International Monetary FundJanuary 28, 2021

THE 9th NCAER

C. D. DESHMUKH LECTURE 2021

Global Economic Outlook: Averting a Great Divergence

Gita Gopinath

Chief Economist

0

2

4

6

8

10

12

Mar-

20

Ap

r-20

May-2

0

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec-

20

Jan

-21

0

100

200

300

400

500

600

700

Mar-

20

Ap

r-20

May-2

0

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec-

20

Jan

-21

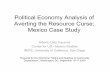

Health: Race between Virus and Vaccines

New deaths 1/(per million population)

New cases 1/(per million population)

Sources Haver Analytics; OxCGRT; Duke Global Health Innovation Center; and IMF staff calculations.

1/ Lines denote median of 7-day moving averages. Shaded areas are interquartile ranges.

2/ Includes only vaccines that have been approved.

Vaccine doses, approved and

procured 2/(millions of doses, confirmed agreement only) AEs EMs LICs India AEs EMs LICs India

1/24 1/240

500

1000

1500

2000

2500

AstraZeneca Pfizer Gamaleya

research

institute

Moderna Sinovac

1

86

88

90

92

94

96

98

100

102

-2 -1 0 1 2 3

Devia

tio

n f

rom

peak

Quarters around real GDP peak

Great Lockdown, AEs Great Lockdown, EMs Great Financial Crisis Other recessions

Economic activity: Q3 surprised strongly on upside; Q4 backsliding

Real GDP 1/ (index; pre-recession peak = 100)

Sources: IMF, World Economic Outlook; IMF, Global Data Source; Haver Analytics; and IMF staff calculations.

1/ Lines denote averages.2

-35

-30

-25

-20

-15

-10

-5

0

May-2

0

May-2

0

Jun

-20

Jul-

20

Jul-

20

Au

g-2

0

Sep

-20

Sep

-20

Oct

-20

No

v-2

0

No

v-2

0

Dec-

20

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

Sources: Haver Analytics; OxCGRT; Google, COVID-19 Community Mobility Data; Duke Global Health Innovation Center; Global Advisor; and IMF staff calculations.

1/ Lines denote median of 7-day moving averages. Shaded areas are interquartile ranges. A full lockdown includes all “containment and closure” measures in the OxCGRT. The

regression sample includes 128 countries.

Targeted lockdowns and economies adapting to social distancing

Sensitivity of mobility to cases

and lockdowns 1/ (coefficient)

Impact of full lockdown

Impact of doubling of daily cases (rhs)

PMI services (index; >50 = expansion)

AUS

BRA

CHN

DEU

ESPFRA

GBR

IND

IRL

ITA

JPN

KAZRUS

USA

AUS

BRA

CHN

DEUESP

FRAGBRIND IRL

ITA

JPN

RUS

USA

0

10

20

30

40

50

60

0 5 10 15 20 25 30 35 40 45 50 55

PM

I se

rvic

es

Cases per million population

Apr. 20 Dec. 20

12/31

3

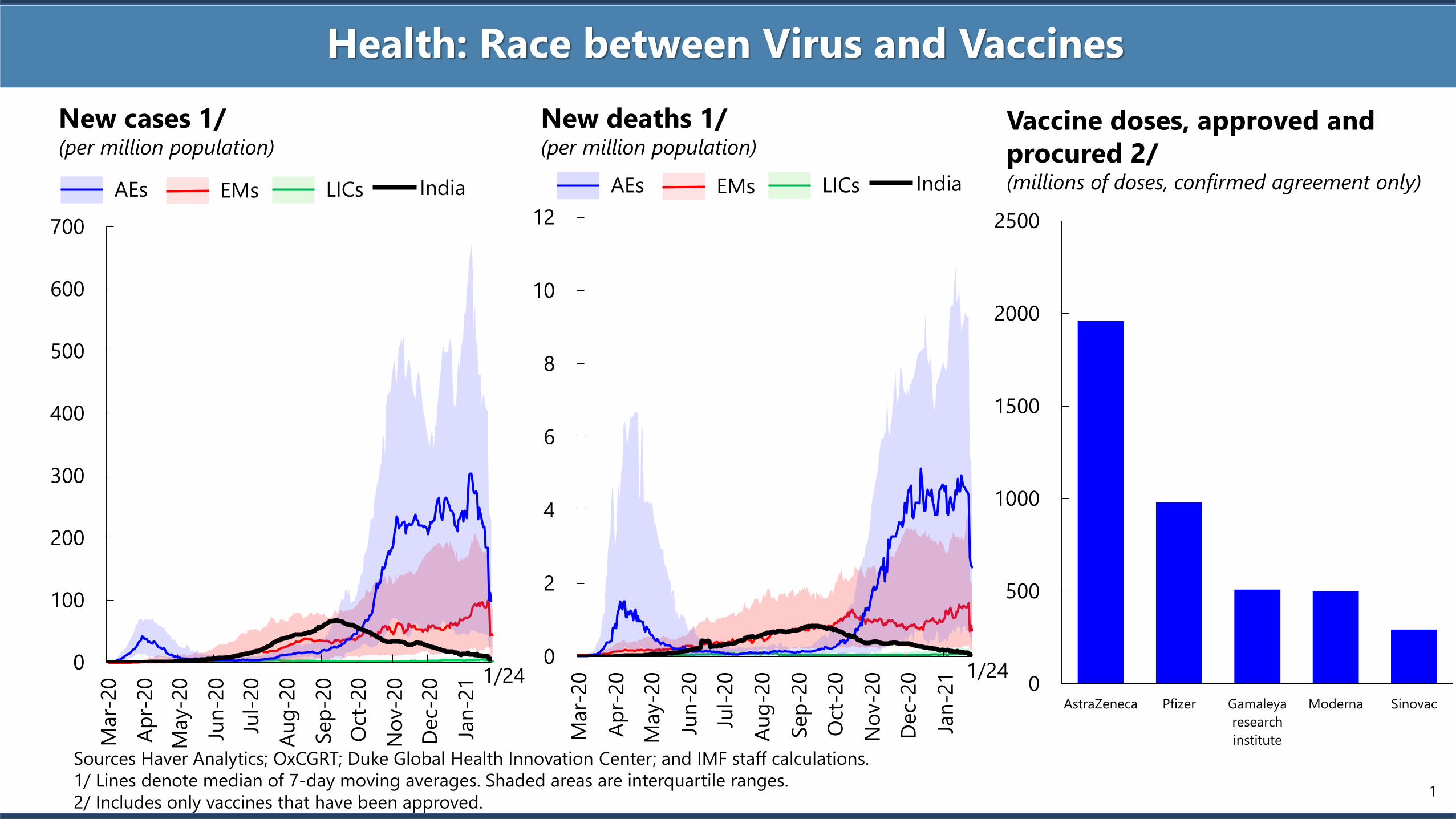

Lifelines to households and firms supported the rebound

Income support(share of countries in each income group with

higher than 50% replacement income support;

percent)

Sources: OxCGRT; CEIC; Haver Analytics; and IMF staff calculations.

1/ Lines denote medians. Shaded area denotes interquartile ranges.

