What does the future retail city centre look like? White Paper Shopping Tomorrow Expert Group: Future Retail City Centre 2030 March 2016

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 2

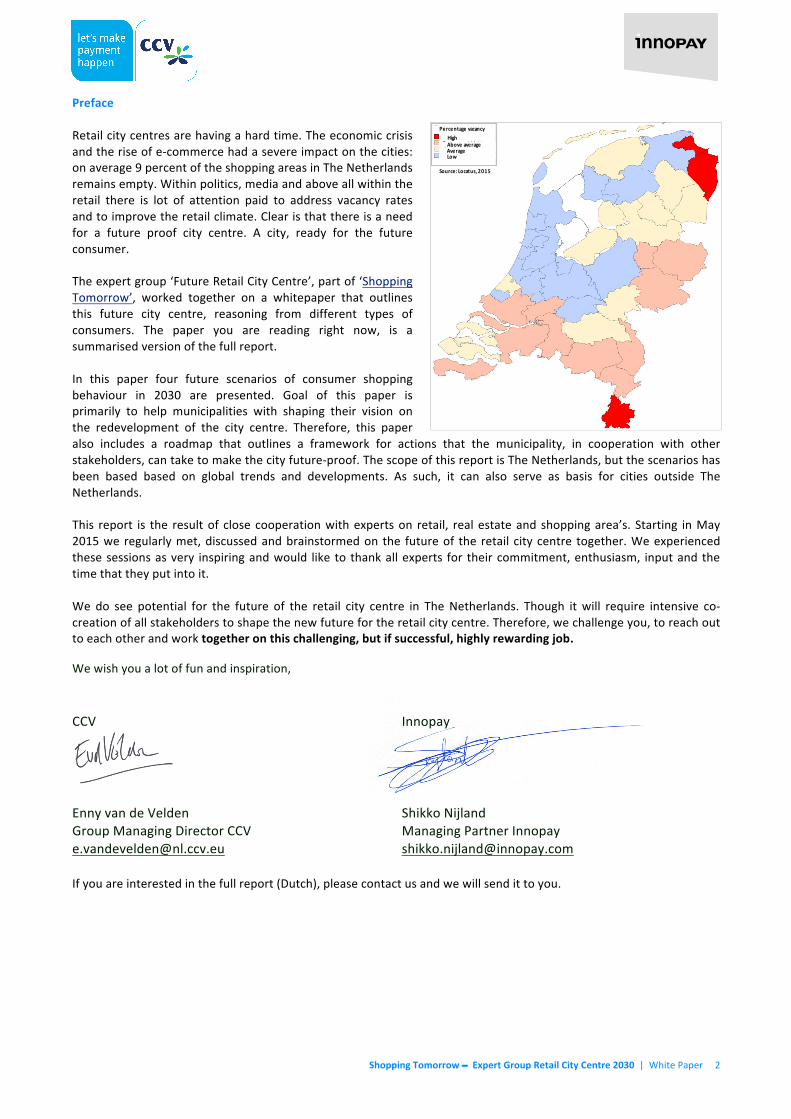

Preface Retail city centres are having a hard time. The economic crisis and the rise of e-‐commerce had a severe impact on the cities: on average 9 percent of the shopping areas in The Netherlands remains empty. Within politics, media and above all within the retail there is lot of attention paid to address vacancy rates and to improve the retail climate. Clear is that there is a need for a future proof city centre. A city, ready for the future consumer. The expert group ‘Future Retail City Centre’, part of ‘Shopping Tomorrow’, worked together on a whitepaper that outlines this future city centre, reasoning from different types of consumers. The paper you are reading right now, is a summarised version of the full report. In this paper four future scenarios of consumer shopping behaviour in 2030 are presented. Goal of this paper is primarily to help municipalities with shaping their vision on the redevelopment of the city centre. Therefore, this paper also includes a roadmap that outlines a framework for actions that the municipality, in cooperation with other stakeholders, can take to make the city future-‐proof. The scope of this report is The Netherlands, but the scenarios has been based based on global trends and developments. As such, it can also serve as basis for cities outside The Netherlands. This report is the result of close cooperation with experts on retail, real estate and shopping area’s. Starting in May 2015 we regularly met, discussed and brainstormed on the future of the retail city centre together. We experienced these sessions as very inspiring and would like to thank all experts for their commitment, enthusiasm, input and the time that they put into it. We do see potential for the future of the retail city centre in The Netherlands. Though it will require intensive co-‐creation of all stakeholders to shape the new future for the retail city centre. Therefore, we challenge you, to reach out to each other and work together on this challenging, but if successful, highly rewarding job. We wish you a lot of fun and inspiration, CCV Innopay

