Page 1 of 67

A STUDY OF TRENDS OF INFLATION

AND UNEMPLOYMENT IN INDIAN

ECONOMY

A DESCRIPTIVE ANALYSIS

This term paper is submitted in partial completion of MBA

SUBMITTED TO:

Faculty Guide: Mr. Rajneesh Mishra

Assistant Professor Economics

Amity University Dubai

SUBMITTED BY:

Student: Ms. Anu Damodaran

Registration No: AUD0260

Program: MBA - General

Year: 2012 to 2014

Page 2 of 67

CERTIFICATE FROM FACULTY GUIDE

This is to certify that Ms. Anu Damodaran, Reg. No. AUD0260, a 1st Year MBA – General

student of Amity University, Dubai, UAE, has carried out her term paper - “A Study of Trends

of Inflation and Unemployment in Indian Economy – A Descriptive Analysis” from 12-Oct-

2012 to 13-Dec-2012. She has completed the term paper successfully. She has done this term

paper work independently and submitted the same on 13-Dec-2012.

Mr. Rajneesh Mishra, Faculty Guide,

Assistant Professor of Economics,

Amity University, Dubai, UAE

Page 3 of 67

ACKNOWLEDGEMENT

I, Ms. Anu Damodaran, sincerely thank and acknowledge the valuable inputs and guidance

extended to me by Mr. Rajneesh Mishra, Assistant Professor of Economics at Amity University,

Dubai, toward successful completion of this term paper “A Study of Trends of Inflation and

Unemployment in Indian Economy – A Descriptive Analysis”.

I offer my sincere thanks to my husband Mr. Pradeep Kumar Raju for his enduring support in

every aspect for the completion of this term paper.

Thanking you,

Yours sincerely,

Ms. Anu Damodaran

Reg. No. AUD0260,

1st Year MBA – General,

Amity University, Dubai, U.A.E.

Page 4 of 67

TABLE OF CONTENTS

NO. TOPIC PAGE NO

1 INTRODUCTION 6

1.1 OBJECTIVES OF THE TERM PAPER 7

1.2 RESEARCH METHODOLOGY 8

1.3 LITERATURE REVIEW 8

2 INFLATION: AN OVERVIEW 11

2.1 MEANING OF INFLATION 11

2.2 ECONOMIC INFLATION 12

2.3 WHAT IS "DEFLATION"? 12

2.4 HOW IS DEFLATION MEASURED? 13

2.5 HOW IS DEFLATION STOPPED? 13

2.6 WHY IS DEFLATION WORSE THAN INFLATION? 14

2.7 CAN DEFLATION EVER BE A GOOD THING? 14

2.8 DEFINITION OF COST-PUSH INFLATION 14

2.9 DEFINITION OF DEMAND-PULL INFLATION 15

2.10 DEMAND PULL AND COST PUSH INFLATION WITH EXAMPLES 15

2.11 ANTICIPATED INFLATION, INVESTMENT, AND THE CAPITAL STOCK 18

2.12 EFFECTS OF INFLATION ITS CONSEQUENCES AND POLICY MEASURES 18

2.13 THE COSTS OF REDUCING INFLATION 20

2.14 INFLATION AS A TAX 21

2.15 MEASURES TO CONTROL INFLATION 22

2.16 INFLATION IN DEVELOPING COUNTRIES 26

2.17 INDIA INFLATION RATE 27

2.18 INFLATION IN INDIA 2012 28

2.19 CONDITION OF THE INR 29

2.20 CONDITION OF EXPORT AND IMPORT 29

2.21 INDIA ECONOMIC GROWTH 29

3 UNEMPLOYMENT: AN OVERVIEW 31

3.1 MEANING OF UNEMPLOYMENT 31

3.2 VOLUNTARY VERSUS INVOLUNTARY UNEMPLOYMENT 31

3.3 FRICTIONAL UNEMPLOYMENT 31

3.4 WHAT CAUSES FRICTIONAL UNEMPLOYMENT? 33

3.5 TYPES OF FRICTIONAL UNEMPLOYMENT 33

3.6 STEPS TO REDUCE FRICTIONAL UNEMPLOYMENT 34

3.7 CYCLICAL UNEMPLOYMENT 35

3.8 STRUCTURAL UNEMPLOYMENT 37

3.9 CAUSES OF STRUCTURAL UNEMPLOYMENT 37

3.10 EXAMPLES OF STRUCTURAL UNEMPLOYMENT 38

3.11 STEPS TO REDUCE STRUCTURAL UNEMPLOYMENT 38

Page 5 of 67

3.12 POLICIES FOR REDUCING UNEMPLOYMENT 39

3.13 DEMAND SIDE POLICIES 39

3.14 POLICIES TO REDUCE SUPPLY SIDE UNEMPLOYMENT 40

3.15 UNEMPLOYMENT IN INDIA 41

3.16 REASONS FOR UNEMPLOYMENT IN INDIA 43

3.17 INFLATION AND UNEMPLOYMENT: WHAT IS THE CONNECTION? 44

3.18 FOUR PHASES OF BUSINESS CYCLE 45

3.19 EXPLANATION OF FOUR PHASES OF BUSINESS CYCLE 46

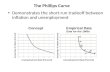

3.20 THE PHILLIPS CURVE 49

3.21 EXPLANATION OF PHILLIPS CURVE 51

3.22 MONETARIST VIEW OF THE PHILLIP CURVE 52

3.23 STAGFLATION – AN OVERVIEW 53

3.24 WHAT IS STAGFLATION AND WHY IS IT SO DANGEROUS? 54

3.25 WHAT ARE THE CAUSES OF STAGFLATION? 55

3.26 HOW TO PREVENT STAGFLATION 56

4 DATA ANALYSIS 58

5 RESULTS AND CONCLUSION 62

BIBLIOGRAPHY 64

TABLE OF FIGURES & TABLES

NO. TOPIC PAGE NO

Fig.2.1 DEMAND PULL INFLATION 16

Fig.2.2 COST PUSH INFLATION 17

Fig.2.3 INDIA INFLATION RATE 28

Fig.3.1 DIAGRAM OF FOUR PHASES OF BUSINESS CYCLE 46

Fig.3.2 PHILLIPS CURVE 51

Fig.3.3 MONETARIST VIEW OF THE PHILLIP CURVE 52

Fig.3.4 STAGFLATION 53

Fig.4.1 CPI INFLATION RATES: 2002-2012 58

Fig.4.2 WPI INFLATION RATES GRAPH (2010-2012) 59

Fig.4.3 UNEMPLOYMENT RATE (%) GRAPH (2002-2011) 60

Fig.4.4 INDIA ECONOMIC FORECAST GRAPH (2012-2016) 61

Table: 4.1 CPI INFLATION RATES GRAPH (2002-2012) 58

Table: 4.2 YEARLY WHOLESALE PRICE INDEX - BASE YEAR 2004-05 59

Table: 4.3 UNEMPLOYMENT RATE (%) 60

Table 4.4 INDIA ECONOMIC FORECAST 61

Page 6 of 67

1 INTRODUCTION

The topic of the term paper “A Study of Trends of Inflation and Unemployment in Indian

Economy – A Descriptive Analysis” is to know the Inflation's effects on unemployment in the

Indian economy. It is to know whether the effects are positive or negative in nature. In India

inflation and employment rates are playing hide and seek on the basis of global crisis and rural

and urban crisis. For the last three years, since the global financial crisis of 2008, unemployment

rates have been rising in large number of countries. Due to global crisis developed countries

were not left with enough money for investment in developing countries as they had to pay their

debts. Due to this investment in Indian businesses is very less which deprive businesses to buy

enough raw materials for production and when there are less production then unemployment

increases.

Inflation and Unemployment are the two important variables in macroeconomics. The

phenomenon of very high inflation and unemployment is generally bad and should be avoided if

possible. There is considerable disagreement over which of the two is more harmful. Since, a

certain amount of inflation and unemployment is unavoidable and since efforts to reduce one,

usually result in an increase in the other.

