Naval & Maritime Markets A Global & APAC Perspective

2011

Table of Contents

Global &

APAC

Naval &

Recession Analysis

Sectors for Growth in Defence

. 2 .

Naval &

Maritime

OutlookAPAC Overview

Conclusions and Recommendations

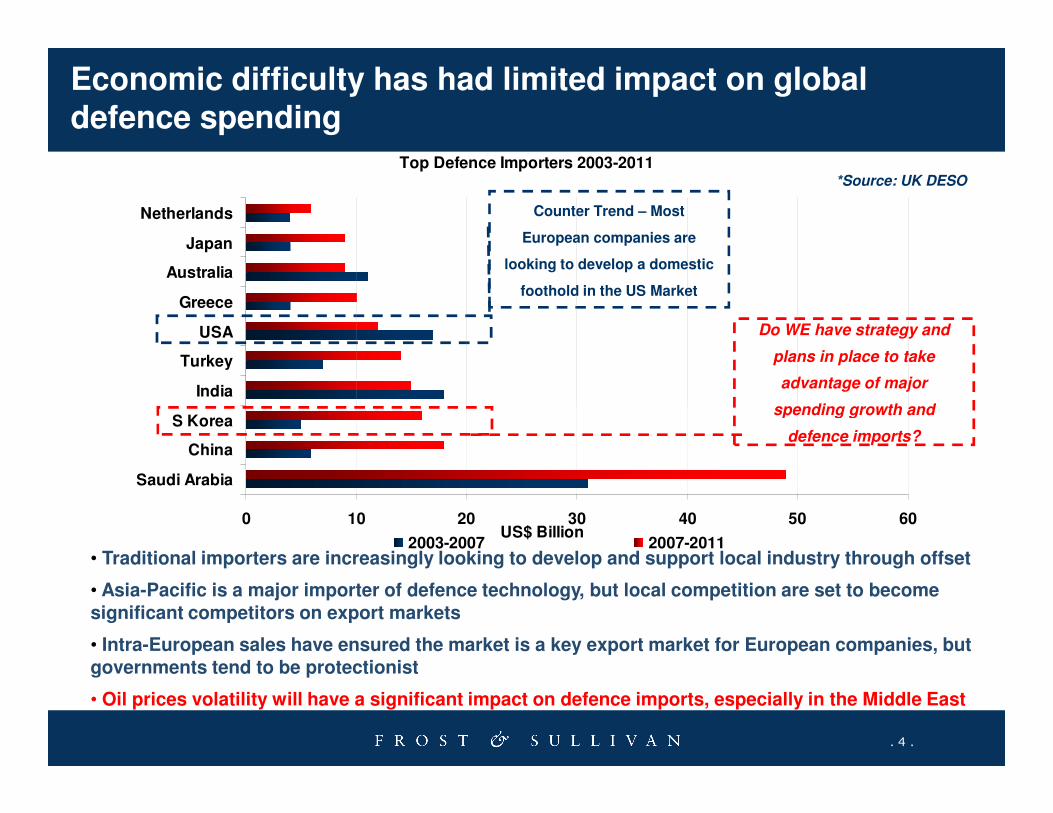

Economic difficulty has had limited impact on global defence spending – other factors have greater influence

Defence Budgets (Global), 2007-2016

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Bil

lio

n $

US$1.4 Trillion

21%

7%

3%

US$1.65

Trillion

30%

10%

4%

. 3 .

Global Defence Spending is expected to continue to grow at a steady rate over the next decade, with major growth centred in the Asia-Pacific region, much of which as a result of China’s incredible rise in spending

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

NORTH AMERICA EUROPE ASIA PACIFIC MIDDLE EAST ROW

2007

46%

23%

2016

34%

22%

2009-2012

Strong Growth Driven by Afghanistan & Iraq conflict

Significant spend on UORs

Market unpredictable and driven by events

2013-2016

Market stabilises as forces begin withdrawing from Afghanistan (such as Canada and The Netherlands)

Market increasingly driven by Asia-Pac

Unclear how futureUS-PRC rivalry will impact

Economic difficulty has had limited impact on global defence spending

*Source: UK DESOTop Defence Importers 2003-2011

India

Turkey

USA

Greece

Australia

Japan

Netherlands Counter Trend – Most

European companies are

looking to develop a domestic

foothold in the US Market

Do WE have strategy and

plans in place to take

advantage of major

spending growth and

. 4 .

