sole’, it makes it stronger so as to

make it sufficient and valuable having regard to facts, circumstances and necessities of

case”

No additional benefit to the supplier other than the price, directly or indirectly

No flow back of additional consideration in cash or kind

Price is the only thing ultimately the supplier gets

CA Vasant K. Bhat5

Absence of Consideration Vs. presence of Non-Monetary Consideration

Absence of Consideration:

Supply - only in case of

Permanent transfer/disposal of business assets where ITC availed

Supply of goods or services between related persons, or distinct persons , when made in the course or furtherance of Business

Supply between agent and principal

Import of service from a related person

Transfer or disposal of business asset

Business assets put to private or other than business purpose

CA Vasant K. Bhat6

Presence of Non-Monetary Consideration:

Consideration not wholly in money transaction value not applicable

Valuation shall be based on provisions of Valuation Rules.

Rule 1:

• Open market value

• Consideration in money + monetary value of non-monetary consideration, if suchamount is known

• Value of supply of goods or services or both of like kind and quality

• Consideration in money + monetary value of non-monetary consideration based on valuation rules

CA Vasant K. Bhat7

Selling below cost - Is there any Non-Monetary Consideration?

Transaction value cannot be rejected just because price was less than the cost of

manufacture in the absence of allegation to the effect that price is not the sole

consideration, transaction was not at arm’s length etc.

[Collector v. Guru Nanak Refrigeration Corpn. - 1997 (96) E.L.T. A230 (S.C)]

CA Vasant K. Bhat8

Selling below cost - Is there any Non-Monetary Consideration? Contd..

Selling below cost for 5 years thereby continuously incurring losses, it was not

normal price.

No prudent business person would continuously suffer huge loss only to penetrate

market

It was extra commercial consideration in fixing of price, and artificially depressed it

It is immaterial that no allegation was made that buyer was related person or there

was flowback directly from buyer to seller - Allegation that price was not the sole

consideration was sufficient

[CCE Mumbai v. Fiat India Pvt Ltd. [2012(283) ELT 161 (SC)]

CA Vasant K. Bhat9

Selling below cost - Is there any Non-Monetary Consideration? Contd..

Manufacturer selling goods at price less than cost of manufacturing - It may be

considered normal price when assessee wants to switch over their business for any

other manufacturing activity, or

where goods cannot be sold within a reasonable time

[CCE Mumbai v. Fiat India Pvt Ltd. [2012(283) ELT 161 (SC)]

CA Vasant K. Bhat10

Difference between Assessable Value in Excise & Transaction Value in GST

Assessable Value in Excise Transaction Value in GST

Value shall be the transaction value, where;- Goods are sold by the assesse for

delivery at the time and place of removal

- Assessee and Buyer are not related- Price is the sole consideration

Value shall be the transaction value, where;- Supplier and Recipient are not related- Price is the sole consideration

Excludes:Excise duty, Sales Tax and other taxes

Includes:-Any taxes, duties, cesses, fees and charges levied under any law other than CGST Act, SGST Act UTGST Act and GST (Compensation to states) Act.

