0 0

Public Workshop Regulatory, in particular access, regimes for

network investment models in Europe

(SMART 2015/0002)

Ilsa Godlovitch, WIK-Consult

Wolter Lemstra, TUDelft/Industry-Insights

Christoph Pennings, IDATE

Alexandre de Streel, Université de Namur

6 April 2016

1

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

2

Aims of the study

• Provide evidence and analytical insights in support

of the EC Review of the Regulatory Framework for

Electronic Communications with focus on NGA

• Attention to

- NRA objectives (competition, efficient investment)

- Market analysis process, imposition of SMP remedies

- Symmetric obligations (Article 12 FWD, 4-5 AID)

- Mechanisms to foster consistent application

(Recommendations, article 7 process, BEREC)

• Input to evaluation of the current framework; and

• Impact of alternative options

3

Study elements

• Task 1: Future developments

- Scenarios for supply and demand of fast broadband

- Organisational change

- Will access bottlenecks persist?

• Task 2: Evaluate current models through KPIs

- NGA business models in urban and ‘challenge’ areas

- Regulatory models and their effects

• Task 3: Identify future EU regulatory models for access

- Identify key models at EU level based on challenges, objectives

- Preliminary Impact Assessment

• Tasks 4/5: Implications for evaluation and review of RF

4

Methodology

• Data gathering

- KPI data (inputs, intermediate, outputs) from EC, IDATE, OECD

- Analysis of Commission online consultation

- ~30 Interviews (End-users, industry, investors, BEREC, NRAs)

- Desk research

• Analytical tools

- Modelling of supply and demand scenarios

- Econometrics: which factors are linked to positive outcomes?

- Case studies: more granular assessment of impact of different

business and regulatory models on structures and outcomes

• Presentation of conclusions

- Follow ‘better regulation’ guidelines on evaluation, IA

5

Timetable

Date Activity

Nov-15 Kick-off

Dec 2015-Mar 2016 Data gathering/interviews

Mar-16 Interim report (tasks 1-3)

6-Apr-16 Public workshop

Apr-May 2016 Implications for framework

Jun-16 Finalise report

6

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

Theoretical perspective

7

What will customers need in 2025?

What will operators provide in 2025?

• Broadband market outcomes:

Result of Interaction between

Supply and Demand

• Supply side factors:

Type of legacy network: PSTN/CATV/FttH/3-4G

Availability tech. upgrades and capacity increases:

G.Fast/DOCSIS3.1/ TWDM-PON/5G

Cost, ease of upgrade + Willingness to pay + Competition

=> Technology mix in the field

=> Start of end-user adoption

8

What will customers need in 2025?

What will operators provide in 2025?

• Broadband market outcomes:

Result of Interaction between Supply and Demand

• Demand side factors:

Availability of applications: HDTV/Cloud/Gaming/M2M/

Social Networking/…

For each application: Adoption rate – Age/Education/GDP

For each application: Data volumes/Data rates/Latency

Aggregation: Fixed = Home => Family

Fixed = Business => Professional SME

Mobile = Individual/Professional

9

What will customers need in 2025?

Modelled three demand scenarios

1. Bandwidth demand Status Quo Extrapolation of current growth trends

Data volume/Data rates/Ratios

2. Bandwidth demand – Case HDTV/UHDTV NextGen TV: HDTV/4k/8k

NextGen data compression

Aggregation of simultaneous use – Up market family

3. Bandwidth demand All-NGA – Case Germany Various applications and usage environments

Aggregation of simultaneous use

10

What will customers need in 2025:

Bandwidth demand Status Quo

11

What will customers need in 2025:

Bandwidth demand HDTV/UHDTV (1)

• Up market family:

Early adopters

Extra screen after one year

Family room with 8k

Source: EITOZetacast for Ofcom (2012) Generation Format

(pixels x lines; frames/s) Mpixel/s

Min.

viewing

angle (0)

SDTV 720p 1280 x 720; 50 46 20

HDTV1 1080i 1920 x 1080; 25

1440 x 1080; 25

52

39

HDTV2 1080p 1920 x1080; 50 104 30

UHDTV1 4kx2k 3840 x 2160; 50

4096 x 2048; 50

4096 x 2304; 50

4112 x 2168; 50

415 55

UHDTV2 8kx4k 7680 x 4320; 50 1659 100

12

What will customers need in 2025:

Bandwidth demand HDTV/UHDTV (2)

0

50

100

150

200

250

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

Total continuous 3D Total continuous

0.0

50.0

100.0

150.0

200.0

250.0

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

Total cont+disc-1 3D Total cont+disc-1

13

What will customers need in 2025:

Bandwidth demand All-NGA – Germany (1)

17% of population

5% of population

13% of population

15% of population

32% of population

18% of population

Sceptical Outsider

Occasional Users

Job Users

Trend Users

Enthusiastic Users

Smart Mobile Users

Source: D21, WIK assumptions, Expert judgment

14

What will customers need in 2025:

Bandwidth demand All-NGA – Germany (2)

SME segment Usage Number

Micro(Up to 9 employees and up to

2 mn Euro annual sales volume)

Standard User* ca. 590.000

Heavy User** ca. 2,7 Mio.

Small(Up to 49 employees and up to

10 mn Euro annual sales volume)

Standard User ca. 80.000

Heavy User ca. 165.000

Medium

(Up to 249 employees and up to 50 mn

Euro annual sales volume)

Standard User ca. 20.000

Heavy User ca. 35.000

Assumed number of companies

There is no structural change within

company and SME segments for the

future in Germany.

The vast majority of companies

operates within the micro segment of

up to 9 employees.

Medium-sized companies constitute

only a small fraction of the company

structure.

Assumption: One site per company.

Assumptions

15

What will customers need in 2025:

Bandwidth demand All-NGA – Germany (3)

16

What will customers need in 2025:

Bandwidth demand All-NGA – Germany (4)

„Top Level“-demand: 500 – 1000 Mbit/s downstream

300 – 600 Mbit/s upstream

„Medium Level“-demand:

150 – 500 Mbit/s downstream

100 – 300 Mbit/s upstream

„Top Level Plus“-demand: 1 Gbit/s and more downstream

600 Mbit/s and more upstream

Ca.12.1 mn households

Ca. 300.000 companies

Ca. 19 mn households

Ca. 3.5 mn households

Ca. 2,7 mn companies

Ca. 3.1 mn households

Perf

orm

ance o

f bro

adband

co

nn

ectio

n

„Low Level“-demand: up to 150 Mbit/s downstream

up to 100 Mbit/s upstream

Ca. 3 mn households

Ca. 590.000 companies

No broadband / Refusal

100% ∑ ca. 44,8 Mn.

