Refer to important disclosures at the end of this report

BUYBUYBUYBUY RMRMRMRM2.182.182.182.18 KLCIKLCIKLCIKLCI : : : : 1,795.81,795.81,795.81,795.85555

(Upgrade from HOLD)

Price Target :Price Target :Price Target :Price Target : 12-Month RM 2.60 (Prev RM 2.60)

Shariah Compliant:Shariah Compliant:Shariah Compliant:Shariah Compliant: No

Reason for Report :Reason for Report :Reason for Report :Reason for Report : Earnings revision and rating upgrade

Potential Catalyst: Potential Catalyst: Potential Catalyst: Potential Catalyst: Recovery in yields, cheaper fuel costs, further

milestone in the leasing house

AllianceDBSAllianceDBSAllianceDBSAllianceDBS vs vs vs vs Consensus:Consensus:Consensus:Consensus: Below consensus for FY16/17F Analyst TAN Kee Hoong +603 2604 3913 [email protected]

Price Relative

Forecasts and Valuation FY FY FY FY DecDecDecDec ((((RMRMRMRM m) m) m) m) 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF

Revenue 5,416 5,674 5,869 6,124 EBITDA 1,573 2,078 2,132 2,274 Pre-tax Profit 23 286 863 909 Net Profit 83 256 835 884 Net Pft (Pre Ex.) 416 854 835 884 EPS (sen) 15.0 30.7 30.0 31.8 EPS Pre Ex. (sen) 15.0 30.7 30.0 31.8 EPS Gth (%) (29) 105 (2) 6 EPS Gth Pre Ex (%) (29) 105 (2) 6 Diluted EPS (sen) 3.0 9.2 30.0 31.8 Net DPS (sen) 0.6 1.8 6.0 6.4 BV Per Share (sen) 163.9 172.5 200.6 226.4 PE (X) 14.6 7.1 7.3 6.9 PE Pre Ex. (X) 14.6 7.1 7.3 6.9 P/Cash Flow (X) 31.0 4.8 4.0 3.6 EV/EBITDA (X) 10.9 8.4 8.2 8.0 Net Div Yield (%) 0.3 0.8 2.8 2.9 P/Book Value (X) 1.3 1.3 1.1 1.0 Net Debt/Equity (X) 2.4 2.4 2.1 1.9 ROAE (%) 1.7 5.5 16.1 14.9 Earnings Rev (%):Earnings Rev (%):Earnings Rev (%):Earnings Rev (%): (10) (22) (29) Consensus EPS Consensus EPS Consensus EPS Consensus EPS (sensensensen):::: 30.7 34.6 36.3 Other Broker Recs:Other Broker Recs:Other Broker Recs:Other Broker Recs: B: 18 S: 1 H: 7

ICB IndustryICB IndustryICB IndustryICB Industry : Consumer Services ICB Sector: ICB Sector: ICB Sector: ICB Sector: Travel & Leisure Principal Business:Principal Business:Principal Business:Principal Business: Low cost carrier

Source of all data: Company, AllianceDBS, Bloomberg Finance L.P.

At A Glance Issued Capital (m shrs) 2,783 Mkt. Cap (RMm/US$m) 6,067 / 1,635 Major Shareholders Tune Air (%) 19.0 Wellington Management LLP (%) 14.0 Employees Provident Fund (%) 7.4 Free Float (%) 59.6 Avg. Daily Vol.(‘000) 11,445

Malaysia Equity Research

24 Mar 2015

Company Focus

AirAsia Bloomberg: AIRA MK | Reuters: AIRA.KL Refer to important disclosures at the end of this report

A beating unduly severe • Recent share price correction overdone

• Expect fuel cost savings to be more apparent in FY15F, given the lower average hedged costs

• Monetisation of non-core assets underway

• Upgrade to BUY, RM2.60 TP (35% discount to SOP)

Share price correction too steep. AirAsia's share price has fallen by 26% from the peak in Dec 2014, due to the QZ8501 accident, stronger USD, and the launch of flymojo. While these concerns are valid, we think the market may have overly punished the stock, as its valuation remains decent at 7.1x FY15F PE.

Fuel cost savings to be more apparent in FY15F. Investors were generally disappointed with AirAsia’s 4Q14 results, as fuel cost savings were not apparent in the quarter (-4% y-o-y). But this was due to: (1) previous fuel hedges that were made at higher price (USD115/bbl), and (2) the stronger USD. We expect fuel cost savings to be more apparent starting 1Q15, given the cheaper average hedged cost of USD98/bbl. This is expected to further fall to USD88/84/84 per bbl in 2Q/3Q/4Q. We believe investors will re-focus on this theme, once they begun to see the earnings impact from the cheap fuel in 1Q15.

Cashing out non-core assets. The recent divestment of a 25% stake in AAE Travel was a pleasant surprise, as the USD86.25m price tag beat market expectations. Next, the group plans to sell a stake in its leasing arm (AAC) to strategic investors, in order to realise the value from its fleet of aircraft. We think AAC could fetch a valuation of USD300m, assuming only 45 aircraft are injected into it.

Upgrade to BUY, RM2.60 TP. Our TP is derived by applying a 35% discount to our SOP value. There are concerns that IAA's woes may be a drag on the group, but we think the current share price has provided a sufficient margin of safety, as our TP implies a complete write-off of IAA’s related assets (receivables due, equity, etc).

62

82

102

122

142

162

182

202

222

2.0

2.5

3.0

3.5

4.0

4.5

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

Relative IndexRM

AirAsia (LHS) Relative KLCI INDEX (RHS)

Page 2

Company Focus

AirAsia

INVESTMENT THESIS

Profile Rationale

AirAsia is a low-cost airline flying short-haul, point-to-point

domestic and international routes. AirAsia operates from

hubs in Malaysia, Thailand, Indonesia and Philippines.

Share price correction overdoneShare price correction overdoneShare price correction overdoneShare price correction overdone

• Share price has corrected substantially due to the QZ8501

accident, stronger USD and the launch of flymojo. But, we

think this is overdone, as its valuation remains decent

even as we impute a weaker RM into our earnings

forecasts.

Unit costUnit costUnit costUnit cost to ease on cheaper oil prices to ease on cheaper oil prices to ease on cheaper oil prices to ease on cheaper oil prices

• We expect AirAsia’s unit cost to fall in the coming

quarters, following the substantial decline in jet fuel price

to USD65/bbl. While fuel cost savings will be fettered by

intense competition (which lead airlines to pass on the

savings) and stronger USD, we think the net impact would

still be positive for AirAsia. Our earnings forecasts are

conservative as it implies 86% of the cost savings will be

passed on to the consumers.

Harvesting its portfolio of nonHarvesting its portfolio of nonHarvesting its portfolio of nonHarvesting its portfolio of non----core ascore ascore ascore assetssetssetssets

• The recent divestment of a 25% stake in AAE Travel at

USD86.25m was a pleasant surprise to the market, given

the hefty valuation. Next, the group plans to monetise its

aircraft fleet by setting up a leasing house, and disposing

a stake in it to strategic investors. We think the leasing

house could fetch a valuation of USD300m.

IAA woes adequately accounted for at current share priceIAA woes adequately accounted for at current share priceIAA woes adequately accounted for at current share priceIAA woes adequately accounted for at current share price

• IAA’s turnaround efforts could be hampered by the recent

QZ8501 accident. This could put further pressure on the

group’s balance sheet, as it may require further working

capital support, if the turnaround fails to materialise.

However, we think the current share price has adequately

priced in this risk.

Valuation Risks

Our RM2.60 TP is derived by applying a 35% discount to our

SOP valuation, mainly to reflect the operating challenges

surrounding IAA. We think the SOP discount is sufficient to

withstand a full write-off of the amounts due from related

parties (i.e. associates and JV), IAA’s equity value, and 32%

impairment of aircraft leasing business (24 aircraft from the

75-aircraft fleet are deployed for IAA).

Further depreciaFurther depreciaFurther depreciaFurther depreciattttion in RM against USDion in RM against USDion in RM against USDion in RM against USD

• A stronger USD will pressure AirAsia’s profitability as

c.57% of its cost base is in USD. Debt repayments will

also be a concern as most of its borrowings are in USD.

Irrational competition Irrational competition Irrational competition Irrational competition

• Irrational competition could persist if MAS decides to

change track, and refocus on market share gains. If so,

yield compression will continue to plague the industry.

