© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Accounting for ReceivablesChapter

99

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Learning ObjectivesLearning Objectives

1. Recognize Accounts Receivable

2. Valuing Accounts Receivable Bad debt allowance & Bad debt expense

3. Notes Receivable

4. Disposing of Receivables

5. Decision Analysis: Accounts Receivable Turnover

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

1. Recognizing Accounts Receivable- Accounts Receivable

1. Recognizing Accounts Receivable- Accounts Receivable

Amounts due from customers for credit sales.

Credit sales require:• Maintaining a separate

account receivable for each customer.

• Accounting for bad debts that result from credit sales.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

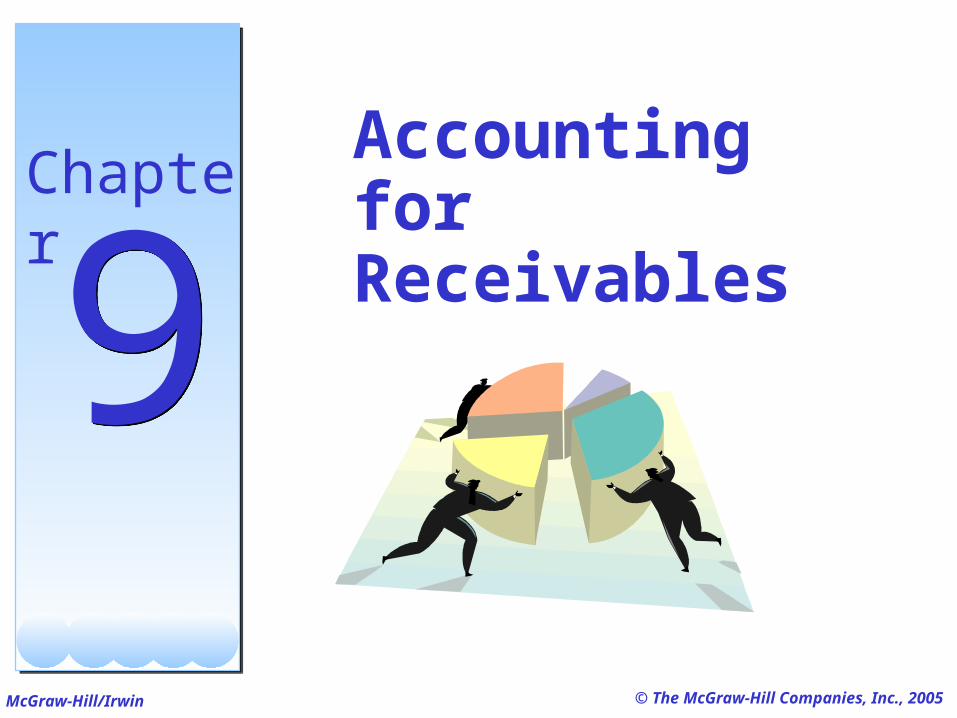

$20.5 Mil.

$92.2 Mil.

$6,785 Mil.

$97.4 Mil.

As a percentage of total assets

1. Recognizing Accounts Receivable- Firms’ percent assets in Account receivables

1. Recognizing Accounts Receivable- Firms’ percent assets in Account receivables

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

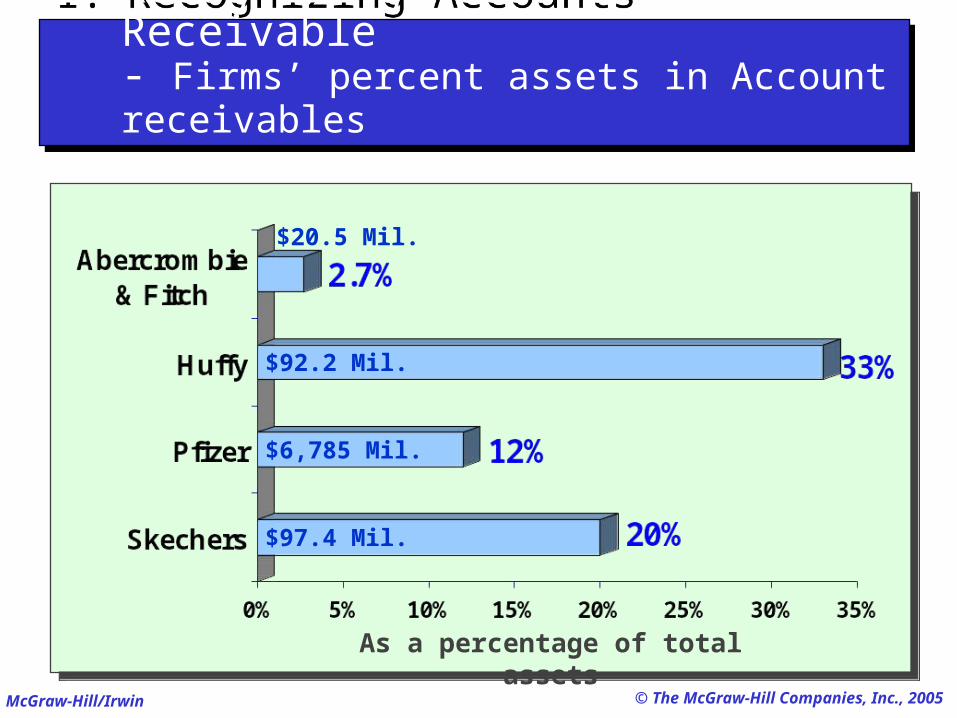

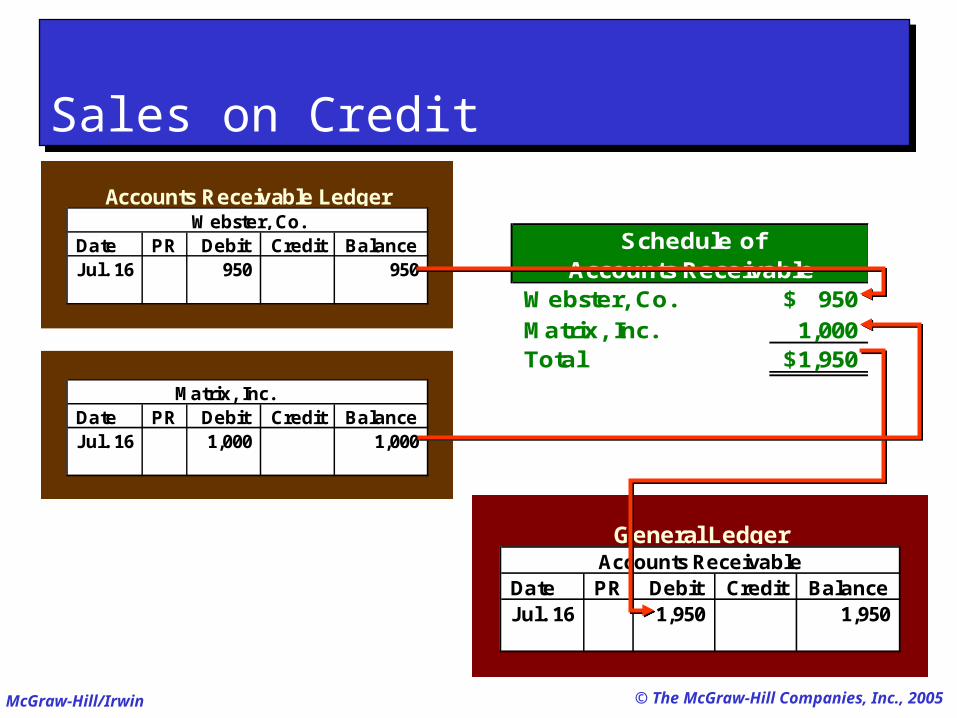

On July 16, Barton, Co. sells $950 of merchandise on credit to Webster, Co., and $1,000 of merchandise on account to Matrix, Inc.

On July 16, Barton, Co. sells $950 of merchandise on credit to Webster, Co., and $1,000 of merchandise on account to Matrix, Inc.

1. Recognizing Accounts Receivable - Sales on Credit

1. Recognizing Accounts Receivable - Sales on Credit

Jul. 16 Accounts Receivable - Webster 950 Sales 950

To record credit sales to Webster Co.

Accounts Receivable - Matrix 1,000 Sales 1,000

To record credit sales to M atrix, Inc.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

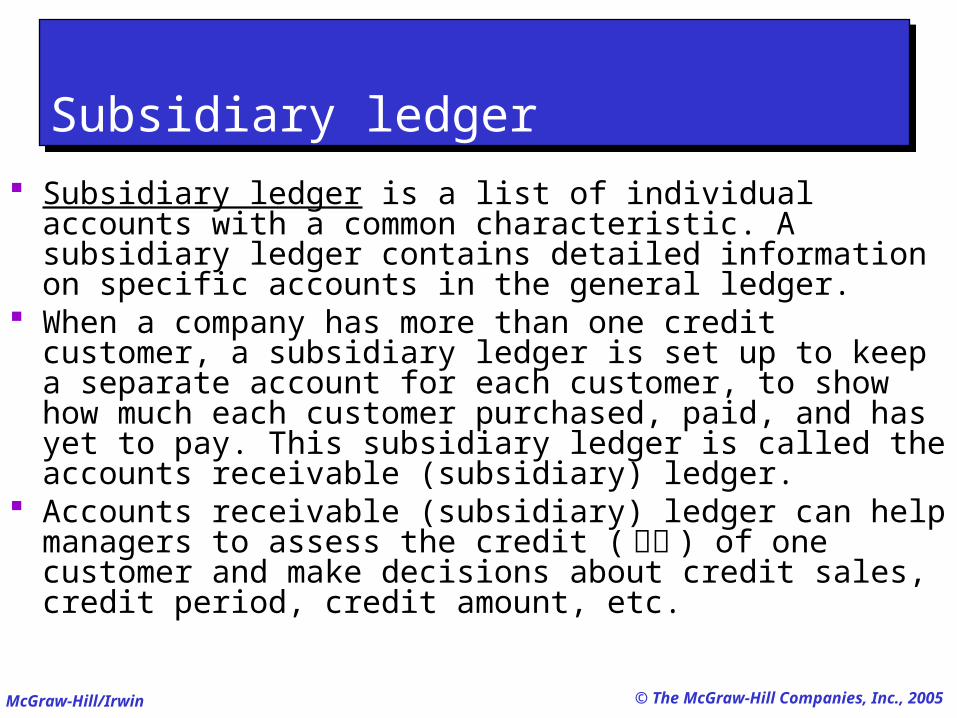

Subsidiary ledgerSubsidiary ledger

Subsidiary ledger is a list of individual accounts with a common characteristic. A subsidiary ledger contains detailed information on specific accounts in the general ledger.

When a company has more than one credit customer, a subsidiary ledger is set up to keep a separate account for each customer, to show how much each customer purchased, paid, and has yet to pay. This subsidiary ledger is called the accounts receivable (subsidiary) ledger.

