SHALE GAS - CHALLENGES

AND OPPORTUNITIES

Gopal Singh,

Alok Kumar Singh

13th November ’2013

BP Statistical Review of World Energy 2013

Primary energy consumption per capita 2012Tonnes oil equivalent

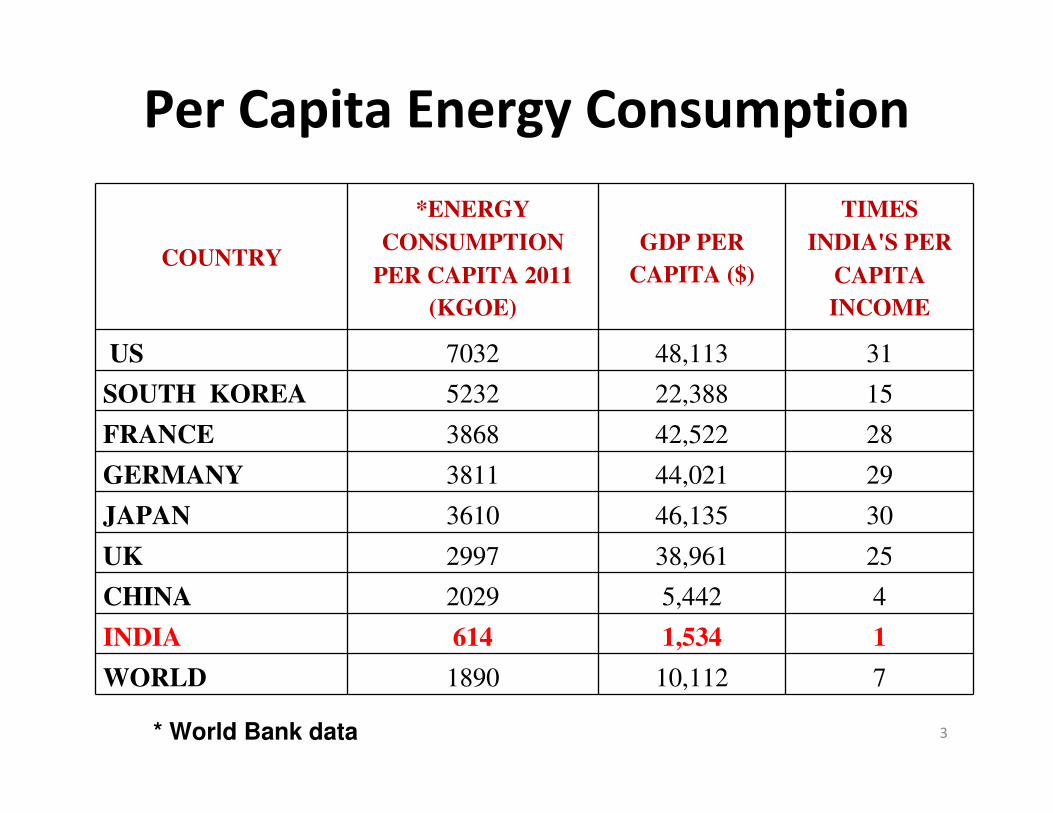

Per Capita Energy Consumption

3

COUNTRY

*ENERGY

CONSUMPTION

PER CAPITA 2011

(KGOE)

GDP PER

CAPITA ($)

