ANNUAL REPORT 2005

Contents

Vision 1

Operational Philosophy 1

Ethos 2

Group Statistics 3

Directorate 4 – 5

Chairman’s Report 6 – 8

Chief Executive Officer’s Report 9 – 12

Corporate Governance 13 – 20

Annual Financial Statements 21

Report of the Independent Auditors 22

Directors’ Report 23 – 27

Income Statements 28

Balance Sheets 29

Statements of Changes in Equity 30

Cash Flow Statements 31

Notes to the Cash Flow Statements 32

Notes to the Financial Statements 33 – 62

Subsidiary Companies 63

Joint Ventures 64

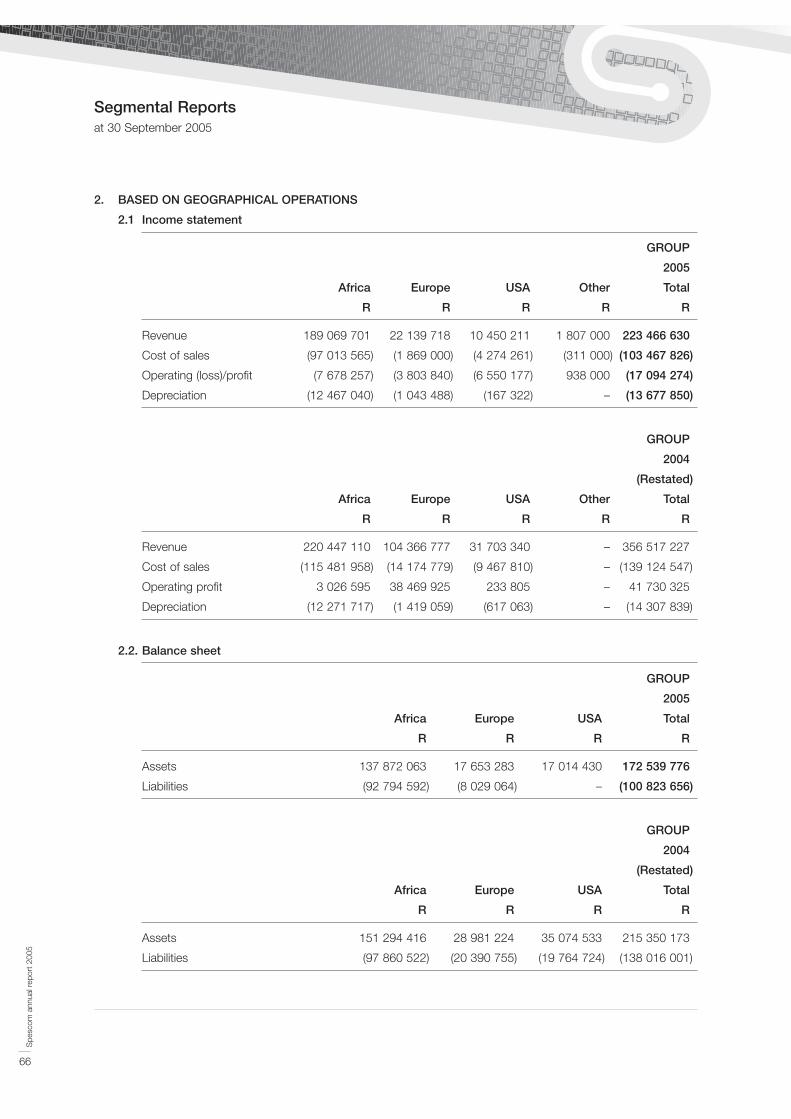

Segmental Reports 65 – 66

Directors’ Remuneration 67

Directors’ Share Options 68 – 69

Notice of Annual General Meeting 70 – 71

Annual General Meeting – Explanatory Notes 72 – 75

Administration 76

Shareholders’ Diary 76

Form of Proxy Inserted

Shareholders’ Update Form Inserted

Contact Details Inside Back cover

Spescom Vision

To see all leading organisations worldwide utilising Spescom’s products and solutions

to manage information and connect to the networked knowledge economy.

Operational Philosophy

In pursuit of our vision, Spescom promotes a culture that focuses on a five-point operational strategy:

1. COMMITMENT TO QUALITY – As an ISO 9001 company, Spescom’s commitment to quality is effected by

developing and maintaining close relationships with all stakeholders, thereby enabling us to understand and

cater for their requirements in an innovative and cost-effective manner.

2. COMPETE THROUGH INNOVATION – We are committed to sustained innovation through continued research

and development in our selected markets. Speed in bringing product to market is our priority. We encourage

our people to be innovative, not only technologically but in all aspects of business.

3. COMPETITIVE ADVANTAGE – Our objective is to dominate the markets in which we operate by formulating a

comprehensive competitive strategy that takes cognisance of the characteristics of the market as well as

knowledge of competitors.

4. GLOBALISATION – We strive to globalise our business in terms of allocation of resources and market

penetration. We will continue to identify and establish markets offshore.

5. SHORTER LEAD TIMES – We are committed to sustained programmes that lead to cost reduction and

productivity improvement in all areas of operation. Our objective is to shorten cycle times in all we do.

Spe

scom

ann

ual r

epor

t 20

05

1

Ethos

Ethos: Spirit or values of a community

THE SPESCOM ENVIRONMENT

Business is conducted in an atmosphere of professional entrepreneurship. Spescom’s perspective is global, thus

constant change is inevitable as we strive to be innovative in a highly competitive market. Successful growth is

achieved through individuals committing themselves to customer satisfaction and ‘the greater good of the

company’. This is to enhance the pervading sense of purpose – of building for the future.

Spescom has a long-term view of business

SPESCOM IN BUSINESS

To be proactive and achieve innovation, one must be passionate about business. However, the aggressive business

attitude is always influenced by the deep respect for human dignity and ethics so essential in negotiation. At

Spescom, we believe in the notion of ‘a deal is a deal’. It is expected that all who interact with Spescom mirror this

strong sense of business ethics that characterises operations. This sense of dignity is harnessed in entrepreneurial

individuals who are businesspeople, who respond to quick-paced action and change effectively, realising the

opportunities and outperforming the competition.

Spescom is passion and competence in business

THE SPESCOM FAMILY

In a dynamic, innovative industry, only a certain type of businessperson flourishes. Spescom is ideally suited to the

assertive self-starter who operates best in a team environment. Competency combines with honesty when one

respects the dignity of others in all transactions. We do not hide bad news from each other. Spescom recognises

and rewards performance, banking on the high level of intellectual capital available and supporting ambitious

business people with clearly defined company and personal goals.

When a group of winners work together, the result is success

Spe

scom

ann

ual r

epor

t 20

05

2

Group Statistics

Africa

International

15,4

84,6

38,2

61,8

2005 2004GEOGRAPHICAL REVENUE STREAMS

Own IP

3rd Party IP

2005 2004

61,4 38,6 53,0 47,0

PROPRIETARY TECHNOLOGY

Enterprise contentmanagement solutions

Communications

Services & other

2005 2004

21,5 59,8

18,7

10,4 71,2

18,4

REVENUE SPLIT

Spe

scom

ann

ual r

epor

t 20

05

3

Directorate

Tony Farah (57) BSc (Eng), MBA, AMP (Harvard)

Chief Executive Officer – Spescom Group

Member of Nomination Committee

Hilton J Isaacman (52) CA (SA)

Executive Director – Corporate Finance

Thomas Makore (40) Bsc Eng (Hons), MBL, Pr Eng, C Eng

Chief Executive Officer – Spescom Telecommunications

Dr James P Myers (65) American

PhD (Maths)

Independent Non-Executive Director and Chairperson

Acting Chairperson of Nomination Committee

Member of Audit Committee

Walter Kansteiner (51) American

Independent Non-Executive Director

Spe

scom

ann

ual r

epor

t 20

05

4

Mutle C Mogase (41) BCom, EDP (New York)

Non-Executive Director

Member of Audit Committee

Member of Nomination Committee

Colin Rezek (50) BCom, MBA

Alternate Non-Executive Director

Directorate

Lynne Ogilvy (51) BSc (Maths)

Independent Non-Executive Director

Chairperson of Remuneration Committee

Nyeleti Magadze (32) BProc, HDip Tax

Company Secretary

Phillip Vallet (58) BA LLB

Non-Executive Director

Chairperson of Audit Committee

Member of Remuneration Committee

Jené I Palmer (35) BCom, BCompt (Hons), CA (SA)

Chief Financial Officer

Member of Nomination Committee

Spe

scom

ann

ual r

epor

t 20

05

5

Chairman’s Report

This has been a demanding year in

the South African ICT arena.

Companies specifically involved in

telecommunications have been

frustrated by the lack of movement

in the sector. Deregulation became

a legislative reality on 1 February

2005, but little followed in the way

of true liberalisation of the market.

It would be inappropriate to

minimise the challenges we have

faced this past year. Difficult

decisions had to be made to

ensure Spescom remains well

positioned to capitalise on

opportunities resulting from the full

deregulation of the telecoms

sector. We have been forced to

manage costs in a manner that

guarantees that situation. This

strategy is evidenced by the

manner in which we supported

Spescom Software in its efforts to

obtain the necessary financing to

bolster product marketing. The

result has been a change in the

relationship between Spescom and

Spescom Software that over time

should benefit both companies.

We expect to continue in our

support of their efforts and believe

their future will be secured by

aligning with a powerful market

leader in their specific business

arena. The altered relationship will

allow Spescom’s management

team to devote their energies to

prospects that will more directly

impact value enhancement for

group shareholders and

employees.

Looking at the history of the South

African telecoms industry it is

difficult to predict how the market

will evolve. However, the SNO was

licensed at the end of 2005 and it

is expected that this development

will produce lucid information on

where Telkom will focus its efforts.

The anticipated aggressive start up

budget of the SNO alone should

stimulate the sector and promote

competitive expansion in the

market as a whole.

Spe

scom

ann

ual r

epor

t 20

05

6

Spescom’s strategic direction remainsfocused on value creation for allstakeholders. In this regard we are devoting our energies to maximising ourpotential and growing the business.

Jim Myers

Independent Non-Executive

Chairman

Chairman’s Report

It is predicted that the SNO will

emphasise a more modern,

upgraded network for corporate

business. Our challenge will be to

assure this focus will result in

business opportunities for Spescom.

Internationally, telecoms has also

been in a slump but trends are

indicating that this is changing. We

anticipate the world market will

improve this year, providing an

additional catalyst for local

advancement.

Moreover, the telecoms needs on

the African continent hold great

promise for the company in light of

the unique understanding and

knowledge we can bring to bear

on the technology requirements of

emerging nations. This expertise is

founded on almost 30 years’

experience of doing business in

this region. At considerable

expense, we have maintained our

key resources, without which we

would not be positioned to take

advantage of these opportunities.

GLOBALLY

Last year we experienced a weak

global economy, the effects of

which were clearly visible in the

telecommunications sector which

experienced very poor growth.

However, there are signs of a

recovery underway which will

positively impact on spending.

Africa specifically is recognised as

one of the few remaining

developing markets where

aggressive expansion is predicted

for telecommunications.

Spescom’s strategic direction

remains focused on value creation

for all stakeholders. Our

unwavering commitment to this

objective has underpinned all of

the difficult tactical decisions that

have recently been made.

In this regard we are devoting our

energies to maximising our

potential and growing the

business. This will be achieved by

maintaining strong client

relationships, preserving key

growth skills, expanding our

knowledge base in line with the

evolving sector and diligently

preserving our financial capability.

Our globalisation strategies are

very much on track. Spescom

DataVoice has made substantial

progress in broadening its

international channels to market.