Household saving 1/(percent of household disposable income)

0

10

20

30

40

50

60

70

80

20Q1 20Q2 20Q3 20Q4

AEs EMs LICs

0

5

10

15

20

25

30

18Q1 18Q3 19Q1 19Q3 20Q1 20Q3

Bankruptcies (index; last pre-recession quarter=100)

70

80

90

100

110

120

130

140

-8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

Recession quarter

The Great Lockdown

Global financial crisis

Other recessions

4

25

30

35

40

45

40

50

60

70

80

90

100

Jan-19 Jul-19 Jan-20 Jul-20

Share of countries with inflation below target

Share of countries with one-year ahead inflation

exp. below target

Share of countries with policy rate near ZLB, rhs

0

200

400

600

800

1000

1200

Jan-20 May-20 Sep-20 Jan-21

EM investment grade

EM non-investment grade

LIC/Frontier non-inv grade

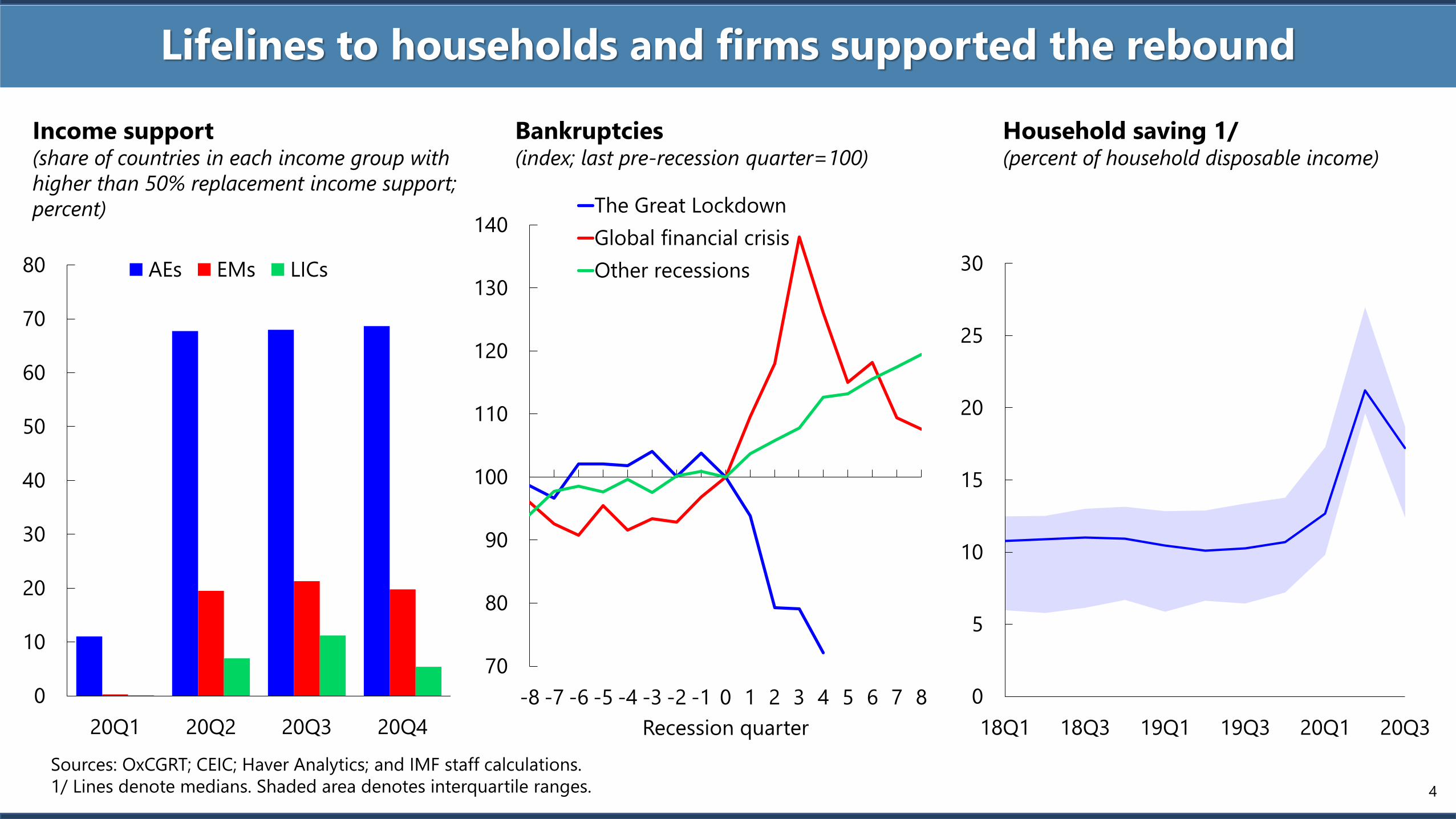

Merchandise trade recovers and financial conditions buoyant

World: merchandise imports 1/(index; Jul 2008=100 for GFC; Dec

2019=100 for GL)

Sources: CPB; Bloomberg; IMF, World Economic Outlook; IMF, Global Data Source; Haver Analytics; Consensus Forecast; and IMF staff calculations.

1/ Lighter lines indicate nowcasts.

2/ ZLB threshold at 0.5 percent.

EMBIG spread(median; basis points)

1/7

Inflation and policy space 2/(percent)

