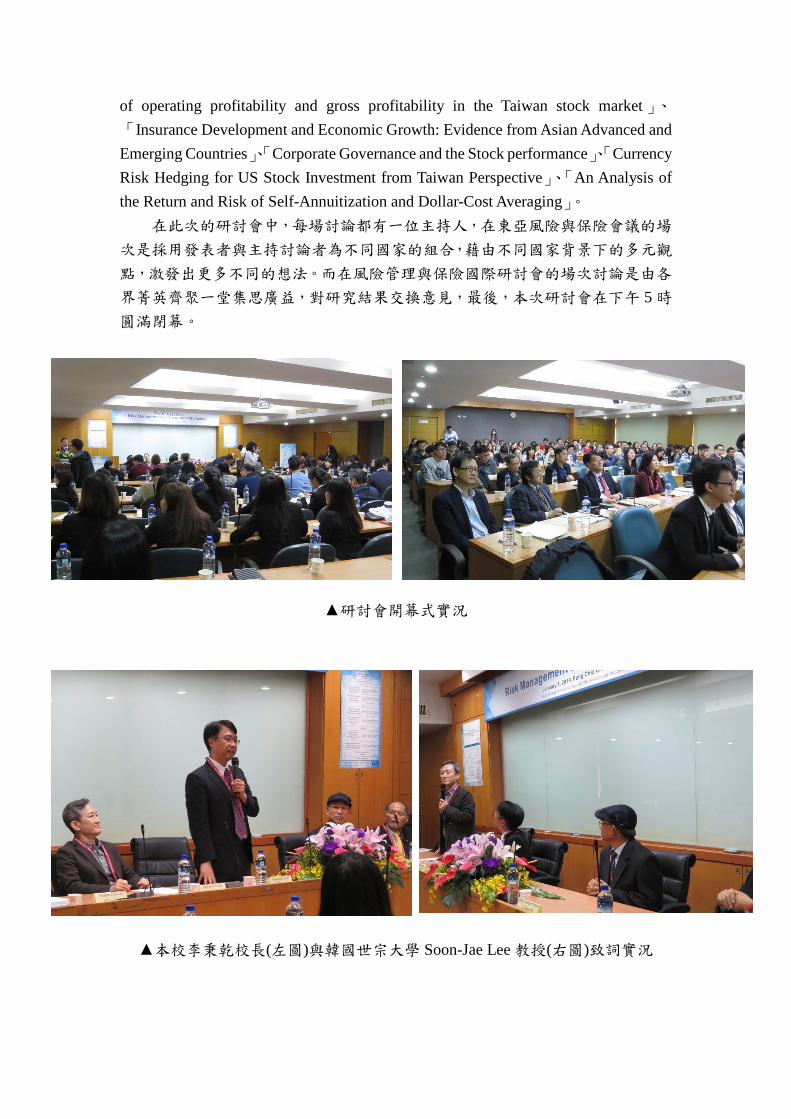

「2019 風險管理與保險國際研討會 - 第六屆東亞風險與保險會議」由逢甲

大學金融學院及風險管理與保險學系聯合主辦,學術研討會於 1 月 5 日在本校第

八國際會議廳召開,開幕儀式首先由本校李秉乾校長致詞,接著分別由日本早稻

田大學大塚忠義教授、韓國世宗大學 Soon-Jae Lee 教授、本校財務工程與精算學

士學位學程呂瑞秋主任致詞。之後為感謝本次研討會之贊助者-喬美國際網路公

司與喬安網路平台公司的簡永松董事長,由本校金融學院陳森松院長致贈禮品予

簡董事長,並邀請簡董事長致詞,為本次研討會正式拉開序幕。與會者還包括日

本的同志社女子大學、明治大學、東京理科大學、東京經濟大學、大阪產業大學、

京都產業大學;韓國的東亞大學、東西大學、韓國保險研究機構(KIRI) ;美國的

天普大學;香港的香港中文大學;台灣的國立高雄科技大學、國立臺中科技大學、

淡江大學等各地學者,以及本校風險管理與保險學系曾鹿鳴主任、財務金融學系

劉炳麟主任、金融碩士在職學位學程與金融博士學位學程林昆立主任等多位師生,

共計有 100 餘人。 東亞風險與保險會議於開幕後在第八國際會議廳進行,每位論文發表者都有

45 分鐘的發表時間(20 分鐘報告時間、10 分鐘為討論時間、15 分鐘問答時間)。此場研討會中共發表以下 6 篇論文:「An Economic Analysis of Joint Products under Demand Uncertainty」、「Private Health Insurance Operation and Cooperation Model」、「Effects of Price Increases on Smoking Behavior of Smokers and Non-Smokers」、「Adverse Selection in the Private Surgery and Hospitalization Health Insurance、「An Ambiguity Measure under EUUP and Its Application to a Portfolio Problem」、「Multi-population Mortality Modeling: When the Data is Too Much and Not Enough」。 風險管理與保險國際研討會在同時間於商 804A 召開,每位論文發表者有 30分鐘的時間(20 分鐘發表時間、5 分鐘討論時間、5 分鐘的問答時間)。此場研討

會中共發表 7 篇論文:「The Affordable Care Act and Medical Malpractice Insurance Industry: A Generalized Synthetic Control Method」、「Consumer Benefit and Design of Long-Term Care Annuity Product」、「A preliminary study of long-short strategies formulated by size, value, momentum or contrarian effects and by the income measures

of operating profitability and gross profitability in the Taiwan stock market」、「Insurance Development and Economic Growth: Evidence from Asian Advanced and Emerging Countries」、「Corporate Governance and the Stock performance」、「Currency Risk Hedging for US Stock Investment from Taiwan Perspective」、「An Analysis of the Return and Risk of Self-Annuitization and Dollar-Cost Averaging」。 在此次的研討會中,每場討論都有一位主持人,在東亞風險與保險會議的場