New distributors and value added

resellers have been signed up in

both Europe and the Middle East.

Our assertive marketing campaign

is already yielding results with

orders emanating from these new

business conduits.

On the South African front, the

addition of a performance

management component, in the

shape of the Qnique Insight

product, to Spescom DataVoice’s

current market offerings is an

exciting prospect. It positions both

the call centre operation and the

voice transaction management

division to bring a comprehensive

contact centre and voice recording

solution to the market.

PROSPECTS

The long awaited opening up of the

telecommunications sector is

expected to become a reality in

South Africa. We are seeing clear

indicators that global investors

recognise the potential for value

creation in emerging markets such

as sub-Saharan Africa. It is

acknowledged that the region is

viewed as one of the few remaining

areas capable of yielding strong

growth in the next ten years.

ICT sector valuations have

significantly increased in the last

year with foreign investment being

seen as a boost to expansion,

which should in turn attract

attention from South African

suppliers and operators.

Spescom’s continued focus on

telecoms as one of its core

business activities puts the

Spe

scom

ann

ual r

epor

t 20

05

7

Chairman’s Report

company in a strong position to

take advantage of the dynamics at

play in this market. Through

existing relationships, augmented

by our reputation for service and

quality, we expect to see

opportunities emerge.

The business plans implemented

for our in-house developed

DataVoice technology products are

beginning to show results. The

restructured operation with a

closer association with the

DataFusion division is yielding

results. We are finding that South

African based technology provides

some unique advantages in the

global market. Spescom’s voice

solutions remain one of the most

advanced technology offerings

available, all of which translates

into competitive edge.

As the South African and other

African economies continue to

develop with increasing business

competition and capacity,

DataFusion should see improved

opportunities to offer turnkey

services in the call centre market.

Spescom’s product line and

service continues to be recognised

as best in class.

WORLD CUP FEVER

The positive economic effects of

hosting the world’s biggest

sporting event, after the Olympic

Games, in the shape of the 2010

World Cup, cannot be

underestimated.

It may seem very far away but

preparation and planning for the

right technology to be in place to

assure a successful hosting is

already underway. The media are

currently exposing the

implementation of plans for

upgrades in various sectors

including security, rail and airport

services.

The technology needs on the

broadcast and telecommunications

side will hold great opportunity for

Spescom’s divisions operating in

these areas.

The company is looking forward to

the challenges and business

potential that South Africa’s

hosting of this major event will

afford.

APPRECIATION

I would like to take this opportunity

to thank management, staff and all

stakeholders for their continued

hard work and support.

The Spescom team all join me in

expressing our appreciation of our

customers and their continued

confidence in our products,

services and staff. As with any

company, Spescom’s success

hinges on their ongoing

commitment and loyalty.

Jim Myers

Independent Non-Executive

Chairman

Spe

scom

ann

ual r

epor

t 20

05

8

Chief Executive Officer’s Report

FINANCIAL RESULTS

Spescom achieved a headline

earnings profit of R26,2 million.

This translates into 36,1 cents per

share (cps) for the year in contrast

to 63,5 cps for the comparative

year.

Subsequent to taking into account

the non-trading items and the

decision to write off all offshore

loans owing to the Group,

Spescom reports a loss for the

year of R3,4 million as compared

to a profit of R29,4 million for the

previous year.

However, it is rewarding to note

that the results for the second

six months of the year reflect a

vast improvement on those of

the first half.

During the year under review, the

Group restructured its shareholding

in its US operation, Spescom

Software Inc., facilitating external

financing and permitting the

redeployment of critical resources.

This has resulted in this investment

being equity accounted with effect

1 April 2005 as well as in a

recoupment of R52,6 million prior

year minority losses.

The gearing levels of the Group

remain satisfactory and largely

unchanged. Subsequent to year

end, the Group made further debt

repayments.

A RETROSPECTIVE VIEW OF

THE YEAR

This challenging year has been

characterised by business gaps in

the form of large contracts coming

to an end and not being replaced

swiftly enough by new deals. This,

of course, translates into

undesirable lulls in the revenue

stream. Spescom’s

telecommunications business in

the United Kingdom is one such

example. One large commitment

Spe

scom

ann

ual r

epor

t 20

05

9

Spescom is entering a new cycle in itshistory focused, aggressive, highly ambitiousand intent on unlocking the inherent value ofthe company. Tony Farah

Chief Executive Officer

Chief Executive Officer’s Report

came to an end and despite

arduous commercial exertions,

replacement with a contract of

similar size and value has proven

to be difficult to date.

The depressed revenues in the first

financial half can be directly

attributed to the unpredictability and

lack of movement in the South

African telecommunications market.

Deregulation remains little more than

an announcement – made earlier in

2005 – with the reality of the

situation being that this proclamation

has had little or no positive impact

on trading conditions in this arena.

Liberalisation is slow to take place,

leaving the telecoms business still

heavily dependent on large deals

and a small customer base.

Uncertainty in this market has also

contributed to delays in the

finalisation of large commitments as

well as the awarding of new

contracts.

However, it is hoped that the

licensing of the second network

operator will lead to movement in

the sector.

The first half of the year also saw

Spescom divesting itself of its Test

and Measurement operation,

which market sector formed the

foundation of the company’s early

days. Despite not being core

business for some time, Spescom

continued with this operation due

to its profitability. However, grey

importing and eroded margins

have latterly led to a steep decline

in profit prompting the decision to

exit this arena.

IMPROVED SECOND HALF

Overall the performance for the

second half of the year was much

improved. Notably, the Group’s

broadcast division, Spescom

Media IT, and contact centre

operation, Spescom DataFusion,

performed exceptionally well. This

included major institutional

corporate network rollout with

voice over IP functionality.

There are even more exciting

prospects for Spescom Media IT

with Avid Technology broadening

the terms of its current sole

distributorship agreement to

encompass exclusive rights to

market Avid’s newly acquired

range of Pinnacle broadcast

products. This development

followed on the heels of Avid’s

acquisition of Pinnacle Systems.

During the period under review,

Spescom DataVoice entered into a

strategic alliance with Key

Performance Technologies (KPT),

extending its range of market

offerings to include Qnique, a

powerful contact centre

performance assessment tool. The

product has been rebranded

DataVoice Qnique Insight and will

include a DataVoice

communications recording

component.

Spescom Telecommunications

successfully concluded strategic

alliances with the global leaders in

the wireless market – Samsung,

Redline and Gilat – a leading

supplier of satellite products. This

leaves Spescom uniquely well

positioned in this arena for the

expected uptake of these

technologies in South Africa.

Overall for the year, the Group’s

expense base has been up due to

investment in greater skills levels

and the acquisition of new people

aimed at driving an aggressive

sales and marketing campaign.

It is pleasing to note that our

customer base of “blue chip”

companies continues to grow and

includes such well known names as

IBM, Telkom, SABC, Old Mutual

and Auto & General, to name a few.

EXPANDING GLOBAL

CHANNELS TO MARKET

Internationally Spescom remains

focused on the globalisation of its

own products and technology.

Spe

scom

ann

ual r

epor

t 20

05

10

Chief Executive Officer’s Report

In support of these objectives

Spescom increased its global

footprint by breaking into Middle

Eastern markets. The channels to

market set up in that region by

Spescom DataVoice have started

to yield results.

Moreover, the UK office has

successfully focused its energies

on growing and working the

channel to identify specialised

niche applications for the

DataVoice range.

Spescom Software Inc. the

NASDAQ bulletin board

company, has excelled in

establishing the product range

in the content management

space, which is identified as the

future technology wave.

However, during the build-up

phase over the last few years the

brunt of the financial losses have

been fully borne by Spescom –

due to its 51% shareholding. The

returns for the first half of the

year under review exemplify the

situation. Moreover, the ongoing

cost of going to market and

providing the required level of

financial support for a US$

operation from a Rand-based

concern is punitive. This has

necessitated the raising of

expensive short-term funds from

US sources.

The resultant dilution of Spescom’s

interest in this enterprise – bringing

it below 51% – has brought about

the decision not to consolidate the

Group’s investment in Spescom

Software Inc. This can be viewed as

the first step in Spescom’s tactical

plan to find a powerful equity

partner to broaden Spescom

Software’s marketing footprint.

This opens up a possibility of new

structures to bring in the necessary

strategic ownership by leaders in

the market.

The profits arising on the minority

interest, due to the restructuring of this

offshore investment, have positively

affected headline earnings per share.

The Group has taken a conservative

view in writing off loans owed to it

by Spescom Software Inc.

BLACK ECONOMIC

EMPOWERMENT

Spescom continues to prioritise its

BEE programmes.

From an equity perspective the

Group’s BEE standing is high, with

25,4% of Spescom Limited being

owned by Vantage Capital – a

majority black owned venture

capital concern. Moreover, 40% of

Spescom Telecommunications is

held by wholly black owned

Puisano Telecommunications.

The Group is already actively

pursuing plans to upgrade its

empowerment status in all areas

and in this regard has

commissioned a BEE audit in order

to highlight where improvements

can be effected.

PROSPECTS

Business is cyclical in nature. It is

affected by market conditions and

the prevailing economic climate.

Companies go through a well-

defined life-cycle pattern which

includes a peak and trough

scenario.

Earlier this year one of the South

Africa’s major daily newspapers –

Business Report National,

March 7, 2005 – took a

retrospective look at the

Johannesburg Stock Exchange

and examined the listings over the

past ten years.

The first time the stocks page was

published in Business Report,

there were 638 listings. Ten years

later, the number had shrunk by a

staggering 37% to 400.

Only 60 of the companies currently

listed on today’s exchange

survived the decade.

Spescom is cited as one of those

enduring names.

Spe

scom

ann

ual r

epor

t 20

05

11

Chief Executive Officer’s Report

Spescom is an interesting enterprise

that has prevailed in the face of ups

and downs in the IT industry. It is a

company that boasts many

technological world firsts.

It has always been the company to

watch – this has been shown time

and again since its listing in 1987.

Spescom is entering a new cycle

in its history focused, aggressive,

highly ambitious and intent on

unlocking the inherent value of the

company.

The business targets for the next

two to three years are ambitious.

The Group intends to take a

forceful lead in the core business

areas of the ICT sector. In doing

this Spescom will explore

acquisitions in order to accomplish

its strategic objectives.

Spescom will continue to focus on

content management and is actively

strengthening the application side of

its technology offerings.

The main emphasis will be on

telecommunications and voice.

In the telecommunications sector

opportunities are expected to come

on line in 2006. However, the results

of this may not become apparent

until the 2007 financial year.

Voice is recognised as a key

technology driver in 21st century

business. Spescom is a leader in

this field, as evidenced by the

global achievements already on

record, including the world’s first

speaker verification technology and

other applied applications in this

field. The company’s

understanding of this market

sector is formidable.

Business is increasingly conducted

on the move, with the demands on

customer service levels growing

exponentially. Contact centres,

voice recording, speaker

recognition and performance

management assessment – for

both customer service and legal

requirements – denote voice as a

major technology mover.

The contact centre business

continues to grow with the world

trend towards offshoring holding

great potential. Market research

houses have indicated that India’s

grip on this market is decreasing,

which in turn will provide

opportunity for South Africa.

The reality of the convergence and

synergy of contact centre and

voice technologies is unassailable.

Spescom is exceptionally placed

to benefit from these trends.

Spescom Media IT is well

positioned to take advantage of

the opportunities that will emanate

from the awarding of the soccer

World Cup in 2010.

In any country the business

landscape changes all the time.

One of the most important

changes in the history of South

African business is imminent –

namely the opening up of the

telecommunications arena through

the introduction of competition.

Telecoms is acknowledged as a

growth enabler in all sectors of any

economy.

