B M O N E S B I T T B U R N SThe

Gabri Lalonde Advisory Group Fundamental vs. Technical Analysis

Kevin Gabri, B.A. Economics, CIM Vice President, Branch Manager, Wealth Advisor, Associate Portfolio Manager

Tel: 613-938-0151 [email protected]

Troy Lalonde, B.A. Comm. Wealth Advisor, Associate Portfolio Manager

Tel: 613-938-0151 [email protected]

Cindy Charlebois, B.A. Econ Investment Representative

Tel: 613-938-0151 [email protected]

BMO Nesbitt Burns 100 - 55 Water Street West Cornwall, ON K6J 1A1

www.kevingabri.com

Introduction

How many times have you heard on BNN or

read news articles that talked about funda-

mental or technical research? The likelihood

is pretty high that at some point you have

come across these terms. For many however,

they don’t fully understand the differences

and advantages that each type of research

provides. As a team we have decided that it is

imperative that our clients fully comprehend

the methods we use in constructing portfolios

and that we continually educate our clients.

History of Fundamental and Technical Analysis

Fundamental analysis is as old as the markets

themselves. The modern day fathers of

“fundamental analysis” can be traced back

to the publication of “Security Analysis”

which was authored by Benjamin Graham

and David Dodd in 1934. Dodd & Graham

offered investors an insight as to what factors

one should be examining when making

an investment decision. These included;

earnings, revenues, growth rates, cash flow

assessments etc. Most investors are aware

and use this type of analysis whether they

realize it or not.

Technical analysis on the other hand goes

back roughly 100 years and has evolved

considerably over the last century. Charles

Dow the first editor of the Wall Street Journal

played a pivotal role in the development of

technical analysis. He began what is known

as “Point and Figure Charting” which is a

simple logical way of recording the supply

and demand relationship in any stock. Dow’s

definition of what a trend is and his focus

on studying price action for gaining insight

into stocks set the foundation for technical

analysis as we know it today.

Fundamental Analysis

So what exactly is fundamental analysis?

Well the purpose of fundamental analysis is

to estimate a security’s “intrinsic value” by

examining a combination of qualitative and

quantitative factors.

Once an estimate of a security’s intrinsic

value is determined it is then compared

to the security’s current price. The

security can be one of three things when

compared to intrinsic value; 1) Overvalued

(current price>intrinsic value estimate), 2)

Undervalued (current price < intrinsic value

estimate), or, 3) Properly valued (current

price=intrinsic value estimate).

If the security is deemed to be “overvalued”

we sell or go short and if we believe it is

“undervalued” we go long or buy. The idea

is that over time the security’s price will

converge and reach our estimated intrinsic

value producing a return in the process.

Fundamental vs. Technical Analysis

The Gabri Lalonde Wealth AdvisoryGroup

The Gabri Lalonde Advisory Group

In conducting this type of analysis two significant assumptions

are made. The first is that the current price of the security being

analyzed is incorrect. Essentially, this means that the market is

believed to be wrong. The second assumption is that over the

long-term the security will approach its “intrinsic value”.

These two assumptions open the door to significant criticism.

Those that believe that the markets are “efficient” and in what

is known in finance as the Efficient Market Hypothesis argue

that the current price of a security reflects all information both

current and future. The other criticism comes in the assumption

that the security will approach its intrinsic value. Is it really

realistic to assume that the security’s price in the market will

converge to your estimate of intrinsic value? Some would argue

no while fundamental analysis proponents would say yes.

Conducting Fundamental Analysis

When a fundamental analyst sits down to begin his/her

analysis they must gather a wide variety of data in order to

compare and analyze both quantitative and qualitative factors.

Before the analysis begins the analyst lays out a wide range

of questions which they will attempt to answer on their way

to generating that ever important “intrinsic value” estimate.

These questions include but are not limited to:

• What is the company’s current business?

• Is revenue growing?

• Are they profitable?

• What are their products/services?

• How are they faring vs. competitors?

• What is the industry structure?

• What is their financial situation?

• Do they have a strong management team?

Both quantitative and qualitative factors are used to answer

these questions.

