This article was downloaded by: [Hesham Alyousef]On: 12 November 2012, At: 01:34Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Social SemioticsPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/csos20

An investigation of postgraduateBusiness students' multimodal literacyand numeracy practices in Finance: amultidimensional explorationHesham Suleiman Alyousef a ba Discipline of Linguistics, University of Adelaide, Adelaide,Australiab Department of English & Literature, King Saud University,Riyadh, Saudi ArabiaVersion of record first published: 12 Nov 2012.

To cite this article: Hesham Suleiman Alyousef (2012): An investigation of postgraduate Businessstudents' multimodal literacy and numeracy practices in Finance: a multidimensional exploration,Social Semiotics, DOI:10.1080/10350330.2012.740204

To link to this article: http://dx.doi.org/10.1080/10350330.2012.740204

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representationthat the contents will be complete or accurate or up to date. The accuracy of anyinstructions, formulae, and drug doses should be independently verified with primarysources. The publisher shall not be liable for any loss, actions, claims, proceedings,demand, or costs or damages whatsoever or howsoever caused arising directly orindirectly in connection with or arising out of the use of this material.

RESEARCH ARTICLE

An investigation of postgraduate Business students’ multimodal literacyand numeracy practices in Finance: a multidimensional exploration

Hesham Suleiman Alyousefa,b*

aDiscipline of Linguistics, University of Adelaide, Adelaide, Australia; bDepartment of English &Literature, King Saud University, Riyadh, Saudi Arabia

(Received 20 May 2010; final version received 17 July 2011)

Empirical research studies of finance have investigated students’ performance inPrinciples of Finance courses and the effect of class attendance on students’performance. Similarly, accounting research has been directed at readability ofaccounting narratives and lexical choices. However, no published study hasexplored and analysed the multimodal literacy and numeracy social practices ofinternational students in a core business module, and within a multidimensionalresearch framework. This study is of interest as most international ESL/EFLstudents in Australia and elsewhere are enrolled in business programmes. Thispaper explores the literacy and numeracy social practices of 10 first-year Masterof Commerce Accounting international students in a Principles of Financemodule. It is underpinned by the proposed multidimensional framework which isframed by Halliday’s systemic functional linguistic theory and by O’Halloran’smultisemiotic framework for the analysis of mathematical symbolism. Thefindings are presented in terms of (1) the epistemologies of Principles ofFinance, (2) a Systemic Functional Multimodal Discourse Analysis (SF-MDA)of the experiential meanings in students’ capital budgeting management reports,and (3) a description of the actual practices the participants engaged with tocomplete the assignment and their explanations of their texts. Implications ofthese findings and the research framework presented. The SF-MDA contributesto the description of experiential meaning in financial tables and graphs. Itindicates a potential research tool for the systemic functional analysis ofmultimodal finance and accounting discourses. The multidimensional explorationof participants’ literacy practices presented here could also provide a frameworkfor similar investigation across a broad range of educational settings.

Keywords: literacy practice; experiential meaning; systemic functional multi-modal; discourse analysis; multimodal; business discourse; finance literacies

1. Introduction

This ethnographic study explores and investigates the literacy and numeracy

practices of 10 first-year Master of Commerce accounting international students,

divided into three groups, who worked on a key topic in the Principles of Finance

module, capital budgeting management report: Abdulhadi, Saud, Jim and Cathy

(Group 1), Abdulrahman and Jiang (Group 2), and Ibrahim, Hasan, Sharon and

Tracey (Group 3). This study is part of a larger investigation into the numeracy and

literacy experiences of 19 Master of Commerce international students at a South

*Email: [email protected]

Social Semiotics

2012, 1�29, iFirst article

ISSN 1035-0330 print/1470-1219 online

# 2012 Taylor & Francis

http://dx.doi.org/10.1080/10350330.2012.740204

http://www.tandfonline.com

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

Australian university which is supported by a long-term ethnographic engagement

with academics and students both inside and outside the campuses.

The aim of this paper is to provide an account of the multimodal and

multisemiotic meanings that are construed in a key topic in Principles of Finance

Master of Commerce foundation module. This includes investigating the social

practices, events and texts. It aims to investigate (1) the social academic literacy and

numeracy practices postgraduate students are expected to engage in while perform-

ing the assigned Principles of Finance capital budgeting management report; (2) how

ESL/EAL postgraduate students studying in Australia represent the experiential,

conceptual financial knowledge; (3) how mathematical symbolism is represented and

interwoven into natural language in management reports; and (4) the social practices

Saudi EAL postgraduate students engaged in to complete the capital budgeting

management report.

Most of the academic literacy studies have focused only on specific aspects of the

writing tasks, rather than providing a systemic interpretive analysis of students’

discursive practices and experiences. As Garzone (2009, 156) points out that ‘‘so far,

contributions from linguists specifically dealing with multimodality in business

discourse have been relatively few, and most of them have been based on the analysis

of single cases or genres.’’

Lea and Street (2006) argue that multimodal analysis reveals the range of

meanings expressed in learners’ activities and genres. As they put it, multimodal

analysis aids in theorising ‘‘the multimodal nature of literacy, and thus of different

genres, that students needed to master in order to represent different types of

curriculum content for different purposes, and therefore to participate in different

activities’’ (Lea and Street 2006, 373). Tools for the systemic functional description

and analysis of capital budgeting management reports are not yet developed.

Empirical research studies of finance have investigated major and non-major

students’ performance in Principles of Finance courses (Sen et al. 1997) and the effect

of class attendance on students’ performance (Chan, Shum, and Wright 1997).

Similarly, accounting research has been directed at readability of narratives in

financial accounting textbooks over the past years, as measured by word and

sentence length (Davidson 2005) and lexical choices as measured by word choice and

frequency of use (Conaway and Wardrope 2010; Hyland 1998; Rutherford 2005).

Baskin (2000, 70) states, although there are divergent applications of literacy across

the business professions, ‘‘there remains a distinct lack of consensus over the

meaning of literacy in higher education communities.’’ In his final editorial for

English for Specific Purposes (1994), Swales appealed for more data-based

investigations into business English, which may be valuable for English for specific

purposes (ESP) teachers. Although management reports utilising capital budgeting

techniques are one of the most commonly used genre in Principles of Finance

module, there is a lack of multidimensional research framework that explores and

analyses international students’ multimodal literacy and numeracy social practices

that construe such reports. Kress (2000, 157) argues that ‘‘the single, exclusive and

intensive focus on written language has dampened the full development of all kinds

of human potentials.’’ This study is pertinent as most international ESL/EFL

students in Australia and elsewhere are enrolled in business and commerce

programmes (Alyousef and Picard 2011).

2 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

Numeracy practices are conceived as ‘‘literacy practices involving ‘numerate’

texts’’ (Barwell 2004, 21), a sub-set of literacy practice, since they are social processes

of making meaning with numerate text. This ethnographic research study is

underpinned by the proposed multidimensional framework for the investigation of

literacy practices. The Systemic Functional Multimodal Discourse Analysis

(SF-MDA) of participants’ capital budgeting management reports is framed by

systemic functional linguistics (Halliday 1985; Halliday and Martin 1993) and by

O’Halloran’s (1999, 2000) multisemiotic framework for the analysis of mathematical

symbolism. The SF-MDA aims to analyse the experiential meaning in the

multimodal texts, which encompass financial tables and graphs.

The multidimensional exploration of students’ literacy and numeracy social

practices is presented in terms of (1) the epistemologies of a Principles of Finance

module, (2) an SF-MDA of the experiential meaning in students’ capital budgeting

management reports and (3) a description of the participants’ actual practices they

engaged with to complete the assignment and their explanations of their texts. This is

followed by the discussion and the conclusion (Section 5), followed by the

implications (Section 6).

2. The epistemologies of the Principles of Finance module

This section describes the epistemologies of a Principles of Finance module which

encompass the social context of the study (2.1), materials (2.2), an overview of capital

budgeting techniques (2.3), the graduate attributes and learning outcomes (2.4), and

nature of the participants’management report assignment task sheets (2.5).

2.1. Social context

Context encompasses the research site and the participants. The setting of this study

was the University of Adelaide in South Australia. This study explores the literacy

and numeracy social practices of 10 first-year Master of Commerce Accounting

international students, who were given the pseudonyms: Abdulhadi, Saud, Jim and

Cathy (Group 1), Abdulrahman and Jiang (Group 2), and Ibrahim, Hasan, Sharon

and Tracey (Group 3). The participation of five of these students was non-focal as

they only consented to the analysis of their written assignments which was completed

with the other five focal Saudi participants: Abdulhadi, Saud, Abdulrahman,

Ibrahim and Hasan. To enrol in the Master of Commerce Accounting programme,

the students needed to achieve six or more in the International English Language

Testing System (IELTS) examinations, thus they have a ‘‘generally effective

command of the language, despite some inaccuracies, inappropriacies and mis-

understandings’’ (IELTS 2011). Since they completed their Accounting under-

graduate programme in Saudi Arabia they did not have opportunities to practise

their English outside the school or at the university. Unlike his peers, Hasan’s

undergraduate study programme in Saudi Arabia was not related to business, but to

computer science. All the five participants enrolled in an English course when they

arrived in Australia, and which ranged between 37 and 55 weeks.

Social Semiotics 3

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

2.2. Materials

The corpus is composed of three assignments written in English (7844 words) in the

field of business finance, capital budgeting management report genre: text 1 (2483

words), text 2 (1975 words) and text 3 (3386 words), excluding the cover sheet, table

of contents and the appendices. It also includes three task sheets, the study-guide (or

information booklet), Fundamentals of Financial Management textbook (Brigham

and Houston 2009), structured and unstructured interviews with Saud (Group 1),

Abdulrahman (Group 2) and Ibrahim (Group 3) and an unstructured interview with

one of the tutors, Janet (March 4, 2010). The interviews were transcribed in situ talk.

