Chain reactionForces shaping the retail supply chain today

Contents3 Executivesummary

5 Thesupplychaintoday

6 Brexitbites

10 Forcesshapingthesupplychain

14 Changingseasons

16 Shiftinggeographies

18 Thefulfilmentchallenge

20 Theethicaldimension

22 Strategiesforsuccess

24 Casestudy:JohnLewis

26 Abouttheauthor

ThisreportwascomposedfromtwopiecesofresearchconductedbyConluminoforBarclays.Themajorityofthereportwasproducedfrompre-EUreferendumresearchandapostEUreferendumsurveywasconductedforthe‘Brexitbites’.

Allcontenthasbeenresearched,developedandproducedbyConluminoattherequestofBarclaysforthepurposeofthisreport.Allcharts,dataandstatisticsfeaturedinthisreportaretheproductofthisresearch.

Allrightsreserved.

www.conlumino.com

2of26

Executive summaryEnsuringacost-effectivesupplychainisakeychallengeforretailersinthefaceofchangingconsumerbehaviour.

Thesupplychainisclearlycriticaltobusinessperformanceinacompetitiveretailmarketplace.Soit’snosurprisethatoursurveyofretailersrevealsthatprotectingprofitmarginsistheirtopsupplychainpriority.Thisisfollowedcloselybyensuringstabilityandmaintainingagoodreputationonethicalissues.

Thereiscertainlyroomforimprovementintheirsupplychains,accordingtoourrespondents.Closetotwothirds(63%)saytheirsupplychainsarenotveryornotatallcost-effective,whileamajoritybelievetheycouldbemoreefficientandnimble.

Thescaleoftheimpactretailersexpectthereferendumresulttohaveontheirsupplychainsgivesamixedpicture.Althoughhalf(52%)thinkthattheirbusinessisunpreparedforBrexit,asmallmajority(56%)actuallythinkthatBrexitwillhavenorealimpact(41%)orapositiveimpact(15%)ontheirsupplychain.

Changingshoppingpatterns

Ourresearchshowsthatconsumers‘travel’anaverageof6,281miles*whileshoppingonlineeachyear–andtheyexpectever-fasterdeliveryandawiderrangeofdeliveryoptions.Copingwithdeliveryofonlineordersfromoverseasisamajorsupplychainchallenge.Despitetheprevalenceofonlineshopping,manyofourretailerrespondentssaytheyarestillgettingtogripswiththeimpactofonlineontheiroperations.

Average

Hard-to-predictdemandisanotherkeyforceforchange,drivenbymoreunusualweatherpatterns,theincreasedfrequencyandintensityofseasonalpromotionsandotherchangesinshoppinghabits.Moreerraticweather,inparticular,ismakingitincreasinglydifficultforretailerstomeetcustomerneeds.Inaddition,theuseofmultipletouchpointsandchannelsbyconsumersisincreasingthecomplexityofsupplychains.

distancefromhomepeoplehavetravelledtoshopovertheyearsMilesforeachyear,shopincludesresearching,browsingandbuying

15.6 miles

42.1 miles

49.1 miles

358.1 miles

6,281 miles

1985

1955

1995

2005

2015

*Conluminoresearch.

3of26

Withincreasedcompetitionforashareofconsumerspendingfromotherleisurepursuits,consumersbecomesavvier,expectingasteadyflowofnewretailproductsandexperiencestokeepthemcomingback.Surveyrespondentshighlighttheincreasingimportanceofreactingtotrends,with81%offashionretailers,forexample,sayingthatfashioncycleshavebecomefaster;mostbelievethiswillaccelerateinthefuture.

BuyingBritish

BuyingfashiongoodsmadeinBritainisfairlyimportanttomostoftheconsumersinoursurveyandamajority(53%)ofretailerssayitisnoweasiertomanufactureproductsintheUK.However,mostretailersinoursurveysaythecostofbringingproductionbacktotheUKisprohibitiveandonlyaboutathirdsaythattheyhaveactuallydoneso.

Despitehighercosts,ourpost-referendumsurveyshowsthattheUKisnowexpectedtobenefitfromarenewedfocusasasourcingdestination,withathird(32.4%)ofretailerssurveyedexpectingtoincreasetheirdomesticpurchasingactivity.

Moredeliveryoptions

Retailersareincreasingthenumberofdeliveryandcollectionoptionsfortheircustomersandplantoaddmoreoverthenextfewyears.Whileconsumerssaytheywanttheseextraoptions,thereisconsiderablereluctancetopayforthem,withthemajorityofshoppers(64%)sayingthatdeliverychargesarealreadytoohigh.Oursurveyhighlightslackofflexibilityofdeliverytimesandpoorreliabilityasconsumers’maincriticisms.

Click-and-collectservicesfromretailstores,whichcanprovidealower-costalternativetodelivery,tendtoberatedmorefavourablybyconsumersandareincreasinglyimportanttoshoppersandretailersalike,accordingtorespondents.

Ourpost-referendumsurveyresultssuggestthat,broadlyspeaking,retailersappearmorelikelytotakeahitonmarginsorabsorbhighercostsbystreamliningthesupplychainormakingsavingselsewherethantopassonhighercoststocustomers.

Ethicalpriorities

Oursurveyshowsthatminimisingenvironmentalimpactsandmeetingcorporatesocialresponsibilitytargetsarekeyissuesinfluencingretailersandthisislikelytocontinueinthefuture.

Consumersandretailersgenerallyagreeontheethicalconcernstheycaremostabout:childlabour,theimpactonlocalcommunitiesandworkingconditionsarethetopissuesforbothretailersandconsumers,followedbyfactorslikepollutionandclimatechange.Youngerconsumerstendtobemoreconcernedaboutethicalissuesthanolderagegroupsandalsomorescepticalaboutretailers’ethicalpolicies.

Despitethis,consumersadmitthattheirshoppingbehaviourisnotalwaysdrivenbytheseethicalconcerns.Forexample,nearlytwothirds(61%)saythattheytendtoforgetaboutethicaltreatmentofworkerswhenbuyingproducts.Whileourretailersurveyshowsthatrespondentsgenerallyacknowledgethelimitedimpactofethicalconcernsonactualbuyingpatterns,theyhaveneverthelessalmostalltaken,orplantotake,someformofethicalactionovertheirsupplychains.However,manyadmitthatthelengthofthesupplychaincanlimittheircontrolovertheseissues.

IanGilmartinHeadofRetailandWholesaleCorporateBankingBarclays

Prepared As prepared

as we can be13.2%

35.3%Unprepared

51.5%

How preparedisyourbusinessforBrexitregardingsupplychain?

4of26

The supply chain todayRetailers highlight the need for more cost-effective supply chains to help protect profit margins.

Protecting profit margins is the number one priority for 64% of retailers, according to our survey, underlining the perennial challenge of maintaining cost-effectiveness.

While the views of our respondents on the supply chain are mixed, it’s clear that retailers are far from giving themselves a clean bill of health. Nearly two thirds of respondents say their supply chains are not very or not at all cost-effective, while a majority also say they could be more efficient and nimble.

Looking ahead

Besides maintaining margins, our pre-referendum survey research shows that top priorities for the year ahead include ensuring stability (60%), closely followed by protecting ethical reputation (57%). Also mentioned as goals for 2016 are quality control (41%), speed of supply (38%) and foreign exchange rates (32%).

However, the post-referendum survey suggests slight shifts in these priorities, with FX rates becoming the top concern ahead of labour costs, streamlining supply chain and import costs.

Forecasting and predicting erratic demand is a factor that impacts on all retailers. Our research shows this is particularly true of food and drink retailers, who rate it as the second most important issue after protecting profit levels. Food sector respondents also identify the importance of transparency and traceability in the supply chain and minimising wastage and loss as key issues.

CompletelyVery

Not veryNot at all

Somewhat

ROBUST NIMBLECOST-

EFFECTIVE EFFICIENTTIME-

SENSITIVE

8%

10%

61%

16%

5%

11%

39%

41%

25%

38%

22%

6%

14%

44%

31%

12%

19%

28%

32%

9%

10%

1%3%

6% 9%

Taking action

Given the various supply chain challenges identified in this report, it is not surprising that the vast majority of retailers say they are taking some form of action. Most commonly this involves working more closely with suppliers to find cost savings and efficiency gains – 60% of our retailer respondents say this will be an area of future focus. Collaboration with suppliers to identify efficiencies will clearly be a key challenge for the sector going forward.

How would

One recent trend has seen retailers adjusting trading terms to take control of goods closer to the point of manufacture. This allows them to better control freight costs, which has been particularly advantageous with falling oil prices.

Some retailers are also investing in fulfilment centres in the UK and overseas to lower distribution costs. This investment in the supply chain creates efficiencies that can be passed on to increasingly demanding consumers.

you describe your supply chain?

5 of 26

Brexit bitesConcernsoverthepost-referendumeconomycouldtransformretailers’approachtosupplychainmanagement.

OursurveyconductedfollowingtherecentEUreferendumresultsuggeststhatBrexithasnotfoundfavourwithretailers.

Anunexpectedresult

Theresultofthereferendumappearstohavecomeasasurprisetolotsofpeopleandretailersarenoexception.Eventhoughoverathirdofthosesurveyedafterthereferendum(35.3%)saytheirsupplychainprocessesareaspreparedastheycanbeatthepresenttime,overhalfoftherespondents(51.5%)feeltheirsupplychainsareunpreparedforBrexit.Onlyasmallminority(13.2%)believetheyarefullyreadyforseparationfromtheEuropeanUnion(EU),suggestingthatthesector,aswithmostotherbusinessesinthedomesticmarkets,iswaitingforclarityastothelong-termconsequencesoftheresult.

Theoverallattitudeisoneofcaution.Lessthanafifth(14.7%)expectBrexittobepositivefortheirsupplychain–while,incomparison,almosthalf(44.1%)anticipateanegativeimpact.

How willthefollowingaspectsofyoursupplychainbeimpactedbyBrexit?

7.4%

4.4%

2.9%

30.9%

13.2%

2.9%

11.8%

27.9%

17.6%

NEGATIVEPOSITIVE NEUTRAL

64.7%

55.9%

69.1%

20.6%

27.9%

80.9%

16.2%

45.6%

42.6%

27.9%

39.7%

27.9%

48.5%

58.8%

16.2%

72.1%

26.5%

39.7%

Finding enough labour for supply chain operations

Finding the right quality of staff for supply chain operations

Cost of importing goods

Cost of exporting goods

Complexity of imports and exports

Managing foreign exchange rates

Speed of the supply chain

Dealing with administration and red tape

Selling products overseas

However,noteveryoneissopessimisticandmanyhaveaneutralattitudetowardsBrexit.Asignificantproportion(41.2%)expectBrexittohavenorealeffect,whilealmostathird(29.4%)believeitwillhaveonlyaslightlynegativeimpact.

Thehighproportionofneutralresponsessuggeststhatatleastsomeretailershavemitigationplansalreadyinplace,withuncertaintythebiggestcurrentconcern.

OverhalfofthosesurveyedafterthereferendumsaytheirsupplychainsareunpreparedforBrexit.