Source: AllianceDBS

Page 3

Company Focus

AirAsia

AirAsia’s share price declined mainly due to a stronger

USD; but the launch of flymojo exacerbated the

situation

1) 1) 1) 1) Share price Share price Share price Share price has has has has corrected by corrected by corrected by corrected by 26262626% since the peak in Dec % since the peak in Dec % since the peak in Dec % since the peak in Dec

2014201420142014

AirAsia’s share price has fallen by 26% from its recent peak

on 26 Dec 2014, as investors have been concerned about the

potential impact from the QZ8501 incident, the stronger USD

and the announcement of a new airline entering the crowded

Malaysian market (i.e. flymojo). Conversations with

institutional investors suggest that the stronger USD and the

launch of flymojo were the bigger concerns for them, and

were the key factors behind the recent decline in AirAsia’s

share price.

We had previously warned of the negative impacts from a

stronger USD (i.e. higher OPEX, higher borrowing costs, and

translation losses), and downgraded our rating on the stock

to HOLD (from BUY) in our report titled “AirAsia – Forex

headache” that was published on 29 Dec 2014. However, we

think the recent share price correction has excessively priced

in this risk.

AirAsia: Share price has corrected by c.26% due to the QZ8501 incident, stronger USD and flymojo

Sources: Bloomberg Finance L.P.

2) 2) 2) 2) Cut earnings on revised forex assumptions; but Cut earnings on revised forex assumptions; but Cut earnings on revised forex assumptions; but Cut earnings on revised forex assumptions; but current current current current

valuation remains decentvaluation remains decentvaluation remains decentvaluation remains decent as share price has corrected as share price has corrected as share price has corrected as share price has corrected

substantiallysubstantiallysubstantiallysubstantially

We are revising our forex assumptions to RM3.69/3.75/3.75

per USD in FY15/16/17F (previous: RM3.41/3.41/3.41 per

USD), to bring it in line with the revised forex forecasts

provided by the DBS economics team. As a result, we cut our

FY15/16/17F core earnings by 10%/22%/29%. We also

imputed a RM597.3m translation loss on its USD-

denominated borrowings in FY15F, which we think will

chiefly be recognised in 1Q15. For a more detailed discussion

on the earnings revision, please refer to the “Financial

Forecasts” section in the subsequent pages of our report.

However, AirAsia’s valuations remain decent even after the

earnings cut. Current share price implies 7.1x FY15F P/E, 1.3x

F1Y5F P/BV and 8.6x FY15F adjusted EV/EBITDAR; all of these

multiples are close to -1 standard deviation to the stock’s 5-

year average valuation. We think this is unjustified as the

group’s earnings momentum is at the cusp of an inflection

point, buoyed by: (1) MAS’s restructuring, (2) cheaper oil

prices, and (3) the potential recovery of its key associates (i.e.

TAA and IAA).

Also, the group’s solvency and liquidity is not yet a concern

for us, as our forecasts suggest that interest coverage and

gearing ratio would remain healthy at 2.4x-2.7x and 1.8x-

2.4x respectively in FY15-17F. These have already taken into

account the impact of the stronger USD on the group’s

finance cost and borrowings.

AirAsia: Liquidity and gearing ratios expected to remain manageable in FY15-17F

Sources: AirAsia, AllianceDBS

A new entrant to the crowded Malaysian aviation

sector - flymojo

1) Announcement of new airline during LIMA exhibition 1) Announcement of new airline during LIMA exhibition 1) Announcement of new airline during LIMA exhibition 1) Announcement of new airline during LIMA exhibition

surprisesurprisesurprisesurprisessss investment communityinvestment communityinvestment communityinvestment community

Fly Mojo Sdn Bhd (Fly Mojo) announced the setting-up of a

new airline dubbed “flymojo” during the Langkawi

International Maritime and Aerospace (LIMA) exhibition on 17

Mar 2015. In conjunction with that, it also signed a letter of

intent with Bombardier Commercial Aircraft to acquire 20

CS100 aircraft which comes together with an option for

another 20 more.

Investors were understandably concerned on this latest

development. The launch of a new airline could increase the

competition risks in the crowded Malaysian aviation sector,

which has seen two years of yield compression in 2013-14.

Reflecting this risk, AirAsia’s share price has fallen by 5%

since the announcement of flymojo.

2.00

2.10

2.20

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

Jan

-14

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct

-14

Oct

-14

No

v-1

4

De

c-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Fe

b-1

5

Ma

r-1

5

RM

AirAsia's Share Price

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015F 2016F 2017F

x

Net Gearing Interest Coverage Ratio

Page 4

Company Focus

AirAsia

2) 2) 2) 2) Details of the new airline Details of the new airline Details of the new airline Details of the new airline

Flymojo will operate out of Senai International Airport, Johor

as its primary hub with Kota Kinabalu International Airport

(BKI) as its secondary hub. The airline is reportedly targeting

to operate domestic and regional flights (i.e. ASEAN). Media

reports suggest that flymojo will be a hybrid carrier (akin to

Malindo).

It is unclear whether Fly Mojo has the necessary regulatory

approval to operate an airline in Malaysia. FlightGlobal

reported that the airline has already obtained its air operator’s

certificate (AOC), but certain industry sources suggest the

new airline could not have obtained the AOC without any

aircraft on hand.

Also, media reports indicate that Fly Mojo is fully Malaysian-

owned, with 81% of the shares being held by Azharuddin

Satyapal Das Abdullah. The other shareholders are Ismail Hue

Kor Ming (10%), and Janardhanan Gopala Krishnan (9%).The

company is currently helmed by its managing director, Datuk

Janardhanan Gopala Krishan. Datuk Seri Alies Anor Abdul is

the chairman of the airline.

3) 3) 3) 3) Regulatory challenges and financial support should not be Regulatory challenges and financial support should not be Regulatory challenges and financial support should not be Regulatory challenges and financial support should not be

an issue, considering the political supportan issue, considering the political supportan issue, considering the political supportan issue, considering the political support

It would seem that Fly Mojo has strong political support and

backing, going by the various government officials (Prime

Minister, Datuk Seri Najib Razak amongst many others) who

graced the launching ceremony of flymojo. In addition,

government officials from both Malaysia and Canada had

made encouraging comments about the airline. As such, we

do not think the company will encounter much difficulty in

securing the necessary regulatory approvals and financial

backing to begin operations in Oct 2015.

Various government dignitaries were present during the launch of flymojo

Left to right: (1) flymojo MD, Datuk Janardhanan Gopala Krishnan; (2) VP, Sales, China and Asia-Pacific, Bombardier Commercial Aircraft, Andy Solem; (3) Canada’s High Commissioner to Malaysia, Her Excellency Judith St. George; (4) Minister of Transport, Datuk Seri Liow Tiong Lai; (5) Prime Minister of Malaysia, Datuk Seri Najib Razak; (6) flymojo Chairman, Datuk Seri Alies Anor Abdul; (7) Chief Minister of Kedah, Datuk Seri Mukhriz Mahathir; (8) Deputy Minister of Transport, Datuk Aziz Kaprawi; and (9) Regional Vice President, Sales, Asia-Pacific, Frank Baistrocchi.

Sources: New Straits Times

Page 5

Company Focus

AirAsia

4) 4) 4) 4) Flymojo could lead to Flymojo could lead to Flymojo could lead to Flymojo could lead to heightened competitiheightened competitiheightened competitiheightened competitive risksve risksve risksve risks at BKat BKat BKat BKIIII; ; ; ;

a negative for AirAsiaa negative for AirAsiaa negative for AirAsiaa negative for AirAsia

While flymojo’s business model is yet uproven amid limited

operational details and history, we think the entry of flymojo

would be negative for established domestic airlines such as

AirAsia and Malaysian Airlines (MAS), due the already

crowded market. Including flymojo, we estimate that there

would be a total of seven airlines plying the domestic routes

in Malaysia.

Flymojo’s plan to locate its secondary hub at BKI would also

give rise to increase competitive pressure there, which is the

second largest hub for AirAsia. We are concerned that

flymojo would initially offers rock bottom fares, in order to

garner the requisite critical mass and market share.

AirAsia: Top 10 hubs in Malaysia

Sources: CAPA

5) The use of CS100 would afford flymojo an advantage in 5) The use of CS100 would afford flymojo an advantage in 5) The use of CS100 would afford flymojo an advantage in 5) The use of CS100 would afford flymojo an advantage in

routes with lower demand; but routes with lower demand; but routes with lower demand; but routes with lower demand; but is is is is unlikely to be threat to unlikely to be threat to unlikely to be threat to unlikely to be threat to

AirAsia until it has the requisite scale AirAsia until it has the requisite scale AirAsia until it has the requisite scale AirAsia until it has the requisite scale

According to a study published by AirInsight, a commercial

aviation consultancy, the Bombardieer CS100 (which is the

planned workhorse of flymojo) is competitive vs Airbus 320

(A320), which is the mainstay of AirAsia’s current fleet.

Despite CS100’s lower seat density, its cost per seat mile is

said to be slightly lower (or at least comparable) to the

A320’s.