60

65

70

75

80

85

90

95

100

105

0 4 8 12 16 20 24

Great Lockdown: Value

Great Lockdown: Volume

Global Financial Crisis: Value

Global Financial Crisis: Volume

Nov-20

5

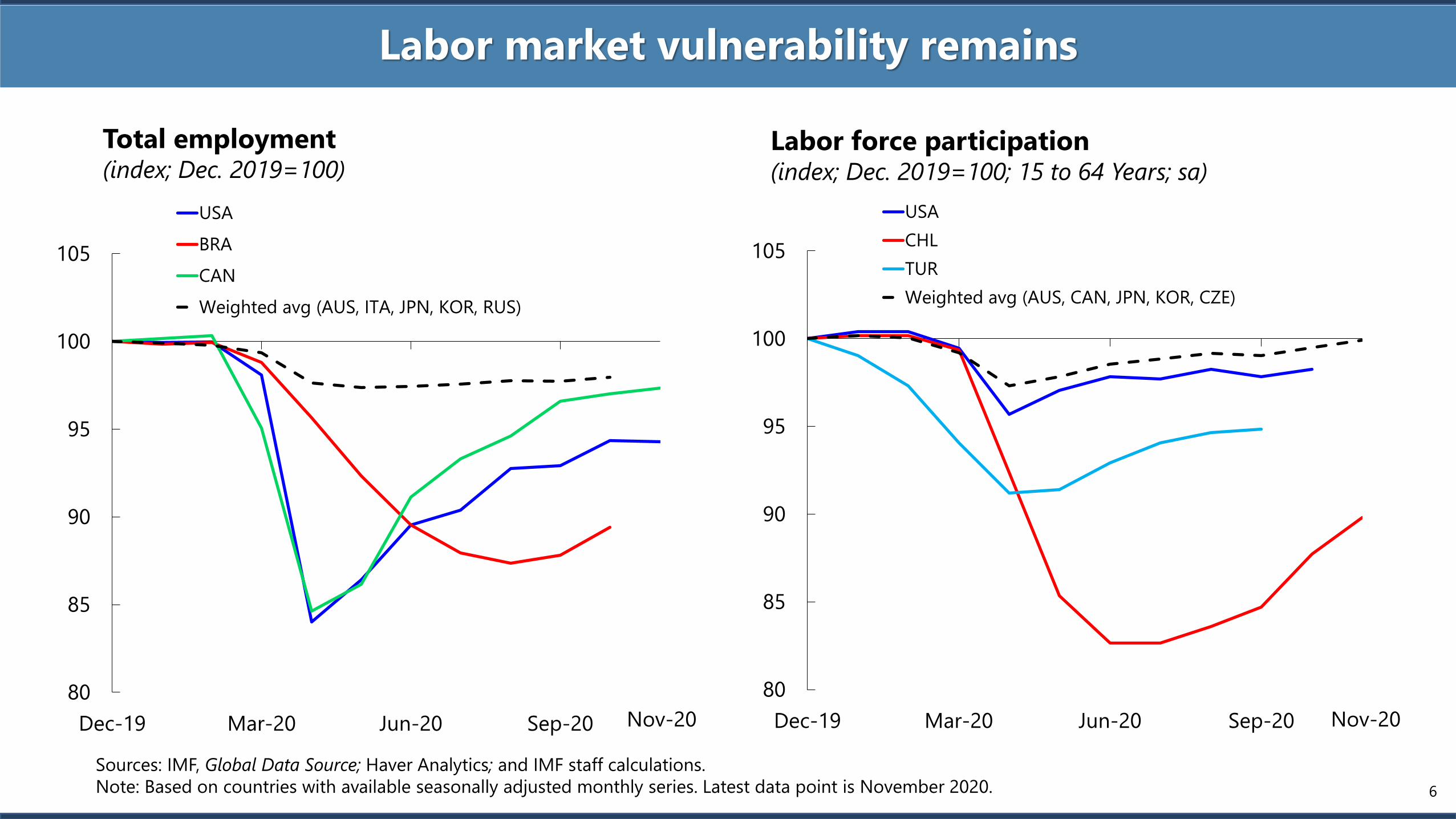

Labor market vulnerability remains

Labor force participation (index; Dec. 2019=100; 15 to 64 Years; sa)

Total employment(index; Dec. 2019=100)

Sources: IMF, Global Data Source; Haver Analytics; and IMF staff calculations.

Note: Based on countries with available seasonally adjusted monthly series. Latest data point is November 2020.

80

85

90

95

100

105

Dec-19 Mar-20 Jun-20 Sep-20

USA

CHL

TUR

Weighted avg (AUS, CAN, JPN, KOR, CZE)

80

85

90

95

100

105

Dec-19 Mar-20 Jun-20 Sep-20

USA

BRA

CAN

Weighted avg (AUS, ITA, JPN, KOR, RUS)

Nov-20Nov-20

6

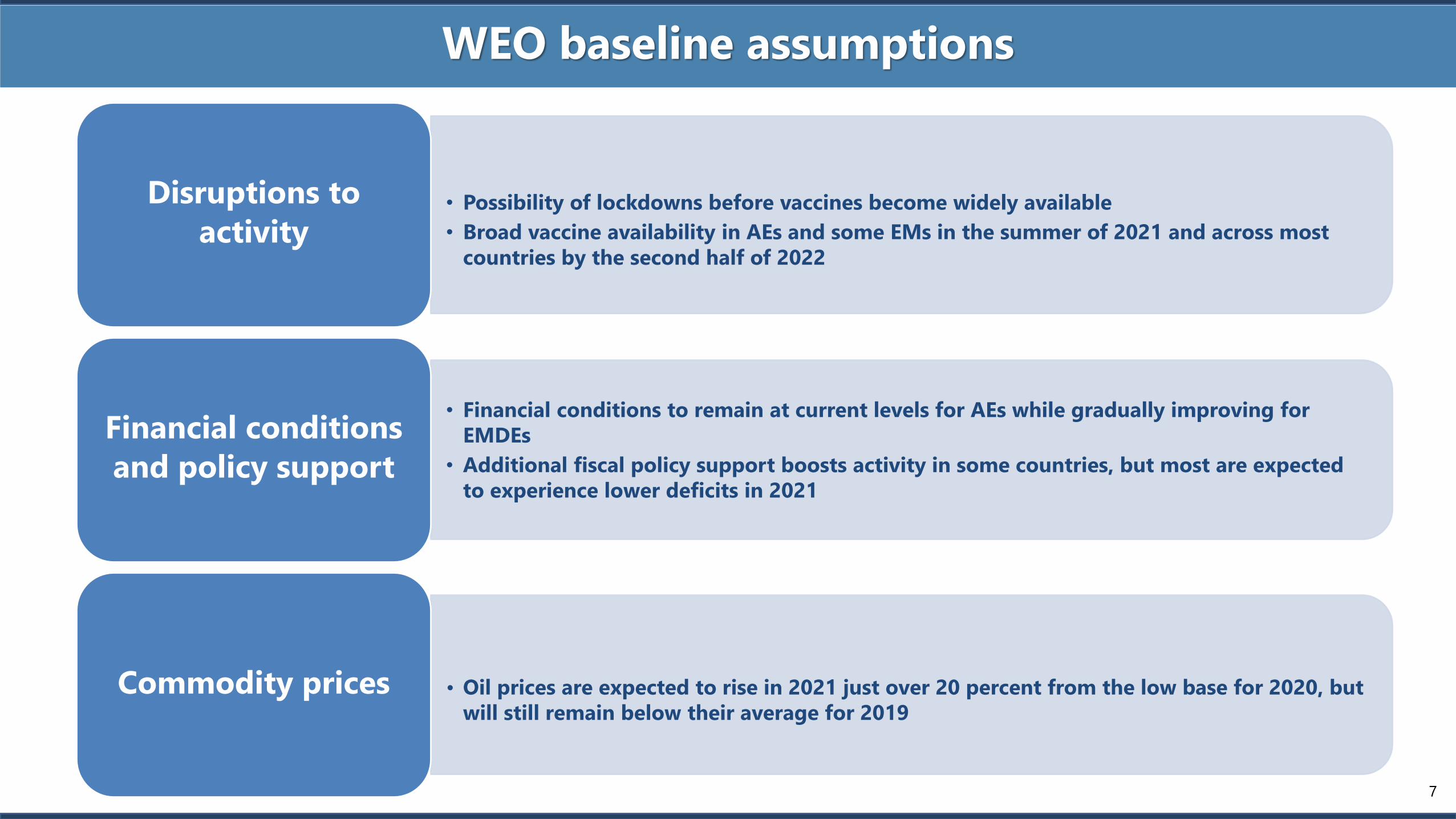

WEO baseline assumptions

• Possibility of lockdowns before vaccines become widely available

• Broad vaccine availability in AEs and some EMs in the summer of 2021 and across most

countries by the second half of 2022

Disruptions to

activity

• Financial conditions to remain at current levels for AEs while gradually improving for

EMDEs

• Additional fiscal policy support boosts activity in some countries, but most are expected

to experience lower deficits in 2021

Financial conditions

and policy support

• Oil prices are expected to rise in 2021 just over 20 percent from the low base for 2020, but

will still remain below their average for 2019

Commodity prices

7

WEO Projections

World

Advanced

Economies U.S. Euro Area Japan U.K. Canada

Other

Advanced

Asia

2020 -3.5 -4.9 -3.4 -7.2 -5.1 -10.0 -5.5 -1.5

Revision from

Oct. 2020 0.9 0.9 0.9 1.1 0.2 -0.2 1.6 1.4

2021 5.5 4.3 5.1 4.2 3.1 4.5 3.6 3.6

Revision from

Oct. 2020 0.3 0.4 2.0 -1.0 0.8 -1.4 -1.6 0.3

2022 4.2 3.1 2.5 3.6 2.4 5.0 4.1 2.9

Revision from

Oct. 2020 0.0 0.2 -0.4 0.5 0.7 1.8 0.7 0.1

Growth projections: Advanced economies (percent change from a year earlier)