The aim of the interview was to explore students’ socio-cultural practices and

experiences and their perceptions of disciplinary conventions in the Principles of

Finance module. The structured interviews with the participants were guided by a

number of questions, whereas the unstructured were guided by prompts, such as the

use of capital budgeting, spreadsheets, financial calculators and the textbooks/sites.

The assignment is individual/group work on a key topic in the Principles of Finance

module, capital budgeting techniques. It is allotted 15% of the total mark for this

course. The three written assignments were performed by three groups of two to four

students. Though the three groups had different assignment task sheets, they were

comparable since the main topic underlying the tasks is similar, except for the

second part of the Group 1 task sheet (portfolio management) which was

excluded. Henceforth, each group will be referred to by the group numbers displayed

in Table 1.

Before describing the requirements of each task sheet, the learning outcomes and

the graduate attributes of capital budgeting management reports it is worthwhile to

overview the fundamental financial theoretical aspects underlying capital budgeting

techniques.

2.3. An overview of capital budgeting techniques

The term capital refers to ‘‘long-term assets used in production, while a budget is a

plan that outlines projected expenditures during some future period’’ (Brigham and

Houston 2009, 336). Thus, capital budgeting refers to a process in which a business

determines which project is worth pursuing. In capital budgeting, valuation

techniques are used to analyse the impact of real assets instead of financial assets.

As a result, future cash inflows and outflows are estimated to decide the economic

feasibility of a prospective investment. Management reports should thereforedetermine which project will yield the most return over an applicable period of time.

Mutually exclusive projects (Brigham and Houston 2009) mean that the

acceptance of a project entails rejecting the other one(s). The major capital budgeting

decision criteria are net present value (NPV), internal rate of return (IRR), multiple

Table 1. The distribution of the three groups in the finance module.

Participants Group number

Abdulhadi, Saud, Jim and Cathy 1

Abdulrahman and Jiang 2

Ibrahim, Hasan, Sharon and Tracey 3

4 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

internal rates of return (MIRR) and payback period (PP). PP (Brigham and Houston

2009) refers to the time it takes to recovering the costs of an investment. NPV and

IRR are the two most widely used measures of project worth. NPV is used to

determine how much value an investment adds to a company. It is equal to thePresent Value (PV) of an investment in ‘‘today’s dollars’’ of the future net cash flows

(CFs) discounted at the cost of capital. IRR is an estimate of the required rate of

return that forces PV of inflows to equal the cost, and the NPV to equal zero; any

project should be avoided if the cost of capital exceeds this rate. The analysis of

mutually exclusive projects with unequal lives could be adjusted either through the

equivalent annual annuity (EAA) model or the Replacement Chain (common life)

approach. When comparing investments with unequal lives, the one with the higher

EAA should be chosen. Next, a sensitivity analysis is applied to assess riskiness ofCFs. Sensitivity analysis focuses on analysing the effects of changes in key variables

on the project’s IRR or NPV.

Having introduced the mathematical demands and the financial concepts

underlying capital budgeting techniques, in the next section I describe the graduate

attributes and learning outcomes of the management report task.

2.4. The graduate attributes and the learning outcomes of the management report task

The purpose of the assignment is to apply into practice the theoretical framework for

project valuation. Students are required to write a management report in a group of

two to five students. As stated in the Group 2 task sheet, the specific objectives

underlying the group task were to:

� develop dynamic group skills;

� learn to communicate and cooperate with peers;

� develop problem-solving skills; and� improve interpersonal communication skills.

Indeed the Business School insists in its Communication Skills Guide (Hancock 2006)

on the overriding importance of communication for success during tertiary study and

beyond. Similarly, Jackson and Durkee (2007, 91�92) argue that ‘‘owing to the ever-

changing demands on the accounting professional, the professional community

considers it imperative that accounting educators incorporate into their curricula a

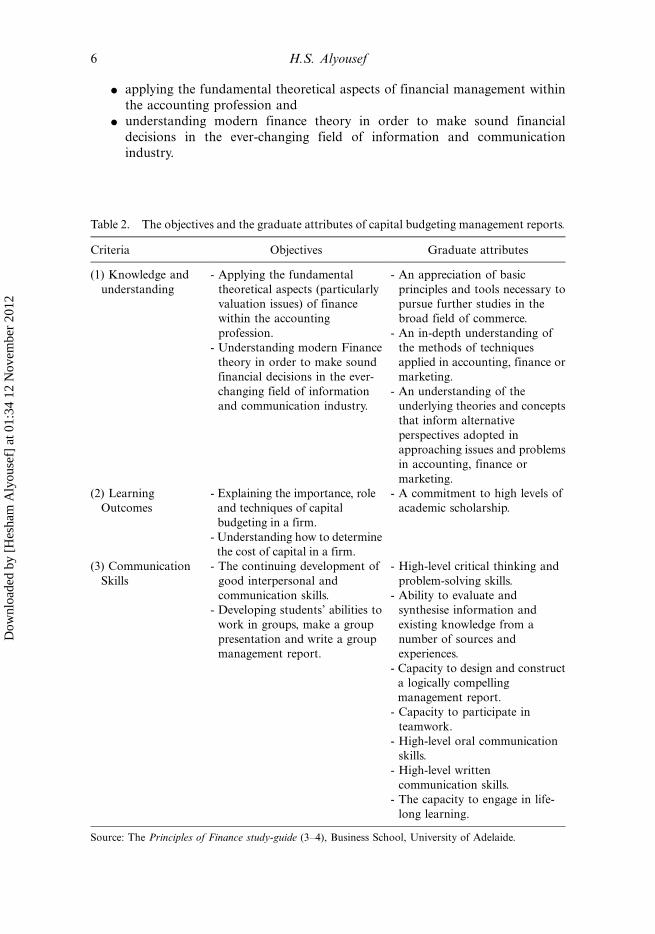

focus on life-long learning skills.’’ The module’s study-guide lists the objectives andthe graduate attributes (or qualities) of Principles of Finance in terms of (1)

knowledge and understanding; (2) learning outcomes; and (3) communication skills.

Judging from the task sheet, it seems that the tutor places high value on

communication and problem-solving skills since these will enable students to gain

disciplinary-specific knowledge in financial management, and in turn provide them

with relevant and meaningful life-long learning experiences that will most likely help

them succeed in their future work. The objectives of capital budgeting task/topic and

their corresponding graduate attributes are listed in Table 2.The graduate attributes of communication skills include exhibiting analytical and

critical thinking, working in teamwork and engaging in life-long learning. Based on

the course objectives outlined in Table 2, the purpose of this task is to display

knowledge and understanding by:

Social Semiotics 5

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

� applying the fundamental theoretical aspects of financial management within

the accounting profession and

� understanding modern finance theory in order to make sound financial

decisions in the ever-changing field of information and communicationindustry.

Table 2. The objectives and the graduate attributes of capital budgeting management reports.

Criteria Objectives Graduate attributes

(1) Knowledge and

understanding

- Applying the fundamental

theoretical aspects (particularly

valuation issues) of finance

within the accounting

profession.

- Understanding modern Finance

theory in order to make sound

financial decisions in the ever-

changing field of information

and communication industry.

- An appreciation of basic

principles and tools necessary to

pursue further studies in the

broad field of commerce.

- An in-depth understanding of

the methods of techniques

applied in accounting, finance or

marketing.

- An understanding of the

underlying theories and concepts

that inform alternative

perspectives adopted in

approaching issues and problems

in accounting, finance or

marketing.

(2) Learning

Outcomes

- Explaining the importance, role

and techniques of capital

budgeting in a firm.

- Understanding how to determine

the cost of capital in a firm.

- A commitment to high levels of

academic scholarship.

(3) Communication

Skills

- The continuing development of

good interpersonal and

communication skills.

- Developing students’ abilities to

work in groups, make a group

presentation and write a group

management report.

- High-level critical thinking and

problem-solving skills.

- Ability to evaluate and

synthesise information and

existing knowledge from a

number of sources and

experiences.

- Capacity to design and construct

a logically compelling

management report.

- Capacity to participate in

teamwork.

- High-level oral communication

skills.

- High-level written

communication skills.

- The capacity to engage in life-

long learning.

Source: The Principles of Finance study-guide (3�4), Business School, University of Adelaide.

6 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

Capital budgeting literacy could be defined in terms of the objectives of the three

tasks. In the next section, I therefore investigate the literacy and numeracy

requirements of the three task sheets.

2.5. Nature of the management report assignment task sheets

The assignment task sheets present the social purpose which in turn determines the

schematic structure of management reports. The social purpose of the three tasks is

to evaluate the best investment alternative through the application of capital

budgeting techniques, and to present the findings in the form of a management

report (Table 3).

The three groups were required to evaluate the best investment alternative. They

were also required not to exceed the 2000 word limit, excluding appendices. The

Group 1 task sheet requires students to take the position of the CEO of Voortco, a

leading maker of electric and acoustic guitars, and decide the best choice of the three

investments: continuing with business as normal, upgrading existing equipment, or

discontinue using current equipment and building a new production line. The Group

2 task sheet requires students to evaluate whether it is worthwhile to install tanning

equipment in a full-service salon and day spa and if they assess it is, they should

decide which of the two types of tanning equipment, Dome Unit and Tanning Bed, is

more suitable. The Group 3 task sheet includes one case study. The scenario in the

task was to choose one of the three alternatives: (1) the closure of one of the two

factories in Australia and relocating operations to Thailand; (2) installing new IT

system for the two factories; and (3) to develop new product designs and to improve

quality control. Pardoe (2000, 130) argues that although aspects of experience ‘‘may

represent merely one set of practices among many’’ within the profession, explicitly

attaching a particular activity or experience to a particular professional scenario is

central to students’ understanding of the profession.