Having a comparable cost per seat mile, despite the lower

seat density would enable the aircraft to have a lower cost

per flight (in absolute terms). As such, this will allow the

aircraft to operate sustainably at a lower critical mass. This

confers a competitive edge to flymojo in operating the less

popular point-to-point routes. It is this type of routes, where

we think flymojo will be able to give AirAsia a run for its

money.

Aircraft mile and seat-mile cost comparison

Sources: AirInsight

Low fuel prices remain a boon for AirAsia on a net basis

1) 1) 1) 1) Fuel cFuel cFuel cFuel cost savings fettered byost savings fettered byost savings fettered byost savings fettered by intense competition and intense competition and intense competition and intense competition and

stronger USD; but market completely ignores any potential stronger USD; but market completely ignores any potential stronger USD; but market completely ignores any potential stronger USD; but market completely ignores any potential

benefitsbenefitsbenefitsbenefits

We had previously warned that cost savings for AirAsia from

cheaper fuel prices would be fettered by: (1) intense

competition; and (2) stronger USD. The intense competition

within the aviation sector would lead airlines to pass on the

cost savings to consumers via lower fares (i.e. removal of fuel

surcharge), while the stronger USD would make jet fuel more

expensive in RM terms.

However, our warnings came at a time when AirAsia was

trading at RM2.70-2.90 per share. It was meant to caution

investors against bidding up the share price too high, as we

believed the consensus had overestimated the earnings

impact from the cheaper fuel prices (after adjusting for lower

yield and stronger USD). But its share price has since retraced

to the previous levels, and is now completely ignoring the

potential boon from the cheap fuel.

AirAsia: Share price has retraced to previous levels

Sources: Bloomberg Finance L.P.

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

3.60

Jan

-13

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

Jun

-13

Jul-

13

Au

g-1

3

Se

p-1

3

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct

-14

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

RM

AirAsia's share price

Share price rally from Jun 2014 to Dec 2014 completely wiped off in the first two months of 2015, despite fuel prices remain cheap and MYR only weakened by 8% from year end close

Page 6

Company Focus

AirAsia

2) 2) 2) 2) Fuel cost savings not apparent in 4Q14 due to previous Fuel cost savings not apparent in 4Q14 due to previous Fuel cost savings not apparent in 4Q14 due to previous Fuel cost savings not apparent in 4Q14 due to previous

hedges; but cost savings is expected to be more apparent in hedges; but cost savings is expected to be more apparent in hedges; but cost savings is expected to be more apparent in hedges; but cost savings is expected to be more apparent in

FY15FFY15FFY15FFY15F

At present, we think investors have downplayed the potential

boon from cheaper fuel prices, as the fuel cost savings were

not apparent in 4Q14 (fuel cost fell by only 4% y-o-y to

RM620.9m). Fuel cost/ASK stood at 6.7 sen in 4Q14 (-16% y-

o-y; +10% q-o-q), despite jet fuel prices falling by 26% y-o-y

and 21% q-o-q in the quarter. This was mainly due to: (1)

50% of the fuel requirements in 4Q had been hedged at a

higher price, and (2) strengthening of USD had made fuel

cost more expensive in RM terms

Jet fuel prices have fallen by 48% since the recent peak on 20 Jun 2014

Sources: Bloomberg Finance L.P.

We expect the fuel cost savings to be more apparent starting

1Q15, given the cheaper average hedged cost of USD98/bbl.

This is expected to further fall to USD88/84/84 per bbl in

2Q/3Q/4Q. Average hedged cost for 2015 currently stands at

USD88/bbl (vs USD115/bbl in 4Q14). We expect the fuel cost

savings to be a key earnings driver in FY15F, and investors

would once again pay attention to this theme after the 1Q15

results.

AirAsia: Group hedging profile

Sources: AirAsia

3) Our FY15F earnings forecast implies 86% of the fuel cost 3) Our FY15F earnings forecast implies 86% of the fuel cost 3) Our FY15F earnings forecast implies 86% of the fuel cost 3) Our FY15F earnings forecast implies 86% of the fuel cost

savings savings savings savings would be passed on to consumerswould be passed on to consumerswould be passed on to consumerswould be passed on to consumers

Our earnings forecasts currently assume jet fuel cost per

barrel of USD96/107/107 in FY15/16/17F respectively.

Additionally, we assume that fare/RPK will decline by 6.9% in

FY15F (removal of fuel surcharge, but raise base fare/RPK by

14%), increase by 5% in FY16F, and remain flattish in FY17F.

These assumptions imply AirAsia would pass on 86% of the

fuel cost savings to consumers, a scenario which we think is

likely to take place, given the intense competition and the

need to stimulate demand in the face of a potential

slowdown in private consumption. Our earnings forecasts

also imply MAA’s FY15/16/17F unit profitability will remain

below FY12F levels, which is prudent considering the

competitive landscape within the domestic aviation sector.

MAA: Jet fuel cost assumptions FY15F FY16F FY17F Remarks Hedged ratio 50% 0% 0% Hedged price (USD/bbl)

88.00 N/A N/A

Spot ratio 50% 100% 100% Spot price (USD/bbl)

85.00 97.00 97.00 Assume USD15 crack spread to Brent

USD / bblUSD / bblUSD / bblUSD / bbl Jet Fuel Price 86.50 97.00 97.00 (+) D-Factor 9.72 9.72 9.72 Based on FY14 Jet Fuel Cost 96.22 106.72 106.72

* DBS’ Brent price forecasts is USD70/82/82 per bbl for FY15/16/17F

Sources: AirAsia, AllianceDBS

MAA: Implied unit profitability for FY15-17F remains below FY12 levels; this suggest our forecasts remain conservative

Sources: AirAsia, AllianceDBS

Investments in non-core businesses ripe for harvesting

1) 1) 1) 1) DDDDivestment of 25% stake in AAE ivestment of 25% stake in AAE ivestment of 25% stake in AAE ivestment of 25% stake in AAE Travel Travel Travel Travel suggest there may suggest there may suggest there may suggest there may

be other hidden gems within the group’s balance sheetbe other hidden gems within the group’s balance sheetbe other hidden gems within the group’s balance sheetbe other hidden gems within the group’s balance sheet

AirAsia has recently completed the divestment of a 25%

stake in AAE Travel Pte. Ltd. (AAE) to its JV-partner, Expedia

Inc. group for USD86.25m. Post-divestment, AirAsia would

have a remaining stake of 25% in AAE. To recap, AAE was

originally set up as 50:50 JV between AirAsia and Expedia Inc.

in 2011, to operate an online travel agent based in

Singapore. The unit sells both hotel accommodation and

50

60

70

80

90

100

110

120

130

140

150

Jul-

11

Se

p-1

1

No

v-1

1

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-

12

Se

p-1

2

No

v-1

2

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-

13

Se

p-1

3

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Se

p-1

4

No

v-1

4

Jan

-15

USD/bbl

Singapore Jet Kerosene

3.39

1.49

1.96

1.57

1.19

1.73 1.74 1.89

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2010A 2011A 2012A 2013A 2014A 2015F 2016F 2017F

sen/RPK

Unit Profitability - Malaysia AirAsia excluding leasing operations

Page 7

Company Focus

AirAsia

flights across the ASEAN region, which provides AirAsia with

an additional distribution channel and access to a wider

market.

AAE Travel: Net profit trends

Sources: AirAsia, AllianceDBS

The divestment which was first announced on 17 Feb 2015,

came as a surprise to the investment community. While

management had always reiterated that it was looking to exit

its non-airline businesses, most were not expecting the

group’s stake in AAE (i.e. 50%) to be valued at above

RM500m. As such, the transaction has led investors to realise

that there could be more hidden gems among the group’s

portfolio of non-airline businesses.

2) 2) 2) 2) To monetise its nonTo monetise its nonTo monetise its nonTo monetise its non----Malaysian fleet Malaysian fleet Malaysian fleet Malaysian fleet bybybyby setting up a leasing setting up a leasing setting up a leasing setting up a leasing

househousehousehouse

Also, AirAsia is planning to monetise its large fleet of aircraft

via the setting up of a leasing house, named Asia Aviation

Capital Ltd (AAC). Already, the Labuan-based subsidiary has

obtained the regulatory approvals to carry out the leasing

business, and is set to take delivery of 45 aircraft by 1H15.

The leasing house will only manage aircraft that are on lease

to the group’s associates (i.e. non-Malaysian fleet).

We expect AirAsia to have a 75 aircraft on lease to its

associates by end-FY15F, but not all of these could be

injected into the leasing house in the near term. The situation

in Indonesia AirAsia (IAA) remains challenging, as the recent

QZ8501 incident has thrown a spanner to restructuring

efforts. It remains cash-strapped and is not likely to be able to

make good on the lease payments due. Thus, it would be

difficult to secure third party investors in the leasing house, if

IAA’s aircraft are injected into AAC.