次是採用發表者與主持討論者為不同國家的組合,藉由不同國家背景下的多元觀

點,激發出更多不同的想法。而在風險管理與保險國際研討會的場次討論是由各

界菁英齊聚一堂集思廣益,對研究結果交換意見,最後,本次研討會在下午 5 時

圓滿閉幕。

▲研討會開幕式實況

▲本校李秉乾校長(左圖)與韓國世宗大學 Soon-Jae Lee 教授(右圖)致詞實況

▲本校金融學院陳森松院長(左)致贈禮品予

喬美國際網路公司與喬安網路平台公司簡永松董事長(右)

▲全體參與人員合照留念

▲研討會論文發表實況

1

2019 Risk Management and Insurance Conference and

The 6th East Asia Risk Management and Insurance Workshop

Feng Chia University, Taiwan

General Information:

Date:

January 4, 2019 (Friday) (Welcome dinner)

January 5, 2019 (Saturday) (Workshop day)

January 6 and 7 (Sunday and Monday) (Field trip days)

Workshop Venue:

No. 100, Wenhwa Rd., Seatwen, Feng Chia University, Taichung, Taiwan

(Webpage: http://en.fcu.edu.tw/wSite/mp?mp=3)

Workshop Rooms:

1. East Asia RMI Workshop: The 8th International Conference room (on the 8 th

floor of Business Building)

2. FCU RMI Workshop: 804A room (on the 8 th floor of Business Building)

(Also See Campus Map in: http://www.clc.fcu.edu.tw/index.php?id=1)

Organizers:

Tadayoshi Otsuka (Waseda University) (Japan)

Don (DongHan) Chang (Konkuk University) (Korea)

Richard Lu (Feng Chia University) (Taiwan)

Welcome Dinner:

6:00pm at Insky hotel (No. 18, Fuxing North Rd., Taichung) on Friday, January 4.

(Hosted by the dean of College of Finance, Pr. Sen-Sung Chen)

Registration Desk Opening time: from 9:30am to 9:50am, January 5.

Workshop opening: At 9:50am at the 8th International Conference room

Close Up Dinner:

6:00pm at Insky hotel (No. 18, Fuxing North Rd., Taichung) on Saturday, January

5. (Hosted by the dean of College of Finance, Pr. Sen-Sung Chen)

Field Trip:

Two-day field trip to Sun Moon Lake at your own expense. Please register before

December 15. Gather and Start at the East Gate of FCU at 9:30am January 6.