The task sheets state the minimum information students are supposed to present.

Since each group enrolled in this module in different semesters, the task sheets’

requirements differed accordingly. Group 1 was given complete freedom with regard

to the arrangement of the steps. This group’s task sheet explicitly required students to

be concise by using multi-semiotic texts such as graphs and tables where relevant, i.e.

when examining the discount rate, sales growth, machine costs and cost of goods

sold (COGS). This was repeated two times, as shown below.

You are required to complete a detailed report assessing the viability of the investmentproposals. As a starting point determine the Net Present Value for the business as stands

Table 3. The scenario and the word limit of the three task sheets.

Group

number

Task

sheet Scenario Word limit

1 1 Three investment proposals for a leading maker of

electric and acoustic guitars

1500�2000

words

2 2 Two investment proposals for salon and day spa 2000 words

3 3 Three investment proposals for two manufacturing

factories

2000 words

Social Semiotics 7

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

today. Then begin your analysis on the other investment proposals. In yourrecommendations be sure to provide relevant and concise data tables, graphs andoutline any assumptions made.

In addition to the report of the above information provide a one page sensitivitiesanalysis. Examine the discount rate, sales growth, machine costs, and COGS. You willneed to make this as concise as possible so be sure to use graphs and tables whererelevant. Further details of this will be made available during lectures.

Group 1 needs to be ‘‘as concise as possible’’ by largely providing its explanations

through tables and graphs. The Group 1 task sheet includes explicit semiotic

processes that require action, decision and an understanding: ‘‘Complete a detailed

report,’’ ‘‘Determine,’’ ‘‘Provide’’ and ‘‘Examine.’’

In contrast, both Group 2 and Group 3 task sheets stated the minimum

information the management report should include. The requisite to include multi-

semiotic texts in the report occurred only once in Group 2 and Group 3 task sheets,

as shown in Table 4.

Students are expected to read the scenario and engage in social communication

skills with their group members in order to apply the theoretical aspects of financial

management and understand modern finance theory to make sound financial

decisions in the ever-changing field of information and communication industry.

Having introduced the requirements underlying the successful completion of

capital budgeting management reports, I present in the next section the SF-MDA of

management reports. As stated earlier in 2.1, the three reports were written by three

groups: Group 1, Abdulhadi, Saud, Jim and Cathy, Group 2, Abdulrahman and

Jiang, and Group 3, Ibrahim, Hasan, Sharon and Tracey.

Table 4. The requirements in Groups 2 and 3’s task sheets.

Group 2 task sheet Group 3 task sheet

1. A schedule of operating CF forecasts for

the relevant lives of each type of tanning

equipment using 100% (best case), 70%

(most likely case) and 40% (worst case)

occupancy estimates for each tanning

option.

2. The NPV, PP and the IRR for each tanning

option under the various scenarios.

3. An analysis of your findings, recommending

which of the two units would provide the

greatest economic benefits to Patsy? Why?

4. Sensitivity analyses for both tanning

options (using the most likely case � 70%

occupancy estimates).

5. What are some externalities and other

relevant issues that could affect the

decision?

6. Assumptions related to your calculation

and findings.

1. A schedule of incremental after-tax net

operating CF for all three proposals.

2. Use appropriate capital budgeting decision

criteria to evaluate the three alternatives.

However, your decision should be based on

at least 3 criteria such as the NPV, PP and

the IRR.

3. An analysis of your findings and a

recommendation of which proposal would

provide the greatest economic benefits to

the company? Provide justifications.

4. Sensitivity analyses for all three proposals.

5. Other intangible or qualitative factors

relevant for all three proposals.

6. Assumptions related to your calculations

and findings.

8 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

3. An SF-MDA of the experiential meaning in capital budgeting management reports

Students construct disciplinary-specific finance knowledge through meaning-making

processes which involves the interaction of the experiential, the interpersonal and the

textual meanings. The SF-MDA of the experiential meaning seeks to provide an

account of how capital budgeting management reports are typically constructed and

how they relate to their contexts of use through the social purposes. The socio-

cultural context of the three tasks is represented in terms of the three register

variables of FIELD, TENOR and MODE:

� FIELD: accounting and finance mathematical calculations of investment

proposals, using specialised technical terms related to capital budgeting

techniques that are only known by specialists in the field.

� TENOR: students formally engaged with an assessment genre which will only

be read by the tutor (the assessor).Type of interaction: monologue/occasionally

dialogic through the declarative mood element.

� MODE: written to be assessed by a finance academic tutor.Multimodal

discourse: texts, tables and graphs: the latter two are multisemiotic since theyencompass language (titles and labels) and mathematical symbolism.Medium:

print, accompanied by other semiotics (spreadsheets and graphs).Site of

display: assignment submitted on A4 paper.Frame: informative expository

report.

In order to successfully complete the capital budgeting management report students

need to manage the expressions of FIELD, TENOR and MODE through

experiential, interpersonal and textual language metafunctions. Due to space

constraints I investigate here only the way ESL/EAL postgraduate students represent

the experiential, conceptual financial knowledge (3.1). The study of the three

metafunctions in management reports, however, is part of a larger investigation into

the numeracy and literacy experiences of 19 Master of Commerce international

students. In the next section I conduct an SF-MDA of the experiential meaning in

the three groups’ texts (3.1). I also explore the participants’ intuitive interpretations

of the conceptual and procedural capital budgeting procedures (3.2), in addition to

expansion of the experiential meaning (3.3). Group one, two and three management

reports will be labelled, hereafter, texts one, two and three.

3.1. The experiential meaning in capital budgeting management reports

In this section I investigate students’ experience of reality through the TRANSI-

TIVITY choices: their use of participants and process types (material, mental,

verbal, existential, relational and behavioural). The analysis of the TRANSITIVITY

patterns in the three groups’ texts contributes to understanding how the language of

finance construes participants’ experience of the world through technicality

(participants), process types and circumstances. The experiential meaning is also

revealed by investigating structural condensation in mathematical symbolism. The

logical metafunction concerns the representation of the relations between one

process and another, i.e. between clauses. This is achieved through the conjunctive

relationships that are beyond the scope of this paper.

Social Semiotics 9

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

Table 5. The frequency percentage of process types in the three texts.

Process

Relational

Identifying

Text Material Attributive Explicit Implicit Total Behavioural Existential Mental Verbal Total

One 79 35 55 257 312 6 1 24 1 458

17.25% 7.64% 12.00% 56.12% 68.12% 1.31% .22% 5.24% .22% 100%

Two 68 27 20 183 203 0 1 22 5 326

20.86% 8.28% 6.13% 56.14% 62.27% 0.00% .30% 6.75% 1.54% 100%

Three 153 23 46 440 486 1 12 40 3 718

21.31% 3.20% 6.41% 61.28% 67.69% .14% 1.67% 5.57% .42% 100%

10

H.S

.A

lyo

usef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

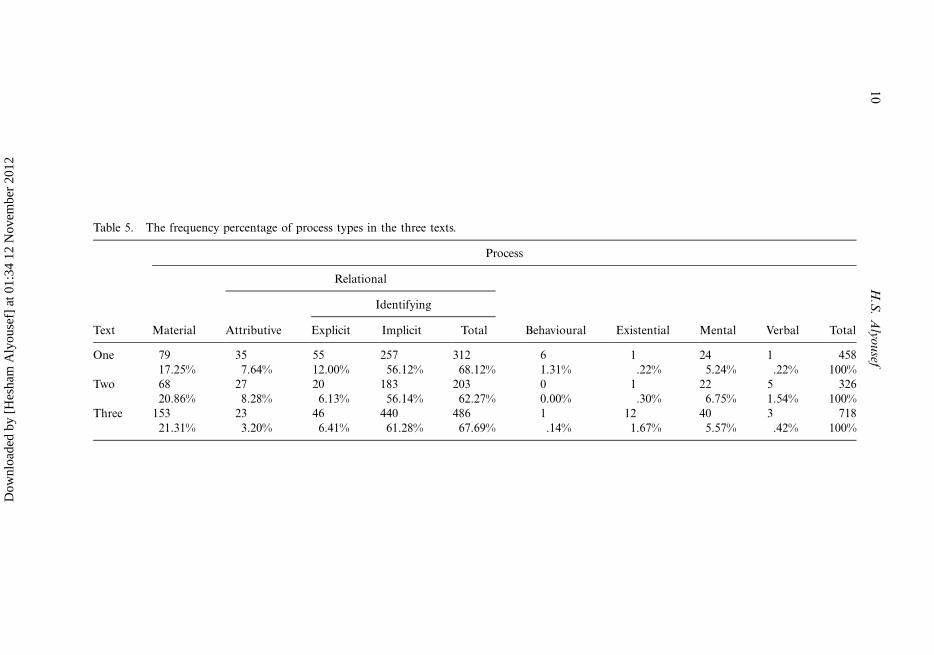

The TRANSITIVITY analysis of the experiential metafunction construed in the

participants’ texts reveals that the most frequently occurring process is the relational

identifying, as shown in Table 5.The analysis reveals that over 62% of the process types are relational identifying,

while material process is the second most frequently occurring type. It should be

noted here that the appendices in the Excel Worksheets had very high frequency of

relational identifying processes in the financial tables, but they were excluded from

the analysis because Group 1 did not manage to save a copy of this file before

submitting it. The use of relational attributive processes ranged between 3.20% and

