Credit Derivatives in 2009 & Current Developments

d-fine – Risk Management Breakfast – Tower 42

London, 25 September 2009

Tim Brunne Credit Strategist

2

Introductory Remarks

During the crisis, credit derivatives "enjoyed" particular attention by politicians, regulators and the media (as well as securitizations and structured credits).

Regulation, processing, standardization and central clearing of OTC derivative markets have been debated for years.

CDS sometimes became a sort of scapegoat for the financial market crisis (Buffet, Soros, Dinallo, Petersen, etc.). But not the instruments failed, investment strategies did.

“Naked” CDS long; opaque market; central counterparty clearing

The demise of Bear Stearns, Lehman Brothers and, last but not least, the bailout of AIG (Financial Products) put the industry under intense pressure to improve the resilience of the market with respect to counterparty risks.

Some not-so-constructive proposals are not yet entirely off the table, but much has changed during the past 11 months

"Financial regulatory overhaul", "Resilience of OTC derivatives market", ISDA, ICE

3

AGENDA

GLOBAL OTC DERIVATIVES

VERY SHORT COURSE ON CDS

CORPORATE AND SOVEREIGN CDS

TRADING CREDITS DURING THE CRISIS

CDS CENTRAL COUNTERPARTIES

4

From more than 100% annual growth to a 50% decline

Source: ISDA, UniCredit Research

CDS outstanding volumes (ISDA semi-annual primary member survey)

0

10

20

30

40

50

60

70

Jun 01 Jun 02 Jun 03 Jun 04 Jun 05 Jun 06 Jun 07 Jun 08 Jun 09survey effective-date

tota

l CD

S o

utst

andi

ngs

(US

D tn

eq.

) ISDA primary member survey

5

Shrinking global CDS volumes indicate change in 1H08

Source: BIS, UniCredit Research

CDS outstanding volumes (BIS semi-annual G10 survey data)

0

10

20

30

40

50

60

Dec 04 Jun 05 Dec 05 Jun 06 Dec 06 Jun 07 Dec 07 Jun 08 Dec 08

notio

nal a

mou

nt o

utst

andi

ng (U

SD

tn e

q.)

Multi-name instruments

Single-name instruments

6

Gross market value surges to USD 5.7tn at YE 2008

Source: BIS, UniCredit Research

Global CDS gross market values (BIS semi-annual survey data)

0

1

2

3

4

5

6

Dec 04 Jun 05 Dec 05 Jun 06 Dec 06 Jun 07 Dec 07 Jun 08 Dec 08

gros

s m

arke

t val

ue (U

SD

tn e

q.) Multi-name instruments

Single-name instruments

7

CDS gross market value grows at fastest pace

Source: BIS, UniCredit Research

Global OTC derivatives gross market values (BIS semi-annual survey data)

0

1

2

3

4

5

6

Dec 04 Jun 05 Dec 05 Jun 06 Dec 06 Jun 07 Dec 07 Jun 08 Dec 08

gros

s m

arke

t val

ue (U

SD

tn)

0

4

8

12

16

20

24

gros

s m

arke

t val

ue (U

SD

tn) (

IR)Credit default swaps

FX contracts

Interest rate contracts (right scale)

8

DTCC covers about 80% of the market

Source: ISDA, DTCC, UniCredit Research

ISDA semi-annual primary member survey compared to DTCC TIW data

0

10

20

30

40

50

60

2007-12-28 2008-05-23 2008-10-17 2009-03-13 2009-08-07 2010-01-01end-of-week date

tota

l CD

S no

tiona

l (U

SD tn

eq.

