CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Chapter 16

Objectives: Identify accounting concepts & practices related to adjusting

and closing entries for a merchandising business organized as a corporation

Record adjusting entries Record closing entries for income statement accounts Record closing entry for dividends Prepare a post closing trial balance

1

LESSON 16-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 16-1: Recording Adjusting Entries

• Adjustments on a work sheet are the source for journalizing adjusting entries.

• Adjusting entries are recorded in the general journal.• Adjusting entries are recorded on a new general journal

page with the heading “Adjusting Entries” centered on the first line of the journal.

• Adjusting entries are journalized in their debit and credit parts identified by corresponding letters in the work sheet.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 16-1

ADJUSTING ENTRIES RECORDED FROM A WORK SHEET

3

page 480

2 1 4 56 7

1. Heading

2. Date

3. Identify the first adjustment

4. Account debited

5. Debit

6. Account credited

7. Credit

8. Continue down the Adjustments columns

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 16-1

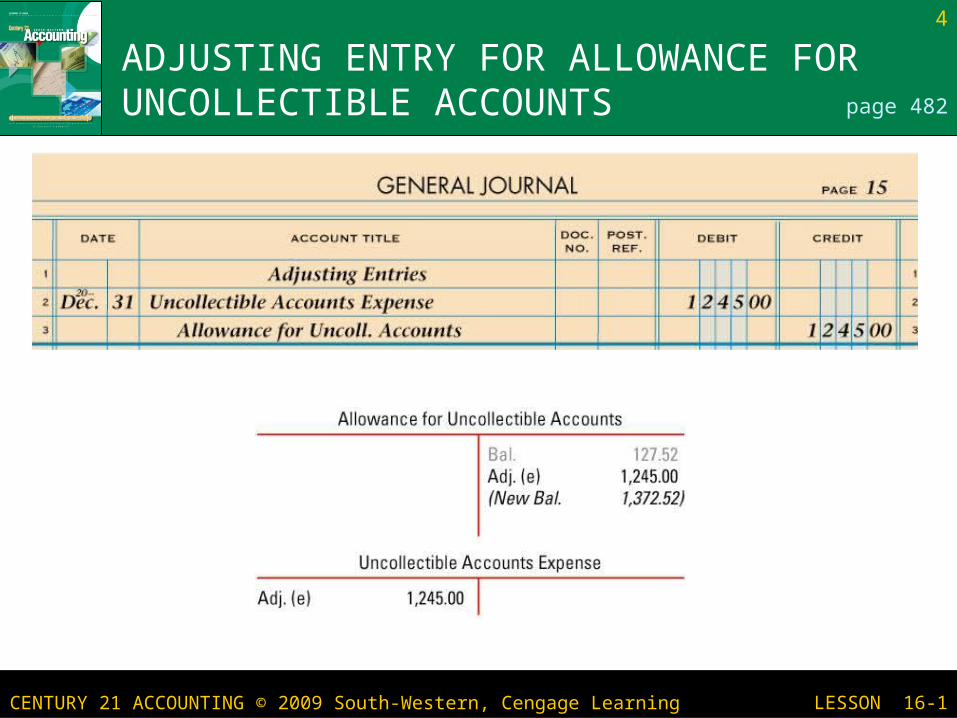

ADJUSTING ENTRY FOR ALLOWANCE FOR UNCOLLECTIBLE ACCOUNTS page 482

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

5

LESSON 16-1