From Spescom’s perspective, the

company is well placed, with its

product and service profile and

strategic planning, to capitalise on

the opportunities expected to

emanate from the expected new

phase of the SA business

environment.

Tony Farah

Chief Executive Officer

Spe

scom

ann

ual r

epor

t 20

05

12

Corporate Governance

Corporate governance may be

defined as the guardianship of a

company’s standards of integrity

and dedication to the interests of

all stakeholders, including investors,

customers and staff.

It is an intricate and diverse subject

composed of an anthology of

ideologies. Moreover, good

governance is far more complex

than the mere confines of statutory

compliance. It should encompass

active concern for a company’s

strategy and how it is implemented.

Global market research indicates

that companies reflecting

transparency of dealings,

augmented by good governance

practices, show a stronger

investment profile. Therefore, it can

be said that success in the

modern business environment is

inextricably linked to the

implementation of sound

governance procedures.

Spescom’s approach to corporate

governance is founded on six

fundamental principles, namely:

accountability, transparency,

responsibility, independence, fairness

and corporate social development.

These principles serve to boost

Spescom’s existing strong set of

values and business ethics, as

detailed in the company ethos.

The Spescom Group is committed

to adhering to the doctrines of

good governance as detailed in the

King Report on Corporate

Governance for South Africa

2002 (hereafter referred to as “the

King Report”).

The Spescom Board continually

strives to adhere to these values

and applies them in decision

making processes as well as all

aspects of its business dealings.

The Board of Directors is satisfied

that the correct systems are in

Spe

scom

ann

ual r

epor

t 20

05

13

“Organisations endure, however, in proportionto the breadth of the morality by which theyare governed. Thus the endurance of anorganisation depends upon the quality ofleadership; and that quality derives from thebreadth of the morality upon which it rests.”Chester Irving Barnard (1886 – 1961)

American business executive, public administrator and sociological theorist

Nyeleti MagadzeCompany Secretary

Corporate Governance

place to practise and improve the

principles of good corporate

governance within the Group.

BOARD OF DIRECTORS

The Spescom Board Charter

defines the parameters of

interaction for the Board. It is a

comprehensive policy document

the contents of which clearly define

the Board ethos, its constitution,

the roles of the Chairman, CEO,

and the appointment of directors.

The Charter also details the

responsibilities of the Audit

Committee.

The establishment of a charter is a

King Report requirement as well as

a recommendation of the JSE. The

full Charter may be viewed on the

Spescom website by clicking on

the appropriate link.

The Board structure and

composition has been devised in

accordance with the dictates of the

King Report and JSE Listings

Requirements and predominantly

consists of non-executive

directors. The composition

guarantees a balance of power

and circumvents dominance, by

any individual, in decision making

processes.

Non-executive directors are

selected for the broad base of

knowledge and experience that

they bring to the Board.

As reported in the previous financial

year, and in accordance with the

JSE Listings Requirements and the

King Report recommendations, the

roles of CEO and Chairman have

been divided.

Non-executive directors:

• Mr M Mogase

• Mr P Vallet

• Mr C Rezek (alternate non-

executive director to

Mr M Mogase)

Independent non-executive

directors:

• Ms L Ogilvy

• Mr W Kansteiner

• Dr J Myers

During the period under review, the

Remuneration Committee adopted

a decision to institute service

contracts for executive directors.

At the expense of the company,

directors may also seek counsel

from independent professionals,

when required. The Company

Secretary acts in an advisory

capacity to the Board.

Board members are compelled to

declare their interests in material

contracts regarding the Group.

This serves to negate conflicts of

interests. These include

shareholdings in Spescom and

other directorships. Where

necessary, it is mandatory for

Board members to excuse

themselves from involvement in

discussions or decisions that could

be influenced by vested interests.

The table on page 15 details

Board meeting attendance by

Spescom directors, for the period

under review, noting both

resignations of previous, and

appointment of new members.

Directors are subject to retirement

by rotation and re-election by

shareholders at least once every

three years in accordance with

Article 13.1 of Spescom’s Articles

of Association.

Appointment of Directors

During the period under review, the

Board resolved to reinstate a

dedicated nomination committee

tasked with the selection of

appropriately skilled and

experienced Board members. The

purpose of the Nomination

Committee is to evaluate the

structure and composition of the

Board and appoint members in

accordance with company

requirements, current trends and

business climate. The Committee

Spe

scom

ann

ual r

epor

t 20

05

14

Corporate Governance

Spe

scom

ann

ual r

epor

t 20

05

15

Board Meetings

1 October 2004 – 30 September 2005

During the past financial year, the Board has met on six occasions. Attendance of directors at Board meetings for

the period under review was as follows:

08/10/04 12/11/04 11/03/05 24/05/05 12/08/05 20/09/05

Special Special

Directors’ Directors’ Directors’ Directors’ Directors’ Directors’

Meeting Meeting Meeting Meeting Meeting Meeting

Executive Directors

A Farah P2 P P P P P

H Isaacman P2 P P P P P

C Mostert P2 A A1 A1 A1 A1

J Palmer P2 P A P P P

Non-Executive Directors

J Myers (Chairman) P P P P P P

W Kansteiner A P P2 P P2 A

M Mogase A P P P A P

C Rezek (Alt) P P P A P P

L Ogilvy P2 P P P P P2

P Vallet P2 P P P P P

1 C Mostert resigned from the Board on 1 March 20052 Attended by teleconference

A = Absent

P = Present

R = Recused

Corporate Governance

serves to ensure that the presence

of a self-perpetuating board is

avoided. The Committee is made

up of executive and non-executive

directors to ensure a balance of

technical and financial expertise.

Members of the Nomination

Committee:

• Mr A Farah

• Ms J Palmer

• Dr J Myers

• Mr M Mogase

During the past financial year, the

Nomination Committee has met

once to review the composition of

the Board.

Members 28/09/2005

J Myers (Chairperson) P

M Mogase P

J Palmer P

A Farah P

P = Present

REMUNERATION COMMITTEE

Remuneration

Philosophy/Policies

Remuneration polices are devised

in accordance with trends and the

prevailing business climate. They

are designed to attract and retain

highly skilled and experienced

individuals from the ICT industry

for appointment to all levels within

the Group.

The main function of the

Remuneration Committee is to

formulate policies that concur with

the Group’s strategic aims. The

Committee devises appropriate

salaries and benefits for senior

management and executives, in

accordance with industry standards

and shareholder interests.

The Committee is chaired by

independent non-executive director,

Ms L Ogilvy and is wholly made up

of non-executive directors.

Remuneration Committee

Meetings

1 October 2004 – 30 September

2005

The Remuneration Committee

convened on two occasions during

the period under review and

attendance was as follows:

12/11 12/08

Members 2004 2005

L Ogilvy

(Chairperson) P P

P Vallet P P

P = Present

Spescom Group CEO, Mr A Farah

and the Group Human Resources

Manager, Mrs C Lamprecht attend

committee meetings by invitation

only. Mr Farah does not partake in

resolutions regarding his

remuneration package.

The Committee safeguards the

interests of stakeholders by

collaborating with the Spescom

Share Trust to match the share

incentive scheme with the JSE

Listings Requirements, the King

Report and current developments.

At the Annual General Meeting on

April 1, 2005, shareholders approved

an amendment to the share incentive

scheme whereby share options are

considered part of the remuneration

package for directors and

employees. The allocation of share

options to staff is discussed and

approved by the Board and Trustees

of the share incentive scheme. The

Trustees are independent individuals

who are not directors or beneficiaries

of the scheme.

The Committee has defined and

agreed its terms of reference,

which are regularly re-evaluated

and adjusted when necessary, and

then referred to the Board for

approval. Directors’ emoluments

are referred to in detail on page 67.

The Chairperson of the Remuneration

Committee attends the Annual

General Meeting and responds to

queries from shareholders.

AUDIT COMMITTEE

During the period under review,

Spescom’s Audit Committee was

Spe

scom

ann

ual r

epor

t 20

05

16

Corporate Governance

made up of the following

members:

• Mr P Vallet – Chairperson and

non-executive director

• Mr I Friedland – independent

chartered accountant

• Mr M Mogase – non-executive

director

• Dr J Myers – independent non-

executive director

Mr Friedland, in his capacity as an

independent chartered accountant,

brings valuable knowledge to the

Committee.

The Audit Committee fulfils the

JSE Listings Requirements and

recommendations of the King Report.

The Committee has formal terms

of reference which are frequently

reassessed and approved by the

Board of Directors. This ensures

compliance with changes in

accounting standards, as well as

proposed changes in the

accounting sector.

The Audit Committee thoroughly

observes the use of the external

auditors for non-audit services.

The external auditors, Ernst &

Young, have unrestricted access to

the Audit Committee and attend

meetings by invitation. Spescom is

currently finalising co-sourcing of

the internal audit function.

Ms J Palmer, Chief Financial Officer

of the Group, also attends

meetings by invitation.

In accordance with Section 242 of

the Companies Act of 1973 (as

amended), the minutes of the

meeting are transcribed by the

Company Secretary, Ms N Magadze,

who is present by invitation.

The Chairperson of the Committee

attends the Annual General Meeting to

respond to queries from shareholders.

The Committee convened on three

occasions during the financial year

ending 30 September 2005.

The internal audit function

formed one of the points of

discussion, as well as

examination and approval of year

end and interim results,

contingent liabilities, risk

management and the impact of

the new International Financial

Reporting Standards (IFRS).

Audit Committee Meetings

1 October 2004 – 30 September

2005

Attendance of members at

meetings for the period under

review was as follows:

09/11 09/05 27/07

Members 2004 2005 2005

P Vallet

(Chairperson) P P P

I Friedland P A P

J Myers P P P

M Mogase P P P

P = Present

A = Absent

RISK MANAGEMENT

The Board of Directors is tasked

with the evaluation and

management of all aspects of risk,

whether financial or otherwise. The

Audit Committee, on behalf of the

Board, is tasked with the continual

assessment of all issues relating to

risk evaluation and management.

Moreover, the Board has assigned

senior executives with the

responsibility of formulating detailed

risk detection and management

plans, as well as scrutiny of internal

financial and operating controls and

the authentication and preservation

of assets.

FINANCIAL REPORTING

CONTROLS

The Board of Directors is

responsible for scrutinising the

accounting practices applied in the

preparation of the financial

statements, as well as the integrity

of the information contained in this

Annual Report.

Spe

scom

ann

ual r

epor

t 20

05

17

Corporate Governance

The independent auditors endorse

the accuracy of the financial

statements and certify that they

properly reflect the financial

position, results of operations,

cash flow and changes in

Spescom equity.

Financial statements have been

drawn up in concurrence with

South African Statements of

Generally Accepted Accounting

Practices and include feasible and

sensible accounting

approximations and judgements,

except where otherwise stated.

THE ROLE OF THE COMPANY

SECRETARY

Ms N Magadze, the Spescom

Group Company Secretary, was

appointed by the Board on

11 March 2005. Ms Magadze is a

qualified and admitted attorney.

The Company Secretary is tasked

with offering counsel and assistance

to the Board, individually or

collectively, on all matters relating to

their responsibilities and powers.

The Company Secretary is also

responsible for providing training to

new directors regarding the Group’s

core business activities, ethics and

corporate governance policies.

Furthermore, the Company

Secretary assists in the recognition

and management of risk, provides

the foundation for ongoing legislative

compliance and is required to report

failures in this regard to stakeholders

and the Board.

Ms Magadze fulfils the functions

set out in Section 268G of the

Companies Act of 1973 (as

amended) and records the minutes

of shareholder meetings, directors’

meetings and Audit Committee

meetings in accordance with

Section 242 of the Companies Act

of 1973 (as amended).