)

0

10

20

30

40

50

60total CDS outstandings (ISDA)

total gross notional (DTCC; CDS,indices & index tranches)

9

AGENDA

GLOBAL OTC DERIVATIVES

VERY SHORT COURSE ON CDS

CORPORATE AND SOVEREIGN CDS

TRADING CREDITS DURING THE CRISIS

CDS CENTRAL COUNTERPARTIES

10

Premium Leg

Default LegEffective Date Maturity Date

Premium Payments

Single-name CDS – The most simple contract

(A) No default event

(B) Default event

Premium Leg

Default LegEffective Date Maturity Date

Default Payment(1 – Recovery)

Accrued Premiumat Default

11

Index CDS – The cornerstone of CDS liquidity

Example with two default events

Reference notional

Effective date Maturity date

Reference notional will be reduced by 1/125

Default payment(1 – Recovery)/125

Reduced premium payments

Effective date Maturity date

Premium leg

Default leg

12

Credit derivatives referencing corporate and sovereign credit risk

Risk type

Credit Default Swaps (CDS)Digital Default Swaps (DDS)Forward CDSConstant Maturity CDS

Linear Spread

Risk

Single-name Portfolio

CDS Indices (iTraxx, …), FuturesBespoke Linear BasketsDynamic Leverage Note (e.g. CPDO)CPPI Structures

DefaultCorrel.

First-to-Default (FTD) BasketsIndex Tranches (iTraxx, CDX)(Bespoke) Coll. Debt Obl. (CDO)CDO^2Equity Tranches, POETs, Tranchelets

Credit Default SwaptionsSpreadVolatility

CD Swaptions, Variance SwapsOptions on Futures / TR Locks

Hybrid Capital (Financials/Non-Fin.)Sub CDS, Equity Default SwapsCapital Structure Arbitrage

HybridRisk

First-to-Trigger Baskets on EDSCollateralized Fund Obligations (CFO)

13

AGENDA

GLOBAL OTC DERIVATIVES

VERY SHORT COURSE ON CDS

CORPORATE AND SOVEREIGN CDS

TRADING CREDITS DURING THE CRISIS

CDS CENTRAL COUNTERPARTIES

14

Outstanding CDS volumes continue to shrink in 2009

Source: DTCC, UniCredit Research

Aggregated CDS gross volume (DTCC trade information warehouse, weekly data)

0

5

10

15

20

25

30

35

2008-10-31 2009-01-16 2009-04-03 2009-06-19 2009-09-04end-of-week date

CD

S g

ross

vol

ume

(US

D tn

eq.

) Index CDS Single-name CDS Index tranches

15

Dealer vs. customer – Who buys CDS?

Source: DTCC, UniCredit Research; effective date: 18 September 2009

Global CDS breakdown by CDS type, CDS buyer and seller (DTCC)

1.301

1.403

0.1041.1901.240

0.135

65%

70%

75%

80%

85%

90%

95%

100%

Index (8.4 USD tn) Single (15.6 USD tn) Tranche (3.1 USD tn)CDS type (total gross volume)

(per

c.) t

otal

gro

ss n

otio

nal (

US

D tn

)

Customer(protection buyer) - Customer(investor)

Dealer(protection buyer) - Customer(investor)

Customer(protection buyer) - Dealer(investor)

Dealer(protection buyer) - Dealer(investor)

16

Investment-grade CDS indices are most liquidly traded

Source: DTCC, UniCredit Research; effective date: 11 September 2009

Gross notional: Break-down by index/index tranche family

00.5

11.5

22.5

33.5

44.5

5

iTraxx E

urope

Main

iTraxx E

urope

Fin

iTraxx E

urope

HiVol

iTraxx E

urope

XO

iTraxx E

urope

othe

rCDX.N

A.IG

CDX.NA.IG

.HVOL

CDX.NA.H

Y

CDX.NA ot

her

CDX.EM indic

esLC

DX.NA

iTraxx L

evX

ABX/CMBX/TABXiTrax

x othe

r

other

CDS indic

esgros

s no

tiona

l vol

ume

(US

D tn

eq.