Accounts receivable (subsidiary) ledger can help managers to assess the credit (信用 ) of one customer and make decisions about credit sales, credit period, credit amount, etc.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Subsidiary ledgerSubsidiary ledger

Date PR Debit Credit BalanceJul. 16 xxxx xxxx

General LedgerAccounts Receivable

Date PR Debit Credit BalanceJul. 16 xxx xxx

Accounts Receivable LedgerAccounts Receivable - Mr. A

Date PR Debit Credit BalanceJul. 16 xxx xxx

Accounts Receivable LedgerAccounts Receivable - Mr. C

Date PR Debit Credit BalanceJul. 16 xxx xxx

Accounts Receivable LedgerAccounts Receivable - Mr. B

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Subsidiary ledgerSubsidiary ledger

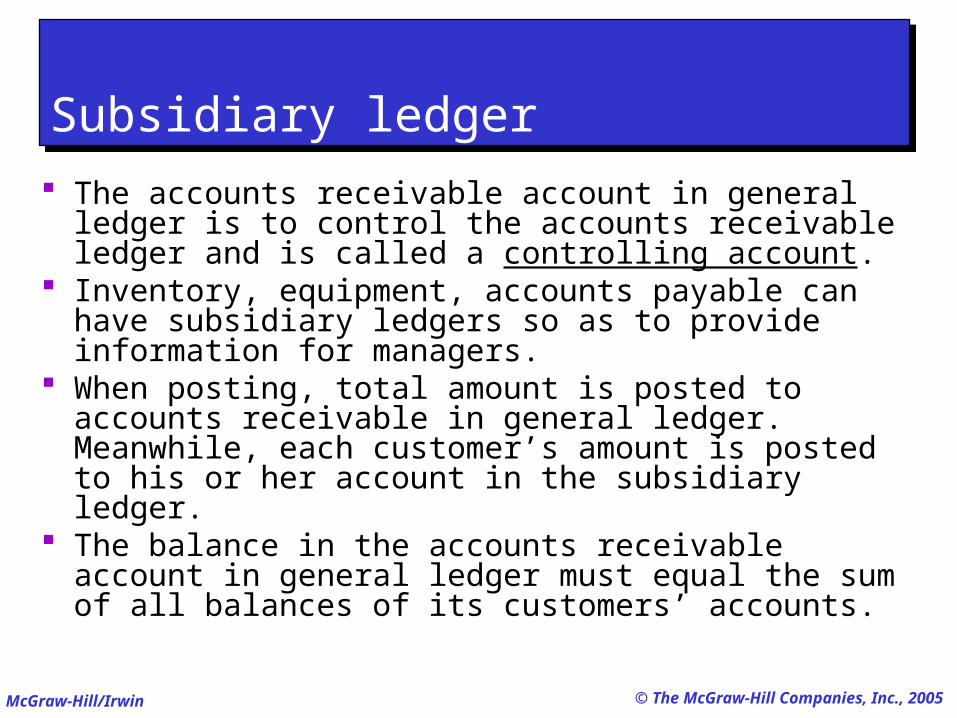

The accounts receivable account in general ledger is to control the accounts receivable ledger and is called a controlling account.

Inventory, equipment, accounts payable can have subsidiary ledgers so as to provide information for managers.

When posting, total amount is posted to accounts receivable in general ledger. Meanwhile, each customer’s amount is posted to his or her account in the subsidiary ledger.

The balance in the accounts receivable account in general ledger must equal the sum of all balances of its customers’ accounts.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

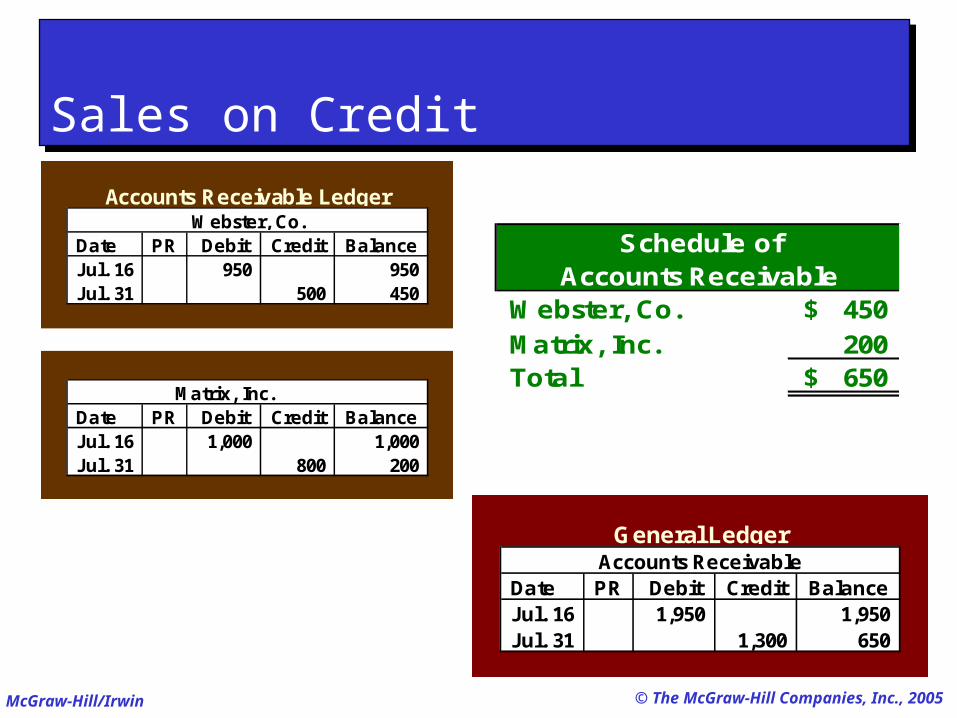

Sales on CreditSales on Credit

Date PR Debit Credit BalanceJul. 16 950 950

Matrix, Inc.Date PR Debit Credit BalanceJul. 16 1,000 1,000

Accounts Receivable LedgerWebster, Co.

Webster, Co. 950$ Matrix, Inc. 1,000 Total 1,950$

Schedule ofAccounts Receivable

Date PR Debit Credit BalanceJul. 16 1,950 1,950

General LedgerAccounts Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

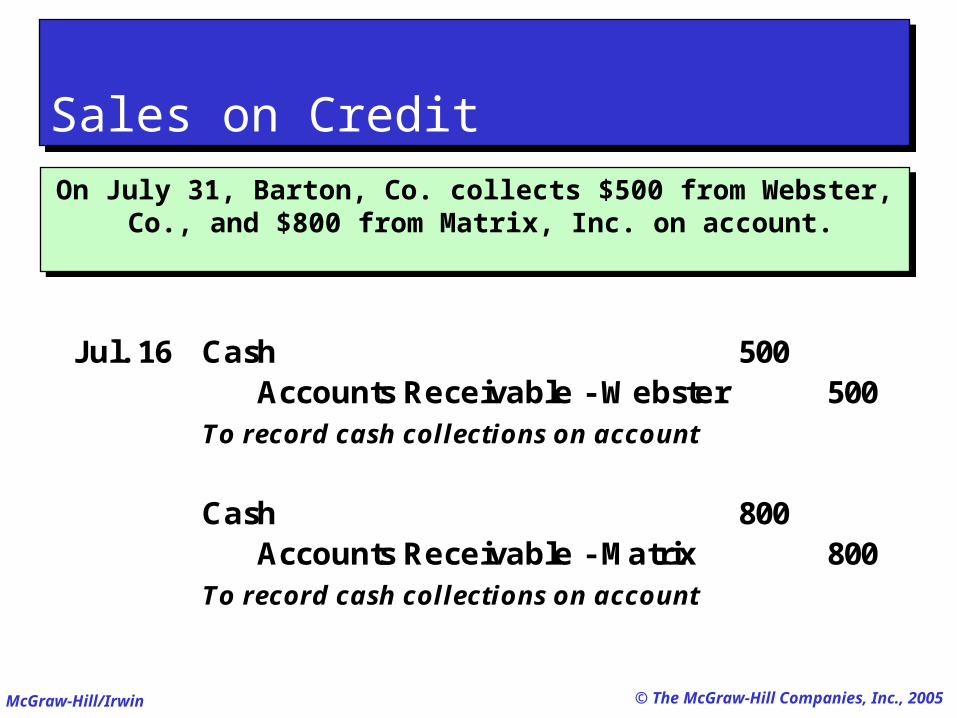

On July 31, Barton, Co. collects $500 from Webster, Co., and $800 from Matrix, Inc. on account.

On July 31, Barton, Co. collects $500 from Webster, Co., and $800 from Matrix, Inc. on account.

Sales on CreditSales on Credit

Jul. 16 Cash 500 Accounts Receivable - Webster 500

To record cash collections on account

Cash 800 Accounts Receivable - Matrix 800

To record cash collections on account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Sales on CreditSales on Credit

Date PR Debit Credit BalanceJul. 16 950 950 Jul. 31 500 450

Matrix, Inc.Date PR Debit Credit BalanceJul. 16 1,000 1,000 Jul. 31 800 200

Accounts Receivable LedgerWebster, Co.

Webster, Co. 450$ Matrix, Inc. 200 Total 650$

Schedule ofAccounts Receivable

Date PR Debit Credit BalanceJul. 16 1,950 1,950 Jul. 31 1,300 650

General LedgerAccounts Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

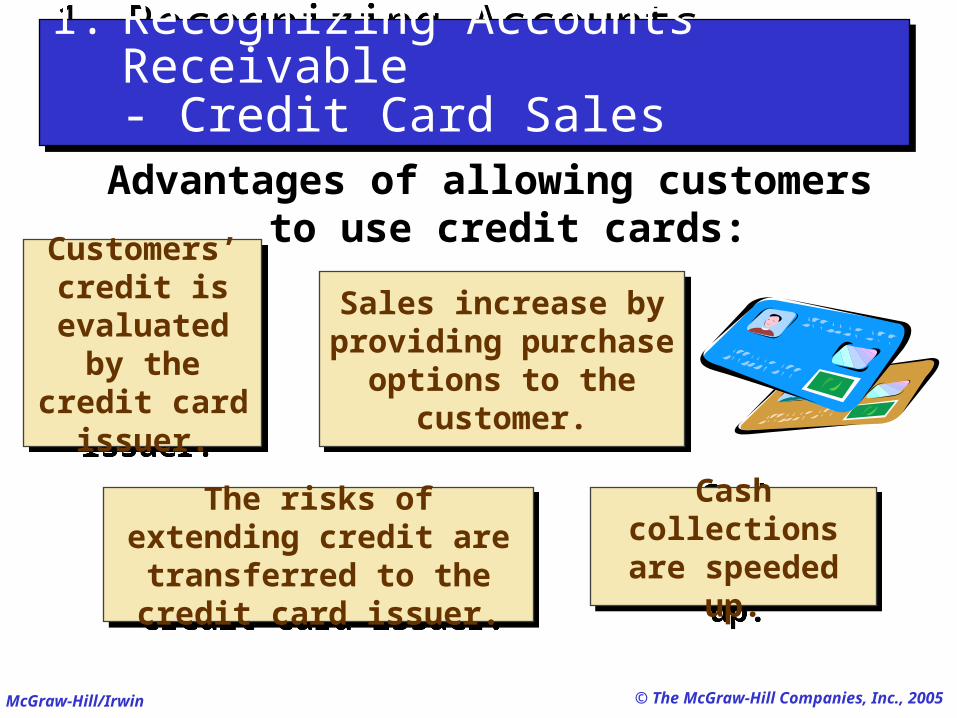

Advantages of allowing customers to use credit cards:

Customers’ credit is

evaluated by the credit

card issuer.

Customers’ credit is

evaluated by the credit

card issuer.

The risks of extending credit are transferred to the credit card issuer.

The risks of extending credit are transferred to the credit card issuer.

Cash collections are speeded up.

Cash collections are speeded up.

Sales increase by providing purchase

options to the customer.

Sales increase by providing purchase

options to the customer.

1. Recognizing Accounts Receivable - Credit Card Sales

1. Recognizing Accounts Receivable - Credit Card Sales

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

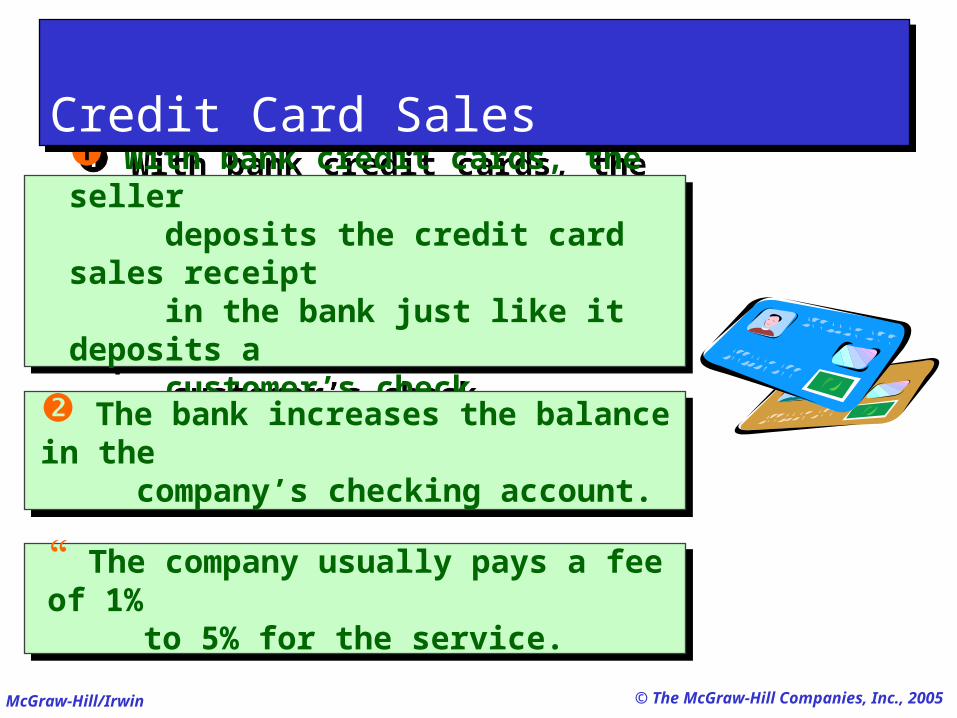

With bank credit cards, the seller deposits the credit card sales receipt in the bank just like it deposits a customer’s check.