Quantitative Factors

Quantitative factors are measured in numerical terms. They

would include things such as earnings, cash flow needs,

growth rates etc... and the data used to compile them is pulled

from a variety of financial sources. The three main sources of

data used in compiling quantitative values are the company’s

balance sheet, income statement and cash flow statement.

The company’s balance sheet shows their assets, liabilities

and equity at a particular point in time. The income statement

shows a summary of a company’s revenue and expenses for a

given period and the cash flow statement shows a company’s

cash inflows and outflows. From these three statements

analysts are able to answer some of the questions listed above.

A fundamental analyst will then take all of the quantitative data

and calculate various financial metrics in order to get a sense of

the company’s prospects going forward and to compare them

relative to their peers and the industry they operate in. They

also use Ratio Analysis to gauge whether the company appears

to be undervalued, or overvalued versus their peers.

Qualitative Factors

Qualitative factors are much more challenging to analyze

compared to quantitative factors in that they are very difficult to

measure. They include but are not limited to intangibles such

as: the strength of the company’s business model, the quality of

their management team, patents, their competitive position and

corporate governance structure. Analysts attempt to come up

with some way of attaching a value to these things that can be

used in the determination of the company’s intrinsic value.

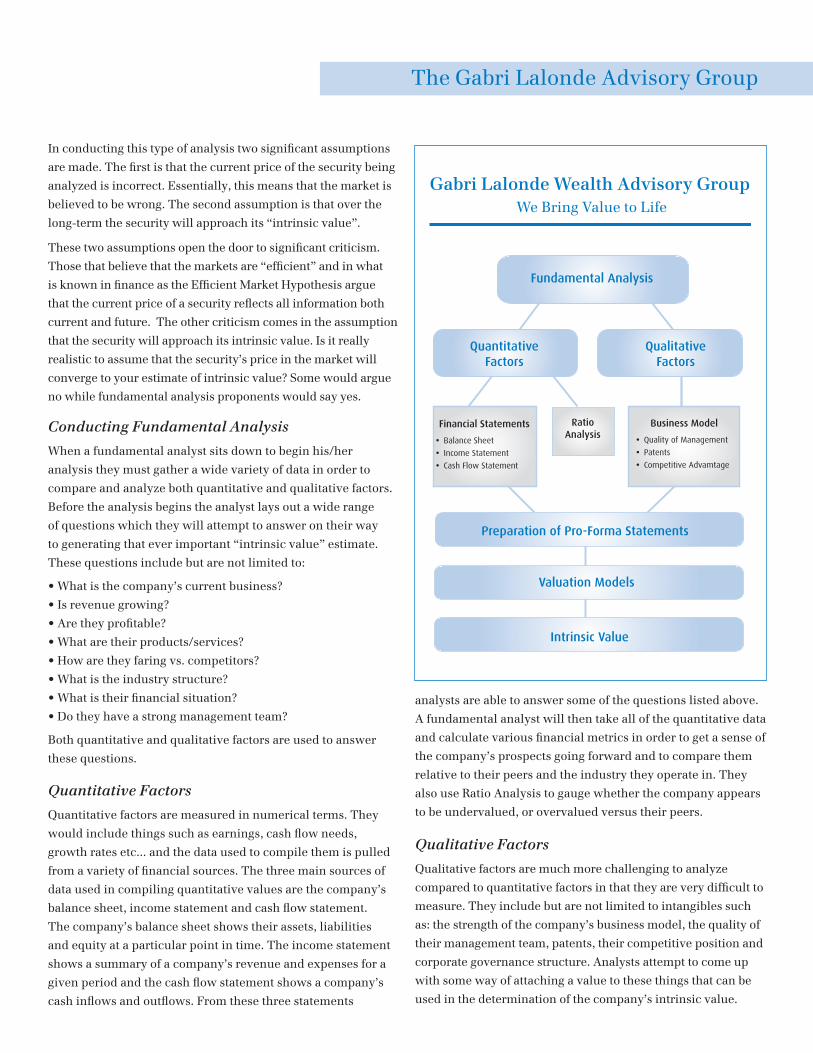

Gabri Lalonde Wealth Advisory GroupWe Bring Value to Life

Fundamental Analysis

QuantitativeFactors

QualitativeFactors

RatioAnalysis

Intrinsic Value

Preparation of Pro-Forma Statements

Valuation Models

Financial Statements

� Balance Sheet

� Income Statement

� Cash Flow Statement

Business Model

� Quality of Management

� Patents

� Competitive Advamtage

Pro-Forma Statements Preparation and Valuation Models

Once the analyst has compiled the quantitative data and

analyzed qualitative factors they then produce what is called

“Pro-Forma” financial statements. These are forward looking

financial statements that analysts use to project out companies

cash flows, earnings etc. After pro-forma statements have been

created, analysts then turn their attention to plugging the data

into valuation models. These are usually proprietary and vary

substantially in the way that they arrive at a final “intrinsic