• Traditional importers are increasingly looking to develop and support local industry through offset

• Asia-Pacific is a major importer of defence technology, but local competition are set to become significant competitors on export markets

• Intra-European sales have ensured the market is a key export market for European companies, but governments tend to be protectionist

• Oil prices volatility will have a significant impact on defence imports, especially in the Middle East

0 10 20 30 40 50 60

Saudi Arabia

China

S Korea

US$ Billion2003-2007 2007-2011

spending growth and

defence imports?

Growth in Global Defence Spending is largely driven by growth in APAC, including China & South Asia

Top 20 Defence Budgets (excluding USA), 2008 vs 2018

0

50

100

150

200

250

300

CH

INA

UK

RU

SS

IA

FR

AN

CE

JA

PA

N

GE

RM

AN

Y

SA

UD

I AR

AB

IA

SO

UT

H K

OR

EA

IND

IA

ITA

LY

AU

ST

RA

LIA

SP

AIN

BR

AZ

IL

TU

RK

EY

CA

NA

DA

ISR

AE

L

NE

TH

ER

LA

ND

S

IND

ON

ES

IA

TA

IWA

N

GR

EE

CE

Billio

n $

2008 2018

US$1.4 Trillion US$1.65

Trillion

4%

3.4%

2.5%

2.9%

3.7%

2%

2.5%

1.8%

2.9%

1.6%

1.5%

. 5 .

Strong budgetary growth in markets like South Korea, India, Brazil and Turkey highlight where business opportunities will emerge and continue to drive and support the wider market growth

CH

INA

UK

RU

SS

IA

FR

AN

CE

JA

PA

N

GE

RM

AN

Y

SA

UD

I AR

AB

IA

SO

UT

H K

OR

EA

IND

IA

ITA

LY

AU

ST

RA

LIA

SP

AIN

BR

AZ

IL

TU

RK

EY

CA

NA

DA

ISR

AE

L

NE

TH

ER

LA

ND

S

IND

ON

ES

IA

TA

IWA

N

GR

EE

CE

2009 2018

10%

17%4.6%

4.1%

4.6%

4.3%

4.5%

4%

3.6%3.1%2.9%

CHINA UK RUSSIA FRANCE JAPANGERMANY SAUDI ARABIA SOUTH KOREA INDIA ITALY

Key Issues Impacting Industry Today

• Top line growth facing headwinds, Commercial aerospace and Defense cycles

peaking

• Change of US administration and shifting defense procurement priorities across

US and NATO

• Asian growth drives need for exposure across entire industry

• PMA and MRO models evolving

. 6 .

• Increasing industry consolidation, European firms building presence in US

defense market, Asian firms expanding globally

• Maintaining earnings growth as cycles slow, managing costs and margins

• Effective position in homeland security market to maximize opportunities

Sectors for Growth in Defence Markets

. 7 .

Sectors for Growth in Defence Markets

Defence Electronics Market worth cumulative US$ 314 Billion over the next decade

US$ 27 Billion US$ 35 BillionMarket Revenues by Segment (Global), 2007-2016

0

5000

10000

15000

20000

25000

30000

35000

40000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Millio

n $

17%

10%

8%

5%

10%

8%

16%

8%

5%

. 8 .

Major growth opportunities exist in C2, Communications and UAS segments

2007 2016

C2 Land Communications Land ISR Air ISR UAS Air T&S Land T&S

25%

25%

11%

12%

14%

8%5%

25%

23%

12%

25%

29%

Despite widespread procurement of new air platforms over the next decade, the total number of platforms in service will reduce significantly. Legacy systems will not be replaced on a 1 to 1 basis

Military Aircraft Procurement by Region (2008-2012)

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012

13%

30%

15%6%

1%

11%

11%

1%7% 1% 4%

Boeing Lockheed Martin Eurofighter Gmbh Dassault

SAAB Sukhoi EADS Alenia

BAE Systems Pilatus KAI

Aircraft Market Share by Company, 2008-2012 Lockheed will

continue to

dominate, but

consolidation

is a key

dynamic

. 9 .