Enny van de Velden Shikko Nijland Group Managing Director CCV Managing Partner Innopay [email protected] [email protected] If you are interested in the full report (Dutch), please contact us and we will send it to you.

Average

Percentage+vacancyHighAbove+average

Low

Source:+Locatus,+2015

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 3

1. Introduction The future of Dutch city centres is a much-‐discussed subject. Visitor numbers are falling, whereas the vacancy rates of shops and offices are rising. Policy-‐makers, retailers and property owners are concerned about the vitality of city centres. City centres are traditionally locations for making non-‐standard purchases and recreational shopping (retail therapy), which are activities relatively sensitive to the economy1. The measured drop in visitors can therefore be partly blamed on the economic crisis. Market research by GfK shows that early 2013, consumer confidence and the propensity to buy reached a record low. This was followed by a slow recovery with positive signals seen returning early 20152 (see figure 1).

Figure 1 Consumer confidence and the propensity to buy in the Netherlands. Source: CBS, from: GfK Shopping Tomorrow Consumer Research, 2015

Although confidence and the propensity to buy appear to be recovering, concerns about the vitality of city centres are far from over. An important development is that more and more often consumers make their purchases online, instead of physically in the shops. A rise can be seen in the share of online purchases across all product groups (figure 2).

1 PBL, 2015 2 Shopping Tomorrow, how do you shop in 2020? GfK, 2015

Consumer)trustWillingness)to)buy

Source:)CBS,)2015

30%

26%

26%

19%

16%

15%

14%

14%

12%

10%

9%

5%

FoodSport & recreation

ToysHealth & care

Media & entertainmentTelecom

Household appliancesConsumer equipment

Shoes & lifestyleClothing

ITLiving & gardening

Growth in online expenditure (Jan-‐Jun 2014)

Figure 2 Online expenditure. Source: GfK Shopping Tomorrow Consumer Research, 2015

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 4

Figure 3 and Figure 4 Online expenditure. Source: GfK Shopping Tomorrow Consumer Research, 2015 Measured in sales and as expected, the share in online shopping compared to offline shopping is rising, from 19 percent in 2015 to 38 percent in 2020 (figures 3 and 4). Consumers experience online shopping as convenient and the wide range of product offering stated as the primary reason to prefer the Internet above shopping physically3. These days the main reason for consumers to opt for the city instead of the Internet is user experience and a personal approach. However, it remains to be seen to what extent city centres continue to have sufficient distinctiveness compared to shopping online and to herewith keep attracting visitors. The way in which consumers want to shop (in the future) differs per type of consumer. On the one hand, we see a trend where the consumer wants to do more and more in a shorter period of time. The rise of the Internet, Smartphones and social media means that people continuously want to engage in social contacts, whereas money still needs to be earned, preferably as dual-‐income couples, and the children still need looking after. Companies increasingly respond to this development by making the shopping experience as convenient and time-‐efficient as possible. Concepts such as the one-‐stop shop and shops in easy-‐to-‐access locations are examples of that. On the other hand, there are consumers who look for distraction. Shopping is experienced as fun. The city centre is perfectly suited to entertain people for a whole day and, in addition to shopping, you can engage in dining, entertainment and culture. However, with the current pace of development in technologies, 3 Shopping Tomorrow, how do you shop in 2020? GfK, 2015