2

Workshop Day (January 5) information:

Welcome Speech (10 am at the 8th International Conference room):

Dr. Bing-Jean Lee, President of FCU

Mr. Yung-Sung Chien, Chairman of Shacom

Photo Time (10:20 am at the 8th International Conference room)

East Asia RMI Workshop Program: (at the 8th International Conference room)

Each presentation: 45 min. (Presentation: 20 min. Discussant: 10 min. Q&A: 15

min.)

o Section 1 (moderator: Lu-Ming Tseng (Feng Chia University)):

o 10:30: Presentation 1

o Title: An Economic Analysis of Joint Products under Demand

Uncertainty

o Presenters: Mahito Okura (Doshisha Women's College of

Liberal Arts)

o Discussant: DaeHwan Kim (Dong-A University)

o 11:15: Presentation 2

o Title: Private Health Insurance Operation and Cooperation

Model

o Presenter: SungHee Chung (Korea Insurance Research

Institute)

o Discussant: Yusuke Osaki (Waseda University)

o 12:00: Lunch

o Section 2 (moderator: Noriyoshi Yanase (Tokyo University of Science)):

o 13:30: Presentation 3

o Title: Effects of Price Increases on Smoking Behavior of

Smokers and Non-Smokers

o Presenter: DaeHwan Kim (Dong-A University)

o Discussant: Yoichiro Fujii (Osaka Sangyo University)

o 14:15: Presentation 4

o Title: Adverse Selection in the Private Surgery and

Hospitalization Health Insurance

o Presenter: Chia-Ling Ho (Tamkang University)

3

o Discussant: SungHee Chung (Korea Insurance Research

Institute)

o 15:00 Coffee break

o Section 3 (moderator: Soon-Jae Lee (Sejong University, Seoul, Korea)):

o 15:30: Presentation 5

o Title: An Ambiguity Measure under EUUP and Its Application

to a Portfolio Problem

o Presenter: Hideki Iwaki (Kyoto Sangyo University)

o Discussant: Jason J. H. Yeh (The Chinese University of Hong

Kong)

o 16:15: Presentation 6

o Title: Multi-population Mortality Modeling: When the Data is

Too Much and Not Enough

o Presenter: Ko-Lun Kung (Feng Chia University)

o Discussant: Yin-Yee Loeng (Feng Chia University)

o

o 17:00: Workshop closing, general meeting (for discussing next

workshop and other topics)

o 18:00: Dinner at Insky Hotel

4

An Economic Analysis of Joint Products under Demand

Uncertainty+

Mahito Okura

Department of Social System Studies, Faculty of Contemporary Social Studies,

Doshisha Women’s College of Liberal Arts

Kodo, Kyotanabe, Kyoto, 610-0395, Japan

Abstract:

The purpose of this study is to analyze the market under demand uncertainty when

two firms compete with two joint products which are indivisible multiple goods, such

as petroleum products. We investigate the situations in which no, either, or both firms

have either no demand information, or have demand information in one or both

markets, and examine how the differences in information structures affect the

equilibrium expected profit of each firm.

Keywords:

Joint products, Demand uncertainty, Information

5

Private Health Insurance Operation and Cooperation Model

SungHee Chung

Korea Insurance Research Institute

1.National Health Expenditure

2.Classification

3.Role and Market

4.GDP & Medical Expenditure

5.Cost Structure

6.Product Operation

7.Rating Structure

8.Medical Cost Management

9.Policy Goal, Objective & Instrument

6

Effects of Price Increases on Smoking Behavior of Smokers and

Non-Smokers

DaeHwan Kim

Associate Professor in the Department of Economics at Dong-A University, Korea

Abstract

Smoking increases not only medical costs by causing serious illness, but also

adversely affects economic growth in the sense that it could reduce productivity. In an

effort to ease the higher smoking rate in Korea compared to other OECD countries’

average smoking rate, the Korean government has raised cigarette prices by 80

percent from 2,500 won to 4,500 won since 2015. In 2004, it raised the prices from

2,000 won to 2,500 won, but the magnitude of price increases was not that high and

there was not enough data to study the effects of cigarette price hikes.