TIMES

INDIA'S PER

CAPITA

INCOME

US 7032 48,113 31

SOUTH KOREA 5232 22,388 15

FRANCE 3868 42,522 28

GERMANY 3811 44,021 29

JAPAN 3610 46,135 30

UK 2997 38,961 25

CHINA 2029 5,442 4

INDIA 614 1,534 1

WORLD 1890 10,112 7

* World Bank data

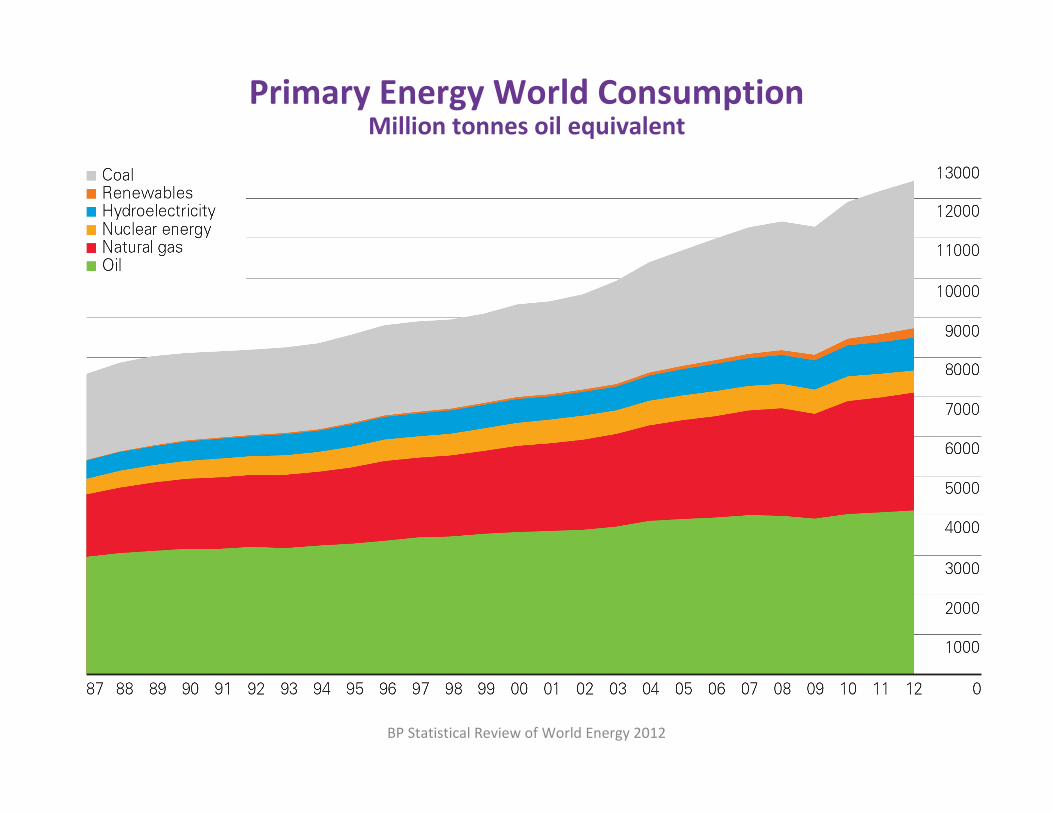

BP Statistical Review of World Energy 2012

Primary Energy World ConsumptionMillion tonnes oil equivalent

5

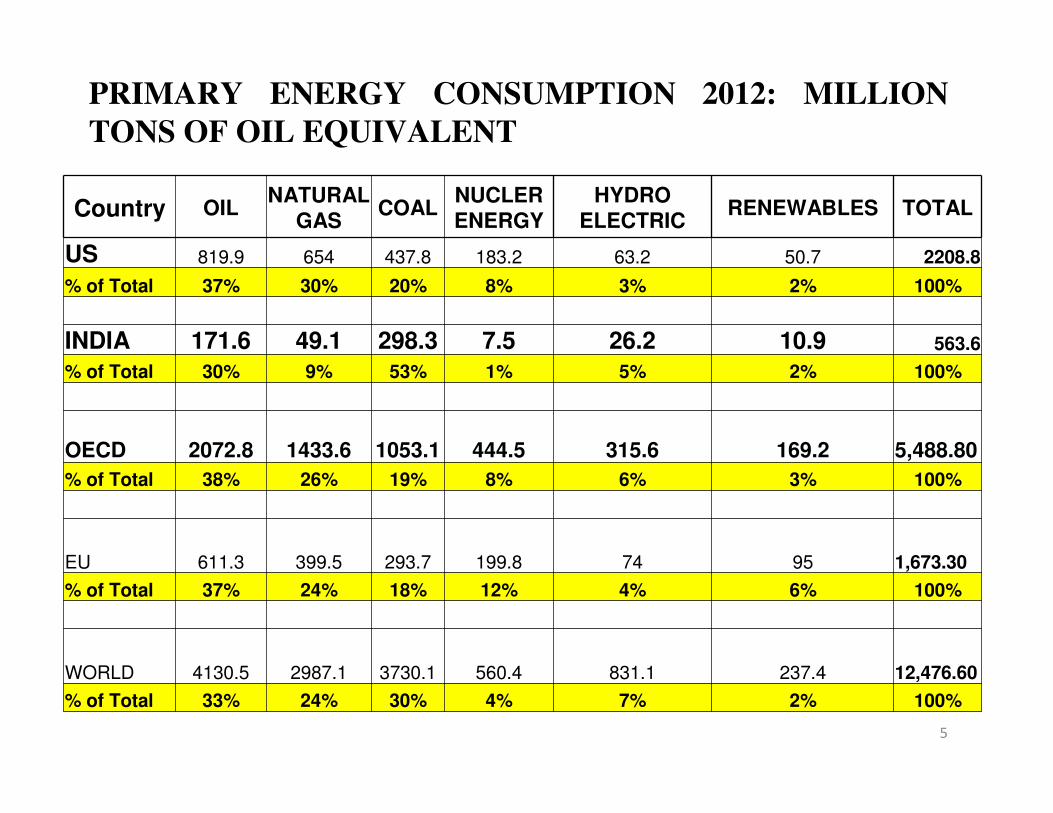

Country OILNATURAL

GASCOAL

NUCLER ENERGY

HYDRO ELECTRIC

RENEWABLES TOTAL

US 819.9 654 437.8 183.2 63.2 50.7 2208.8

% of Total 37% 30% 20% 8% 3% 2% 100%

INDIA 171.6 49.1 298.3 7.5 26.2 10.9 563.6

% of Total 30% 9% 53% 1% 5% 2% 100%

OECD 2072.8 1433.6 1053.1 444.5 315.6 169.2 5,488.80

% of Total 38% 26% 19% 8% 6% 3% 100%

EU 611.3 399.5 293.7 199.8 74 95 1,673.30

% of Total 37% 24% 18% 12% 4% 6% 100%

WORLD 4130.5 2987.1 3730.1 560.4 831.1 237.4 12,476.60

% of Total 33% 24% 30% 4% 7% 2% 100%

PRIMARY ENERGY CONSUMPTION 2012: MILLION

TONS OF OIL EQUIVALENT

Trends in Supply of Primary Commercial

Energy – INDIA (mtoe)*

6

DOMESTIC PRODUCTION 2000-01 2006-07 2011-122016-17

(Proj.)

2021-22

(Proj.)

COAL 130.61 177.24 222.16 308.55 400

LIGNITE 6.43 8.76 10.64 16.8 29

CRUDE OIL 33.4 33.99 39.23 42.75 43

NATURAL GAS 25.07 27.71 42.79 76.13 103

HYDRO POWER 6.4 9.78 11.22 12.9 17

NUCLEAR POWER 4.41 4.91 8.43 16.97 30

RENEWABLE ENERGY 0.13 0.87 5.25 10.74 20

TOTAL DOMESTIC

COMMERCIAL ENERGY 206.45 263.26 339.72 481.84 642