value”.

Summation

Performing fundamental analysis should provide analysts/

investors with a strong understanding of the security’s

business model, the industry it operates in and its competitive

advantage. By using both quantitative and qualitative factors,

analysts are then able to generate pro-forma financial state-

ments and take the results and plug them into a valuation

models in order to produce an estimate of the security’s

intrinsic value. Once the analyst has performed the pain

staking task of gathering and analyzing all the data and has

produced the “intrinsic value” estimate they simply compare it

to the security’s current price and buy if the price is below the

intrinsic value and sell if the security’s current price is above

the estimate.

Technical Analysis

Technical analysis differs from fundamental analysis in

that the emphasis is not on determining an intrinsic value

but rather it focuses on identifying “patterns” and “trends”

which may suggest future price movements. It uses statistics

generated by past movements in both price and volume data.

Technical analysts hold the belief that historical performance

of both stocks and the markets are indicators of future perfor-

mance and focus their attention on identifying patterns.

Some analysts rely on chart patterns and others on technical

indicators in order to predict future security performance.

At its root technicians rely solely on supply/demand of a

particular security in forecasting future performance.

The field of technical analysis relies on three assumptions

holding true. The first assumption is that the markets discount

everything. That is all information is already incorporated in

the price of a security. The second is that prices move in trends.

The final assumption which is probably the most important of

the three is that history repeats itself.

Technicians believe that investor psychology provides

consistent reaction given certain stimuli over time.

Like fundamentalists technicians do suffer from criticism.

The largest comes from fundamentalists who argue that

technical analysis ignores company fundamentals completely.

Technicians know nothing and care to know nothing about the

security they are analyzing. Instead they focus their attention

on strictly supply and demand conditions.

Conducting Technical Analysis

Technicians begin their analysis by compiling price and

volume data. From there they use a wide array of statistical

tools which can be broken down into two categories;

1) Charting

2) Technical Indicators.