Reasons for the priority and urgency to control inflation and unemployment can be appreciated

only after knowing their causes and consequences for the society. There are several effects of

inflation. It has adverse impact on income distribution. A price rise tends to benefit some

individuals and harm others. While for some income earners, income rises more rapidly than

prices during inflation, for many people just the opposite is true. Those who have fixed incomes

are seriously affected as the real income decline during periods of inflation. Inflation also has

effect on lending and savings. Inflation benefits the borrowers at the expense of the lenders and

savers. The saving rate and hence investment rate is affected adversely. Inflation, in a country,

has also adverse effects on foreign trade. The competitiveness of a country may be seriously

affected.1

1 http://www.ijeronline.com/documents/volumes/Vol%203%20Iss%204/ijerv3i4JuAu2012(2).pdf

Page 7 of 67

Regarding unemployment, economists general classify unemployment into three types according

to the causal factors, namely, frictional unemployment, cyclical unemployment and structural

unemployment. The structural unemployment refers to the persons who are between the jobs.

Cyclical unemployment results from business recessions and depressions when total spending in

the economy is below the full employment productive capacity of the economy. In such a

situation, the economy has same natural resources, manpower and productive equipment as

before the cyclical unemployment occurred but the problem is that economy does not produce

because the goods and services being produced are not being purchased. The people were not

buying because they either had lost their jobs or feared the loss of their jobs. Structural

unemployment arises due to a mismatch between job seekers and job openings. It refers to a

situation when both the jobs and job seekers exist but something prevents the filling up the

vacancies. Unemployment has both economic and social implications for a country like India.

Occurrence of unemployment results in the loss of output, loss in revenue of the government and

in consequence disastrous effect on developmental works. The social cost of unemployment

cannot be measured in money terms, but it involves an intolerable amount of human suffering.

Unemployment means loss of self-respect, poverty and frustration. It can even lead to social

unrest in the country. There are other types of unemployment also in developing countries like

India. These are underemployment and disguised unemployment. Disguised unemployment

refers to zero or very low productivity level and is most prevalent in Indian agriculture sector.

The presence of this type of unemployment makes functioning of labor market inefficient.

1.1 OBJECTIVES OF THE TERM PAPER:

1. To relook into the concepts of inflation and unemployment from a macroeconomic

perspective.

2. To study the rate of inflation and unemployment

3. To analyze the rate of inflation and unemployment in Indian economy for the past 10

years and to examine the trends of inflation and unemployment.

4. To explain the problems of inflation and unemployment and their impacts on macro

economy.

Page 8 of 67

5. To become familiar with basic facts and concerns and to develop a well-grounded picture

of the situation.

1.2 RESEARCH METHODOLOGY

The research method adopted in this term paper is exploratory in nature. It relies on secondary

research such as reviewing available literature and data. In this term paper, exploratory research

has been taken to gain experience that will be helpful to formulate relevant hypothesis for more

definite investigation at some point later. The results of this exploratory research may not be

useful for decision-making by themselves, but they provide significant insight into the given

situation.

1.3 LITERATURE REVIEW

In the paper “The inexorable and mysterious tradeoff between inflation and unemployment “N.

Gregory Mankiw, Sept 2000 states that price stickiness can easily explain why society faces a

short-run tradeoff between inflation and unemployment. The dynamic relationship between

inflation and unemployment remains a mystery. The so-called "new Keynesian Phillips curve" is

appealing from a theoretical standpoint, but it is ultimately a failure. It is not at all consistent

with the standard stylized facts about the dynamic effects of monetary policy, according to which

monetary shocks have a delayed and gradual effect on inflation. The failure to produce a

dynamic relationship between inflation and unemployment that is derived from first principles

and that fits the facts is surely such a puzzle. The economics profession is not likely to ever

reject the short-run tradeoff between inflation and unemployment, so it had better get on with the

task of explaining it.2

2 http://www.nber.org/papers/w7884 http://www.business.otago.ac.nz/econ/research/discussionpapers/DP_1109.pdf http://bnarchives.yorku.ca/159/01/900101N_Macro_perspectives_on_inflation_unemployment.pdf http://www.umt.edu.pk/icobm2012/pdf/2C-90P.pdf http://www.ijeronline.com/documents/volumes/Vol%203%20Iss%204/ijerv3i4JuAu2012(2).pdf http://www.umt.edu.pk/icobm2012/pdf/2C-90P.pdf http://www.eurojournals.com

Page 9 of 67

In the paper “Unemployment in the Long Run” Alfred A. Haug, University of Otago and Ian

P. King, University of Melbourne have used a statistical approach is atheoretical in nature, but

provides evidence in accordance with the predictions of Friedman (1977) and the recent New

Monetarist model of Berentsen, Menzio, and Wright (2011): the relationship between inflation

and unemployment is positive in the long run. They have examined the relationship between

inflation and unemployment in the long run, using quarterly US data from 1952 to 2010.

In his paper “Macroeconomic perspectives on inflation and unemployment” by Jonathan Nitzan

(late 1950s) has mentioned that there is a dual love-hate relationship with the Phillips Curve.

Scholars who endorsed the Phillips Curve on the basis of historical evidence were surprised

when it started to crumble as soon as they assimilated it into their macroeconomic models. He

stated that the gradual emergence of stagflation and the progressive breakdown of the Phillips

Curve presented mainstream macroeconomics with the most serious challenge since the Second

World War. Macroeconomists attacked the Phillips Curve but their criticisms sought to modify,

not nullify.

The idea that inflation and unemployment were inversely related was apparently too significant

to discard so the notional relationship was simply ‘augmented’ by auxiliary factors. The cost of

saving the Phillips Curve was substantial. He concluded that to explain stagflation,

macroeconomists resorted to ‘disequilibria, ‘rigidities’ and “exogenous shocks’ and they

abandoned, at least temporarily, the ideal formulation of the neoclassical synthesis.

In the paper “Inflation and Unemployment: The Roles of Goods and Labor Markets Institutions

Lucy Qian Liu, November 23, 2008, says that empirical evidence on inflation and

unemployment suggests that they can be either positively or negatively related in the long run.

The study was on this relationship in an environment in which inflation has differential effects

on employed and unemployed workers. She found that due to either heterogeneous money

holdings or imperfect indexation of unemployment insurance, the unemployed are affected by

the inflation tax to a larger extent than the employed. A higher rate of inflation increases

workers’ incentives to work and generates a negative effect on unemployment.

http://www.eurojournals.com

Page 10 of 67

On the other hand, inflation lowers a firm’s return from creating job vacancies, thereby raising

unemployment. In the steady state the inflation-unemployment relationship is either positive or

negative, depending on goods and labor markets institutions. Sales taxes, the degree of

heterogeneity in money holdings and the market power of firms are major factors determining

the direction of this relationship. Through a comparison of market institutions, the model

generates an inflation unemployment relation that is qualitatively consistent with the empirical

evidence.

In the paper “An empirical study of Phillips curve in India” by Mr. Manoj Kumar,Research

Scholar & Prof. D.C.Vashist, Head, Department of Economics, Central University of Haryana,

Jant-Pali,Temp Building: Govt. B.Ed College(New Building), Narnaul(Mahendergarh) Haryana,

India, brought out the fact that the past studies have found mixed evidence about the shape of the

Phillips curve from being horizontal to vertical. The researchers have also observed that there are

very few studies about the developing countries including India. The present finding does not

support the hypothesis of vertical Phillips curve. There is a trade-off between prices and

unemployment. Rather it suggests that there is a short run Phillips curve in India. The study is

based on secondary sources of data. Regarding data source has been taken from Handbook of

Statistics on Indian Economy, RBI and construction of variables is used from the Indian annual

data for the period 1951-52 to 2007-08.