INFORMING STAKEHOLDERS

Corporate communications

procedures and disclosure policies

are in place to ensure transparent

communication with the media,

institutional investors, stakeholders

and staff.

Continuous updates are conveyed to

institutional, domestic and

international shareholders, fund and

asset managers and financial analysts

through investor road shows,

presentations and one on one liaison.

Annual General Meetings

provide shareholders with a

platform for participation in

significant and proactive

discussion and debate with the

Board. Accordingly, shareholders

are encouraged to attend.

The Spescom Group operates

closed periods as set out in the

JSE Listings Requirements. These

closed periods are communicated

to directors, officers, members of

the Spescom Limited Share Trust

and employees, via email, intranet

and corporate policy documents

available in hard copy. During

closed periods, directors, officers,

participants in the share incentive

scheme and staff may not trade in

Spescom securities. Further closed

periods are imposed, when

necessary, in terms of corporate

activities.

A written policy is also in place that

regulates securities dealings by

Spescom’s directors and other

officers. The policy is in line with

the JSE Listings Requirements and

forms part of the Group’s ISO9001

quality system.

DEMATERIALISATION OF

SHARES

Shareholders must convert all share

certificates into an electronic record

before they may be traded and

settled on the JSE. This is achieved

via STRATE, the electronic

settlement system for securities on

the JSE (dematerialisation).

Shareholders who do not have a

Central Securities Depository

Participant (CSDP) or broker may

Spe

scom

ann

ual r

epor

t 20

05

18

Corporate Governance

contact STRATE Share Care Line

on 0800 202 363 or contact

Computershare Investor Services

2004 (Pty) Limited on

011 370 5000 for assistance.

SPESCOM’S TRIPLE BOTTOM

LINE APPROACH

PEOPLE PLANET PROFIT

The Spescom Group adheres to a

triple bottom line philosophy that

continuously assesses the effects

of its activities on people, the

environment and financial gain.

The three Ps are systems within

themselves and cannot be

evaluated or changed in isolation.

Spescom’s Greatest Asset

– Its People

The Group is committed to

providing a fair and balanced

working environment for all levels

of staff.

Spescom is an equal

opportunities employer and is

steadfast in its recruitment,

training, and development of

employees regardless of race,

creed, or sex.

The Employment Equity

Committee, in co-operation with

the Board, surveys affirmative

action legislative requirements and

trends in this arena.

Employment Equity

Spescom is committed to its

Employment Equity programmes

aimed at satisfying requirements of

the Employment Equity Act and

the Broad Based Black Economic

Empowerment Act. This is evident

in the implementation of

comprehensive employment

initiatives that are continually

evaluated to ensure compliance

with legislative criteria and

relevance to employees.

These policies outline the

Group’s aims in the equity arena

and detail strategies to support

and motivate the development

and career advancement of all

staff members, particularly those

from historically disadvantaged

groups.

Employment equity and

transformation policies are

reviewed and executed by

Spescom’s Employment Equity

and Black Economic Forum in

conjunction with a dedicated

manager in this arena.

Skills Development

Spescom’s employment policies

tackle issues such as skills

shortages and past inequalities.

They include a separate budget

over and above operating costs for

skills development.

The policies exist to ensure staff

members are educated,

encouraged and developed with a

view to personal empowerment,

realising career potential and

capitalising on opportunities.

Training needs are evaluated

annually as part of an internal skills

development programme.

Spescom complies fully with the

Skills Development Act (as

amended) and the Skills

Development Levies Act.

Health Policies

The Spescom Group meets the

terms of South Africa’s

Occupational Health and Safety

Act of 1993, as amended.

The Group is committed to the

support and maintenance of good

health for all staff members.

An HIV/AIDS management policy

exists to ensure that the rights and

dignity of employees are safeguarded.

The policy encompasses Spescom’s

responsibilities in this arena and

details interaction guidelines for staff

diagnosed with life threatening

diseases.

Black Economic Empowerment

The road to true transformation lies

in empowerment and enablement.

Spe

scom

ann

ual r

epor

t 20

05

19

Corporate Governance

Spescom’s BEE philosophy is built

on four main pillars that support

these themes, namely:

shareholding, employment equity,

procurement and social

responsibility.

Shareholding with

Representation

Spescom’s commitment to BEE

endeavours in the ICT industry is

evidenced by the fact that

historically disadvantaged

individuals own 31,42% of the

Group.

Employment Equity

Policies exist to guide the

selection, development and

retention of all staff.

Procurement

Constantly evolving policies exist

that aid Spescom in achieving its

aims in the areas of affirmative

procurement and retention of high

quality black professionals. These

policies also focus on the use of

BEE subcontractors.

Social Responsibility

Spescom is dedicated to

community development and

upliftment. The Leseding

Electronics Investment Trust is an

equity sharing programme that

sees historically disadvantaged

employees owning 90% of the

trust with Spescom holding the

remaining 10%.

Spescom’s commitment to BEE is

further evidenced by the fact that

the company has commissioned a

BEE audit in order to highlight

areas where improvements can be

implemented.

STRATE Charity Shares Initiative

This initiative seeks to allocate the

proceeds from donated cash and

shares to various charitable

organisations.

Shareholders wishing to contribute

to the scheme can contact

STRATE Charity Shares Toll Free

on 0800 202 363 (+27 11 870 8207

if outside SA) or on

SOCIAL AND ENVIRONMENTAL

RESPONSIBILITY

Spescom’s commitment to the

community and the larger

environment is clear in its definitive

and sustained education initiatives.

Through education Spescom

endeavours to uplift and develop

the community with a view to

utilising technology as the enabler.

The Group is engaged in various

science, technology and

management programmes that

focus on enhancing the national

skills base and addressing the IT

skills shortage.

These initiatives include a

programme at the University of the

Witwatersrand Graduate School of

Business and scholarship

sponsorship for second year

Computer Science students from

previously disadvantaged

communities.

Spe

scom

ann

ual r

epor

t 20

05

20

Spe

scom

ann

ual r

epor

t 20

05

21

Annual Financial Statements

Report of the Independent Auditors 22

Directors’ Report 23 – 27

Income Statements 28

Balance Sheets 29

Statements of Changes in Equity 30

Cash Flow Statements 31

Notes to the Cash Flow Statements 32

Notes to the Financial Statements 33 – 62

Subsidiary Companies 63

Joint Ventures 64

Segmental Reports 65 – 66

Directors’ Remuneration 67

Directors’ Share Options 68 – 69

Jené Palmer

Chief Financial Officer

Spe

scom

ann

ual r

epor

t 20

05

22

Report of the Independent Auditors

TO THE MEMBERS OF SPESCOM LIMITED

We have audited the annual financial statements and Group annual financial statements of Spescom Limited set out

on pages 23 to 69 for the year ended 30 September 2005. These financial statements are the responsibility of the

company’s directors. Our responsibility is to express an opinion on these financial statements based on our audit.

SCOPE

We conducted our audit in accordance with statements of South African Auditing Standards. Those standards

require that we plan and perform the audit to obtain reasonable assurance that the financial statements are free of

material misstatement. An audit includes:

• examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements

• assessing the accounting principles used and significant estimates made by management

• evaluating the overall financial statement presentation

We believe that our audit provides a reasonable basis for our opinion.

AUDIT OPINION

In our opinion, the financial statements fairly present, in all material respects, the financial position of the company

and the Group at 30 September 2005 and the results of their operations, cash flows and changes in equity for the

year then ended in accordance with South African Statements of Generally Accepted Accounting Practice, and in

the manner required by the Companies Act in South Africa.

ERNST & YOUNG

Chartered Accountants (S.A.)

Johannesburg

27 January 2006

Spe

scom

ann

ual r

epor

t 20

05

23

Directors’ Reportfor the year ended 30 September 2005

Your directors have pleasure in submitting their report together with the annual financial statements of SpescomLimited (“Spescom” or “the company”) and of the Spescom Group for the year ended 30 September 2005.

NATURE OF BUSINESS

Spescom, a Proudly South African group of companies, is a multi-national technology innovator with directoperations in the United States, United Kingdom and South Africa. The Group is publicly listed on the JSE Limited(Spescom Limited) and Spescom Software Inc., an associate company is listed on the NASDAQ OTCBB:SPCO.OB.

Spescom is an information and communications technology group focused on various aspects of enterprise contentmanagement. The Group provides products and solutions to connect to the networked economy, as well asenterprise software to manage information and knowledge. Spescom successfully competes in a crowded globalICT (Information and Communication Technology) marketplace due to its innovative and entrepreneurial businessapproach, coupled with its leading proprietary technology and products.

Spescom markets its products worldwide through appointed partners and distributors under the eB brand for itsenterprise software, and the DataVoice brand for its multimedia transaction recording solutions. The Group’s globalcustomer base consists of multi-national organisations including leading enterprises in utilities, telecommunications,transportation, financial, banking and insurance.

OVERVIEW OF RESULTSSpescom reflects a headline earnings profit of R26,2 million which translates into 36,1 cents per share for the yearas compared to 63,5 cents per share for the comparative year.

After taking into account the non-trading items and the write off of all offshore loans owing to the Group, Spescomreports a loss for the year of R3,4 million as compared to a profit of R29,4 million for the previous year.

It is rewarding to note, however, that the operating results for the second six months of the year reflect a vastimprovement on those of the first half.

During the year under review, the Group restructured its shareholding in its US operation, Spescom Software Inc.,facilitating external financing and permitting the redeployment of critical resources. This opens up a possibility ofnew structures to bring in the necessary strategic ownership by leaders in the market. This restructuring hasresulted in this investment now being accounted for as an associate company and being equity accounted witheffect 1 April 2005. The effect of this change in holding from a subsidiary to an associate company resulted in achange in holding of profit of R52,6 million.

Spescom’s reduced turnover can be mainly attributed to:

– equity accounting instead of consolidating the US operation– completion of major international telecommunications contracts with British Telecoms (BT) and delays in the

awarding of replacement business– discontinuation of non-core test and measurement activities– continued delays in the full deregulation of the telecommunications sector in South Africa

The gearing levels of the Group remain satisfactory and largely unchanged. Subsequent to year end, the Group hasmade further debt repayments.

Spescom is entering a new cycle in its history. The Group intends to take a forceful lead in core business areas ofthe ICT sector. This includes considering all the opportunities for growth, such as exploring acquisitions, in order toaccomplish its strategic objectives.

Spe

scom

ann

ual r

epor

t 20

05

24

Directors’ Reportfor the year ended 30 September 2005

Spescom will continue to focus on content management and is actively strengthening the application side of itstechnology offerings. The main emphasis will be on telecommunications and voice.

Internationally, Spescom remains focused on the globalisation of its own products and technology. In support ofthese objectives Spescom increased its global footprint by breaking into Middle Eastern markets.

The telecommunications industry continues to be characterised by delays and uncertainties. However, it isanticipated that the landscape will change significantly over the next year revealing above average growth, for whichthe Group is well positioned. The ongoing momentum of this transformation is expected to be realised in the 2007financial year.

The contact centre business continues to grow with the world trend towards offshoring, holding great potential asIndia’s grip on this market lessens, providing opportunities for South Africa.

The reality of convergence and synergy of contact centre and voice technologies is unassailable. Spescom is wellplaced to take advantage of these trends.

FINANCIAL RESULTS

The financial results of the company and the Group are fully disclosed on pages 28 to 69.

DIVIDENDS

Due to Spescom’s position in the dynamic ICT arena, and taking into consideration trends for similar companies inthis rapidly changing sector, the directors have resolved not to declare a dividend for the financial year under review.This will provide additional funds to position Spescom to take advantage of local acquisition opportunities, marketchanges as well as to finance globalisation plans.