In this study, I analyzed the effect of cigarette price increases on smoking

behavior by using the Korea Health Panel (KHP) data from 2011 to 2016. The

empirical analysis showed that a rise in cigarette prices has lowered the smoking rate

and the daily cigarette consumption for both men and women. If the sample was

restricted to smokers only, the increase in cigarette prices reduced men's cigarette

consumption, but failed to incentivize smoking cessation. On the other hand, if the

sample of non-smokers only was analyzed, the increase in cigarette prices prevented

both men and women from smoking and even reduced the amount of cigarette

consumption even though they started smoking. Thus, the decline in smoking rates

after a rise in cigarette prices has resulted from the non-smokers not starting to smoke,

rather than the existing smokers.

Keywords: cigarette price, smoking rate, cigarette consumption, smoking cessation,

smoking prevention

7

Adverse Selection in the Private Surgery and Hospitalization Health

Insurance

Chia-Ling Ho1

Gene C. Lai2

Abstract

This study investigates adverse selection using private surgery and hospitalization

health insurance policies in Taiwan as a sample. We find that a significant and

positive relation between coverage and occurrence of claim and frequency of claim,

indicating insureds with high-coverage are more likely to have high occurrence of

claim and frequencies of claim. Our evidence also shows that insureds with

high-coverage are more likely to have higher claim payments (number of days of

hospitalization) than insureds with lower-coverage. In other words, adverse selection

exists. We also find the requirement of physical examination can help to alleviate the

severity of adverse selection. The evidence of interaction effects between physical

examination and highcoverage shows that insureds with high-coverage who go

through physical examinations have less claim payments than those who do not go

through physical examination. This evidence indicates that physical examination can

mitigate adverse selection.

1 Department of Risk Management and Insurance, Tamkang University, 151

Ying-Chuan Rd., Tamsui, New Taipei City 251, Taiwan, Tel: 886-2-26215656

ext.2865, [email protected] 2 Belk College of Business, James J. Harris Chair/Scholar of Risk Management and

Insurance of the Department of Finance, University of North Carolina at Charlotte,

Charlotte, NC, 28223, Tel: +1-704- 687-7013, Fax: +1-704-687-1412, [email protected]

8

An Ambiguity Measure under EUUP and Its Application to a

Portfolio Problem.

Hideki Iwaki1

1Faculty of Business Administration, Kyoto Sangyo University

December 9, 2018

Abstract

Ordering alternatives by their degree of ambiguity is crucial in decisionmaking under

Knightian uncertainty. This paper derives a measure of ambiguity which quantifies

the degree of ambiguity under expected utility with uncertain probability (EUUP) by

Izhakian (2017a). Since EUUP can completely distinguish tastes from beliefs and risk

from ambiguity, the ambiguity measure is independent of risk and tastes. With the

measure, the degree of ambiguity can be measured by the volatility of uncertain

probabilities just as the degree of risk can be measured by the volatility of outcomes.

Although Izhakian (2017b) also derives an ambiguity measure based on the volatility

of uncertain probabilities, ours is more flexible and it discriminates between

ambiguity in favorable outcomes and it in unfavorable ones. Based on the measure,

we also discuss effects of ambiguity on financial investments through comparative

statics.

Keywords: Ambiguity measurement, Knightian uncertainty, EUUP, Portfolio

selection.

9

Multi-population Mortality Modeling: When the Data is Too Much

and Not Enough

Richard D. MacMinn, Ko-Lun Kung, Weiyu Kuo, Chenghsien Tsai3

November 12, 2018

Abstract

We apply the framework of the approximate factor model to tackling the issues

of large dimensions, conditional cross-section heteroskedasticity, conditional

time-series heteroskedasticity, and conditional correlations among idiosyncratic errors

that emerge when modeling multi-population mortality rates. The empirical tests on

45 individual populations show that incorporating these heteroskedasticities and

correlations into estimations improves insample _ttings. We demonstrate such

incorporations lead to superior in-sample _tting to well-known single- and

multi-population models using _ve-population mortality data. They result in

consistent outperformance in out-of-sample forecasting as well.

3 Corresponding author: [email protected]; tel & fax: +886-2-29369647. The author is grateful to the Ministry

of Science and Technology (project number: 102-2410-H-004-027-MY3 and 105-2410-H-004 -070 -MY3) and the

Risk and Insurance Research Center for their _nancial support as well as to the California State University,

Northridge (CSUN) and the California State University, Fullerton (CSUF) for the kind supports during the visit

of the author. A major portion of the research was completed while the author was visiting CSUN and CSUF.