NON COMMERCIAL

ENERGY136.64 153.28 174.2 187.66 202.16

TOTAL 343.09 416.54 513.92 669.5 844.16

*XII PLAN DOCUMENT, PLANNING COMMISSION

Trends in Supply of Primary Commercial

Energy – INDIA (mtoe)

7

IMPORTS 2000-01 2006-07 2011-122016-1 7

(Proj.)

2021-22

(Proj.)

COAL 11.76 24.92 54 90 150

PETROLEUM PRODUCTS 71.25 98.41 129.86 152.44 194

LNG 0 8.45 12.56 24.8 31

HYDRO POWER 0 0.26 0.45 0.52 0.6

TOTAL NET IMPORTS 83.01 132.04 196.87 267.76 375.6

Total Commercial Energy 289.46 395.3 536.59 749.6 1017.6

Commercial Energy

requirement met by

Imports

29% 33% 37% 36% 37%

CAGR over previous 5 years 5.01% 6.25% 6.91% 6.30%

Total Primary Energy 426.1 548.58 710.79 937.26 1219.76

CAGR over previous 5 years 4.09% 5.28% 5.69% 5.41%Primary Energy

requirement met by

Imports

19% 24% 28% 29% 31%

Shale Gas – An introduction

8

Natural gas (mainly methane) is generally classified under two heads:

(a)Conventional Gas: Most of the natural gas that is produced globally comes under the category of

conventional gas where, after drilling in a sedimentary basin that is rich in gas, the gas migrates through

porous rocks into reservoirs and flows freely to the surface where it is collected, treated, and then piped

to various users.and

(b) Unconventional Gas: Shale gas on the other hand is located in rocks of very low permeability and

does not easily flow. Therefore, the technique for recovery of shale gas is quite different from that of

conventional gas.