SUBSIDIARIES

During the year under review, the Group’s US operation successfully raised US$2,2 million in cash by way of aprivate placement of convertible preference shares. The issuance of these shares diluted the Group’s interest inSpescom Software Inc. from 51% to 42,6% and consequently required that the Group’s investment in SpescomSoftware Inc. no longer be accounted for as a subsidiary. As the Group still has significant influence over thisoperation, Spescom Software Inc. with effect 1 April 2005 is being treated as an associate company and has beenequity accounted from that date.

Details of the company’s interest in its subsidiaries, including the aggregate profits and losses of these subsidiaries,are set out on page 63.

DIRECTORS AND SECRETARY

Mrs N Magadze succeeded Mr AG Johnston as company secretary on 11 March 2005. Mr AG Johnston resignedfrom the company and as company secretary with effect 15 February 2005. Mrs N Magadze’s business and postaladdresses appear on page 76 of this annual report.

The directors of the company during the period under review and up to the date of this annual report are set out onpages 4 and 5 respectively.

The following changes were made to the composition of the board of directors.

Executive appointmentsT Makore 21 October 2005

ResignationsC Mostert 1 March 2005H Isaacman 21 October 2005

Spe

scom

ann

ual r

epor

t 20

05

25

Directors’ Reportfor the year ended 30 September 2005

In line with the recommendations of King II, the Spescom Board is currently constituted by more non-executive

directors than executive directors and the roles of Chairperson and Chief Executive Officer continue to be separated.

Details of the directors’ emoluments and benefits as well as their participation in the Group’s share option schemes

are detailed on pages 67 to 69.

SHARE CAPITAL

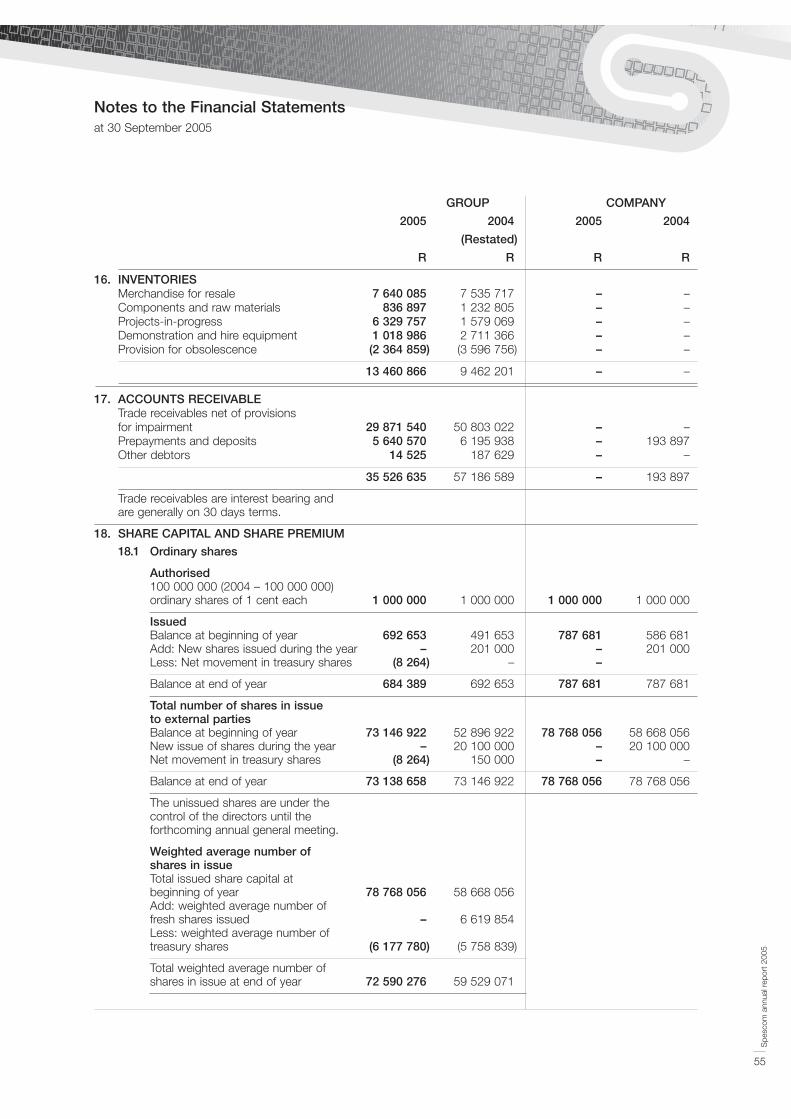

Details of the company’s authorised and issued share capital appear in note 18 to the financial statements.

• Directors’ interest in shares

The beneficial interest of directors, directly and indirectly, in the share capital of the company at 30 September

2005 was:

DIRECT INDIRECT

Director Beneficial Non-beneficial Beneficial Non-beneficial Total

Number Number Number Number Number

A Farah 3 678 944 – 608 893 24 891 4 312 728

H Isaacman 521 674 – – 439 000 960 674

J Myers – – – – –

L Ogilvy – – – – –

J Palmer – – – – –

P Vallet – – – – –

M Mogase – – – – –

C Rezek – – – – –

W Kansteiner – – – – –

Total 4 200 618 – 608 893 463 891 5 273 402

The beneficial interest of directors, directly and indirectly, in the share capital of the company at 30 September

2004 was:

DIRECT INDIRECT

Director Beneficial Non-beneficial Beneficial Non-beneficial Total

Number Number Number Number Number

A Farah 515 594 – 3 588 870 14 531 4 118 995

H Isaacman 521 674 – – 439 000 960 674

C Mostert (resigned 1 March 2005) 134 122 – – – 134 122

J Myers – – – – –

L Ogilvy – – – – –

J Palmer – – – – –

P Vallet – – – – –

M Mogase – – – – –

C Rezek – – – – –

W Kansteiner – – – – –

Total 1 171 390 – 3 588 870 453 531 5 213 791

Spe

scom

ann

ual r

epor

t 20

05

26

Directors’ Reportfor the year ended 30 September 2005

No material changes in their holdings have taken place between balance sheet date and the date of this annual

report.

• Major shareholders

According to the register of shareholders at 30 September 2005, the following are the only shareholders/nominee

holdings, other than directors of the company as disclosed above, who hold in excess of 3% of the shareholding

of the company at that date.

Shareholder Number of shares % of total shareholding

Vantage Capital Fund Managers (Proprietary) Limited 20 000 000 25,4%

The Spescom Limited Share Trust 6 447 516 8,2%

Allan Gray Fund Managers (Proprietary) Limited 4 368 800 5,5%

Farah Anthony Family Trust 2 979 977 3,8%

Credit Suisse Zurich 2 717 712 3,5%

Total 36 514 005 46,4%

No non-public shareholders, other than directors, hold 10% or more of the issued share capital of the company

for the financial year under review (2004 – nil).

• Share analysis

2005 2004

% %

Non-public 40,3 39,5

Public (consisting of 2 561 shareholders (2004 – 2 697)) 59,7 60,5

100,0 100,0

• Shareholder spread

Number of Number of

Shares shareholders % shares %

1 – 1 000 1 066 41,3 425 392 0,5

1 001 – 10 000 1 047 40,6 4 565 906 5,8

10 001 – 100 000 386 14,9 12 634 600 16,1

100 001 – 1 000 000 72 2,8 22 392 424 28,4

1 000 001 and over 9 0,4 38 749 734 49,2

2 580 100,0 78 768 056 100,0

The above information was supplied by the company’s registrars.

Spe

scom

ann

ual r

epor

t 20

05

27

Directors’ Reportfor the year ended 30 September 2005

RESOLUTIONS

No special resolutions, the nature of which might be significant to shareholders in their appreciation of the state ofaffairs of the Group, were passed by any subsidiary companies during the period covered by this annual report.

MATERIAL EVENTS SUBSEQUENT TO THE 2005 FINANCIAL YEAR END

During October 2005, the Group’s US-based associate company, Spescom Software Inc., successfully raised US$500 000 through a private placement of shares with Mercator Advisory Group LLC and Monarch Pointe Fund LLC.

Subsequent to year end, the Group made further debt repayments of US$350 000 in respect of its foreign loanfacility as well as a further R1,75 million repayment of its local loan facilities.

The directors are not aware of any other facts or circumstances that took place between financial year end being30 September 2005 and the date of this annual report which would be of importance in assessing the Group’sstate of affairs.

APPROVAL OF ANNUAL FINANCIAL STATEMENTS

The financial statements set out in this annual report have been prepared in accordance with Statements ofGenerally Accepted Accounting Practice in South Africa and are based on appropriate accounting policies, whichare supported by reasonable and prudent judgements and estimates. These have been consistently applied.

The directors are responsible for the preparation of the financial statements and related financial information thatfairly presents the state of affairs and results of the company and Group.

These financial statements have been prepared on the going concern basis. This basis presumes that the assetswill be realised and the liabilities settled in the normal course of business.

The directors have every reason to believe that the company and the Group will be able to continue in operation forthe foreseeable future. Accordingly, no adjustments have been made to the valuation or classification of assets orliabilities, which may have been necessary if the Group had been unable to continue as a going concern.

The annual financial statements set out on pages 28 to 69 were approved by the Board of Directors on 27 January 2006and are signed on its behalf by:

A FARAH J PALMERChief Executive Officer Chief Financial Officer

27 January 2006

COMPANY SECRETARY’S STATEMENTI certify that the company has lodged with the Registrar of Companies all such returns as are required of a publiccompany in terms of section 268G(d) of the Companies' Act and that all such returns are true, correct and up to date.

N MAGADZECompany Secretary

27 January 2006

Spe

scom

ann

ual r

epor

t 20

05

28

Income Statementsfor the year ended 30 September 2005

NOTES GROUP COMPANY

2005 2004 2005 2004

(Restated)

