Earnings Presentation

First Quarter 2012

May 2012

Source: Cencosud and AC NielsenNote: Revenue and Adjusted EBITDA breakdown exclude Other Businesses1 As of March 17, 20122 EBITDA, further adjusted to exclude the effect of exchange differences, increase on revaluation of investment properties, results from price level restatement and negative goodwill associated with Johnson’s acquisition3 Last twelve months ended March 2012

Company overview

Supermarkets

Home Improvement

Department Stores

Financial Services

Shopping Centers

� 726 stores across 4 countries

� 81 stores in Argentina, Colombia and Chile

� 74 stores in Chile

� 25 shopping centers in Argentina, Chile and Peru

� USD 1.5 bn consumer loans outstanding

2

Supermarkets74%

Home Improvement

12%

Shopping Centers

2%

Financial Services

3%Department Stores

9%

Revenue Breakdown (LTM 3) Adjusted EBITDA 2 Breakdown (LTM 3)

Total: US$16,456 mm

Department Stores

6%

Shopping Centers

14%

Financial Services

13%

Home Improvement

12%

Supermarkets56%

Total: US$1,310 mm

Number of stores: 906

Selling space: 3,3 million sq2

Number of customers: 800mm

Number of employees: 139,082

Credit cards issued: 4.3mm

Market capitalization1: US$12,5 bn

Key metrics (LTM 2012 1)

Revenues evolution (US$bn)

Revenues and EBITDA continue their positive evoluti on

Source: CencosudNote: Figures in IFRS; CAGRs calculated in local currency assuming CLP per USD exchange rates of 507, 468, 479 and 487, 519 for end of period 2009, 2010, 2011, 1Q2011 and

1Q2012, respectively; Figures in IFRS

3

9,912,2

15,6

3,6 4,4

2009 2010 2011 1Q 2011 1Q 2012

Adjusted EBITDA (US$mm) and margin (%)

377

747

1,187

208 298

2009 2010 2011 1Q 2011 1Q 2012

Capex (US$ mm) excl. acquisitions

+26%

CAGR

+80%

CAGR

+23%

+46%

+35%

CAGR+5%

…balance sheet flexibility and solid operational pe rformance haveallowed the company to maintain sustainable credit ratios

2,7 2,7 3,13,6

2009 2010 2011 1Q 2012

Net debt / Adjusted EBITDA

57% 53%72% 80%

2009 2010 2011 1Q 2012

3.6

7.7 7.0

4.5

2009 2010 2011 1Q 2012

Financial debt / EquityAdjusted EBITDA / Net interest expenses

4

Source: CencosudNote: Figures in IFRS; Ratios calculated in local currency assuming CLP per USD exchange rates of 507, 468, 519 and 487 for end of period 2009, 2010, 2011 and 1Q2012

Net debt evolution (US$bn)

2,03,1 3,7

4,7

2009 2010 2011 1Q 2012

� Duration of debt is 6 years at March 2012

� 28% of Cencosud’s debt is USD denominated, however, after cross currency swaps the exchange rate risk reduce to 9%

� The remaining is primarily UF and CLP denominated d ebt, matching the strong Chilean component in the E BITDA generation

Investment Highlights

Financial performance

First Quarter ResultsFirst Quarter Results

452606

777

193172

2009 2010 2011 1Q 2011 1Q 2012

Geographical presence and market position

Revenues evolution (US$bn) Adjusted EBITDA evolution (US$mm)

Source: Cencosud, Public filings, Planet Retail, ABRAS, INDECNote: Figures in IFRS; Growth rates calculated in local currency; figures converted to USD at exchange rates of 507, 468, 519, 479 and 487 for end of period 2009, 2010, 2011, 1Q2011 and 1Q2012, respectively; Market share in terms of net revenues, as of 2011; Chile and Peru figures as of September 2011; Peru market share estimated based solely on reported sales from the three main competitors

SSS evolution by country in local currency

Supermarkets: The impact of Prezunic

6

3,32,6

11,58,87,2

2009 2010 2011 1Q 2011 1Q 2012

+26%

+13%

2% 6% 5%

5%7%

(1%)

7%

1%

5%3%

11%

25%

23%24%

22%

(3%) (2%)