With bank credit cards, the seller deposits the credit card sales receipt in the bank just like it deposits a customer’s check.

The bank increases the balance in the company’s checking account.

The bank increases the balance in the company’s checking account.

The company usually pays a fee of 1% to 5% for the service.

The company usually pays a fee of 1% to 5% for the service.

Credit Card SalesCredit Card Sales

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

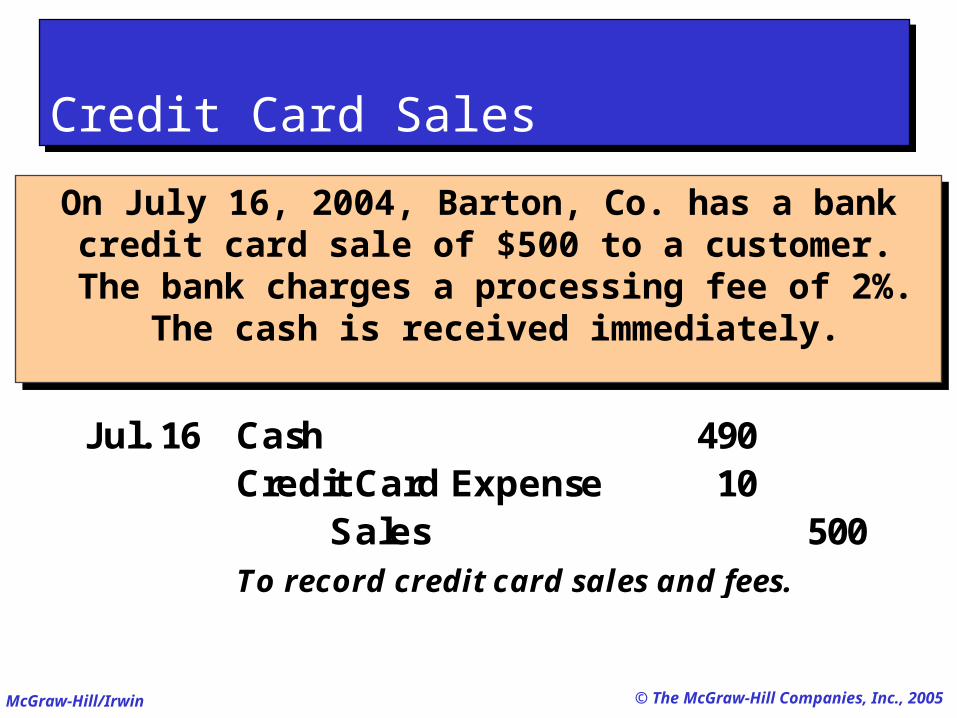

On July 16, 2004, Barton, Co. has a bank credit card sale of $500 to a customer. The bank

charges a processing fee of 2%. The cash is received immediately.

On July 16, 2004, Barton, Co. has a bank credit card sale of $500 to a customer. The bank

charges a processing fee of 2%. The cash is received immediately.

Credit Card SalesCredit Card Sales

Jul. 16 Cash 490 Credit Card Expense 10

Sales 500 To record credit card sales and fees.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

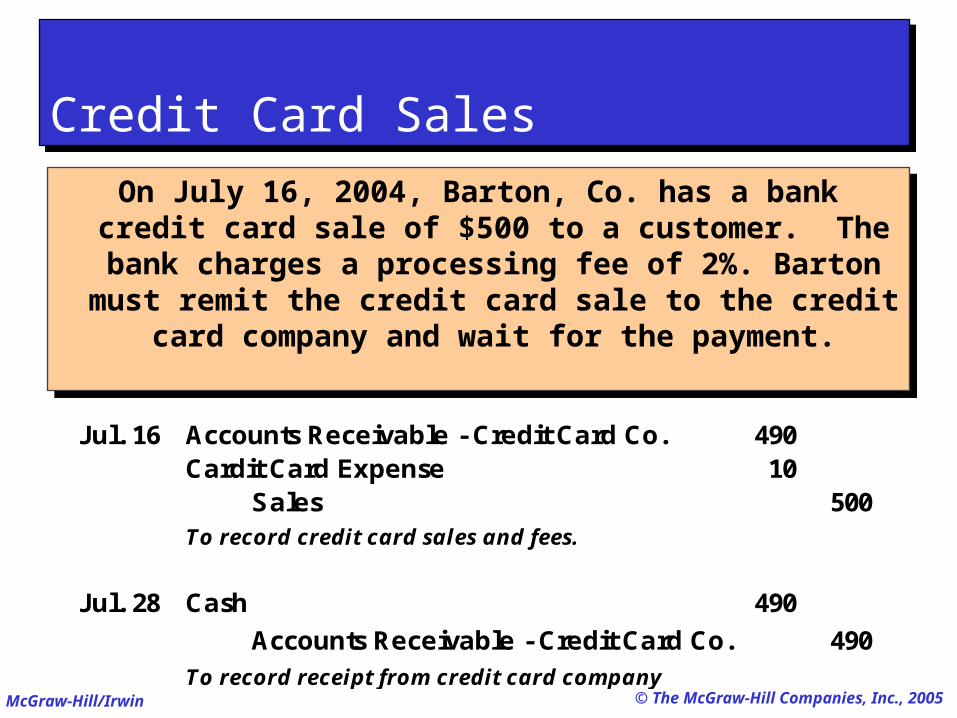

On July 16, 2004, Barton, Co. has a bank credit card sale of $500 to a customer. The bank

charges a processing fee of 2%. Barton must remit the credit card sale to the credit card

company and wait for the payment.

On July 16, 2004, Barton, Co. has a bank credit card sale of $500 to a customer. The bank

charges a processing fee of 2%. Barton must remit the credit card sale to the credit card

company and wait for the payment.

Credit Card SalesCredit Card Sales

Jul. 16 Accounts Receivable - Credit Card Co. 490 Cardit Card Expense 10

Sales 500 To record credit card sales and fees.

Jul. 28 Cash 490

Accounts Receivable - Credit Card Co. 490

To record receipt from credit card company

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Installment Accounts ReceivableInstallment Accounts Receivable

Amounts owed by customers from credit sales for which payment is required in periodic amounts over

an extended time period. The customer is usually charged interest.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

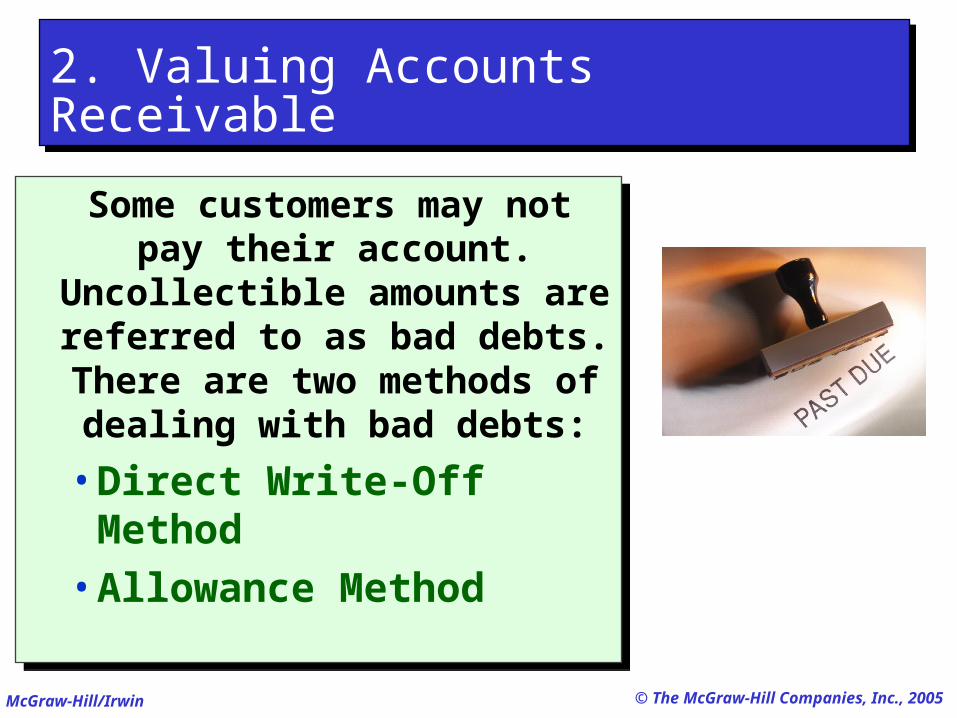

Some customers may not pay their account. Uncollectible amounts are referred to as bad debts. There are two

methods of dealing with bad debts:

• Direct Write-Off Method• Allowance Method

Some customers may not pay their account. Uncollectible amounts are referred to as bad debts. There are two

methods of dealing with bad debts:

• Direct Write-Off Method• Allowance Method

2. Valuing Accounts Receivable2. Valuing Accounts Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

On August 4, Barton determines it cannot collect $350 from Martin, Inc., a

credit customer.

On August 4, Barton determines it cannot collect $350 from Martin, Inc., a

credit customer.

2. Valuing Accounts Receivable - Direct Write-Off Method2. Valuing Accounts Receivable - Direct Write-Off Method

Aug. 4 Bad Debts Expense 350 Accounts Receivable - Martin 350

To write-off uncollectible account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

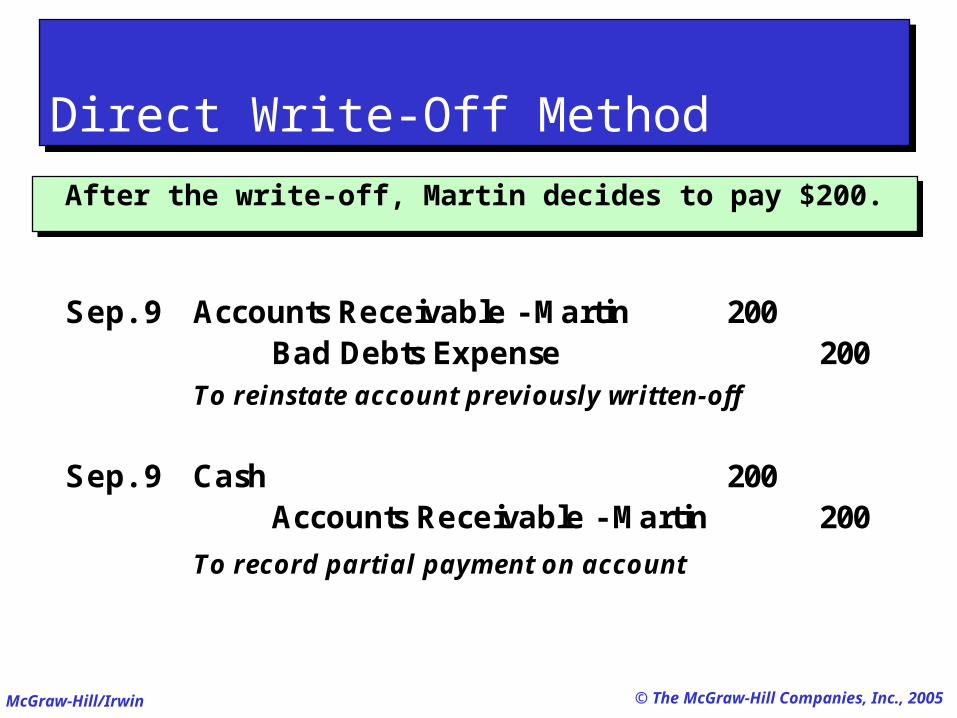

After the write-off, Martin decides to pay $200.After the write-off, Martin decides to pay $200.