Reducing numbers of air platforms combined with higher-tempo operations highlights the importance of through-life management of defence platforms

Air Platform Inventory (Europe), 2008-2017

0

2000

4000

6000

8000

10000

12000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Un

its

F/A F/W Other Rotary

10652

Air Platforms

9234

Air Platforms

Europe North-America Middle East Asia-Pacific

4000000

6000000

8000000

10000000

9, 449, 400 Personnel

8, 943, 998 PersonnelAsia-Pacific

A trend towards increased

professionalism in major

modernising Asia-Pacific

nations will see a strong

decrease in force numbers in

order to increase spend on

equipment.

Middle East

Middle-Eastern states will

generally be increasing in

size in response to significant

geo-political threats in the

region. Israel is an exception

in that it is expected to

reduce in size.

- +

Soldier Modernisation programmes and increasing use of electronics equipment could offer significant revenue potential in the form of support contracts and through life capability management

. 10 .

Top spenders on defence are reducing their force numbers to enable higher spend on equipment programmes, whilst a trend towards increased professionalism has meant a downturn in

conscription levels in developing countries

2000000

4000000

2008 2017

2007 2016

USA CHINA UK RUSSIA FRANCE JAPAN GERMANY

SAUDI ARABIA SOUTH KOREA INDIA ITALY AUSTRALIA SPAIN BRAZIL

TURKEY CANADA ISRAEL NETHERLANDS INDONESIA TAIWAN

Europe

European Countries are

tending to downsize their

militaries as part of plans to

modernise the force structure

and take advantage of next

generation technology and

outsourcing opportunities to

save money and maintain or

increase capability

North America

Both the US and Canada are

looking to significantly

increase the number of

military personnel they have

in response to shortages

observed as a result of high

operational commitments.

Spending per Soldier ratio

will likely suffer, however.

Continued Penetration of Tactical communications into lower force echelons will see the market grow at a rapid rate

Global Tactical Communications Unit Breakdown

600,000

700,000

800,000

900,000

1,000,000

Tactical Communications Installed Base, 2005

48%

17%

30%

2% 3%

2000

. 11 .

-

100,000

200,000

300,000

400,000

500,000

2005 2020

Un

its

Europe North America Latin America Africa M.East Asia Pac

Tactical Communications Installed Base, 2020

19%

15%

25%

36%

2% 3%

Vehicular Manpack Handheld Soldier Radio Airborne LOS Comms

2000

Global Unmanned Aerial Systems Market

US$2.8 Billion US$5.5 BillionUAS Market Revenues (Global), 2007-2016

0

1000

2000

3000

4000

5000

6000M

illio

n $

22%

21%

18%

. 12 .

Experience on operations will enable significant growth in the UAS market, with total spend of US$44.5 Billion over the next 10 years

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US Europe Asia-Pac

2007 2016

61%21%

18%

62%

16%

61%

Key hot-topics in Defence

Unmanned

Systems

Unmanned

Systems

Weapons

Systems

Ground

Ships

• Increased focus on unmanned systems capabilities and less focus on the platform (Sensors, Data Links, Navigation, GCSs)

• Companies are looking to expand their Unmanned Systems product offerings through partnering and acquisition

• The UAS industry in the U.S. is increasingly becoming consolidated with approximately 80 percent of the market held by four

companies

• Significant budget resources will be allocated to upgrade programs for fire control systems

• Missiles will have improvements to the seeker and control technology and will have “re-pours” or new propulsion packages

procured

• Army vehicle reset is having a profound impact on the U.S. Defense vehicle industry for both manufacturers and suppliers

• Despite being on the chopping block for the last two years, programs such as the Navy’s Littoral Combat Ship (LCS) will have some

support from President Obama in 2009 and beyond

• It is expected however that the U.S. Navy’s acquisition system will change and this will have an impact on not only ship programs

but other naval acquisitions programs as well

. 13 .