7%

2%

9%

2009 2010 2011 1Q 2011 1Q 2012

Chile Brazil Argentina Peru

CAGR

272 stores

189 storesNorth East Region (34%) #2State of Minas Gerais (23%) #1Rio de Janeiro (13%) #3

726 stores726 stores

#1

191 stores

#2

74 stores

#1

+25%

+31%

CAGR

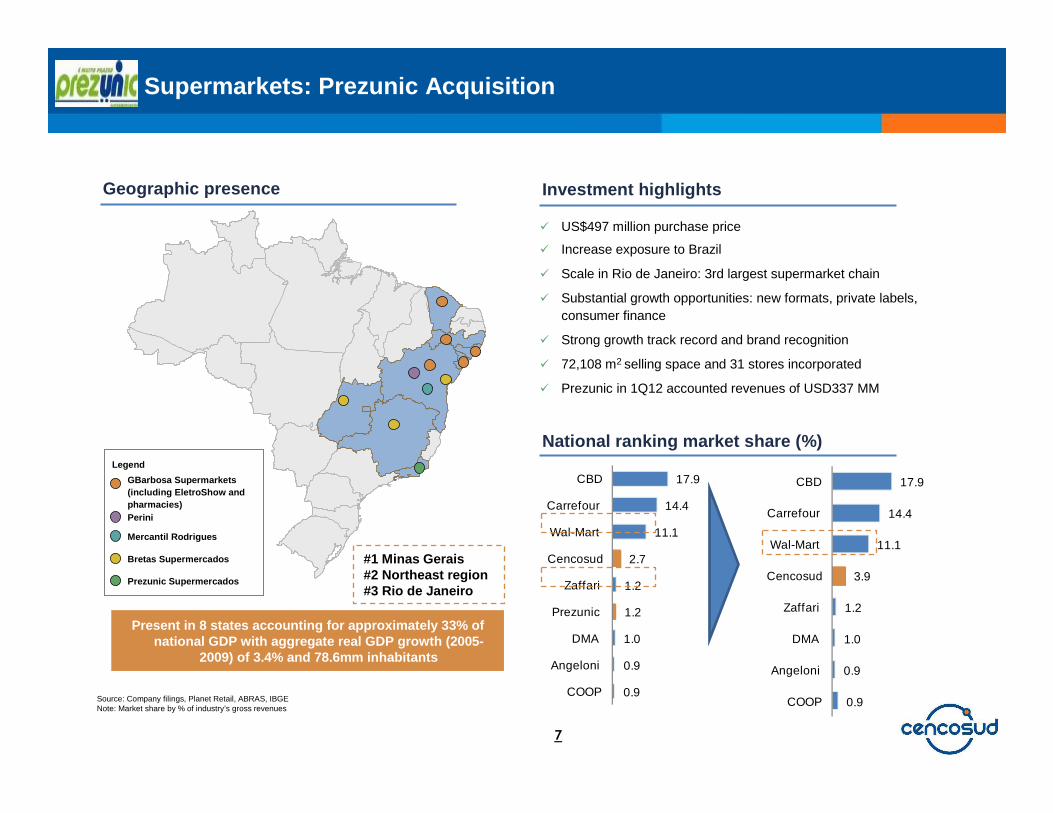

� US$497 million purchase price

� Increase exposure to Brazil

� Scale in Rio de Janeiro: 3rd largest supermarket chain

� Substantial growth opportunities: new formats, private labels, consumer finance

� Strong growth track record and brand recognition

� 72,108 m2 selling space and 31 stores incorporated

� Prezunic in 1Q12 accounted revenues of USD337 MM

17.9

14.4

11.1

2.7

1.2

1.2

1.0

0.9

0.9

CBD

Carrefour

Wal-Mart

Cencosud

Zaffari

Prezunic

DMA

Angeloni

COOP

Supermarkets: Prezunic Acquisition

Geographic presence

7

National ranking market share (%)

Source: Company filings, Planet Retail, ABRAS, IBGENote: Market share by % of industry’s gross revenues

GBarbosa Supermarkets (including EletroShow and pharmacies)Perini

Legend

Mercantil Rodrigues

Bretas Supermercados

Prezunic Supermercados

#1 Minas Gerais#2 Northeast region#3 Rio de Janeiro

17.9

14.4

11.1

3.9

1.2

1.0

0.9

0.9

CBD

Carrefour

Wal-Mart

Cencosud

Zaffari

DMA

Angeloni

COOP

Investment highlights

Present in 8 states accounting for approximately 33 % of national GDP with aggregate real GDP growth (2005-