probabilities are that this distraction can also be increasingly offered online. Examples include virtual and augmented reality. The use of such technologies is still in the early days, yet in 2030 this could be common practice. You no longer need to leave your home to view products, or to walk through the shopping aisles. The personal approach, that is so appreciated by consumers in the city centre today, could also be offered online in 2030. During shopping, people are connected with friends through social media, and bloggers and other social influencers determine what the trends for a large group of young people will be. Social platforms interconnect people across the globe with inspiration sought and shared. Online styling advisers can help you compile your wardrobe, making the personal approach an online reality. The wish for personalised products too can be met online. Whereas in the past a consumer merely had a pair of trousers shortened, today he can compile his own muesli online or design his own shoes and have them delivered on his doorstep. The combination of data and technology makes it possible for the entrepreneur to be distinctive in his services or products and to attach a personal service to it.

Online38%

Offline62%

B2C online sharein value 2020

Online19%

Offline81%

B2C online share in value 2015

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 5

These technology-‐driven developments still seem to have little relevance for a large group of (quite often older) consumers. Yet a new generation is arriving who are used to being online all the time, the so-‐called Generation Z, or digital natives. They expect a seamless integration between online and offline events in their lives, also in terms of shopping. Research into the shopping and purchasing behaviour of Generation Z, conducted within the framework of Shopping Tomorrow in 20144, showed that 62 percent of digital natives deemed it important that a shop can be approached in multiple ways and feedback shows that they switch effortlessly between the use of different devices during the customer journey (figure 5).

Purchases are done anywhere, anytime and anyhow. Currently, the city centre shopping area is geared towards this concept to a limited extent only. Retailers indicate that they struggle with this multi-‐channel approach and do not know exactly how to invest5. Retailers do recognise the added value of the use of customer data and the ability to offer the customer customised solutions, thereby creating customer loyalty. And although consumers appreciate personalised offers, it is at odds with the need for privacy. Research by GfK shows that Dutch people, in comparison with other countries, are very privacy-‐sensitive6. The development of a reliable, digital identity can be a solution here. A digital identity enables consumers to choose themselves which data they want to share with retailers. With the rise of the

4 How does Generation Z purchase and pay in 2020? CCV and Innopay, 2014 5 How does Generation Z purchase and pay in 2020? CCV and Innopay, 2014 6 Shopping Tomorrow, how do you shop in 2020? GfK, 2015

Internet of things, such a digital identity becomes even more important. After all, how else would you authorise devices in your home to place orders on your behalf? How these trends that can be seen today, will develop in the future is largely uncertain. Expectations are that the effects of this development on the future of retail and the city centre as a shopping area will be enormous. The rise of the internet during the past 15 years has been a breakthrough technology. Only the future can tell what the breakthrough technology will be of the next 15 years.

These trends and developments feed the discussion on the vitality of the city centre, which includes arguments on a possible change in function of that centre. A change in function involves a lot of stakeholders. Entrepreneurs, property owners, municipalities and consumers all have an interest in the (retail) function of the city centre, and these interests are not always the same. The municipalities play a leading role therein. Hence the municipality is the focal point in this report at which the advice is aimed. The development or redevelopment of a city centre is a complex, extensive and time-‐consuming process. Hence it is important that the discussion on the function of the city extends beyond tomorrow or 2020. And that is why this report paints a picture of the city centre in the year 2030. We do this by means of scenarios. They will be described further in the next chapter.

Orientation Selection Loyalty Transaction Delivery

Channels

Devices

Customer Journey

Figure 5 The customer journey. Source: Bonsing Mann model, Innopay analysis (2014).

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 6

2. Scenarios of the city centre in 2030 All trends and developments referred to in chapter 1 have a direct effect on the retail sector and the function of the city centre. Some trends are characterised by a high level of certainty, whereas with others the extent of the impact on the future of the city centre is uncertain. Since the future cannot be predicted, the choice has been to opt for scenario planning. Scenario planning is a method of creating various future visions on the basis of trends and developments that can be foreseen today. Scenarios are not means for predicting the future, yet a point of reference to handle the uncertainty factor. The creation of different future scenarios gives something to go by and enables every municipality to assess for themselves what actions they need to take should a certain scenario become reality. The trends that are most uncertain and which are expected to have a major impact on the function of the city form the axes that are decisive for the scenarios. This report reasons from the consumer’s perspective. The largest factor of uncertainty is the extent to which consumers, as result of technological and social-‐economic