29.7%

46.6%

8.7%

7.5%

7.5%

Source: WIK market potential model 2015

17

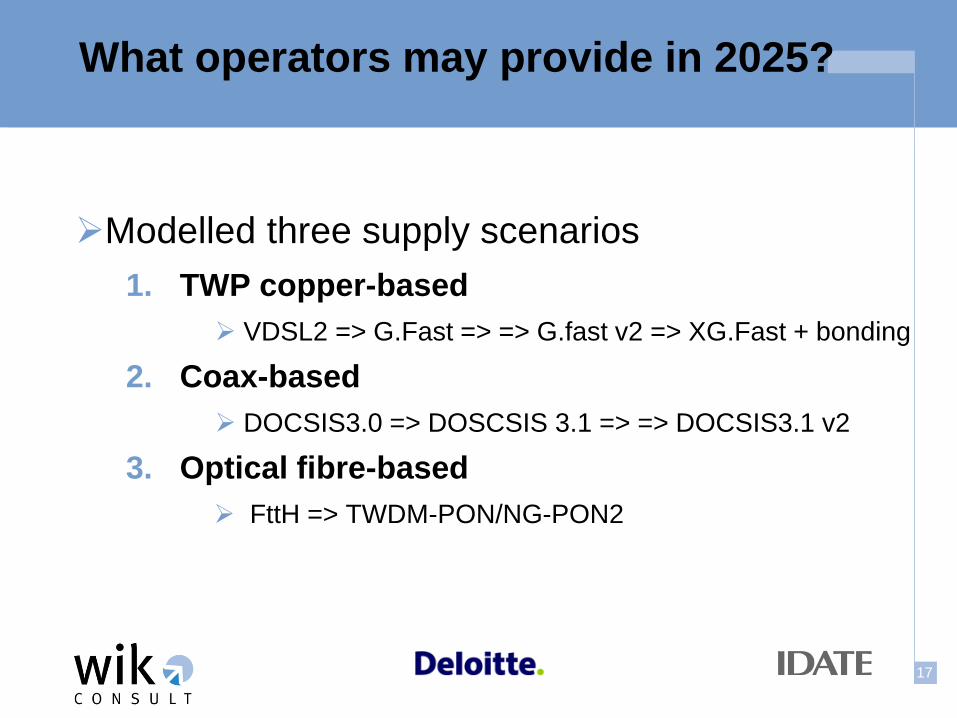

What operators may provide in 2025?

Modelled three supply scenarios

1. TWP copper-based

VDSL2 => G.Fast => => G.fast v2 => XG.Fast + bonding

2. Coax-based

DOCSIS3.0 => DOSCSIS 3.1 => => DOCSIS3.1 v2

3. Optical fibre-based

FttH => TWDM-PON/NG-PON2

18

What operators may provide in 2025:

TWP copper based

• Legacy PSTN networks:

Western Europe: ~100% of Households

Central Europe: ~60% of Households => Mobile broadband

Distance to local exchange

G.Fast @ 100 m:

Symmetrical – 250/250 Mbit/s

Availability: From 2017-2018

19

What operators may provide in 2025:

Coax based

Legacy CATV networks:

Europe: 0 - 95% of Households

Legend:

Last Amplifier for Distribution Point

Source: EITO (1999)

DOCSIS3.1:

Shared – 10/1 Gbit/s

=>=> 10/10 Gbits

Availability: From 2016-2017

20

What operators may provide in 2025

FttH – TWDM-PON

TWDM-PON:

4x – 10/10 Gbit/s

=>=>8x – 10/10

Availability: From 2016-2017

21

What customers need in 2025 - Status Quo

What operators could provide on copper

22

What customers need in 2025 HDTV-scen.

What operators could provide in 2025

23

What customers need in 2025 ALL-NGA

What operators could provide in 2025

„Top Level“-demand:

500 – 1000 Mbit/s downstream

300 – 600 Mbit/s upstream

„Medium Level“-demand:

15o – 500 Mbit/s downstream

100 – 300 Mbit/s upstream

„Top Level Plus“-demand:

1 Gbit/s and more downstream

600 Mbit/s and more upstream

Ca.12.1 mn households

Ca. 300.000 companies

Ca. 19 mn households

Ca. 3.5 mn households

Ca. 2,7 mn companies

Ca. 3.1 mn households(refusing Broadband/Internet)

Perf

orm

ance o

f bro

adband

connection

„Low Level“-demand:

up to 150 Mbit/s downstream

up to 100 Mbit/s upstream

Ca. 3 mn households

Ca. 590.000 companies

No broadband / Refusal

100%∑ ca. 44,8 Mn.

29.7%

46.6%

8.7%

7.5%

7.5%

Source: WIK market potential model 2015

FttDP/

FttLA

FttH

24

Could mobile technologies meet users needs?

-------5G 50 Mbps

25

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

Modelling NGA developments

26

Where does Europe stand today? Good level of coverage – but standard BB still dominant

75%

80%

85%

90%

95%

100%

PL

SK

EE

RO LV

HU

BG SI

ES IE

HR FI

EU

28

CZ

DE

LT

AT

DK

EL IT SE

BE

CY

FR

LU

MT

NL

PT

UK

73%

12%

8% 7%

basic BB FTTLA FTTH/B VDSL

Broadband coverage (% of households, 2014) Broadband mix (% of lines, 2014)

Source: IDATE based on EC Source: IDATE based on operators, NRAs

Add jap

In 2014, 27% of EU fixed broadband

lines are NGA, compared to 55% in

Japan

27

8,79

53,96

63,49

0 20 40 60 80

xDSL

FTTx

cable

0,86

25,43

7,65

0 5 10 15 20 25 30

Average bandwidth (Mbps)

Source: IDATE based on EC

downstream upstream

Where does Europe stand today? Average speeds of NGA technologies progressing rapidly