2009) of 3.4% and 78.6mm inhabitants

1,258 1,356 1,460 1,552 1,476 1,338 1,361 1,412 1,469 1,496 1,431 1,547 1,797 1,942 2,127

83 116 124

333 458

2007 2008 2009 2010 2011 2007 2008 2009 2010 2011 2007 2008 2009 2010 2011 2007 2008 2009 2010 2011

9.1 12.3 13.0 16.5 17.3

7.7 9.8 10.4 13.3 15.4 7.7 9.2 9.8 12.6 14.4

0.2 1.1 1.1 1.7

4.2

2007 2008 2009 2010 2011 2007 2008 2009 2010 2011 2007 2008 2009 2010 2011 2007 2008 2009 2010 2011

Cencosud Brazil Carrefour Brazil CBD Food Walmart Brazil

CAGR 17%CAGR 19% CAGR 17%

Date Target Acquirer Amount (US$mm) EV/sales

Apr-07 Atacadao Carrefour 1,087 0.6x

Nov-07 Assaí CBD 197 0.4x

Nov-07 GBarbosa Cencosud 430 0.5x

Mar-10 Super Familia Cencosud 33 0.3x

Apr-10 28 -

Oct-10 Bretas Cencosud 705 0.5x

Jan-12 Prezunic Cencosud 497 0.4x

Median 0.5x

CAGR 118%

CAGR 4%CAGR 3% CAGR 10%

CAGR 53%

Net Revenues (US$bn)

Selling space (‘000s m 2)

Only active and successful consolidator in Brazil 1

Supermarkets: Competitive Landscape in Brazil

8

Source: Company filings, Planet Retail, equity researchNote: Carrefour Brazil figures based on gross revenues; Cencosud figures are pro-forma to Prezunic acquisition; Average FX rate during the respective period used for calculations1 Only considers transactions with deal size of US$25mm and greater

87137

171

46 51

2009 2010 2011 1Q 2011 1Q 2012

2%

24%

5%

11%

3%

(4%)

12%

7%

11%

2%

28%32%

28%30%

2009 2010 2011 1Q 2011 1Q 2012

Chile Colombia Argentina

Geographical presence and market position

Adjusted EBITDA evolution (US$mm)Revenues evolution (US$mm)

29 stores

#2

4 stores

48 stores

#1

81 stores81 stores

SSS evolution by country in local currency

Home Improvement: Remarkable Argentina performance

9

529472

1.9581.613

1.202

2009 2010 2011 1Q 2011 1Q 2012

Source: CencosudNote: Figures in IFRS; Growth rates calculated in local currency; figures converted to USD at exchange rates of 507, 468, 519, 479 and 487 for end of period 2009, 2010, 2011, 1Q2011 and 1Q2012, respectively;

Market position based on net revenues, as of 2011

+28%

CAGR

+40%

CAGR

+12% +11%

Shopping Centers: 2Q12 opening of Costanera

10

Adjusted EBITDA evolution (US$mm)Revenues evolution (US$mm)

140175 206

44 44

2009 2010 2011 1Q 2011 1Q 2012

6761

268230194

2009 2010 2011 1Q 2011 1Q 2012

Source: CencosudNote: Figures in IFRS; Growth rates calculated in local currency; figures converted to USD at exchange rates of 507, 468, 519, 479 and 487 for end of period 2009, 2010, 2011, 1Q2011 and 1Q2012, respectively;

Figures exclude intercompany operations; Market position based on gross leased area, as of 2011

+18%

CAGR

+21%

CAGR

Geographic presence and occupancy rates

#214 Shopping Centers

Gross Leased Area: 228,999 m2

99% occupancy rate

#29 Shopping Centers

Gross Leased Area: 282,693 m2

98% occupancy rate

2 Shopping CentersGross Leased Area: 54,750 m2

95% occupancy rate

25 Shopping Centers25 Shopping Centers

+9%+0,4%

Costanera Center

� Largest multi-purpose commercial complex in Chile

� 335 stores, including Jumbo, Easy and Paris

� Food court, 12 movie theaters, bowling court, medical centers and gym

� Shopping mall opened May 2012 with 150,000 sq GLA

� 2 premium Office Towers and 1 Hotel schedule to open end of 2013

� Costanera Center tower, designed by Cesar Pelli, is the highest building in South America, standing 300 meters tall