Source: IMF, World Economic Outlook January 2021. 9

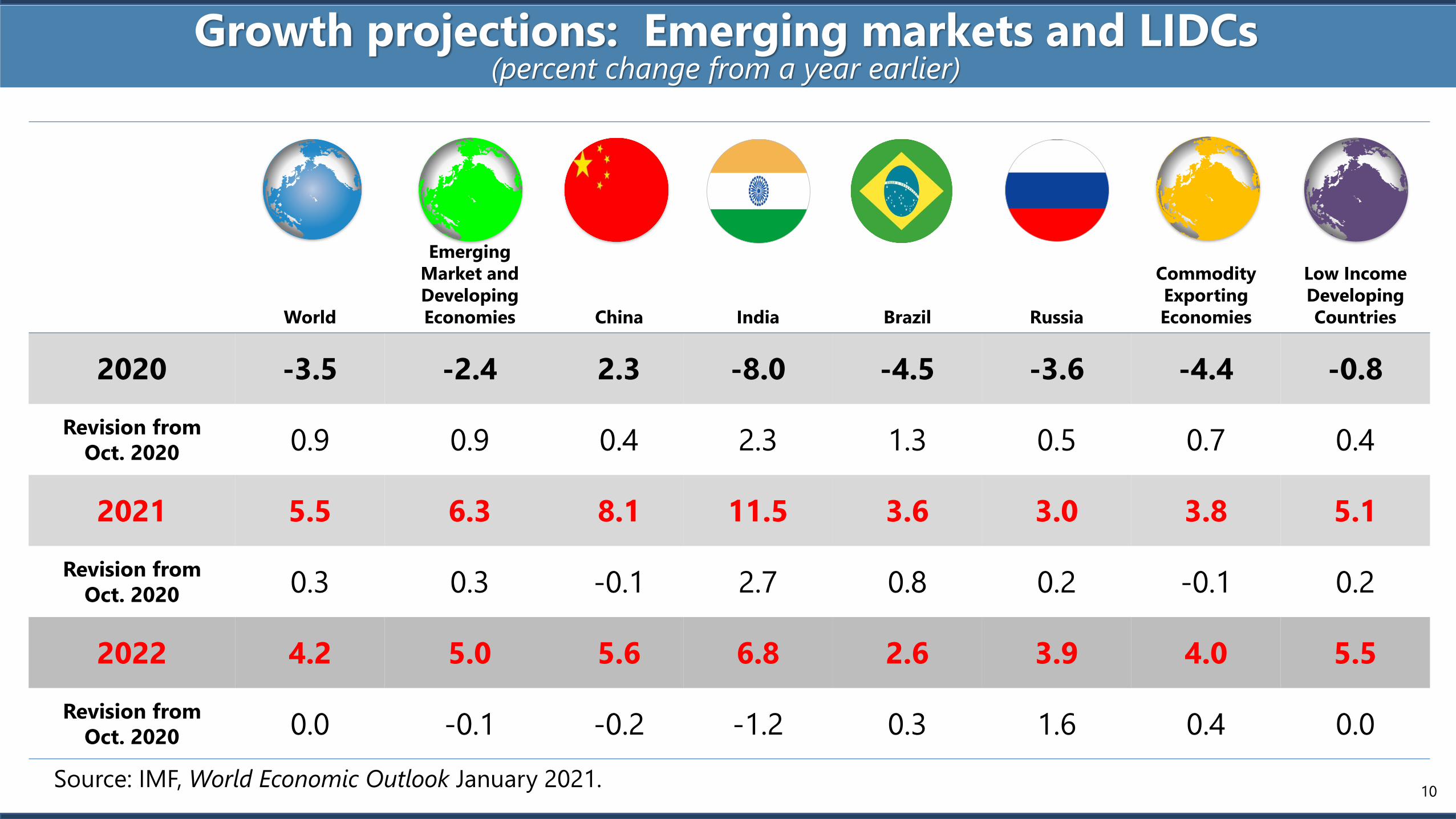

World

Emerging

Market and

Developing

Economies China India Brazil Russia

Commodity

Exporting

Economies

Low Income

Developing

Countries

2020 -3.5 -2.4 2.3 -8.0 -4.5 -3.6 -4.4 -0.8

Revision from

Oct. 2020 0.9 0.9 0.4 2.3 1.3 0.5 0.7 0.4

2021 5.5 6.3 8.1 11.5 3.6 3.0 3.8 5.1

Revision from

Oct. 2020 0.3 0.3 -0.1 2.7 0.8 0.2 -0.1 0.2

2022 4.2 5.0 5.6 6.8 2.6 3.9 4.0 5.5

Revision from

Oct. 2020 0.0 -0.1 -0.2 -1.2 0.3 1.6 0.4 0.0

Growth projections: Emerging markets and LIDCs (percent change from a year earlier)