AirAsia: Aircraft on lease to associates

Sources: AirAsia, AllianceDBS

According to management, its first priority with regards to

AAC is to secure a strategic investor to take up a stake in the

former. An Initial Public Offering (IPO) will only take place at a

later stage, presumably after all the non-Malaysian fleet of

aircraft have been novated to AAC. We do not expect this to

take place within the near term.

Based on management guidance that AAC could generate a

USD30m net income in FY15F, we think the unit could easily

fetch a valuation of USD300m (i.e. RM1.1bn), based on 10x

FY15F PE. This is in line with the average P/E valuation of

aircraft lessors listed in the US. As such, the sale of a 50%

stake in the AAC could easily raise c.RM550m for the group.

Valuation of listed aircraft leasing companies

Sources: Bloomberg Finance L.P.

-24.0

16.2 16.2 17.8

19.6 21.6

(30)

(20)

(10)

0

10

20

30

2012A 2013A 2014A 2015F 2016F 2017F

RM m

AAE Travel - Net Profit

-

10

20

30

40

50

60

70

80

90

100

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015F 2016F 2017F

# of aircrafts

B737s on lease to associates A320s on lease to associates

Company Country Call

Target

Price

Current

Price

Market

Cap

(LC) (LC) (USD m) CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16

China Aircraft

Leasing

Hong Kong NR NR 9.83 742 37 35 13.2 9.8 2.6 2.4 24.2 26.8 2.2 3.1 29.6 19.1

Aercap Holdings US NR NR 44.41 9,429 7 5 8.5 8.1 1.1 1.0 11.8 11.9 0.0 0.0 8.6 8.6

Air Lease US NR NR 38.85 3,984 16 18 14.0 11.9 1.3 1.2 11.0 11.8 0.4 0.5 10.4 9.5

Aircastle US NR NR 23.30 1,886 -3 11 11.7 10.5 1.0 1.0 8.3 9.2 3.8 3.9 8.1 7.9

Fly Leasing US NR NR 14.94 619 3 21 10.6 8.8 0.7 0.7 8.2 10.5 7.0 7.5 8.0 8.1

Sector Average 10 11 10.5 9.4 1.2 1.1 11.6 12.2 0.9 1.0 9.9 9.2

* Estimates based on Bloomberg consensus

EPS Growth P/E (x) P/BV (x) ROE (%)

Dividend Yield

(%) EV/EBITDA (x)

Page 8

Company Focus

AirAsia

IAA to remain a drag on the group; but a necessary

investment for AirAsia to be a pan-ASEAN airline

1) 1) 1) 1) Reasons behind IAA’s weak performance in FY13Reasons behind IAA’s weak performance in FY13Reasons behind IAA’s weak performance in FY13Reasons behind IAA’s weak performance in FY13----14141414

Indonesia AirAsia reported a loss in FY13-14, due to the

weakness in IDR, which had depreciated rapidly by 27% in

2013-14. This proved to be a challenge for IAA as the

majority of its revenue is denominated in IDR while a

significant portion of its OPEX (i.e. fuel, lease, maintenance) is

USD-denominated.

IDR has depreciated by 27% in 2013-14

Sources: Bloomberg Finance L.P.

Making matters worse, fares for the domestic routes are

regulated by the Indonesian aviation authorities. There is a

price ceiling for every domestic route and different classes of

airlines can charge different levels of maximum fares. Full-

service airlines can charge up to 100% of the price ceiling,

while medium-service airlines can charge up to 90% and no-

frills airlines, 85%.

In light of the rigid pricing regulations, IAA was unable

initially to raise fares sufficiently to offset the higher OPEX, at

a time when IDR was depreciating rapidly. While the price

ceiling was subsequently lifted, intense competition in the

domestic routes continues to be a dampener on fares.

How Indonesian regulators classify the different airlines

Full ServiceFull ServiceFull ServiceFull Service Medium ServiceMedium ServiceMedium ServiceMedium Service No FrillsNo FrillsNo FrillsNo Frills

Services and optional requirements covered by the fares (maximum service)

Some services covered by the fares (Iimited services)

Only essential services covered by the fares

Provide free baggage (30kg for international, 20kg for domestic)

Limited free baggage

Baggage fee implemented

Provide full inflight service

Provide limited inflight service

Inflight service is available on charged basis

Sources: CAPA, Indonesia DGCA

2) 2) 2) 2) TurnaroundTurnaroundTurnaroundTurnaround efforts proved fruitful in 2H14; should have efforts proved fruitful in 2H14; should have efforts proved fruitful in 2H14; should have efforts proved fruitful in 2H14; should have

been on track to breakbeen on track to breakbeen on track to breakbeen on track to break even in FY15F, but QZ8501 even in FY15F, but QZ8501 even in FY15F, but QZ8501 even in FY15F, but QZ8501 accidentaccidentaccidentaccident

could be stumbling blockcould be stumbling blockcould be stumbling blockcould be stumbling block

Given the challenging operating environment in Indonesian

domestic routes, IAA has decided to reduce capacity in the

domestic segment, and focus on its core international

segment. It terminated nine routes and reduced frequencies

in another six routes in 1H14. While IAA did not manage to

turn profitable as per management’s target for 2H14, we

view the network rationalisation strategy as being effective,

given the significant reduction in 2H net loss (-86% y-o-y; -

92% h-o-h).

However, the QZ8501 accident could prove to be a stumbling

block to IAA’s turnaround efforts. Promotional and marketing

activities were put on hold following the crash, out of

concern for the sensitivities of the victims’ families. We are

wary that this could have a negative impact on demand, and

thus affect yields and load factors in 1H15.

IAA: Originally on track to turn around in FY15F; but this could be disrupted by QZ8501 incident

Sources: AirAsia

However, we remain hopeful that the QZ8501 accident will

have no lasting harm on the group’s branding and goodwill.

Anecdotal evidence suggests the group CEO, Tan Sri Tony

Fernandes had done a wonderful job in handling the QZ8501

crisis. He took personal responsibility for the situation, made a

public apology to the victims’ families. He ensured that they

were well-informed of the situation on the ground and were

well taken care of. This has won AirAsia and IAA much

goodwill among the Indonesian citizens.

8,000

9,000

10,000

11,000

12,000

13,000

14,000

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-

12

Se

p-1

2

No

v-1

2

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-

13

Se

p-1

3

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

IDR/USD

Indonesia Rupiah

(500)

(400)

(300)

(200)

(100)

0

100

200

1Q

FY

10

2Q

FY

10

3Q

FY

10

4Q

FY

10

1Q

FY

11

2Q

FY

11

3Q

FY

11

4Q

FY

11

1Q

FY

12

2Q

FY

12

3Q

FY

12

4Q

FY

12

1Q

FY

13

2Q

FY

13

3Q

FY

13

4Q

FY

13

1Q

FY

14

2Q

FY

14

3Q

FY

14

4Q

FY

14

IDR bn

Net Profit - IAA

Page 9

Company Focus

AirAsia

3333) ) ) ) Delays in IAA’s turnaround could put further stress on Delays in IAA’s turnaround could put further stress on Delays in IAA’s turnaround could put further stress on Delays in IAA’s turnaround could put further stress on

AirAsia’s balance sheet; but we think this will not be too AirAsia’s balance sheet; but we think this will not be too AirAsia’s balance sheet; but we think this will not be too AirAsia’s balance sheet; but we think this will not be too

much of a problemmuch of a problemmuch of a problemmuch of a problem

AirAsia has seen the amount due from related parties (i.e.

associates and JV) surge from RM921m in 3Q13 to RM2.4bn

in 4Q14, mainly due to IAA. Faced with the difficult operating

environment in Indonesia, IAA was forced to defer payments

to AirAsia, and the latter had to step in to provide working

capital funding to the former.

AirAsia: Amounts due from related parties have surged since 3Q13, mainly due to IAA

Sources: IAA

The reclassification of RM1.8bn worth of these receivables

from current assets to non-current assets indicate that

management no longer expects that IAA would be able to

repay these dues within the near term. However,

management assured us that there would be no impairments

on any of these receivables from IAA, as there is sufficient

evidence to indicate that IAA would be able to repay these in

due time.

The potential delay in the turnaround of IAA could put

further stress on AirAsia’s balance sheet, as the latter may

have to continue to provide working capital support for the

former. However, we are not overly concern on this as: (1)

any setback to the turnaround due to the QZ8501 accident

would likely be temporary, (2) the monetisation of AirAsia’s

various non-core businesses would provide sufficient cash

inflow for the group, and (3) management’s decision to stop

adding aircraft to IAA’s network until it turns around, will

help to limit the size of the latter’s losses and cash needs.