6of26

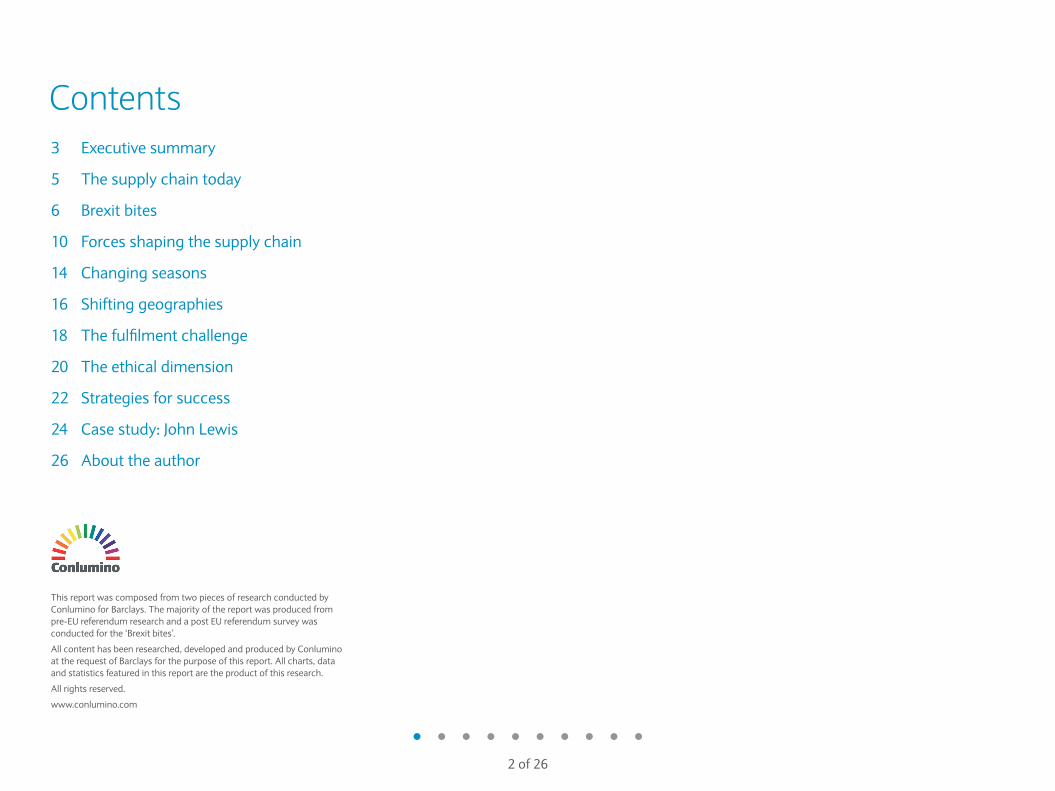

70.6Hedging currency

11.8Setting up separate UK and European supply chains

17.6Reassessing product mixes and product ranges

1.5Closing down existing selling operations in Europe

76.5Streamlining and cutting supply chain costs

10.3Opening new selling operations in Europe

14.7None of these

30.9Changing suppliers

16.2Relocating parts of your supply chain operation

Moving manufacturing capacity to different geographies

13.2

27.9Sourcing from different countries

ForeignExchange(FX)effect

Accordingtoourpost-Brexitsurvey,themostimmediateconcernsarefocusedaroundcurrency,with81%ofretailersexpressingnegativesentimentovermanagementofFXrates.Whiledepreciationofsterlinghasbeenoneofthemoreimmediateeffectsofthereferendumresult,thiscouldalsohavealonger-termimpact.Manyretailersarelikelytobereasonablywell-hedgedgoingintonextyear,meaningthattherealconsequencescouldbeseenfrommid-2017onwards.Hedgingcurrencyisthereforeunsurprisinglythetoppriorityforourrespondentspost-referendum,with71%highlightingitasanactionforimmediatereview.

Whatwillyou bereviewingoractingoninlightofthevotetoleavetheEuropeanUnion(%)?

However,whileacheapersterlingwillinevitablyhaveamajoreffectonmanyretailers,particularlyagainsttheUSdollarandtheeuro,itmaynotbealldoomandgloomforthesector.

Currencyvolatilitywillhaveaverydifferentimpactoneachretailer,dependingontheircircumstances.Thosethatareheavilyreliantonimportswillnodoubtbelookingtoexploitopportunitiestomarkettheirproductsmorewidelyinnewmarkets,whilemajorexporterswithalargelydomesticsupplychaincouldbenefitfromcurrencymovementsintheshorterterm.

7of26

Costconsequences

RetailersmightbeworriedaboutpotentialsupplychaincostincreasesinthewakeofaUKdeparturefromtheEUbut,accordingtothelatestsurvey,theresultsmaybelessseverethanexpected.Themajorityofretailerssurveyed(58.8%)expectthatthecostsofsupplychainmanagementwillremainthesameorincreaseslightly,whilenearly15%seeapositiveimpactfromBrexitinbringingtheirsupplychaincostsdown.

Incomparison,however,overtwothirds(69.1%)ofretailersbelievethatBrexitcouldhaveanegativeimpactontheirimportcosts.Asimilarproportion(64.7%)areworriedaboutfindingadequatelabourofsuitablequalityfortheirsupplychainoperations,possiblyresultinginhigherrecruitmentandhumanresourcescosts.

OvertwothirdsofretailersbelievethatBrexitcouldhaveanegativeimpactontheirimportcosts.

Eventhough42%ofrespondentsthinkthatsellingproductsoverseasmaybecomemoreofachallenge,possiblyduetotheuncertaintyaroundfreetradewiththeEU,athirdofrespondents(30.9%)expectexportcoststofall,bringingopportunitiesforhighermarginsfromoverseasmarkets.

Howwillyourespondtothecostchanges?

Streamline the supply chain to

mitigate cost increases

69.1%

Renegotiate terms with suppliers to reduce

fees/costs

38.2%Absorb the

cost increases internally and take a hit on margins

52.9% Make savings elsewhere to offsetthe cost increases

64.7%

Increase the price of products for customers

30.9%Outsource some

aspects of the supplychain to save money

19.21%Increase delivery and fulfilment costs

to customers

35.3%

8of26

Spreadingtheimpact

Inthecurrentclimateofuncertainty,mostretailersappearkeentoabsorbthecostimpact,ratherthanpassingitontotheirconsumers.Asignificantmajority(76.5%)plantostreamlinetheirsupplychains,andoverhalf(52.9%)ofretailerssurveyedexpecttotakeahitonmarginsbyabsorbingcostincreasesthemselves.

Only30.9%saytheyplantoincreaseproductprices,whileasimilarnumber(35.3%)saytheymightconsiderincreasingdeliveryandfulfilmentcostsforcustomers.Anotablemajority(64.7%)insteadhopetospreadthecostimpactandmakesavingselsewheretooffsethighercosts.

Thekeyhereisriskmanagementandmitigation,andcompaniesshouldbecarefullyconsideringtheirnextmove.

Location,location,location

AsretailersseektomitigatetheimpactofBrexit,anewevaluationofsupplierlocationandpurchasingactivityislikely.Aroundathirdofretailers(30.9%)saytheyarethinkingofchangingtheirsuppliers.

Beforethereferendum,EasternEuropewasakeyregionofinterestforpurchasers,with48%ofretailersconsideringapotentialincreaseinsourcinginthisregion.Inourpost-Brexitsurvey,however,thissentimenthas,unsurprisingly,swungtheotherway,withasharpdropininterest–almosthalfofrespondents(42.6%)expecttoseeanoveralldeclineinEuropeanpurchasingactivity.

Indiaisnowlookinglikethemostpopulardestination,withover51%ofretailersexpectingtheirpurchasingactivityintheregiontoincrease(comparedto42%beforethereferendum).InterestinChinaandSoutheastAsiaassourcingdestinationsforUKretailershasalsorecentlyincreased.

FortheUK,oursurveysuggeststhatBrexitmayalsoreinforceatrendtowards‘buyingBritish’.WhileproductionintheUKmightbemoreexpensive,athird(32.4%)ofretailersnowplantoincreasetheirdomesticsourcingactivitypost-Brexit.

Lookingahead

Inthelongerterm,thereareofcourseawiderangeofBrexitconsequencesthatretailbusinesseswillneedtoconsiderintheirforwardplanning,notleastthepossibilityofreducedoverallconsumerpurchasingpowerintheeventofawidereconomicdownturn.

Thesechallengeswillbecompoundedbyuncertaintyoverdomesticandforeigninvestmentandthelikelyintroductionofnewtariffsandlegislation.ThelikelyrestrictionsonfreemovementoflabourandthepossibilityofresultingwageinflationwillnodoubtremainamajorconcerntoUKretailersuntilaclearerpictureemerges.

However,thepossibleremovalofsomebarrierstotradewiththerestoftheworldprovidesopportunitiesforgreaterexpansionintonewmarketsandhigherpenetrationofexistingones.Withnewplansforreassessingproductoperationsandstreamliningcostsinthewakeofthereferendumresult,thechangescouldevenactasapositivecatalystforincreasedefficiencywithinthesupplychain.

ThelikelyrestrictionsonfreemovementoflabourandthepossibilityofresultingwageinflationwillnodoubtremainamajorconcerntoUKretailers.

9of26

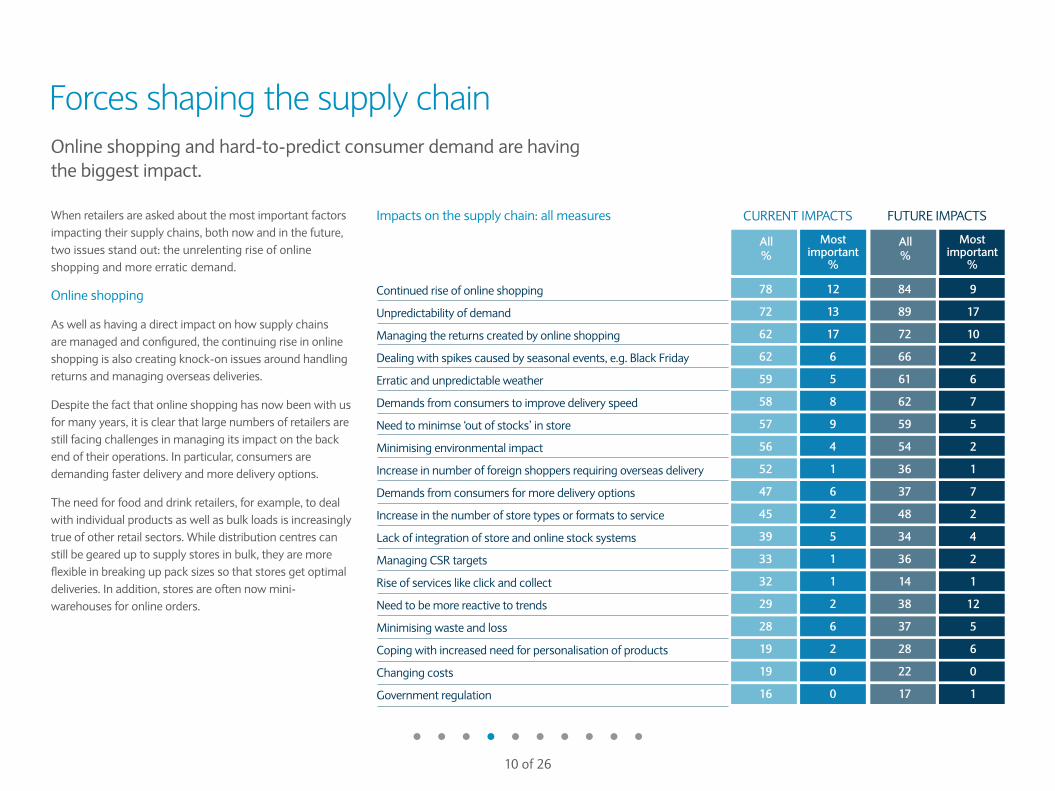

78

72

62

62

59

58

57

56

52

47

45

39

33

32

29

28

19

19

16

Mostimportant

%

CURRENT IMPACTS

All%

Mostimportant

%

FUTURE IMPACTS

All%

12

13

17

6

5

8

9

4

1

6

2

5

1

1

2

6

2

0

0

84

89

72

66

61

62

59

54

36

37

48

34

36

14

38

37

28

22

17

9

17

10

2

6

7

5

2

1

7

2

4

2

1

12

5

6

0

1

Continued rise of online shopping

Unpredictability of demand

Managing the returns created by online shopping

Dealing with spikes caused by seasonal events, e.g. Black Friday

Erratic and unpredictable weather

Demands from consumers to improve delivery speed

Need to minimse ‘out of stocks’ in store

Minimising environmental impact

Increase in number of foreign shoppers requiring overseas delivery

Demands from consumers for more delivery options

Increase in the number of store types or formats to service

Lack of integration of store and online stock systems

Managing CSR targets

Rise of services like click and collect

Need to be more reactive to trends

Minimising waste and loss

Coping with increased need for personalisation of products

Changing costs

Government regulation

Forces shaping the supply chainOnlineshoppingandhard-to-predictconsumerdemandarehavingthebiggestimpact.