developments, will still visit the city for shopping or whether they will mainly do so from their own homes. The consumer's orientation (read: preferred shopping location) is therefore the first axis. Orientation of the consumer: one end of the scale is that consumers will do most of their shopping in the city centre. When consumers are oriented outward, physical retailers have right of existence and the city centres will have potential for growth. On the other end of the scale, most of the purchases will be made from home and physical retail will cease to exist in the city centre; empty retail units will dominate the streetscape and a different functional layout for the city will need to be found. The desired user experience is another factor of uncertainty that will have a major impact on how the city centre needs to be organised. The desired user experience manifests itself in the consumer's retail behaviour. This is the second axis. Retail behaviour of the consumer: on the one hand, the consumer can be efficiency-‐oriented and therefore his purchase decisions will be ratio-‐based. This type of consumer is a busy person and prefers not to spend too much time shopping and likes everything to be fast

1. Home as a shop

3. Fun @home

2. Fast & Easy

4. Experience city

Outside Home

A complete experience

Efficient and rational shopping

Figure 6 Scenarios of the consumer in 2030. Source: Retail City Centre expert group, 2015

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 7

and efficient. In that case, the city centre needs to provide proper access. Visits to the city must be fast and fit in within the other activities undertaken by the consumer. Chances are that a large part of the efficiency is found in the online channel. On the other hand, there are consumers who look for a fun experience and who make their purchase decisions on the basis of emotion. This type of consumer loves shopping and likes to make time for it. He likes to be entertained and is looking for interaction. This can be found both online and offline. By combining the two axes, a total of four scenarios are created as to how consumers will be shopping in 2030 (figure 6). It is important to note that it is not the intention for municipalities to opt for one specific (preferred) scenario. As a municipality, they cannot decide for themselves which scenario will become reality. A scenario develops as a result of consumer behaviour and this is difficult to influence. It is important that the municipality thinks about how the city centre must be organised on the basis of each of the four scenarios described, so that a strategy is ready when it becomes clear, between now and fifteen years, what scenario will become reality. The four scenarios will be described from the consumer’s perspective in the following chapters.

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 8

3. Scenario 1: Home as a shop Extensive shopping used to be a favourite leisure activity, yet that era is clearly behind us now. In 2030, the technological possibilities, changes in consumer behaviour and the social rat race mean that the shopping experience has become as much as doing groceries. And doing the groceries in this scenario has been fully integrated in the domestic domain. The consumer makes rational choices, minimises his efforts (time spent) and is used to retailers and manufacturers knowing his personal wishes and serving these to a maximum extent. Consumers have their own SMART home platform, in which the family lifestyle, preferences and desires are communicated to only these retailers and manufacturers who are trusted. As a result, retailers can make customised proposals and offer products, entirely in line with the consumer's expectations. All smart devices at home mean that the consumer no longer needs to leave his home. The refrigerator orders the groceries when running out, people will have full-‐length virtual mirrors and the 3D printer can just as easily print products itself. A global retail world has been formed in which the consumer is no longer limited by the borders of his national country. Purchases are made online, where the choice is enormous. Global players such as Amazon have conquered the European market. Placing orders in China has now become just as easy with deliveries arriving promptly and relatively low prices. This has become logistically possible as drones have become commonly accepted by now. The power of retailers is declining to the advantage of intermediaries (e.g.

providers of home shopping platforms and eID systems) who manage the customer data.

In addition to high-‐tech technology making life easy, the modern mobile supermarket on-‐demand-‐service is efficient and handy too. They will personally bring the goods to the door at a time that is convenient to the consumer and assist with the installation and any returns. The ageing population and urbanisation mean that such home services are scalable. More and more people need these services and they all live closely together.

Figure 7 Illustration of Scenario 1. Source: Future Retail City Centre, 2015.