4) 4) 4) 4) Launch of Launch of Launch of Launch of IAAXIAAXIAAXIAAX could drive some traffic to IAAcould drive some traffic to IAAcould drive some traffic to IAAcould drive some traffic to IAA

The upcoming launch of Indonesia AirAsia X (IAAX) with its

first hub at Denpasar International Airport, Bali could help to

feed more traffic into IAA’s network. IAAX has launched its

inaugural service to Taipei, Taiwan on 19 Jan 2015. Also, the

airline has launched its service to Melbourne, Australia on 18

Mar 2015, after it managed to overcome the Australian

regulatory hurdles. With Denpansar being the second largest

hub for IAA, we think there could potentially be spill-over

effects to IAA as IAAX launches more services in the future.

IAA: Depansar International Airport is the airline’s second largest hub

Sources: CAPA

Financial forecasts

1) 1) 1) 1) Split MAA Split MAA Split MAA Split MAA intointointointo airline airline airline airline operations and operations and operations and operations and aircraft aircraft aircraft aircraft leasing leasing leasing leasing

operations; operations; operations; operations; cut earnings on weaker RM and lower TAA cut earnings on weaker RM and lower TAA cut earnings on weaker RM and lower TAA cut earnings on weaker RM and lower TAA

earningsearningsearningsearnings

We have decided to review the presentation of our earnings

forecasts, and split Malaysia AirAsia’s (MAA) into two

different earnings stream: (1) airline operations, and (2)

aircraft leasing operations.

In doing this, we assume the group’s asset cost (i.e.

depreciation and lease expense) and finance costs are pro-

rated based on the respective segment’s fleet size. The

purpose of this exercise is to better reflect the inherent

differences of the two key earnings streams in our earnings

forecasts, and to facilitate the valuation of the leasing arm.

We have cut our FY15/16/17F earnings forecasts by

10%/21%/22%, to reflect: (1) the weaker MYR, and (2)

lower earnings of Thai AirAsia (TAA), which is the key reason

behind the steeper earnings cut in FY16/17F.

2) Key assumptions for our earnings forecasts2) Key assumptions for our earnings forecasts2) Key assumptions for our earnings forecasts2) Key assumptions for our earnings forecasts

Our earnings assumptions for MAA’s airline operations are as

follows:

a. Core PBT to double in FY15F, driven by higher load

factor of 82% (vs 79% in FY14, due to active

capacity management) and cheaper fuel.

600 602 473

380 263 239 265

808 791 760 727 818 812

917 921

1,338 1,434

1,816

2,323 2,445

0

500

1,000

1,500

2,000

2,500

3,000

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

RM m

Amount due from associates and JV

Page 10

Company Focus

AirAsia

b. Subsequently, core PBT would fall by 14% in FY16F,

as fuel costs revert to a higher level (USD85/bbl vs

USD97/bbl in FY15F

c. Core PBT would resume its growth trajectory (+3%)

in FY17F, which is in line with the expected ASK

growth

MAA: Airline operations’ key financial trends

Sources: AirAsia, AllianceDBS

Our earnings assumptions for MAA’s aircraft leasing

operations are as follows:

a. Core PBT to grow by 93% due to stronger USD, as

lease income is denominated in USD while 90% of

the asset cost (i.e. depreciation) is denominated in

RM (based on historical costs).

b. Core PBT to subsequently grow by 19%/16% in

FY16/17F, slightly outperforming the expected fleet

growth of 12% p.a. on higher average USD in FY16F

and stagnant interest costs (debt repayments equal

new debts).

MAA: Leasing operations’ key financial trends

Sources: AirAsia, AllianceDBS

Other general assumptions are as follows:

a. TAA’s net profit to rebound strongly in FY15F

(+650%), driven by cheaper fuel and stronger

demand from a recovery in Thailand’s tourism. Net

profit to grow by 11%/5% in FY16/17F.

b. IAA would be able to turn around with a small net

profit of IDR31bn in FY15F. But, no earnings would

be consolidated in FY15-17F due to the large

cumulative unrecognised loss (RM334.4m or

IDR1,193bn as at 4Q14).

c. The group to recognise the start-up loss of

RM27.1/6.9m from AirAsia India in FY15/16F, after

which its equity investment in the unit will be fully

impaired. Thus, no further recognition of loss is

necessary in FY17F.

d. The group to recognise the start-up loss of

RM32.2/64.4m from AirAsia Japan in FY16/17F.

Valuation and Recommendation

1) 1) 1) 1) Changes in our SOPChanges in our SOPChanges in our SOPChanges in our SOP----valuationvaluationvaluationvaluation

We revised our SOP-valuation following: (1) the earnings cut,

and (2) our segregation of MAA into airline and aircraft

leasing operations. Instead of valuing MAA as a single unit,

we are valuing the airline and aircraft leasing operations

separately, to better reflect the fundamental differences

between these two segments. Also, we imputed the amounts

due from associates and JVs in our computation of the SOP,

to reflect the debt investments in these units (as the lender).

2) RM2.60 TP based on 2) RM2.60 TP based on 2) RM2.60 TP based on 2) RM2.60 TP based on a a a a 35%35%35%35% discount to SOPdiscount to SOPdiscount to SOPdiscount to SOP valuation; valuation; valuation; valuation;

value has emerged value has emerged value has emerged value has emerged –––– uuuupgrade to BUYpgrade to BUYpgrade to BUYpgrade to BUY

Our SOP valuation for AirAsia is RM3.98 per share, but we

applied a 35% discount to the SOP value, in order to arrive at

our RM2.60 TP. In light of the operating challenges

surrounding IAA, we believe such a steep discount is

necessary in order to have a sufficient margin of safety. The

RM1.38 SOP discount is sufficient to account for: (1) a

complete write-off of the amounts due from associates, (2)

complete write-off of IAA, and (3) 32% impairment to the

aircraft leasing segment (i.e. 24 aircraft on lease to IAA from

the total fleet of 75 aircraft).

We are upgrading our rating on AirAsia to BUY, given the

implied potential upside to our RM2.60 TP (+19%). We

believe the recent sell-down has been overdone, and the

market has ignored the significant value of its portfolio

comprising non-airline businesses within the group. Our TP

implies 8.5x FY15F P/E, 1.5x FY15F P/E and 8.8x FY15F

adjusted EV/EBITDAR.

(5%)

0%

5%

10%

15%

20%

25%

(1,000)

0

1,000

2,000

3,000

4,000

5,000

6,000

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015F 2016F 2017F

RM m

Revenue (lhs) Core PBT (lhs) Core PBT margin (rhs)

(5%)

0%

5%

10%

15%

20%

25%

(1,000)

0

1,000

2,000

3,000

4,000

5,000

6,000

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015F 2016F 2017F

RM m

Revenue (lhs) Core PBT (lhs) Core PBT margin (rhs)

Page 11

Company Focus

AirAsia

AirAsia: SOP valuation

SegmentSegmentSegmentSegment StakeStakeStakeStake Value Value Value Value

(RM m)(RM m)(RM m)(RM m)

Per Per Per Per share share share share (RM)(RM)(RM)(RM)

CommentsCommentsCommentsComments

Malaysian AirAsia 100.0% 8,514 3.06

- Airline operations 100.0% 3,344 1.20 8x FY15F Adjusted EV/EBITDAR (less debt + capitalised lease)

- Aircraft leasing business 100.0% 2,664 0.96 10x FY15F P/E (less debt + capitalised lease)

- Net amount due from related parties 100.0% 2,506 0.90 As at 4Q14

Thai AirAsia 45.0% 1,441 0.52 9x FY15F Adjusted EV/EBITDAR (less debt + capitalised lease)

Indonesia AirAsia 48.9% 219 0.08 7x FY15F Adjusted EV/EBITDAR (less debt + capitalised lease)

AirAsia Philippines 40.0% 76 0.03 Cost of investment

AirAsia India 40.0% 47 0.02 Cost of investment

AirAsia X 13.8% 153 0.06 Based on our TP of RM0.47

Tune Ins 13.7% 199 0.07 Current market capitalisation

AAE Travel 25.0% 318 0.11 USD86.25m in line with latest transacted value

Asia Aviation Centre of Excellence 50.0% 103 0.04 1x FY13 P/BV, in line with APFT's valuation

SumsSumsSumsSums----OfOfOfOf----Parts ValueParts ValueParts ValueParts Value 11,069.5 11,069.5 11,069.5 11,069.5 3.98 3.98 3.98 3.98

Less: 35% SOP discount (3,874.3) (1.39) To reflect the challenges surrounding IAA

Target Equity ValueTarget Equity ValueTarget Equity ValueTarget Equity Value 7,195.2 7,195.2 7,195.2 7,195.2 2.602.602.602.60 Rounded to the nearest 5 sen