ADJUSTING ENTRY FOR MERCHANDISE INVENTORY page 482

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 16-1

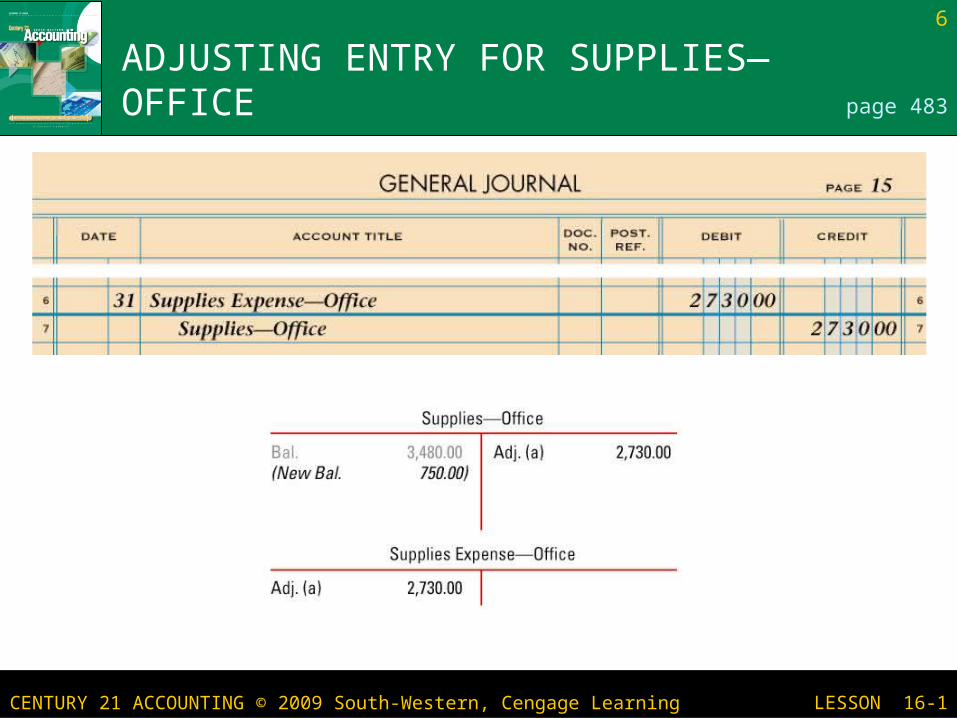

ADJUSTING ENTRY FOR SUPPLIES—OFFICE page 483

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 16-1

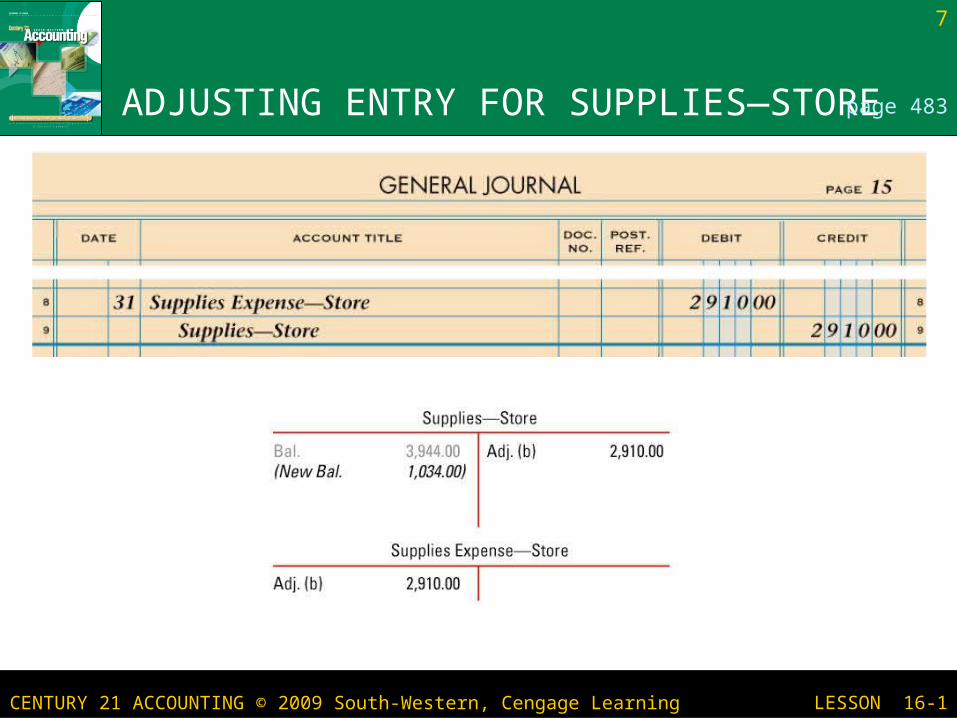

ADJUSTING ENTRY FOR SUPPLIES—STORE page 483

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 16-1

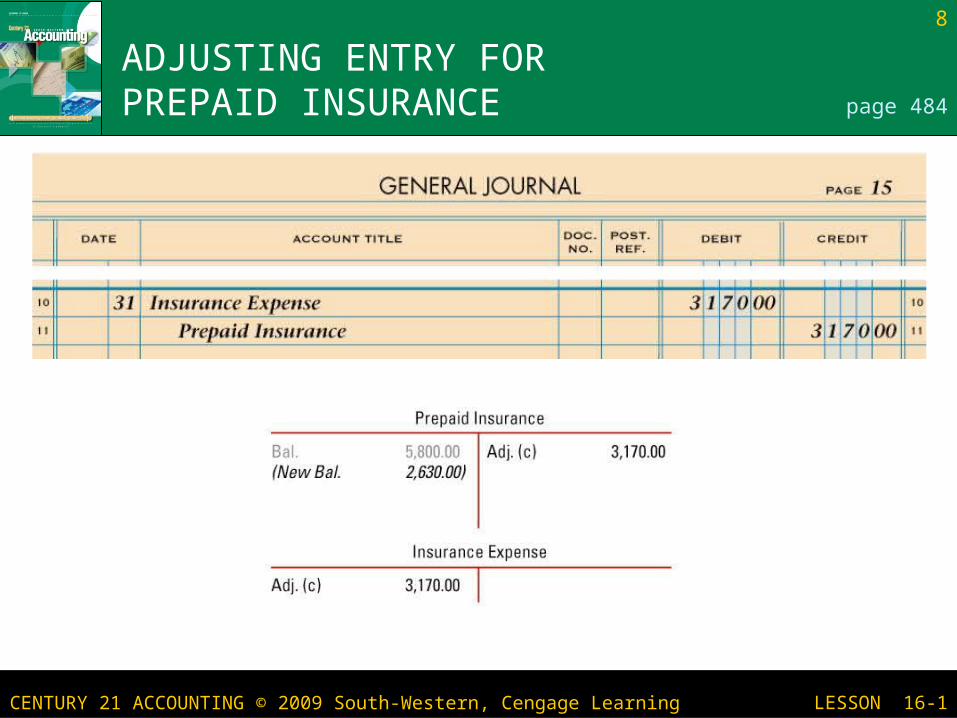

ADJUSTING ENTRY FOR PREPAID INSURANCE page 484

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

9

LESSON 16-1

ADJUSTING ENTRY FOR DEPRECIATION—OFFICE EQUIPMENT page 484

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 16-1

ADJUSTING ENTRY FOR DEPRECIATION—STORE EQUIPMENT page 485

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 16-1

ADJUSTING ENTRY FOR FEDERAL INCOME TAXES page 485

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Lesson 16-1

Let’s do Work Together 16-1 and On Your Own 16-1 on textbook page 486.

12

LESSON 16-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 16-2: Recording Closing Entries for Income Statement Accounts

• The income summary account is used only at the end of the fiscal period to summarize the closing entries for revenue, cost, and expenses.

• At the end of a fiscal period, temporary accounts are closed to prepare the general ledger for the next fiscal period.

• There are four kinds of closing entries:

1. To close income statement accounts with credit balances

2. To close income statement accounts with debit balances

3. To record net income or loss and close the income

summary account

4. To close the dividends account• Amounts needed for closing entries are obtained from the income

statement and balance sheet columns of the work sheet.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

14

LESSON 16-2

THE INCOME SUMMARY ACCOUNT page 487

The income summary account is unique because it does not have a normal balance side. The balance of this account is determined by the amounts posted to the account at the end of a fiscal period.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

15

LESSON 16-2

CLOSING ENTRY FOR ACCOUNTS WITH CREDIT BALANCES

12

page 488

3. Debits to close

41. Heading

2. Date

4. Credit to Income Summary

33

To close each account, the account is debited for the balance of the account and Income Summary is credited for the total debits.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

16

LESSON 16-2

CLOSING ENTRY FOR INCOME STATEMENT ACCOUNTS WITH DEBIT BALANCES

12 4

page 489

3. Credits to close

1. Date

2. Account debited

4. Debit amount

3

3The sum of all the income statement accounts with debit balances will be debited to the Income Summary account.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