Ftth/c

28

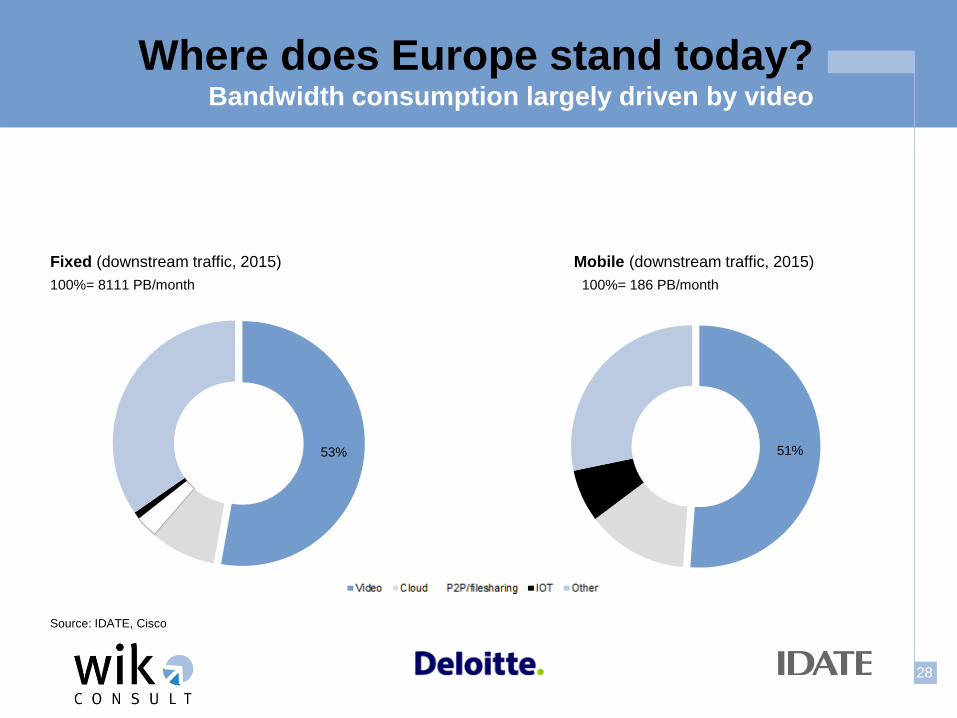

Where does Europe stand today? Bandwidth consumption largely driven by video

Source: IDATE, Cisco

53% 51%

Fixed (downstream traffic, 2015) Mobile (downstream traffic, 2015)

100%= 8111 PB/month 100%= 186 PB/month

29

Where might we stand in 2025? Many countries may miss DAE targets

• Several countries may miss

100Mbit/s take-up target

• Technological evolution and business

decisions will be critical

NGA take-up by country

EU-wide NGA take-up Source: IDATE

30

What can we expect in practice? 2025 horizon

Modelling future data consumption

• EU28 and reference countries: JP,US, CA, AU

• Bottom-up approach built around 4 major service types:

- Video

- Cloud

- M2M/IoT

- P2P

• 5th category: other (web browsing…)

• Different network deployment scenarios for the EU28

• Built on Cisco VNI, IDATE databases (World Internet Markets, World OTT Markets,

Future TV 2025, World FTTX Markets…) and other inputs (Ofcom, FTTH Council,

Sandvine, Nielsen..)

31

Where might we stand in 2025? Europe likely to lag in Internet usage in ‘status quo’ scenario

Evolution of fixed downstream traffic per geography

(fixed broadband traffic / line/month, EU28 2015 = 100)

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU28

100,0

119,0

141,9

169,5

202,4

232,3

268,7

311,7

361,7

420,2

488,4

US

185,8

224,3

271,4

329,3

398,6

464,2

542,6

628,4

723,4

828,3

945,8

CA

129,4

158,9

198,7

247,7

313,3

376,1

446,0

529,0

620,6

721,5

892,7

JP

65,8

87,9

117,4

156,5

208,3

255,4

316,1

386,6

477,7

584,0

721,2

AUS

83,4

100,4

117,0

144,6

180,1

212,1

232,1

271,3

310,2

355,0

406,5

Source: IDATE, based on proprietary research, Cisco VNI and other research

(GB/ line/month)

2015 2020 2025

EU28

62,0

144,1

303,0

US

115,2

288,0

586,8

CA

80,3

233,3

553,8

JP

40,8

158,4

447,5

AUS

51,8

131,6

252,2

32

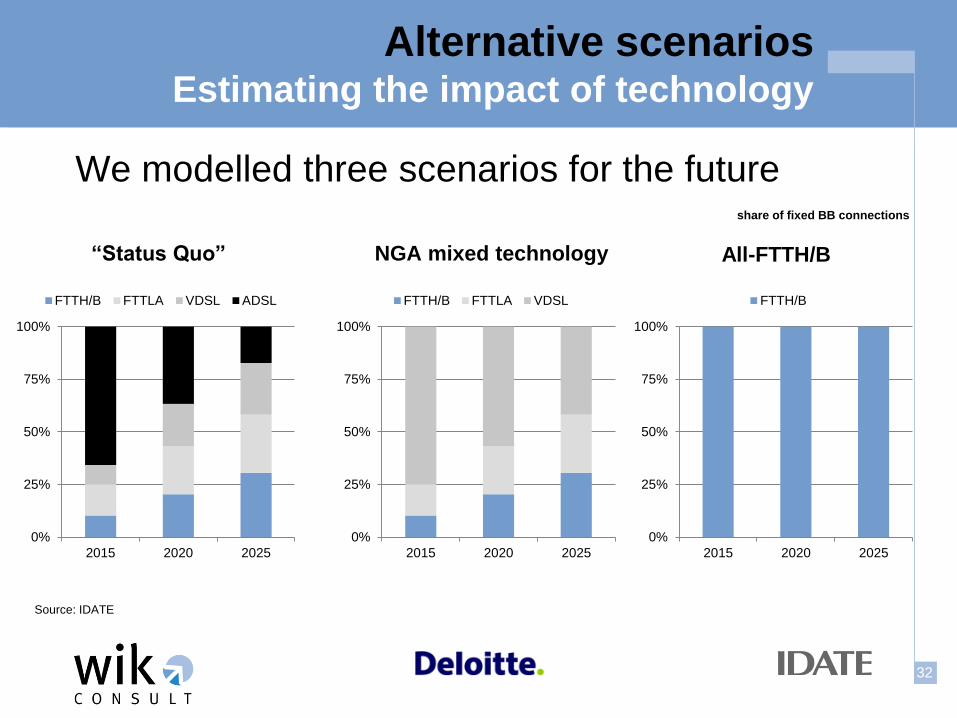

Alternative scenarios Estimating the impact of technology

We modelled three scenarios for the future

“Status Quo”

NGA mixed technology

All-FTTH/B

0%

25%

50%

75%

100%

2015 2020 2025

FTTH/B FTTLA VDSL ADSL

0%

25%

50%

75%

100%

2015 2020 2025

FTTH/B

0%

25%

50%

75%

100%

2015 2020 2025

FTTH/B FTTLA VDSL

Source: IDATE

share of fixed BB connections

33

Alternative scenarios

• Examined alternative scenarios

- NGA technology mix (FTTx and Docsis, xDSL phased out)

