1

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurship and Venture Capital Entrepreneurship and Venture Capital

Jerome S. EngelAdjunct Professor, Haas School of Business

Executive Director, Lester Center For Entrepreneurship and Innovation University of California at Berkeley

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Jerry Engel

• UC Berkeley– Founder and Executive Director of the Lester Center

for Entrepreneurship and Innovation– Chair: Entrepreneurship Faculty– Teach Entrepreneurship, Venture Capital & Private Equity,

Technology Commercialization in the MBA and Executive Ed• Outside of Academe:

– Venture Capital• Monitor Venture Partners, General Partner• Co-founded: Kline Hawkes Capital early ’90s

– Entrepreneur• Co-Founder: AllBusiness.com, ElectraScan Inc., CardioProfile• Angel Investor, Board member, Advisor: Maxis, Leapfrog, MedAmerica

– Big Company Experience• 1980s: Ernst & Young, Managing Partner, Entrepreneurial Services

» Clients: Apple, Intel, Genentech, Sun, Autodesk,Fair Isaac, The Learning Company and more..

• 1970s: KPMG

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurship and Venture Capital

• What are the Drivers of Innovation?• Why are Entrepreneurship and Venture Capital

Important?• What is Entrepreneurship?• How Does Venture Capital Work• What are the current trends?• What does all this mean to me?

2

Drivers of Innovation in the US

High Tech Model

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

U.S. Example:Private R&D Spending Increasing

0

50

100

150

200

250

300

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Bill

ions

of 1

996

Dol

lar

TOTAL

PRIVATE

FEDERAL

Note: Expenditures are deflated using the GDP implicit price deflator.Source: National Science Board (2000) and Economic Report of the President (2002)

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

The Proportion of Research Expenditure atOur Largest Corporations is Decreasing

Company Size 1981 1989 1999 2000

<1000 employees 4.4% 9.2% 22.5% 22.4%1,000 - 4,999 6.1% 7.6% 13.6% 15.4%5,000 - 9,999 5.8% 5.5% 9.0% 8.4%10,000 - 24,999 13.1% 10.0% 13.6% 14.4%25,000+ 70.7% 67.7% 41.3% 39.5%

Original - H. Chesbrough, 2003 Updated J. Engel 2003Source: National Science Foundation, Science Resource Studies, Survey of Industrial Research Development, 1991,1999 and 2000.