17

LESSON 16-2

SUMMARY OF CLOSING ENTRY FOR INCOME STATEMENT ACCOUNTS WITH DEBIT BALANCES page 490

Bal. 209,960.00 Closing 209,960.00

(New Bal. zero)

Purchases

Adj. (mdse. inv.) 15,840.00 Closing (credit amounts) 500,253.10

Closing (debit accounts) 404,099.15 (New Bal. 80,313.95)

Income Summary

After the sales, cost, and expense accounts are closed, the balance in the income summary account is the net income (if a credit balance) or net loss (if a debit balance) for the fiscal period.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

18

LESSON 16-2

CLOSING ENTRY TO RECORD NET INCOME page 491

12

3

3. Credit Retained Earnings

1. Date

2. Debit Income SummaryThe balance of Income Summary is the same as the net income amount on the work sheet and income statement.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

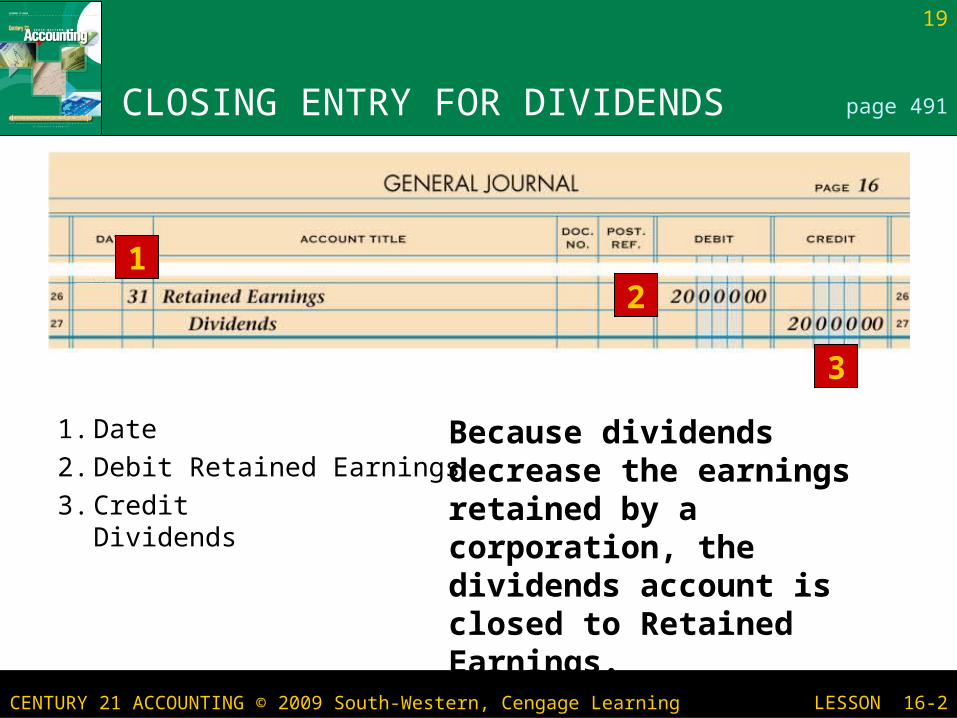

19

LESSON 16-2

CLOSING ENTRY FOR DIVIDENDS page 491

3. Credit Dividends

1. Date

2. Debit Retained Earnings

12

3

Because dividends decrease the earnings retained by a corporation, the dividends account is closed to Retained Earnings.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