Source: IMF, World Economic Outlook January 2021.10

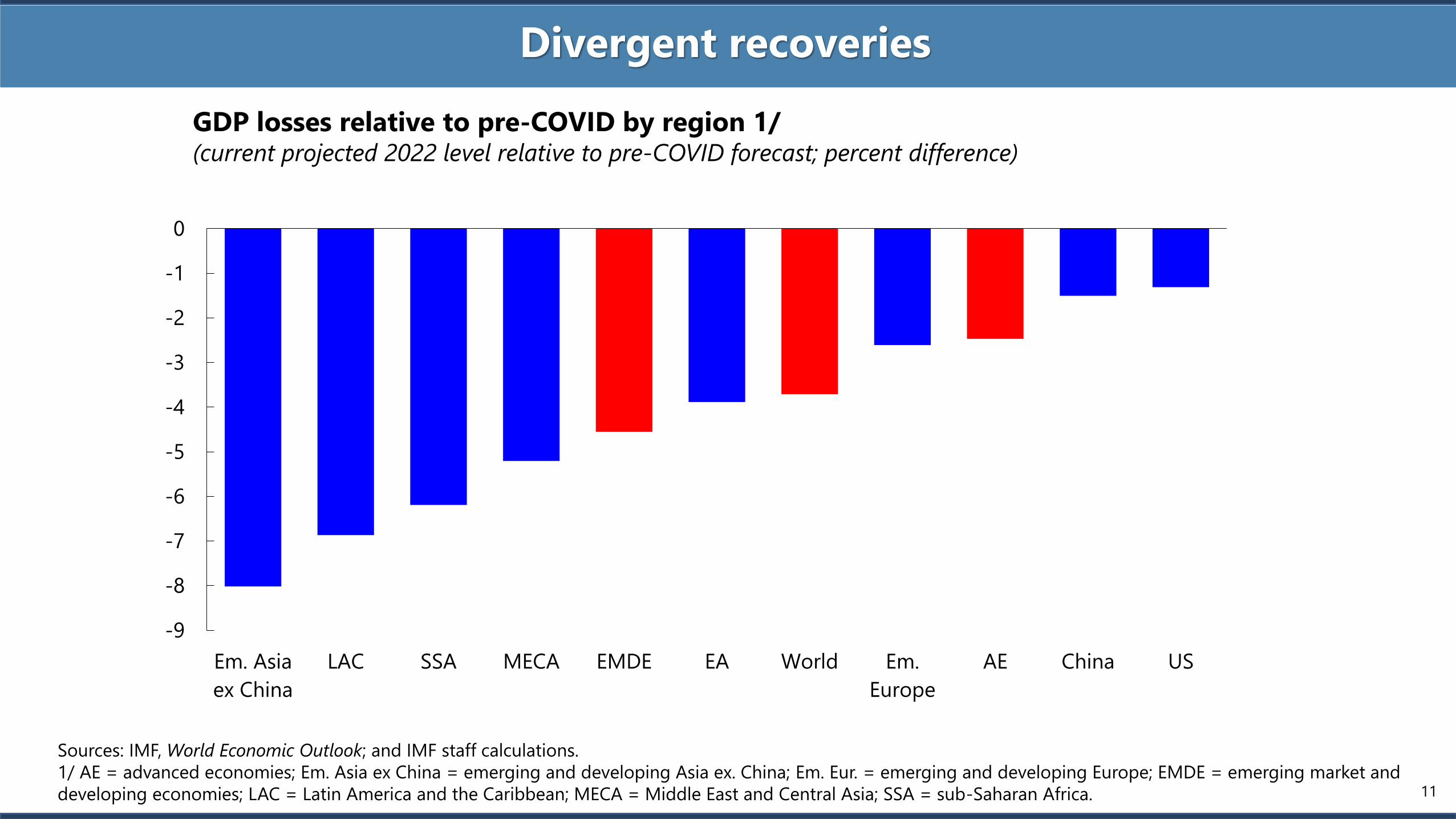

Divergent recoveries

Sources: IMF, World Economic Outlook; and IMF staff calculations.

1/ AE = advanced economies; Em. Asia ex China = emerging and developing Asia ex. China; Em. Eur. = emerging and developing Europe; EMDE = emerging market and

developing economies; LAC = Latin America and the Caribbean; MECA = Middle East and Central Asia; SSA = sub-Saharan Africa.

GDP losses relative to pre-COVID by region 1/(current projected 2022 level relative to pre-COVID forecast; percent difference)

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

Em. Asia

ex China

LAC SSA MECA EMDE EA World Em.

Europe

AE China US

11

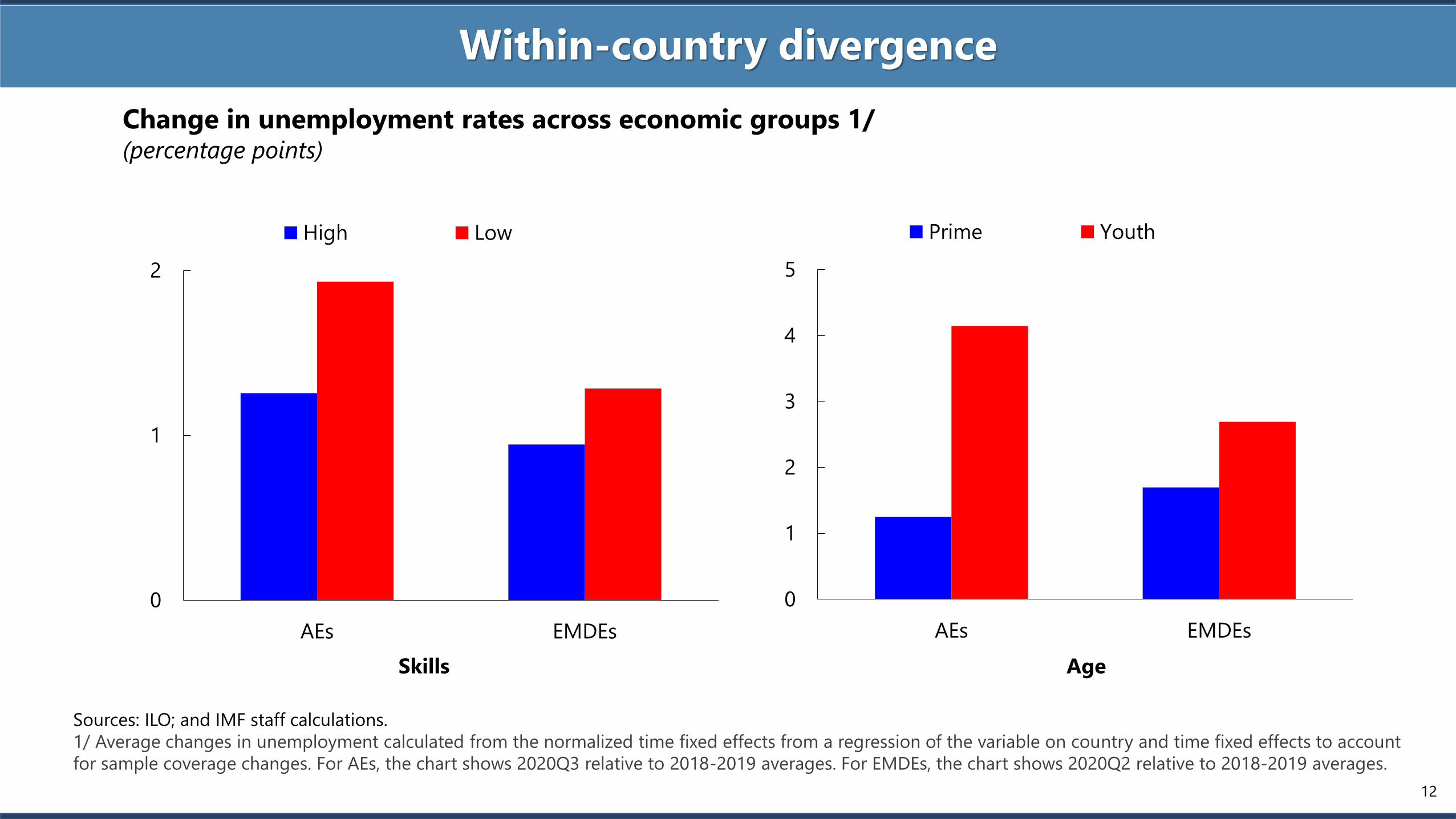

Within-country divergence

Sources: ILO; and IMF staff calculations.

1/ Average changes in unemployment calculated from the normalized time fixed effects from a regression of the variable on country and time fixed effects to account

for sample coverage changes. For AEs, the chart shows 2020Q3 relative to 2018-2019 averages. For EMDEs, the chart shows 2020Q2 relative to 2018-2019 averages.

Change in unemployment rates across economic groups 1/(percentage points)

0

1

2

3

4

5

AEs EMDEs

Prime Youth

0

1

2

AEs EMDEs

High Low

Skills Age

12

40%

43%

53%

60%

62%

62%

65%

64%

71%

75%

75%

77%

77%

78%

80%

54%

68%

69%

65%

64%

69%

69%

76%

83%

79%

78%

79%

81%

85%

35% 55% 75% 95%

France

Russia

South Africa

Japan

Italy

Spain

Germany

United States

Canada

South Korea

Australia

Mexico

United Kingdom

Brazil

China

Willingness to get COVID-19 vaccine

Sources Haver Analytics; OxCGRT; Duke Global Health Innovation Center; Global Advisor; Ipsos; and IMF staff calculations.