3

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

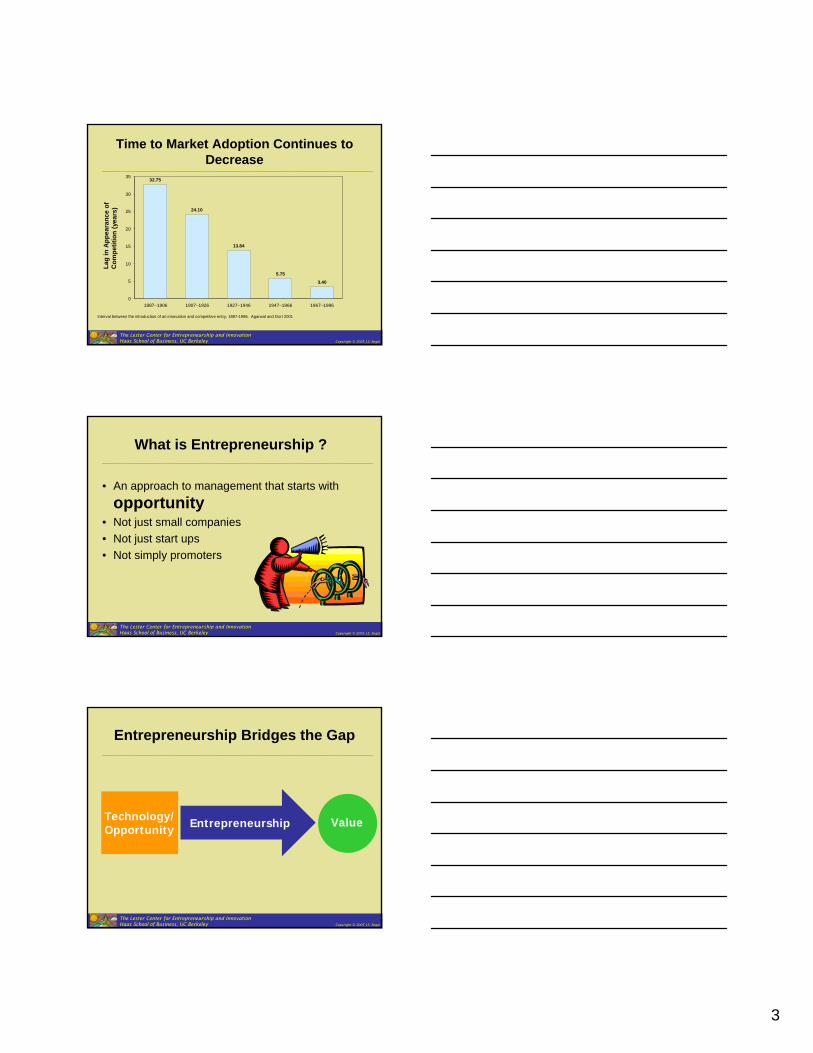

Time to Market Adoption Continues to Decrease

32.75

24.10

13.84

5.75

3.40

0

5

10

15

20

25

30

35

1887–1906 1907–1926 1927–1946 1947–1966 1967–1986

Lag

in A

ppea

ran c

e of

C

ompe

t itio

n ( y

ears

)

Interval between the introduction of an innovation and competitive entry, 1887-1986. Agarwal and Gort 2001

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

What is Entrepreneurship ?

• An approach to management that starts with opportunity

• Not just small companies• Not just start ups• Not simply promoters

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurship Bridges the Gap

Technology/Opportunity

ValueEntrepreneurship

4

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurship is:

A processNot a person

About BIG companies that happen to be smallNot about small business

Important to BIG business

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurship

The pursuit of Opportunity beyond the Resources you currently control

Prof. Howard StevensonWorking Definition

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurial Process

• Identify– Need– Solution– ‘Unfair Advantage’

• Acquire– Technology rights– People– Money

Resources

Opportunity

5

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

The Entrepreneur’s Task….

• Key Resources– Technology– Money– People

People

MoneyTechnology

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Major Trends……

• Technology– Discoveries of large companies and universities

commercialized by small companies• Money

– From Venture Capitalists: new structures for pooling risk-tolerant investors

• People– The rise of the professional entrepreneur and

entrepreneurial teams as a management process

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurial Process

• Key Mechanisms:

– Mobile Technology

– Mobile People

– Mobile Money

People

MoneyTechnology

6

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurial Process

• Mobile Technology– Transfer of

technology from research institutions to commercial application

• Formal - through licensing

• Informal - through people

People

MoneyTechnology

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurial Process

• Mobile People– The emergence of

the “professional”entrepreneurial management team

• Lifestyle: personal mobility, multiple employers

• Equity compensation• Acceptance of the

risk of failure

People

MoneyTechnology

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

Entrepreneurial Process

• Mobile Money– New forms of Private

Equity• International

investments by US Venture Capital

• Multinational corporations become more active

• Buy-out funds becoming more active

• Increased sophistication of the Angel communities

People

MoneyTechnology

7

Liquidity Cycle in Venture Capital

CompanyCompanyliquidityliquidityeventsevents

VCVCinvestmentsinvestments

in companiesin companies

CompanyCompanygrowthgrowth

LPLPinvestmentinvestment

in VCin VC

VCVCinvestmentsinvestmentsin companiesin companies

VC: A Cyclical IndustryUS Fundraising

Fund

s Ra

ised

($B

)

$11.5

$24.5

$18.3

$9.4$13.1

$49.8

$83.5

$57.6

$26.7

$17.0$12.7

$0

$20

$40

$60

$80

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 1H06

Am

ount

Inv e

s ted

($ B

) Num

ber of Deals

Investment Levels Reflect the Same Cycle

Deal Flow and Equity into Venture-Backed Companies

Source: Dow Jones VentureOne/Ernst &Young

$9.2$13.1

$17.9

$49.5

$94.8

$36.4

$22.1 $19.5 $22.2 $23.4

$13.0

19122211

2547

4590

6333

3280

24022193 2293 2351

1213

$0

$25

$50

$75

$100

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 1H06

0

1,000

2,000

3,000

4,000

5,000

6,000

Amount Invested ($B) Number of Deals

8

VC InvestmentVC Investment1980 1980 –– 2006 The Long View2006 The Long View

($ in billions)