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 9

4. Scenario 2: Fast & easy shopping

In this scenario, time is a costly commodity and the consumer wants to do more in less time. The choice for a physical visit to the shop is a rational one, it saves time. All processes surrounding a visit to the city centre and the purchase of products are efficient and are aimed at having the consumer buy more. The mobile phone and other smart devices play a central role therein. It is the device for assisting, informing and directing consumers for making efficient, targeted and rational purchases. Once arrived in the city, the consumer, by means of BLE7 technology, receives notifications of where the product is on offer and, when entering, the consumer is recognised and greeted personally. In the supermarket, an app shows the most efficient route, after all, the refrigerator has already indicated what is needed. In the shops, clothing is no longer fitted, as the mirror automatically shows how it looks on the basis of the biometric profile of the consumer. It is also indicated in what other colours the product is available and suggestions are made for matching products. When having questions, are robots on standby for further assistance. We are looking for a personal approach, yet this does not necessarily need to be provided in the form of human contact. In addition to technology being deployed in order to make the customer journey as convenient as possible, technology also plays a major role in

7 Bluetooth Low Energy

achieving customer intimacy between organisations and their customers. This means that the manner in which the consumer lives his life, makes choices and the dilemmas he experiences are better understood. As a result, and with the help of Big Data, offers can be better geared to the consumers. Although this theme is often linked to the creation of increased distraction, this trend also offers opportunities for the retail industry to respond to consumer wishes/demands more efficiently.

Figure 8 Illustration of Scenario 2. Source: Future Retail City Centre, 2015.

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 10

5. Scenario 3: Fun @ Home The consumer no longer needs to leave his home to experience a fun day of shopping. New technologies provide experience and interaction at home, whilst shopping online. This applies to both young and old. Meanwhile the older generation have en masse, become digitally active and therefore no longer need to leave their homes to do shopping. Globalisation means that the world is only one mouse click away. Trends in New York are ordered directly from the home and delivered. In the case of physical shopping, having a lot of people together in the city centre increases the risk of people buying the same things as someone else, whereas the consumer is increasingly looking for unique products. Based on personal preferences, online experiences can be created geared specifically to individual wishes. The consumer uses social media, among other things, to obtain information on potential purchases. Suggestions are found on platforms such as Pinterest, where consumers share their products and tips with each other en masse. Bloggers and social influencers play an important role as well. Testing and trying new products becomes an integrated part of the customer journey. From audio systems to furniture. Virtual fitting rooms enable the consumer to try items on in his living room. Virtual styling assistants provide advice and come up with suggestions, depending on the weather, the occasion and known preferences. Consumers share their looks via social platforms and other media with friends giving feedback.

Shopping together is a whole new experience by means of Virtual Reality. This involves consumers shopping with like-‐minded people from across the globe. Habituation to experiencing emotions in a virtual environment means the experience becomes more and more identical to the emotional experience of shopping in the year 2015. in addition, sharing products with each other has become common practice. The social component also has a hand in this. Young consumers in particular attach less and less value to owning a product. This particularly applies to functional products such as cars, bicycles, washing machines, DIY tools and garden products.

Figure 9 Illustration of Scenario 3. Source: Future Retail City Centre, 2015.

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 11

6. Scenario 4: Experience city The Internet as purchase site has been fully integrated in the multi-‐channel experience, as part of a customer journey with many physical touch points outside the home. In those places where there is personal contact and consumers can physically touch, feel and try the products, obtain advice and experience them. Consumers want to be entertained in the city for at least half a day. In addition to shopping, they also visit the city for culture, meetings and entertainment. Hence there will be more and more hybrid shops. In addition, shops become bigger and integrate catering establishments and service desks, with many specialist personnel that excels in hospitality and product knowledge. Consumers are looking for unique experiences and also like to see that reflected in the products. Clothing is customised by means of laser devices geared to the biometric profile, with 3D printing aisles that print the customised products. They are located outside the centre, where the square meter price is lower. Everything is aimed at creating valuable memories. Interaction is important in that

regard. There are interactive shopping windows, virtual reality, possibilities to easily track and meet your friends, share online purchases and the consumer is given his personalised offers via his telephone or other smart device.