Whenretailersareaskedaboutthemostimportantfactorsimpactingtheirsupplychains,bothnowandinthefuture,twoissuesstandout:theunrelentingriseofonlineshoppingandmoreerraticdemand.

Onlineshopping

Aswellashavingadirectimpactonhowsupplychainsaremanagedandconfigured,thecontinuingriseinonlineshoppingisalsocreatingknock-onissuesaroundhandlingreturnsandmanagingoverseasdeliveries.

Despitethefactthatonlineshoppinghasnowbeenwithusformanyyears,itisclearthatlargenumbersofretailersarestillfacingchallengesinmanagingitsimpactonthebackendoftheiroperations.Inparticular,consumersaredemandingfasterdeliveryandmoredeliveryoptions.

Theneedforfoodanddrinkretailers,forexample,todealwithindividualproductsaswellasbulkloadsisincreasinglytrueofotherretailsectors.Whiledistributioncentrescanstillbegeareduptosupplystoresinbulk,theyaremoreflexibleinbreakinguppacksizessothatstoresgetoptimaldeliveries.Inaddition,storesareoftennowmini-warehousesforonlineorders.

Impactsonthesupplychain:allmeasures

10of26

17.7

8.1

68.3

40.6

ONE TWO

4.1

8.49.9

39.1

0.03.8

THREE FOUR FIVE+

Patterns of demand

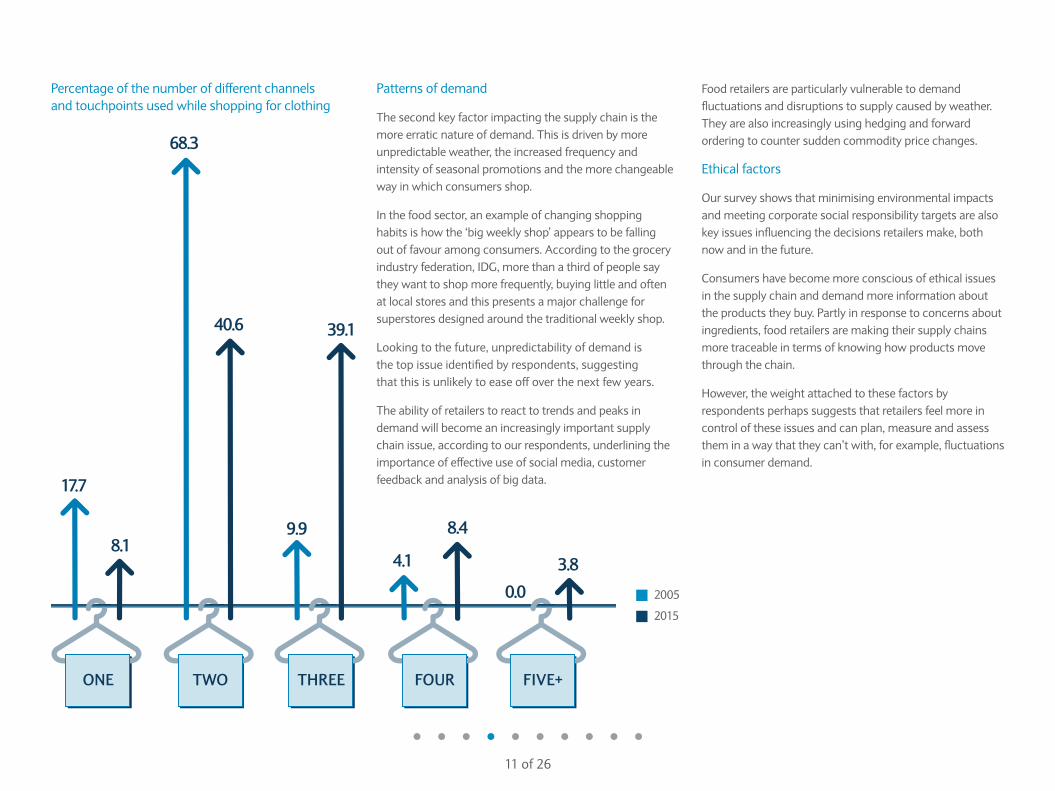

The second key factor impacting the supply chain is the more erratic nature of demand. This is driven by more unpredictable weather, the increased frequency and intensity of seasonal promotions and the more changeable way in which consumers shop.

In the food sector, an example of changing shopping habits is how the ‘big weekly shop’ appears to be falling out of favour among consumers. According to the grocery industry federation, IDG, more than a third of people say they want to shop more frequently, buying little and often at local stores and this presents a major challenge for superstores designed around the traditional weekly shop.

Looking to the future, unpredictability of demand is the top issue identified by respondents, suggesting that this is unlikely to ease off over the next few years.

The ability of retailers to react to trends and peaks in demand will become an increasingly important supply chain issue, according to our respondents, underlining the importance of effective use of social media, customer feedback and analysis of big data.

Percentage of the number of different channels and touchpoints used while shopping for clothing

Food retailers are particularly vulnerable to demand fluctuations and disruptions to supply caused by weather. They are also increasingly using hedging and forward ordering to counter sudden commodity price changes.

Ethical factors

Our survey shows that minimising environmental impacts and meeting corporate social responsibility targets are also key issues influencing the decisions retailers make, both now and in the future.

Consumers have become more conscious of ethical issues in the supply chain and demand more information about the products they buy. Partly in response to concerns about ingredients, food retailers are making their supply chains more traceable in terms of knowing how products move through the chain.

However, the weight attached to these factors by respondents perhaps suggests that retailers feel more in control of these issues and can plan, measure and assess them in a way that they can’t with, for example, fluctuations in consumer demand.

2005

2015

11 of 26

Morewaystoshop

Anotherforceshapingthesupplychainisthatconsumersarenowspoiledforchoiceintermsofhowtheycanshop.Manynowusemultipletouchpointsandchannelswhenbuyingproductslikeclothing.

Evenfoodretailersreportconsumersusingmorenon-traditionalchannelslikeAmazon.Whilethishasincreasedflexibilityforconsumers,ithasalsoincreasedthecomplexityofretailers’supplychains.

Retailersmustnowbepreparedtofulfilproducts,manageinventoryanddealwithreturnsacrossanumberofdifferentchannels.Thisfragmentationhasalsoarguablymadeunderstandingthepatternofdemandfarmoredifficult.

Customerscravingnewness

Oneconsequenceoftheincreasedfrequencyofshoppingandtherelativeeasewithwhichconsumerscanbuythingsonlineisboredom.Inoursurveyofconsumers,55%agreethattheyoftengetboredofusingthesamestoresandbrands.

Oursurveysuggeststhattoday’sconsumersaresomewhatjadedwiththeireverydayretailexperiencesandlookfornewproducts,brandsorexperiencestokeepthemsatisfiedandengaged.Inoursurvey,twothirds(66%)saytheyagreeitfeelsgreattodiscoveranewbrandorproductthattheylike.

Thismeansretailershavetoworkhardtokeepoffersandrangeslookingfreshandnew.Inturn,thisplacesmorepressureonthesupplychaintobequickerandmoreflexible–aparticularchallengeforlargerretailers,comparedtosmaller,independentcompetitors.

However,inthefoodsector,busyconsumersappeartobeputtinglessvalueontherangeofproductchoiceinfavourofanarrowerselectionofmorecarefullychosenproducts.Inresponse,retailersarereducingthenumberofproducts–creatingclarityfortheircustomers,butalsoimprovingefficienciesandeconomiesofscale.

“Customerswantmoreandmore,and thatputspressureonthewholesupplychain.”

Globalretailoptions

Onlineshoppinghasopenedupaworldofchoicetoconsumersthatincludesretailersthousandsofmilesawayandbrandstowhichtheyhaven’tpreviouslyhadaccess.Afifth(20%)ofconsumersinoursurveysaytheypurchasedsomethingonlinefromanoverseasretailerinthelastyear.

Translatedintophysicaldistance,theaverageconsumer‘travelled’anaverageofmorethan6,000mileswhileshoppinglastyear.

Thiscompareswithafigureofjust15.6milesin1955and358.1milesin2005.Forretailers,thismeansthatsupplychainshavetocopewithdeliveringproductsovermuchlongerdistances,includingfromoverseas.

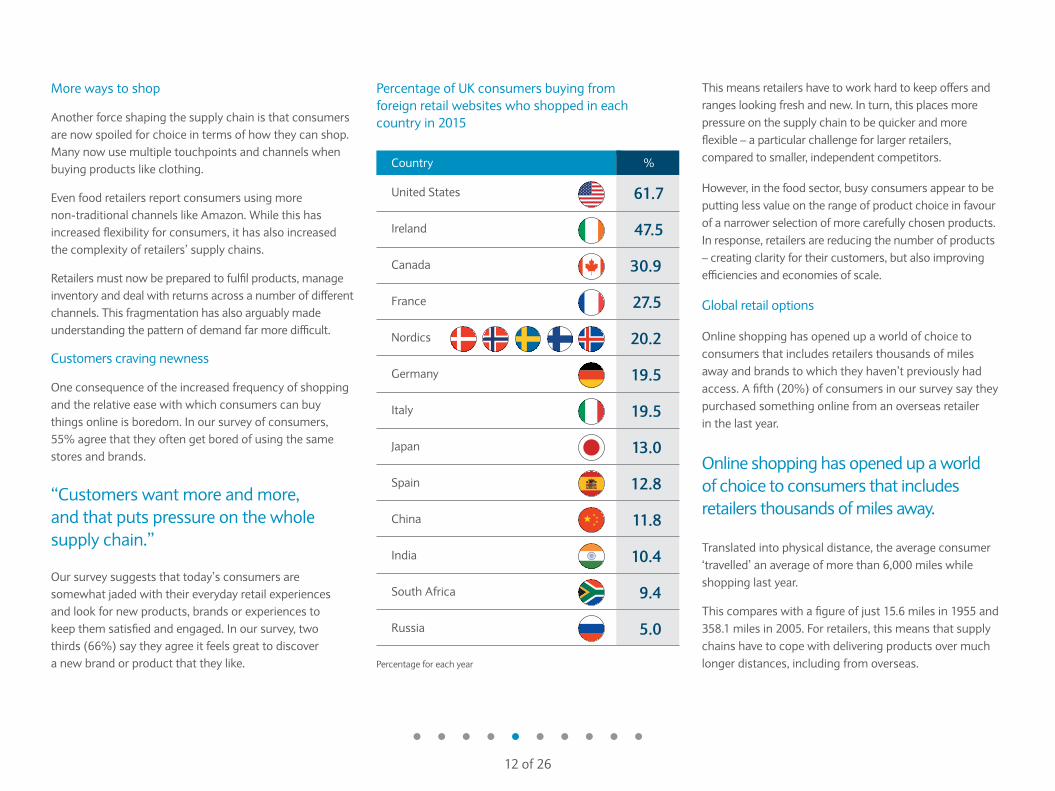

Percentage ofUKconsumersbuyingfromforeignretailwebsiteswhoshoppedineachcountryin2015

Percentageforeachyear

Country %

UnitedStates 61.7

Ireland 47.5

Canada 30.9

France 27.5

Nordics 20.2

Germany 19.5

Italy 19.5

Japan 13.0

Spain 12.8

China 11.8

India 10.4

SouthAfrica 9.4

Russia 5.0

Onlineshoppinghasopenedupaworldofchoicetoconsumersthatincludesretailersthousandsofmilesaway.