In the paper “Is There Any Tradeoff between Inflation and Unemployment? The Case of

SAARC Countries” Sagar Katria, Niaz Ahmed Bhutto, Falahuddin Butt, Azhar Ali Domki,

Hyder Ali Khawaja, Javeria Khalid, Sukkur Institute of Business Administration, Sukkur the

aim was to identify the relationship between inflation and unemployment in SAARC countries

from the perspective of Phillips curve. Unbalanced annual panel data of 8 SAARC members

(Afghanistan, Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan and Sri Lanka) and 6

expected member of SAARC (Republic of China, Russia, Indonesia, Iran, Myanmar and South

Africa) had been used for the period 1980-2010. This paper found significant results; there is a

negative relationship between inflation and unemployment rate in the SAARC Countries.

Concept of Phillips curve holds true.

Page 11 of 67

In the paper “The South Asian Phillips Curve: Assessing the Gordon Triangle” Muhammad

Imtiaz Subhani, Amber Osman and Muhammad Nayaz have investigated the Phillips Curve

in connection with the Gordon Triangle for the South Asian Countries i.e. Pakistan, India,

Bangladesh and Sri Lanka. The systematic investigation is based on historical thirty years of the

rates of inflation and unemployment for the countries outlined. The split analysis of each country

highlights the relationship between inflation and unemployment, which is positive for Pakistan

and negative for Bangladesh, while no relationship has been observed between the two variables

(no Phillips curve) for India and Sri Lanka. The negative impact of unemployment on inflation is

actually the confirmation of Phillips Curve, which is identified for Bangladesh, while the

positive association between the unemployment and inflation (Stagflation) is also observed that

is a confirmation of the Gordon triangle empirically observed and identified for Pakistan.

In the paper “Phillips curves and unemployment dynamics: a critique and a holistic perspective

”Marika Karanassou, Hector Sala and Dennis J. Snower show that frictional growth, i.e. the

interplay between lags and growth, generates an inflation–unemployment tradeoff in the long

run. They argue that a holistic framework, such as the chain reaction theory (CRT), should be

used to jointly explain the evolution of inflation and unemployment.

2 INFLATION: AN OVERVIEW

2.1 MEANING OF INFLATION

The overall general upward price movement of goods and services in an economy (is often

caused by an increase in the supply of money) usually measured by the Consumer Price Index

and the Producer Price Index. Over time, as the cost of goods and services increase, the value of

a dollar or rupee is going to fall because a person won’t be able to purchase as much with that

dollar or rupee as he/she previously could.

Page 12 of 67

2.2 ECONOMIC INFLATION

Price increases powerfully assist in reducing demand and increasing supply so that inflation can

be brought to a halt. Price controls below market rates and/or the expenditure of national savings

(financial reserves) to hold down monetary devaluation are inflationary. Price controls and the

expenditure of financial reserves subsidize inflationary levels of demand and deter increases in

supply. They make it much more difficult much more painful to bring inflation to a halt and

restore healthy and sustainable economic growth. Many people have vested interests in the

simplistic and invalid concepts that define inflation in terms of the price increases that it causes.

This fallacy is widely accepted without critical analysis.

By defining inflation simplistically in terms of the current rate of price increases economists,

politicians, and others with vested interests in the continuance of the policies actually causing

inflation can pretend that inflation doesn't exist or can minimize its extent for the long periods

when inflationary forces manifest themselves in ways other than in pushing prices higher.

Econometric technicians who have to ignore all economic factors that cannot be expressed as

equations and have to reduce all recognized economic concepts to the simplistic point where they

can be mathematically measured or weighted are forced to ignore the existence and extent of

inflationary forces until those forces cause price increases that can be measured. This is like

those medical tests that never show what is wrong until the patient is already half dead.

2.3 WHAT IS "DEFLATION"?

When prices decline due to productivity increases, the declining prices powerfully increase

purchasing power and demand even as the productivity gains increase supply. Deflation is a

process, not a thing. The real problem is thus to define those factors that cause deflation - those

factors that are "deflationary.” The standard deflation definition is when asset and consumer

prices continue to fall. This may seem like a great thing to consumers, except that the cause for

widespread deflation is a long-term drop in demand. Unfortunately, a drop in demand means that

a recession is probably already underway, with job losses, declining wages, and an ongoing

Page 13 of 67

decline in the value of your home and your stock portfolio. Deflation is a result of businesses

dropping prices in a desperate attempt to get people to buy their products.

2.4 HOW IS DEFLATION MEASURED?

Officially, deflation is measured by a decrease in the Consumer Price Index. However, the CPI

does not measure stock prices, which retirees use to fund purchases, and businesses use to fund

growth. More important, the CPI does not include sales price of homes. Instead, it calculates the

monthly equivalent of owning a home, which it derives from rents. This is very misleading, since

rental prices are likely to drop when there is high vacancy, usually when interest rates are low

and housing prices are rising. Conversely, when home prices are dropping due to high interest

rates, rents tend to increase. Therefore, the CPI gives a false low reading when home prices are

high (and rents are low).

2.5 HOW IS DEFLATION STOPPED?

To combat deflation, the Central Bank must stimulate the economy with expansionary monetary

policy. It reduces interest rates, and increases the money supply, in an attempt to jump-start

economic growth. In addition, the government can offset deflation with expansionary fiscal

policy. It can put more money into circulation by lowering taxes, increasing government

spending, and incurring a temporary deficit to do so. Of course, if the deficit is already at record

levels, that tool becomes less available. Why does expansionary monetary or fiscal policy work?

If done correctly, it stimulates demand. People have more money to spend, and they are willing

to buy now even though they expect prices to continue to fall. Once the government restores

confidence in economic growth, a lot of people will feel like low prices have hit their bottom,

and will "get in while the getting is good." When enough people do this, demand will outstrip

supply and prices will reverse their downward trend.

Page 14 of 67

2.6 WHY IS DEFLATION WORSE THAN INFLATION?

Like inflation, deflation is very difficult to combat once it is entrenched. As businesses and

people feel less wealthy, they spend less, reducing demand further. Prices drop in response,

giving businesses less profit. Once people expect the price declines, they delay purchases as long

as possible. They know the longer they wait, the lower the price will be. This further decreases

demand, causing businesses to slash prices even more. It is a vicious, downward spiral. Massive

deflation turned a recession into the Great Depression of 1929. As unemployment rose, demand

for goods and services fell. Prices dropped 10% a year. As prices fell, companies went out of

business. More people became unemployed. When the dust settled, world trade essentially

collapsed. The amount of goods and services traded fell 25%, but thanks to deflation the value of

this trade was down 65% (as measured in dollars).

2.7 CAN DEFLATION EVER BE A GOOD THING?

Massive, widespread deflation is always bad for the economy. However, deflation in certain

asset classes can be good. For example, the price of consumer goods, especially computers and

electronic equipment, continues to fall. This isn't because of lower demand, but from innovation.

In the case of consumer goods, production has moved to China, where wages are lower. This is

an innovation in manufacturing, which results in lower prices for many consumer goods. In the

case of computers, manufacturers find ways to make the components smaller, adding more

power for the same price. This is technological innovation, and it keeps computer manufacturers

competitive.

2.8 DEFINITION OF COST-PUSH INFLATION

The text "Economics" (2nd Edition) by Parkin and Bade gives the following explanation for

cost-push inflation: "Inflation can result from a decrease in aggregate supply.

Page 15 of 67

The two main sources of decrease in aggregate supply are:

1. An increase in wage rates

2. An increase in the prices of raw materials

These sources of a decrease in aggregate supply operate by increasing costs, and the resulting

inflation is called cost-push inflation. Other things remaining the same, the higher the cost of

production, the smaller is the amount produced. At a given price level, rising wage rates or rising

prices of raw materials such as oil lead firms to decrease the quantity of labor employed and to

cut production." Aggregate supply is the "the total value of the goods and services produced in a

country" or simply factor "The supply of goods". The supply of goods can be influenced by

factors other than an increase in the price of inputs (say a natural disaster), so not all factor

inflation is cost-push inflation.