$41.0

$13.0$22.2

$8.2

$21.3

$4.2$3.7

$23.4$19.5$21.5

$54.7

$105.9

$14.9$11.5

$3.6$2.2$2.8$3.3$3.4$3.3$3.1$2.8$3.0$3.0$1.6$1.2$0.6$0

$20

$40

$60

$80

$100

$120

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 1H'06

Annual Venture Capital Investments 1980 to YTD 1H 2006

U.S. Investment: Overall

IT Leads Deal AllocationDeal Flow Allocation by Industry Sector

0%

20%

40%

60%

80%

100%

3Q03 1Q04 3Q04 1Q05 3Q05 1Q06 3Q06

Other

Business,Consumer,Retail

IT

Healthcare% o

f To

t al V

C Ro

und s

24%

62%

12%

27%

16%

26%

60%

9%

65%

5%

13%

2%

Source: Dow Jones VentureOne/Ernst &Young

5%

9

IT Dollars Pick Up in 3Q’06Investment Allocation by Industry Sector

0%

20%

40%

60%

80%

100%

3Q03 1Q04 3Q04 1Q05 3Q05 1Q06 3Q06

Other

Business,Consumer,Retail

IT

Healthcare

% o

f D

olla

r s In

vest

e d

36%

53%

16%

32%

54%

12%

16%6%

62%

4%

36%

10%1%

9%

Source: Dow Jones VentureOne/Ernst &Young

Investment in IT Companies Stable in 3Q’06Equity Investment in Information Technology Companies

$3.6$3.6

$3.7$3.2$3.4$3.5$3.2$3.2

$2.9

$3.6

$3.1$3.1

$2.6

365387

363384

356369351

383

326

392

350364327

$0

$1

$2

$3

$4

3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q060

100

200

300

400

Amount Invested ($B) Number of Deals

Am

ount

Inv e

s ted

($ B

)

Num

ber of Deals

Source: Dow Jones VentureOne/Ernst &Young

Software Garners Most IT InvestmentIT Investment Allocation by Sector

0%

20%

40%

60%

80%

100%

3Q03 1Q04 3Q04 1Q05 3Q05 1Q06 3Q06

Semiconductors

InformationServices

Electronics

Communications

Software% o

f D

o lla

rs I n

vest

e d

37%

26%

12%

15%

10%

41%

24%

14%

9%

12%

18%

12%

31%

48%

19%

Source: Dow Jones VentureOne/Ernst &Young

10

Bay Area Draws Most Investment DollarsRegional Investment in the United States 3Q’06

Potomac4%

Research Triangle

2%

All Other US19%

Washington State3%

Texas5%

New York Metro8% New England

10%

Southern California

11%

Bay Area 38%

Source: Dow Jones VentureOne/Ernst &Young

45% of Deals in California CompaniesRegional Deal Flow in the United States 3Q’06

Bay Area 35%

New England11%

Southern California

10%

Texas5%

New York Metro7%

Potomac4%

Washington State3%

All Other US24%

Research Triangle

1%

Source: Dow Jones VentureOne/Ernst &Young

European Investment: Overview

11

Perspective on European MarketEquity Investment in Venture-Backed Companies, US vs. Europe ($)

Overall Investment

3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06$0

$1

$2

$3

$4

$5

$6

$7

European Equity Investment

U.S. Equity Investment

Am

ount

Inv e

s ted

($ B

)

Source: Dow Jones VentureOne/Ernst &Young

Biopharm Leads InvestingEquity Investment in European Venture-Backed Companies by Industry, 3Q‘06

Media2%

Biopharmaceuticals36%

Medical Devices7%

Healthcare Services0.3%

Communications12%

Medical IS1%

Products1%Services

1%

Retail1%

Software14%

Semiconductors15%

Information Services6%

Electronics4%

Info. Tech.51%

Bus. Cons. Retail

9%Healthcare

44%

Source: Dow Jones VentureOne/Ernst &Young

UK & France Garner Over Half of Deal FlowTotal Deals in Europe by Country, 3Q’06

United Kingdom 30%

France23%

Sweden12%

Germany9%

Denmark6%

Switzerland3%

Ireland2%

Other15%

Source: Dow Jones VentureOne/Ernst &Young

12

Valuation of the Venture Capital Funded Venture

U.S. Investment: Valuations

This section will be updated in December.