)

tranche volume (est.) (weekending 11-Sep-09)

index volume (est.) (weekending 11-Sep-09)

17

Index-CDS standardization facilitates trade compression

Source: DTCC, UniCredit Research

Aggregated index CDS gross volume (DTCC TIW, weekly data)

7

8

9

10

11

12

13

14

15

2008-10-31 2009-01-02 2009-03-06 2009-05-08 2009-07-10 2009-09-11end-of-week date

gros

s no

tiona

l vol

ume

(US

D tn

eq.

)

90

110

130

150

170

190

210

230

num

ber o

f con

tract

s (th

sd)

gross notional (index CDS) (LS) number of contracts (RS)

18

The fingerprints of index-portfolio compression trades

Source: DTCC, UniCredit Research; *DTCC only releases data for a particular index series if a minimum activity level is reached within the respective week.

New-trade volumes of iTraxx Europe Main, index & tranched-index (not complete*)

0

50

100

150

200

250

300

350

400

2009-01-02 2009-03-06 2009-05-08 2009-07-10 2009-09-11end-of-week date

iTra

xx M

ain

new

trad

es (i

nd./t

r.) (E

UR

bn)

S 1S 2S 3S 4S 5S 6S 7S 8S 9S 10S 11

19

During the crisis sovereign and financial CDS gained in importance

Single-name corporate and sovereign CDS: breakdown by sector and CDS seller

Source: DTCC, UniCredit Research; effective date: 18 September 2009

0

1

2

3

4

Financ

ials

Indus

trials

Techn

ology

& Tele

com

Consu

mer Goo

ds

Consu

mer Serv

ices

Health

Care

Basic

Materia

lsOil &

Gas

Utilitie

s

Other c

orpora

te CDS

Sovere

igns &

Stat

es

CMBSRMBS

Loan

CDS

Other C

DS

gros

s vo

lum

e (U

SD

tn e

q.) Customer (week ending 18-Sep-2009)

Dealer (week ending 18-Sep-2009)

20

iBoxx € Corporates credit risk – Cash outweighs CDS

Source: Markit, DTCC, UniCredit Research; effective date 24 July 2009; CDS volumes for iBoxx-DTCC entities and single-name CDS only; iBoxx-DTCC entities are iBoxx € issuers which are also listed among the most important single-name CDS reference entities by the DTCC TIW

0

50

100

150

200

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB BB-

bond

not

iona

l am

ount

(EU

R b

n)iBoxx € Financials iBoxx € Non-Financials

0

10

20

30

40

50

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB BB-

CD

S n

et n

otio

nal

(EU

R b

n)

iBoxx € Financials iBoxx € Non-Financials

21

AGENDA

GLOBAL OTC DERIVATIVES

VERY SHORT COURSE ON CDS

CORPORATE AND SOVEREIGN CDS

TRADING CREDITS DURING THE CRISIS

CDS CENTRAL COUNTERPARTIES

22

CDS market only became illiquid in 4Q08

iTraxx Europe index skew (index fair value vs. traded spread)

0

50

100

150

200

250

300

Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09

CD

S s

prea

d (b

p)Fair Value iTraxx Main 5Y

25

Are single-name CDS for trading or hedging?

Aggregate single-name contract volume by maturity

Source: DTCC, UniCredit Research

0

0.5

1

1.5

2

2.5

3

3.5

2009 2014 2019 2024 2029 2034year of scheduled maturity

gros

s no

tiona

l vol

ume

(US

D tn

eq.

)

0

10

20

30

40

50

60

70

Avg

. not

iona

l (U

SD

mn

eq.)

Gross notional (LS) (week ending 18-Sep-2009)

Mean contract size (RS)

26

Single-name CDS market activity: Staying liquid vs. cash-hedging

-100

-80

-60

-40

-20

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014CDS maturity

wee

kly

gros

s no

tiona

l cha

nge

(US

D b

n)

2009-01-09 2009-01-162009-01-23 2009-01-302009-02-06 2009-02-132009-02-20 2009-02-272009-03-06 2009-03-132009-03-20 2009-04-032009-04-10

Aggregate weekly single-name gross vol. changes by year of scheduled termination

Source: DTCC, UniCredit Research.