1/ Based on18,526 online adults aged 16-74 across 15 countries.

Divergences: Vaccines/Therapies

COVID-19 doses administered (per100 persons; as of 1/25/ 2021)

Vaccine supply coverage

(percent of population; confirmed

agreements only)December 2020 October 2020

0

50

100

150

200

250

300

G20 AEs G20 EMs non-G20

EMs

non-G20

LIDCs

2020Q4

2021Q1

2021Q2

2021Q3

2021Q4

Unknown

Vaccine demand 1/(percent)

(1/23/2021)

(1/24/2021)

(1/23/2021)

(1/24/2021)

(1/13/2021)

(1/23/2021)

(1/17/2021)

(1/24/2021)

(1/24/2021)

(1/22/2021)

(1/24/2021)

(1/20/2021)

(1/22/2021)

(1/23/2021)

(1/23/2021)

(1/23/2021)

(1/20/2021)

(1/23/2021)

(1/24/2021)

(1/24/2021)

0 10 20 30 40 50

India

Brazil

Mexico

Argentina

Russia

World

Saudi Arabia

Turkey

France

Germany

Italy

Ireland

Spain

Slovenia

Denmark

United States

Bahrain

United Kingdom

United Arab Emirates

Israel

13

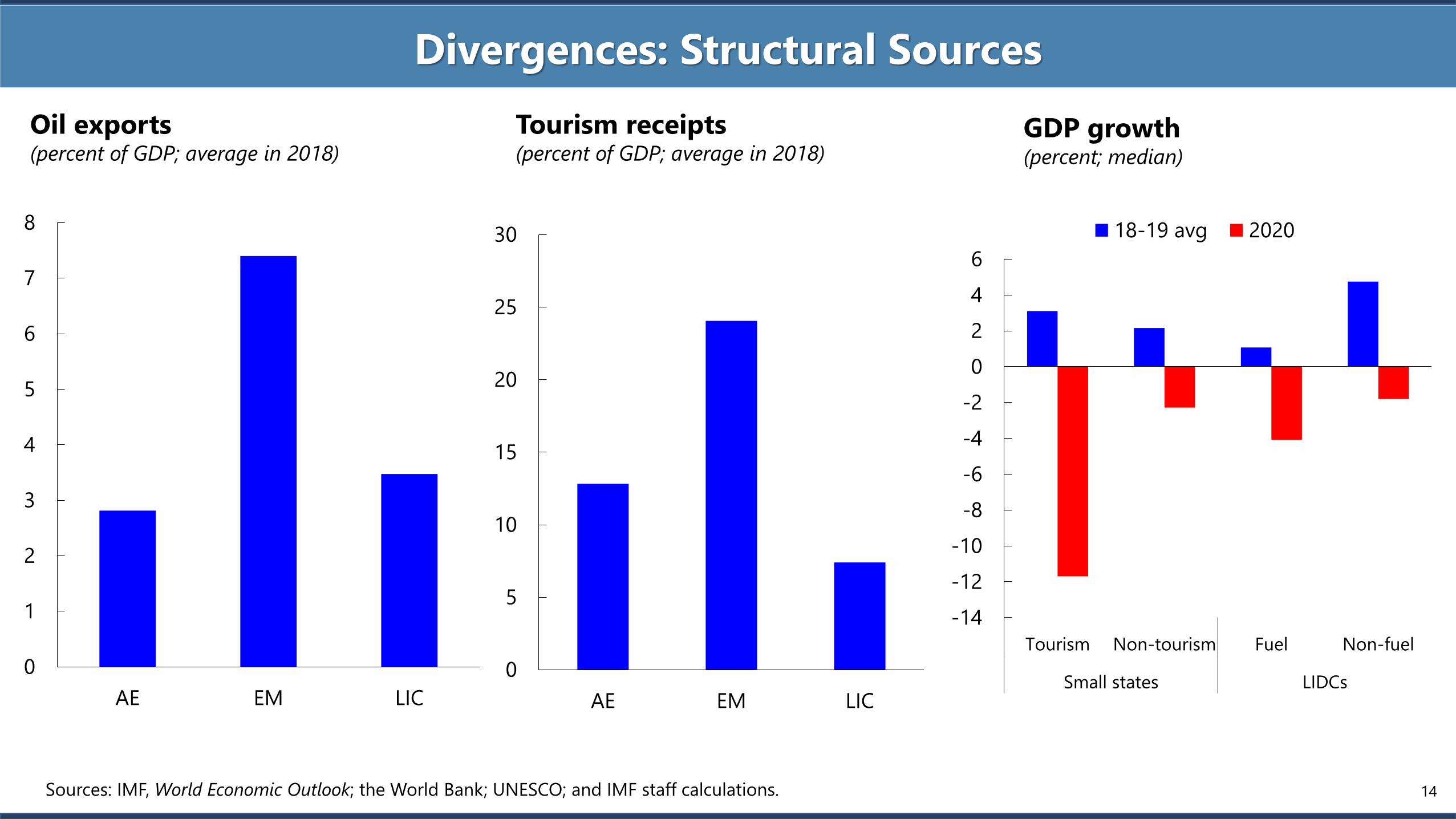

Divergences: Structural Sources

Sources: IMF, World Economic Outlook; the World Bank; UNESCO; and IMF staff calculations.

GDP growth(percent; median)

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

Tourism Non-tourism Fuel Non-fuel

Small states LIDCs

18-19 avg 2020

Oil exports(percent of GDP; average in 2018)

Tourism receipts(percent of GDP; average in 2018)

0

1

2

3

4

5

6

7

8

AE EM LIC

0

5

10

15

20

25

30

AE EM LIC

14

Divergences: Income support, Education

Sources: IMF, World Economic Outlook; the World Bank; UNESCO; and IMF staff calculations.

School closures and enrollment(percent of students)

0

10

20

30

40

50

60

70

80

90

100

3/15 6/1 10/15 1/5 3/15 6/1 10/15 1/5

Advanced economies Emerging and developing

economies

Closed Partially open Fully open Academic break

Share of households with falling income and share

of households that received support (percent)