12of26

OurresearchshowsthatoftheforeignretailwebsitesusedbyUKconsumers,most(62%)arefromtheUS,followedbyIrelandandCanada.Languagemaybethekeyfactorbehindtheseresults,giventhat,asEnglish-speakingcountries,thesewebsitesaretypicallymostaccessibletoUKconsumers.InthecaseofIreland,proximitytotheUKmayalsoplayarole.UsageofUSandCanadianretailwebsitesisalsoprobablyboostedbythefactthattherearemoreretailersinthosecountriesthatarenotphysicallypresentintheUK.

Distractedconsumers

Non-retailactivitiesareincreasinglycompetingwithretailforconsumers’disposableincome,asevidencedbythefactthatgrowthinspendingonservicesisoutstrippingthatonretailgoods.Retailislosingouttoaraftofleisureactivities:peopleareeatingoutmoreoftenandspendingmoreonentertainmentlikecinema,musicaleventsandartexhibitions.

Similarly,consumersaretravellingmoreoften,mixingshortbreakswithlongerholidays,meaningthatretailspendingisbeingdivertedtowardsthetravelsectorandoverseasretailers.

SpendingonsubscriptionservicessuchasNetflix,AppleMusic,Spotifyandothersgrew6.8%lastyear,whileretail’sshareofconsumerspendinghasslippedfrom39%to31%overthepast10years.*

*Conluminoresearch.

Consumerpriceexpectations

Thereis,ofcourse,constantconsumerpressureforlowerprices.Retailersrespondtothisinpartbytryingtocuttheirsupplychaincosts.Inthefoodsector,ourresearchrevealsthatmostconsumersdonotbelievelowpriceshavemadefoodlesssafe.Aslimmajoritybelievethatithasreducedthequalityoffood.Alargermajoritybelieveithasputpressurefurtherdownthesupplychainonfoodproducers(83%)and,toalesserextent,suppliers(72%).

Peopleareeatingoutmoreoftenandspendingmoreonentertainmentlikecinema,musicaleventsandartexhibitions.

believepricecutsputpressureonfoodproducers believe pricecuts

putpressureonfoodsuppliers

83% 72%

Labourcosts

Ourresearchshowsthatrisinglabourcostsareanincreasinglyimportantfactorinthefoodsector.Thishitsfoodretailersparticularlyhardbecauseoftheircomplex,time-sensitiveandintricatedeliveryandlogisticsnetworks.

Tocounterthis,retailersarefocusingonlabourefficiencies,tryingtoensureitisallocatedwhereitismosteffectiveinthesupplychain,aidedbyimprovedforecasting.

Brexitwillpotentiallyputmorepressureonlabourcosts,giventhatretailershaveconcernsoverthesupplyoflabouraswellasthequalityandsuitability.

13of26

Changing seasonsTraditionalseasonalpatternsarebeingovertakenbyacontinualsearchbyconsumersforsomethingnew.

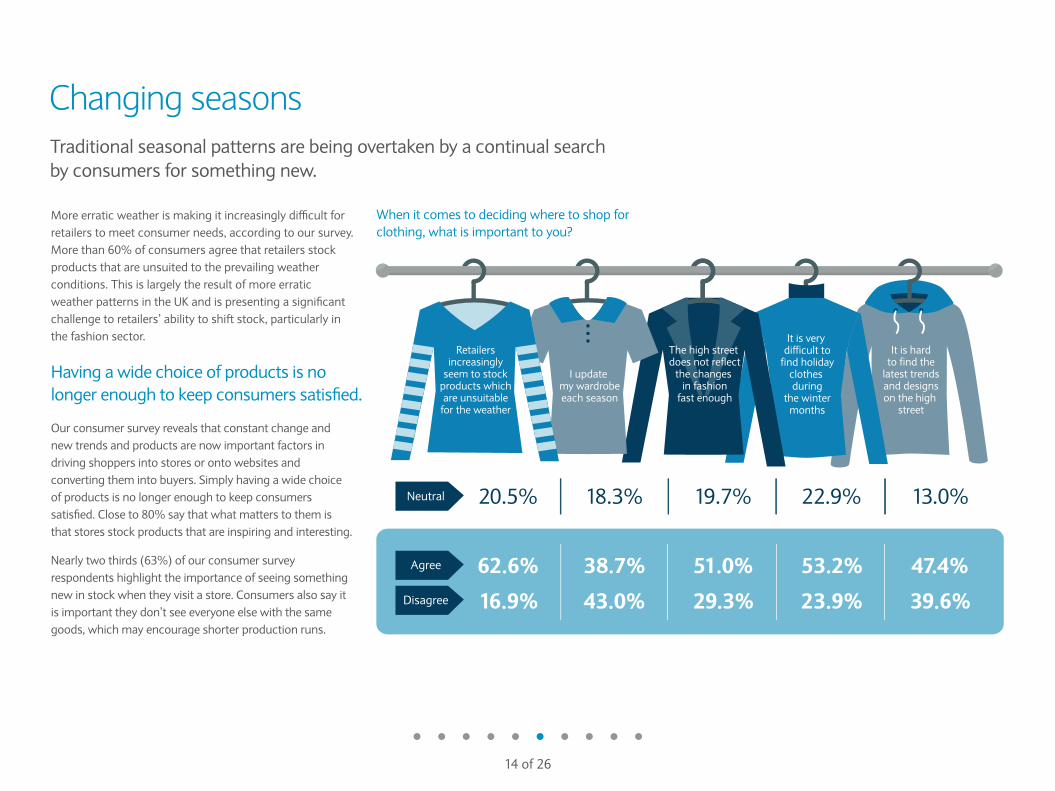

Moreerraticweatherismakingitincreasinglydifficultforretailerstomeetconsumerneeds,accordingtooursurvey.Morethan60%ofconsumersagreethatretailersstockproductsthatareunsuitedtotheprevailingweatherconditions.ThisislargelytheresultofmoreerraticweatherpatternsintheUKandispresentingasignificantchallengetoretailers’abilitytoshiftstock,particularlyinthefashionsector.

Ourconsumersurveyrevealsthatconstantchangeandnewtrendsandproductsarenowimportantfactorsindrivingshoppersintostoresorontowebsitesandconvertingthemintobuyers.Simplyhavingawidechoiceofproductsisnolongerenoughtokeepconsumerssatisfied.Closeto80%saythatwhatmatterstothemisthatstoresstockproductsthatareinspiringandinteresting.

Nearlytwothirds(63%)ofourconsumersurveyrespondentshighlighttheimportanceofseeingsomethingnewinstockwhentheyvisitastore.Consumersalsosayitisimportanttheydon’tseeeveryoneelsewiththesamegoods,whichmayencourageshorterproductionruns.

Retailersincreasingly

seem to stockproducts whichare unsuitable

for the weather

I update my wardrobeeach season

The high street does not reflect

the changes in fashion

fast enough

It is very difficult to

find holidayclothes during

the wintermonths

It is hardto find the

latest trendsand designson the high

street

20.5% 18.3% 19.7% 22.9% 13.0%

62.6% 38.7% 51.0% 53.2% 47.4%

16.9% 43.0% 29.3% 23.9% 39.6%

Agree

Neutral

Disagree

Havingawidechoiceofproductsisnolongerenoughtokeepconsumerssatisfied.

Whenitcomestodecidingwheretoshopforclothing,whatisimportanttoyou?

14of26

Howstronglydoyou agreeordisagreewiththefollowingstatementsaboutseasons?(retailers)

Retailerresponse

Retailers’feedbackseemstochimewithconsumers’.Forexample,inthefashionsectorthereisgrowingrecognitionthattraditionalseasonsarelessrelevant–81%ofretailersnotethatfashioncycleshavebecomefaster,and87%believetheywillspeedupstillfurtheroverthenextfiveyears.

Themajorityoffashionretailersagreetheyneedtobemoreflexibleinthetypeofproductstheyoffer,andthatconstantchangeofproductsontheshopfloorisnowdemandedbyconsumers.Morethanhalfsaythatcostsinfashionsupplychainsareincreasing.

Inaddition,retailersneedtomaintainstrongrelationshipswithadiversegroupofsupplierstobeabletoadapttotrendsandpeaksindemand.

“It’snotimagination:theweatherisweirdnowandit’sgettingworse.Makesithardtoknowwhatstocktocommitto.”

The costs in fashion supply

chains areincreasing

13% 2% 9%14% 18%

42% 93% 73%47% 54%Agree

Neutral

45% 5% 18%39% 28%Disagree

Seasons are increasingly

irrelevantin fashion

now

Consumers now demand

constant change in

the product on the

shop floor

We are producing a lot

more collections each year than

we used to

Seasons are relevant but

we have to be more flexible

in terms of the type of product

we offer

15of26

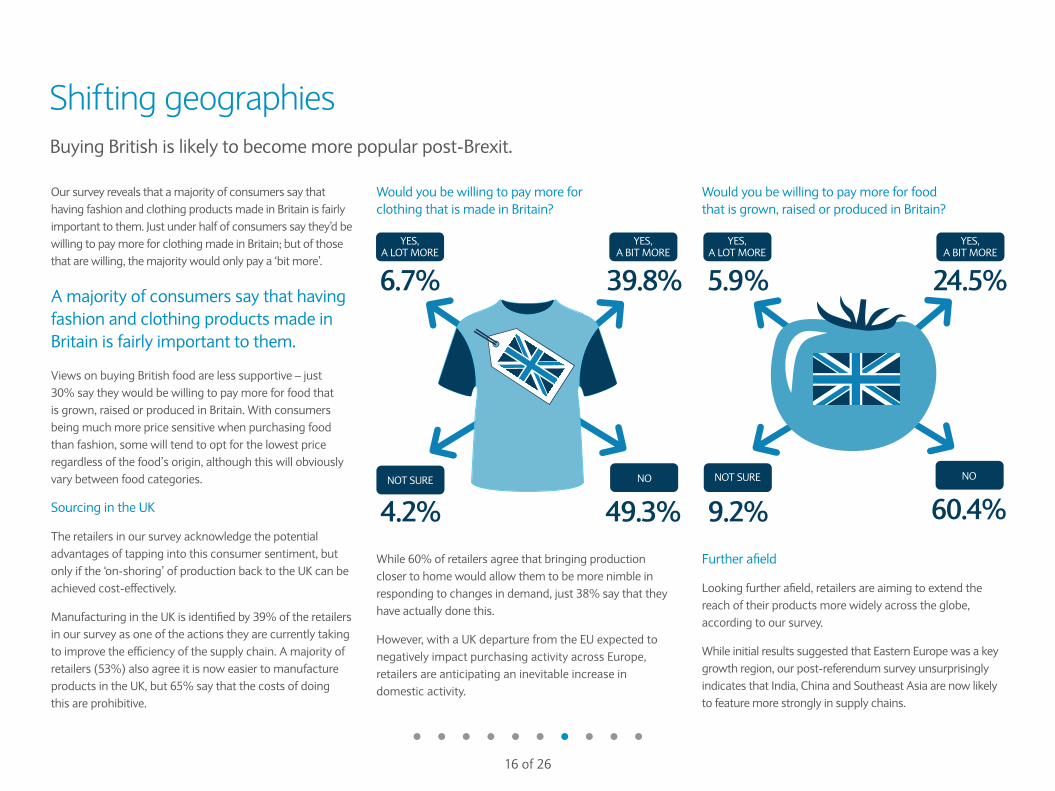

Shifting geographiesBuyingBritishislikelytobecomemorepopularpost-Brexit.