10

FCU RMI Workshop Program: (at Room 804A)

Each presentation: 30 min. (Presentation: 20 min. Discussant: 5 min. Q&A: 5

min.)

o Section 1 (moderator: Chu Shiu Li (National Kaohsiung University of Science

and Technology)):

o 10:30: Presentation 1

o Title: The Affordable Care Act and Medical Malpractice

Insurance Industry: A Generalized Synthetic Control Method

o Presenters: Jingshu Luo (Temple University)

o Discussant: Chu Shiu Li (National Kaohsiung University of

Science and Technology)

o 11:00: Presentation 2

o Title: Consumer Benefit and Design of Long-Term Care

Annuity Product

o Presenter: Yen-Chih Chen (Feng Chia University)

o Discussant: Karen C. Su (National Taichung University of

Science and Technology)

o 12:00: Lunch

o Section 2 (moderator: Nathan Liu (Feng Chia University)):

o 13:30: Presentation 3

o Title: A preliminary study of long-short strategies formulated

by size, value, momentum or contrarian effects and by the

income measures of operating profitability and gross

profitability in the Taiwan stock market

o Presenter: Jai-Jen Wang (Feng Chia University)

o Discussant: Nathan Liu (Feng Chia University)

o 14:00: Presentation 4

o Title: Insurance Development and Economic Growth: Evidence

from Asian Advanced and Emerging Countries

o Presenter: Hung-Yu Cheng (Feng Chia University)

o Discussant: Vincent Chang (Feng Chia University)

o 14:30: Presentation 5

o Title: Corporate Governance and the Stock performance

o Presenter: Chen-Chen Yang (Feng Chia University)

o Discussant: Jai-Jen Wang (Feng Chia University)

11

o 15:00 Coffee break

o Section 3 (moderator: Wei-Feng Hung (Feng Chia University)):

o 15:30: Presentation 6

o Title: Currency Risk Hedging for US Stock Investment from

Taiwan Perspective

o Presenter: Chien-Hsing Chou (Feng Chia University)

o Discussant: Wei-Feng Hung (Feng Chia University)

o 16:00: Presentation 7

o Title: An Analysis of the Return and Risk of Self-Annuitization

and Dollar-Cost Averaging

o Presenter: Meng-Sung Hsieh (Feng Chia University)

o Discussant: Yen-Chih Chen (Feng Chia University)

18:00: Dinner at Insky Hotel

12

The Affordable Care Act and Medical Malpractice Insurance

Industry: A Generalized Synthetic Control Method

Jingshu Luo

Temple University

Abstract

This paper studies the impact of Medicaid expansion from the Affordable Care Act

(ACA) on the medical malpractice insurance industry under the background of tort

reforms. Medicaid expansion increases millions of new insureds to the healthcare system

while the physician supply is roughly the same. The sudden increase in the demand for

healthcare service might place pressure on medical practitioners and increase the medical

malpractice risk. Using the generalized synthetic control method, this paper shows that

states adopting Medicaid expansion experience higher economic loss ratios and economic

loss incurred than without expansion. Unobservable common trends such as the

underwriting cycle cannot explain the results. In addition, this paper shows that although

tort reforms, especially caps on noneconomic damages, have reduced medical malpractice

losses in the reformed states significantly, they did not offset the impact of Medicaid

expansion.

Key Words: The Affordable Care Act, Tort Reforms, Medical Malpractice Insurance,

The Generalized Synthetic Control Method

13

Consumer Benefit and Design of Long-Term Care Annuity Product

Yen-Chih Chen

Assistant Professor,The Bachelor’s Degree Program in Financial Engineering and

Actuarial Science, College of Finance, Feng Chia University, Taiwan

Jennifer L. Wang

Professor, Department of Risk Management and Insurance

National Chengchi University, Taiwan

Ming-hua Hsieh

Associate Professor, Department of Risk Management and InsuranceNational

Chengchi University, Taiwan

Abstract

This paper discuss the product design of Long-term care annuity (LCA), which provides

comprehensive protection for the longevity risk. With the effect of lowering adverse

selection cost, LCA products can provide a cheaper retirement product with higher

coverage. In this paper, we explore the consumer benefits and lowering adverse

selection cost effect under different product designs of LCA. LCA products can attract

both annuity and long-term care insurance policyholders because policyholders in the

annuities market with relative high risk are with relative low risk in the long-term care

insurance market. To estimate the benefits of LCA product design, we generate three

health state models of transition probability matrices: good health, average health and

poor health under continuous-time Markov process assumption. Our results show that a

good design of LCA can provide cheaper longevity risk protection with higher coverage

than traditional insurance products and thus create a win-win situation for both consumers

and insurers.