20

LESSON 16-2

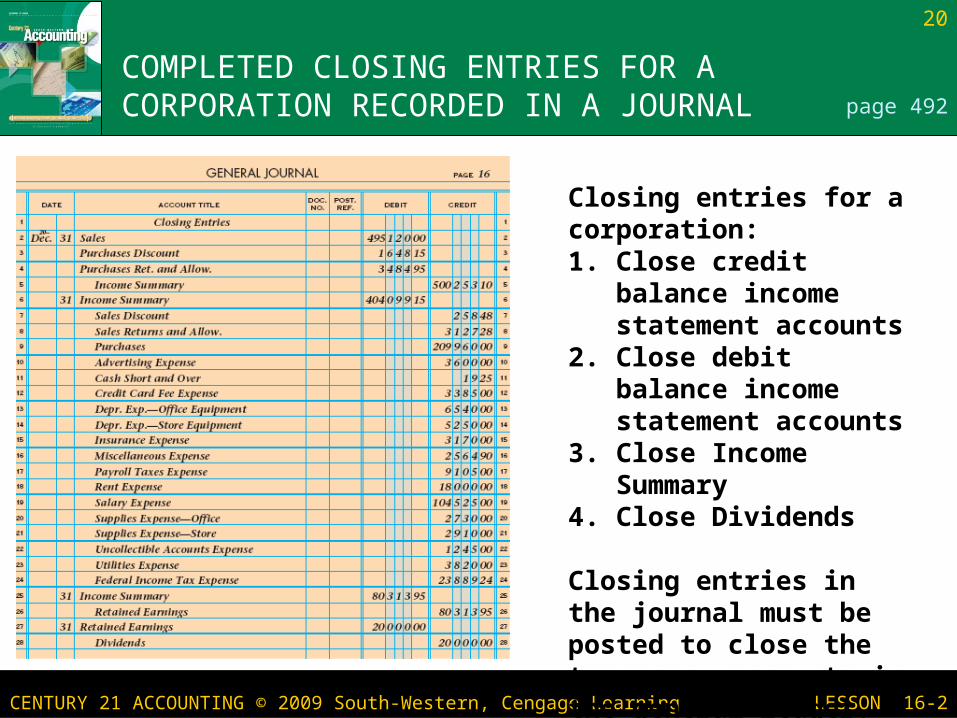

COMPLETED CLOSING ENTRIES FOR A CORPORATION RECORDED IN A JOURNAL page 492

Closing entries for a corporation:1. Close credit balance

income statement accounts

2. Close debit balance income statement accounts

3. Close Income Summary4. Close Dividends

Closing entries in the journal must be posted to close the temporary accounts in the general ledger.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 16-2

Let’s do Work Together 16-2 and On Your Own 16-2 on textbook page 493.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 16-3: Preparing a Post-Closing Trial Balance

After all adjusting and closing entries have been posted, the only general ledger accounts that should have balances are the balance sheet accounts—assets, liabilities, and capital accounts.

The income statement accounts—revenue, cost, and expense accounts—plus the Dividends account should all have zero balances to start the new fiscal period.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

23

LESSON 16-3

POST-CLOSING TRIAL BALANCE page 496

• After adjusting and closing entries have been posted, a post closing trial balance should be prepared to prove the equality of debits and credits in the general ledger.

• The post closing trial balance should contain only balances for asset, liability, and capital accounts. All revenue, cost, expense, and the Dividends accounts should have zero balances.

• The post closing trial balance should list all the balance sheet accounts in the order they are listed in the chart of accounts.

• The debit balance amounts should be listed in the first column and the credit balance amounts should be listed in the second column of the form.

• If the total debits equal total credits, then the equality of debits and credits is proved.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

24

LESSON 16-3

3. Balances of asset accounts

4. Balances contra asset, liability, and capital accounts

POST-CLOSING TRIAL BALANCE

1

6

page 496

7. Double lines

6. Totals

5. Word Totals

2. Accounts that have balances

1. Heading

2

3

4

75

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

25

LESSON 16-3

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

1

2

3

4

5

page 497

(continued on next slide)

1. Source documents are checked, and transactions are analyzed.

2. Transactions are recorded in journals.

3. Journal entries are posted to the accounts payable ledger, the accounts receivable ledger, and the general ledger.

4. Schedules of accounts payable and account receivable are prepared from the subsidiary ledgers.

5. A work sheet is prepared from the general ledger.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

26

LESSON 16-3

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

6. Financial statements are prepared.

page 497

(continued from previous slide)

6

7

8

9

9. A post-closing trial balance of the general ledger is prepared.

8. Adjusting and closing entries are posted to the general ledger.

7. Adjusting and closing entries are journalized from the work sheet.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Lesson 16-3

27

LESSON 16-1

Let’s do Work Together 16-3 and On Your Own 16-3 on textbook page 498.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Chapter 16 Assignments

28

LESSON 16-1

• Study Guide• Application Problem 16-1• Application Problem 16-2• Application Problem 16-3• Application Problem 16-4• Mastery Problem 16-5