8.28%. These processes are used for classification and description. From the

TRANSITIVITY analysis it can also be deduced that the participant roles in Texts

1 and 3 are all occupied by inanimate entities, while the ACTOR roles in Text 2 are

occupied by both humans (the writers and Patsy) and inanimate entities. Over 82%

of the relational identifying processes are implicit since they are found in tables, and

are used to identify the value of accounting and finance key terms. The financial

table discourse is highly metaphorical since its components use the implicit

relationships between Token and Value to refer to the participants in a relational

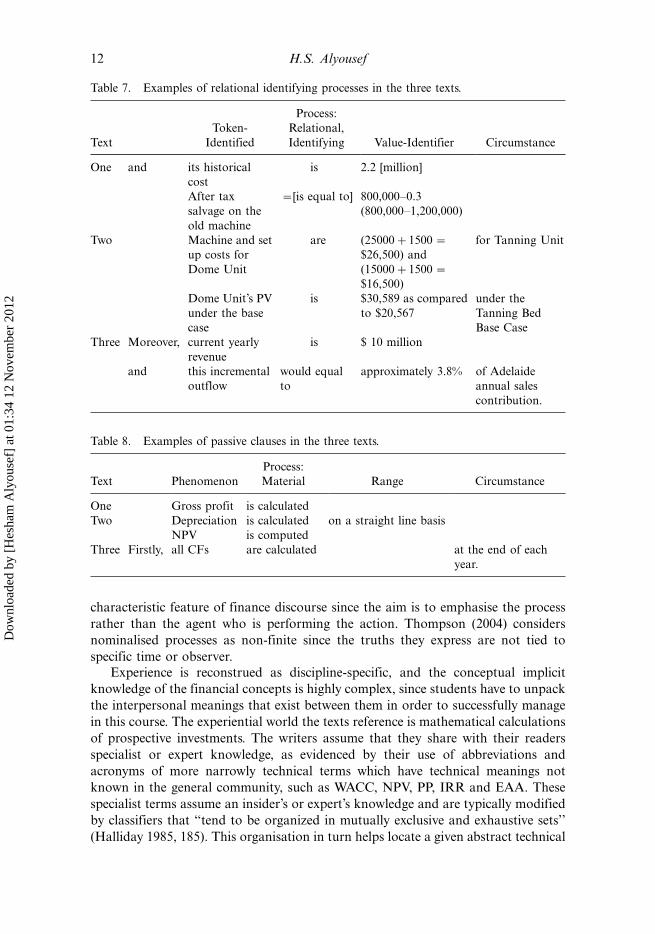

identifying clause; examples extracted from the three texts are given in Table 6.

This process type is used for identification, rather than location or possession.

Halliday and Matthiessen (2004, 234) state that the Token-Value structure plays an

important role in the register of commercial and scientific discourse. Similarly, the

presentation of findings uses the relationship between Token and Value to refer to

the participants in a relational identifying clause; examples extracted from the three

texts are given in Table 7.The three mathematical formulae in Texts 1 and 2 in Table 7 include a number of

material (or operative) processes as discussed in Section 3.3.2. The constituents

‘‘and’’ and ‘‘moreover’’ do not contribute to the experiential meaning, but rather

express textual meanings. As seen in Table 5, Group 1 used more relational

identifying explicit processes (12.00%) than the other two groups. There are also

instances of agentless passives where the writers deleted the ACTORS in passive

clauses because their identity is known to the reader and replaced them with

nominalised abstract technical terms, as in the examples shown in Table 8.

Baratta (2010, 1017) argues that in addition to creating textual cohesion

nominalisations in academic writing ‘‘can assist in maintaining an impersonal

tone, often by deleting a human agent within a given sentence.’’ This seems to be a

Table 6. Examples of implicit relational identifying processes in the financial tables.

Text Token-Identified Process: Relational-Identifying Value-Identifier

One Sales forecast on the basis of 10%

growth rate for the year 2009

[is] 6,600,000

Operating CFs in 2008 [are] 850,000

Two Long-term debt (D) [is] 200,000

The PV of the Dome unit [is] �30588.79

Three Incremental labour cost savings

under the 30% increase from the

base level

[are] 1,378,423

Social Semiotics 11

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

characteristic feature of finance discourse since the aim is to emphasise the process

rather than the agent who is performing the action. Thompson (2004) considers

nominalised processes as non-finite since the truths they express are not tied to

specific time or observer.

Experience is reconstrued as discipline-specific, and the conceptual implicit

knowledge of the financial concepts is highly complex, since students have to unpack

the interpersonal meanings that exist between them in order to successfully manage

in this course. The experiential world the texts reference is mathematical calculations

of prospective investments. The writers assume that they share with their readers

specialist or expert knowledge, as evidenced by their use of abbreviations and

acronyms of more narrowly technical terms which have technical meanings not

known in the general community, such as WACC, NPV, PP, IRR and EAA. These

specialist terms assume an insider’s or expert’s knowledge and are typically modified

by classifiers that ‘‘tend to be organized in mutually exclusive and exhaustive sets’’

(Halliday 1985, 185). This organisation in turn helps locate a given abstract technical

Table 7. Examples of relational identifying processes in the three texts.

Text

Token-

Identified

Process:

Relational,

Identifying Value-Identifier Circumstance

One and its historical

cost

is 2.2 [million]

After tax

salvage on the

old machine

�[is equal to] 800,000�0.3

(800,000�1,200,000)

Two Machine and set

up costs for

Dome Unit

are (25000�1500 �$26,500) and

(15000�1500 �$16,500)

for Tanning Unit

Dome Unit’s PV

under the base

case

is $30,589 as compared

to $20,567

under the

Tanning Bed

Base Case

Three Moreover, current yearly

revenue

is $ 10 million

and this incremental

outflow

would equal

to

approximately 3.8% of Adelaide

annual sales

contribution.

Table 8. Examples of passive clauses in the three texts.

Text Phenomenon

Process:

Material Range Circumstance

One Gross profit is calculated

Two Depreciation is calculated on a straight line basis

NPV is computed

Three Firstly, all CFs are calculated at the end of each

year.

12 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

term within its subclass: for example, in present value the classifier present puts the

item value in a subclass of values, distinguishing it from future value. The three texts

include some terms which do not assume an expert’s knowledge such as profit,

company, tax, bulbs, working hours, revenue and factory.

3.2. Participants’ intuitive interpretations of the conceptual and procedural capitalbudgeting procedures

Since this qualitative study is underpinned by the interpretive worldview it seeks to

explore how participants describe and understand learning tasks rather than merely

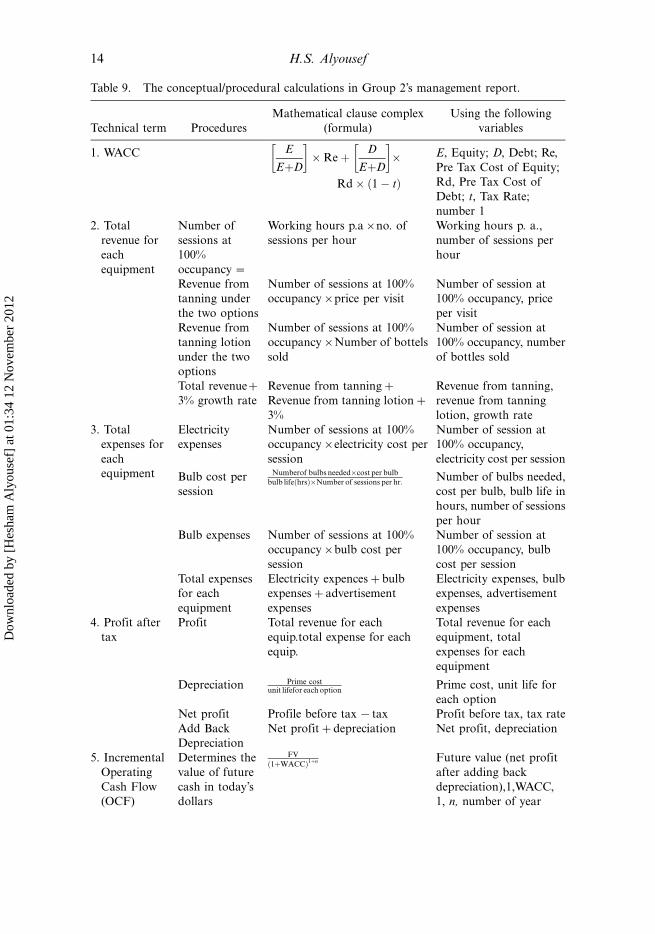

explain what they do (Terre Blanche and Kelly 2002). I therefore unpack in Table 9

the procedures Group 2 performed to successfully complete the management report.