Valuations Continue Upward TrendMedian Premoney Valuation by Year

$9.3$11.1

$13.0

$15.5

$21.0

$25.2

$16.0

$10.7 $10.0

$13.0$15.0

$20.0

$0

$5

$10

$15

$20

$25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 1H06

Med

i an

Pre m

o ne y

Val

u ati

on (

$M)

13

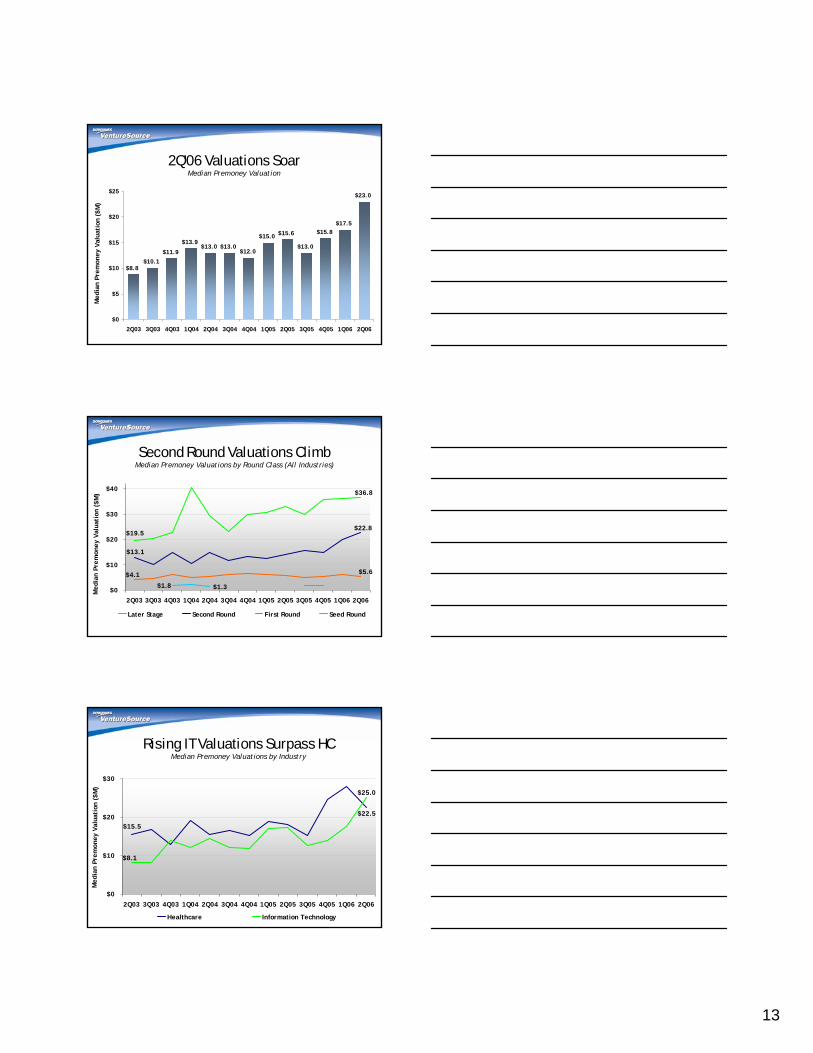

2Q’06 Valuations SoarMedian Premoney Valuation

$8.8$10.1

$11.9

$13.9$13.0 $13.0

$12.0

$15.0 $15.6

$13.0

$15.8$17.5

$23.0

$0

$5

$10

$15

$20

$25

2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06

Med

i an

Pre m

o ne y

Val

u ati

on (

$M)

Second Round Valuations ClimbMedian Premoney Valuations by Round Class (All Industries)

$1.3

$36.8

$19.5$22.8

$13.1

$5.6$4.1

$1.8$0

$10

$20

$30

$40

2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06

Later Stage Second Round First Round Seed Round

Med

i an

Pre m

o ne y

Val

u ati

on (

$M)

Rising IT Valuations Surpass HCMedian Premoney Valuations by Industry

$22.5

$15.5

$25.0

$8.1

$0

$10

$20

$30

2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06

Healthcare Information Technology

Med

i an

Pre m

o ne y

Val

u ati

on (

$M)

14

U.S. Liquidity

M&As Remain Primary Exit OptionPercentage Breakdown of Venture Backed Liquidity Events: IPO vs. M&A

0% 20% 40% 60% 80% 100%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

YTD06*

IPOs M&AsYTD06*: 1Q06 – 3Q06

The Lester Center for Entrepreneurship and InnovationHaas School of Business, UC Berkeley Copyright © 2005 J.S. Engel

What are the Trends we have Observed?• Venture Capital is a very special and unique

category of PE• It is highly concentrated in a few unique

locations and industries• Cyclicality and uncertainty are key factors • There are surprising consistencies given these

factors• UC Berkeley, right here, right now – is a unique

and great place to study VC!

15

Thank You