- All-FTTH/B

• Evidence for speed projections

- Samknows provides evidence of speed differential between technologies

and pace of speed increases

- Annual speed increases of 15-20% in line with Akamai data

- ADSL speed growth low to flat

• Evidence for consumption projections

- Ofcom, Palaiseau provide evidence of impact of FTTx technologies on

consumption

- Further insights from Japanese experience

34

Scenarios

further assumptions

• For status quo, all-NGA and FTTH assuming speed growth patterns

per technology from Samknows continue

• Speed growth may be fastest in FTTH/B

• Users of FTTH/B will tend to consume significantly more data than

users of constrained networks, once they have become used to the

quality of service

• Assumptions apply to technologies across the scenarios, outcomes

are driven by different technology mix

35

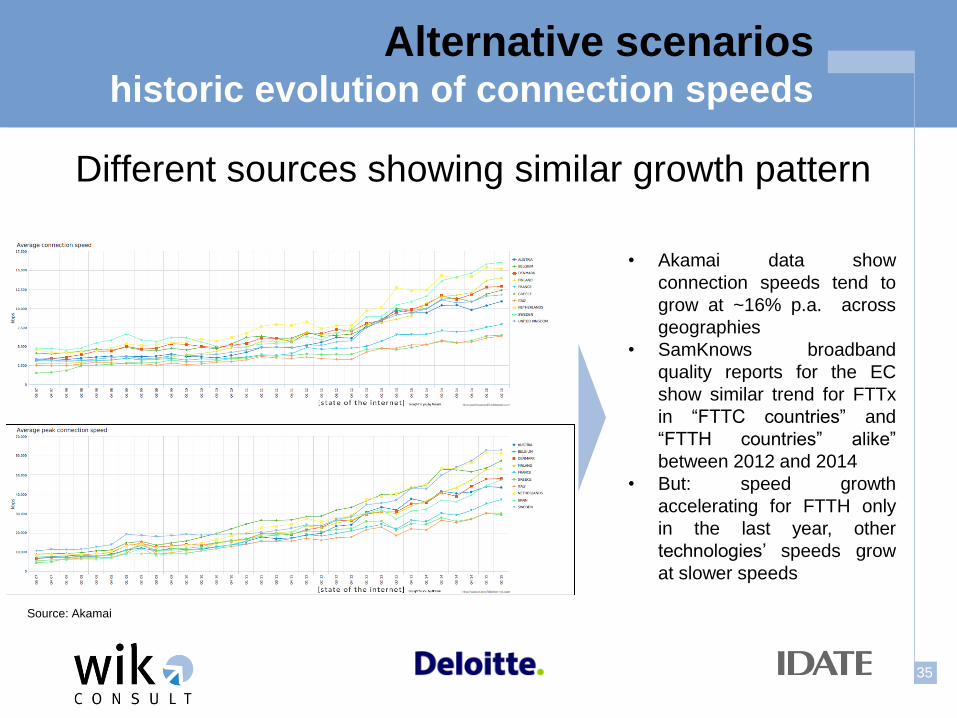

Alternative scenarios historic evolution of connection speeds

Source: Akamai

• Akamai data show

connection speeds tend to

grow at ~16% p.a. across

geographies

• SamKnows broadband

quality reports for the EC

show similar trend for FTTx

in “FTTC countries” and

“FTTH countries” alike”

between 2012 and 2014

• But: speed growth

accelerating for FTTH only

in the last year, other

technologies’ speeds grow

at slower speeds

Different sources showing similar growth pattern

36

Alternative scenarios further evidence behind FTTH/B scenario

Source: IDA Singapore Source: PTS

Source: Ovum

• Experience in FTTH countries show

• Speed packages from 100Mbit/s to

1Gbit/s (Singapore, Japan, SK)

• FTTH/B replacing cable

• Delayed bandwidth consumption

increases (Japan)

37

some evidence some evidence

Average connection speed per scenario (Mbps, EU28)

Alternative scenarios Impact on connection speeds to 2025

Outcomes

• Even in status quo scenario, bandwidth multiplied by 6.6 downstream, by factor 10 upstream

• FTTH/B downstream bandwidth in 2025 1.9 times ‘status quo’ ; 1.7 times ‘mixed NGA’

• NGA bandwidth estimates very much on the conservative side

• DAE goals could be met

28 51

77 77 99

163 185

203

345

8 14

54 29 34

113 84 88

236

0

70

140

210

280

350

SQ mixed NGA FTTH/B SQ mixed NGA FTTH/B SQ mixed NGA FTTH/B

2015 2020 2025

down up

38

some evidence some evidence

0

100

200

300

400

500

600

700

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 20250

10

20

30

40

50

60

70

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Fixed traffic per scenario (GB/ line/month, EU28)

downstream upstream

Alternative scenarios Impact on traffic levels

39

Where might we stand in 2025? EU to leapfrog other geographies in all-FTTH/B scenario (only)

Evolution of fixed downstream traffic per geography (GB/ line/month)

Source: IDATE, based on proprietary research, Cisco VNI and other research

611 587

554

448

382

303 252

-

100

200

300

400

500

600

700

EU

28

-FT

TH

/B

US

CA

JP

EU

28

-NG

A m

ix

EU

28

-SQ

AU

S

2 015 2 020 2 025

‘Ranking’ unchanged for mixed NGA scenario

40

What might the industry look like in 2025?

Key organisational trends impacting economics

Telecom-audiovisual convergence

• the Internet ‘s role in TV and video distribution will expand

• On-demand and individual consumption supported by the growing adoption of personal multimedia devices

- switch from a family package to a customized offer targeting the individual

- global consolidated content groups will be able to deliver products on all consumer devices

• communications network operators will have 3 options : maintaining ties with the consumers through vertical integration,

separating the network and retail sales business, or becoming meta-operators

Strategic options available to veteran TV market players

Source : IDATE, Future TV 2025, mai 2015

Source: IDATE

41

What might the industry look like in 2025?