This includes the procedures, mathematical clause complexes) underlying the

formulae and the variables in order to show how a given technical term was

calculated. This explication was elicited from Abdulrahman’s (personal communica-

tion, March 24, 2010) intuitive understandings of the conceptual and procedural

capital budgeting procedures, in addition to my reading of the module’s textbook

(Brigham and Houston 2009).The mathematical clause complexes underlying the formulae are ordered in linear

sequence where each clause is dependent on the previous clause(s), forming what I

call interclausal relations. These relations exhibit the analytical skills since both

participants discern the conceptual ideas underlying the order of the steps. The

Communication Skills Guide for business students (Hancock 2006, 38) states that an

analytical questioning approach refers to students’ ability in ‘‘pulling apart the

elements of the ideas and examining how they operate on each other,’’ while critical

questioning refers to their ability ‘‘in always looking for what is not obvious or for

different points of view.’’ For example, in step 9, critical questioning was experienced

by Group 2 when it decided to use EAA model rather than the Replacement Chain

approach because the longer project (Tanning Dome) does not have exactly twice the

life of the shorter one (Tanning Bed). In addition, intraclausal dependency relations

exist within mathematical clauses. For example, in Step 7 two intraclausal dependency

relations exist between PP and ‘‘investment outlay’’ and PP and ‘‘annual cash

inflows’’ since the calculation of PP is dependent on both ‘‘investment outlay’’ and

‘‘annual cash inflows.’’ Students’ intuitive understanding (or the intended reading

path) of the conceptual and procedural financial processes is contingent upon their

analytical and critical skills to expand the meaning potential by deciphering the

paradigmatic experiential codes underlying interclausal relations and intraclausal

dependency relations. O’Halloran (1999, 23) argues that this results in the semiotic

metaphor, rather than grammatical metaphor, since the ‘‘shifts take place as a result

of movements between semiotic codes.’’ Lemke (1990, 164) states:

Mathematics is a creative art form . . .The knowledge of mathematics consists of twoparts: a practical knowledge of how to perform various manipulations of quantitativeand logical relationships and a theoretical knowledge of how those relationships fittogether to form an overall system within which the manipulations make sense. It is onlythe first part that most people have any conceivable use for, but it is only the second partthat enables you to understand why mathematical procedures work.

Social Semiotics 13

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

Table 9. The conceptual/procedural calculations in Group 2’s management report.

Technical term Procedures

Mathematical clause complex

(formula)

Using the following

variables

1. WACC E

EþD

� �� Re þ D

EþD

� ��

Rd � 1 � tð Þ

E, Equity; D, Debt; Re,

Pre Tax Cost of Equity;

Rd, Pre Tax Cost of

Debt; t, Tax Rate;

number 1

2. Total

revenue for

each

equipment

Number of

sessions at

100%

occupancy �

Working hours p.a�no. of

sessions per hour

Working hours p. a.,

number of sessions per

hour

Revenue from

tanning under

the two options

Number of sessions at 100%

occupancy�price per visit

Number of session at

100% occupancy, price

per visit

Revenue from

tanning lotion

under the two

options

Number of sessions at 100%

occupancy�Number of bottels

sold

Number of session at

100% occupancy, number

of bottles sold

Total revenue�3% growth rate

Revenue from tanning�Revenue from tanning lotion�3%

Revenue from tanning,

revenue from tanning

lotion, growth rate

3. Total

expenses for

each

equipment

Electricity

expenses

Number of sessions at 100%

occupancy�electricity cost per

session

Number of session at

100% occupancy,

electricity cost per session

Bulb cost per

session

Numberof bulbs needed�cost per bulb

bulb life hrsð Þ�Number of sessions per hr:Number of bulbs needed,

cost per bulb, bulb life in

hours, number of sessions

per hour

Bulb expenses Number of sessions at 100%

occupancy�bulb cost per

session

Number of session at

100% occupancy, bulb

cost per session

Total expenses

for each

equipment

Electricity expences�bulb

expenses�advertisement

expenses

Electricity expenses, bulb

expenses, advertisement

expenses

4. Profit after

tax

Profit Total revenue for each

equip.total expense for each

equip.

Total revenue for each

equipment, total

expenses for each

equipment

Depreciation Prime costunit lifefor each option

Prime cost, unit life for

each option

Net profit Profile before tax �tax Profit before tax, tax rate

Add Back

Depreciation

Net profit�depreciation Net profit, depreciation

5. Incremental

Operating

Cash Flow

(OCF)

Determines the

value of future

cash in today’s

dollars

FV

1þWACCð Þ1þn Future value (net profit

after adding back

depreciation),1,WACC,

1, n, number of year

14 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

To successfully manage capital budgeting techniques, students need to have the

ability to unpack the mathematical idea(s) compressed in a given formula

(intraclausal relation) and relate it to the preceding and/or the following procedures

(interclausal relation). To do so, they need to exhibit both analytical and critical

skills that will enable them to build logically and linearly sequenced mathematical

clause complexes, as evidenced by their intuitive expansion of the experiential

meaning. For example, depreciation is deducted from revenue and then added back

(Step 4) before applying PV formula (Step 5) because it is a non-cash expense. The

PV is determined by discounting the future CF at the appropriate discount rate (the

project’s cost of capital, WACC). Similarly, the idea of NPV (Step 6) is to determine

how much value an investment adds to a company. NPV is calculated by adding

initial investment cost (negative value) to the sum of the discounted CFs. In Step 7,

PP refers to the time it takes to recovering the costs of an investment; it does not take

account of risk and the time value of money. Investments with shorter PP are

preferable since risk is minimised and liquidity is maximised. An alternative to this

approach is the discounted payback. The IRR, Step 8, is the break-even discount

rate, and it refers to the required rate of return that forces PV of inflows equal to cost,

and the NPV equals to zero; any project should be avoided if the cost of capital

exceeds this rate. IRR is the break-even discount rate, and it is found by trial and

Table 9 (Continued )

Technical term Procedures

Mathematical clause complex

(formula)

Using the following

variables

6. NPV NPV

determines the

net value of

future cash in

today’s dollars

after deducting

investment

outlay

PTt�1

Ct

1þrð Þt � Co

S, sum of PVs of CFs

expected from the

project; t, project/

investment’s duration in

years; Ct, OCFs; r,

discount rate/the

required minimum rate

of return on investment;

and Co, investment

outlay (initial investment

made).

7. PP Investment outlay

annual cash inflowsInvestment outlay,

annual cash inflows

8. IRR Similar in many

ways to the

NPV approach

CF1

1þrð Þ1 þ CF2

1þrð Þ2 þ CF3

1þrð Þ3 þ CFn

1þrð Þn ¼ 0 CF �cash flow

generated in the specific

period (the last period

being ‘n’); R, WACC

9. EAAa R NPVð Þ1� 1þRð Þ�n NPV �net PV of the

project; r, rate of return;

n, number of years

10. Sensitivity

analysis

Repeat steps 2-8 but with increase as well as decrease in revenues to the

extent of 10%

Source: Adapted from Group 2’s appendices, the textbook (Brigham & Houston, 2009) and financeformula’s website Bhttp://www.financeformulas.net�aInvestopedia, http://www.financeformulas.net/Equivalent_Annual_Annuity.html

Social Semiotics 15

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

error. The analyst creates a given set of scenarios to determine how changes in one

variable will impact the target variable. Finally, the investments are evaluated: accept

if NPV �0 and/or IRR �WACC. If IRR exceeds WACC, the difference will be the

bonus which a company receives. In Step 9, EAA refers to the benefit from theproject spread out over the life of the project. Finally, sensitivity analysis (Step 10)

focuses on analysing the effects of changes in key variables on the project’s IRR or

NPV. Scenario analysis (Brigham and Houston, 2009, 378) allows for a change in

‘‘more than one variable at a time, and it incorporates the probabilities of changes in

key variables’’ that may be influenced by market conditions such as sales price,

variable cost per unit, number of units sold, fixed operating costs and WACC.

Abdulrahman’s group conducted scenario analyses for an increase as well as decrease

in revenues to the extent of 10% by repeating Steps 2�8.The next section’s focus is on investigating the way the mathematical symbolism

is represented and interwoven into natural language in management reports.

3.3. Expansion of the experiential meaning

O’Halloran (1999) contends that semantic extensions in mathematical symbolism are

characterised by the introduction of multiple levels of rankshifted configurations of

new participants, new ‘‘operative’’ processes and the deletion of the human agent. In

this section I focus on the semantic extensions in financial graphs and a financial

formula.

3.3.1. The experiential meaning in financial graphs

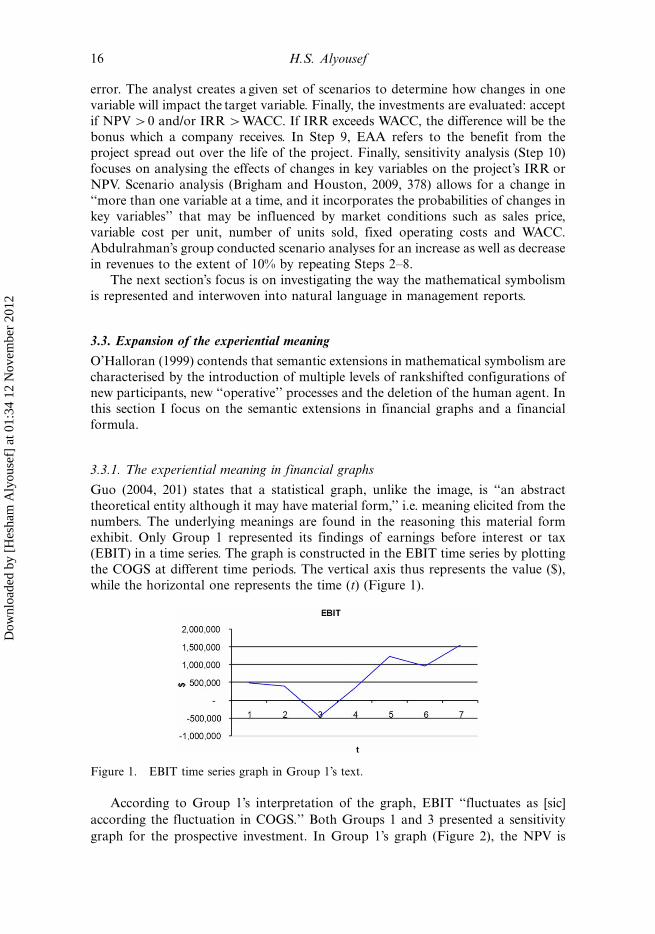

Guo (2004, 201) states that a statistical graph, unlike the image, is ‘‘an abstract

theoretical entity although it may have material form,’’ i.e. meaning elicited from the

numbers. The underlying meanings are found in the reasoning this material formexhibit. Only Group 1 represented its findings of earnings before interest or tax

(EBIT) in a time series. The graph is constructed in the EBIT time series by plotting

the COGS at different time periods. The vertical axis thus represents the value ($),

while the horizontal one represents the time (t) (Figure 1).