Sources: AirAsia, AllianceDBS

Peer comparison of regional LCCs

Sources: Bloomberg Finance L.P., AllianceDBS, DBS Vickers

Company Country Call

Target

Price

Current

Price

Market

Cap

(LC) (LC)

(USD

m) CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16 CY15 CY16

AirAsia Malaysia Buy 2.60 2.18 1,655 105 -2 7.1 7.3 1.3 1.1 5.5 16.1 0.8 2.8 8.6 8.1

AirAsia X Bhd Malaysia Fully

Valued

0.47 0.47 304 N/M 32 N/M N/M 2.3 3.1 -34.2 -32.4 0.0 0.0 10.1 8.2

Tiger Airways

Holdings

Singapore Buy 0.39 0.33 221 -104 775 124.2 14.2 3.2 2.6 -11.9 20.5 0.0 0.0 15.4 10.2

Cebu Air* Philippines NR NR 86.85 1,177 84 6 9.5 8.9 1.9 1.6 21.8 19.7 2.0 1.8 7.0 6.6

Asia Aviation PCL* Thailand NR NR 5.75 858 903 13 15.1 13.3 1.3 1.2 8.4 8.8 1.0 1.8 7.7 7.2

Nok Air* Thailand NR NR 13.00 250 288 19 9.2 7.7 1.7 1.5 19.3 21.1 5.4 6.8 7.2 6.8

Virgin Australia* Australia NR NR 0.51 1,414 148 46 22.4 15.4 1.6 1.4 2.1 9.9 0.0 0.2 6.4 6.0

Air Arabia PJSC* UAE NR NR 1.44 1,830 19 8 10.0 9.3 1.2 1.1 13.0 13.3 6.2 6.8 8.4 7.8

Southwest Airlines* US NR NR 45.44 30,717 75 6 12.9 12.1 3.3 2.7 29.7 24.9 0.6 0.7 5.9 5.4

JetBlue Airways* US NR NR 19.44 6,043 141 7 11.5 10.8 2.0 1.7 21.0 18.9 N/A N/A 5.7 5.2

Westjet Airlines* Canada NR NR 30.08 3,069 39 0 8.8 8.8 1.8 1.6 21.9 17.2 1.8 2.1 5.8 5.8

EasyJet Plc* UK NR NR 1868.00 11,086 28 6 12.6 11.9 2.9 2.5 21.9 21.7 3.3 3.6 8.2 7.4

Ryanair Holdings* Ireland NR NR 10.58 15,934 37 1 13.3 13.1 3.5 2.9 23.7 24.6 1.0 1.6 9.1 7.7

Sector Average 74 8 12.9 11.9 2.9 2.5 24.0 22.2 1.4 1.7 7.1 6.4

* Estimates based on Bloomberg consensus

Adjusted EV/

EBITDAR (x)EPS Growth P/E (x) P/BV (x) ROE (%)

Dividend Yield

(%)

Page 12

Company Focus

AirAsia

Key Investment Risks

1) 1) 1) 1) Further weakness in Further weakness in Further weakness in Further weakness in RMRMRMRM

RM has depreciated significantly (-15%) against the USD

since Jun 2014. This was mainly due to a myriad of factors:

(1) weaker fiscal outlook following the recent plunge in oil

prices, (2) negative publicity surrounding 1MDB, and (3) fund

outflow in anticipation of the interest rate hike by the US

Federal Reserve. If the trend continues, this could have grave

repercussions for AirAsia, as it will result in higher OPEX (55%

is USD-denominated) and finance cost (87% of borrowings is

in USD). However, we think AirAsia’s current share price has

sufficiently priced in this risk.

2) Perceived relationsh2) Perceived relationsh2) Perceived relationsh2) Perceived relationship with AAXip with AAXip with AAXip with AAX

The perceived relationship between AirAsia and AirAsia X

(AAX) has been a drag on the former’s share price

performance. Faced with mounting losses amid the difficult

operating environment, AAX was forced to seek fresh capital

and is currently in the midst of undertaking a rights issue.

Given the operating challenges faced by AAX, investors may

be concerned that AirAsia may have to underwrite the rights

issue. There are also worries that AirAsia may have to bail out

AAX, if the latter’s financial performance continues to

deteriorate in the future. The appointment of AirAsia

stalwarts Datuk Kamaruddin bin Meranun and Mr. Benyamen

bin Ismail to the executive positions at AAX further

accentuates this perception.

However, management has reiterated that AirAsia and AAX

are two separate legal entities, and it will not allow AAX's

problems to affect AirAsia. We understand that AirAsia would

only subscribe to a portion of the rights issue, even if AAX’s

rights issue fails to garner sufficient interest. Instead, the

rights issue will likely be underwritten by the other major

shareholders (i.e. Tune Group and Datuk Kamaruddin bin

Meranun).

Page 13

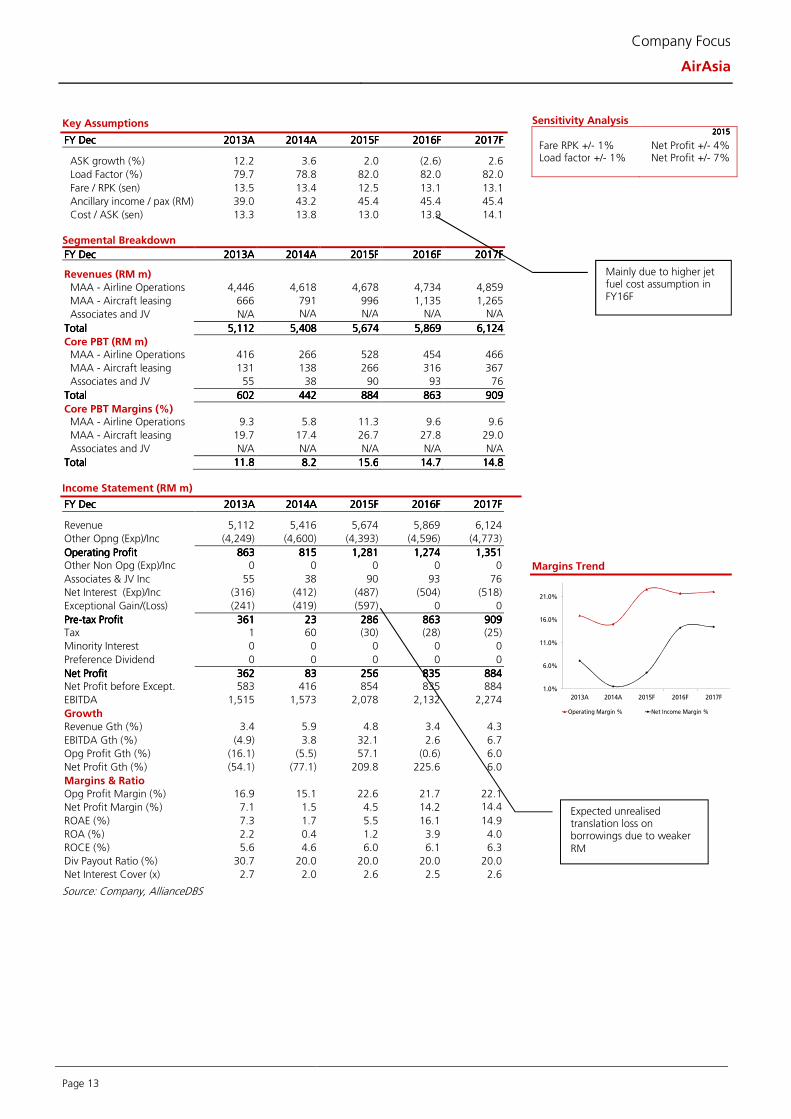

Company Focus

AirAsia

Key Assumptions

FY FY FY FY DecDecDecDec 2013201320132013AAAA 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF

ASK growth (%) 12.2 3.6 2.0 (2.6) 2.6

Load Factor (%) 79.7 78.8 82.0 82.0 82.0

Fare / RPK (sen) 13.5 13.4 12.5 13.1 13.1

Ancillary income / pax (RM) 39.0 43.2 45.4 45.4 45.4

Cost / ASK (sen) 13.3 13.8 13.0 13.9 14.1 Segmental Breakdown

FY FY FY FY DecDecDecDec 2013201320132013AAAA 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF Revenues (RM m)

MAA - Airline Operations 4,446 4,618 4,678 4,734 4,859

MAA - Aircraft leasing 666 791 996 1,135 1,265

Associates and JV N/A N/A N/A N/A N/A TotalTotalTotalTotal 5,1125,1125,1125,112 5,4085,4085,4085,408 5,6745,6745,6745,674 5,8695,8695,8695,869 6,1246,1246,1246,124