OursurveyrevealsthatamajorityofconsumerssaythathavingfashionandclothingproductsmadeinBritainisfairlyimportanttothem.Justunderhalfofconsumerssaythey’dbewillingtopaymoreforclothingmadeinBritain;butofthosethatarewilling,themajoritywouldonlypaya‘bitmore’.

ViewsonbuyingBritishfoodarelesssupportive–just30%saytheywouldbewillingtopaymoreforfoodthatisgrown,raisedorproducedinBritain.Withconsumersbeingmuchmorepricesensitivewhenpurchasingfoodthanfashion,somewilltendtooptforthelowestpriceregardlessofthefood’sorigin,althoughthiswillobviouslyvarybetweenfoodcategories.

SourcingintheUK

Theretailersinoursurveyacknowledgethepotentialadvantagesoftappingintothisconsumersentiment,butonlyifthe‘on-shoring’ofproductionbacktotheUKcanbeachievedcost-effectively.

ManufacturingintheUKisidentifiedby39%oftheretailersinoursurveyasoneoftheactionstheyarecurrentlytakingtoimprovetheefficiencyofthesupplychain.Amajorityofretailers(53%)alsoagreeitisnoweasiertomanufactureproductsintheUK,but65%saythatthecostsofdoingthisareprohibitive.

While60%ofretailersagreethatbringingproductionclosertohomewouldallowthemtobemorenimbleinrespondingtochangesindemand,just38%saythattheyhaveactuallydonethis.

However,withaUKdeparturefromtheEUexpectedtonegativelyimpactpurchasingactivityacrossEurope,retailersareanticipatinganinevitableincreaseindomesticactivity.

Furtherafield

Lookingfurtherafield,retailersareaimingtoextendthereachoftheirproductsmorewidelyacrosstheglobe,accordingtooursurvey.

WhileinitialresultssuggestedthatEasternEuropewasakeygrowthregion,ourpost-referendumsurveyunsurprisinglyindicatesthatIndia,ChinaandSoutheastAsiaarenowlikelytofeaturemorestronglyinsupplychains.

AmajorityofconsumerssaythathavingfashionandclothingproductsmadeinBritainisfairlyimportanttothem.

WouldyoubewillingtopaymoreforclothingthatismadeinBritain?

Wouldyoubewillingtopaymoreforfoodthatisgrown,raisedorproducedinBritain?

NOT SURE NO

YES,A BIT MORE

49.3%4.2%

YES,A LOT MORE

6.7% 39.8%

NOT SURE NO

YES,A BIT MORE

60.4%9.2%

YES,A LOT MORE

5.9% 24.5%

16of26

Financialframework

Itisimportanttoensurethatasuitablefinancialframeworkisinplacewhenconsideringmovingsupplierbasetoanewdestination.Thereareanumberofsupplychainfinancesolutionsthatretailerscanusetoimproveworkingcapitalandreducetheadditionalrisksassociatedwithcross-bordertrade.Thesesolutionscanincludelookingtoincreasepaymenttermswhileatthesametimetryingtoeasetheburdenthatslowingpaymentshaveonsuppliers.Keyconsiderationsalsoincludereducingtheriskofstockdeliverydelaysorevencompletedeliveryfailureandguardingagainstadversecurrencymovements.

Tradefinancehasbeenanimportantcross-borderinstrumentforretailerslookingtoimplementasupplychainsolution.Agrowingnumberoffirmsarealsoconsidering‘payable-centric’bankproducts,suchastradeloans,supplierfinanceprogrammes,documentarytradefinance

andasset-basedlendingsolutions.However,forsuchaframeworktobesuccessful,allpartiesneedtoworktogethertosetitupandmanagethechange–fromtreasuryandprocurementtosuppliersanddistributors.

Digitisationoftheseproductsvianewtechnologies,suchassupplierfinanceplatforms,SWIFTanddocumentarytradeplatforms,ismakingbusinesseasierforretailers,enablingthemtonegotiatebetterpaymentterms,mitigategoodsdeliveryrisksandreducecosts.

FXrisksandlocalcurrencyinvoicing

UKretailerswithinternationalsupplychainscanbeexposedtoforeignexchangerisk.Companiesneedtobeawareoftherisksandidentifytheirunderlyingcurrencyexposuresandbusinessvulnerabilities.Evenbeforeacontracthasbeensigned,businessesshouldconsidercurrencyexposureandplantomitigateit.

Sometimesthisexposuremaynotbeimmediatelyapparentassuppliersmaynotinvoicedirectlyintheirlocalcurrency.Forexample,manyretailerspaysuppliersbasedinChinainUSdollars,andsuppliersinEasternEuropeinsterling.Payingsuppliersinnon-domesticcurrencycanattractapremium.SuppliersmayallocateabufferintheirpricestoprotectmarginsagainstFXrisk.Someretailershavemanagedtonegotiatediscountswiththeirsuppliersbyagreeingtopayinlocalcurrency.

Localcurrencyinvoicingincreasespricetransparencyinthesupplychain.ExplicitFXriskiseasiertomanageandbuildintooverallhedgingpolicythanimplicitFXrisk,whereimportersmayfindthatsterlingorUSdollarpricesincreaseduetosuppliersnotmanagingtheirFXriskseffectively,orsimplylackingtheknowledgeandmarketaccessofalargerfirm.BuyersshouldbeawareofthisimplicitaswellasexplicitFXrisk,andrequestdualpricing,whereapplicable,togainvisibilityovertheFXratesbeingapplied.

Itisimportanttonote,however,thatsomesuppliersareexperiencedexportersandhavedevelopedexpertiseforinternationaltrade.TheymayprefertomanagetheirFXrisksratherthanpassthemon.

Anotherconsiderationisthattheymaywantforeigncurrencyreceiptstooffsetcosts,forexampleaChinesesuppliermayhavesignificantUSdollar-denominatedrawmaterialcosts.Ineithercase,betterunderstandingoftheembeddedFXrisksthatfirmsareexposedtocanreduceoreliminatethepremiumbuiltintopricesquotedbysuppliers.

BetterunderstandingoftheembeddedFXrisksthatfirmsareexposedtocanreduceoreliminatethepremiumbuiltintopricesquotedbysuppliers.

InlightofBrexit,inwhichregionsareyouconsideringincreasing/decreasingpurchasingactivity?

NumbersstatedasNetpercentageincrement.

-5Other

-36.8Europe

36.8Africa

11.8North America

20.6Latin/South

America

20.6United Kingdom

35.3China

27.9South East Asia

(Vietnam/Thailand/Indonesia)

50.0South Asia

(India)

17of26

5.3 7.2 10.1

The fulfilment challengeServiceimprovementsand‘clickandcollect’mayhelptoimprovecustomersatisfactionandmanage‘lastmile’costs.

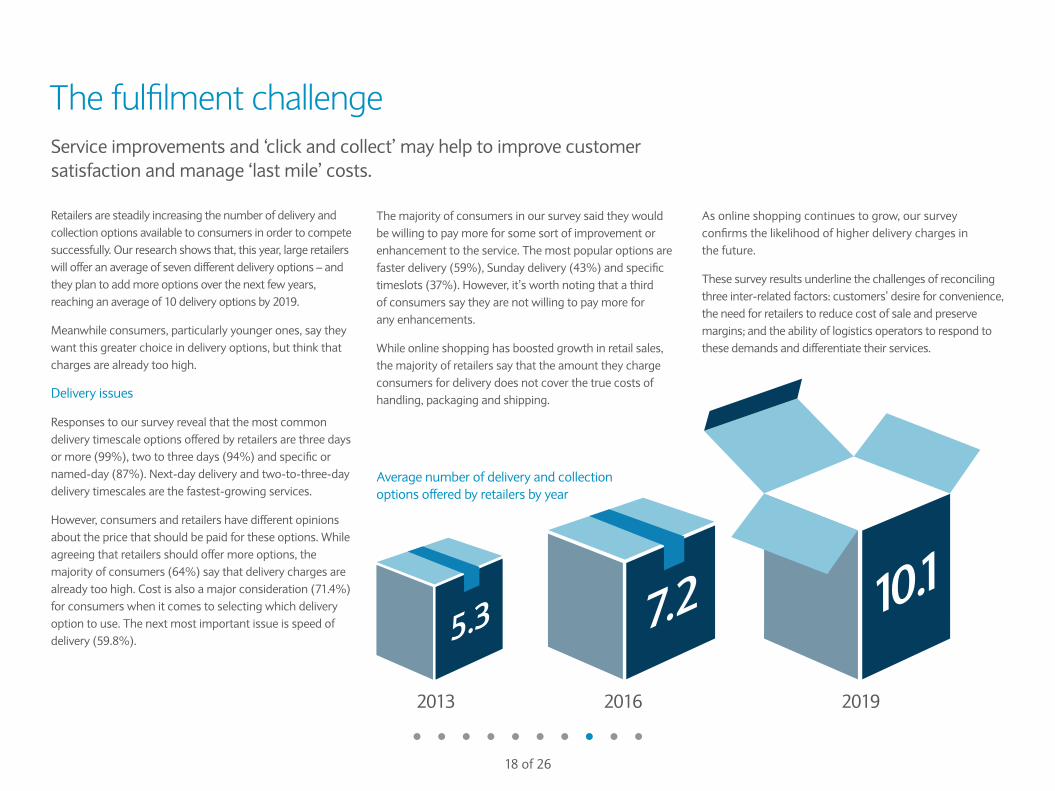

Retailersaresteadilyincreasingthenumberofdeliveryandcollectionoptionsavailabletoconsumersinordertocompetesuccessfully.Ourresearchshowsthat,thisyear,largeretailerswillofferanaverageofsevendifferentdeliveryoptions–andtheyplantoaddmoreoptionsoverthenextfewyears,reachinganaverageof10deliveryoptionsby2019.

Meanwhileconsumers,particularlyyoungerones,saytheywantthisgreaterchoiceindeliveryoptions,butthinkthatchargesarealreadytoohigh.