According to Group 1’s interpretation of the graph, EBIT ‘‘fluctuates as [sic]

according the fluctuation in COGS.’’ Both Groups 1 and 3 presented a sensitivity

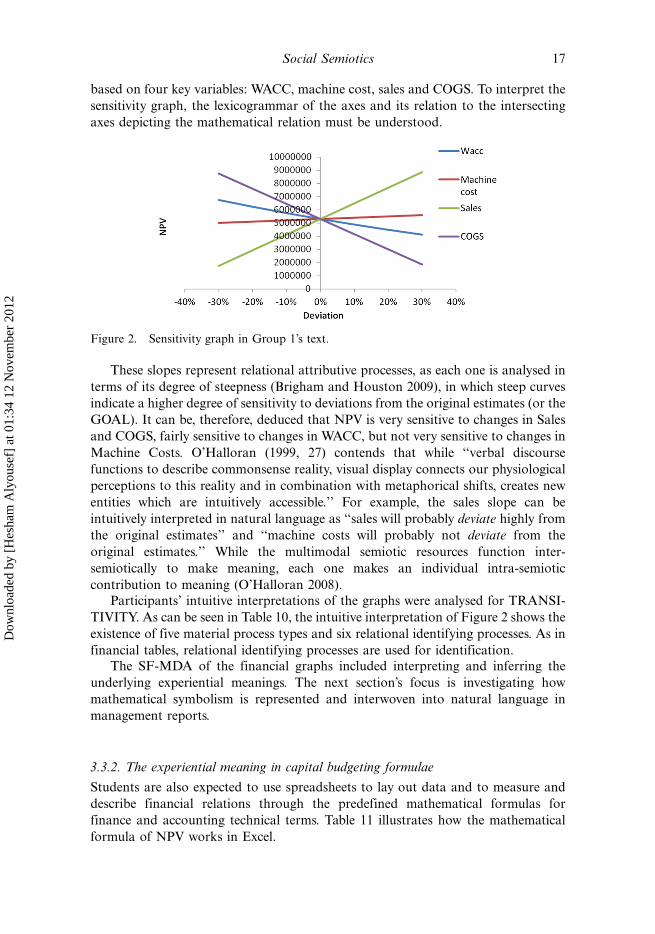

graph for the prospective investment. In Group 1’s graph (Figure 2), the NPV is

Figure 1. EBIT time series graph in Group 1’s text.

16 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

based on four key variables: WACC, machine cost, sales and COGS. To interpret the

sensitivity graph, the lexicogrammar of the axes and its relation to the intersecting

axes depicting the mathematical relation must be understood.

These slopes represent relational attributive processes, as each one is analysed in

terms of its degree of steepness (Brigham and Houston 2009), in which steep curves

indicate a higher degree of sensitivity to deviations from the original estimates (or the

GOAL). It can be, therefore, deduced that NPV is very sensitive to changes in Sales

and COGS, fairly sensitive to changes in WACC, but not very sensitive to changes in

Machine Costs. O’Halloran (1999, 27) contends that while ‘‘verbal discourse

functions to describe commonsense reality, visual display connects our physiological

perceptions to this reality and in combination with metaphorical shifts, creates new

entities which are intuitively accessible.’’ For example, the sales slope can be

intuitively interpreted in natural language as ‘‘sales will probably deviate highly from

the original estimates’’ and ‘‘machine costs will probably not deviate from the

original estimates.’’ While the multimodal semiotic resources function inter-

semiotically to make meaning, each one makes an individual intra-semiotic

contribution to meaning (O’Halloran 2008).

Participants’ intuitive interpretations of the graphs were analysed for TRANSI-

TIVITY. As can be seen in Table 10, the intuitive interpretation of Figure 2 shows the

existence of five material process types and six relational identifying processes. As in

financial tables, relational identifying processes are used for identification.The SF-MDA of the financial graphs included interpreting and inferring the

underlying experiential meanings. The next section’s focus is investigating how

mathematical symbolism is represented and interwoven into natural language in

management reports.

3.3.2. The experiential meaning in capital budgeting formulae

Students are also expected to use spreadsheets to lay out data and to measure and

describe financial relations through the predefined mathematical formulas for

finance and accounting technical terms. Table 11 illustrates how the mathematical

formula of NPV works in Excel.

Figure 2. Sensitivity graph in Group 1’s text.

Social Semiotics 17

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

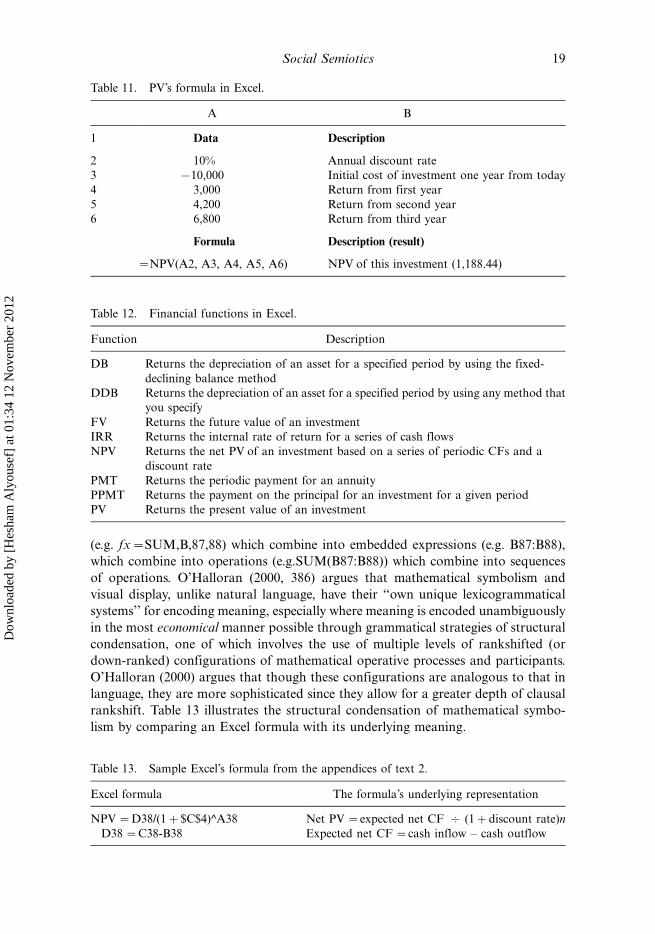

Students enter the values in the cells A2, A3, A4, A5 and A6. Excel includes a

number of preset formulae that are arranged according to the field (e.g. Finance,

Logic and Math). Students tab the FORMULAS button and then choose

FINANCIAL which includes functions such as those given in Table 12.O’Halloran (2005) argues that the grammar of mathematics specifies how

elements of different rank can be combined. For example, Abdulrahman’s group

uses the mathematical symbolism ‘‘fx�SUM(B87:B88)’’ to calculate operating cash

flows (OCFs), where B87 refers to the cell containing ‘‘profit after taxes’’ and B88 to

‘‘depreciation.’’ The structure of this formula is built up from minimal components

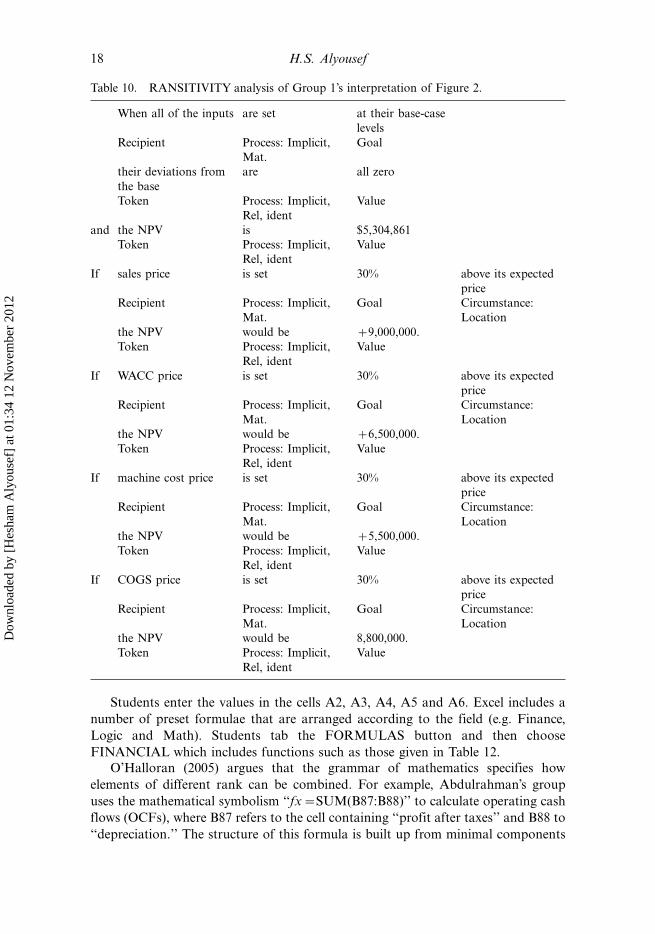

Table 10. RANSITIVITY analysis of Group 1’s interpretation of Figure 2.