Direct Write-Off MethodDirect Write-Off Method

Sep. 9 Accounts Receivable - Martin 200 Bad Debts Expense 200

To reinstate account previously written-off

Sep. 9 Cash 200 Accounts Receivable - Martin 200

To record partial payment on account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

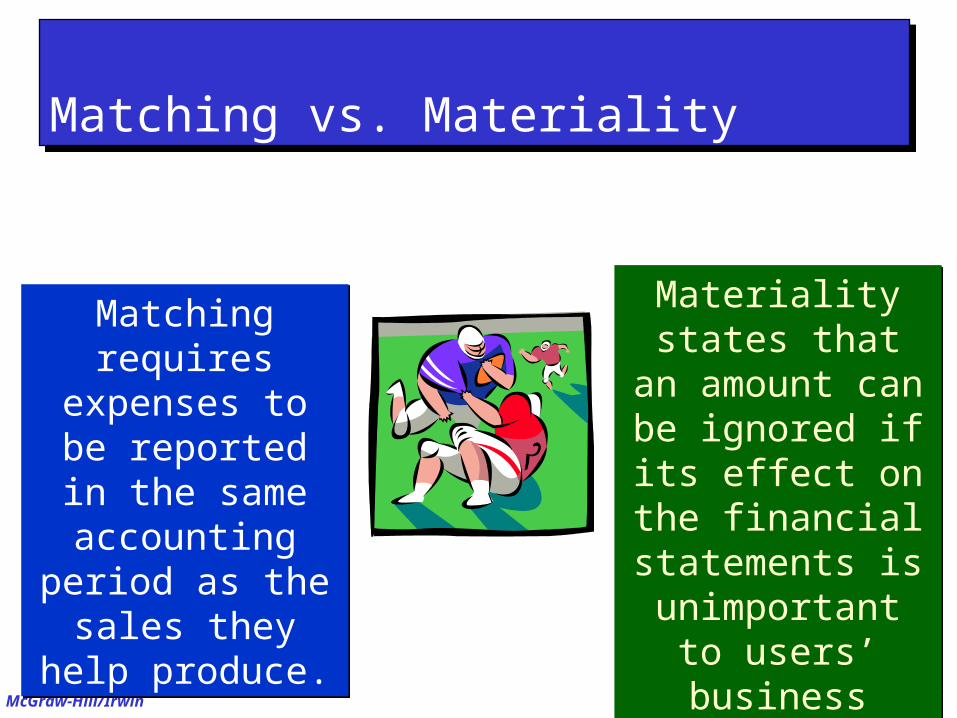

Matching vs. MaterialityMatching vs. Materiality

Matching requires expenses to be

reported in the same accounting period as the sales they help

produce.

Matching requires expenses to be

reported in the same accounting period as the sales they help

produce.

Materiality states that an amount can

be ignored if its effect on the

financial statements is unimportant to users’ business

decisions.

Materiality states that an amount can

be ignored if its effect on the

financial statements is unimportant to users’ business

decisions.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

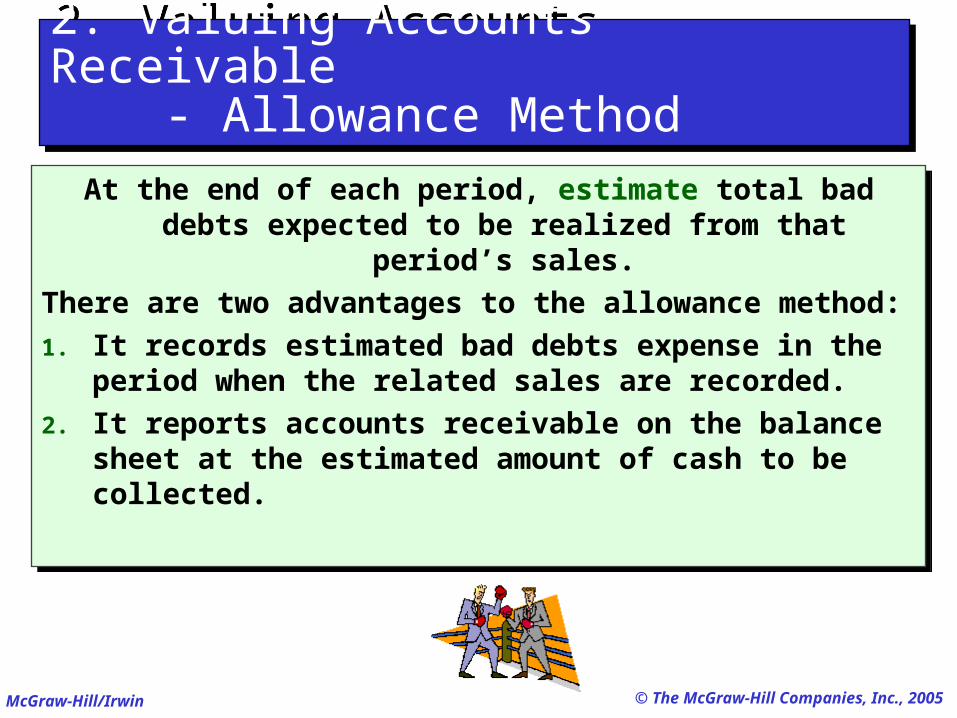

At the end of each period, estimate total bad debts expected to be realized from that period’s sales.

There are two advantages to the allowance method:

1. It records estimated bad debts expense in the period when the related sales are recorded.

2. It reports accounts receivable on the balance sheet at the estimated amount of cash to be collected.

At the end of each period, estimate total bad debts expected to be realized from that period’s sales.

There are two advantages to the allowance method:

1. It records estimated bad debts expense in the period when the related sales are recorded.

2. It reports accounts receivable on the balance sheet at the estimated amount of cash to be collected.

2. Valuing Accounts Receivable - Allowance Method2. Valuing Accounts Receivable - Allowance Method

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

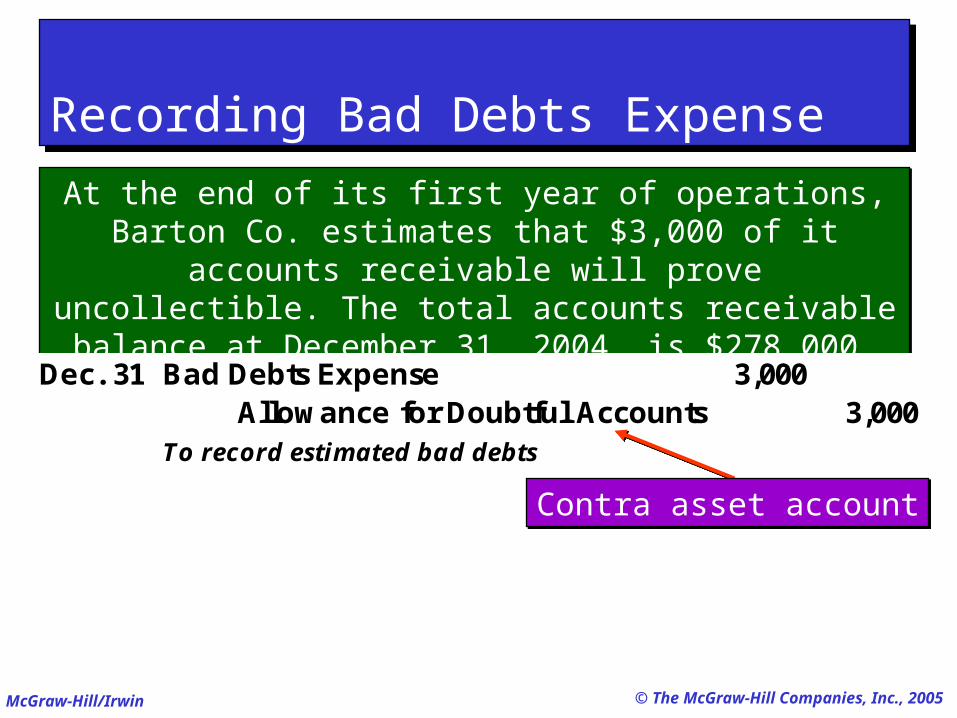

Recording Bad Debts ExpenseRecording Bad Debts Expense

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

Dec. 31 Bad Debts Expense 3,000 Allowance for Doubtful Accounts 3,000

To record estimated bad debts

Contra asset accountContra asset account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

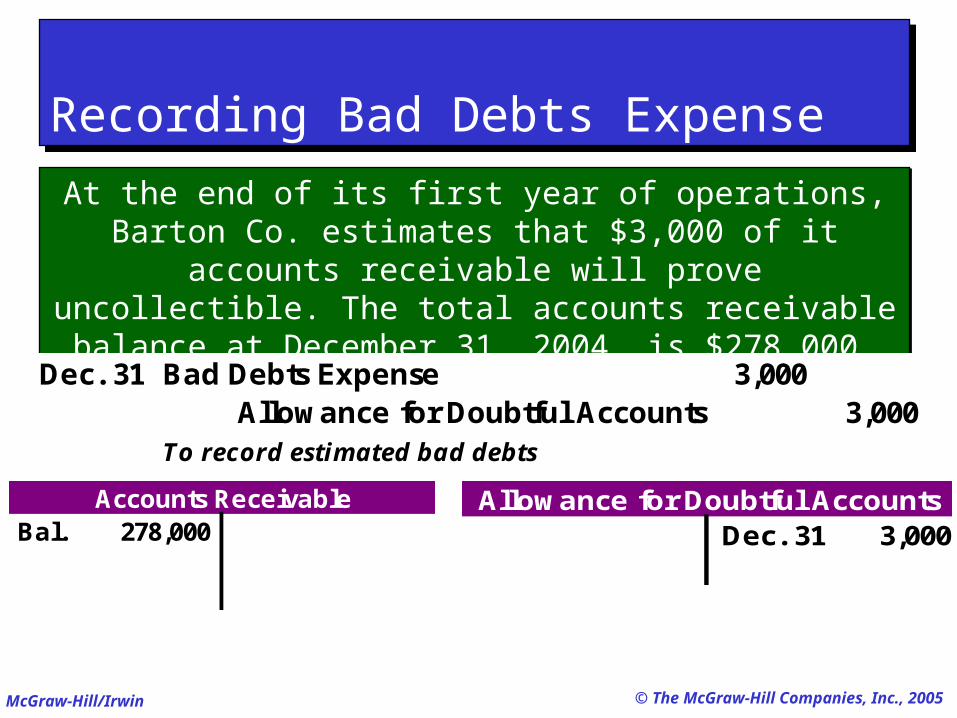

Recording Bad Debts ExpenseRecording Bad Debts Expense

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

Bal. 278,000Accounts Receivable

Dec. 31 3,000Allowance for Doubtful Accounts

Dec. 31 Bad Debts Expense 3,000 Allowance for Doubtful Accounts 3,000

To record estimated bad debts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

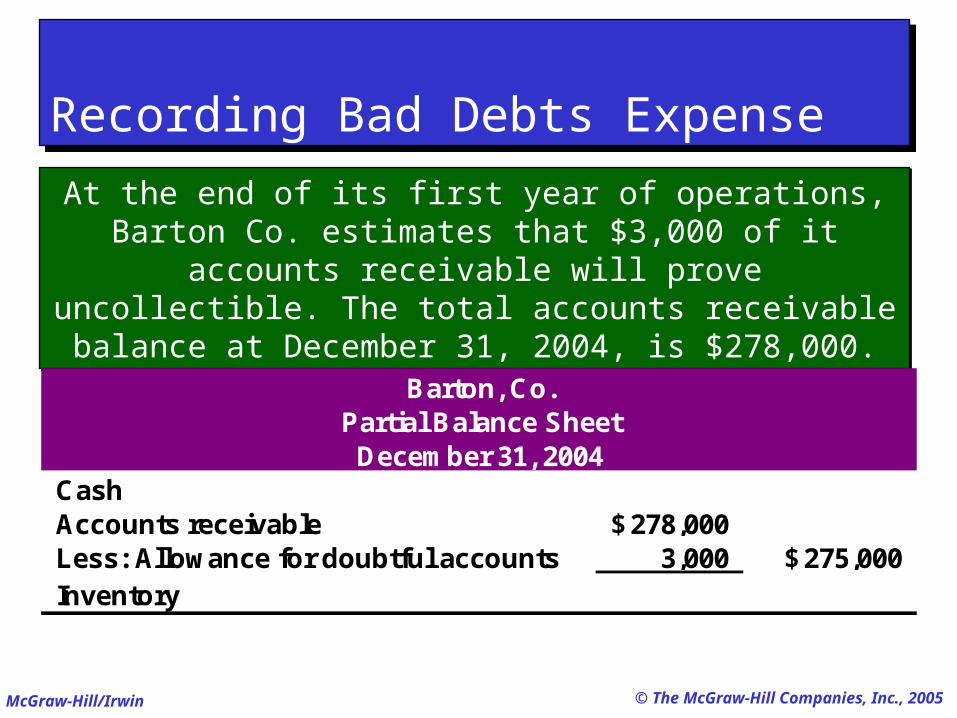

Recording Bad Debts ExpenseRecording Bad Debts Expense

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

At the end of its first year of operations, Barton Co. estimates that $3,000 of it accounts receivable will prove uncollectible. The total accounts receivable balance at

December 31, 2004, is $278,000.