Figure 10 Illustration of Scenario 4. Source: Future Retail City Centre, 2015.

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 12

7. Co-‐creation by municipalities, retailers, property owners and consumers

The local authorities play a key role in the spatial planning of the city centre, as they can exercise influence in practically every place within the decision chain8. Hence the conclusion of the paper is primarily aimed at towns and cities with a description of steps that can be taken now, as part of the process towards a future-‐proof city centre in 2030. In the full report, a distinction is made between different types of cities. In all scenarios and for all types of cities, close cooperation with all stakeholders involved is of vital importance. In a nutshell, there are 10 steps the local authorities can take:

1. Determine which scenario is becoming reality for the towns and cities; 2. Translate the change in consumer behaviour into impact in general (what does this mean to Dutch towns and

cities) and into implications for own city in particular; 3. Find other towns and cities of the same type, that are dealing with the same scenario and consequences; 4. Develop a (future) vision with regard to the role the local authorities can and want to play as a town or city for

living, working, shopping and/or leisure within the Netherlands; 5. Compile a formal working group that consists of representatives of relevant stakeholders and involve them in the

development of the vision; 6. Translate the vision into a plan of action and a programme for the years to come; 7. Investigate the feasibility and support of the plan of action; 8. Test the plan of action against the working group and ensure this is continued on a regular basis; 9. Have stakeholders record their commitment by means of a letter of intent in order to shape the future-‐proof city

centre together; 10. Appoint an independent project leader who will be responsible for the implementation of the action plan.

8. What's next? Although the Shopping Tomorrow 2016 programme has come to an end, this does not apply to the Future Retail City Centre expert group. The experts show a strong need and ambition to specify the ideas that have been presented in this report. The key question therein is how the city centre can be made future-‐proof and how to make a retail vision based on zoning plans in which the consumer is a moving target. Your contribution is of course much appreciated. And vice versa, the experts like to think along with you on how your city centre can be made future-‐proof. If you are interested in this, feel free to contact us. Enny van de Velden Shikko Nijland Managing Director CCV Group Managing Partner Innopay [email protected] [email protected]

8 PBL, 2015

Shopping Tomorrow − Expert Group Retail City Centre 2030 | White Paper 13

Experts who contributed to this report

Oedsen Boersma SITE Urban development oedsen@site-‐ud.nl

Xander Lub NHTV Breda [email protected]

Gordon Tiemstra Afdeling Buitengewone Zaken gordon@afdelingbuiten gewonezaken.nl

Josje Fiolet Innopay [email protected]

Shikko Nijland Innopay Shikko.nijland@innopay. com

Gino Thuij GfK [email protected]

Daphne Hagen Hogeschool van Amsterdam [email protected]

Eus Peters Nederlandse Detailhandel [email protected]

Enny van de Velden CCV [email protected]

Charlotte Hooijdonk BeBurrs charlotte@hooijdonk management.nl

Jan Willem Speetjens [email protected]

Jesse Weltevreden Hogeschool van Amsterdam [email protected]

Jaap Kaai Emma retail [email protected]

Bart Stek WPM groep [email protected]

Wesley Weerdenburg Glass Shop Wall [email protected]

Paul Kerkhof CCV [email protected]

Martin Pronk Noclichés [email protected]

![arXiv:1305.1332v4 [math.DG] 16 Jun 2015We now state our counting and equidistribution results. We avoid any compactness assumption on M, we only assume that the Bowen-Margulis measure](https://static.cupdf.com/doc/110x72/5e63c3e45346ca7edc4444d1/arxiv13051332v4-mathdg-16-jun-2015-we-now-state-our-counting-and-equidistribution.jpg)

![arXiv:1502.06191v1 [hep-lat] 22 Feb 2015We investigate the phase structure of two-color QCD at both real and imaginary chemical potentials (µ), performing lattice simulations and](https://static.cupdf.com/doc/110x72/60e6a245ed04070ec45dd6d8/arxiv150206191v1-hep-lat-22-feb-2015-we-investigate-the-phase-structure-of-two-color.jpg)