Key organisational trends impacting economics

Fixed-mobile convergence

• Long-awaited convergence of fixed and mobile services finally materialising

• Significant take-up of 4-play bundles in certain markets

• Retail bundling attractive for users (through discount) and operators (lower churn)

• Convergence also driven by the evolution of networks with deployment of small cells, Wifi

off-loading etc…

Fixed/mobile bundle take-up

(Spain, 000s)

Source: CNMC

Max. theoretical

downstream speed

Backhaul capacity

required # of E1 lines

GSM 9,6 Kbps 1.3 Mbps 1

GPRS/

EDGE 171/384 Kbps 6?1 Mbps 4

HSDPA 14 Mbps 21 Mbps 14

LET-E 300 Mbps 40 to 300 Mbps 40++

Backhaul requirements

Source: IDATE

0

2.500

5.000

7.500

10.000

4Q/2011 4Q/2012 4Q/2013 3Q/2015

fixed and mobile telphony and broadband + pay -TV

fixed and mobile telphony and broadband

42

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

Prospects for bottlenecks

43

Will access bottlenecks remain? Fixed mobile substitution

• Some demand-side substitution amongst lighter users

(see eg Austria)… but otherwise complementary

- Mobile functionality will not support more demanding

residential (eg multi-screen HDTV) or business applications

- Pricing unlikely to support substitution for higher usage

- Trend towards converged bundled retail offers

• On supply-side potential threats and opportunities

- Next generation mobile relying increasingly on fibre backhaul

- Greater reliance by mobile operators on fixed assets? OR

- Potential for mobile operators to enter fixed markets as

infrastructure competitors?

Can fixed backhaul and fibre access be replicated?

44

Will access bottlenecks remain? Prospects for replicability vary by geography

Cost per customer and month at 70% penetration (FTTH/P2P without

inhouse cabling)

• Replicability more likely in dense urban clusters

• Some areas are clearly natural monopolies

• In rural areas (cross)-subsidies would be needed for viability

45

Will access bottlenecks remain? Replicability improved by facility sharing

• 2008 WIK study noted how replicability increased with facility sharing

• HCA duct costs and depreciation would likely improve picture

• ITU (2014) notes cost savings from network sharing could reach 40%

Mark

et

share

of

passed h

om

es r

equired f

or

pro

fita

bili

ty

Impact of passive access on the critical market shares of alternative operators in the

urban cluster – prices based on CCA-LRIC+ estimate

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FR DE IT ES

PON own infrastructure using 80% infrastructure sharing (duct access)

Fibre SLU with limited (20%) dark fibre and duct access

Fibre SLU with 80% dark fibre and duct access

46

Replicability in practice

• Case studies allow us to see how far

replicability is possible in practice for FTTH

- France: ~17% households are in ‘very dense areas’

where replicating FTTB is considered viable

• The NRA designated ‘very dense’ areas through an ex ante mapping

exercise, and later made adjustments (to reduce the area) as it learned

through experience

- Spain: 35% households are now in areas deemed

to be ‘NGA prospectively competitive’

• The NRA identified areas for prospective competition on the basis of

actual deployments and projections following a 6 year observation period

in which access to the incumbent NGA network was capped at 30Mbit/s

47

Conclusions from market trends

• Supply and demand of fast broadband are interlinked

• In the status quo, DAE targets unlikely to be met in many EU

member states, and Internet usage may lag other regions

• More widespread NGA or FTTH/B may increase speeds and usage,

although supply is not the only factor – demand-side also important

• Fixed access bottlenecks are likely to remain at least outside dense

urban areas

• Low cost duct access can improve the prospects for replication

• Fixed mobile convergence might provide scope for more stable

facilities-based entry and competition in fixed access based on own

infrastructure and network sharing

48

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

Business models

49

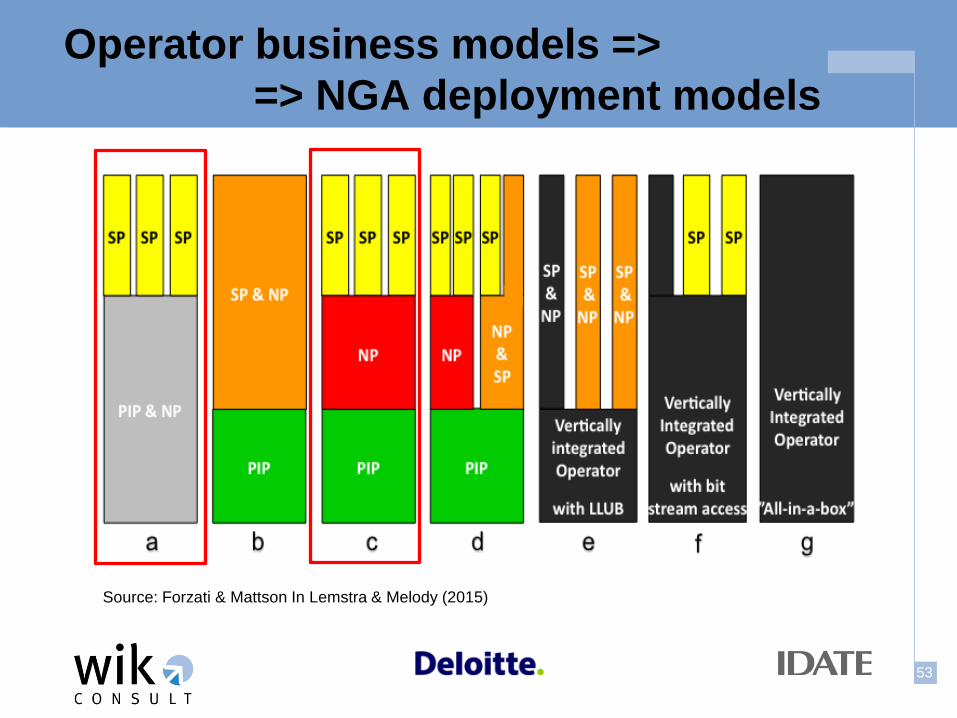

Operator business models =>

=> NGA deployment models (1)

• Type of business model - fully integrated… …structural separation;

- passive infrastructure provider… …service provider

• Type of technology deployed - wired – copper, optical; wireless

• Type of ownership – partnership - private, public, cooperative | PPP… …co-invest., sharing… …BOT

• Sources of funding – type of financing - Int./ext.; public/private, users, subsidy | cash flows, assets, project

• Degree of openness - network layer – passive and/or active layer; services layer

• Geographical scope - national, regional, municipal

•

50

• Incumbents – Legacy networks - PSTN => DSL modems => Increm. upgrades: VDSL/G.fast

=> Greenfield: FttH

- CATV => DOCSIS modems => Increm. upgrades: DOCSIS3.0/3.1

• Alternative operators - PSTN LLU => DSL modems => Increm. upgrades: ADSL2/VDSL??

=> Final rung: FttH

- FttH: Iliad => DSL + FttH

- FotF: SMEs in Bulgaria, Latvia, etc.