R R R R

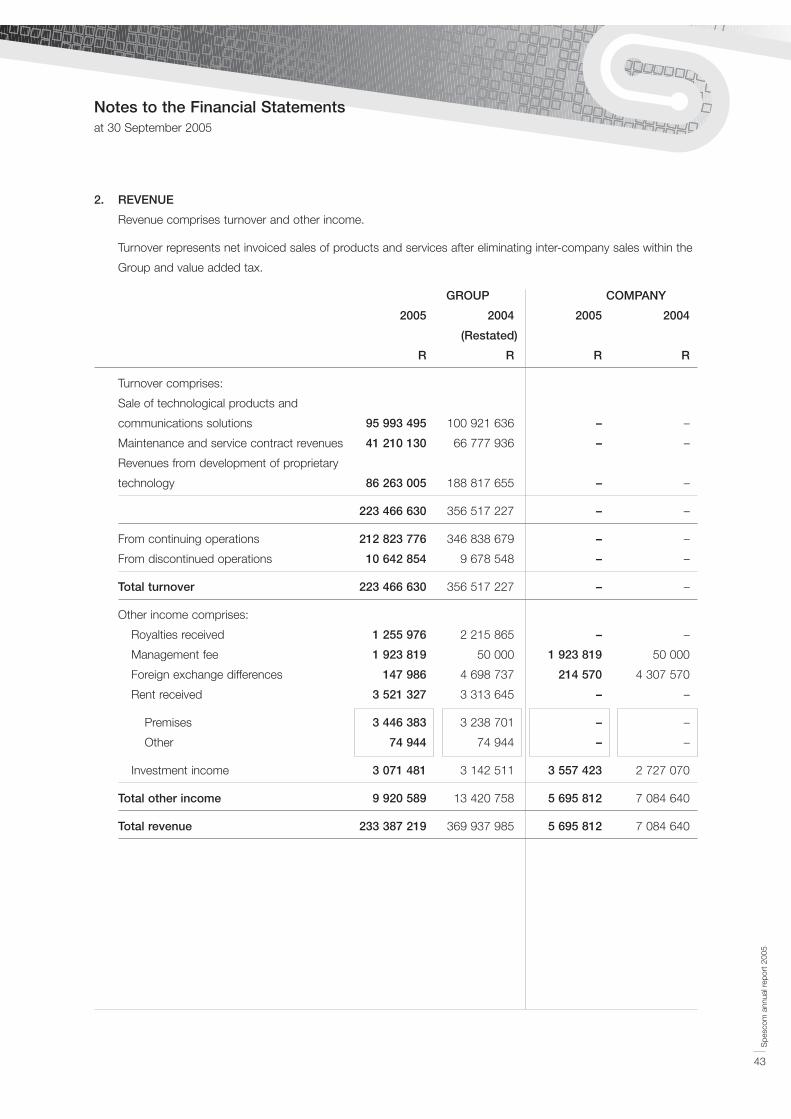

Revenue 2 223 466 630 356 517 227 – –

From continuing operations 212 823 776 316 268 227 – –

From discontinued operations 3 10 642 854 40 249 000 – –

Other income 2 9 920 589 13 420 758 5 695 812 7 084 640

Total revenue 233 387 219 369 937 985 5 695 812 7 084 640

Cost of sales 103 467 826 139 124 547 – –

From continuing operations 95 646 879 113 584 721 – –

From discontinued operations 3 7 820 947 25 539 826 – –

Gross profit 119 998 804 217 392 680 – –

From continuing operations 117 176 897 202 683 506 – –

From discontinued operations 3 2 821 907 14 709 174 – –

Expenses (143 942 186) (185 940 602) (3 903 612) (1 098 708)

Selling and general (138 018 131) (171 361 155) (3 903 612) (1 098 708)

Direct marketing (5 924 055) (14 579 447) – –

Operating (loss)/profit 4 (17 094 274) 41 730 325 (1 765 223) 3 258 862

From continuing operations (17 234 225) 40 918 999 (1 765 223) 3 258 862

From discontinued operations 3 139 951 811 326 – –

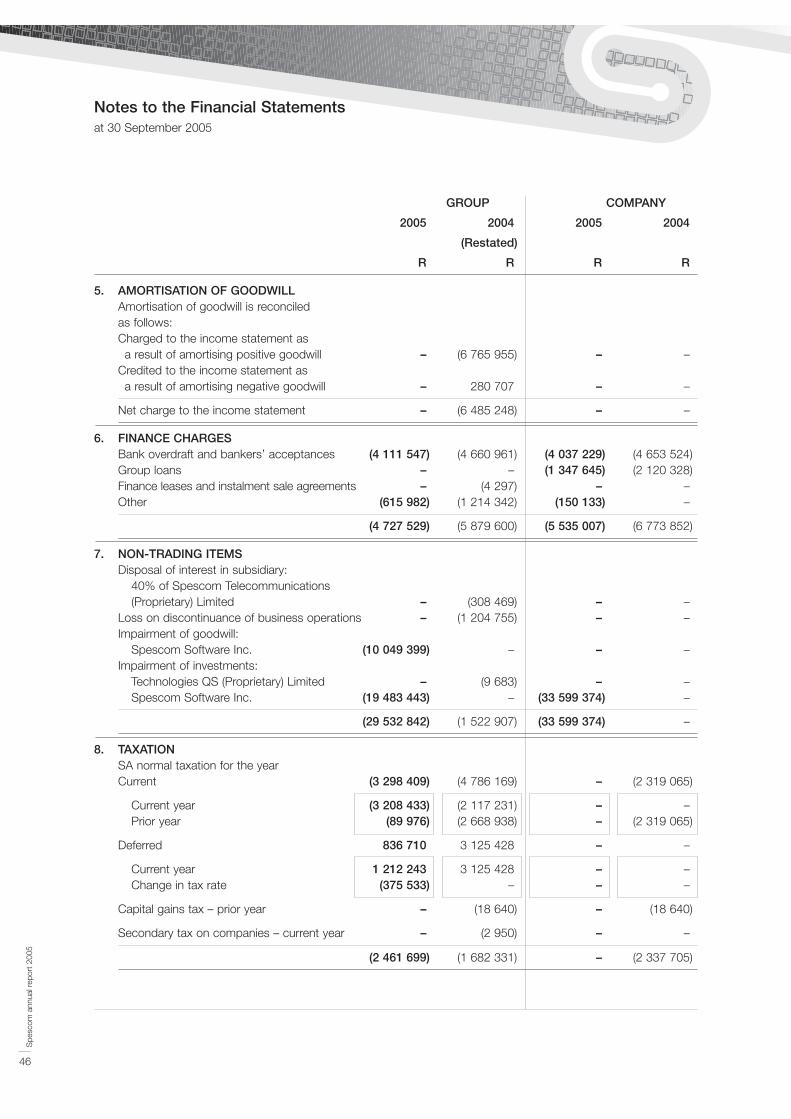

Amortisation of goodwill 5 – (6 485 248) – –

Finance charges 6 (4 727 529) (5 879 600) (5 535 007) (6 773 852)

Investment income 3 071 481 3 142 511 3 557 423 2 727 070

Net (loss)/profit before non-trading items (18 750 322) 32 507 988 (3 742 807) (787 920)

Non-trading items 7 (29 532 842) (1 522 907) (33 599 374) –

Net (loss)/profit before taxation (48 283 164) 30 985 081 (37 342 181) (787 920)

Taxation 8 (2 461 699) (1 682 331) – (2 337 705)

Net (loss)/profit after taxation (50 744 863) 29 302 750 (37 342 181) (3 125 625)

Loss from associate company (6 214 422) – – –

Attributable to minorities 53 513 124 100 264 – –

Net (loss)/profit for the year attributable to

holding company shareholders (3 446 161) 29 403 014 (37 342 181) (3 125 625)

Headline earnings per share (cents) 9 36,1 63,5

(Loss)/earnings per share (cents) 9 (4,8) 49,4

Diluted (loss)/earnings per share (cents) 9 (4,8) 49,4

Spe

scom

ann

ual r

epor

t 20

05

29

Balance Sheetsat 30 September 2005

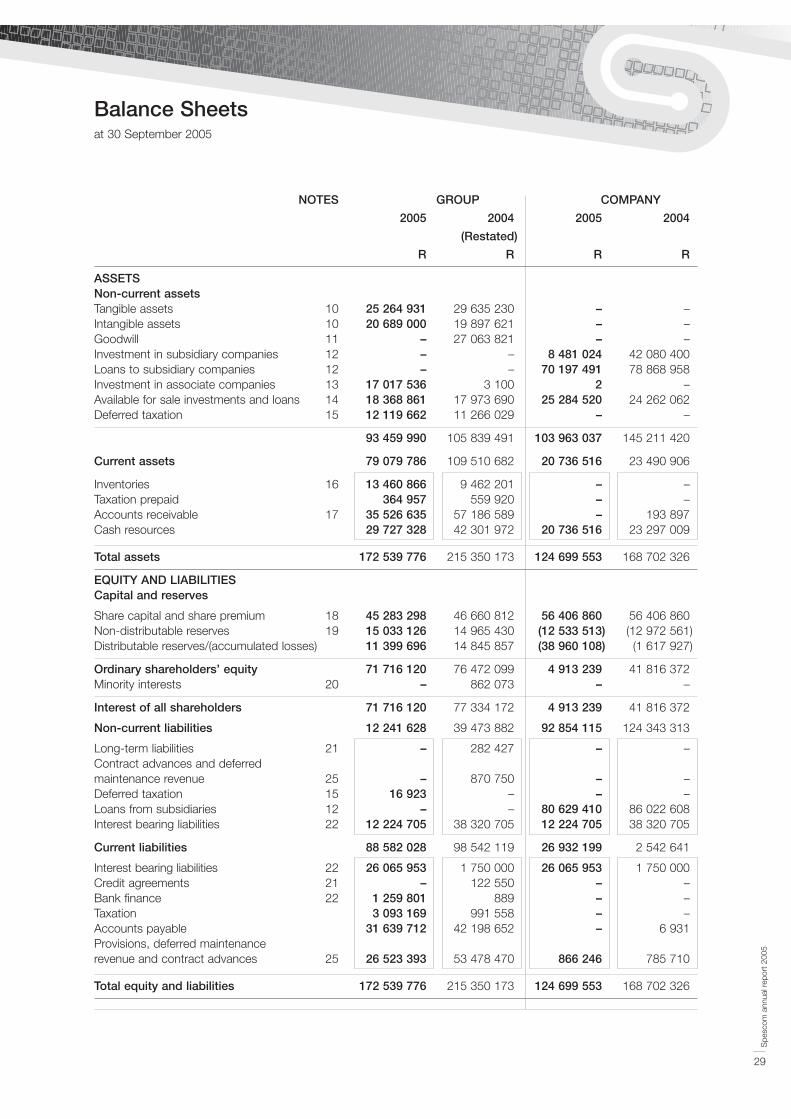

NOTES GROUP COMPANY

2005 2004 2005 2004

(Restated)

R R R R

ASSETSNon-current assetsTangible assets 10 25 264 931 29 635 230 – –Intangible assets 10 20 689 000 19 897 621 – –Goodwill 11 – 27 063 821 – –Investment in subsidiary companies 12 – – 8 481 024 42 080 400Loans to subsidiary companies 12 – – 70 197 491 78 868 958Investment in associate companies 13 17 017 536 3 100 2 –Available for sale investments and loans 14 18 368 861 17 973 690 25 284 520 24 262 062Deferred taxation 15 12 119 662 11 266 029 – –

93 459 990 105 839 491 103 963 037 145 211 420

Current assets 79 079 786 109 510 682 20 736 516 23 490 906

Inventories 16 13 460 866 9 462 201 – –Taxation prepaid 364 957 559 920 – –Accounts receivable 17 35 526 635 57 186 589 – 193 897Cash resources 29 727 328 42 301 972 20 736 516 23 297 009

Total assets 172 539 776 215 350 173 124 699 553 168 702 326

EQUITY AND LIABILITIESCapital and reserves

Share capital and share premium 18 45 283 298 46 660 812 56 406 860 56 406 860Non-distributable reserves 19 15 033 126 14 965 430 (12 533 513) (12 972 561)Distributable reserves/(accumulated losses) 11 399 696 14 845 857 (38 960 108) (1 617 927)

Ordinary shareholders’ equity 71 716 120 76 472 099 4 913 239 41 816 372Minority interests 20 – 862 073 – –