When all of the inputs are set at their base-case

levels

Recipient Process: Implicit,

Mat.

Goal

their deviations from

the base

are all zero

Token Process: Implicit,

Rel, ident

Value

and the NPV is $5,304,861

Token Process: Implicit,

Rel, ident

Value

If sales price is set 30% above its expected

price

Recipient Process: Implicit,

Mat.

Goal Circumstance:

Location

the NPV would be �9,000,000.

Token Process: Implicit,

Rel, ident

Value

If WACC price is set 30% above its expected

price

Recipient Process: Implicit,

Mat.

Goal Circumstance:

Location

the NPV would be �6,500,000.

Token Process: Implicit,

Rel, ident

Value

If machine cost price is set 30% above its expected

price

Recipient Process: Implicit,

Mat.

Goal Circumstance:

Location

the NPV would be �5,500,000.

Token Process: Implicit,

Rel, ident

Value

If COGS price is set 30% above its expected

price

Recipient Process: Implicit,

Mat.

Goal Circumstance:

Location

the NPV would be 8,800,000.

Token Process: Implicit,

Rel, ident

Value

18 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

(e.g. fx�SUM,B,87,88) which combine into embedded expressions (e.g. B87:B88),

which combine into operations (e.g.SUM(B87:B88)) which combine into sequences

of operations. O’Halloran (2000, 386) argues that mathematical symbolism and

visual display, unlike natural language, have their ‘‘own unique lexicogrammatical

systems’’ for encoding meaning, especially where meaning is encoded unambiguously

in the most economical manner possible through grammatical strategies of structural

condensation, one of which involves the use of multiple levels of rankshifted (or

down-ranked) configurations of mathematical operative processes and participants.

O’Halloran (2000) argues that though these configurations are analogous to that in

language, they are more sophisticated since they allow for a greater depth of clausal

rankshift. Table 13 illustrates the structural condensation of mathematical symbo-

lism by comparing an Excel formula with its underlying meaning.

Table 11. PV’s formula in Excel.

A B

1 Data Description

2 10% Annual discount rate

3 �10,000 Initial cost of investment one year from today

4 3,000 Return from first year

5 4,200 Return from second year

6 6,800 Return from third year

Formula Description (result)

�NPV(A2, A3, A4, A5, A6) NPV of this investment (1,188.44)

Table 12. Financial functions in Excel.

Function Description

DB Returns the depreciation of an asset for a specified period by using the fixed-

declining balance method

DDB Returns the depreciation of an asset for a specified period by using any method that

you specify

FV Returns the future value of an investment

IRR Returns the internal rate of return for a series of cash flows

NPV Returns the net PV of an investment based on a series of periodic CFs and a

discount rate

PMT Returns the periodic payment for an annuity

PPMT Returns the payment on the principal for an investment for a given period

PV Returns the present value of an investment

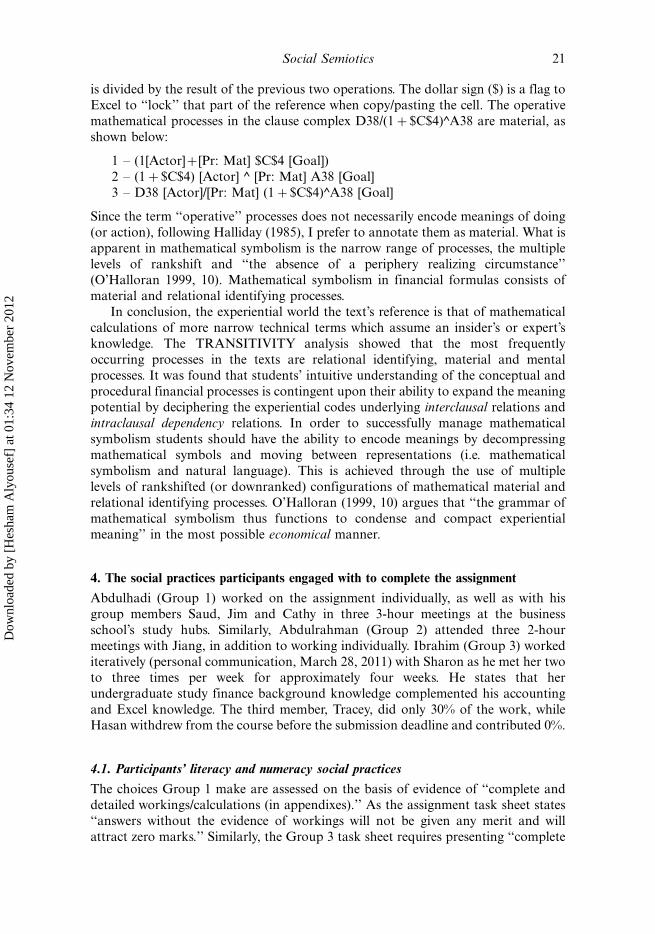

Table 13. Sample Excel’s formula from the appendices of text 2.

Excel formula The formula’s underlying representation

NPV �D38/(1�$C$4)^A38

D38 �C38-B38

Net PV �expected net CF } (1�discount rate)n

Expected net CF �cash inflow � cash outflow

Social Semiotics 19

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

The symbol ‘‘D38’’ refers to the cell containing the ‘‘Expected Net Cash Flow,’’

the symbol (1�$C$4) means adding one to the discount rate located in cell C4, and

the circumflex accent (caret) in ^A38 means raised to the power of the value (the

number of years) in cell A38. The participant D38 refers to an ellipsed operative

process C38-B38. Invoking Halliday’s (1985) system of TRANSITIVITY, O’Hallor-

an (1999) argues that semantic extensions in mathematical symbolism are repre-

sented experientially by participants’ intuitive verbal interpretations of the operative

processes which result in the semiotic metaphor since these processes lead to the

creation of a thing or entities. Operative processes are conceived as arithmetic

operations performed on mathematical objects such as numbers, variable and other

abstract quantities. Since operative processes include multiple mediums (or interact

with an unlimited number of participants) Halliday’s notion of a single central

medium (or participant) may no longer be applicable in mathematical symbolism

(O’Halloran 1999). For example, the Excel formulae in Table 13 consist of the

following ascending rank scale:

Term or ‘‘atom’’: NPV, D38, 1, $C$4, A38, C38, B38 (i.e. word)Expression: NPV, D38, 1, $C$4, A38, �$C$4, C38, B38, �B38 (i.e. word group/phrase)Clause: C38-B38 and (1�$C$4)^A38 (i.e. clause)Clause complex: NPV �D38/(1�$C$4)^A38, where D38 �C38-B38 (i.e. clausecomplex)

Expressions in mathematical statements consist of an implicit relational intensive

identifying process, exemplified by the equal sign: i.e. NPV [Token: Agent, Identified]

equals [Process: Relational, Intensive identifying] D38/ (1�$C$4)^A38

[Value: Mediums, identifier]. The medium, D38/ (1�$C$4)^A38, consists of what

O’Halloran (1999, 5) calls ‘‘multiple mediums connected with operative processes as

opposed to the notion of a single medium found in the process types of natural

language.’’

In addition to the relational intensive identifying process, the mathematical

formula shown in Table 14 includes operative processes of subtraction, exponentia-

tion, addition and division: D38 calculated by subtracting C38 from B38, $C$4 is

added to one, raised to the power of the value (the number of years) in A38, and D38

Table 14. Rankshifted nuclear configurations of mathematical processes and participants in

NPV formula.

Rank Process Participants

Rank 1 (ranking clause) � (Relational) NPV

D38/(1�$C$4)^A38

Rank 2 � (Operative) C38

B38

Rank 3 � (Operative) 1

$C$4

Rank 4 ^ (Operative) (1�$C$4)

A38

Rank 5 /(Operative) D38 (�C38-B38)

(1�$C$4)^A38

20 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

is divided by the result of the previous two operations. The dollar sign ($) is a flag to

Excel to ‘‘lock’’ that part of the reference when copy/pasting the cell. The operative

mathematical processes in the clause complex D38/(1�$C$4)^A38 are material, as

shown below:

1 � (1[Actor]�[Pr: Mat] $C$4 [Goal])

2 � (1�$C$4) [Actor] ^ [Pr: Mat] A38 [Goal]

3 � D38 [Actor]/[Pr: Mat] (1�$C$4)^A38 [Goal]

Since the term ‘‘operative’’ processes does not necessarily encode meanings of doing

(or action), following Halliday (1985), I prefer to annotate them as material. What is

apparent in mathematical symbolism is the narrow range of processes, the multiple

levels of rankshift and ‘‘the absence of a periphery realizing circumstance’’(O’Halloran 1999, 10). Mathematical symbolism in financial formulas consists of

material and relational identifying processes.

In conclusion, the experiential world the text’s reference is that of mathematical

calculations of more narrow technical terms which assume an insider’s or expert’s

knowledge. The TRANSITIVITY analysis showed that the most frequently

occurring processes in the texts are relational identifying, material and mental

processes. It was found that students’ intuitive understanding of the conceptual and

procedural financial processes is contingent upon their ability to expand the meaningpotential by deciphering the experiential codes underlying interclausal relations and

intraclausal dependency relations. In order to successfully manage mathematical

symbolism students should have the ability to encode meanings by decompressing

mathematical symbols and moving between representations (i.e. mathematical

symbolism and natural language). This is achieved through the use of multiple

levels of rankshifted (or downranked) configurations of mathematical material and

relational identifying processes. O’Halloran (1999, 10) argues that ‘‘the grammar of

mathematical symbolism thus functions to condense and compact experientialmeaning’’ in the most possible economical manner.