2.9 DEFINITION OF DEMAND-PULL INFLATION

Parkin and Bade give the following explanation for demand-pull inflation: "The inflation

resulting from an increase in aggregate demand is called demand-pull inflation. Such inflation

may arise from any individual factor that increases aggregate demand, but the main ones that

generate ongoing increases in aggregate demand are:

1. Increases in the money supply

2. Increases in government purchases

3. Increases in the price level in the rest of the world

2.10 DEMAND PULL AND COST PUSH INFLATION WITH EXAMPLES

Demand-pull inflation happens when aggregate demand (AD) increases in an economy and

intersects the short run aggregate supply curve (SRAS) to the right of where SRAS and long run

aggregate supply (LRAS) cross. This causes some inflation to occur in the short run, and even

more in the long run as the economy adjusts (and the labor market moves back to equilibrium).

Demand-pull inflation can occur for a reason that causes AD to increase but the most common

Page 16 of 67

are expansionary fiscal and monetary policy, and positive expectations about the future

(increased growth/income expectations). Cost-push inflation happens when SRAS shifts to the

left (decreases) and intersects the AD curve to the left of where AD and LRAS cross. This will

cause inflation in the short run, but prices will drop back down again in the long run as the labor

market adjusts back to equilibrium (with wages dropping). Note that some classes ignore the

long run, and only care about where AD and AS cross and in this case cost-push inflation is a

permanent shift in the AS curve causing some amount of inflation.

Fig.2.1

A common question considers whether inflation caused by an increase in wages (such as

increasing the minimum wage) is caused by demand-pull inflation or cost-push inflation. In fact,

it is caused by both. An increase in wages is an increase in the cost of inputs which shifts the AS

curve to the left (a decrease). An increase in wages also translates to an increase in income which

means consumers can spend more making GDP larger and shifting AD to the right (an increase).

Page 17 of 67

Fig.2.2

These two effects happening at the same time mean that the price level must rise, but that the

new equilibrium point is uncertain, depending on whether AD’s increase or AS’s decrease was

greater in magnitude. There are many ways to consider this:

1. The increase in costs is equal to the increase in income to the shifts must be the same and

equilibrium GDP will be the same only at a higher price level.

2. Assume that some of the income is saved or paid in taxes so the AD shift will be smaller

than the AS shift.

3. Finally, you can assume that the multiplier effects from the increase in consumption

spending (and investment from savings and government spending from taxes) is large so

that the AD shift will be larger than the AS shift.

The third scenario probably the most likely, but we do not know for sure unless we have some

equations or data to base it on. So the real answer here is that inflation caused by an increase in

wages is a double whammy of both demand-pull and cost-push inflation, we cannot blame it on

one source.

Page 18 of 67

2.11 ANTICIPATED INFLATION, INVESTMENT, AND THE CAPITAL

STOCK

Since inflation indirectly taxes the return on investment, higher inflation leads agents to reduce

their investment as well, and the capital stock falls. The falls in consumption and investment

imply that agents work less, and the combination of a lower supply of labor and a lower capital

stock means that output is lower as well. Prolonged and intense inflation upsets many habits of

economic life, confronting consumers with price increases and price dispersions that send them

shopping; making them doubt their ability to maintain their living standards, and downgrade the

value of their career jobs and long-term savings; and forcing them to compile more information

and to try to predict the future--costly and risky activities that they are poorly qualified to

execute and bound to view with anxiety [Okun 1975: 383].

Furthermore, since unanticipated inflation also produced arbitrary wealth redistributions from

some individuals to others. Since the amounts involved can be very large, even for relatively

moderate inflation rates and most people desire security, they naturally regard the possibility of

such redistributions as a serious threat to their livelihood. Each of these factors such as confusion

over price signals, the undermining of social institutions, and the threat of inflationary

redistributions of income and wealth generates its own distinctive welfare losses. If they were

estimable, these losses ought to be included in any sensible estimate of the `true' welfare cost of

real-world inflation, as opposed to the hypothetical welfare costs that arise in models that assume

there is no inflation uncertainty to worry about. But they should not be ignored simply because

we do not know how to estimate them, and they are almost certainly much more important than

the more estimable costs of anticipated inflation.

2.12 EFFECTS OF INFLATION ITS CONSEQUENCES AND POLICY

MEASURES

There is also evidence that output and employment can be reduced by inflation variability or

inflation uncertainty. In his Nobel lecture, Friedman (1977) implied that inflation variability has

Page 19 of 67

a detrimental effect on economic activity by making agents less willing to enter into long-term

relationships and by reducing the effectiveness of market price signals as indicators of relative

scarcity. To the extent that agents have not adjusted to it, higher inflation variability should

therefore lead to a temporary though perhaps long-lasting reduction of output and employment.

However, the Friedman logic applies more naturally to inflation uncertainty than it does to

inflation variability, and modified in this way, it suggests that greater inflation uncertainty should

lead to lower output and employment and higher unemployment. Extending the Friedman story

further, we might also expect inflation variability or uncertainty to reduce the rate of growth of

output as well. There have been a number of attempts to examine these effects empirically.

Maurice Levi and John Makin (1980) postulated that inflation uncertainty should be entered as

an additional variable in an expectations-augmented Phillips curve. Using the standard deviation

of the cross-section dispersion of Livingston inflation expectations as their proxy for inflation

uncertainty, they found that inflation uncertainty had a positive and significant effect on U.S.

unemployment (1980: 1024). Donald Mullineaux (1980) also used a Phillips-curve approach and

a similar measure of inflation uncertainty, and he obtained robust results that suggest that

inflation uncertainty has a positive and very significant and long-lasting effect on unemployment

(1980: 166-67).

Comparable estimates suggest that inflation uncertainty also has a significantly negative impact

on industrial production as well (1980: 167). Mullineaux also allowed inflation uncertainty to

respond to policy, and his results led him to conclude that "even if it were possible to generate a

sustained unanticipated increase in the rate of inflation, within a fairly short period the effect of

added uncertainty would more than offset the employment gains from unanticipated inflation"

(1980: 166-67). Using postwar U.S. data and a Livingston-type index of inflation uncertainty,

Steven Holland (1986: 242) and Lawrence Kantor (1986: 407) found that increased inflation

uncertainty raised unemployment, Yakov Ahimud (1981: 785-786) found that it had a

significantly negative effect on output and a significantly positive one on unemployment, and

Rick Hafer (1986: 367-368) got much the same results as Ahimud using the American Statistical

Association-National Bureau of Economic Research measure of e dispersion of one-period ahead

inflation forecasts instead of the Livingston measure. Richard Froyen and Roger Waud (1987)

found that inflation uncertainty (as measured by the variance of one-period-ahead forecasts of

Page 20 of 67

the price level) had a negative effect on output for their sample of the UK, U.S., Canada, and

West Germany, and Cozier and Selody (1991) found some evidence that output was negatively

affected by inflation variability even when allowance was made for the inflation rate itself.

2.13 THE COSTS OF REDUCING INFLATION

Perhaps the most commonly cited argument against reducing inflation is the cost of the lost

output or employment associated with doing so. If expectations or price or output decisions have

some element of stickiness, reducing inflation could lead to lower output and employment as

indicated by Phillips-curve analysis. If the disinflation persists, macroeconomic theory suggests

that the economy should eventually adjust to the new monetary policy and output and

employment should recover.

According to the natural rate hypothesis of Friedman (1968) and Phelps (1967), the output and

employment losses should be entirely transitory, and output and employment would tend to be

restored to their former natural levels. We would then be comparing the permanent benefits of

lower inflation against the temporary losses resulting from the disinflation needed to achieve it.

According to the more recent hysteresis argument (see, e.g., Blanchard and Summers 1986),

however, the natural levels of employment and output themselves depend on the past history of

those variables. Hysteresis is a situation "where one-time disturbances permanently affect the

path of the economy." (Romer Advanced Macroeconomics page 471). In unemployment,

hysteresis can occur from as results of type described by Insider-outsider Models. Deterioration

of skills from unemployed people lessens their human capital and can exacerbate the effect.