27

Single-name CDS market activity: 5-year is king

-250

-200

-150

-100

-50

0

50

100

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019CDS maturity

wee

kly

gros

s no

tiona

l cha

nge

(US

D b

n)

2009-01-09 2009-01-16

2009-01-23 2009-01-30

2009-02-06 2009-02-13

2009-02-20 2009-02-27

2009-03-06 2009-03-13

2009-03-20 2009-04-03

2009-04-10

Aggregate weekly single-name gross vol. changes by year of scheduled termination

Source: DTCC, UniCredit Research.

30

AGENDA

GLOBAL OTC DERIVATIVES

VERY SHORT COURSE ON CDS

CORPORATE AND SOVEREIGN CDS

TRADING CREDITS DURING THE CRISIS

CDS CENTRAL COUNTERPARTIES

31

CDS central counterparty – A simple notion that bears subtleties

A clearinghouse acts as the buyer to every seller and seller to every buyer, reducing the risk of a counterparty defaulting on a transaction. It also provides one location for regulators to gain insight into traders’ positions (and possibly their prices).Assuming the existence of 2 CCPs and around 20 major dealers, the number of bilateral relationships is reduced from 190 to 40 by using the CCP CDS settlement model.The schematic view depicted above hides the complexities that are associated with switching from one regime to the other: Credit event settlement, efficient and prudent margining/risk management, trading model.

Major CDS DealerMajor CDS DealerCentral Counterpart Major CDS DealerCentral Counterpart Major CDS Dealer

Purely bilateral trading and settlement Central counterparty clearing of CDS

CDS central counterparty

32

ICE Trust US cleared USD 2.1tn CDS to date

Source: ICE Trust US, ICE Clear Europe, UniCredit Research

0

60

120

180

240

300

2009-03-27 2009-05-01 2009-06-05 2009-07-10 2009-08-14 2009-09-18

wkl

y gr

oss

notio

nal

(US

D b

n)

0

0.6

1.2

1.8

2.4

3

wkl

y co

ntra

cts

(thsd

)Cleared CDX.NA CDS (USD bn)Number of cleared CDX contracts (RS)

0

40

80

120

160

200

2009-03-27 2009-05-01 2009-06-05 2009-07-10 2009-08-14 2009-09-18

wkl

y gr

oss

notio

nal

(EU

R b

n)

0

0.6

1.2

1.8

2.4

3

wkl

y co

ntra

cts

(thsd

)Cleared iTraxx Europe CDS (EUR bn)Number of cleared iTraxx contracts (RS)

33

On-the-run iTraxx Europe avg weekly turnover exceeds EUR 40bn

Weekly turnover in the most liquid euro-denominated CDS: iTraxx Europe S11

Source: DTCC, UniCredit Research

-160

-120

-80

-40

0

40

80

2009-03-27 2009-05-01 2009-06-05 2009-07-10 2009-08-14 2009-09-18end-of-week date

CD

S-n

otio

nal w

kly

turn

over

(EU

R b

n)

iTraxx Europe S11 (new trades)

iTraxx Europe S11 (trade terminations)