Keywords: Long-term Care Insurance, Annuity, Product Design, Long-term Care

Annuity

14

A preliminary study of long-short strategies formulated by size, value,

momentum or contrarian effects and by the income measures of

operating profitability and gross profitability in the Taiwan stock

market

Richard Lu4

Jai-Jen Wang5

Abstract

Cross-sectional characteristics of stocks such as market value, market-to-book ratio,

and accumulated past return can be applied to formulate equity portfolios, which

relate to the well-known size, value, and momentum or contrarian strategies in

literature. Alternatively, income measures in financial statements drive investors in

stock markets to buy or sell in an intuitive way. This study applies these types of

information in the formation period to formulate long-short strategies and investigates

their return and risk profiles in the holding period afterward. According to the

empirical results in the Taiwan market during 2008/1~2018/6 given different lengths

of holding period and different equity segments, strategies filtered by the income

measure of gross profitability outperform the counterparts filtered by the operating

profitability. Moreover, while the momentum or contrarian effect is not, the size and

value effects are helpful to improve the performance of long-short strategies filtered

by the gross profitability only in the double filtered setting.

4 Corresponding author, Department of Risk Management andInsurance, FengChia

University, No. 100 Wenhwa Rd., Situn, Taichung, Taiwan 40724. Tel.:

+886-04-24517250x4132, Fax: +886-04-424512176, e-mail:[email protected]. 5 Department of Finance, FengChia University, No. 100 Wenhwa Rd., Situn,

Taichung, Taiwan 40724. Tel.: +886-04-24517250x4162, Fax: +886-04-24513796,

e-mail:[email protected].

15

Insurance Development and Economic Growth: Evidence from Asian

Advanced and Emerging Countries

Gengnan Chiang6, Hung-yu Cheng7

Abstract

The purpose of this study is to explore the correlation between insurance

development and economic growth among advanced and emerging countries in Asia. The

proportion of gross premium to the gross domestic product (known as insurance

penetration) and the insurance premium per capita (known as insurance density) indicate

the country’s level of development of insurance.

To verify the relationship between insurance development and economic growth, we

analyze a set of data related to 11 Asian countries from 1990 to 2017. These Asian

countries comprise of advanced and emerging countries. We adopt panel least squares

regression as the research method to analyze the relationship between the insurance

indicators and real GDP per capita (proxy variable of economic growth). The obtained

results are compared with those from other markets.

Primary evidences deriving from empirical analyses are shown as follows:

When insurance density is used as the insurance development measurement indicator, life

insurance is positively correlated with the economic growth of advanced countries,

emerging countries and the overall sample countries. Chen et al. (2012), Dhiab and

Tunisia (2015), Din et al. (2017b), Han et al. (2010) and Sibindi (2014) also have the

same results. Non-life insurance exhibits positive correlation with the economic growth of

advanced countries, emerging countries and the overall sample countries in Asia. Dhiab

and Tunisia (2015), Din et al. (2017b) and Han et al. (2010) also have the same results.

When insurance penetration is used as the insurance development measurement

indicator, life insurance positively affects the economic growth of emerging countries and

6 Gengnan Chiang

Associate Professor, Dept. of Finance

No. 100, Wenhwa Rd., Seatwen, Taichung, Taiwan 40724, R.O.C.

Phone:+886-4-24517250

Email:[email protected] 7 Hung-yu Cheng (oral)

Ph.D. Candidate, Ph.D. Program of Finance, Feng Chia University, Taichung, Taiwan.

No. 100, Wenhwa Rd., Seatwen, Taichung, Taiwan 40724, R.O.C.

Phone:+886-4-24517250

Email: [email protected]

16

the overall sample countries in Asia. The result is similar to the positive effect of life

insurance penetration on economic growth in the studies conducted by Alhassan and

Fiador (2014), Arena (2008), Beck et al. (2003), Ouédraogo et al. (2016) and Webb et al.