• New entrants – Demand aggregation – FttH - Private: e.g. Reggefiber + Housing corporations => Citizens, rural

- Public: Municipalities + Internal use => Citizens, rural

- Citizens: Cooperatives, rural

Challenge areas… ….Non-Challenge areas

Operator business models =>

=> NGA deployment models (2)

Non-Telco Models… ….Telco Models

51

Non-telco NGA deployment - NL:

Major cities… …Challenge areas

• Early case:

Amsterdam

• Demand bundling

• Non-telco actor

• Recent cases:

Cooperatives Bladelglas

MoergestelGlas

OirschotGlas

Reusel-DeMierdenGlas

KempenGlas

Etc.

52

NGA deployment - SE:

Major cities… …Challenge areas

• Early case:

Stokab

• Govt. funding

€800 million

- Studies

- Deployment

• 1 out of 2

municipalities

in FttH

53

Operator business models =>

=> NGA deployment models

Source: Forzati & Mattson In Lemstra & Melody (2015)

54

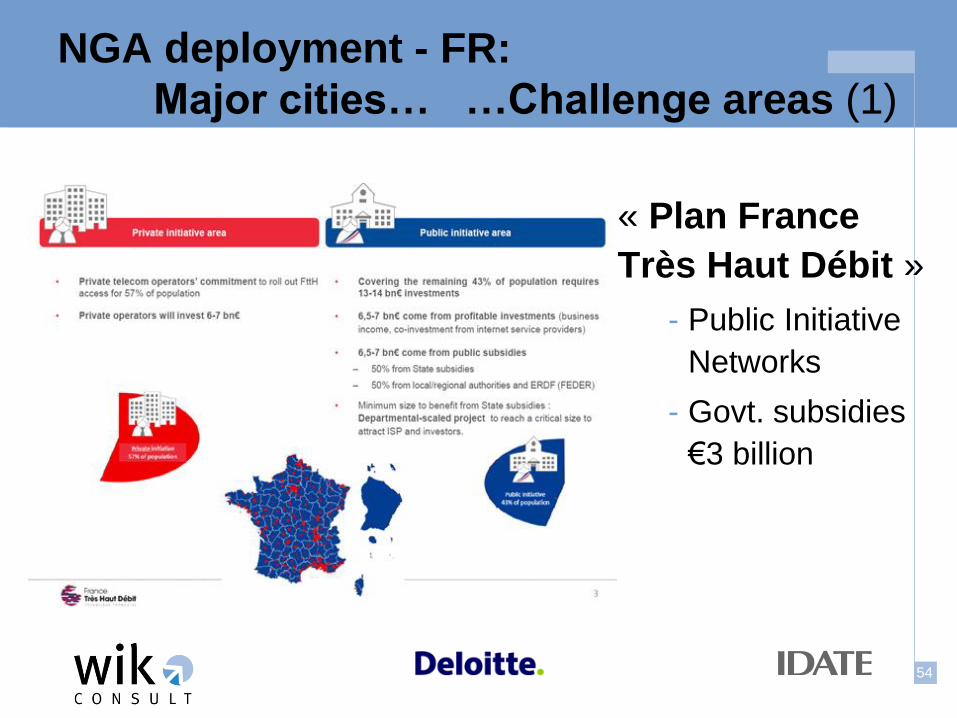

NGA deployment - FR:

Major cities… …Challenge areas (1)

« Plan France

Très Haut Débit »

- Public Initiative

Networks

- Govt. subsidies

€3 billion

55

NGA deployment - FR:

Major cities… …Challenge areas (2)

First Generation PIN -

DSL

Second Generation PIN -

FttH

56

Business models for NGA Challenge areas - conclusions

• Size of challenge areas is significant

• Role Non-Telco actors and Governments essential National NGA

Coverage Rual NGA Coverage

Ratio (National/Rural)

Share Rural HH

BG 69% 1% 49,9 20%

EE 83% 57% 1,5 22%

EL 34% 0% 74,6 20%

HR 57% 10% 5,6 23%

HU 80% 19% 4,1 31%

IE 71% 8% 8,9 37%

LT 97% 59% 1,7 31%

LV 90% 44% 2,0 29%

PL 53% 31% 1,7 21%

RO 69% 27% 2,5 21%

SI 78% 58% 1,3 25%

SK 63% 4% 14,6 29%

EU 28 68% 25% 2,7 14%

Source: EU Commission, Broadband Coverage in Europe 2014

57

Business models for NGA Commercial areas - incumbent NGA strategies

• Incumbents have pursued varying technological strategies for NGA

• FTTH often where disruptive alternative investors

• FTTC common strategy elsewhere. Belgacom pioneer (2004), extensive

deployments also by incumbent operators in UK, Germany

• Mainly (although not all) integrated models, some with long term

commercial wholesale offers eg NL, DE

NGA coverage by technology for selected incumbent operators 2010-2015

58

Business models for NGA Incumbent separation models

• BT agreed to implement functional separation in 2005

- Undertakings in lieu of reference to Competition Commission

- BT Group makes strategic investment decisions, but assets

deemed under control of Openreach – supplies mainly on basis

of EoI, Governance mechanisms to ensure equivalence

• O2 CZ applied voluntary structural separation in 2015

- Cited business streamlining, easing of regulation and

addressing financial needs

- Company facing significant infrastructure competition

• Both companies (for the moment) focus on FTTC

• Positive initial shareholder reaction

• FS may have supported BT market position vs cable

59

Business models for NGA Entrant NGA investment strategies

• In countries with intensive duct access focus – entrants

have ‘climbed the ladder’ to FTTH in dense areas

• Swaps and co-investment have been pursued by

operators to extend fast broadband coverage

- In Portugal VF concluded commercial FTTH co-investment with

PT on basis of long term IRU and passive access

- In Spain VF has concluded a co-investment arrangement with

Orange on FTTH and access to VF cable network

- France (less dense areas) characterised by regulated FTTH co-

investment amongst main operators on basis of IRU

• Joint ventures by alternative operators and energy

companies in Ireland (SIRO), announcements Italy (Enel)

60

Business models for NGA Commercial areas – conclusions

• Incumbent technological choice (FTTC vs FTTH) may be

influenced by initial competitive impetus

• Examples of incumbents offering wholesale access to

support position (long-term agreements or separation) –

especially where facing challenge of competing platforms

• Entrants have invested in FTTH in some countries

- A key enabler has been access to ducts – either regulated or

from utility partnerships

- Co-investment arrangements have helped to expand coverage

beyond dense urban areas

- Key question: what might foster participation of incumbent?