Natural Gas Resources

9

Natural Gas & Oil Production in India

10

YEAR CBM (BCM)CBM as % of Natural Gas

NATURAL GAS (billion cubic metres)

OIL (Million Tonnes)

2004-05 31.763 33.981

2005-06 32.202 32.19

2006-07 31.747 33.988

2007-08 0.015 0.05% 32.417 34.118

2008-09 0.02 0.06% 32.845 33.508

2009-10 0.038 0.08% 47.496 33.69

2010-11 0.041 0.08% 52.219 37.684

2011-12 0.084 0.18% 47.559 38.09

2012-13 0.107 0.25 % 40.68 37.86

11

Natural Gas & Oil Production in India

The extent of the increase in energy requirement over the Twelfth Five Year Plan depends on the elasticity of energy demand with respect to GDP, which has been falling over time and is currently around 0.80.

Allowing for some further decline in the elasticity, a GDP growth rate of 9.0 per cent per year over the Twelfth Plan will require energy supply to grow at around 6.5 per cent per year. The CAGR for the last 9 years for natural gas and oil production in India is 3.1 and 1.4 % respectively. This is a far cry from the 6.5 % growth required for 9 % GDP growth.

BP Statistical Review of World Energy 2013

Major gas trade movements 2012 Trade flows worldwide (billion cubic metres)

Oil and Gas Reserves in India

Natural Gas Oil

Proved

Reserves

(TCF)

% of

World

Reserves

R / P

(Years)

Proved

Reserves (

Billion

Barrels)

% of

World

Reserves

R / P

(Years)

47 (1.33TCM)