Deliveryissues

Responsestooursurveyrevealthatthemostcommondeliverytimescaleoptionsofferedbyretailersarethreedaysormore(99%),twotothreedays(94%)andspecificornamed-day(87%).Next-daydeliveryandtwo-to-three-daydeliverytimescalesarethefastest-growingservices.

However,consumersandretailershavedifferentopinionsaboutthepricethatshouldbepaidfortheseoptions.Whileagreeingthatretailersshouldoffermoreoptions,themajorityofconsumers(64%)saythatdeliverychargesarealreadytoohigh.Costisalsoamajorconsideration(71.4%)forconsumerswhenitcomestoselectingwhichdeliveryoptiontouse.Thenextmostimportantissueisspeedofdelivery(59.8%).

Avop

erage numberofdeliveryandcollectiontionsofferedbyretailersbyyear

2013 2016 2019

Themajorityofconsumersinoursurveysaidtheywouldbewillingtopaymoreforsomesortofimprovementorenhancementtotheservice.Themostpopularoptionsarefasterdelivery(59%),Sundaydelivery(43%)andspecifictimeslots(37%).However,it’sworthnotingthatathirdofconsumerssaytheyarenotwillingtopaymoreforanyenhancements.

Whileonlineshoppinghasboostedgrowthinretailsales,themajorityofretailerssaythattheamounttheychargeconsumersfordeliverydoesnotcoverthetruecostsofhandling,packagingandshipping.

Asonlineshoppingcontinuestogrow,oursurveyconfirmsthelikelihoodofhigherdeliverychargesinthefuture.

Thesesurveyresultsunderlinethechallengesofreconcilingthreeinter-relatedfactors:customers’desireforconvenience,theneedforretailerstoreducecostofsaleandpreservemargins;andtheabilityoflogisticsoperatorstorespondtothesedemandsanddifferentiatetheirservices.

18of26

Speed of service

Cost of service

Reliability of service

Politeness of staff

Amount of care taken of your package/parcel

Quality of packaging

Flexibility to change collection times or options

Amount of information provided

Quality of information provided

Collectionratings

16.3

15.3

26.4

25.2

35.3

36.3

24.2

18.4

29.0

POOR

49.9

54.2

33.4

54.5

30.9

22.5

25.1

40.6

37.2

GOOD

33.8

30.5

40.2

20.3

33.8

41.2

50.7

41.0

33.8

AVERAGE

Deliveryratings

Speed of service

Cost of service

Reliability of service

Politeness of staff

Amount of care taken of your package/parcel

Quality of packaging

Flexibility to change delivery times or options

Amount of information provided

Quality of information provided

28.6

39.5

45.7

33.5

15.0

37.4

50.0

36.6

36.7

POOR

40.9

23.8

23.8

30.9

29.7

23.7

16.5

24.7

18.4

GOOD

30.5

36.7

30.5

35.6

55.3

38.9

33.5

38.7

44.9

AVERAGE

Deliveryratings

Speed of service

Cost of service

Reliability of service

Politeness of staff

Amount of care taken of your package/parcel

Quality of packaging

Flexibility to change delivery times or options

Amount of information provided

Quality of information provided

28.6

39.5

45.7

33.5

15.0

37.4

50.0

36.6

36.7

POOR

40.9

23.8

23.8

30.9

29.7

23.7

16.5

24.7

18.4

GOOD

30.5

36.7

30.5

35.6

55.3

38.9

33.5

38.7

44.9

AVERAGE

Speed of service

Cost of service

Reliability of service

Politeness of staff

Amount of care taken of your package/parcel

Quality of packaging

Flexibility to change collection times or options

Amount of information provided

Quality of information provided

Collectionratings

16.3

15.3

26.4

25.2

35.3

36.3

24.2

18.4

29.0

POOR

49.9

54.2

33.4

54.5

30.9

22.5

25.1

40.6

37.2

GOOD

33.8

30.5

40.2

20.3

33.8

41.2

50.7

41.0

33.8

AVERAGE

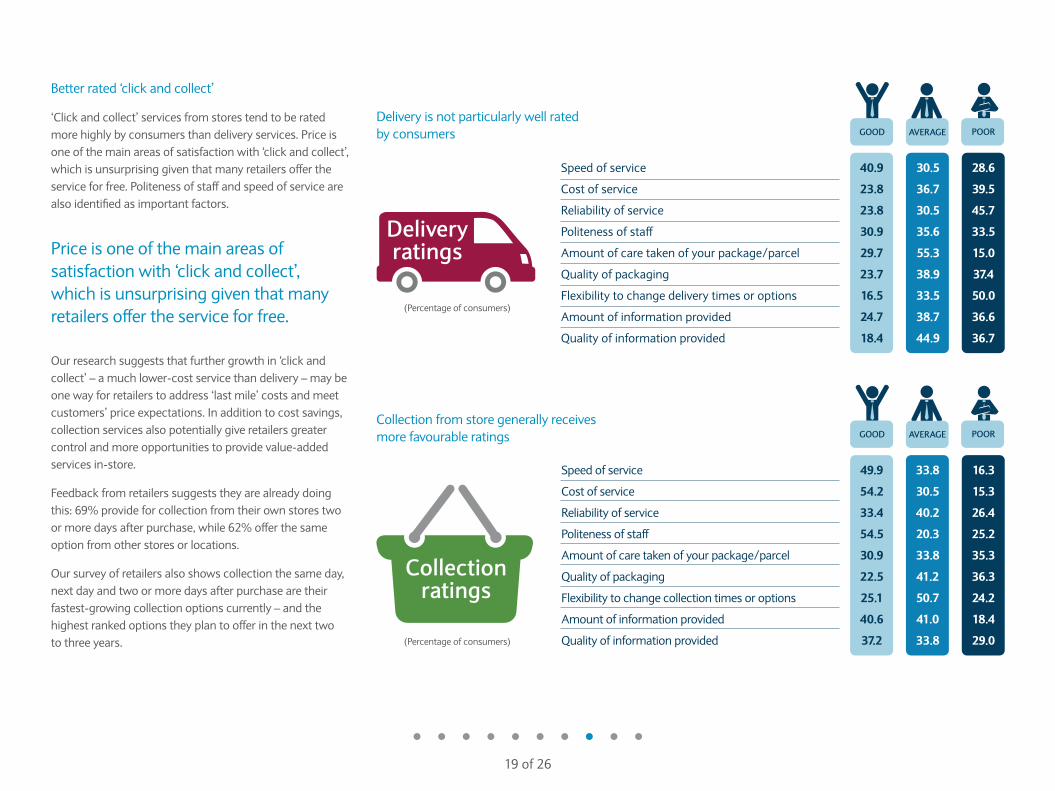

Deliveryisnot particularlywellratedbyconsumers

Collectionfromstoregenerallyreceivesmorefavourableratings

(Percentageofconsumers)

(Percentageofconsumers)

19of26

Betterrated‘clickandcollect’

‘Clickandcollect’servicesfromstorestendtoberatedmorehighlybyconsumersthandeliveryservices.Priceisoneofthemainareasofsatisfactionwith‘clickandcollect’,whichisunsurprisinggiventhatmanyretailersoffertheserviceforfree.Politenessofstaffandspeedofservicearealsoidentifiedasimportantfactors.

Ourresearchsuggeststhatfurthergrowthin‘clickandcollect’–amuchlower-costservicethandelivery–maybeonewayforretailerstoaddress‘lastmile’costsandmeetcustomers’priceexpectations.Inadditiontocostsavings,collectionservicesalsopotentiallygiveretailersgreatercontrolandmoreopportunitiestoprovidevalue-addedservicesin-store.

Feedbackfromretailerssuggeststheyarealreadydoingthis:69%provideforcollectionfromtheirownstorestwoormoredaysafterpurchase,while62%offerthesameoptionfromotherstoresorlocations.

Oursurveyofretailersalsoshowscollectionthesameday,nextdayandtwoormoredaysafterpurchasearetheirfastest-growingcollectionoptionscurrently–andthehighestrankedoptionstheyplantoofferinthenexttwotothreeyears.

Priceisoneofthemainareasofsatisfactionwith‘clickandcollect’,whichisunsurprisinggiventhatmanyretailersoffertheserviceforfree.

The ethical dimensionConsumersandretailersagreeontopethicalconcerns–butshoppingbehaviourisnotalwaysdrivenbyethicalconsiderations.

Whenitcomestoethicalissuesinthesupplychain,ourresearchshowsthatretailersandconsumersbroadlyagree.

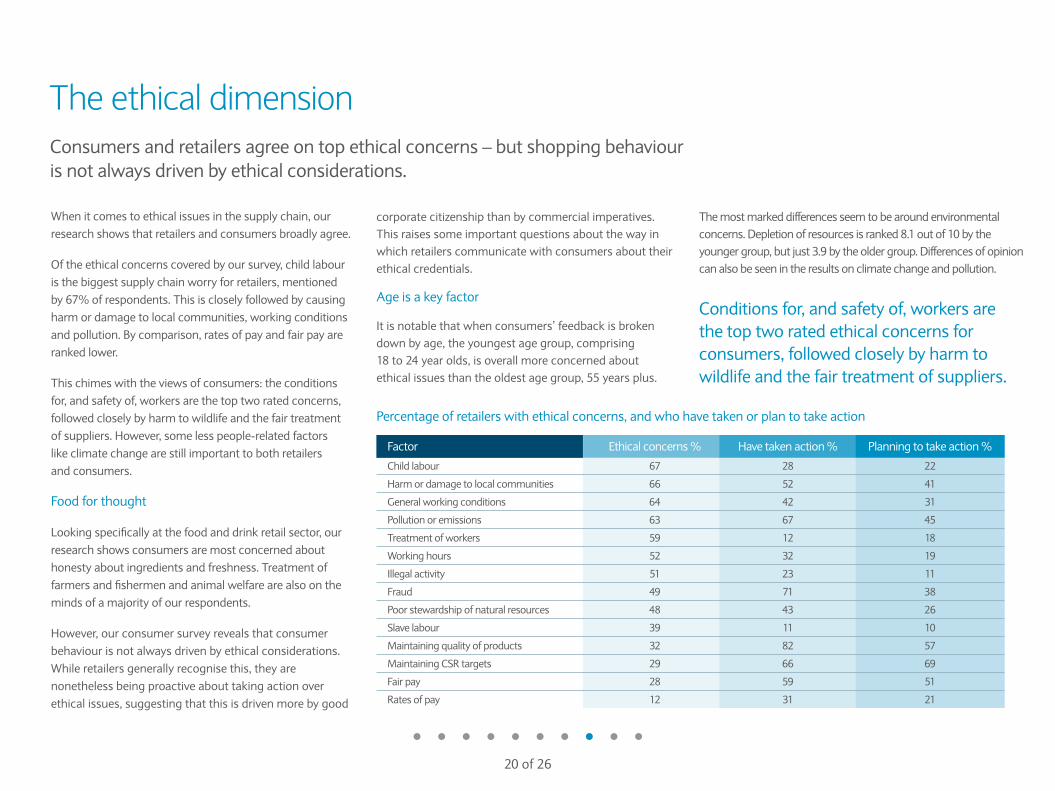

Oftheethicalconcernscoveredbyoursurvey,childlabouristhebiggestsupplychainworryforretailers,mentionedby67%ofrespondents.Thisiscloselyfollowedbycausingharmordamagetolocalcommunities,workingconditionsandpollution.Bycomparison,ratesofpayandfairpayarerankedlower.