34

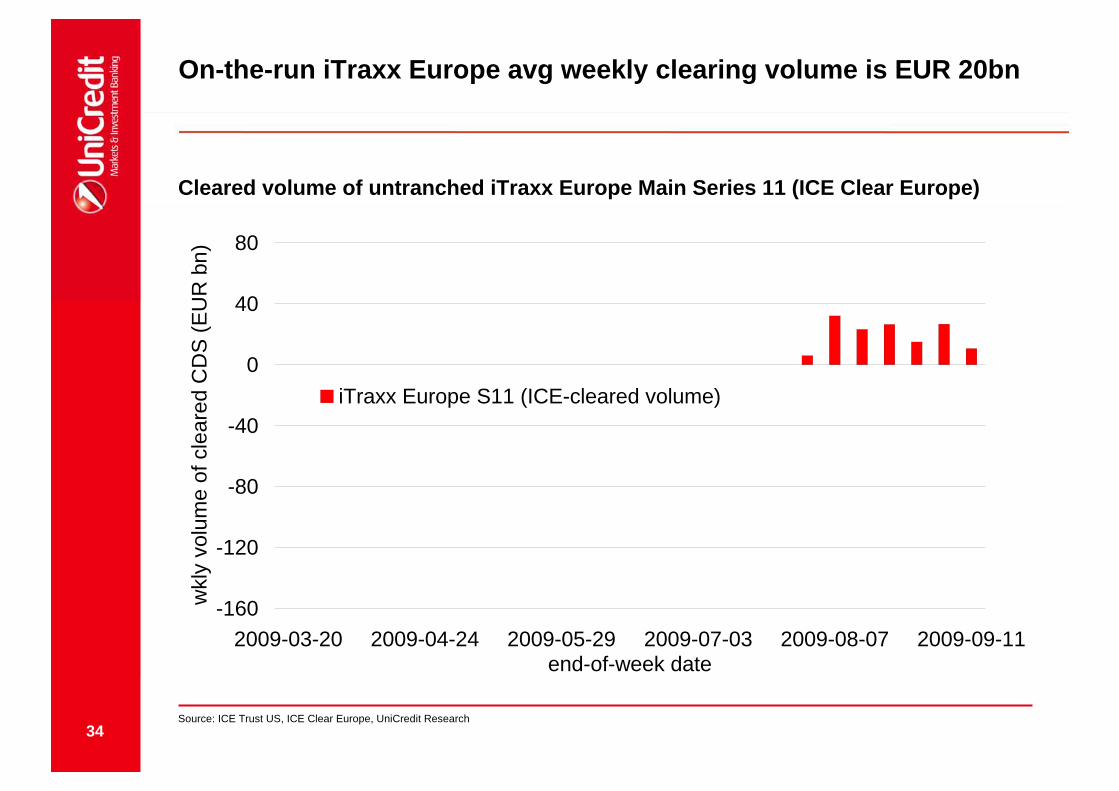

On-the-run iTraxx Europe avg weekly clearing volume is EUR 20bn

-160

-120

-80

-40

0

40

80

2009-03-20 2009-04-24 2009-05-29 2009-07-03 2009-08-07 2009-09-11end-of-week date

wkl

y vo

lum

e of

cle

ared

CD

S (E

UR

bn)

iTraxx Europe S11 (ICE-cleared volume)

Cleared volume of untranched iTraxx Europe Main Series 11 (ICE Clear Europe)

Source: ICE Trust US, ICE Clear Europe, UniCredit Research

35

"G15" committed to clearing 80% of historic "eligible" CDS by Oct.

Source: DTCC, ICE Trust US, ICE Clear Europe, UniCredit Research; effective date is 18 September 2009

0 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 2400 2600 2800

CDX.NA.IG

CDX.NA.IG.HVOL

CDX.NA.HY

iTraxx Europe

iTraxx Europe HiVol

iTraxx Europe Crossover

cumulative cleared CDS notional (USD bn)

S8 S9 S10 S11 S12

0 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 2400 2600 2800

CDX.NA.IG

CDX.NA.IG.HVOL

CDX.NA.HY

iTraxx Europe

iTraxx Europe HiVol

iTraxx Europe Crossover

DTCC total gross CDS volume (USD bn)

S8 S9 S10 S11 S12

36

How many single-name CDS will be offered by CCPs?