0.7 % 33.1 5.70 0.3 % 17.50

13

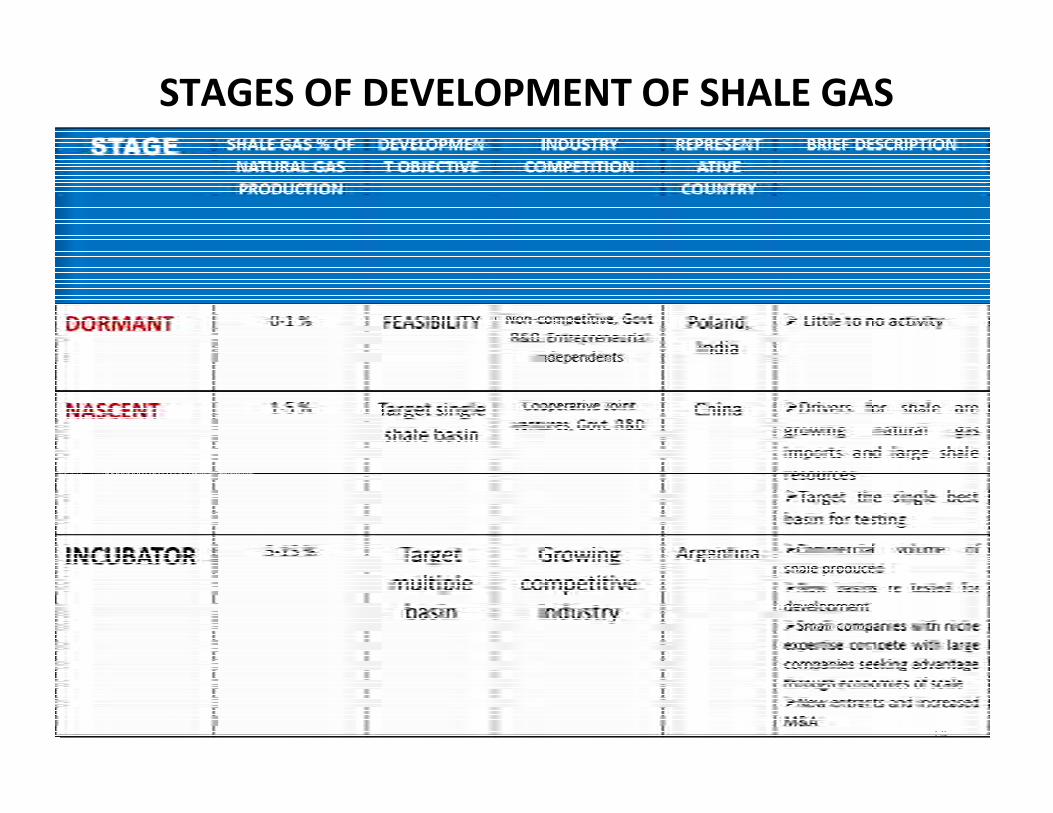

STAGES OF DEVELOPMENT OF SHALE GAS

14

STAGES OF DEVELOPMENT OF SHALE GAS

15

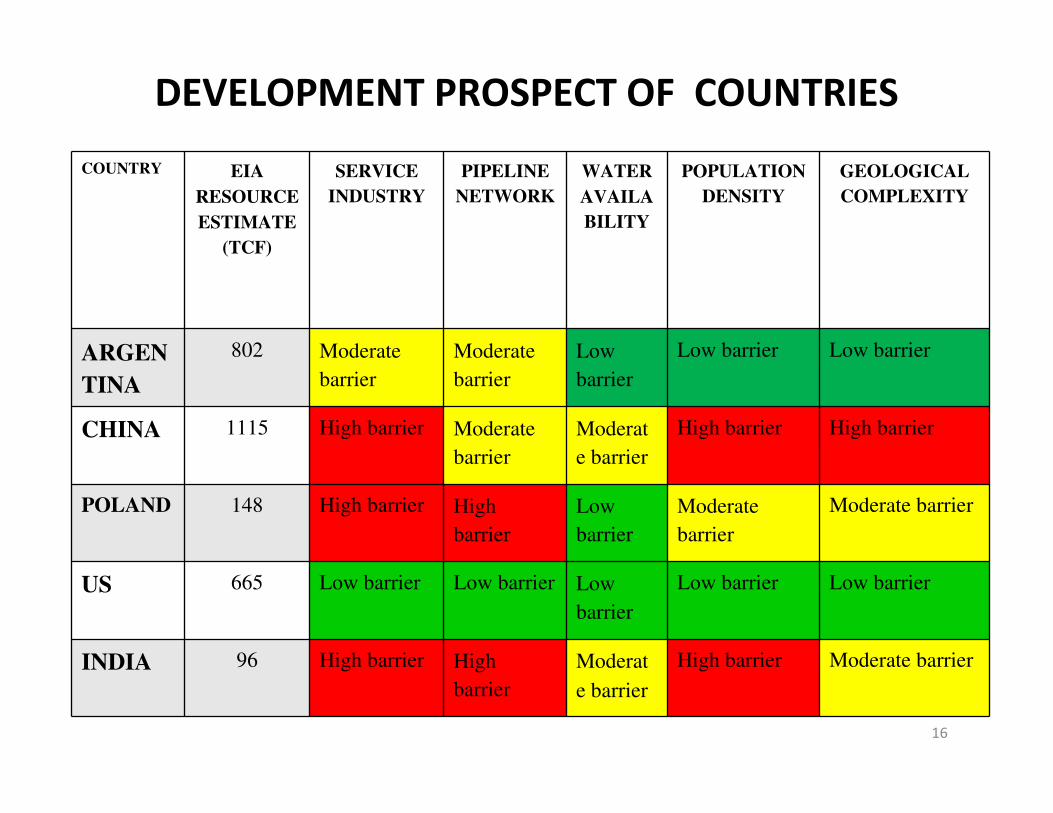

DEVELOPMENT PROSPECT OF COUNTRIES

16

COUNTRY EIA

RESOURCE

ESTIMATE

(TCF)

SERVICE

INDUSTRY

PIPELINE

NETWORK

WATER

AVAILA

BILITY

POPULATION

DENSITY

GEOLOGICAL

COMPLEXITY

ARGEN

TINA

802 Moderate

barrier

Moderate

barrier

Low

barrier

Low barrier Low barrier

CHINA 1115 High barrier Moderate

barrier

Moderat

e barrier

High barrier High barrier

POLAND 148 High barrier High

barrier

Low

barrier

Moderate

barrier

Moderate barrier

US 665 Low barrier Low barrier Low

barrier

Low barrier Low barrier

INDIA 96 High barrier High

barrier

Moderat

e barrier

High barrier Moderate barrier

17

Shale Gas Basins in India

Shale Gas Basins in India *

18

Basin Cambay Basin Damodar Valley

basin

Krishna-

Godavari Basin

Cauvery

Basin

Gross area

(miles2)