CashAccounts receivable 278,000$ Less: Allowance for doubtful accounts 3,000 275,000$ Inventory

Barton, Co.Partial Balance Sheet

December 31, 2004

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

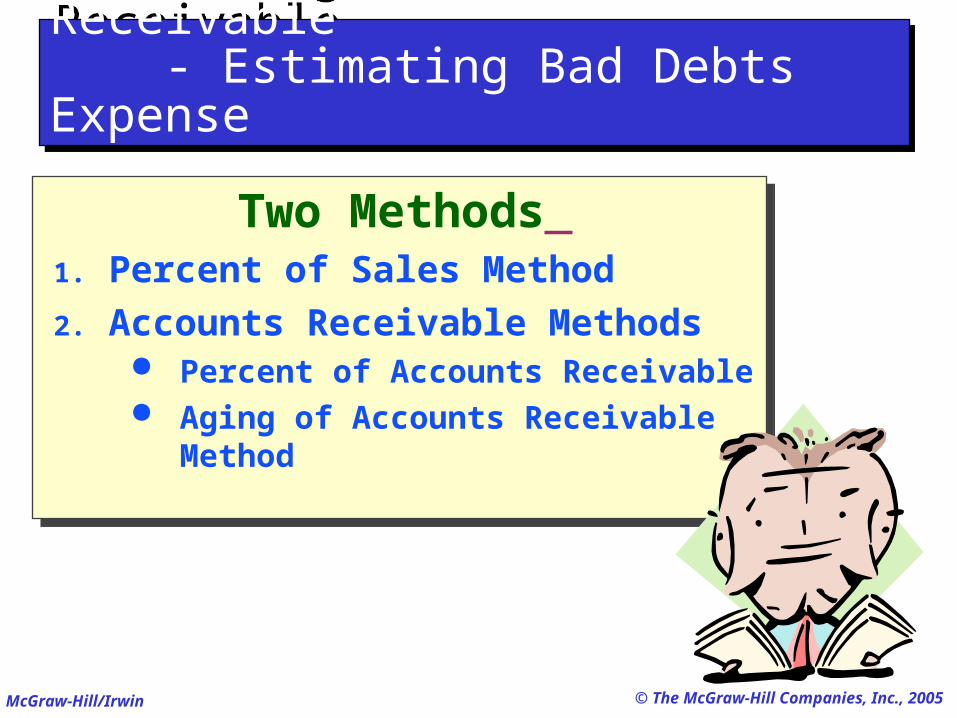

Two Methods 1. Percent of Sales Method

2. Accounts Receivable Methods Percent of Accounts Receivable Aging of Accounts Receivable

Method

Two Methods 1. Percent of Sales Method

2. Accounts Receivable Methods Percent of Accounts Receivable Aging of Accounts Receivable

Method

2. Valuing Accounts Receivable - Estimating Bad Debts Expense2. Valuing Accounts Receivable - Estimating Bad Debts Expense

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

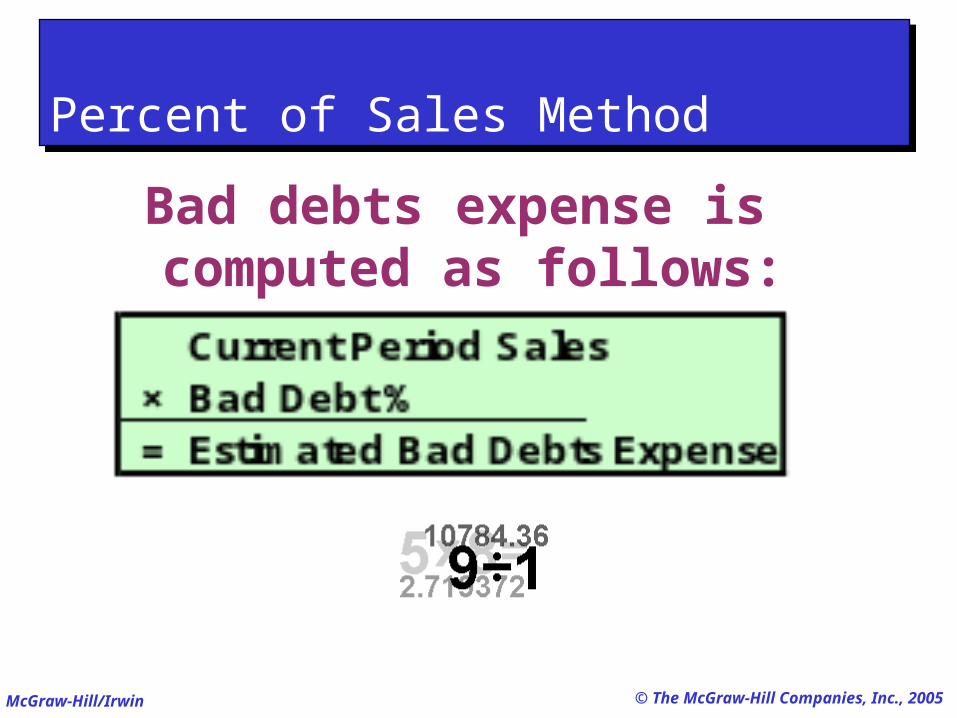

Bad debts expense is computed as follows:

Percent of Sales MethodPercent of Sales Method

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

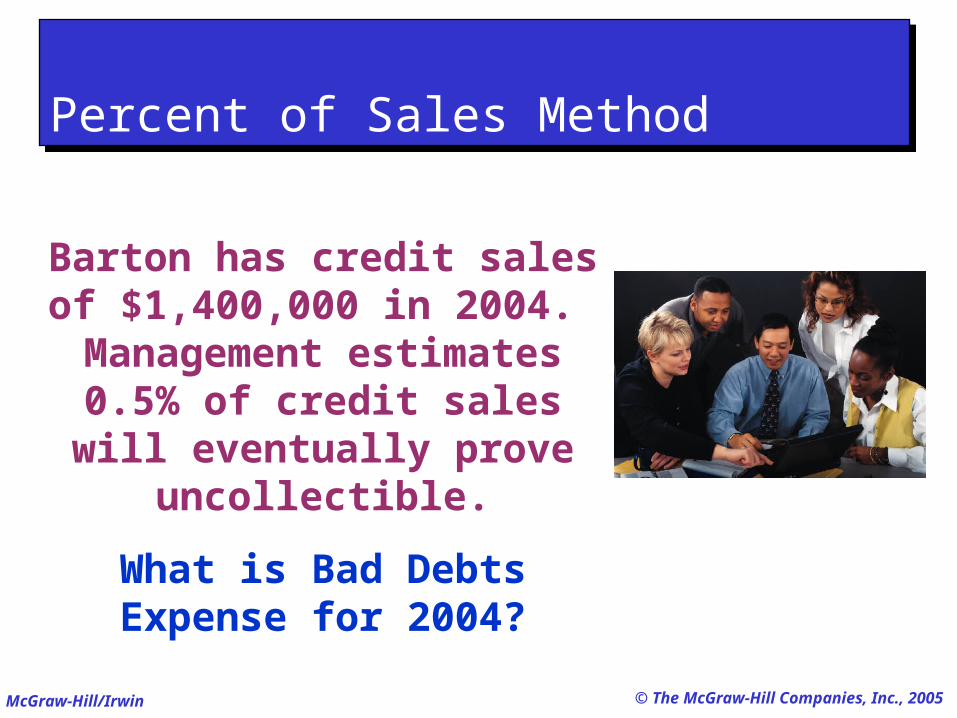

Barton has credit sales of $1,400,000 in 2004.

Management estimates 0.5% of credit sales will eventually

prove uncollectible.

What is Bad Debts Expense for 2004?

Percent of Sales MethodPercent of Sales Method

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

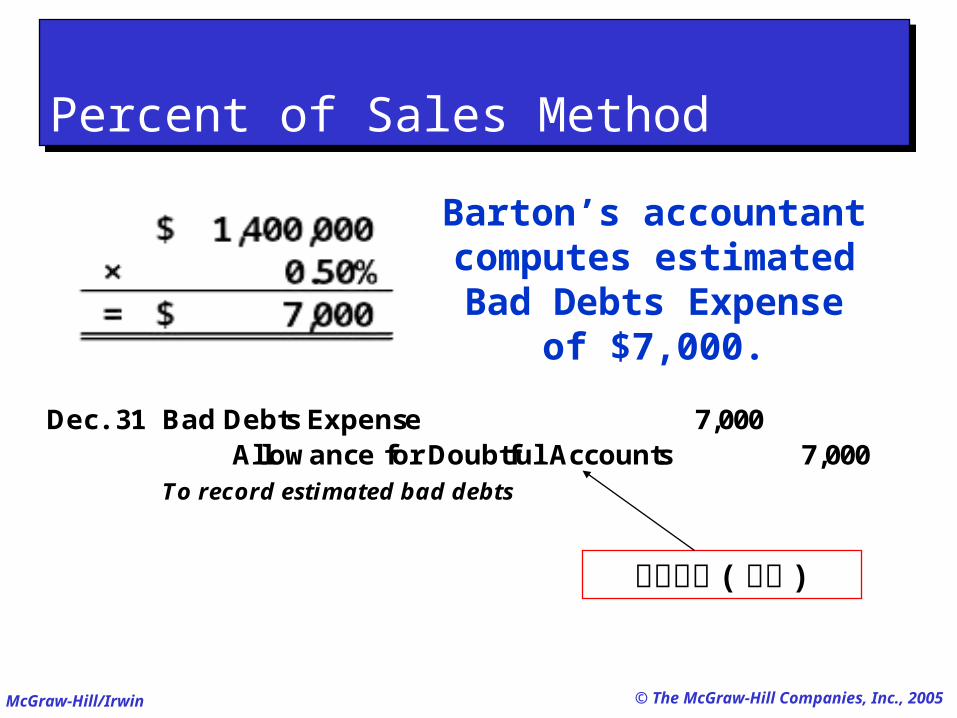

Barton’s accountant computes estimated

Bad Debts Expense of $7,000.

Percent of Sales MethodPercent of Sales Method

Dec. 31 Bad Debts Expense 7,000 Allowance for Doubtful Accounts 7,000

To record estimated bad debts

壞賬準備 (撥備 )

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

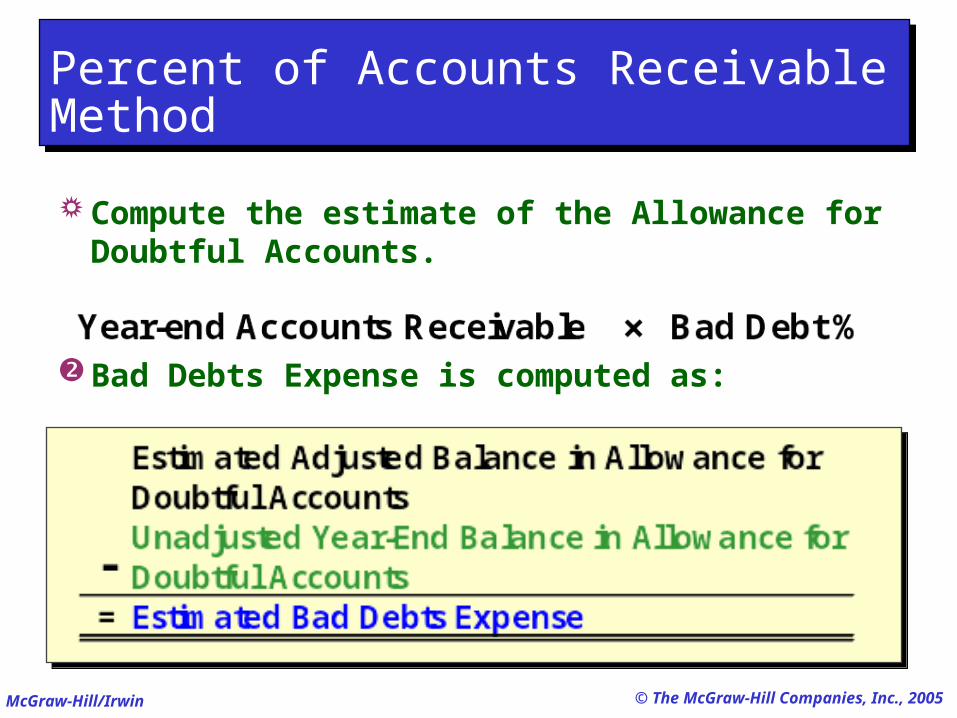

Compute the estimate of the Allowance for Doubtful Accounts.