Thischimeswiththeviewsofconsumers:theconditionsfor,andsafetyof,workersarethetoptworatedconcerns,followedcloselybyharmtowildlifeandthefairtreatmentofsuppliers.However,somelesspeople-relatedfactorslikeclimatechangearestillimportanttobothretailersandconsumers.

Foodforthought

Lookingspecificallyatthefoodanddrinkretailsector,ourresearchshowsconsumersaremostconcernedabouthonestyaboutingredientsandfreshness.Treatmentoffarmersandfishermenandanimalwelfarearealsoonthemindsofamajorityofourrespondents.

However,ourconsumersurveyrevealsthatconsumerbehaviourisnotalwaysdrivenbyethicalconsiderations.Whileretailersgenerallyrecognisethis,theyarenonethelessbeingproactiveabouttakingactionoverethicalissues,suggestingthatthisisdrivenmorebygood

corporatecitizenshipthanbycommercialimperatives.Thisraisessomeimportantquestionsaboutthewayinwhichretailerscommunicatewithconsumersabouttheirethicalcredentials.

Ageisakeyfactor

Itisnotablethatwhenconsumers’feedbackisbrokendownbyage,theyoungestagegroup,comprising18to24yearolds,isoverallmoreconcernedaboutethicalissuesthantheoldestagegroup,55yearsplus.

Themostmarkeddifferencesseemtobearoundenvironmentalconcerns.Depletionofresourcesisranked8.1outof10bytheyoungergroup,butjust3.9bytheoldergroup.Differencesofopinioncanalsobeseenintheresultsonclimatechangeandpollution.

Conditionsfor,andsafetyof,workersarethetoptworatedethicalconcernsforconsumers,followedcloselybyharmtowildlifeandthefairtreatmentofsuppliers.

Factor Ethicalconcerns% Havetakenaction% Planningtotakeaction%

Childlabour 67 28 22

Harmordamagetolocalcommunities 66 52 41

Generalworkingconditions 64 42 31

Pollutionoremissions 63 67 45

Treatmentofworkers 59 12 18

Workinghours 52 32 19

Illegalactivity 51 23 11

Fraud 49 71 38

Poorstewardshipofnaturalresources 48 43 26

Slavelabour 39 11 10

Maintainingqualityofproducts 32 82 57

MaintainingCSRtargets 29 66 69

Fairpay 28 59 51

Ratesofpay 12 31 21

Percentageofretailerswithethicalconcerns,andwhohavetakenorplantotakeaction

20of26

HighlyunethicalIf you found out a retailer was highly unethical in its supply chain, how likely would you be to avoid it and shop elsewhere?

Highly unlikely

12.8%Not sure8.9%

Not reallythink about it

6.8%

Highly likely

12.2%

Fairly likely

14.5%

Fairly unlikely44.8%

Highly likely

19.7%

Fairly likely

28.4%

Fairly unlikely28.7%

Highly unlikely

9.8%Not sure8.2%

Not reallythink about it5.2%

Slightly unethicalIf you found out a retailer was slightly unethical in its supply chain, how likely would you be to avoid it and shop elsewhere?

Retailers’actions

Feedbackfromretailersdemonstratestheyareproactiveabouttakingactiononethicalissues:almostallhavetakenorplantotakesomeformofethicalactionovertheirsupplychains.Themostcommonactionstakenarearoundmaintainingthequalityofproducts(82%),dealingwithpollutionoremissions(67%)ormaintainingcorporatesocialresponsibilitytargets(66%).Lookingaheadatplannedactions,fairpayisalsohighontheagenda,beingmentionedbyoverhalfofretailers(51%).

However,retailerssaytheyhaveconcernsaboutthelevelofcontroltheyhaveovertheirsupplychainsonethicalissues.Thisismostlikelybecausetheirsupplychainscanbesolongthatcompletecontrolisextremelydifficult.Oursurveyalsoshowsthatagreaternumberoffoodretailers(39%)feeltheyhave‘alot’ofcontrolovertheirsupplychainthanfashionretailers(21%).

Impactofethicalconcernsonshopping

Despitegoodintentionsandsomestrongviews,nearlytwothirdsofconsumers(61%)saythattheytendtoforgetabouttheethicaltreatmentofworkerswhenthey’rebuyingproducts.Breakingdownresponsesbyage,fewerinthe18to24yearoldagegroupagreewiththisstatement(52%)thanthe55-and-overgroup(63%).

However,ourresearchstillshowsthatanarrowmajority(52%)ofconsumersofallageswouldbewillingtopay‘alittlemore’toensuresupplychainsweremoreethical.Interestingly,60%ofconsumersacceptthattheyarepartlytoblameforsomeoftheethicalissuesbecauseoftheirdesireforlowerprices.

Thoseaged18to24arethemostcynicalaboutretailers,withmoreofthem(67%)sayingretailersarebecomingworseinthewaytheybehavetowardssuppliersandpeoplewhoworkintheirsupplychainthanthe55-plusagegroup(55%).

Changingbehaviour

Almosttwothirdsofconsumerssaytheywouldbeunlikelytoavoid,orwouldnotthinkaboutavoiding,shoppingataretailerthatwas‘slightlyunethical’initssupplychainpractices.

Thisfiguredropsslightlyforconsumersaged18to24.Unsurprisingly,moreconsumerssaytheywouldbelikelytoavoidshoppingataretailerthathadactedina‘highlyunethical’way.

Notonlydomostconsumersinoursurveyadmittheytendtoforgetabouttheirethicalconcernswhenshopping,butfeedbackfromretailersshowsthattheybelievethatconsumerbehaviourisnotdrivenbyethicalconsiderations.Askedhowmuchitactuallyinfluencesconsumerbehaviourindecidingwhattobuyandwhentoshop,58%ofretailersagreewiththeanswer‘notverymuch’.

60%ofconsumersacceptthattheyarepartlytoblameforsomeoftheethicalissuesbecauseoftheirdesireforlowerprices.

21of26

Highly likely

19.7%

Fairly likely

28.4%

Fairly unlikely28.7%

Highly unlikely

9.8%Not sure8.2%

Not reallythink about it5.2%

Highly unlikely

12.8%Not sure8.9%

Not reallythink about it

6.8%

Highly likely

12.2%

Fairly likely

14.5%

Fairly unlikely44.8%

Strategies for successThereareanumberofconsiderationsthatretailerscankeepinmindwhenoptimisingtheirsupplychains.

Usedataeffectively

Theuseofmultipleretailtouchpointshasmadelogisticsandsupplychainsmorecomplex,buttheyalsoprovidearichstreamofdata.Usedeffectively,thisdatacanbeanalysedtohelppredictpatterns

ofdemandandstreamlineplanningwithinthesupplychain.

Partnerup

Smallerandmedium-sizedretailerscanpiggybackonthesupplychainsofotherproviders.Thissavestheeffortandexpenseofbuildingasupplychainfromscratch,especiallyinanewchannelormarket.Amazon,forexample,allowsmanysuppliersandretailerstodeliverandstoreproducts

initsownwarehousesforonwardfulfilment,aswellasworkinginpartnershipwithMorrisonsandOcado.

Tapintothesharingeconomy

Retailerscanmakeuseoftheonlinesharingeconomytocopewithexceptionaldemandorpocketsof

demandthatarenotlargeenoughtomeettraditionalsupplychains.Forexample,wheresame-daydelivery

isnotpossiblethroughabusiness’ssupplychain,usingUber’scourierservicemayallowittomeet

demandcost-effectively.

Focusonefficiencies

Onceretailershaveinvestedinnewsystems,warehousesandoperations,thefocusshouldswitch

togreaterefficiency–forexample,prioritisingdeliveriesandshipmentsaccordingtoneedratherthanhavingasinglestandarddeliverytimeframe.

Buildintransparencyandshareinformation

Retailersshouldensureproductsaretraceableateverystepofthesupplychain.Thisallowsthemtoshareinformationwithconsumersandgivethem

peaceofmindaboutethicalissues.

Balanceflexibilityandrigidity

Whilesupplychainsneedtoberobust,atleastpartofthechainneedstobeflexibleenoughtorespondtosuddenchangesindemand.

Thismeansretailersneedtobeabletoscaleupandscaledownquickly.

22of26

Putattheheartofthebusiness

Effectiveretailersnowviewthesupplychainastheheartofthebusinessandasameansforsatisfying

consumerdemand.Ensurethatsupplychaincolleaguesmeetandtalkwithbuyers,store

managers,customerinsightteamsandothercustomer-facingpartsoftheorganisation.

Test,testandtestagain

Regulartestingofthesupplychainwithexercises–realorsimulated–isagoodwaytoensuresystemsandoperationscancopewith

changesindemand.

Thinksmall,notbig

Traditionalsupplychainsaregeareduptothinkinbulk:multipleunitsdeliveredandsuppliedtoalimited

numberofdistributionpoints.Themodelhasnowchangedandneedstobeabletocopewithsingle

unitsdeliveredtomanydistributionpoints,includingtocustomersathome.

Spreadrisk

Thiscantakemanyforms,includingusingarangeofsupplierssothataretailerisnotreliantonasinglesourceforanimportantproductorcommodity,

orensuringthatapopularitemisnotdeliveredfromasingledistributioncentre.

Theomni-channelsupplychain

Thesupplychainnolongerendswhenaproductisdeliveredtoastore.Omni-channelmeansthatstoresareoftenmini-warehousesordistributionpointsfrom

whichproductsaresuppliedtootherstoresordeliveredtocustomers.Assuch,retailersneeda‘onestockview’ofthesupplychain,givingthemvisibilityofinventory

acrosstheentireorganisation.

23of26

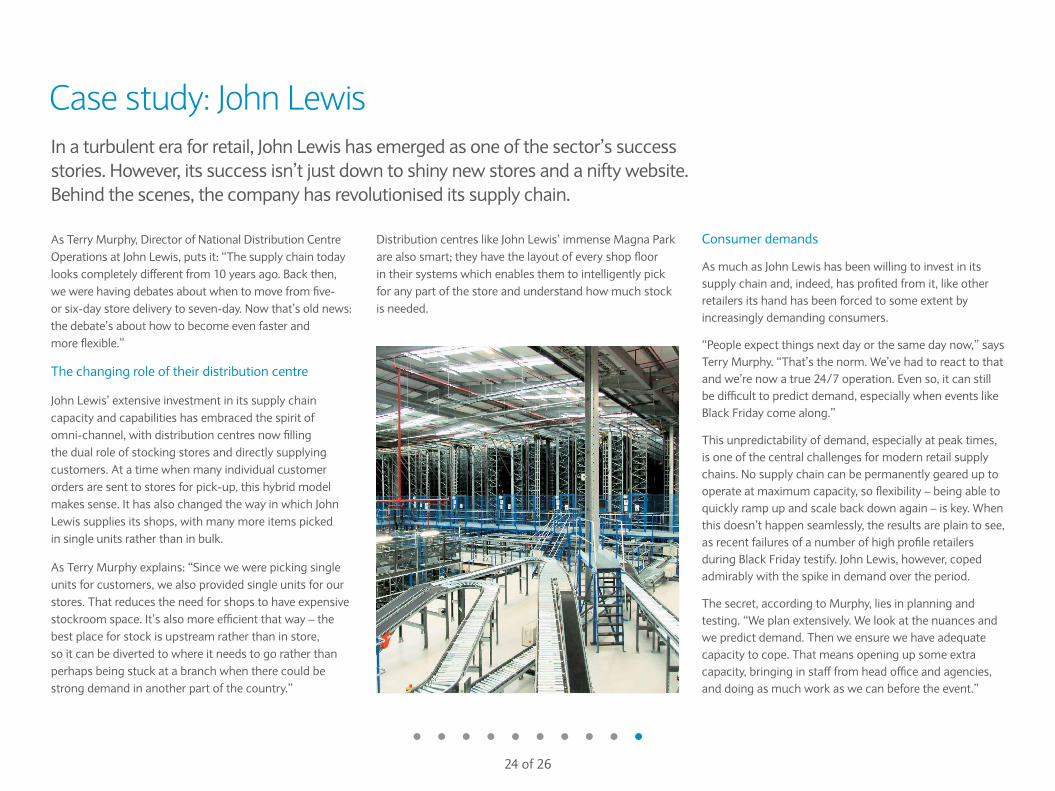

Case study: John LewisInaturbulenteraforretail,JohnLewishasemergedasoneofthesector’ssuccessstories.However,itssuccessisn’tjustdowntoshinynewstoresandaniftywebsite.Behindthescenes,thecompanyhasrevolutioniseditssupplychain.