Fundamental vs. Technical Analysis

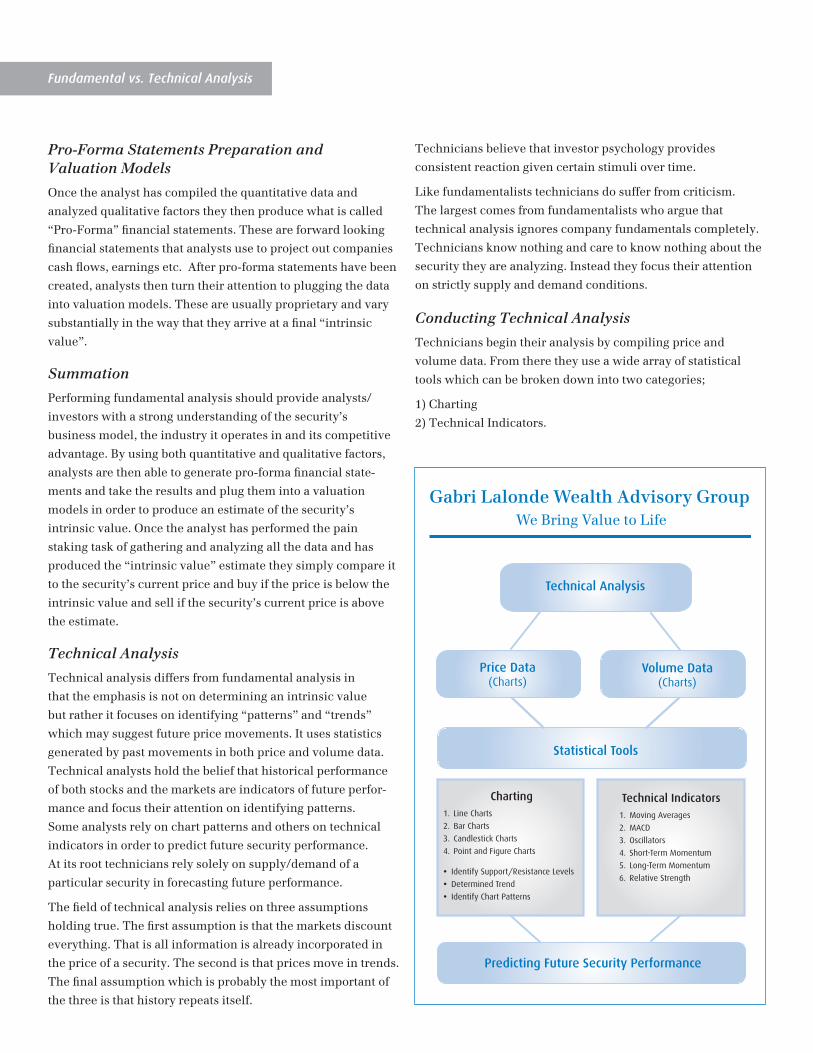

Gabri Lalonde Wealth Advisory GroupWe Bring Value to Life

Technical Analysis

Statistical Tools

Price Data(Charts)

Volume Data(Charts)