Another source is "labor-force attachment." Unemployed workers must adjust their standard of

living to a lower level, and they can get used to it and not try as hard to achieve the higher

previous level. Longer periods of unemployment also reduce the stigma and hence labor supply

may be permanently lower after demand returns to normal. For instance hysteresis is possible in

Europe. Once unemployment spiked, people adjusted to lower levels of living, the stigma for

being unemployed declined, and their skills declined. This contributes to a higher rate of

unemployment.

Page 21 of 67

In labor economics, the insider-outsider theory examines the behavior of economic agents in

markets where some participants have more privileged positions than others. The theory was

developed by Assar Lindbeck and Dennis Snower. The insiders are those incumbent workers

who enjoy more favorable employment opportunities than the outsiders. The reason for this

disparity is that firms incur labor turnover costs when they replace insiders with outsiders.

Examples of labor turnover costs are the costs of hiring, firing and providing firm-specific

training. Insiders may resist competition with outsiders by refusing to cooperate with or

harassing outsiders who try to underbid the wages of incumbent workers. The implications of

this behavior for employment and unemployment is that there is absence of wage underbidding

even when many unemployed workers are willing to work for wages lower than existing insider

wages (normalized for productivity differences).

When some external shock reduces employment, so that some insiders become outsiders, the

number of insiders decreases. This incentivizes the insiders to set even higher wages when the

economy again gets better, as there are not as many insiders remaining as before, instead of

letting the outsiders to again get jobs at earlier wages. This causes hysteresis, i.e., the

unemployment becomes permanently higher after negative shocks. As unemployment rises,

workers lose their skills through lack of use, for example, and the natural rate of unemployment

itself rises. Unemployment eventually returns to its natural rate, but the natural rate has increased

in the meantime. In addition to the temporary losses from output and employment being below

their natural levels, there would now also be permanent losses from the shifts in the natural

levels themselves.

2.14 INFLATION AS A TAX

A second argument against reducing inflation is that the monetary authorities may want to retain

the use of monetary policy as a form of taxation. The basic argument was set out explicitly by

Phelps (1973) and goes as follows:

If the government had access to theoretically ideal lump-sum taxes that could raise the revenues

it desired without any efficiency losses, then efficiency considerations dictate that the

government should rely only on such taxes. There are also other reasons to question the Phelps

Page 22 of 67

argument. As Garfinkel (1989: 10) and Selody (1990a: 18) have pointed out, the Phelps view of

inflation as a tax tends to overlook the impact of inflation on the tax collection machinery as a

whole. The tax collection system was not designed to operate in an inflationary world, and as

already discussed, inflation actually plays havoc with it.

So, far from the optimal inflation rate being positive from a purely fiscal point of view, there is a

good argument that lowering inflation would not only reduce the direct welfare losses from the

use of the inflation tax per se, but would also reduce the welfare losses from other forms of

taxation as well. It is consequently bizarre, to say the least, to defend inflation on fiscal grounds.

As Peter Diamond and James Mirrlees (1971a, b) have pointed out, intermediate goods should

not be taxed even in a world where non distorting taxes are not available. The Ramsey rule

consequently applies only to final and not to intermediate goods. Applying the Diamond-

Mirrlees result to inflation then tells us that inflation is an inefficient form of taxation quite

regardless of any of the other problems already discussed (see also Kimbrough 1986, Faig 1988)

2.15 MEASURES TO CONTROL INFLATION

1) Monetary Measures

2) Fiscal Measures

3) Other Non-monetary Measures

(1) MONETARY MEASURES

A. Quantitative Methods

1. Raising the Bank Rate:

To control inflation the central bank increases the bank rate. With this the cost of borrowing of

commercial banks from central bank will increase so the commercial banks will charge higher

rate of interest on loans. This discourages borrowings and thereby helps to reduce the money in

circulation.

Page 23 of 67

2. Open Market Operations:

During inflation, the central bank sells the bills and securities. These cash reserves of

commercial banks will decrease as they pay central bank for purchasing these securities. Thus

the loan able funds with commercial banks decrease which leads to credit contraction.

3. Variable Reserve Ratio:

The commercial banks have to keep certain percentage of their deposits with the central bank in

the form of cash reserve. During inflation, the central bank increases this cash reserve ratio this

will reduce the lending capacity of the banks.

B. The Qualitative Methods

1. Fixation of Margin Requirements:

Commercial banks have to maintain certain fixed margins while granting loans. In inflation

central bank raises the margin to contract credits and reduces the price level.

2. Regulation of Consumer Credit:

For purchase of durable consumer goods on installment basis, rules regarding payments are

fixed. During inflation initial payment is increased and the number of installments is reduced.

These result in credit contraction and fall in prices.

3. Control through Directives:

Certain directives are issued by central bank to commercial banks and they are asked to follow

them while lending. This keeps in check the volume of money.

4. Rationing of Credit:

The central bank regulates the amount and purpose for which credit is granted by commercial

banks.

Page 24 of 67

5. Moral Suasion:

This refers to request made by central bank to commercial banks to follow its general monetary

policy.

6. Direct Action:

Direct action is taken by central bank against commercial banks if they do not follow the

monetary policy laid by it.

7. Publicity:

The central bank undertakes publicity to educate commercial bank and public about the trends in

money market. By undertaking these measures the central bank can control the money supply

and help to curb inflation.

(2) FISCAL MEASURES

1. Taxation:

The rates of direct and indirect taxes may be raised and new taxes may be imposed. This policy

will reduce the disposable income in the hands of the people and their expenditure.

2. Public Expenditure:

During inflation, the government should reduce its expenditure. This would reduce the income in

the hands of some people. Hence the effective demand would decrease.

3. Public Borrowing:

The government may resort to voluntary and compulsory borrowing. This policy reduces the

income in the hands of some people. Hence the effective demand would decrease.

4. Over Valuation of Domestic Currency:

Currency over valuation of domestic currency makes exports costlier and there is a fall in the

volume of exports. Imports also become cheaper and there is an increase in money supply

causing a fall in prices.

Page 25 of 67

5. Inducement to Save:

The government should induce savings through incentives. This will reduce the supply of money

and purchasing power of the people causing a fall in prices.

6. Public debt management:

The public debt should be handled in such a way that there is no increase in the supply of money.

Hence the surplus in the budget should be used to repay the public debts.

(3) NON –MONETARY MEASURES/OTHER MEASURES

1. Increase in output:

Every country suffering from inflation should take steps to increase the output of scarce goods

and services. The production of essential goods at the cost of luxury goods can so serve as an

anti-inflationary measure.

2. Price control and rationing:

Price control must be introduced in respect of essential commodities. Also rationing should be

introduced for equitable distribution of essential commodities. The supply of essential goods can

be undertaken through public distribution system to keep the prices in check.

3. Imports:

Imports of food grains and other essential goods which are in short supply should be allowed.

4. Legal action:

Legal action should be taken against hoarders and black marketers.

5. Wage-rate:

During inflation, the rise in wage rate should be linked to rise in labor productivity. This will

help to control inflation.

Page 26 of 67

6. Check on population growth:

It is essential to check the growth of population by adopting effective family planning devices.

Above all an efficient and honest administration and good discipline among people are essential.

The various measures stated above have to be combined in a proper manner depending on the

situation of the country.

2.16 INFLATION IN DEVELOPING COUNTRIES

Thirty years ago, financial shocks mainly originated in emerging markets. Today, as we are all

too well aware, those financial shocks are also originating in the developed world. Given today’s

volatile world, it may be time for investors to adopt a more nuanced approach to investing in

emerging markets. Rather than using the traditional frameworks such as emerging markets

versus developed markets it is advisable that investors consider creating their international

allocation on a country or regional basis.