0%

20%

40%

60%

80%

100%

0 250 500 750 1000 1250no. of ref. names / underlying indices (sorted by gross notional)

gros

s no

tiona

l (%

of t

otal

vol

ume)

0

3

6

9

12

15

18

21

24

27

gros

s no

tiona

l (U

SD

tn e

quiv

.)

cumulative volume (single-name, CDX.NA and iTraxx CDS)

Source: DTCC, UniCredit Research; effective date 3 April 2009

CDS central clearing

Top-500 CDS references (indices, single-names) represent ~80% of gross volume

37

Buy-side access to central clearing will be launched in October 09

Non-dealers get access to ICE via account seggregation, separating the customers' margin payments and positions from those of their dealers.Who is eligible to become an ordinary clearing member?How many clearing houses will emerge for CDS?Will regulators sanction bilateral trades among non-dealers?

Source: ECB, UniCredit Research

38

UniCredit GroupMarkets & Investment BankingBayerische Hypo- und Vereinsbank AG

Dr. Tim BrunneSenior Credit StrategistCredit Strategy & Structured Credit ResearchUniCredit ResearchTel. +49 89 378 13521 – Fax +49 89 378 33 [email protected]

ImprintMarkets & Investment BankingBayerische Hypo- und Vereinsbank AGArabellastrasse 12D-81925 Munich

Your contacts

Some of our publications:

Global Credit ResearchDaily Credit Briefing (8:45 AM CET)Euro Credit Pilot (monthly)

Credit Strategy & Structured Credit ResearchCredit Strategy Update, Strategy View, Strategy FlashCredit Strategy SpecialSecuritization Market Watch

39

Disclaimer

The information in this publication is based on carefully selected sources believed to be reliable but we do not make any representation as to its accuracy or completeness. Any opinions herein reflect our judgement at the date hereof and are subject to change without notice. Any investments discussed or recommended in this report may be unsuitable for investors depending on their specific investment objectives and financial position. Any reports provided herein are provided for general information purposes only and cannot substitute the obtaining of independent financial advice. Private investors should obtain the advice of their banker/broker about any investments concerned prior to making them. Nothing in this publication is intended to create contractual obligations on any of the entities composing UniCredit Markets & Investment Banking Division which is composed of (the respective divisions of) Bayerische Hypo- und Vereinsbank AG, Munich, Bank Austria Creditanstalt AG, Vienna, and UniCredit S.p.A., Rome.Bayerische Hypo- und Vereinsbank AG is regulated by the German Financial Supervisory Authority (BaFin), Bank Austria Creditanstalt AG is regulated by the Austrian Financial Market Authority (FMA) and UniCredit S.p.A. is regulated by both the Banca d'Italia and the Commissione Nazionale per le Società e la Borsa (Consob).