� Total capex of USD 1,098 MM

� Mitigation costs are USD 63 MM, of which USD 27 MM are already incurred

10,9%

7,2% 7,6%7,6%10,0%

6,9%7,6%7,6%

2009 2010 2011 1Q 2012

Chile Argentina

8%18%20%

47%

Departmentstores

Homeimprovement

Hypermarkets Supermarkets

8%16%

Home improvement Hyper/Supermarkets

Credit card penetration by division 1Q 2012

Source: CencosudNote: Figures in IFRS; Assumes CLP per USD exchange rates of 507, 468, 519 and 487 for end of period 2009, 2010, 2011 and 1Q2012, respectively

Financial Services: Business Overview

Loan loss allowance as % of all loans

Gross loan portfolio evolution by country (US$mm)

12

770 888 861 862

68

176 243 239838

1.064 1.104 1.101

2009 2010 2011 1Q 2012

Chile Argentina .Chile

Argentina

41%

Hyper/Supermarkets

Brazil

8%

Hyper/Supermarkets

Peru

Market opportunities and strategy

� Ninth largest consumer market in the world: Retail sales of

US$1.1 trillion during 20111

� Demographics capable of supporting Cencosud stores: 100

cities above 250 thousand in population

� Underpenetrated formal retail segment

� Best macroeconomic environment in the last 50 years

� Strong consumption, stable inflation rate and employment growth

� Underpenetrated formal retail market (30% of total spending)

� Growing purchasing power and household spending

� Developed credit markets with access to middle income

consumers

� Underpenetrated market with substantial growth opportunities

� Solid macroeconomic fundamentals

� Sustainable household consumption growth coupled with a

expansionary credit market environment

� Underpenetrated retail market with vast potential

1 Planet Retail13

Market opportunities Strategy

Enhance customer loyalty

Continue to develop and expand our multi-

format and multi-brand approach

Focus on operating margins and cash

flows

Organic expansion in selective markets

Continue to pursue opportunistic

acquisitions while maximizing synergies

Enhance customer loyalty

����

����

����

����

����

����

����

����

����

����

����

����

����

����

����

����

����

��������

����

-1,7%

19,7%

5,2%

17,9%

9,4%

2009 2010 2011 1Q 2011 1Q 2012

2009

Source: CencosudNote: Figures in IFRS; Growth rates calculated in local currency; figures converted to USD at exchange rates of 507, 468, 519, 479 and 487 for end of period 2009, 2010, 2011, 1Q2011, 1Q2012, respectively1 As of December 2011, including 39 Jonhson’s stores

SSS evolution in local currency

Department Stores: Impacted by Johnson’s

35 stores35 stores

Market Share by selling space – Chile 1

14

Adjusted EBITDA evolution (US$mm)Revenues evolution (US$mm)

20

8096

13 5

2009 2010 2011 1Q 2011 1Q 2012

9291.227 1.422

298 377

2009 2010 2011 1Q 2011 1Q 2012

+24% +117%

CAGR CAGR

39 stores39 stores

Cencosud36%

Falabella24%

Ripley24%

La Polar16%

+27%-62%

Department stores: acquisition of Johnson’s

Transaction summary

� In December 2011, we acquired an 85.58% interest

� 39 stores throughout Chile under the Johnson’s brand and 13 stores using the FES brand

� 120,000 m2 of selling space incorporated

Financial highlights

� Aggregate purchase price of Ch$32,606 million

� Of which, Ch$17,576 million to repay indebtedness at Johnson’s, while the rest to be used for working capital

� 2011 sales of Ch$118,447 million from its retail operations

Integration and objectives

� Replace all Johnson’s credit cards with Cencosud credit cards

� Improve our coverage of the low and middle income market segments in Chile

Key considerations Selling space expansion (‘000s m 2)

117

241236216

2009 2010 2011

Paris Johnson's359

359

241

243

236

161

Falabella

Ripley

La Polar

Largest department store presence in Chile (‘000s sq. meters)

+49%

Source: Company filingsNote: Figures as of 4Q11

+

15

Q&A