BGR

CHLCOL

CRIDOM

ECU

GAB

GTM

HRV

PHL

PRY

SLV

TUN ETH

GHA

HND

LAO

MMR

MWINGA

TJKUZB

VNM

ZMB

0

10

20

30

40

50

60

70

80

90

0 10 20 30 40 50 60 70 80 90

Sh

are

of

ho

use

ho

lds

that

rece

ived

su

pp

ort

Share of households with falling income

EMDEs LICs

15

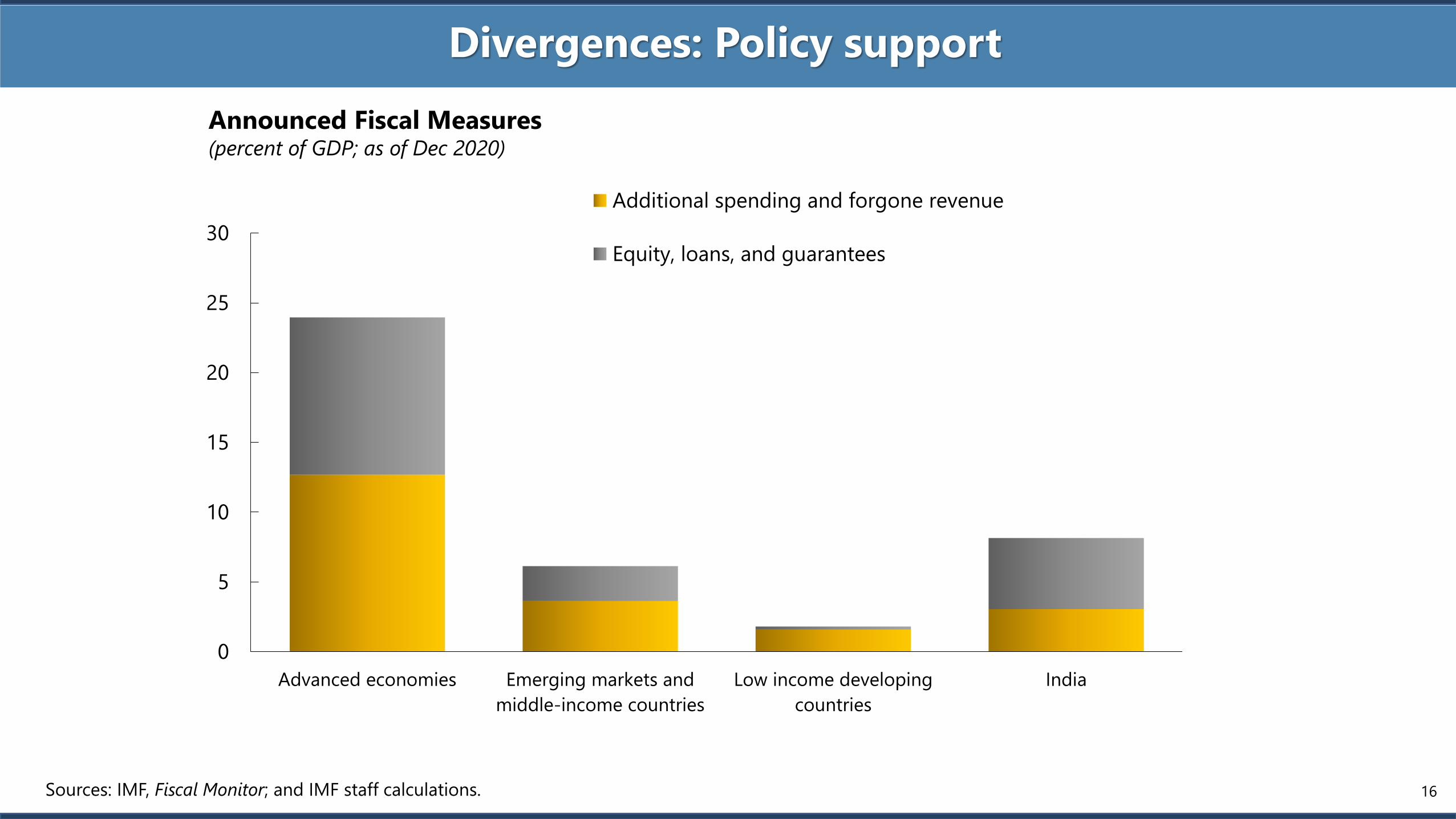

Divergences: Policy support

16

0

5

10

15

20

25

30

Advanced economies Emerging markets and

middle-income countries

Low income developing

countries

India

Additional spending and forgone revenue

Equity, loans, and guarantees

Announced Fiscal Measures(percent of GDP; as of Dec 2020)

Sources: IMF, Fiscal Monitor; and IMF staff calculations.

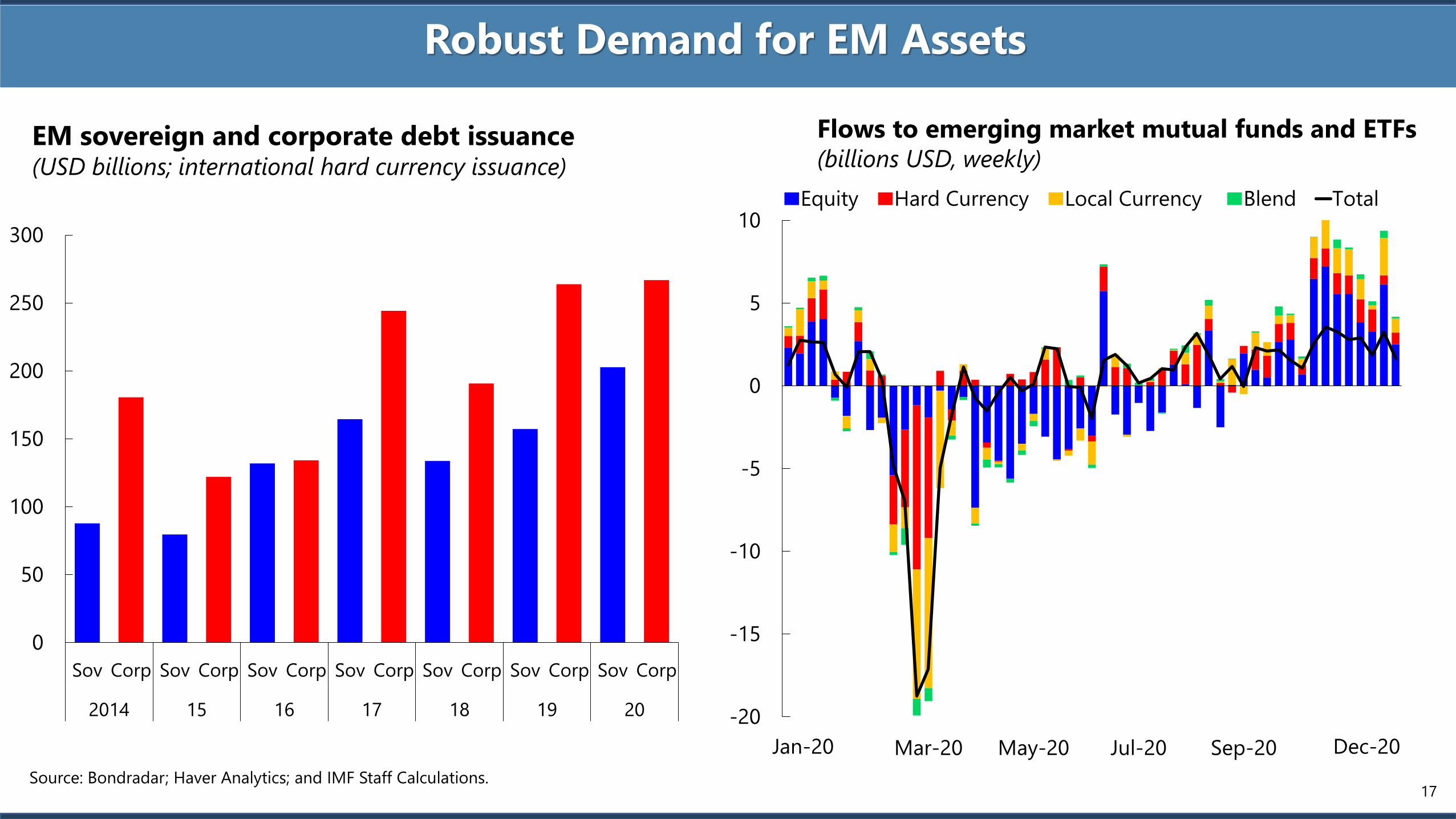

Robust Demand for EM Assets

EM sovereign and corporate debt issuance(USD billions; international hard currency issuance)

17

Flows to emerging market mutual funds and ETFs(billions USD, weekly)

0

50

100

150

200

250

300

Sov Corp Sov Corp Sov Corp Sov Corp Sov Corp Sov Corp Sov Corp

2014 15 16 17 18 19 20

Source: Bondradar; Haver Analytics; and IMF Staff Calculations.