Bad Debts Expense is computed as:

Percent of Accounts Receivable MethodPercent of Accounts Receivable Method

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

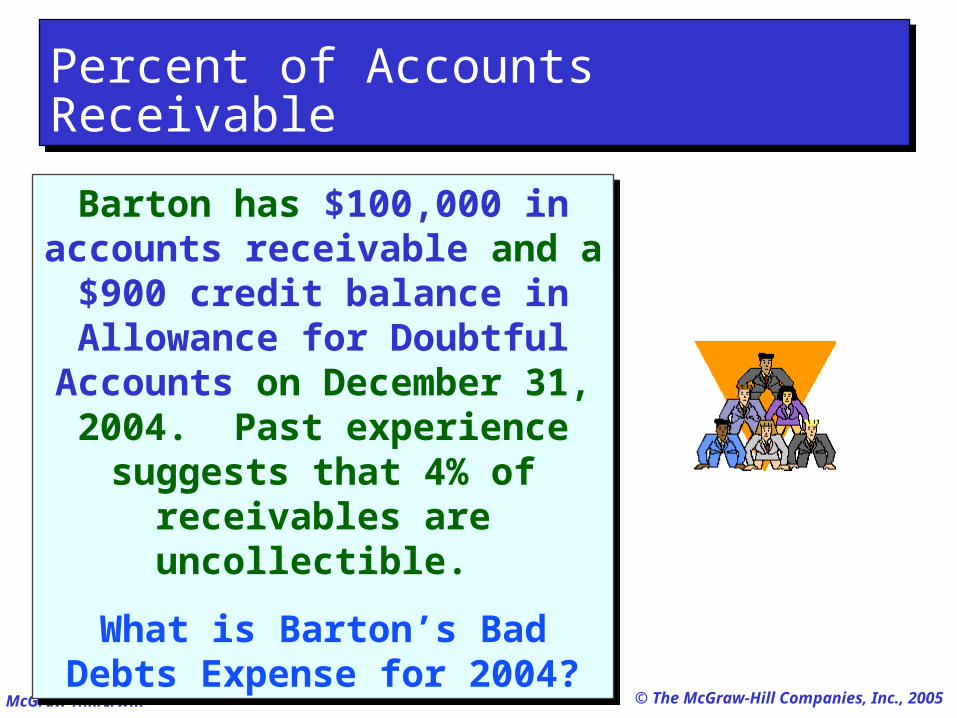

Barton has $100,000 in accounts receivable and a $900 credit balance in Allowance for

Doubtful Accounts on December 31, 2004. Past

experience suggests that 4% of receivables are uncollectible.

What is Barton’s Bad Debts Expense for 2004?

Barton has $100,000 in accounts receivable and a $900 credit balance in Allowance for

Doubtful Accounts on December 31, 2004. Past

experience suggests that 4% of receivables are uncollectible.

What is Barton’s Bad Debts Expense for 2004?

Percent of Accounts ReceivablePercent of Accounts Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

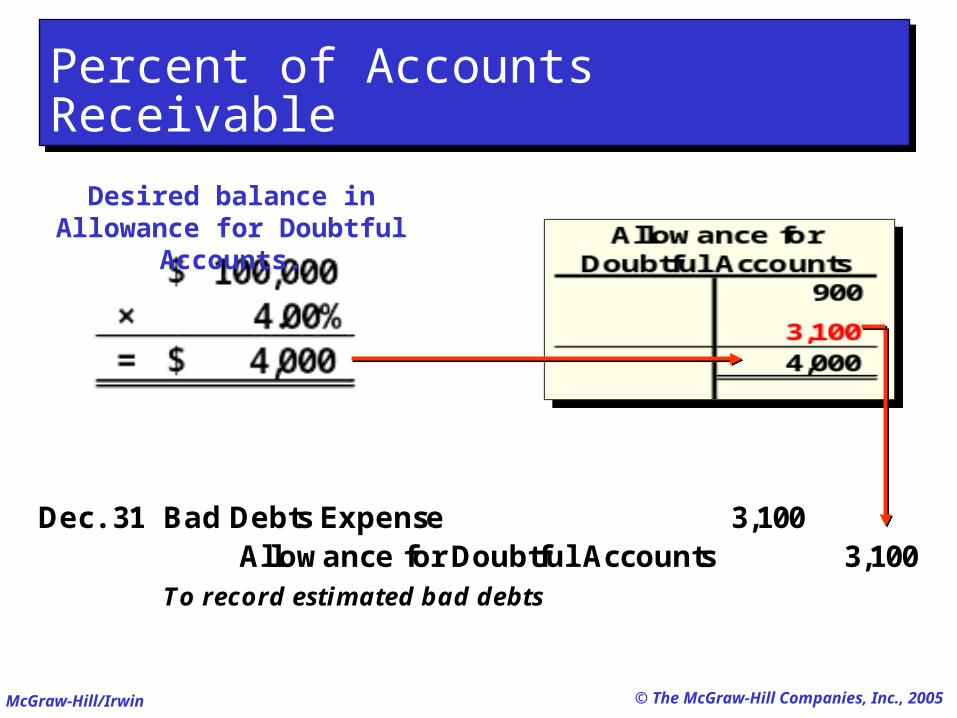

Desired balance in Allowance for Doubtful Accounts.

Percent of Accounts ReceivablePercent of Accounts Receivable

Dec. 31 Bad Debts Expense 3,100 Allowance for Doubtful Accounts 3,100

To record estimated bad debts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

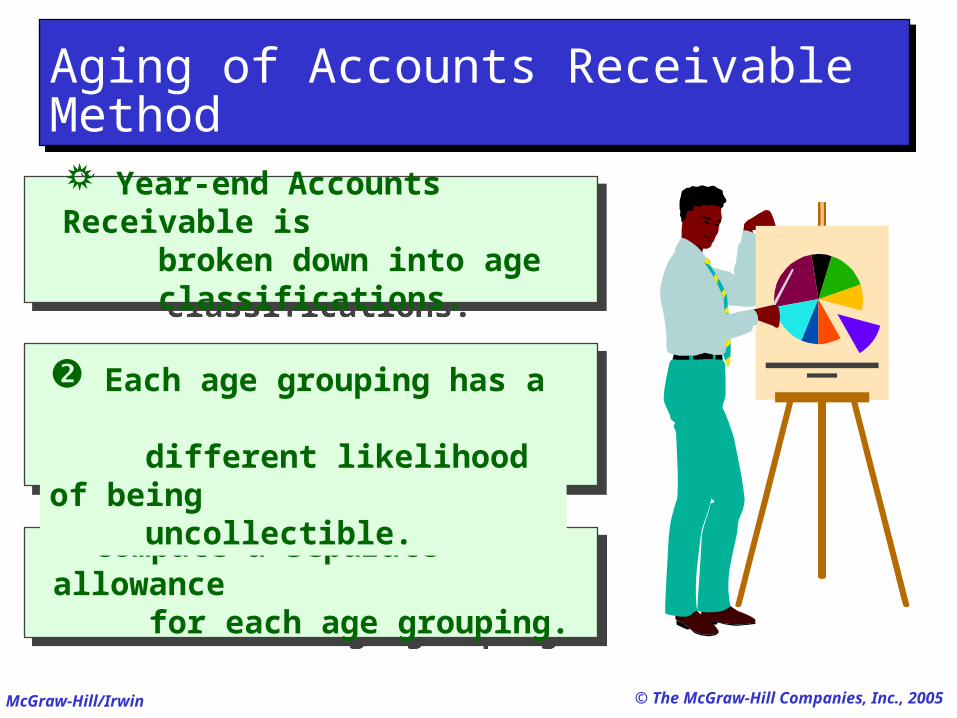

Year-end Accounts Receivable is broken down into age classifications.

Year-end Accounts Receivable is broken down into age classifications.

Compute a separate allowance for each age grouping.

Compute a separate allowance for each age grouping.

Aging of Accounts Receivable MethodAging of Accounts Receivable Method

Each age grouping has a different likelihood of being uncollectible.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

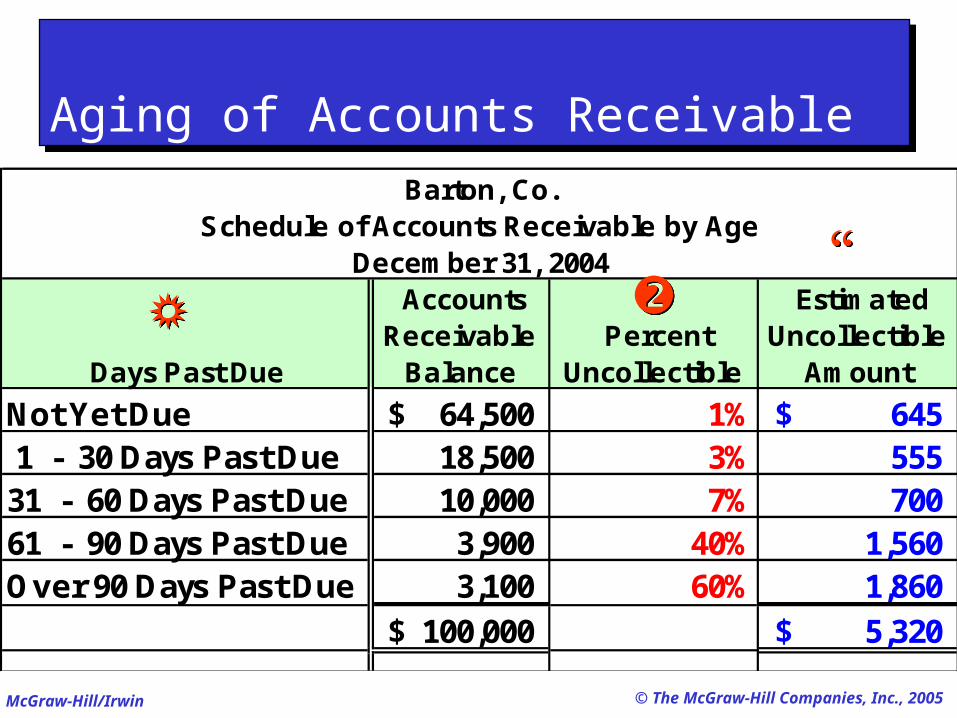

Barton, Co.Schedule of Accounts Receivable by Age

December 31, 2004

Days Past Due

Accounts Receivable

Balance Percent

Uncollectible

Estimated Uncollectible

Amount

Not Yet Due 64,500$ 1% 645$ 1 - 30 Days Past Due 18,500 3% 555 31 - 60 Days Past Due 10,000 7% 700 61 - 90 Days Past Due 3,900 40% 1,560 Over 90 Days Past Due 3,100 60% 1,860

100,000$ 5,320$

Aging of Accounts ReceivableAging of Accounts Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