4. The social practices participants engaged with to complete the assignment

Abdulhadi (Group 1) worked on the assignment individually, as well as with his

group members Saud, Jim and Cathy in three 3-hour meetings at the business

school’s study hubs. Similarly, Abdulrahman (Group 2) attended three 2-hour

meetings with Jiang, in addition to working individually. Ibrahim (Group 3) worked

iteratively (personal communication, March 28, 2011) with Sharon as he met her two

to three times per week for approximately four weeks. He states that her

undergraduate study finance background knowledge complemented his accounting

and Excel knowledge. The third member, Tracey, did only 30% of the work, whileHasan withdrew from the course before the submission deadline and contributed 0%.

4.1. Participants’ literacy and numeracy social practices

The choices Group 1 make are assessed on the basis of evidence of ‘‘complete and

detailed workings/calculations (in appendixes).’’ As the assignment task sheet states

‘‘answers without the evidence of workings will not be given any merit and will

attract zero marks.’’ Similarly, the Group 3 task sheet requires presenting ‘‘complete

Social Semiotics 21

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

and detailed workings/calculations (attach the excel spreadsheets with appropriate

references),’’ and that ‘‘answers without evidence of workings (in appendices or excel

spreadsheets) will not be given any merit and will attract zero marks.’’

Unlike Group 1, Groups 2 and 3 did not face major difficulties when undertaking

the assignment. Abdulrahman (Group 2) read the task sheet several times and then

wrote down some notes to help him plan his representation of the task. Later on he

decided to meet the tutor to enquire whether he should include the inflation rate of

3% in his calculations or not (personal communication, February 26, 2010).

Although the tutor’s reply was positive, Abdulrahman forgot to add this rate. He

adds that the peer-assisted student support (PASS) sessions helped him with

understanding the module’s content. These sessions are facilitated by students who

have excelled in the module. As Abdulrahman was struggling with this module he

sought the tutor’s help who in turn assigned an assistant to work with him. He often

consults the financial management Arabic textbook which he brought with him from

Saudi Arabia. Abdulrahman states that he learnt how to use the financial calculator

when he started his postgraduate study in Australia. He explains the steps for

calculating NPV and the time value of money (TVM):

. . . to calculate NPV of $3000 earned in two years: enter this amount in future value(FV) key - enter 2 for the time period (NPER/N key) - enter 10% by using the % i key foryour rate because that’s what you’d like to earn. TVM is the number of years it takes toreceive FV, and it is calculated by entering interest rate using the i key, present value ofmoney PV key, and future value of money, FV key.

Abdulhadi (personal communication, March 22, 2010) states that he referred to his

classmates in order to ask for clarification on points he did not understand. Saud

(personal communication, March 29, 2010) states that the textbook and the

module’s study-guide were the main sources they referred to. When asked if Group

1 had faced in difficulties in undertaking the assignment, Saud replies ‘‘Yes,

everything was difficult. The calculation in general and data collection in question

2.’’ Ibrahim (personal communication, March 28, 2011) states that the first thing

he did when he was handed the task sheet was to read the requirements before

looking at the given information in order to gain insights about the topics and the

required volume of work. Ibrahim and Sharon met in the study hubs at the

business school. Interestingly, they used the whiteboard to list each step and its

relevant calculations. Ibrahim argues that most of the groups faced ‘‘difficulties in

decoding the scenario’’: i.e. ‘‘what this and that mean?’’ The tutor arranged a

consultation meeting with the students in order to collect their enquiries and then

he sent an e-mail to all the students to clarify the ambiguities. Both Abdulrahman

and Ibrahim utilised their professional accounting work experience when doing the

assignment.

The academic social practices students performed in order to successfully

complete the tasks are listed below, though they are not an exhaustive list of the

whole range of literacy and numeracy practices participants engaged with:

� Attending Principles of Finance lectures and tutorial discussions regularly;

� Checking the university’s e-mail on a daily basis to see if there are any

assignment-related updates;

22 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

� Working with a small-size group (two to five students) to check understanding

of the task by outlining the minimum required information for each proposal,

dividing roles between members, and thereby developing collaborative

response to the assignment;� Taking notes, typing in a Word processor, drawing tables and graphs, using a

financial calculator, and using Excel to build tables, utilise built-in formulas

and to add, subtract, multiply, divide and work out percentages;

� Reading the assignment task sheet, the module’s study-guide, Principles of

Finance textbook � Fundamentals of Financial Management by Brigham and

Houston (2009); and

� Seeking clarification from the tutor, from peers and asking a friend to

proofread the report.

In a 39-minute unstructured interview with Group 2’s tutor, Janet (personal

communication, March 4, 2010), she commented that the major learning outcome

the task seeks to achieve is practising one of the two capital budgeting models in

order to develop their communication and problem-solving skills, thereby gaining

meaningful life-long learning experience that will enable them to deal with those

offering insights into their future career. She argued that most students overlooked

the following aspects in their capital budgeting analysis:

� Labour (‘‘wage expenses’’) and bulb costs in CF;

� Incorporating inflation into the capital budget;

� External factors that may affect business environment; and

� Ignoring much of the information by not reading the case study carefully.

She also added that she did not have time to give students feedback on this task

because, upon their request, they were granted one-week extension to submit theassignment which coincided with the end of the semester. Finally, the tutor commented

that she assessed students’ work on the basis of the procedures they used and not solely

on the basis of final results, as students construct discipline-specific knowledge

through these successive processes. Ibrahim (Group 3) is aware of this as he (personal

communication, March 28, 2011) states ‘‘the tutor assesses the procedures and not the

final numbers’’ which include the assumptions, calculations, the criteria used to

evaluate, the decision, sensitivity analysis and the conclusion based on the analysis.

4.2. Cross-disciplinary knowledge

The linguistic and numeracy choices participants have made are indicators of the

disciplinary-specific accounting and finance knowledge they have acquired and their

subjective interpretation. As Baker, Street, and Tomlin (2003, 12) noted, numeracy

events are ‘‘occasions in which a numeracy activity is integral to the nature of the

participants’ interactions and their interpretative processes.’’ Cross-disciplinary

knowledge is therefore required to successfully complete the capital budgetingmanagement report. This includes

� Knowledge of key technical terms and the relationships that exist between

them;

Social Semiotics 23

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

� Knowledge of the literacy and numeracy skills of finance and financial

accounting (e.g. gross profit, depreciations and CF);

� Calculating operating CFs, NPV, PP, IRR and sensitivity;

� Using a financial calculator to compute basic as well as advance financialanalyses;

� Knowledge of spreadsheets (e.g. Excel software) to lay out data and to

measure and describe relations among theoretical aspects. This includes using

the function key ‘‘fx’’ to set up an Excel formula;

� The ability to encode meanings by decompressing mathematical symbols and

moving between representations;

� The use of multiple levels of rankshifted configurations of mathematical

material and relational identifying processes;� The ability to unpack the underlying meanings of technical terms and the

mathematical ideas compressed in formulae and to translate between

algebraic, numeric and geometric representations; and

� Knowledge of the procedures used in determining the financial concepts

underlying capital budgeting techniques.

4.3. Participants’ literacy social practices and future workplace and life prospects

Literacy and numeracy social practices of capital budgeting management reports

require a repertoire of linguistic practices that are based on complex sets of

discourses, identities and values. The range of the complex literacy and numeracy

practices investigated in this paper lead us to enquire about the extent to which these

practices resemble the functional behaviours (or ‘‘competencies’’) valued in the

workplace. How does what is done in this module impact upon students’ perceptions

of their work prospects?

While Groups 1 and 2 believe that they will be able to apply capital budgeting

techniques in their future work, albeit minimally, Group 3 holds the opposite view.

Abdulhadi (personal communication, March 22, 2010) believes that this task will not

be related to his future work since he is studying Master of Commerce in accounting,

and unfortunately this foundation business module is prerequisite for all Master of

Commerce students. Abdulhadi initially planned to major in accounting and finance,

but later he decided to change his major into accounting. Abdulrahman (personal

communication, March 24, 2010) argues that all capital budgeting decision criteria

like NPV, IRR and PP are analysed by computers. One of the members in Group 3,

Ibrahim (personal communication, March 28, 2011) argues that capital budgeting

procedures resemble 80�90% of workplace practices. As he puts it:

I have a reason to say this. I have worked on project biddings in my company but froman accountant view and not finance. Therefore I faced the same problem in thisassignment when my company wants to make biddings for four or five aircrafts. Sinceyou’re facing competitors you have to study the project biddings carefully, and theassumptions are part and parcel of this report.

The range of the complex literacy and numeracy practices investigated in this

paper shows that students seem to have benefited from this task through a number

24 H.S. Alyousef

Dow

nloa

ded

by [

Hes

ham

Aly

ouse

f] a

t 01:

34 1

2 N

ovem

ber

2012

of aspects. First, as shown in Section 2.4, this task primarily aims at improving

students’ analytic, critical and interpersonal communication skills through their

interaction with peers. Second, students have practised the schematic structure of

management reports, which was elicited from the social purpose of the task sheet.Third, as Abdulrahman explained, students learnt from this course that capital

budgeting requires taking into account any external factors that are difficult to

quantify and may affect costs and benefits, such competition and timing. As

Visscher and Stansfield (1997) argue, capital budgeting complexities arise from

students’ ability to recognise costs and benefits that are difficult to quantify.