Core PBT (RM m) MAA - Airline Operations 416 266 528 454 466

MAA - Aircraft leasing 131 138 266 316 367

Associates and JV 55 38 90 93 76

TotalTotalTotalTotal 602602602602 442442442442 884884884884 863863863863 909909909909

Core PBT Margins (%) MAA - Airline Operations 9.3 5.8 11.3 9.6 9.6

MAA - Aircraft leasing 19.7 17.4 26.7 27.8 29.0

Associates and JV N/A N/A N/A N/A N/A

TotalTotalTotalTotal 11.811.811.811.8 8.28.28.28.2 15.615.615.615.6 14.714.714.714.7 14.814.814.814.8

Income Statement (RM m)

FY FY FY FY DecDecDecDec 2013201320132013AAAA 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF

Revenue 5,112 5,416 5,674 5,869 6,124

Other Opng (Exp)/Inc (4,249) (4,600) (4,393) (4,596) (4,773)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 863863863863 815815815815 1,2811,2811,2811,281 1,2741,2741,2741,274 1,3511,3511,3511,351 Other Non Opg (Exp)/Inc 0 0 0 0 0

Associates & JV Inc 55 38 90 93 76

Net Interest (Exp)/Inc (316) (412) (487) (504) (518)

Exceptional Gain/(Loss) (241) (419) (597) 0 0

PrePrePrePre----tax Profittax Profittax Profittax Profit 361361361361 23232323 286286286286 863863863863 909909909909 Tax 1 60 (30) (28) (25)

Minority Interest 0 0 0 0 0

Preference Dividend 0 0 0 0 0

Net ProfitNet ProfitNet ProfitNet Profit 362362362362 83838383 256256256256 835835835835 884884884884 Net Profit before Except. 583 416 854 835 884

EBITDA 1,515 1,573 2,078 2,132 2,274

Growth

Revenue Gth (%) 3.4 5.9 4.8 3.4 4.3

EBITDA Gth (%) (4.9) 3.8 32.1 2.6 6.7

Opg Profit Gth (%) (16.1) (5.5) 57.1 (0.6) 6.0

Net Profit Gth (%) (54.1) (77.1) 209.8 225.6 6.0

Margins & Ratio

Opg Profit Margin (%) 16.9 15.1 22.6 21.7 22.1

Net Profit Margin (%) 7.1 1.5 4.5 14.2 14.4

ROAE (%) 7.3 1.7 5.5 16.1 14.9

ROA (%) 2.2 0.4 1.2 3.9 4.0

ROCE (%) 5.6 4.6 6.0 6.1 6.3

Div Payout Ratio (%) 30.7 20.0 20.0 20.0 20.0

Net Interest Cover (x) 2.7 2.0 2.6 2.5 2.6

Source: Company, AllianceDBS

Sensitivity Analysis 2015201520152015

Fare RPK +/- 1% Net Profit +/- 4% Load factor +/- 1% Net Profit +/- 7%

Margins Trend

1.0%

6.0%

11.0%

16.0%

21.0%

2013A 2014A 2015F 2016F 2017F

Operating Margin % Net Income Margin %

Mainly due to higher jet fuel cost assumption in FY16F

Expected unrealised translation loss on borrowings due to weaker RM

Page 14

Company Focus

AirAsia

Quarterly / Interim Income Statement (RM m)

FY FY FY FY DecDecDecDec 4Q4Q4Q4Q2013201320132013 1Q1Q1Q1Q2014201420142014 2Q2Q2Q2Q2014201420142014 3Q3Q3Q3Q2014201420142014 4Q4Q4Q4Q2014201420142014

Revenue 1,277 1,302 1,311 1,317 1,478

Other Oper. (Exp)/Inc (1,096) (1,095) (1,170) (1,117) (1,102)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 181181181181 208208208208 141141141141 200200200200 376376376376 Other Non Opg (Exp)/Inc 0 0 0 0 0

Associates & JV Inc 22 16 (9) 27 13

Net Interest (Exp)/Inc (82) (97) (103) (98) (116)

Exceptional Gain/(Loss) (24) 7 226 (103) (502)

PrePrePrePre----tax Profittax Profittax Profittax Profit 97979797 134134134134 255255255255 26262626 (229)(229)(229)(229) Tax 72 6 112 (21) (37)

Minority Interest 0 0 0 0 0

Net ProfitNet ProfitNet ProfitNet Profit 169169169169 140140140140 367367367367 5555 (265)(265)(265)(265) Net profit bef Except. 115 124 26 119 265

EBITDA 326 388 322 407 575

Growth

Revenue Gth (%) (0.3) 2.0 0.7 0.5 12.2

EBITDA Gth (%) (28.5) 19.0 (16.9) 26.4 41.0

Opg Profit Gth (%) (32.4) 14.9 (32.1) 42.2 87.8

Net Profit Gth (%) 374.9 (17.1) 162.8 (98.5) nm

Margins Opg Profit Margins (%) 14.2 15.9 10.7 15.2 25.5

Net Profit Margins (%) 13.2 10.7 28.0 0.4 (17.9)

Balance Sheet (RM m)

FY FY FY FY DecDecDecDec 2013201320132013AAAA 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF Net Fixed Assets 11,935 13,036 13,129 13,925 15,239

Invts in Associates & JVs 954 422 320 412 489

Other LT Assets 2,044 4,676 4,676 4,676 4,676

Cash & ST Invts 1,384 1,623 1,963 1,880 1,224

Inventory 30 18 18 18 18

Debtors 1,510 668 699 724 755

Other Current Assets 0 0 0 0 0

Total AssetsTotal AssetsTotal AssetsTotal Assets 17,85617,85617,85617,856 20,44320,44320,44320,443 20,80620,80620,80620,806 21,63521,63521,63521,635 22,40122,40122,40122,401

ST Debt

1,119 2,275 2,275 2,275 2,275

Creditor 761 626 600 628 652

Other Current Liab 692 984 536 554 578

LT Debt 9,970 10,453 11,050 11,050 11,050

Other LT Liabilities 313 1,548 1,548 1,548 1,548

Shareholder’s Equity 5,001 4,557 4,797 5,580 6,298

Minority Interests 0 0 0 0 0

Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab. 17,85617,85617,85617,856 20,44320,44320,44320,443 20,80620,80620,80620,806 21,63521,63521,63521,635 22,40122,40122,40122,401

Non-Cash Wkg. Capital 87 (924) (418) (440) (457)

Net Cash/(Debt) (9,706) (11,105) (11,362) (11,445) (12,101)

Debtors Turn (avg days) 94.6 73.4 44.0 44.2 44.1

Creditors Turn (avg days) (439.8) (351.7) (316.1) (292.6) (275.7)

Inventory Turn (avg days) (16.3) (12.1) (9.4) (8.7) (7.8)

Asset Turnover (x) 0.3 0.3 0.3 0.3 0.3

Current Ratio (x) 1.1 0.6 0.8 0.8 0.6

Quick Ratio (x) 1.1 0.6 0.8 0.8 0.6

Net Debt/Equity (X) 1.9 2.4 2.4 2.1 1.9

Net Debt/Equity ex MI (X) 1.9 2.4 2.4 2.1 1.9

Capex to Debt (%) 20.3 14.3 6.0 11.7 16.2

Z-Score (X) 1.0 0.8 1.0 1.0 1.1

Source: Company, AllianceDBS

Revenue Trend

Asset Breakdown (2015)

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

1,500

3Q

201

2

4Q

201

2

1Q

201

3

2Q

201

3

3Q

201

3

4Q

201

3

1Q

201

4

2Q

201

4

3Q

201

4

4Q

201

4

Revenue Revenue Growth % (QoQ)

OPEX remain high in 4Q14, as fuel cost were hedged at higher costs

Page 15

Company Focus

AirAsia

Cash Flow Statement (RM m)

FY FY FY FY DecDecDecDec 2013201320132013AAAA 2014201420142014AAAA 2015201520152015FFFF 2016201620162016FFFF 2017201720172017FFFF

Pre-Tax Profit 361 23 286 863 909

Dep. & Amort. 597 719 708 766 847

Tax Paid (29) (15) (30) (28) (25)

Assoc. & JV Inc/(loss) (55) (38) (90) (93) (76)

Chg in Wkg.Cap. (108) (917) (221) 22 17

Other Operating CF 276 424 597 0 0

Net Operating CFNet Operating CFNet Operating CFNet Operating CF 961961961961 196196196196 1,2501,2501,2501,250 1,5291,5291,5291,529 1,6721,6721,6721,672 Capital Exp.(net) (2,254) (1,825) (801) (1,561) (2,161)