The two reasons are:

1. Traditional frameworks are less relevant than they used to be. There are increasing

differences now between how individual emerging market countries are performing, what

their prospects are and where they are in the economic cycle. The same also applies for

developed market economies. Take the BRIC, for instance. It’s the acronym that applies to

the emerging market countries of Brazil, Russia, India and China, and to indices tracking

these economies. While it may be a great acronym, it no longer represents a homogenous

group of countries that are all in a similar stage of economic development. Today, there are

significant differences among the BRIC countries, especially regarding how they are

combating inflation. As a result, if you hold different views of the countries (say, if you love

Brazil and hate Russia) a BRIC fund may be a bad way to implement your view.

Page 27 of 67

2. Potential for improved risk-adjusted-returns

To be sure, whether investors should focus their equity allocation at the global, regional, or

country level will certainly depend on if they want to express tactical views. Still, I believe

investing on a country or regional basis could help investors potentially gain both flexibility

and better risk-adjusted returns. Past performance does not guarantee future results.

2.17 INDIA INFLATION RATE

The inflation rate in India was recorded at 7.45 percent in October of 2012. Inflation Rate in

India is reported by the Ministry of Statistics and Program Implementation. Historically, from

1969 until 2012, India Inflation Rate averaged 7.8 Percent reaching an all-time high of 34.7

Percent in September of 1974 and a record low of -11.3 Percent in May of 1976. In India, the

wholesale price index (WPI) is the main measure of inflation. The WPI measures the price of a

representative basket of wholesale goods.

In India, wholesale price index is divided into three groups: Primary Articles (20.1 percent of

total weight), Fuel and Power (14.9 percent) and Manufactured Products (65 percent). Food

Articles from the Primary Articles Group account for 14.3 percent of the total weight. The most

important components of the Manufactured Products Group are Chemicals and Chemical

products (12 percent of the total weight); Basic Metals, Alloys and Metal Products (10.8

percent); Machinery and Machine Tools (8.9 percent); Textiles (7.3 percent) and Transport,

Equipment and Parts (5.2 percent).

Page 28 of 67

Fig.2.3

2.18 INFLATION IN INDIA 2012

India’s inflation rate has grown more than expectations in May 2012 with increase in fuel and

food prices. The benchmark wholesale price index has increased by 7.55% compared to the

2011-12 fiscal. In April 2012 it had increased by 7.23%. 37 estimates done by a survey

conducted by Bloomberg News had produced a median figure of 7.5 percent. Other reports have

also shown that India’s imports and exports have been going down in May 2012. In the previous

quarter India’s economic growth rate decreased to its lowest in the last ten years. A major reason

for this was the lack of success of the initiatives for economic liberalization.

The international sales prospects of India also took a beating thanks to the situation involving the

debt crisis of Europe. The RBI is expected, as a result of the slowdown, to decrease borrowing

expenses - the Indian economy, which is one of the largest emerging markets globally, is

struggling with one of its quickest inflations. The rate of increase in the prices of non-food

manufactured goods is a proper indicator of core inflation. In April 2012 this rate was calculated

Page 29 of 67

at 4.77 percent, only to go up to 4.86 percent in May 2012. This information has been collected

by Bloomberg, which also reveals that vegetable prices have increased by 49% compared to

2011, and power and fuel expenses have increased by 11.5%

2.19 CONDITION OF THE INR

In the year gone by, the value of the INR with regards to the US Dollar has gone down. This has

affected the share market negatively as well. Duvvuri Subbarao, the RBI Governor, is expected

to bring down the benchmark repurchase rate by 7.75% and this is going to be a decrease of

0.25%.

2.20 CONDITION OF EXPORT AND IMPORT

The global economy is going through its worst phase after the previous meltdown ended in 2009

and this has forced the authorities to take some steps. In May 2012, India exported goods and

services worth 25.68 billion US dollars – this was a reduction of 4.16 percent compared to May

2011. Anup Pujari, the Director General for Foreign Trade of India, provided provisional

statistics at a media briefing session held in New Delhi. According to the information, imports

have come down to 41.9 billion US dollars, which is a decrease of 7.36 percent. The trade deficit

has been calculated at $16.3 billion.

2.21 INDIA ECONOMIC GROWTH

In the quarter that ended in March 2012, India’s GDP saw a growth rate of 5.3 percent compared

to the quarter that ended in March 2011. This was the slowest rate after 2003. India is the 3rd

biggest economy in Asia but its economic growth, of late, has been rather modest and, even, this

rate has been achieved after the RBI Governor increased the rates by 3.75 percentage points,

which was an unprecedented figure. The change took place from mid-March in 2010 till October

2011 and its major aim was to restrict the inflation. For majority of 2011, India’s inflation rate

was more than 9 percent.

Page 30 of 67

In the BRIC group, which also includes Brazil, China, and Russia, India has the quickest rate in

terms of price increase. Standard & Poor’s has already notified on June 11 that India could be the

first country in this group to not have an investment grade credit rating. Several Indian

companies have been on the receiving end of less-than-desirable economic growth and high price

pressure. Maruti Suzuki India Ltd has witnessed a fall in its car sales during May 2012. The

Indian units owned by General Motors and Ford have found the going tough due to high gasoline

prices3

3 http://www.investorwords.com/2452/inflation.html#ixzz2DmTlQ3t2

http://www.futurecasts.com/Understanding%20Inflation.html www.historyhouse.co.uk/articles/coin_clipping.html www.tudorhistory.org/glossaries/d/debasement.html http://www.ehow.com/about_5435731_hard-currency.html#ixzz2EBXd8dvV http://useconomy.about.com/od/pricing/f/Deflation.htm http://economics.about.com/cs/money/a/inflation_terms.htm http://www.freeeconhelp.com/2012/04/demand-pull-and-cost-push-inflation.html http://www.scribd.com/doc/55831120/3/MEASURES-TO-CONTROL-INFLATION http://articles.economictimes.indiatimes.com/2012-11-27/news/35385732_1_brics-countries-headline-inflation-essential-food-products http://business.mapsofindia.com/inflation/ http://www.tradingeconomics.com/india/inflation-cpi

Page 31 of 67

3 UNEMPLOYMENT: AN OVERVIEW

3.1 MEANING OF UNEMPLOYMENT

Total number of able men and women of working age seeking paid work. Unemployment

statistics vary according to how unemployment is defined and who is deemed to be part of the

workforce. International labor organization (ILO) computes unemployment on the basis of

number of people who have looked for employment in the last four weeks and are available to

start work within two weeks, plus those who are waiting to start working in a job already

obtained. Unemployment is the state of an individual looking for a paying job but not having

one. Unemployment does not include full-time students, the retired, children, or those not

actively looking for a paying job. Simply put, unemployment is a situation in which an

individual in an economy is looking for a job and can't find one. That said, economists divide

unemployment into a number of different categories, since defining types of unemployment

more precisely sheds some light on why unemployment occurs and what can be done about it.

3.2 VOLUNTARY VERSUS INVOLUNTARY UNEMPLOYMENT

At a very basic level, unemployment can be broken down into voluntary unemployment-

unemployment due to people willingly leaving previous jobs and now looking for new ones and

involuntary unemployment- unemployment due to people getting laid off or fired from their

previous jobs and needing to find work elsewhere. Not surprisingly, economists generally view

involuntary unemployment as a larger problem than voluntary unemployment since voluntary

unemployment likely reflects utility-maximizing household choices.

3.3 FRICTIONAL UNEMPLOYMENT

Frictional unemployment is unemployment that occurs because it takes workers some time to

move from one job to another. While it may be the case that some workers find new jobs before

they leave their old ones, a lot of workers leave or lose their jobs before they have other work

lined up. In these cases, a worker must look around for a job that it is a good fit for her, and this

Page 32 of 67

process takes some time. During this time, the individual is considered to be unemployed, but

unemployment due to frictional unemployment is usually thought to last only short periods of

time and not is specifically problematic from an economic standpoint. This is particularly true

now that technology is helping both workers and companies make the job search process more

efficient. Frictional unemployment can also occur when students move into the work force for

the first time, when an individual moves to a new city and needs to find work, and when women

re-enter the work force after having children. For example, redundant workers or people joining

the labor market for the first time such as university graduates may take time searching to find

the work they want at wage rates they are prepared to accept.