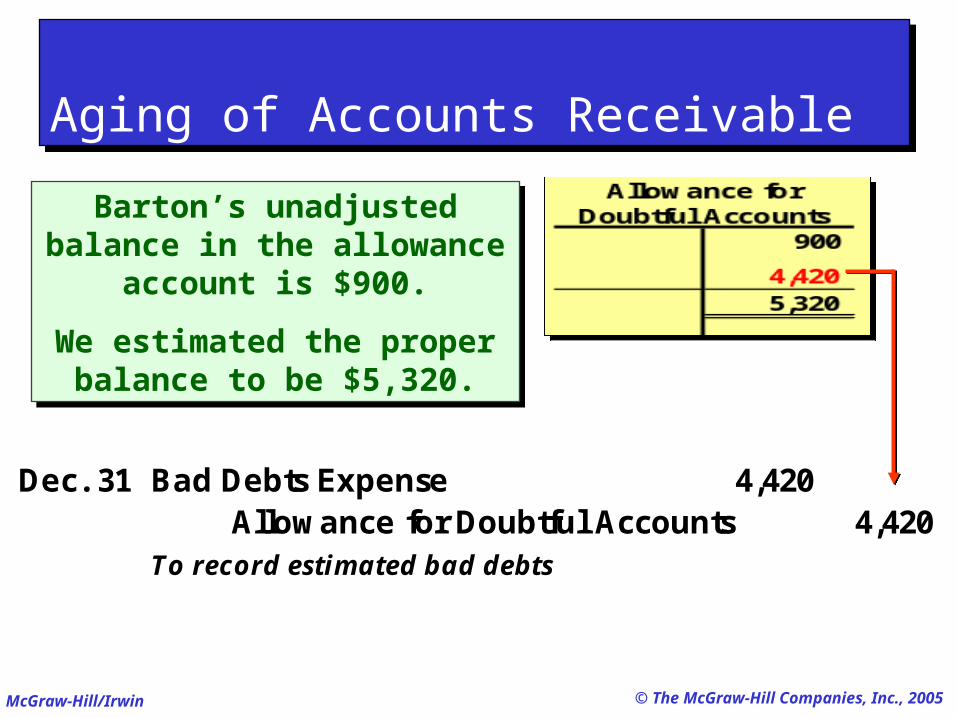

Barton’s unadjusted balance in the allowance account is

$900.

We estimated the proper balance to be $5,320.

Barton’s unadjusted balance in the allowance account is

$900.

We estimated the proper balance to be $5,320.

Aging of Accounts ReceivableAging of Accounts Receivable

Dec. 31 Bad Debts Expense 4,420 Allowance for Doubtful Accounts 4,420

To record estimated bad debts

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

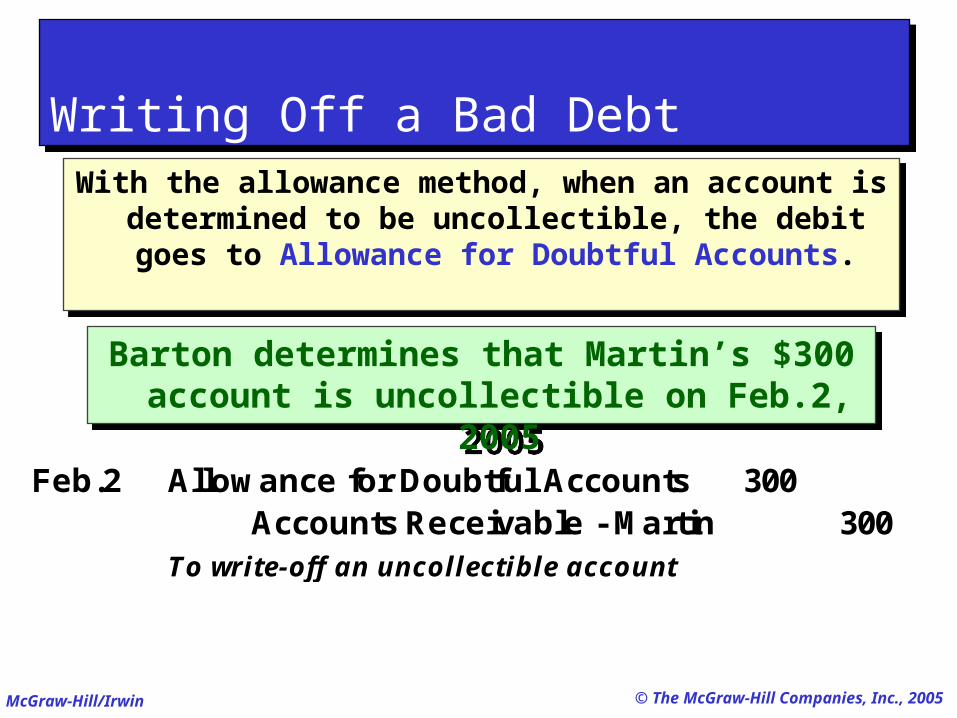

With the allowance method, when an account is determined to be uncollectible, the debit goes to Allowance for Doubtful Accounts.

With the allowance method, when an account is determined to be uncollectible, the debit goes to Allowance for Doubtful Accounts.

Writing Off a Bad DebtWriting Off a Bad Debt

Barton determines that Martin’s $300 account is uncollectible on Feb.2, 2005

Barton determines that Martin’s $300 account is uncollectible on Feb.2, 2005

Feb.2 Allowance for Doubtful Accounts 300 Accounts Receivable - Martin 300

To write-off an uncollectible account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

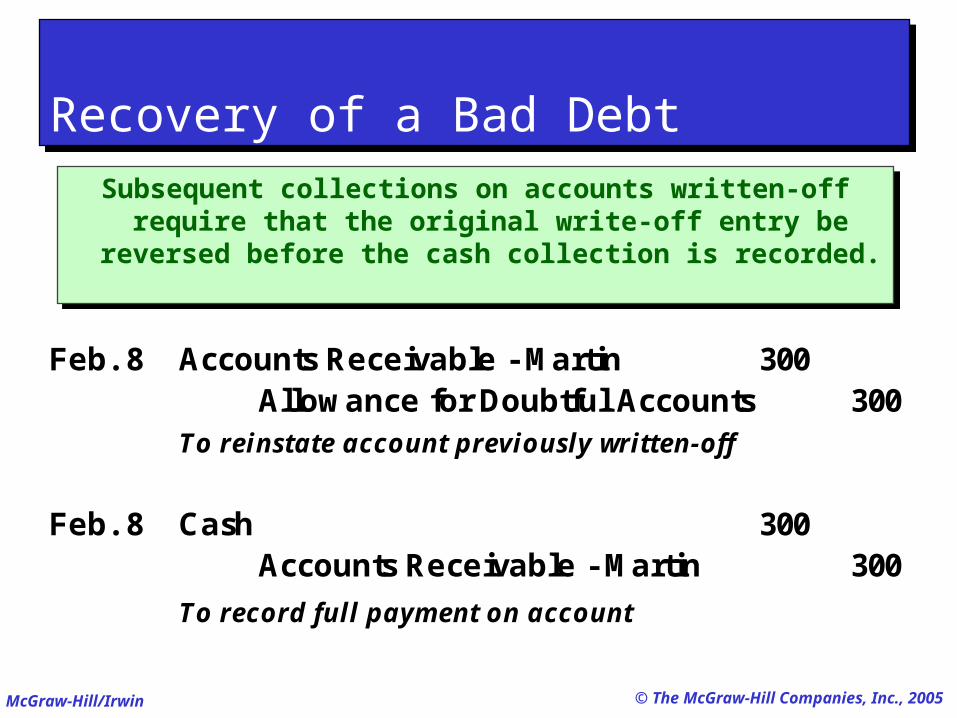

Subsequent collections on accounts written-off require that the original write-off entry be reversed

before the cash collection is recorded.

Subsequent collections on accounts written-off require that the original write-off entry be reversed

before the cash collection is recorded.

Recovery of a Bad DebtRecovery of a Bad Debt

Feb. 8 Accounts Receivable - Martin 300 Allowance for Doubtful Accounts 300

To reinstate account previously written-off

Feb. 8 Cash 300 Accounts Receivable - Martin 300

To record full payment on account

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

% of Sales

Emphasis on Matching

SalesBad

Debts Exp.

Income Statement

Focus

Income Statement

Focus

% of Receivables

Emphasis on Realizable Value

Accts. Rec. All. for

Doubtful Accts.

Balance Sheet Focus

Balance Sheet Focus

Aging of Receivables

Emphasis on Realizable Value

Accts. Rec. All. for

Doubtful Accts.

Balance Sheet Focus

Balance Sheet Focus

2. Valuing Accounts Receivable - Summary of Bad debt expense2. Valuing Accounts Receivable - Summary of Bad debt expense

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Let’s look at notes receivable!

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

A note is a written

promise to pay a specific amount at a

specific future date.

3. Notes Receivable3. Notes Receivable

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

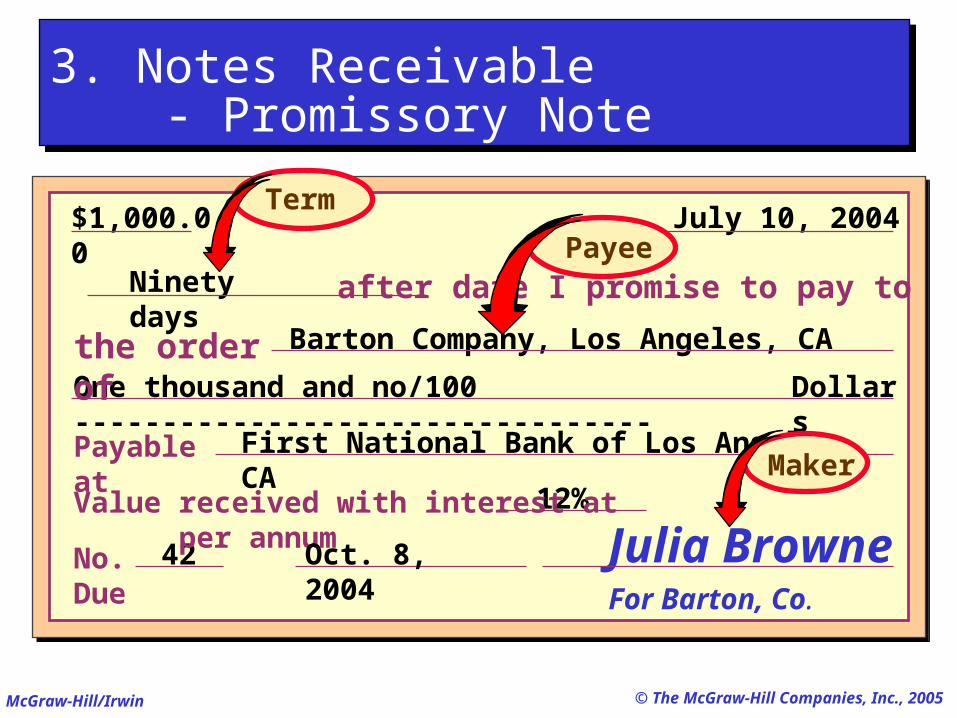

$1,000.00 July 10, 2004

Ninety days

Barton Company, Los Angeles, CA

One thousand and no/100 --------------------------------- Dollars

First National Bank of Los Angeles, CA

42

12%

Julia Browne

after date I promise to pay to

the order of

Payable atValue received with interest at per annumNo. Due Oct. 8, 2004

For Barton, Co.