Interest of all shareholders 71 716 120 77 334 172 4 913 239 41 816 372

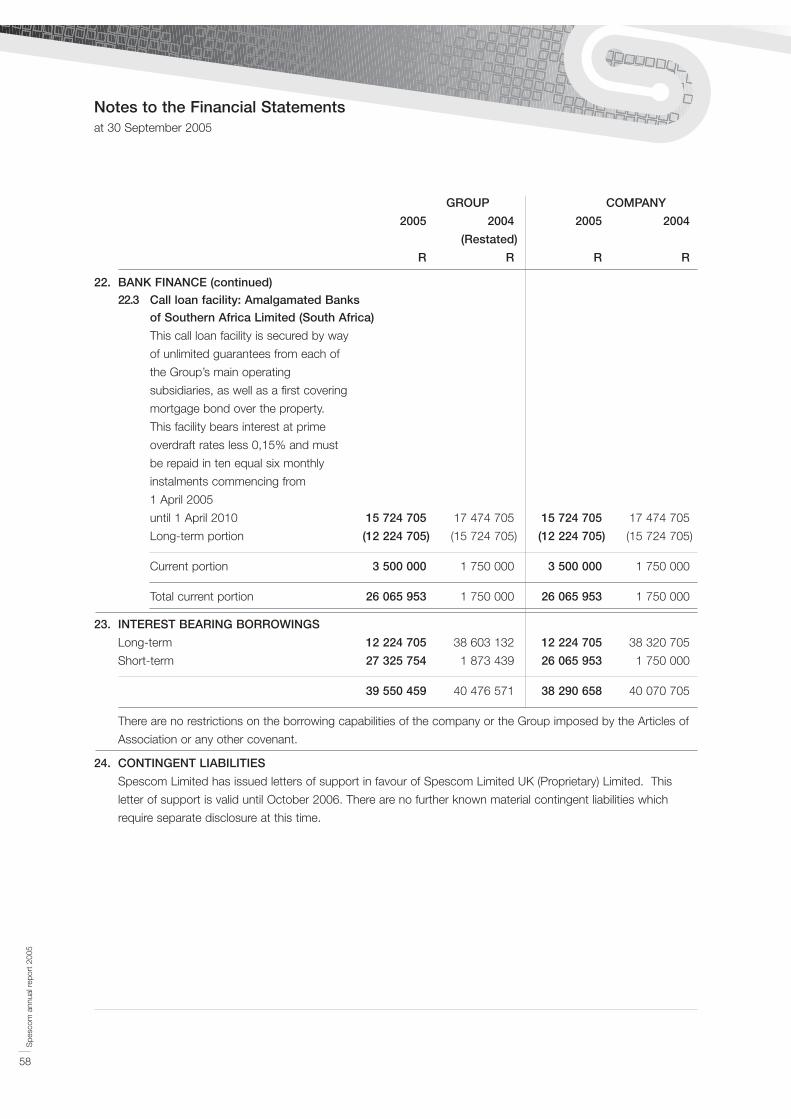

Non-current liabilities 12 241 628 39 473 882 92 854 115 124 343 313

Long-term liabilities 21 – 282 427 – –Contract advances and deferred maintenance revenue 25 – 870 750 – –Deferred taxation 15 16 923 – – –Loans from subsidiaries 12 – – 80 629 410 86 022 608Interest bearing liabilities 22 12 224 705 38 320 705 12 224 705 38 320 705

Current liabilities 88 582 028 98 542 119 26 932 199 2 542 641

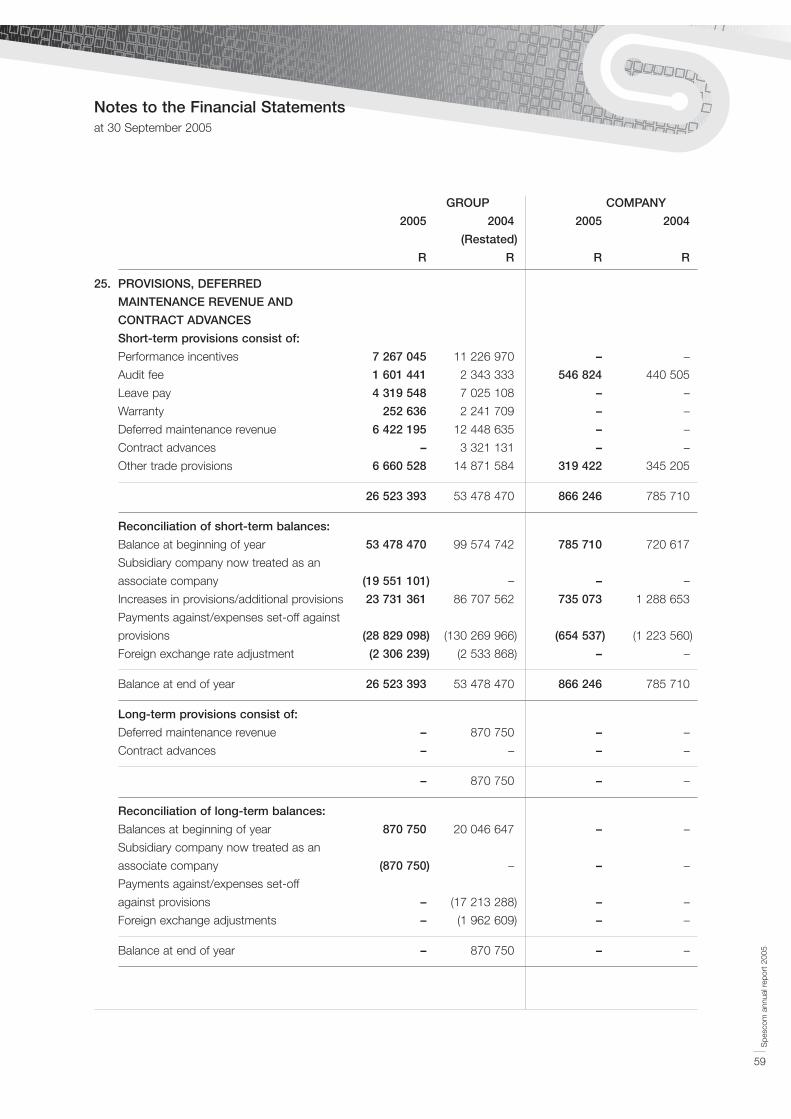

Interest bearing liabilities 22 26 065 953 1 750 000 26 065 953 1 750 000Credit agreements 21 – 122 550 – –Bank finance 22 1 259 801 889 – –Taxation 3 093 169 991 558 – –Accounts payable 31 639 712 42 198 652 – 6 931Provisions, deferred maintenance revenue and contract advances 25 26 523 393 53 478 470 866 246 785 710

Total equity and liabilities 172 539 776 215 350 173 124 699 553 168 702 326

Spe

scom

ann

ual r

epor

t 20

05

30

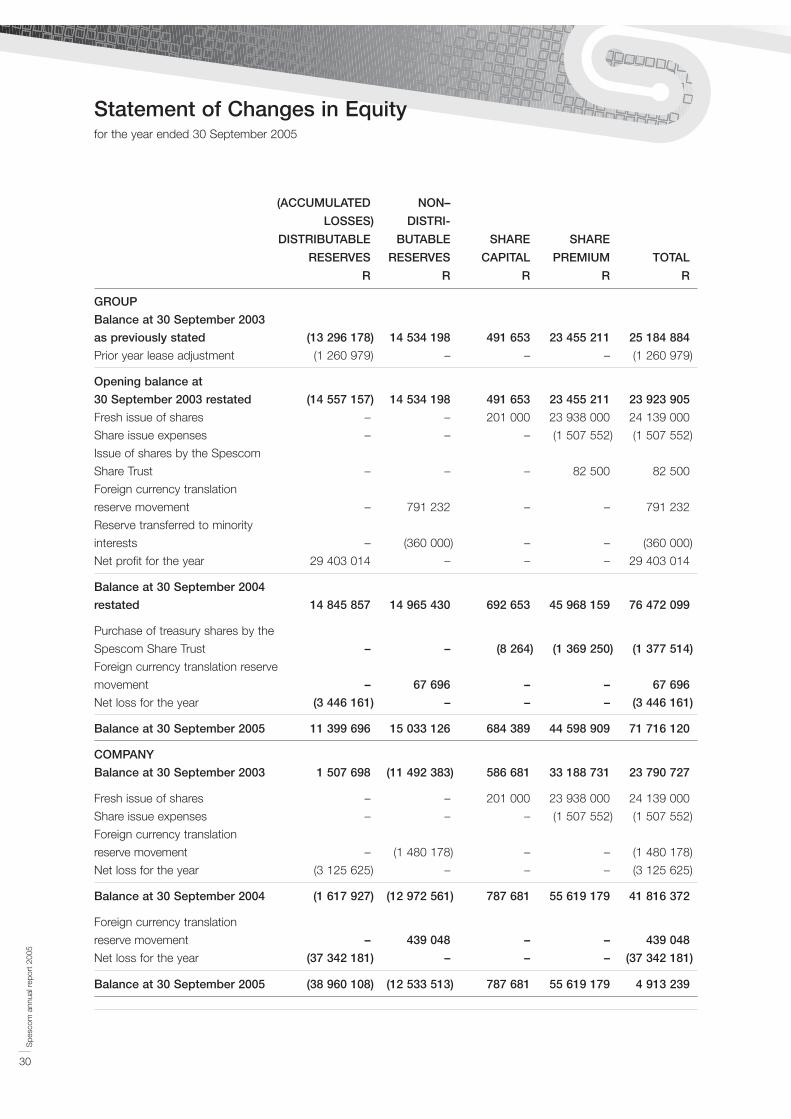

Statement of Changes in Equityfor the year ended 30 September 2005

(ACCUMULATED NON–

LOSSES) DISTRI-

DISTRIBUTABLE BUTABLE SHARE SHARE

RESERVES RESERVES CAPITAL PREMIUM TOTAL

R R R R R

GROUP

Balance at 30 September 2003

as previously stated (13 296 178) 14 534 198 491 653 23 455 211 25 184 884

Prior year lease adjustment (1 260 979) – – – (1 260 979)

Opening balance at

30 September 2003 restated (14 557 157) 14 534 198 491 653 23 455 211 23 923 905

Fresh issue of shares – – 201 000 23 938 000 24 139 000

Share issue expenses – – – (1 507 552) (1 507 552)

Issue of shares by the Spescom

Share Trust – – – 82 500 82 500

Foreign currency translation

reserve movement – 791 232 – – 791 232

Reserve transferred to minority

interests – (360 000) – – (360 000)

Net profit for the year 29 403 014 – – – 29 403 014

Balance at 30 September 2004

restated 14 845 857 14 965 430 692 653 45 968 159 76 472 099

Purchase of treasury shares by the

Spescom Share Trust – – (8 264) (1 369 250) (1 377 514)

Foreign currency translation reserve

movement – 67 696 – – 67 696

Net loss for the year (3 446 161) – – – (3 446 161)

Balance at 30 September 2005 11 399 696 15 033 126 684 389 44 598 909 71 716 120

COMPANY

Balance at 30 September 2003 1 507 698 (11 492 383) 586 681 33 188 731 23 790 727

Fresh issue of shares – – 201 000 23 938 000 24 139 000

Share issue expenses – – – (1 507 552) (1 507 552)

Foreign currency translation

reserve movement – (1 480 178) – – (1 480 178)

Net loss for the year (3 125 625) – – – (3 125 625)

Balance at 30 September 2004 (1 617 927) (12 972 561) 787 681 55 619 179 41 816 372

Foreign currency translation

reserve movement – 439 048 – – 439 048

Net loss for the year (37 342 181) – – – (37 342 181)

Balance at 30 September 2005 (38 960 108) (12 533 513) 787 681 55 619 179 4 913 239