CA Vasant K. Bhat11

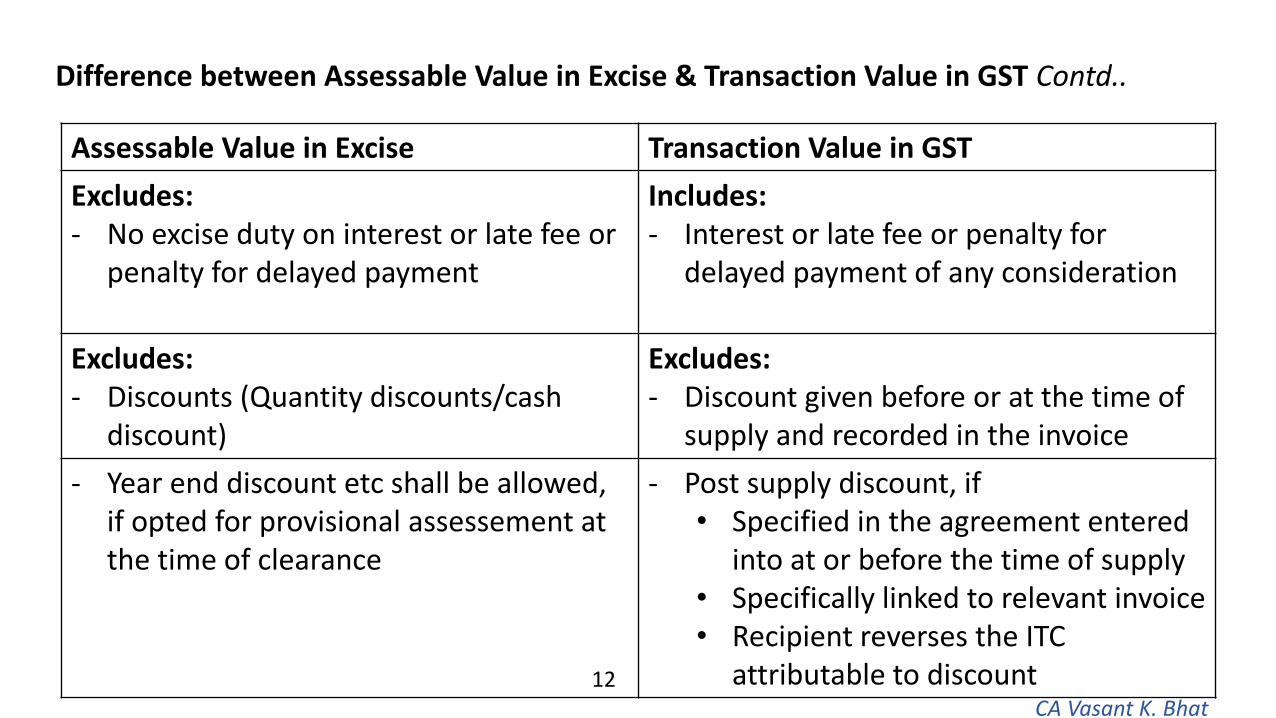

Difference between Assessable Value in Excise & Transaction Value in GST Contd..

Assessable Value in Excise Transaction Value in GST

Excludes: - No excise duty on interest or late fee or

penalty for delayed payment

Includes:- Interest or late fee or penalty for

delayed payment of any consideration

Excludes:- Discounts (Quantity discounts/cash

discount)

Excludes:- Discount given before or at the time of

supply and recorded in the invoice

- Year end discount etc shall be allowed, if opted for provisional assessement at the time of clearance

- Post supply discount, if • Specified in the agreement entered

into at or before the time of supply• Specifically linked to relevant invoice• Recipient reverses the ITC

attributable to discountCA Vasant K. Bhat

12

Difference between Assessable Value in Excise & Transaction Value in GST Contd..

Assessable Value in Excise Transaction Value in GST

Provision for price-cum-duty is in the Act Provision for value inclusive of tax is provided in the Valuation Rules. [Rule 9]

Note: 1Note: 2

CA Vasant K. Bhat13

Difference between Assessable Value in Excise & Transaction Value in GST Contd..

Note 1:

Sec 15. (1) The value of a supply of goods or services or both shall be the transaction

value, which is the price actually paid or payable for the said supply of goods or

services or both where the supplier and the recipient of the supply are not related

and the price is the sole consideration for the supply.

Note 2:

Sec 15.(4) Where the value of the supply of goods or services or both cannot be

determined under sub-section (1), the same shall be determined in such manner as

may be prescribed.

Cum-Tax computation is not available if transaction value is accepted???CA Vasant K. Bhat

14

Valuation for Customs versus Valuation for IGST

Valuation for Customs Valuation for IGST

Assessable value is transaction value as per Sec 14 of the Customs Act

Valuation for IGST is Assessable Value for customs duty + Basic Customs Duty

[Sec 15(2) of CGST Act-other taxes to be included]

Education cess will be on Assessable Value + Basic Customs Duty

GST Compensation Cess will be on Assessable Value for customs duty + Basic Customs Duty

CA Vasant K. Bhat15

Stock Transfer Vs. Sale on Approval

Stock Transfer Sale on Approval

Supply to distinct person (located outside state) liable for GST

Goods can be sent for approval for sale or return

Invoice is to be issued at the time or before supply

Invoice need to be issued before or at the time of supply or 6 months from the date of removal, whichever is earlier

CA Vasant K. Bhat16

![[ Webinar GST Valuation Rules][ Webinar –GST Valuation Rules] [CMA Ashish Bhavsar] [Cost Accountants] [Ahmedabad] Value of taxable Supply Section -15 of CGST Act • Section 15 (1)](https://static.cupdf.com/doc/110x72/5ec71e5bb4972817942093c6/-webinar-gst-valuation-rules-webinar-agst-valuation-rules-cma-ashish-bhavsar.jpg)