-20

-15

-10

-5

0

5

10

Mar-20 May-20 Jul-20 Sep-20

Equity Hard Currency Local Currency Blend Total

Jan-20 Dec-20

Supportive Borrowing Conditions

18

India: Bond Yields and General Government Debt(yield in percent, general government debt in percent of GDP)

Source: IMF, Historical Public Debt Database; IMF, World Economic Outlook; JST Macro-History database; Maddison Database Project; Thomson Reuters Datastream, Global Financial Data;

Refinitiv, Reserve Bank of India; Ministry of Finance of the Government of India and IMF Staff Calculations.

0

2

4

6

8

10

12

14

0

20

40

60

80

100

120

140

1880

1890

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

2010

2020

Advanced

Economies

Debt (% GDP,

LHS)

WWI WWIIGlobal

Financial

Crisis

Great

Lockdown

Advanced

Economies

Long-term

interest rate (%,

RHS)

Great

Depression

50

55

60

65

70

75

80

85

90

5

6

7

8

9

10

2000/0

1

2001/0

2

2002/0

3

2003/0

4

2004/0

5

2005/0

6

2006/0

7

2007/0

8

2008/0

9

2009/1

0

2010/1

1

2011/1

2

2012/1

3

2013/1

4

2014/1

5

2015/1

6

2016/1

7

2017/1

8

2018/1

9

2019/2

0 (

est

imate

)

2020/2

1 (

pro

ject

ion

)

10-Year Sovereign Yields General Government Debt (Right Scale)

Public debt and bond yields in historical perspective(yields in percent; public debt in percent of GDP)

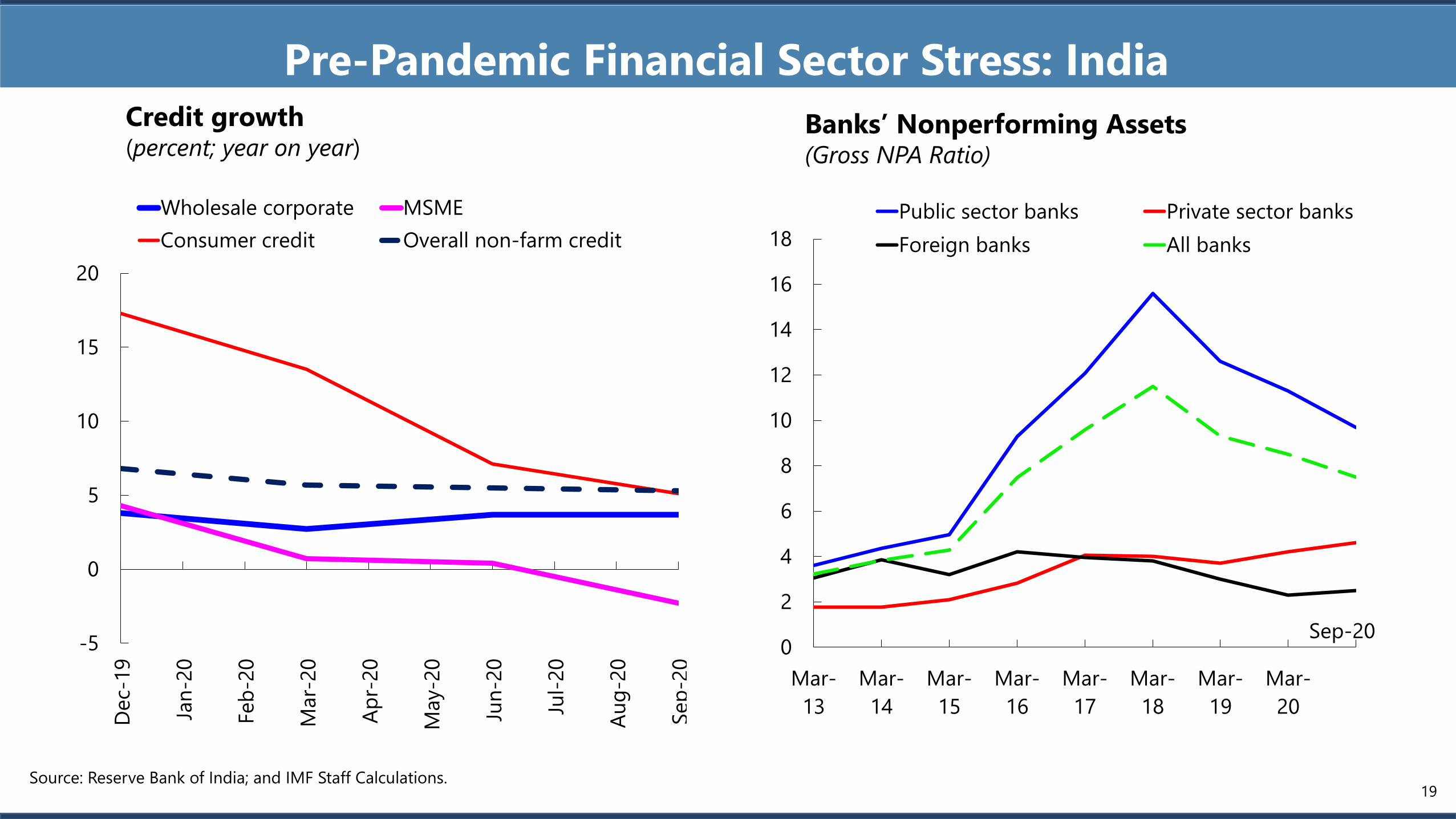

Pre-Pandemic Financial Sector Stress: India

-5

0

5

10

15

20

Dec-

19

Jan

-20

Feb

-20

Mar-

20

Ap

r-20

May-2

0

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Wholesale corporate MSME

Consumer credit Overall non-farm credit

Credit growth(percent; year on year)

0

2

4

6

8

10

12

14

16

18

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Mar-

17

Mar-

18

Mar-

19

Mar-

20

Public sector banks Private sector banks

Foreign banks All banks

Banks’ Nonperforming Assets(Gross NPA Ratio)

Sep-20

Source: Reserve Bank of India; and IMF Staff Calculations.19

Accelerate shift to more inclusive and sustainable growth

Global CO2 emissions(gigatons of CO2)

Sources: carbonmonitor.org; IMF, World Economic Outlook; IMF VE database; and IMF staff calculations.

1/ Other consists of compensatory transfers to households and avoided damages from climate change.

Impact on real GDP from

infrastructure investment(percent deviation from baseline)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20 21 22 23 24 25

G-20 AEs: Without spillovers

G-20 AEs: With spillovers

G-20 EMs: Without spillovers

G-20 EMs: With spillovers

Global: Without spillovers

Global: With spillovers

0

10

20

30

40

50

60

70

80

90

100

EM LIDC

High

Medium

EM and LIDC: Fiscal vulnerabilities(percent of total countries)

0

10

20

30

40

50

60

70

80

20 25 30 35 40 45 50

(1) Baseline

(2) 1 + Deviation from green infrastructure and subsidy

(3) 2 + Deviation from carbon pricing and other 1/

20