Predicting Future Security Performance

Charting1. Line Charts

2. Bar Charts

3. Candlestick Charts

4. Point and Figure Charts

� Identify Support/Resistance Levels

� Determined Trend

� Identify Chart Patterns

Technical Indicators1. Moving Averages

2. MACD

3. Oscillators

4. Short-Term Momentum

5. Long-Term Momentum

6. Relative Strength

The Gabri Lalonde Advisory Group

Charting

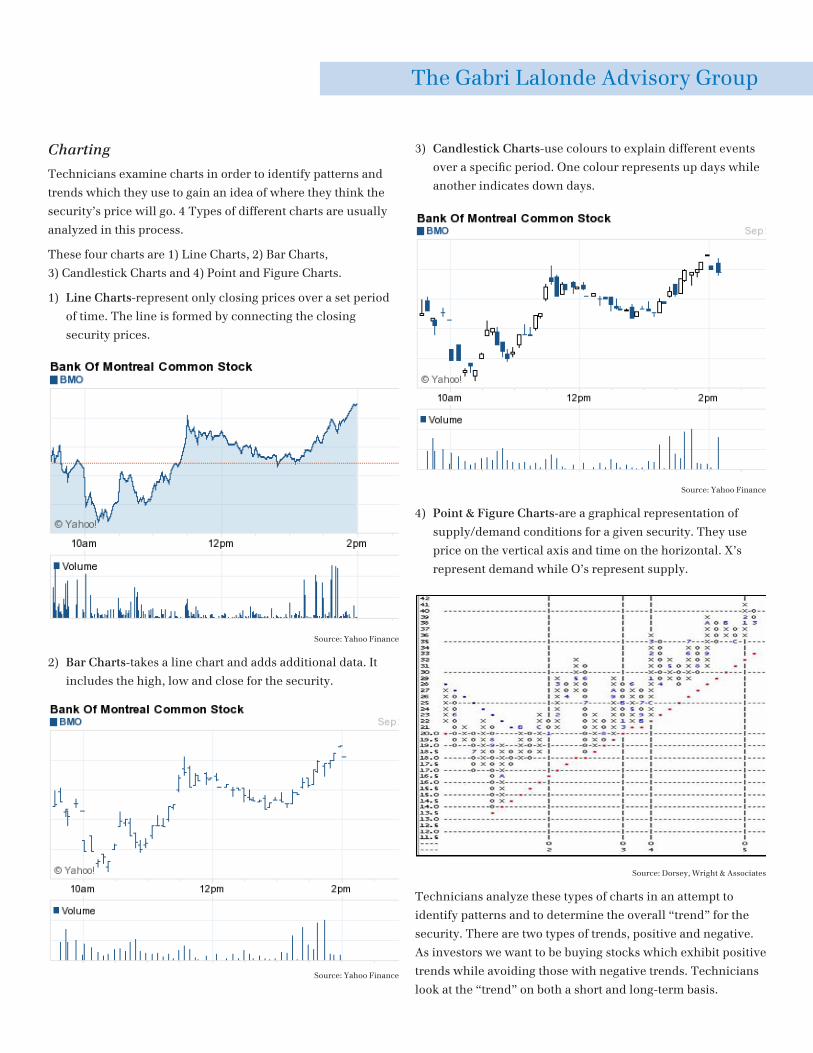

Technicians examine charts in order to identify patterns and

trends which they use to gain an idea of where they think the

security’s price will go. 4 Types of different charts are usually

analyzed in this process.

These four charts are 1) Line Charts, 2) Bar Charts,

3) Candlestick Charts and 4) Point and Figure Charts.

1) Line Charts-represent only closing prices over a set period

of time. The line is formed by connecting the closing

security prices.

Source: Yahoo Finance

2) Bar Charts-takes a line chart and adds additional data. It

includes the high, low and close for the security.

Source: Yahoo Finance

3) Candlestick Charts-use colours to explain different events

over a specific period. One colour represents up days while

another indicates down days.

Source: Yahoo Finance

4) Point & Figure Charts-are a graphical representation of

supply/demand conditions for a given security. They use

price on the vertical axis and time on the horizontal. X’s

represent demand while O’s represent supply.

Source: Dorsey, Wright & Associates

Technicians analyze these types of charts in an attempt to

identify patterns and to determine the overall “trend” for the

security. There are two types of trends, positive and negative.

As investors we want to be buying stocks which exhibit positive

trends while avoiding those with negative trends. Technicians

look at the “trend” on both a short and long-term basis.