Imperfect information in the labor market may make frictional unemployment worse if the

jobless are unaware of the available jobs. Incentives problem can also cause some frictional

unemployment as some people looking for a new job may stay out of work if they believe the tax

and benefit system will reduce the net increase in income from taking work. When this happens

there are disincentives for the unemployed to accept work and this is known as the

unemployment trap. In short, frictional unemployment happens when it takes time for the labor

market to match the available jobs with those people seeking work. Frictional unemployment is

something that always exists, even in the fully developed economies. It is natural for a person to

quit one job to search for a better one.

To understand the concept in a better way, have a look at some examples mentioned below. A

fresh college graduate looking for a suitable job after passing out and not taking any random job

till he / she finds something more suitable. Companies are not hiring employees because there is

a mismatch between the required skills and the jobs available. Many organizations that hire on

seasonal basis will eventually lead to frictional unemployment during off season, while the

employees would look for other suitable jobs.

Page 33 of 67

3.4 WHAT CAUSES FRICTIONAL UNEMPLOYMENT?

As mentioned earlier, the frictional unemployment rate can never be zero in an economy. And

this fact is applicable even to the highest paying economies in the world. This is the reason why

no economy reaches the state of full employment. This makes frictional unemployment different

from other kinds of unemployment. Let us have a look at the causes of frictional unemployment.

The relationship between workers and employers tends to be heterogeneous in some or

the other way. This mismatch can lead to frictional unemployment, which makes it

closely related to structural unemployment.

Fresh graduates looking for a good job, but are not able to get it right away because of

certain demands by the employers in terms of skills and experience, therefore resulting in

frictional unemployment. Factors related to preference, work environment, skills,

remuneration, and location, work timings, etc., always raise a sense of dissatisfaction in

the workers or employers. This is one of the main causes of frictional unemployment.

There are many workers who wait to reenter their jobs. An example for the same would

be homemakers, new mothers, etc.

3.5 TYPES OF FRICTIONAL UNEMPLOYMENT

In some employment sectors, workers receive more than the price-adjusted equilibrium

wage. This restricts the amount of employment in the high-wage sector and attracts

workers from other sectors who wait to get jobs in this high-paying sector. This creates

“wait unemployment,” a type of frictional unemployment. Some sectors such as

agriculture and tourism require seasonal workers and lay off employees during the off-

season. This creates “seasonal unemployment,” another type of frictional unemployment.

Page 34 of 67

3.6 STEPS TO REDUCE FRICTIONAL UNEMPLOYMENT

Though the rate can never go down to zero, there are certain policies and solutions that can be

applied to reduce the rate of frictional unemployment in an economy. These are discussed as

follows.

Proper educational advice to college students in terms of the job demands and skills

required to get job faster.

Reduction in employment discrimination

Proper training facilities should be provided at schools and colleges.

Attempts to reduce the difference between the gross income and the net income.

Proper channel of information should be used to provide details of the available jobs and

potential workers.

If any biased approach exists in the work environment in terms of employees, job

location etc., then proper action must be taken against it.

More facilities should be provided to enable more flexibility and availability.

Though frictional unemployment is a type of unemployment, it is not considered to be

bad. On the contrary, it is considered beneficial because it gives an opportunity to both

the workers and the organizations to look for the best suitable options. If frictional

unemployment didn't exist, then most of the people would have been working in the same

jobs all their life, making it impossible to have a scope for growth, innovation and skill

development. A little bit of friction is required to increase the pace, and frictional

unemployment gives us the opportunity to do the same. Factors related to preference,

work environment, skills, remuneration, and location, work timings, etc., always raise a

sense of dissatisfaction in the workers or employers. This is one of the main causes of

frictional unemployment.

There are many workers who wait to reenter their jobs. An example for the same would

be homemakers, new mothers, etc.

Page 35 of 67

3.7 CYCLICAL UNEMPLOYMENT

It's probably not surprising that unemployment is higher during recessions and depressions and

lower during periods of high economic growth. Because of this, economists have coined the term

cyclical unemployment to describe the unemployment associated with business cycles occurring

in the economy. Cyclical unemployment occurs during recessions because, when demand for

goods and services in an economy falls, some companies respond by cutting production and

laying off workers rather than by reducing wages and prices. (Wages and prices of this sort are

referred to as "sticky."). When this happens, there are more workers in an economy than there are

available jobs, and unemployment must result. As an economy recovers from a recession or

depression, cyclical unemployment tends to naturally disappear. As a result, economists usually

focus on addressing the root causes of the economic downturns themselves rather than think

directly about how to correct cyclical unemployment in and of it.

Cyclical unemployment is a term in economics, which is based on a greater availability of

workers than there are jobs for workers. It is usually directly tied to the state of the economy.

Lower demand for products due to lack of consumer confidence, disinterest, or reduction in

consumer spending results in the workforce cutting back on production. Since production is

reduced, companies that retail such products may also cut back on workforce, creating yet more

cyclical unemployment. The reason this type of unemployment is called cyclical is because it is

usually linked to a country’s business cycle, a system of evaluating how gross domestic product

changes over time. Length of time is not always predictable in a business cycle, which includes

four basic periods. At the beginning of a business cycle, a slowdown in economic activity occurs

resulting in a sharp drop into a trough, which hits the lowest point of the economic cycle and

would be linked to the highest unemployment rate. Gradually, through a variety of factors, pace

of economic activity increases in the expansion period, and then the business cycle hits its peak,

which translates to economic recovery and more available work.

Page 36 of 67

Cyclical unemployment begins to occur during the first part of the business cycle and reaches its

peak when the business cycle is in the bottom of the trough. As economic recovery begins, more

jobs become available. When the business cycle peak is hit, there may be more jobs than there

are workers, the opposite of cyclical unemployment. Typically, business cycles are of short

duration, but occasionally, long-term economic factors create not recession, but depression. This

can mean that the actual time the economy sputters and falters can last for several years, creating

severe unemployment for a long time period.

When a country is in a depression, governments may act by lowering taxes and interest rates to

improve consumer demand and spending, and also by creating jobs. In the Great Depression in

the US, the government-created jobs ended part of the cyclical unemployment problem. More

jobs were offered, and the economy really picked up at the onset of World War II. Other factors

can create cyclical unemployment. When work traditionally done inside a country is outsourced,

this can heighten unemployment rates. Until workers can be retrained for other positions or find

jobs where demand still remains high, they may experience long periods of unemployment.

Cyclical unemployment may also be defined as a negative correlation between Gross Domestic

Product (GDP) and unemployment rate. As Gross Domestic Product shrinks, unemployment rate

expands. It has an impact on the ability for an economy to recover, since fewer jobs create less

consumer spending, and less demand. It also creates higher government spending in order to help

those people who require unemployment checks, and welfare or financial assistance. Usually,

economic recovery does begin, but how it does so can vary with each business cycle.

Therefore this type of unemployment is considered temporary, at least in economic recession,

and based on the economic cycle, it will tend to cease over time when the economy moves out of

the business cycle trough and begins to climb into recovery and then to its peak. For example, in

the US the housing sector employs more people for construction and sales during the non-winter

months and housing booms. Likewise, unemployment rises during times of economic slowdown

and recession, as lower demand for services and goods causes business to lay-off workers and

gives less incentive to hire new workers. One key is to maintain workers' connection to the labor

market by providing employment opportunities. If workers lose their attachment to the labor

Page 37 of 67

market, the evidence suggest they can become a long-term problem, and policymakers need to do

much more than they are doing to create short-term opportunities for unemployed workers to

prevent this from happening.

3.8 STRUCTURAL UNEMPLOYMENT

There are two ways to think about structural unemployment. One way is that structural

unemployment occurs because some labor markets have more workers than there are jobs

available, and for some reason wages don't decrease to bring the markets into equilibrium.