Note to UK Residents:In the United Kingdom, this publication is being communicated on a confidential basis only to clients of UniCredit Markets & Investment Banking Division (acting through Bayerische Hypo- und Vereinsbank, London Branch ("HVB London") and/or UniCredit CAIB Securities UK Ltd. and/or UniCredit CAIB UK Ltd.) who (i) have professional experience in matters relating to investments being investment professionals as defined in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 ("FPO"); and/or (ii) are falling within Article 49(2) (a) – (d) ("high net worth companies, unincorporated associations etc.") of the FPO (or, to the extent that this publication relates to an unregulated collective scheme, to professional investors as defined in Article 14(5) of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 and/or (iii) to whom it may be lawful to communicate it, other than private investors (all such persons being referred to as "Relevant Persons"). This publication is only directed at Relevant Persons and any investment or investment activity to which this publication relates is only available to Relevant Persons or will be engaged in only with Relevant Persons. Solicitations resulting from this publication will only be responded to if the person concerned is a Relevant Person. Other persons should not rely or act upon this publication or any of its contents. The information provided herein (including any report set out herein) does not constitute a solicitation to buy or an offer to sell any securities. The information in this publication is based on carefully selected sources believed to be reliable but we do not make any representation as to its accuracy or completeness. Any opinions herein reflect our judgement at the date hereof and are subject to change without notice. We and/or any other entity of the UniCredit Markets & Investment Banking Division may from time to time with respect to securities mentioned in this publication (i) take a long or short position and buy or sell such securities; (ii) act as investment bankers and/or commercial bankers for issuers of such securities; (iii) be represented on the board of any issuers of such securities; (iv) engage in "market making" of such securities; (v) have a consulting relationship with any issuer. Any investments discussed or recommended in any report provided herein may be unsuitable for investors depending on their specific investment objectives and financial position. Any information provided herein is provided for general information purposes only and cannot substitute the obtaining of independent financial advice. HVB London is regulated by the Financial Services Authority for the conduct of investment business in the UK as well as by BaFIN, Germany. UniCredit CAIB Securities UK Ltd., London, and UniCredit CAIB UK Ltd., London, two subsidiaries of Bank Austria Creditanstalt AG, are authorised and regulated by the Financial Services Authority.Notwithstanding the above, if this publication relates to securities subject to the Prospectus Directive (2005) it is sent to you on the basis that you are a Qualified Investor for the purposes of the directive or any relevant implementing legislation of a European Economic Area ("EEA") Member State which has implemented the Prospectus Directive and it must not be given to any person who is not a Qualified Investor. By being in receipt of this publication you undertake that you will only offer or sell the securities described in this publication in circumstances which do not require the production of a prospectus under Article 3 of the Prospectus Directive or any relevant implementing legislation of an EEA Member State which has implemented the Prospectus Directive.

Note to US Residents:The information provided herein or contained in any report provided herein is intended solely for institutional clients of UniCredit Markets & Investment Banking Division acting through Bayerische Hypo- und Vereinsbank AG, New York Branch and UniCredit Capital Markets, Inc. (together "HVB") in the United States, and may not be used or relied upon by any other person for any purpose. It does not constitute a solicitation to buy or an offer to sell any securities under the Securities Act of 1933, as amended, or under any other US federal or state securities laws, rules or regulations. Investments in securities discussed herein may be unsuitable for investors, depending on their specific investment objectives, risk tolerance and financial position. In jurisdictions where HVB is not registered or licensed to trade in securities, commodities or other financial products, any transaction may be effected only in accordance with applicable laws and legislation, which may vary from jurisdiction to jurisdiction and may require that a transaction be made in accordance with applicable exemptions from registration or licensing requirements.All information contained herein is based on carefully selected sources believed to be reliable, but HVB makes no representations as to its accuracy or completeness. Any opinions contained herein reflect HVB's judgement as of the original date of publication, without regard to the date on which you may receive such information, and are subject to change without notice. HVB may have issued other reports that are inconsistent with, and reach different conclusions from, the information presented in any report provided herein. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them. Past performance should not be taken as an indication or guarantee of further performance, and no representation or warranty, express or implied, is made regarding future performance. HVB and/or any other entity of UniCredit Markets & Investment Banking Division may from time to time, with respect to any securities discussed herein: (i) take a long or short position and buy or sell such securities; (ii) act as investment and/or commercial bankers for issuers of such securities; (iii) be represented on the board of such issuers; (iv) engage in "market-making" of such securities; and (v) act as a paid consultant or adviser to any issuer.The information contained in any report provided herein may include forward-looking statements within the meaning of US federal securities laws that are subject to risks and uncertainties. Factors that could cause a company's actual results and financial condition to differ from its expectations include, without limitation: Political uncertainty, changes in economic conditions that adversely affect the level of demand for the company‘s products or services, changes in foreign exchange markets, changes in international and domestic financial markets, competitive environments and other factors relating to the foregoing. All forward-looking statements contained in this report are qualified in their entirety by this cautionary statement.

UniCredit Markets & Investment Banking DivisionBayerische Hypo- und Vereinsbank AG, Munich; Bank Austria Creditanstalt AG, Vienna and UniCredit S.p.A., Romeas of 28 September 2009