Fundamental vs. Technical Analysis

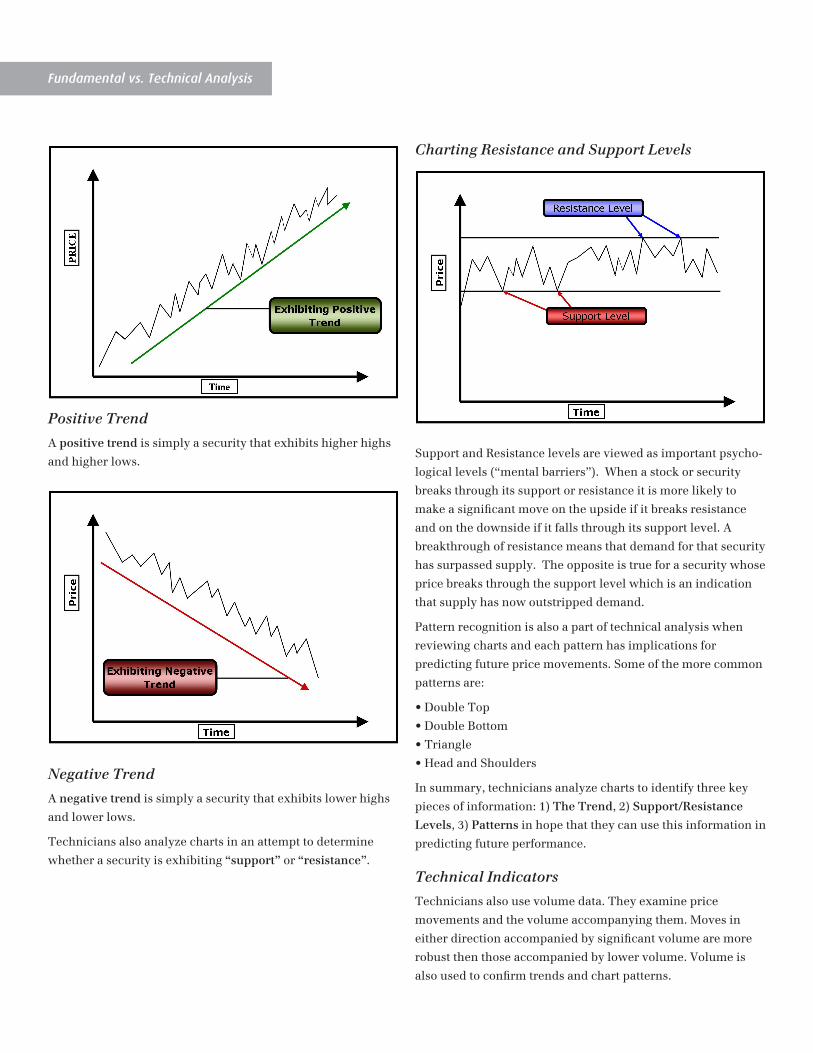

Positive Trend

A positive trend is simply a security that exhibits higher highs

and higher lows.

Negative Trend

A negative trend is simply a security that exhibits lower highs

and lower lows.

Technicians also analyze charts in an attempt to determine

whether a security is exhibiting “support” or “resistance”.

Charting Resistance and Support Levels

Support and Resistance levels are viewed as important psycho-

logical levels (“mental barriers”). When a stock or security

breaks through its support or resistance it is more likely to

make a significant move on the upside if it breaks resistance

and on the downside if it falls through its support level. A

breakthrough of resistance means that demand for that security

has surpassed supply. The opposite is true for a security whose

price breaks through the support level which is an indication

that supply has now outstripped demand.

Pattern recognition is also a part of technical analysis when

reviewing charts and each pattern has implications for

predicting future price movements. Some of the more common

patterns are:

• Double Top

• Double Bottom

• Triangle

• Head and Shoulders

In summary, technicians analyze charts to identify three key

pieces of information: 1) The Trend, 2) Support/Resistance

Levels, 3) Patterns in hope that they can use this information in

predicting future performance.

Technical Indicators

Technicians also use volume data. They examine price

movements and the volume accompanying them. Moves in

either direction accompanied by significant volume are more

robust then those accompanied by lower volume. Volume is

also used to confirm trends and chart patterns.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. (“BMO NBI”). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. BMO NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. ® “BMO (M-bar Roundel symbol)” is a registered trade-mark of Bank of Montreal, used under licence. ® “Nesbitt Burns” is a registered trade-mark of BMO Nesbitt Burns Inc. BMO Nesbitt Burns Inc. is a wholly-owned subsidiary of Bank of Montreal. All insurance products and advice are offered through BMO Nesbitt Burns Financial Services Inc. by licensed life insurance agents, and, in Quebec, by financial security advisors. The comments included in the publication are not intended to be a definitive analysis of tax law: The comments contained herein are general in nature and professional advice regarding an individual’s particular tax position should be attained in respect of any person’s specific circumstances.

Member-Canadian Investor Protection Fund and Member of the Investment Industry Regulatory Organization of Canada

Technical analysis also uses complex mathematical tools in

making investment decisions.

In conjunction with charts, analysts also calculate technical

indicators which are used to identify the “trend”. The technical

indicators are all calculated off of the charts and include;

Moving Averages, MACD, Oscillators, Short and Long-Term

Momentum as well as Relative Strength.

Summation

Unlike fundamentalists, technicians do not care whether or not

a stock is properly valued.

Instead they only care about the underlying supply/demand

relationship of the security being analyzed. If supply is in

control, the price of the security should drop and if demand

is in control the price should rise. They start by collecting

price and volume data. They construct various charts and use

a variety of technical indicators in an attempt to identify the

“trend” and patterns in order to predict future performance.