61

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

Regulatory models

62

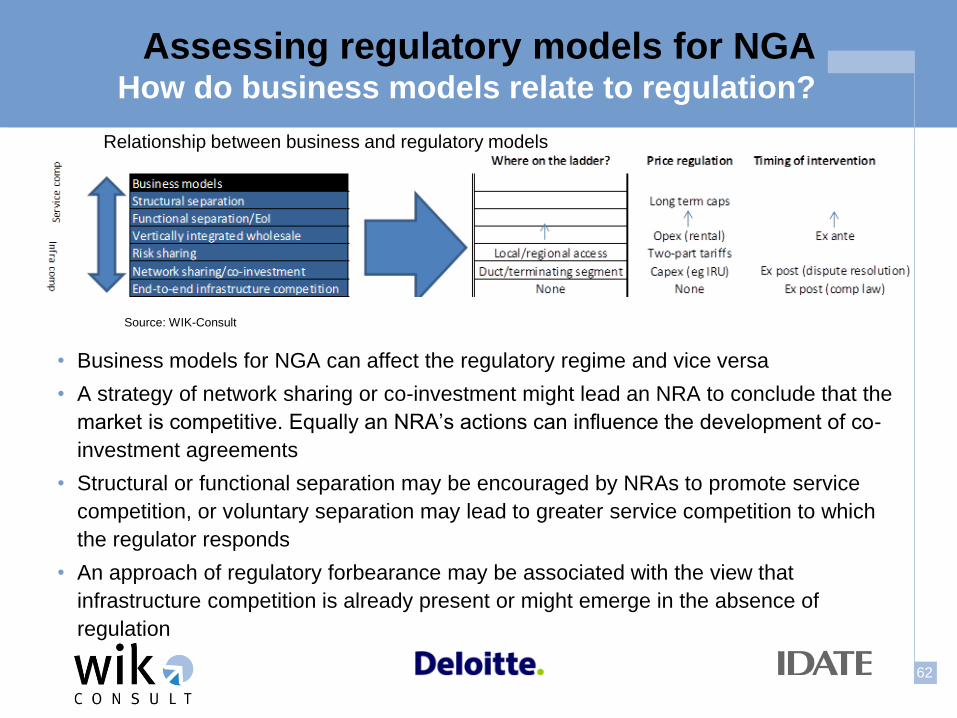

• Business models for NGA can affect the regulatory regime and vice versa

• A strategy of network sharing or co-investment might lead an NRA to conclude that the

market is competitive. Equally an NRA’s actions can influence the development of co-

investment agreements

• Structural or functional separation may be encouraged by NRAs to promote service

competition, or voluntary separation may lead to greater service competition to which

the regulator responds

• An approach of regulatory forbearance may be associated with the view that

infrastructure competition is already present or might emerge in the absence of

regulation

Assessing regulatory models for NGA How do business models relate to regulation?

Relationship between business and regulatory models

Source: WIK-Consult

63

• Strategies range from forbearance (US) to service competition (Australia)

• European models differ by whether they focus on a ‘climb up ladder’ or ‘stay on

the ladder’ or a combination. Romania example of infrastructure competition

Assessing regulatory models for NGA Which types of regulatory model are pursued?

Initial approaches on the ladder of investment

Standard broadband

(EU)

ForbearanceCl imbing up the

ladder

Remaining on the

ladderFul l ladder Service competition

Own

infrastructure

US,

Rom

ania,

Korea,

Canada

(FTTH)

Duct access

Subloop/termina

ting segment

Local access Nearly universa l

UK, N

L,

Belgium

,

Au

stria,

Sweden

Regional

(bi tstream)

access

In process of ful l or

geographic

deregulation

Au

stralia,

Canada

(FTTC)

Resa le Deregulated

Next generation approaches

Portugal, Spain,

France

Italy, Germ

any

Bro

adba

nd la

dder

of

inve

stm

ent

Source: WIK-Consult

64

Country NGA coverage % HH

NGA take-up % homes passed

Average download speed Mbit/s

Price telephony, TV Internet 30-100Mbit/s Mean rating

Average ranking

Austria 7 14 10 13 11 13

Belgium 1 4 8 12 6 4

Czech 12 16 4 6 10 9

France 14 10 14 2 10 11

Germany 8 13 11 10 11 12

Italy 15 15 16 7 13 15

NL 2 5 3 14 6 3

Poland 13 12 11 11 12 14

Romania 11 7 5 3 7 5

Spain 10 8 13 9 10 11

Sweden 9 2 2 4 4 2

UK 6 9 7 8 8 7

Australia 16 11 15 14 16

Canada 4 1 9 16 8 7

Japan 3 3 1 5 3 1

US 4 6 6 15 8 8

Source EC IDATE Akamai EC/Van dijk

Assessing regulatory models for NGA How do countries perform?

• On a range of measures, leading NGA countries are Japan, Sweden,

Netherlands and Belgium

• US and Canada perform well on coverage and have relatively high NGA take-up,

but prices are high and speeds are not exceptional

65

What drives NGA coverage? Role of infrastructure competition

Impact of cable on NGA coverage

• Cable is a key driver of NGA coverage. It can be readily upgraded to NGA

and has been seen to stimulate competitive NGA provision

• Cable explains most of the NGA coverage advantage in the US, Canada,

Belgium and Netherlands

• FTTH triggered by independent investors in several cases

66

What drives NGA outcomes?

• A wider view highlights that many factors (often non-regulatory)

influence NGA outcomes

67

What drives NGA outcomes? Insights from econometrics

• Negative correlation between infrastructure and access

competition

- Link may be causal or circumstantial

• NGA coverage

- Driven by cable coverage – no other factors are clearly

correlated

- No clear indicators explaining FTTH coverage

• NGA take-up (% HH >30M)

- Associated with lower NGA retail prices – which in turn are

linked to more access-based competition and LLU

- Linked to higher GDP and lower rural populations

68

• Actual average speeds

- Negatively linked to access-based competition (LLU and

generally) – may reflect fact that most access is based on

standard BB. It is also possible that LLU may improve standard

broadband quality and therefore make NGA relatively less

attractive

• Fixed capex

- Linked to higher capex in previous period and higher GDP – not

clearly linked to access competition or regulatory measures.

No clear link between fixed capex and NGA coverage

What drives NGA outcomes? Insights from econometrics (2)

69

• Limited

infrastructure

competition

• High prices for high

speeds (and

therefore low take-

up at high speeds)

• NB Canada has

service competition

on FTTC and cable

(but not widely

used), forbearance

on FTTH before

2015

What drives NGA outcomes? Forbearance - insights from US and Canada

70

• Duct access fostering

infrastructure-based

FTTH competition in

dense urban areas

• Competition elsewhere

through commercial

(Spain), or regulated

(France) co-investment

• Tendency towards

consolidation to 3 large

fixed/mobile players in

these markets

What drives NGA outcomes? Deep passive - insights from France and Spain

km of Telefonica subduct occupied – monthly

cumulative – all operators

Actual and planned FTTH coverage by operator

(m premises)

71

• The UK, Austria and Germany pursued flexible pricing for FTTC

NGA bitstream/VULA since 2010

• FTTH also covered by regime in UK and Germany (in theory) while

in Austria FTTH was not included in market analysis initially

• Technological outcomes have been FTTC in these cases

(some scaling back of initial FTTH ambitions)

• Incumbent commercial deployment appears to have extended

beyond cable areas – pricing regime may have played a role in

supporting additional reach

• What would have been/would be impact of applying only to FTTH?