Ground

Vehicles

Military

MRO

Training

Simulation

• Army vehicle reset is having a profound impact on the U.S. Defense vehicle industry for both manufacturers and suppliers

• Reset and refurbishment will positively impact vehicle procurement for the next 3-5 years

• The Joint Light Tactical Vehicle program could face setbacks however since the U.S. Army is consistently placing orders for new

HMMWVs

• Parts Manufacturing Authority (PMA) parts manufacturers are increasingly be challenged by original equipment manufacturers in

the military aircraft MRO space

• High aircraft engine cost in an emerging challenge for the military aircraft MRO market

• The aging military aircraft fleet however is increasing the potential for MRO revenue over the next 5-10 years

• Budget constraints and an inability to sustain funding sources for T&S programs has been restraining the market

• As resources are pulled to support ongoing conflicts in Iraq and Afghanistan, training and simulation has become less of a priority

• The growth in popularity of unmanned systems is helping to spur T&S for this market area, particularly in the UAS market segment

C4ISR

• Reequipping and expanding the ground forces and SOF will be key in 2009

• Technology focuses will be on communications, Intelligence, and Surveillance

• Possible funding shifts from the AF and the Navy to help rebuild the Army and the USMC

• Programs facing cutbacks in 2009 and beyond: FCS, TSAT, JTRS, and Manned Airborne ISR

Defence Budgets in selected Asia / Pacific Markets, 2009-2014

40

60

80

100

120

Billio

n U

S$

Asia/Pacific: Defence Budget Trends

US$ 75.86

Billion

US$ 103.54

Billion

. 14 .

0

20

2009 2010 2011 2012 2013 2014

Australia India S Korea Malaysia Pakistan Singapore

Asia/Pacific: Spending ratios 2010-2014

13%

34%

32%

6%

7%8%

The region is dominated by large-budget countries

such as India, South Korea and Australia

Even smaller

countries in the

region will

contribute to the

strong expected

growth

2009 2014

Solid growth in the Indian defence

budget – from $22 Billion to $36 Billion

from 2007-2014

. 15 .

. 16 .

. 17 .

. 18 .

Asia Pacific Maritime Security Market Assessment

. 20 .

. 21 .

. 22 .

. 23 .

. 24 .

. 25 .

Conclusions and Recommendations

. 26 .

Conclusions and Recommendations

The global recession will have an impact on defence, but other factors are likely to be more influential to the way the market will develop

1. The economic recession had less impact on security and defence markets

2.This is particularly the case in defence where budgets are committed to long-term programmes. However, there

are potential problems emerging:

• Introduction of new competitive forces to the market – If a country is reliant on IMF bailouts, defence

programmes are likely to be delayed significantly

• Long-term contradictions within under-funded defence equipment plans are presenting acute

problems in highly active military forces

• Wider economic slowdown and resulting fall in GDP will be a limiting factor on defence allocations

and potentially on wider related defence programme opportunities

. 27 .

• Prime contractors will have to consolidate their supply chains in critical areas to reduce the risk of a

key supplier failing

3. To overcome these challenges, and disrupt the opposition, it is more important than ever to:

• Look to expand in emerging markets such as India –Asia-Pacific will continue to grow at a relatively

high level

• Focus on after-market opportunities to access sustained revenue streams through PLC support

• Manage and look after the supply chain

• Match customer needs with innovative business models and solutions

After-market support and services are an attractive long-term recurring revenue stream to be addressed across the

defence market and limit the impact of delayed procurement

Speaker’s Details

Thank You

. 28 .

Ratan ShrivastavaDirector, Aerospace & Defence Practice

Hand Phone (Singapore) . +65 9175 1640

Hand Phone (India) Tel. + 91 98105 84849

Email: [email protected]

For Additional Information

Donna Jeremiah

Director

Corporate Communications

(603) 6204 5832

Carrie Low

Executive

Corporate Communications

(603)6204 5910

. 29 .

Jessie Loh

Manager

Corporate Communications

(65) 6890 0942