Another way to think about structural unemployment is that structural unemployment results

when workers possess skills that aren't in high demand in the marketplace and lack skills that are

in high demand. In other words, structural unemployment results when there is a mismatch with

workers' skills and employers' needs. Structural unemployment is thought to be a pretty

significant problem, mainly because structural unemployment tends to be largely of the long-

term variety and retraining workers is not a cheap or easy task. Structural unemployment can

create a higher unemployment rate long after a recession is over. If it is ignored by policy-

makers, it can then even lead to a higher natural unemployment rate.

3.9 CAUSES OF STRUCTURAL UNEMPLOYMENT

Structural unemployment can be created when there are technological advances in an industry.

This has happened in manufacturing, where robots have been replacing unskilled workers. These

workers must now get training in computer operations to manage the robots and other

sophisticated technology to get jobs in the same factories they worked in before. Structural

unemployment can also be caused by trade agreements, such as NAFTA (North American Free

Trade Agreement). When trade restrictions were eased, many factories relocated to Mexico,

leaving their prior employees without a place to work.

Page 38 of 67

3.10 EXAMPLES OF STRUCTURAL UNEMPLOYMENT

Structural unemployment can also occur if a country's economic growth is dependent upon

industries that are in decline. For example, the newspaper industry had been in decline since

2000, as web-based advertising had taken over its source of revenue. Employees, such as

journalists, printers and newspaper delivery boys, who were dependent upon that industry,

contributed to structural unemployment after they had been laid off. Since their skills were

narrowly focused on the newspaper's method of distributing news, they had a harder time getting

a different job unless they are retrained. Farmers in emerging market economies are another

example of structural unemployment.

As free trade allowed global food corporations access to their markets, small-scale farmers were

put out of business. They couldn't compete with the lower prices of the global firms. As a result,

they headed to cities in search of work. This structural unemployment existed until they were

retrained, perhaps in factory work. Seasonal unemployment is, not surprisingly, unemployment

that occurs because the demand for some workers varies widely over the course of the year.

(Pool lifeguards, for example, probably experience a decent amount of seasonal unemployment).

Seasonal unemployment can be thought of as a form of structural unemployment, mainly

because the skills of the seasonal employees are not needed in certain labor markets for at least

some part of the year. That said seasonal unemployment is viewed as less problematic than

regular structural unemployment, mainly because the demand for seasonal skills hasn't gone

away forever and resurfaces in a fairly predictable pattern.

3.11 STEPS TO REDUCE STRUCTURAL UNEMPLOYMENT

While totally eliminating structural unemployment is probably unwise, if not impossible,

it can be reduced through education and training programs.

Education and training are the solution to structural unemployment, but there is a catch.

The benefits accrued from education depend directly on the number of productive years a

worker has remaining before retirement. The young incur the investment expense of a

Page 39 of 67

formal education (college) because they have forty-plus years to recoup this cost.

Whereas the closer a person is to his retirement re-education and training provides little

help to the economy.

Of some importance, expansionary fiscal and monetary policies have little if any long

term effect on structural unemployment. While stimulating the economy can reduce

structural unemployment temporarily, so long as technological progress continues,

structural unemployment eventually returns to its "natural" level.

While stimulating the economy can reduce structural unemployment temporarily, so long

as technological progress continues, structural unemployment eventually returns to its

"natural" level.

3.12 POLICIES FOR REDUCING UNEMPLOYMENT

There are two main strategies for reducing unemployment:

Demand side policies to reduce demand-deficient unemployment (unemployment caused

by recession)

Supply side policies to reduce structural unemployment (the natural rate of

unemployment)

3.13 DEMAND SIDE POLICIES

1. Fiscal Policy

Fiscal policy can decrease unemployment by helping to increase aggregate demand and

the rate of economic growth. The government will need to pursue expansionary fiscal

policy; this involves cutting taxes and increasing government spending. Lower taxes

increase disposable income and therefore help to increase consumption, leading to higher

aggregate demand (AD). With an increase in AD, there will be an increase in Real GDP

Page 40 of 67

(as long as there is spare capacity in the economy.) If firms produce more, there will be

an increase in demand for workers and therefore lower demand-deficient unemployment.

Also, with higher aggregate demand and strong economic growth, fewer firms will go

bankrupt meaning fewer job losses. Keynes was a strong advocate of expansionary fiscal

policy during a prolonged recession. He argued that in a recession, resources (both capital

and labor) are idle; therefore the government should intervene and create additional

demand to reduce unemployment.

2. Monetary Policy

Monetary policy would involve cutting interest rates. Lower rates decrease the cost of

borrowing and encourage people to spend and invest. This increases AD and should also

help to increase GDP and reduce demand deficient unemployment.

3.14 POLICIES TO REDUCE SUPPLY SIDE UNEMPLOYMENT

1. Education and Training.

The aim is to give the long term unemployed new skills which enable them to find jobs in

developing industries, e.g. retrain unemployed steel workers to have basic I.T. skills

which helps them find work in service sector. However, despite providing education and

training schemes, the unemployed may be unable or unwilling to learn new skills. At best

it will take several years to reduce unemployment.

2. Reduce Power of trades unions.

If unions are able to bargain for wages above the market clearing level, they will cause

real wage unemployment. In this case reducing influence of trades unions (or reducing

Minimum wages) will help solve this real wage unemployment.

Page 41 of 67

3. Employment Subsidies.

Firms could be given tax breaks or subsidies for taking on long term unemployed. This

helps give them new confidence and on the job training. However, it will be quite

expensive and it may encourage firms to simply replace current workers with the long

term unemployment in order to benefit from the tax breaks.

4. Improved Geographical Mobility.

Often unemployed is more concentrated in certain regions. To overcome this

geographical unemployment, the government could give tax breaks to firms who set up in

depressed areas.

3.15 UNEMPLOYMENT IN INDIA

There are more than 6 crore well educated youth in India who is unemployed. There has been a

drastic increase in the literacy rate in India over the past few decades, unfortunately leading to a

massive increase in the unemployment rate. The share of agriculture in the total employment has

come down from 61.67% in 1993-94 to 52% in 2004-05.

It is a threatening decrease considering the fact that Agricultural income is a major share of

Indian Economy. Trade, hotel, restaurant, transport and communications sector showed a growth

in the employment rate. But, as said earlier the jobs in these sectors are highly vulnerable and

they tend to impart a sense of insecurity feeling among the employees. Most of the youth are left

to pursue a self-employment or small scale business career. But, they too had a severe blow with

the raising number of multinational companies, supermarkets and wholesale shopping malls. In

India, it seems that there is a huge money flow but this flow bypasses the poor.

Page 42 of 67

Various types of Unemployment seen in India:

1. Structural Unemployment: When demand for work falls short of the supply of labor

force, this type of unemployment arises. Unemployment in India is basically of this

category. Huge population is a main factor for this.

High population More Job Seekers STRUCTURAL Less jobs

2. Under-employment: Some people are employed, but their efficiency and capability are

not utilized to the optimum level. This kind of employment is increasing due to cut throat

competitions and people who are more qualified than necessary also are willing to do a

lesser job to get a job security. This is usually seen in the Public sector. This is uniquely

dangerous in itself because an under-employed person may either develop disinterest in

his work or may opt to corruption to earn more money which he thinks he ought to get for

his over-qualification.

High Competition UNDER-EMPLOYMENT Corruption Black Money fall

in the Economy

3. Seasonal Unemployment: This occurs due to change in the demand with change in the

seasons. Agriculture and agriculture related sectors experience this kind of

unemployment. Indian Agriculture ensures employment for only 7-8 moths and the

agricultural labors remain unemployed for the rest of the year.

Dry Season No crops SEASONAL UNEMPLOYMENT Urban Migration

4. Open Unemployment: When people who are willing to work and are capable to work

cannot find any work, they come under this category. Educated unemployment and

unskilled labor unemployment are of this kind. The increasing migration from rural to

urban areas is the main cause for this.

Page 43 of 67

Urban Migration OPEN UNEMPLOYMENT Slum Dwelling Communicable

Disease Prostitution Antisocial Behavior