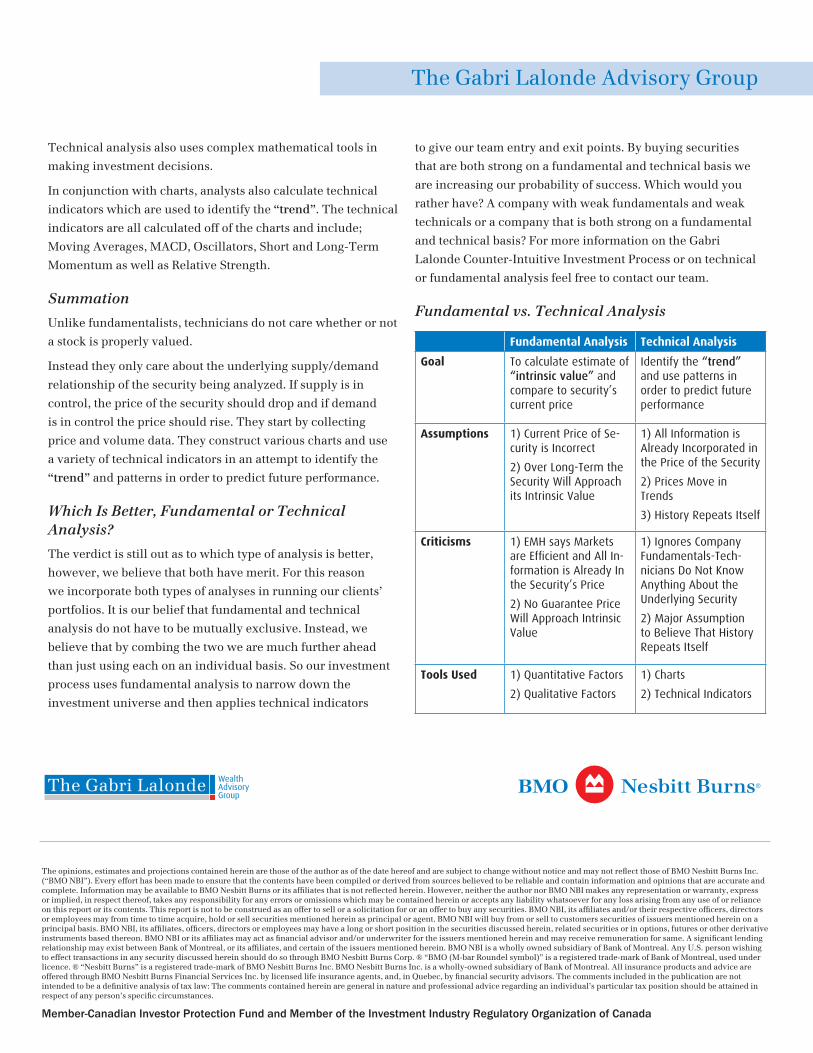

Which Is Better, Fundamental or Technical Analysis?

The verdict is still out as to which type of analysis is better,

however, we believe that both have merit. For this reason

we incorporate both types of analyses in running our clients’

portfolios. It is our belief that fundamental and technical

analysis do not have to be mutually exclusive. Instead, we

believe that by combing the two we are much further ahead

than just using each on an individual basis. So our investment

process uses fundamental analysis to narrow down the

investment universe and then applies technical indicators

to give our team entry and exit points. By buying securities

that are both strong on a fundamental and technical basis we

are increasing our probability of success. Which would you

rather have? A company with weak fundamentals and weak

technicals or a company that is both strong on a fundamental

and technical basis? For more information on the Gabri

Lalonde Counter-Intuitive Investment Process or on technical

or fundamental analysis feel free to contact our team.

Fundamental vs. Technical Analysis

Fundamental Analysis Technical Analysis

Goal To calculate estimate of “intrinsic value” and compare to security’s current price

Identify the “trend” and use patterns in order to predict future performance

Assumptions 1) Current Price of Se-curity is Incorrect

2) Over Long-Term the Security Will Approach its Intrinsic Value

1) All Information is Already Incorporated in the Price of the Security

2) Prices Move in Trends

3) History Repeats Itself

Criticisms 1) EMH says Markets are Efficient and All In-formation is Already In the Security’s Price

2) No Guarantee Price Will Approach Intrinsic Value

1) Ignores Company Fundamentals-Tech-nicians Do Not Know Anything About the Underlying Security

2) Major Assumption to Believe That History Repeats Itself

Tools Used 1) Quantitative Factors

2) Qualitative Factors

1) Charts

2) Technical Indicators

The Gabri Lalonde Advisory Group

The Gabri Lalonde Wealth AdvisoryGroup