• Limited infrastructure competition in these countries. Some service

competition on basis of NGA (less than for standard broadband) –

may be tied to incumbent speed/price offers

What drives NGA outcomes? Pricing flexibility - insights from UK, Austria and Germany

72

• There are a few examples of incumbent separation, but drivers and

context are different – affecting outcomes in each case

• Outcomes in Australia to date have been poor – delays and

uncertainty from changed Govt strategy as well as the planned

phase-out of infrastructure competition may have had impact

• In the UK functional separation:

- Seems not to have undermined NGA investment incentives (widespread FTTC

coverage, increasing take-up); and

- May have supported NGA wholesale access (greater take-up compared with

other countries); BUT

- It has not of itself incentivised further upgrades to legacy network – Ofcom 2016

DCR aims to foster FTTH through infrastructure competition

• Too soon to judge outcome from Czech separation

What drives NGA outcomes? Separation - insights from UK, Czech and Australia

73

• The influence of NGA regulation on outcomes is subtle. Regulation

may not be the most significant factor affecting NGA outcomes today

• Cable plays a strong role in influencing NGA coverage. GDP and

population density provides an important driver for take-up

• Case studies on specific NGA regulation approaches provide further

insights on the role of regulation:

- Forbearance may lead to high prices and limited take-up of high speed offers

- ‘Deep passive approaches’ (FR, ES, PT) have fostered FTTH infrastructure-

based competition in dense urban areas, but tend to more consolidated markets

- Pricing flexibility (UK, AT, DE) may have contributed to extending FTTC beyond

cable areas – what would be effect of applying only to high speed technologies?

- Structural separation could in theory undermine ‘buy build’ decisions and does

not seem of itself to incentivise upgrades of legacy network, but it could be

efficient in areas where only one network is viable

What drives NGA outcomes? Conclusions from regulatory analysis

74

• Regulation which supports fast broadband deployments may also

benefit business customers, but there are important differences (see

eg SMART 2014/0024):

- Business customers may require multi-site or multi-national provision

- Customers may demand consistent quality and service levels across multiple sites

- Business suppliers serving multi-national clients may not have sufficient scale in

every country to engage in co-investment, and therefore may rely on wholesale

access outside dense business districts

- Infrastructure-based operators focused on residential markets may not be willing or

able to offer wholesale products to meet business needs

• Regulation aimed at fostering competition and investment in residential

broadband may not completely address business market challenges

• Current national approaches to business access regulation do not tend

to reflect cross-border aspect

• Product characteristics (business bitstream) and SLAs can vary widely

Serving multi-national corporations Challenges for customers and suppliers

75

• Background to the study

• Future trends in high speed broadband

• Business and regulatory models

• Implications for the review of the EU framework for electronic communications

• Next steps

Agenda

76

Implications for the framework? Is there a problem?

Deployment and uptake trends suggest that Europe

may fail to meet the DAE targets and may fall behind

on Internet usage. Moreover there are significant gaps

between countries and between urban and rural areas

- Question 1: Do you agree with this analysis? If so, is it a

problem? How much of a problem? How might it evolve?

77

Implications for the framework? What should be objectives for the future?

There is evidence that fibre technologies are linked with

higher speeds, and potentially higher usage over time

- Question 2: Should it made clearer that the end-goal of the

framework is to achieve widespread availability and usage of

high performance broadband networks by citizens and

businesses?

There is evidence that disruption from infrastructure

competition stimulates NGA investment

Question 3: Should the framework set an objective to

foster infrastructure competition wherever feasible?

78

Implications for the framework? Are changes needed to the market analysis process?

• Many EU regulatory strategies described have been

implemented within the bounds of today’s framework,

but they are not required or central to the framework

- Infrastructure mapping pursued in Spain, France and increasingly

other MS, but not universal

- The regimes in France, Spain, Portugal rely more on symmetric

measures (eg in-building wiring) and forbearance on SMP

remedies than envisaged in the framework

- Co-investment and commercial arrangements are not specifically

discussed in the Framework

- The separation models in Europe have not been implemented

through the current framework

- The framework does not specifically address the promotion of

investment in challenge areas

79

Implications for the framework? Are changes needed to the market analysis process?

• Question 4: Should NRAs be required to undertake infrastructure

mapping in the context of market analyses?

• Question 5: Should symmetric obligations be considered within the

context of the market analysis process?

• Question 6: Should co-investment and/or commercial arrangements

be encouraged? If so how?

• Question 7: Are wholesale only business models a relevant tool to

promote the diffusion of NGA – generally or in less dense areas? If

so, should this model be incentivised under the framework?

• Question 8: What more could be done in the scope of the framework

to support NGA deployment in rural areas?

80

• In the context of reform to the access regime, it is also relevant to

consider where there is a need for consistent application of the

access rules and what are the implications for the institutional set-up

(Task 4 in the study)

- Question 9: What is the appropriate balance between flexibility for

NRAs and harmonisation at EU level in access rules?

- Question 10: What should be the role of the NRAs, Commission and

BEREC in a reformed framework?

Implications for the framework? Are changes needed to the institutional process?

81

WIK-Consult GmbH

Postfach 2000

53588 Bad Honnef

Deutschland

Tel.:+32 2 830 0380

Fax: +32 497 505641

www.wik-consult.com

![Untitled-1 [] · 2016. 5. 27. · Your flexible CATV solution provider COMTECH Tel.: +36 (96) 412 299 | Fax: +36 (96) 511 200 E-mail: mail@comtech.co.hu | WEB: DOCSIS3.1 compliant](https://static.cupdf.com/doc/110x72/610dca127ebe5836bf072ea4/untitled-1-2016-5-27-your-iexible-catv-solution-provider-comtech-tel.jpg)

![NG-PON2 · Network (ODN) (residential, business, backhaul), embedded test and diagnostics capabilities and PON resilience, including dual parenting [18]. TWDM PON was selected as](https://static.cupdf.com/doc/110x72/5e76968091974149a815ecbe/ng-pon2-network-odn-residential-business-backhaul-embedded-test-and-diagnostics.jpg)