AsTerryMurphy,DirectorofNationalDistributionCentreOperationsatJohnLewis,putsit:“Thesupplychaintodaylookscompletelydifferentfrom10yearsago.Backthen,wewerehavingdebatesaboutwhentomovefromfive-orsix-daystoredeliverytoseven-day.Nowthat’soldnews:thedebate’sabouthowtobecomeevenfasterandmoreflexible.”

Thechangingroleoftheirdistributioncentre

JohnLewis’extensiveinvestmentinitssupplychaincapacityandcapabilitieshasembracedthespiritofomni-channel,withdistributioncentresnowfillingthedualroleofstockingstoresanddirectlysupplyingcustomers.Atatimewhenmanyindividualcustomerordersaresenttostoresforpick-up,thishybridmodelmakessense.IthasalsochangedthewayinwhichJohnLewissuppliesitsshops,withmanymoreitemspickedinsingleunitsratherthaninbulk.

AsTerryMurphyexplains:“Sincewewerepickingsingleunitsforcustomers,wealsoprovidedsingleunitsforourstores.Thatreducestheneedforshopstohaveexpensivestockroomspace.It’salsomoreefficientthatway–thebestplaceforstockisupstreamratherthaninstore,soitcanbedivertedtowhereitneedstogoratherthanperhapsbeingstuckatabranchwhentherecouldbestrongdemandinanotherpartofthecountry.”

DistributioncentreslikeJohnLewis’immenseMagnaParkarealsosmart;theyhavethelayoutofeveryshopfloorintheirsystemswhichenablesthemtointelligentlypickforanypartofthestoreandunderstandhowmuchstockisneeded.

Consumerdemands

AsmuchasJohnLewishasbeenwillingtoinvestinitssupplychainand,indeed,hasprofitedfromit,likeotherretailersitshandhasbeenforcedtosomeextentbyincreasinglydemandingconsumers.

“Peopleexpectthingsnextdayorthesamedaynow,”saysTerryMurphy.“That’sthenorm.We’vehadtoreacttothatandwe’renowatrue24/7operation.Evenso,itcanstillbedifficulttopredictdemand,especiallywheneventslikeBlackFridaycomealong.”

Thisunpredictabilityofdemand,especiallyatpeaktimes,isoneofthecentralchallengesformodernretailsupplychains.Nosupplychaincanbepermanentlygeareduptooperateatmaximumcapacity,soflexibility–beingabletoquicklyrampupandscalebackdownagain–iskey.Whenthisdoesn’thappenseamlessly,theresultsareplaintosee,asrecentfailuresofanumberofhighprofileretailersduringBlackFridaytestify.JohnLewis,however,copedadmirablywiththespikeindemandovertheperiod.

Thesecret,accordingtoMurphy,liesinplanningandtesting.“Weplanextensively.Welookatthenuancesandwepredictdemand.Thenweensurewehaveadequatecapacitytocope.Thatmeansopeningupsomeextracapacity,bringinginstafffromheadofficeandagencies,anddoingasmuchworkaswecanbeforetheevent.”

24of26

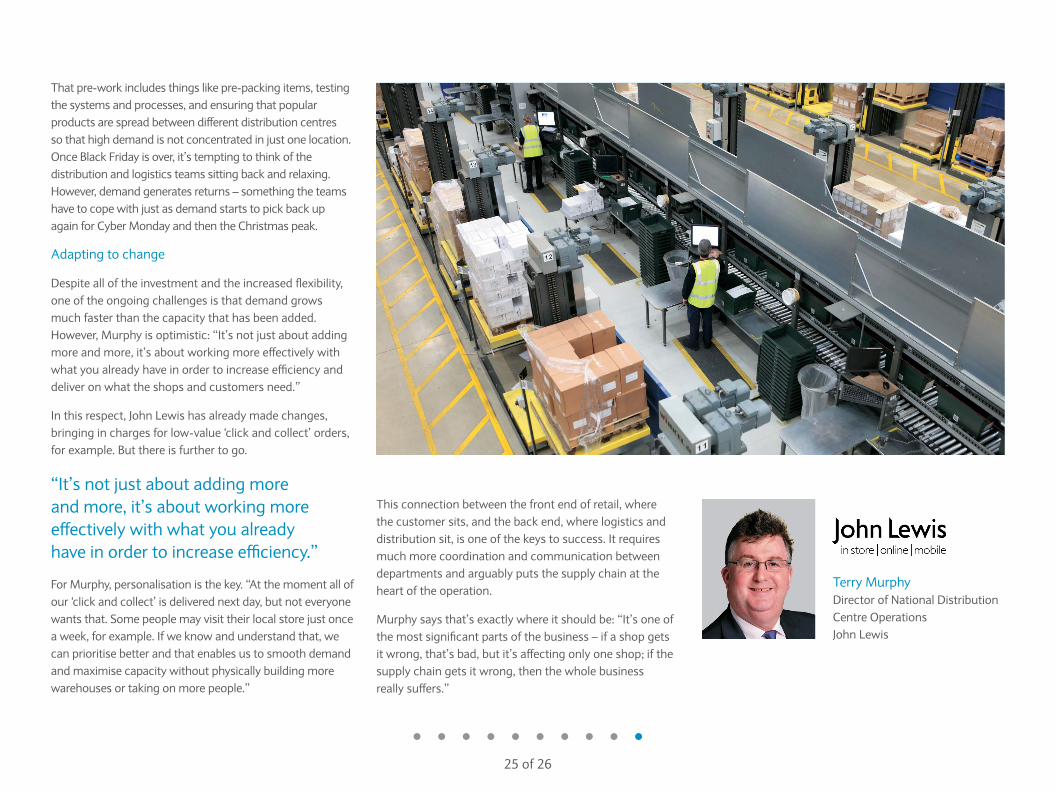

Thatpre-workincludesthingslikepre-packingitems,testingthesystemsandprocesses,andensuringthatpopularproductsarespreadbetweendifferentdistributioncentressothathighdemandisnotconcentratedinjustonelocation.OnceBlackFridayisover,it’stemptingtothinkofthedistributionandlogisticsteamssittingbackandrelaxing.However,demandgeneratesreturns–somethingtheteamshavetocopewithjustasdemandstartstopickbackupagainforCyberMondayandthentheChristmaspeak.

Adaptingtochange

Despitealloftheinvestmentandtheincreasedflexibility,oneoftheongoingchallengesisthatdemandgrowsmuchfasterthanthecapacitythathasbeenadded.However,Murphyisoptimistic:“It’snotjustaboutaddingmoreandmore,it’saboutworkingmoreeffectivelywithwhatyoualreadyhaveinordertoincreaseefficiencyanddeliveronwhattheshopsandcustomersneed.”

Inthisrespect,JohnLewishasalreadymadechanges,bringinginchargesforlow-value‘clickandcollect’orders,forexample.Butthereisfurthertogo.

ForMurphy,personalisationisthekey.“Atthemomentallofour‘clickandcollect’isdeliverednextday,butnoteveryonewantsthat.Somepeoplemayvisittheirlocalstorejustonceaweek,forexample.Ifweknowandunderstandthat,wecanprioritisebetterandthatenablesustosmoothdemandandmaximisecapacitywithoutphysicallybuildingmorewarehousesortakingonmorepeople.”

Thisconnectionbetweenthefrontendofretail,wherethecustomersits,andthebackend,wherelogisticsanddistributionsit,isoneofthekeystosuccess.Itrequiresmuchmorecoordinationandcommunicationbetweendepartmentsandarguablyputsthesupplychainattheheartoftheoperation.

Murphysaysthat’sexactlywhereitshouldbe:“It’soneofthemostsignificantpartsofthebusiness–ifashopgetsitwrong,that’sbad,butit’saffectingonlyoneshop;ifthesupplychaingetsitwrong,thenthewholebusinessreallysuffers.”

TerryMurphyDirectorofNationalDistributionCentreOperationsJohnLewis

“It’snotjustaboutaddingmoreandmore,it’saboutworkingmoreeffectivelywithwhatyoualreadyhaveinordertoincreaseefficiency.”

25of26

About the authorIan Gilmartin Head of Retail and Wholesale Corporate Banking

Ian Gilmartin is Head of Industry for Retail and Wholesale at Barclays Corporate Banking across the UK and Ireland, where Barclays has operated a sector specialism for almost 30 years. He and his team of Relationship Directors are responsible for thousands of clients, ranging from boutique fashion houses and high-street booksellers to department stores and listed companies.

Ian has over 20 years of corporate banking experience and has spent the last five years providing specialist banking services to retailers and wholesalers as part of the leadership within the Retail and Wholesale team. Prior to that, he was a Senior Relationship Director in the Technology, Media and Telecoms team, and has experience of other sector verticals from his early career.

Since taking on his current role, Ian has become a regular commentator in the national, regional and trade media on retail trends and industry issues, as well as retail sales figures.

T: 020 7116 6868 [email protected]

To find out more about how Barclays can support your business, please call 0800 015 4242* or visit barclayscorporate.com

* Calls to 0800 numbers are free from UK landlines and personal mobiles, otherwise call charges may apply. To maintain a quality service we may monitor or record phone calls.

No part of this publication may be reproduced or stored in a retrieval system, in any form or by any means, electrical, mechanical, photocopying or otherwise, without the prior consent of the publishers. The views and forecasts presented in this report represent independent findings and conclusions drawn from a study by Conlumino. Conlumino can accept no responsibility for any investment decision made on the basis of this information or for any omissions or inaccuracies that may be contained in this report. This report has been produced in good faith and independently of any operator or supplier to the industry. We trust that it will be of significant value to all readers.

The views expressed in this report are the views of third parties, and do not necessarily reflect the views of Barclays Bank PLC nor should they be taken as statements of policy or intent of Barclays Bank PLC. Barclays Bank PLC takes no responsibility for the veracity of information contained in third-party narrative and no warranties or undertakings of any kind, whether expressed or implied, regarding the accuracy or completeness of the information given. Barclays Bank PLC takes no liability for the impact of any decisions made based on information contained and views expressed in any third-party guides or articles.

Bar clays is a trading name of Barclays Bank PLC and its subsidiaries. Barclays Bank PLC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (Financial Services Register No. 122702). Registered in England. Registered number is 1026167 with registered office at 1 Churchill Place, London E14 5HP.

August 2016. BD02456.

26 of 26