7,900 2,270 7,800 9,100

Shale

Formation

Cambay shale Barren measure Permian - Triassic Sattapadi-

Andimada

m

Geologic age Upper

cretaceous /

Tertiary

Permian –

Triassic

Permian –Triassic Cretacious

Physical Extent

Prospective

area (miles2)1940 1,080 8,000 1,010

Average Depth

(ft)

13,000 5,000 11,600 10,000

* EIA ,2013 Assessment

Shale Gas Basins in India

19

Basin Cambay

Basin

Damodar

Valley Basin

Krishna-

Godavari Basin

Cauvery

Basin

TOTAL

Reservoir Properties

Reservoir Pressure Moderately

over pressured

Slightly over

pressured

Normal Normal

Average Total Organic

Content (wt %)2.6 % 3.5 % 6 % 2.3 %

Thermal Maturity

(Ro%)1.6 1.2 1.5 1.15

Clay Content Low /Medium High High High

Resource

Gas In Place (Tcf)* 78 (146) 33 (27) 136 (381) 43 (30) 290 (584)

Technically

recoverable Gas

*(Tcf)

20 (30) 7 (5) 27 (57) 9 (5) 63 (96)

Technically recoverable

Oil * (Billion bbl)2.7 0.20 0.60 0.20 3.7

* EIA ,2011 Assessment, () EIA 2013 Assessment

Other Shale Gas Basins in India

20

1.Upper Assam Basin

2.Vindhyan Basin

3.South Rewa Basin

4.Pranhita- Godavari Basin

5.Rajasthan Basin

Data is not available for the rigorous assessment of reserves of these basins.

India’s Shale Gas Policy - 2013

21

�Delay in policy announcement

�ONGC and OIL given the right to drill for shale oil and gas in the blocks they

have, but fresh auction proposed for all other deposits. India’s first shale gas

well drilled and completed by ONGC, north west of Kolkata. ( depth 2000 m)

�Private sector not allowed to exploit blocks for shale oil and gas in the blocks

they have.

� It provides for auction based on simple production sharing between explorer

and government

�No need to treat shale gas different from conventional natural gas. Traditional

oil comes from drilling in porous and permeable rocks like sandstone and

limestone

�It is possible to have thick limestone / sandstone interspersed with shale

layers, all having oil and gas. To have 2 separate companies drill on sandstone

and shale layers does not make sense. It will lead to unnecessary litigation. US

makes no distinction between the two.