(2002). Non-life insurance exhibits positive effect on economic growth of advanced

countries, emerging countries and the overall sample countries in Asia. The result is

similar to the positive effect of life insurance penetration on economic growth in the

studies conducted by Haiss and Sümegi (2008), Kjosevski (2011) and Zouhaier (2014).

In summation, the relationship between insurance and economic growth is intricate.

To clarify this intricate relationship, the present study uses macroeconomic variables,

such as GDP deflator (annual %), gross fixed capital formation (% of GDP), market

capitalization of listed domestic companies (% of GDP), stocks total traded value (% of

GDP), exports and imports of goods and services (% of GDP), inflation GDP deflator

(annual %), central government total debt value (% of GDP) and unemployment total

value (% of total labor force) as control variables to strengthen the reliability of evidence

in this study. Although, the literature exploring the relationship between insurance and

economic growth is rare in Area. The evidence of this study makes up for the lack of

literature in this area.

Keywords: Asia, Economic growth, Life insurance, Non-life insurance, Insurance

Penetration, Insurance Density.

17

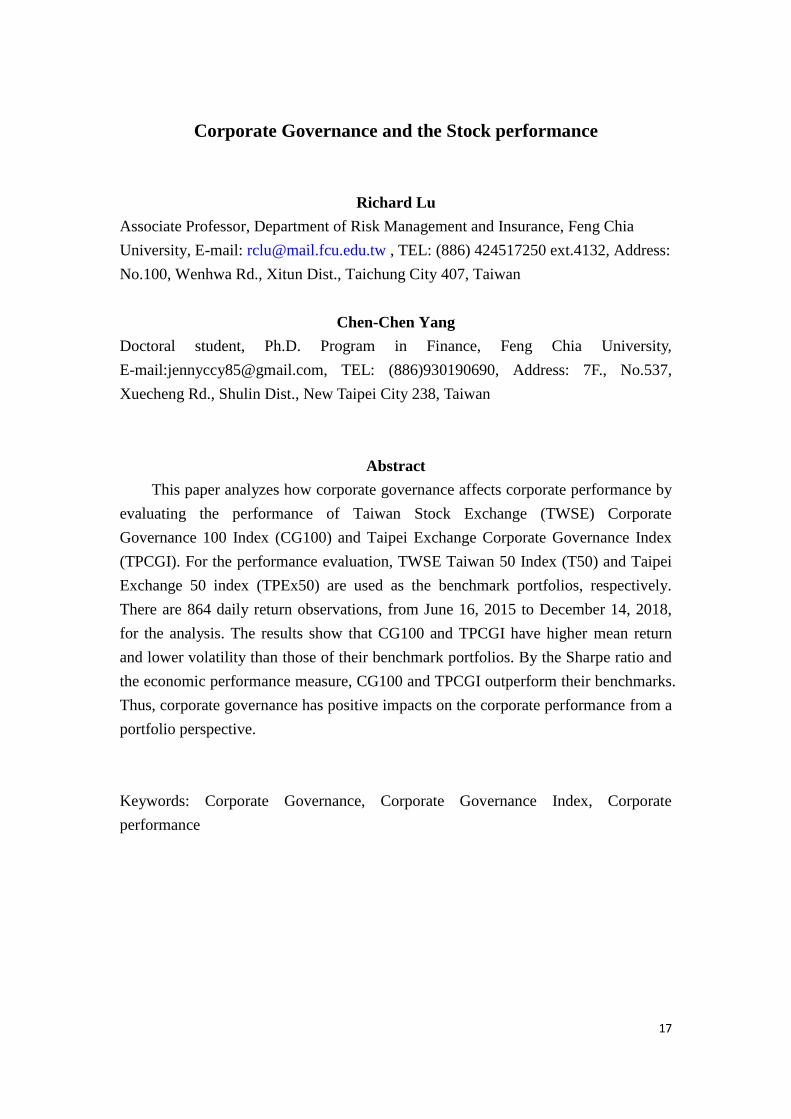

Corporate Governance and the Stock performance

Richard Lu

Associate Professor, Department of Risk Management and Insurance, Feng Chia

University, E-mail: [email protected] , TEL: (886) 424517250 ext.4132, Address:

No.100, Wenhwa Rd., Xitun Dist., Taichung City 407, Taiwan

Chen-Chen Yang

Doctoral student, Ph.D. Program in Finance, Feng Chia University,

E-mail:[email protected], TEL: (886)930190690, Address: 7F., No.537,

Xuecheng Rd., Shulin Dist., New Taipei City 238, Taiwan

Abstract

This paper analyzes how corporate governance affects corporate performance by

evaluating the performance of Taiwan Stock Exchange (TWSE) Corporate

Governance 100 Index (CG100) and Taipei Exchange Corporate Governance Index

(TPCGI). For the performance evaluation, TWSE Taiwan 50 Index (T50) and Taipei

Exchange 50 index (TPEx50) are used as the benchmark portfolios, respectively.

There are 864 daily return observations, from June 16, 2015 to December 14, 2018,

for the analysis. The results show that CG100 and TPCGI have higher mean return

and lower volatility than those of their benchmark portfolios. By the Sharpe ratio and

the economic performance measure, CG100 and TPCGI outperform their benchmarks.

Thus, corporate governance has positive impacts on the corporate performance from a

portfolio perspective.

Keywords: Corporate Governance, Corporate Governance Index, Corporate

performance

18

Currency Risk Hedging for US Stock Investment from Taiwan Perspective

Richard Lu

Associate Professor, Department of Risk Management and Insurance, Feng Chia

University, E-mail: [email protected] , TEL: (886) 424517250 ext.4132, Address:

No.100, Wenhwa Rd., Xitun Dist., Taichung City 407, Taiwan

Chien-Hsing Chou

Doctoral student, Ph.D. Program in Finance, Feng Chia University, E-mail:

[email protected] , Address: No.100, Wenhwa Rd., Xitun Dist., Taichung

City 407, Taiwan

Abstract

This paper studies the proxy hedging for US stock investment from Taiwan

investors’ perspective. To hedge the US currency risk, we use the US dollar, the

Japanese yen, the Australia dollar, the Euro, and the Swiss franc. The

minimum-variance model and the minimum-riskiness model are used for finding out

the optimal proxy hedging demand for currencies. The full sample period studied are

from May 1999 to Oct 2018.The study is also conducted on two subperiods, the

first-half and second-half periods. Both models suggest not to hedge the currency risk

during the full period, and the second subperiod. This is against some people’s

intuition particularly when the US dollar depreciates against Taiwan most of the time

in the second subperiod. In the proxy hedging demand for other currencies, we find

that, under the minimum-variance model, long positions are held for Japanese yen and

Swiss franc, and short positions for the Australia dollar and the Euro. However, under

the minimum-riskiness model, the excess mean return of the currency plays an

important role in hedging the US currency risk. Thus, it creates quite a different proxy

hedging demand for those currencies.

19

An Analysis of the Return and Risk of Self-Annuitizationand Dollar-Cost

Averaging

Richard Lu

Associate Professor, Department of Risk Management and Insurance, Feng Chia

University, E-mail: [email protected] , TEL: (886) 424517250 ext.4132, Address:

No.100, Wenhwa Rd., Xitun Dist., Taichung City 407, Taiwan

Meng-Sung Hsieh

Doctoral student, Ph.D. Program in Finance, Feng Chia University, E-mail:

[email protected], Address: No.100, Wenhwa Rd., Xitun Dist., Taichung

City 407, Taiwan

Abstract

The return and risk of Dollar-Cost Averaging (DCA) and Self-Annuitization (SA)

investments are compared with the underlying in this paper. The underlying return which

is assumed to normally distribute isgenerated by Monte Carlo simulations under four

market scenarios across several investment horizons. Because the multiple cash flows of

DCA and SA, the annual internal rate of return is used to measure the DCA and SA

returns. The results show that the mean return of DCAis slightly higher than the

underlying, while the SA is lower, particularly under short investment horizons. They

produce higher return volatility and riskiness than the underlying. The SA has the highest

negative skewness and kurtosis, followed by the DCA. Furthermore, by usingthe

economic performance measure,which can consider the high moments of distribution, the

underlying is the best, and the SA is the worst. This evidence become even more clear

and convincing as the investment horizon increases.