Spe

scom

ann

ual r

epor

t 20

05

31

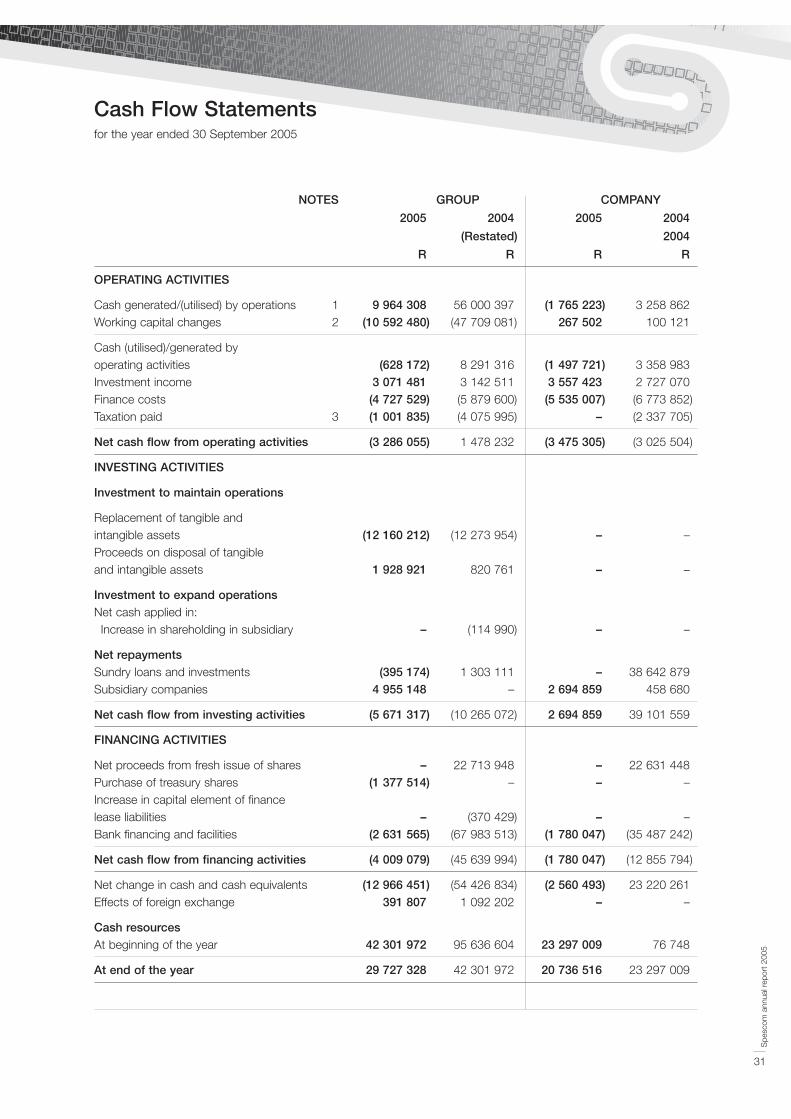

Cash Flow Statements for the year ended 30 September 2005

NOTES GROUP COMPANY

2005 2004 2005 2004

(Restated) 2004

R R R R

OPERATING ACTIVITIES

Cash generated/(utilised) by operations 1 9 964 308 56 000 397 (1 765 223) 3 258 862Working capital changes 2 (10 592 480) (47 709 081) 267 502 100 121

Cash (utilised)/generated by operating activities (628 172) 8 291 316 (1 497 721) 3 358 983Investment income 3 071 481 3 142 511 3 557 423 2 727 070Finance costs (4 727 529) (5 879 600) (5 535 007) (6 773 852)Taxation paid 3 (1 001 835) (4 075 995) – (2 337 705)

Net cash flow from operating activities (3 286 055) 1 478 232 (3 475 305) (3 025 504)

INVESTING ACTIVITIES

Investment to maintain operations

Replacement of tangible and intangible assets (12 160 212) (12 273 954) – –Proceeds on disposal of tangible and intangible assets 1 928 921 820 761 – –

Investment to expand operationsNet cash applied in:Increase in shareholding in subsidiary – (114 990) – –

Net repaymentsSundry loans and investments (395 174) 1 303 111 – 38 642 879Subsidiary companies 4 955 148 – 2 694 859 458 680

Net cash flow from investing activities (5 671 317) (10 265 072) 2 694 859 39 101 559

FINANCING ACTIVITIES

Net proceeds from fresh issue of shares – 22 713 948 – 22 631 448Purchase of treasury shares (1 377 514) – – –Increase in capital element of finance lease liabilities – (370 429) – –Bank financing and facilities (2 631 565) (67 983 513) (1 780 047) (35 487 242)

Net cash flow from financing activities (4 009 079) (45 639 994) (1 780 047) (12 855 794)

Net change in cash and cash equivalents (12 966 451) (54 426 834) (2 560 493) 23 220 261Effects of foreign exchange 391 807 1 092 202 – –

Cash resourcesAt beginning of the year 42 301 972 95 636 604 23 297 009 76 748

At end of the year 29 727 328 42 301 972 20 736 516 23 297 009

Spe

scom

ann

ual r

epor

t 20

05

32

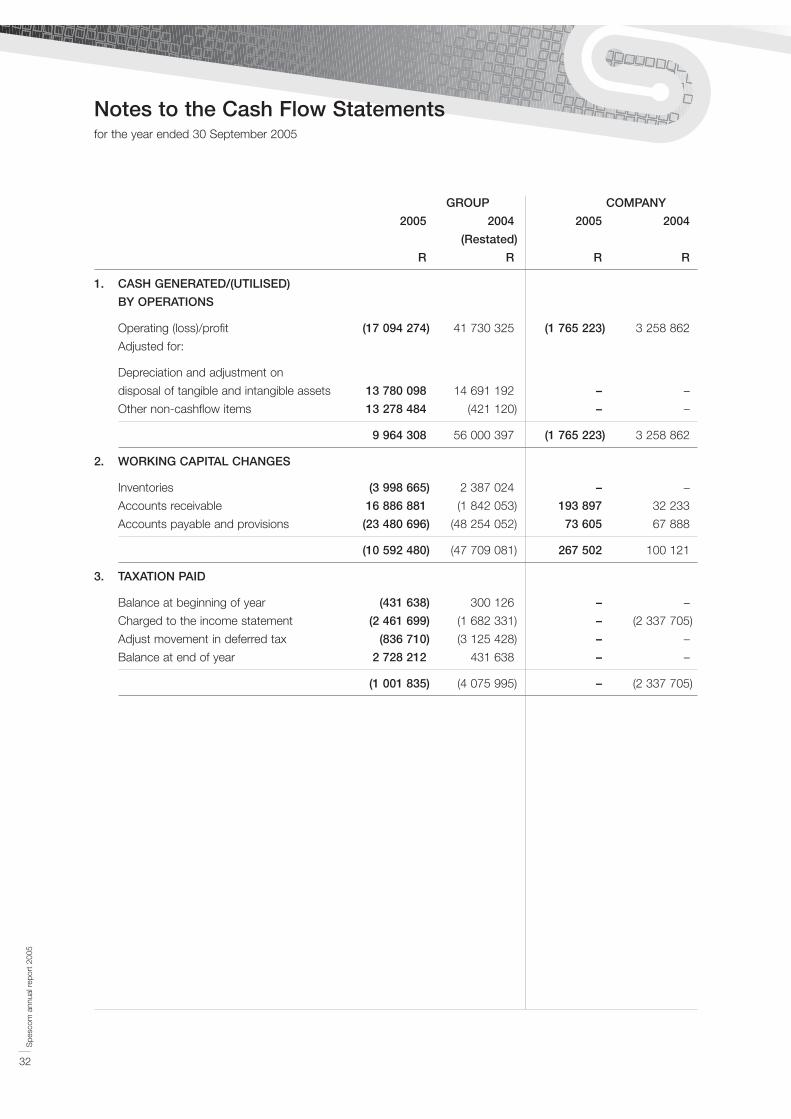

Notes to the Cash Flow Statementsfor the year ended 30 September 2005

GROUP COMPANY

2005 2004 2005 2004

(Restated)

R R R R

1. CASH GENERATED/(UTILISED)

BY OPERATIONS

Operating (loss)/profit (17 094 274) 41 730 325 (1 765 223) 3 258 862

Adjusted for:

Depreciation and adjustment on

disposal of tangible and intangible assets 13 780 098 14 691 192 – –

Other non-cashflow items 13 278 484 (421 120) – –

9 964 308 56 000 397 (1 765 223) 3 258 862

2. WORKING CAPITAL CHANGES

Inventories (3 998 665) 2 387 024 – –

Accounts receivable 16 886 881 (1 842 053) 193 897 32 233

Accounts payable and provisions (23 480 696) (48 254 052) 73 605 67 888

(10 592 480) (47 709 081) 267 502 100 121

3. TAXATION PAID

Balance at beginning of year (431 638) 300 126 – –

Charged to the income statement (2 461 699) (1 682 331) – (2 337 705)

Adjust movement in deferred tax (836 710) (3 125 428) – –

Balance at end of year 2 728 212 431 638 – –

(1 001 835) (4 075 995) – (2 337 705)

Spe

scom

ann

ual r

epor

t 20

05

33

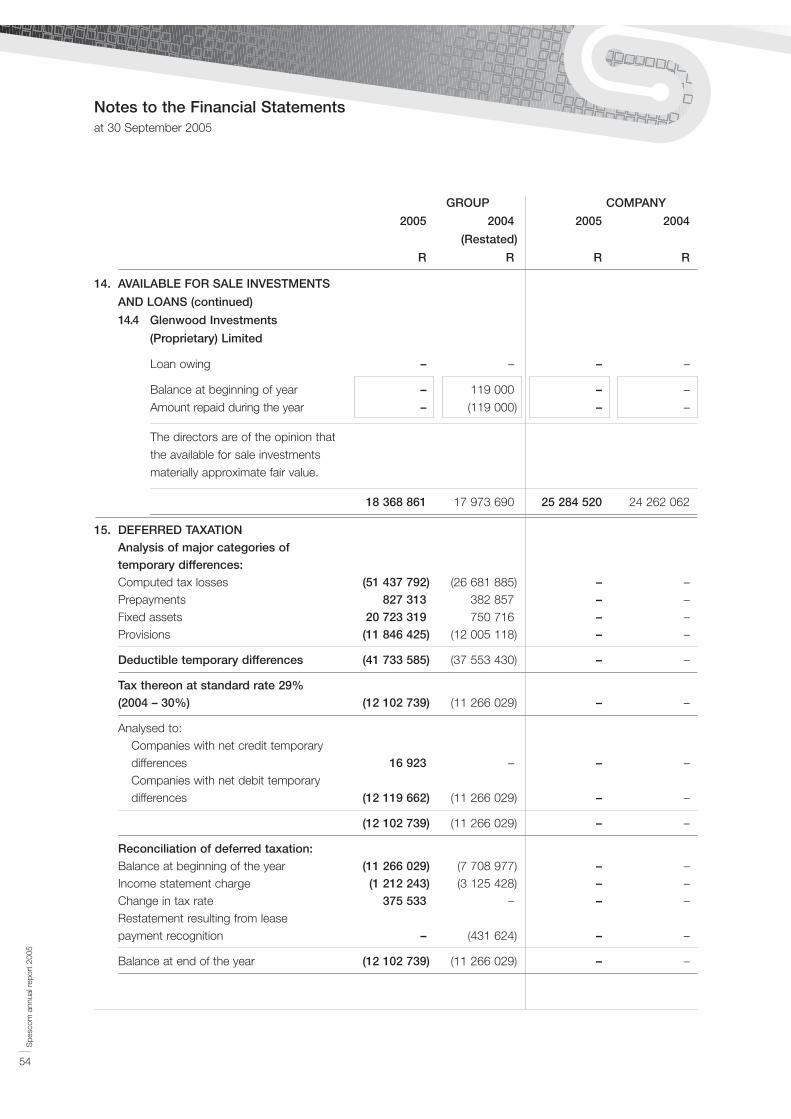

Notes to the Financial Statementsat 30 September 2005

1. ACCOUNTING POLICIES

The financial statements are prepared on the historical cost basis, except where indicated otherwise, and

incorporate the following principal accounting policies which conform with South African Statements of

Generally Accepted Accounting Practice.

The Group’s measurement currency is South African Rand.

Changes in accounting policy