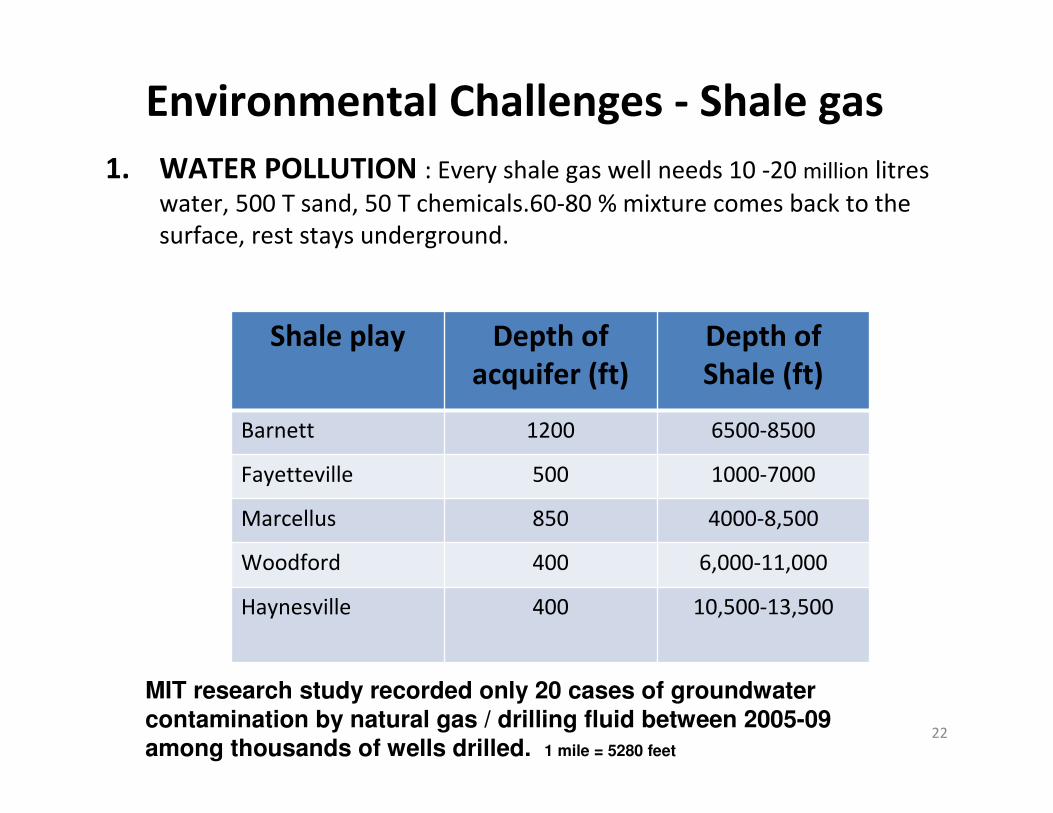

Environmental Challenges - Shale gas

1. WATER POLLUTION : Every shale gas well needs 10 -20 million litres

water, 500 T sand, 50 T chemicals.60-80 % mixture comes back to the

surface, rest stays underground.

22

Shale play Depth of

acquifer (ft)

Depth of

Shale (ft)

Barnett 1200 6500-8500

Fayetteville 500 1000-7000

Marcellus 850 4000-8,500

Woodford 400 6,000-11,000

Haynesville 400 10,500-13,500

MIT research study recorded only 20 cases of groundwater contamination by natural gas / drilling fluid between 2005-09 among thousands of wells drilled. 1 mile = 5280 feet

2. POISONING OF SUB-SOIL BY CHEMICALS

3. Release of methane – a potent greenhouse

gas( 25 times more polluting than CO2) to

atmosphere from shale gas wellsUniversity of Texas study indicated total methane escape is

1 million tons annually from shale gas operations.

However, containment measures captured 99 % of

methane that escaped. Even 3.4 % escape of methane

can change its climate change advantage over coal.

4. MINOR EARTHQUAKES

US HAD HAD OVER 1 MILLION HYDRAULIC

FRACTURING SINCE 1947 WITH FEW ACCIDENTS

Environmental Challenges - Shale gas

US – LEADER IN SHALE GAS

1. HUGE SHALE GAS / TIGHT OIL RESERVES

2. PRIVATE OWNERSHIP OF MINERAL RIGHTS

3. THOUSANDS OF INDEPENDENT OIL COMPANIES : George

P.Mitchell’s ‘Mitchell energy and Development’ was a pioneer,

17 years effort, $ 6 million –”best development money in the

field of gas”