Other Invts.(net) 0 49 0 0 0

Invts in Assoc. & JV (93) (270) 192 0 0

Div from Assoc & JV 0 0 0 0 0

Other Investing CF 0 0 0 0 0

Net Investing CFNet Investing CFNet Investing CFNet Investing CF (2,346)(2,346)(2,346)(2,346) (2,045)(2,045)(2,045)(2,045) (609)(609)(609)(609) (1,561)(1,561)(1,561)(1,561) (2,161)(2,161)(2,161)(2,161) Div Paid (667) (111) (17) (51) (167)

Chg in Gross Debt 1,175 1,886 0 0 0

Capital Issues 1 2 0 0 0

Other Financing CF (1) (1) 0 0 0

Net Financing CFNet Financing CFNet Financing CFNet Financing CF 508508508508 1,7751,7751,7751,775 (17)(17)(17)(17) (51)(51)(51)(51) (167)(167)(167)(167)

Currency Adjustments 24 30 0 0 0

Chg in Cash (853) (44) 625 (83) (656)

Opg CFPS (sen) 38.4 40.0 52.9 54.2 59.5

Free CFPS (sen) (46.5) (58.6) 16.2 (1.1) (17.6)

Source: Company, AllianceDBS

Capital Expenditure

Target Price & Ratings History

Source: AllianceDBS

0

500

1000

1500

2000

2500

2013A 2014A 2015F 2016F 2017F

Capital Expenditure (-)

S.No.S.No.S.No.S.No. Da teDa teDa teDa teClos ing Clos ing Clos ing Clos ing

Pri cePri cePri cePri ce

Ta rge t Ta rge t Ta rge t Ta rge t

Pric ePric ePric ePric eRa ting Ra ting Ra ting Ra ting

1: 09 May 14 2.21 2.40 Hold

2: 21 May 14 2.45 2.80 Buy

3: 02 Jul 14 2.30 2.80 Buy

4: 15 Aug 14 2.37 3.20 Buy

5: 21 Aug 14 2.40 3.20 Buy

6: 02 Sep 14 2.47 3.20 Buy

7: 28 Oct 14 2.39 3.20 Buy

8: 11 Nov 14 2.59 3.20 Buy

9: 20 Nov 14 2.42 3.20 Buy

10: 29 Dec 14 2.69 2.80 Hold

11: 27 Jan 15 2.77 2.80 Hold

12: 27 Feb 15 2.62 2.60 Hold

Note Note Note Note : Share price and Target price are adjusted for corporate actions.

1

2

3

4

5

6

7

8

9

10

11 12

2.07

2.27

2.47

2.67

2.87

3.07

Mar-14 Jul-14 Nov-14 Mar-15

RMRMRMRM

Page 16

Company Focus

AirAsia

DISCLOSURE

Stock rating definitions STRONG BUY - > 20% total return over the next 3 months, with identifiable share price catalysts within this time frame BUY - > 15% total return over the next 12 months for small caps, >10% for large caps HOLD - -10% to +15% total return over the next 12 months for small caps, -10% to +10% for large caps FULLY VALUED - negative total return > -10% over the next 12 months SELL - negative total return of > -20% over the next 3 months, with identifiable catalysts within this time frame Commonly used abbreviations Adex = advertising expenditure EPS = earnings per share PBT = profit before tax bn = billion EV = enterprise value P/B = price / book ratio BV = book value FCF = free cash flow P/E = price / earnings ratio CF = cash flow FV = fair value PEG = P/E ratio to growth ratio CAGR = compounded annual growth rate FY = financial year q-o-q = quarter-on-quarter Capex = capital expenditure m = million RM = Ringgit CY = calendar year M-o-m = month-on-month ROA = return on assets Div yld = dividend yield NAV = net assets value ROE = return on equity DCF = discounted cash flow NM = not meaningful TP = target price DDM = dividend discount model NTA = net tangible assets trn = trillion DPS = dividend per share NR = not rated WACC = weighted average cost of capital EBIT = earnings before interest & tax p.a. = per annum y-o-y = year-on-year EBITDA = EBIT before depreciation and amortisation PAT = profit after tax YTD = year-to-date

Page 17

Company Focus

AirAsia

DISCLAIMER

This report has been prepared for information purposes only by AllianceDBS Research Sdn Bhd (“ADBSR”) (formerly known as HwangDBS Vickers Research Sdn Bhd), a subsidiary of Alliance Investment Bank Berhad (“AIBB”) and an associate of DBS Vickers Securities Holdings Pte Ltd (“DBSVH”). DBSVH is a wholly-owned subsidiary of DBS Bank Ltd. This report is strictly confidential and is meant for circulation to clients of ADBSR, AIBB and DBSVH only or such persons as may be deemed eligible to receive such research report, information or opinion contained herein. Receipt and review of this report indicate your agreement not to distribute, reproduce or disclose in any other form or medium (whether electronic or otherwise) the contents, views, information or opinions contained herein without the prior written consent of ADBSR. This report is based on data and information obtained from various sources believed to be reliable at the time of issuance of this report and any opinion expressed herein is subject to change without prior notice and may differ or be contrary to opinions expressed by ADBSR’s affiliates and/or related parties. ADBSR does not make any guarantee, representation or warranty (whether express or implied) as to the accuracy, completeness, reliability or fairness of the data and information obtained from such sources as may be contained in this report. As such, neither ADBSR nor its affiliates and/or related parties shall be held liable or responsible in any manner whatsoever arising out of or in connection with the reliance and usage of such data and information or third party references as may be made in this report (including, but not limited to any direct, indirect or consequential losses, loss of profits and damages). The views expressed in this report reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendation(s) or view(s) in this report. ADBSR prohibits the analyst(s) who prepared this report from receiving any compensation, incentive or bonus based on specific investment banking transactions or providing a specific recommendation for, or view of, a particular company. This research report provides general information only and is not to be construed as an offer to sell or a solicitation to buy or sell any securities or other investments or any options, futures, derivatives or other instruments related to such securities or investments. In particular, it is highlighted that this report is not intended for nor does it have regard to the specific investment objectives, financial situation and particular needs of any specific person who may receive this report. Investors are therefore advised to make their own independent evaluation of the information contained in this report, consider their own individual investment objectives, financial situations and particular needs and consult their own professional advisers (including but not limited to financial, legal and tax advisers) regarding the appropriateness of investing in any securities or investments that may be featured in this report. ADBSR, AIBB, DBSVH and DBS Bank Ltd, their directors, representatives and employees or any of their affiliates or their related parties may, from time to time, have an interest in the securities mentioned in this report. AIBB, DBSVH and DBS Bank Ltd, their affiliates and/or their related persons may do and/or seek to do business with the company(ies) covered in this report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell or buy such securities from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory or underwriting services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report. AIBB, DBSVH, DBS Bank Ltd (which carries on, inter alia, corporate finance activities) and their activities are separate from ADBSR. AIBB, DBSVH and DBS Bank Ltd may have no input into company-specific coverage decisions (i.e. whether or not to initiate or terminate coverage of a particular company or securities in reports produced by ADBSR) and ADBSR does not take into account investment banking revenues or potential revenues when making company-specific coverage decisions. ADBSR, AIBB, DBSVH, DBS Bank Ltd and/or other affiliates of DBS Vickers Securities (USA) Inc (“DBSVUSA”), a U.S.-registered broker-dealer, may beneficially own a total of 1% or more of any class of common equity securities of the subject company mentioned in this report. ADBSR, AIBB, DBSVH, DBS Bank Ltd and/or other affiliates of DBSVUSA may, within the past 12 months, have received compensation and/or within the next 3 months seek to obtain compensation for investment banking services from the subject company. DBSVUSA does not have its own investment banking or research department, nor has it participated in any investment banking transaction as a manager or co-manager in the past twelve months. Any US persons wishing to obtain further information, including any clarification on disclosures in this disclaimer, or to effect a transaction in any security discussed in this report should contact DBSVUSA exclusively. DBS Vickers Securities (UK) Ltd is an authorised person in the meaning of the Financial Services and Markets Act and is regulated by The Financial Services Authority. Research distributed in the UK is intended only for institutional clients. In reviewing this report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the overriding issue of confidentiality, available upon request to enable an investor to make their own independent evaluation of the information contained herein.

Wong Ming Tek, Executive Director

Published and Printed by

AllianceDBS Research Sdn Bhd AllianceDBS Research Sdn Bhd AllianceDBS Research Sdn Bhd AllianceDBS Research Sdn Bhd (128540 U)

(formerly known as HWANGDBS Vickers Research Sdn Bhd)

19th Floor, Menara Multi-Purpose, Capital Square, 8 Jalan Munshi Abdullah, 50100 Kuala Lumpur, Malaysia.

Tel.: +603 2604 3333 Fax: +603 2604 3921 email : [email protected]

![150324 jeans[1]](https://static.cupdf.com/doc/110x72/568cadce1a28ab186dad4136/150324-jeans1.jpg)