4. HUGE AVAILABILITY OF DRILLING RIGS, OTHER EXPLORATION

AND PRODUCTION TOOLS- 65 % of oil rigs of the world are in US

and Canada. 18,000 DRILL RIGS WITH HORIZONTAL DRILLING

FACILITY .US DRILLS 10,000 SHALE WELLS DRILLED EVERY YEAR

5. ACTIVE FINANCIAL MARKET THAT SUPPLY MONEY FOR NEW

VENTURES

6. LESS POPULATION DENSITY

7. GOVT. SUPPORT IN TERMS OF TAX CREDITS : for drilling in

unconventional natural gas. CARTER’S 1980 LAW TO TAX

WINDFALL PROFITS AT OIL FIRMS ALSO INCLUDED TAX CREDITS

PROVISIONS.24

Ease of Doing Business Index-2013*

25

Economy

Ease of Doing

Business Rank

Starting a Business

Getting Electricity

Getting Credit

Protecting Investors

Paying Taxes

Trading Across Borders

Enforcing

Contracts

Singapore 1 4 5 12 2 5 1 12

Hong Kong 2 6 4 4 3 4 2 10

New Zealand 3 1 32 4 1 21 25 17

United States 4 13 19 4 6 69 22 6

Denmark 5 33 14 23 32 13 4 34

Norway 6 43 14 70 25 19 21 4

United Kingdom 7 19 62 1 10 16 14 21

Korea, Rep. 8 24 3 12 49 30 3 2

Georgia 9 7 50 4 19 33 38 30

Australia 10 2 36 4 70 48 44 15

Finland 11 49 21 40 70 23 6 9

Pakistan 107 98 171 70 32 162 85 155

Nepal 108 105 96 70 82 114 171 137

Bangladesh 129 95 185 83 25 97 119 182

India 132 173 105 23 49 152 127 184

*World Bank Data

26

27

28

POLAND – SHALE GAS EXPERIENCE

1. HUGE SHALE GAS / TIGHT OIL RESERVES, WANTED

TO BECOME SECOND NORWAY

2. DIFFICULT GEOLOGY

3. CUMBERSOME AND DELAYED REGULATION: TAKES

OVER 1 YEAR TO GET PERMITS FOR CHANGED

DRILLING PROGRAM, GOVT’S ENHANCED TAX

PROGRAM – 40 % OF OPERATOR’S PROFIT, ‘NOKE’ A

STATE OWNED COMPANY PROPOSED, TO TAKE

STAKES IN ALL FUTURE PRODUCTION CONCESSIONS

OUTCOME : 40 WELLS DRILLED , MAXIMUM IN EUROPE

WITHOUT ONE PRODUCING COMMERCIAL GAS, EXXON

MOBIL, TALISMAN, MARATHAN OIL QUIT THE COUNTRY29

Qatar’s North Field Vs Iran’s

South Pars Field

30

Qatar’s LNG Development

31

1.Qatar’s North Field discovered by Shell in 1971. Today its reserves are 900 TCF.

2.1970-80s, there was no market for the gas.3.Efficient and determined decision making after

1995 when the Sheikh Hamad became the new Emir saw the development of NF gas reserves.

4.Per capita GDP jumped from 16,238 in 1995 to $ 89,736 in 2011.( almost 6 times). LNG production capacity 77 MTPA.

5.Exxon Mobil technology, $ 60 billion investment6. Iran has not yet been able to export LNG from its

South Pars Field.

Conclusion

1.Shale gas and tight oil exploration and

development is the need of the hour. To start

with we should concentrate on one basin-

Cambay basin .

2. Environmental impact of shale gas

exploration and production is minimal and

manageable.

32

RECOMMENDATIONS

33

1.Development of unconventional gas

resources be given priority by giving it

tax credits, single window clearance.

2. Level playing field - private and public

sector – in policy matters.

3. Investment in upstream and mid stream

infrastructure –drill rigs pipelines –

national grid,

RECOMMENDATIONS

Country R&D Expenditure as a % of GDP

R&D Expenditure ($ Billions)

GDP (2011) ($ Billions)

R&D EXPENDITURE

PER CAPITA ($)

Israel 4.30% 10 243 1250.0Sweden 3.70% 20 539 2083.3

Japan 3.50% 205 5870 1614.2South Korea 3.40% 38 1116 760.0

United

States2.80% 420 14991 1329.1

Germany 2.70% 97 3604 1182.9

China 1.50% 108 7204 79.8

India 0.90% 17 1898 14.0

4. We must encourage innovation and R&D. “Oil and gas lie in the mind of men.

India Vs US- Global Innovation Index

35

12 Disruptive Technologies *

36* McKinsey Global Institute

37

Let me conclude by quoting Daniel Yergin from his famous book - The Quest: “…it is essential

that the conditions are nurtured so that creativity can flourish. For that resource –

creativity- will be critical for meeting the challenges and assuring the security and

sustainability of the energy for a prosperous, growing world. That is at the heart of the

quest; it is as much about the human spirit as it is about technology, and that is why this is

a quest that will never end”.

So let me urge you all to be on the trail of that endless ‘Quest’ for knowledge whereby we would be

skilled enough to put together all the pieces of the large jigsaw puzzle of energy security, and take

the country forward in its quest for prosperity.

Oil is found in the minds of men.

References

1. XII PLAN DOCUMENT, PLANNING

COMMISSION

2. BP Statistical Review of World Energy, June

2013

3. Maugeri, Leonardo. "Oil: The Next

Revolution." Discussion Paper ,June 2012

4. Yergin, Daniel “The Quest”

5. Teri – “Shale Gas in India: Look Before You

Leap”38

References

6. Deloitte – Oil & Gas Reality Check 2013

7. U.S. Energy Information Administration (EIA)

report- Technically Recoverable Shale Oil

and Shale Gas Resources: An Assessment of

137 Shale Formations in 41 Countries

Outside the United States- 2013

39

Thank You

40

Economic Impact of Disruptive

Technologies

41

BP Statistical Review of World Energy 2013

© BP 2013

Primary Energy Regional Consumption pattern 2012Percentage

WORLD SHALE GAS MAP – EIA 2011 Study

43