Term

Payee

Maker

3. Notes Receivable - Promissory Note3. Notes Receivable - Promissory Note

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

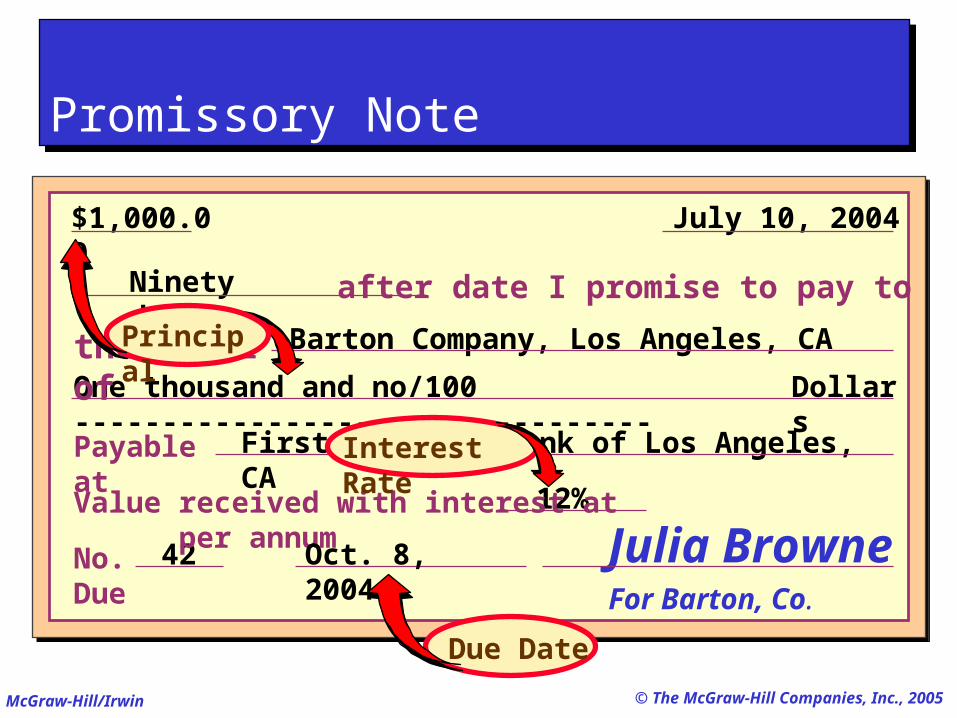

$1,000.00 July 10, 2004

Ninety days

Barton Company, Los Angeles, CA

One thousand and no/100 --------------------------------- Dollars

First National Bank of Los Angeles, CA

42

12%

Julia Browne

after date I promise to pay to

the order of

Payable atValue received with interest at per annumNo. Due Oct. 8, 2004

For Barton, Co.

Due Date

Promissory NotePromissory Note

Principal

Interest Rate

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

If the note is expressed in days, base a year on 360

days.

If the note is expressed in days, base a year on 360

days.

Even for maturities less

than 1 year, the rate is

annualized.

Even for maturities less

than 1 year, the rate is

annualized.

3. Notes Receivable - Interest Computation3. Notes Receivable - Interest Computation

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

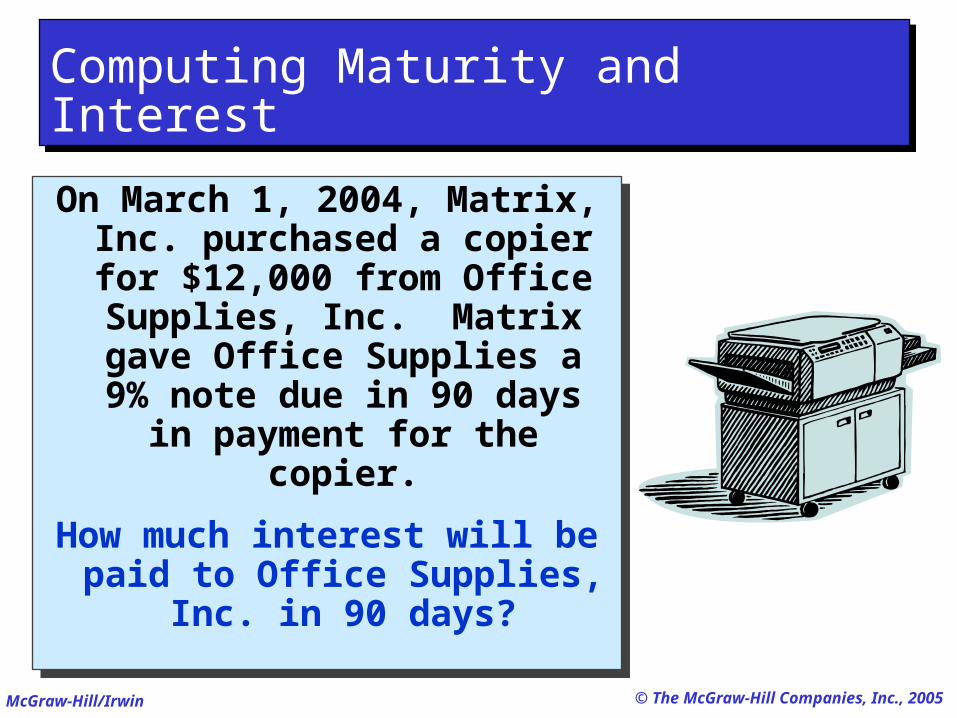

On March 1, 2004, Matrix, Inc. purchased a copier for

$12,000 from Office Supplies, Inc. Matrix gave Office Supplies a 9% note due in 90 days in payment

for the copier.

How much interest will be paid to Office Supplies, Inc.

in 90 days?

On March 1, 2004, Matrix, Inc. purchased a copier for

$12,000 from Office Supplies, Inc. Matrix gave Office Supplies a 9% note due in 90 days in payment

for the copier.

How much interest will be paid to Office Supplies, Inc.

in 90 days?

Computing Maturity and InterestComputing Maturity and Interest

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Computing Maturity and InterestComputing Maturity and Interest

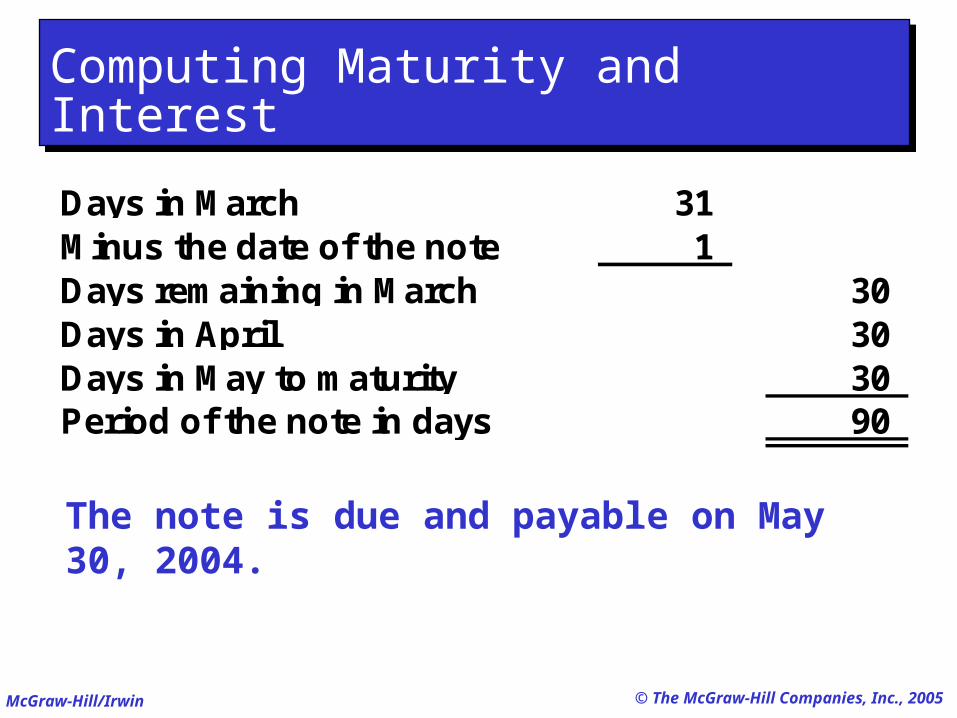

Days in March 31 Minus the date of the note 1 Days remaining in March 30 Days in April 30 Days in May to maturity 30 Period of the note in days 90

The note is due and payable on May 30, 2004.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

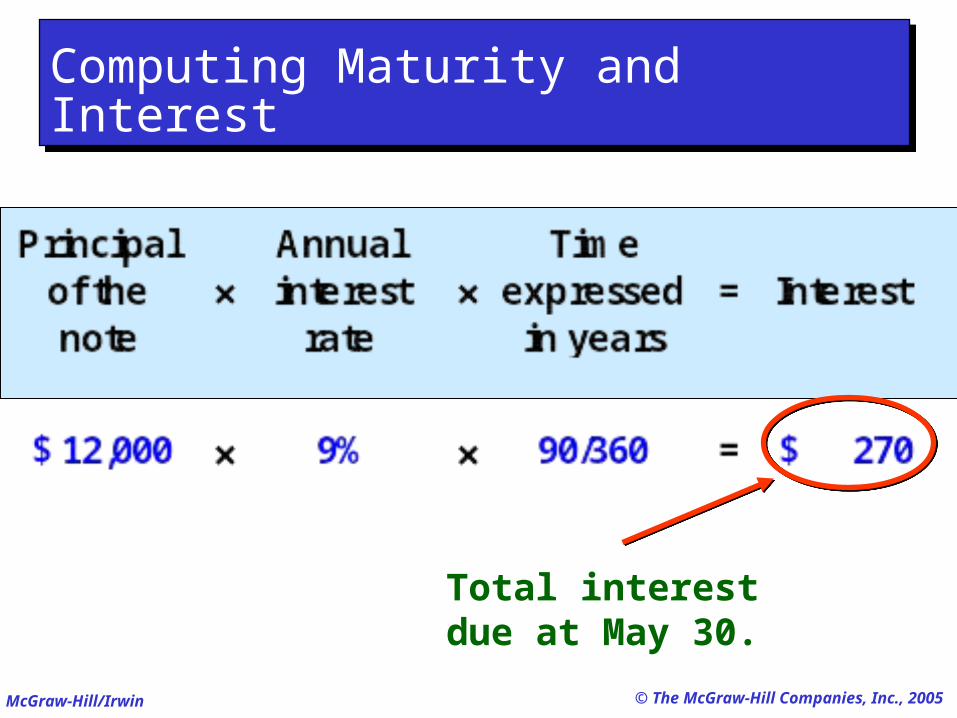

Total interest due at May 30.

Computing Maturity and InterestComputing Maturity and Interest

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Recognizing Notes ReceivableRecognizing Notes Receivable

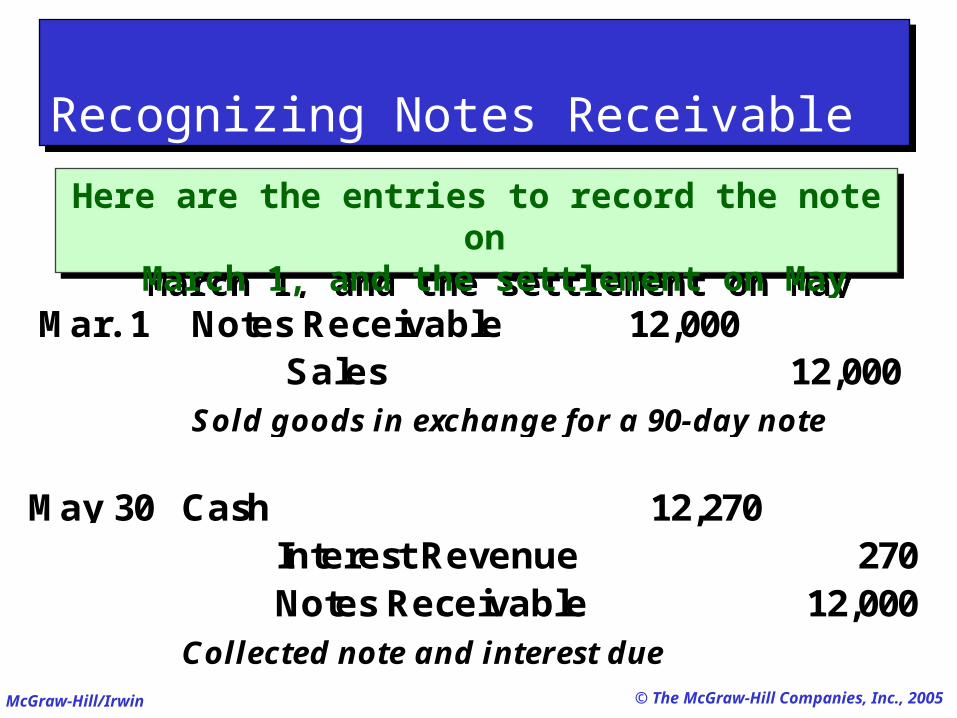

Here are the entries to record the note on March 1, and the settlement on May 30, 2004.Here are the entries to record the note on March 1, and the settlement on May 30, 2004.

Mar. 1 Notes Receivable 12,000 Sales 12,000

Sold goods in exchange for a 90-day note

May 30 Cash 12,270 Interest Revenue 270 Notes Receivable 12,000

Collected note and interest due

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

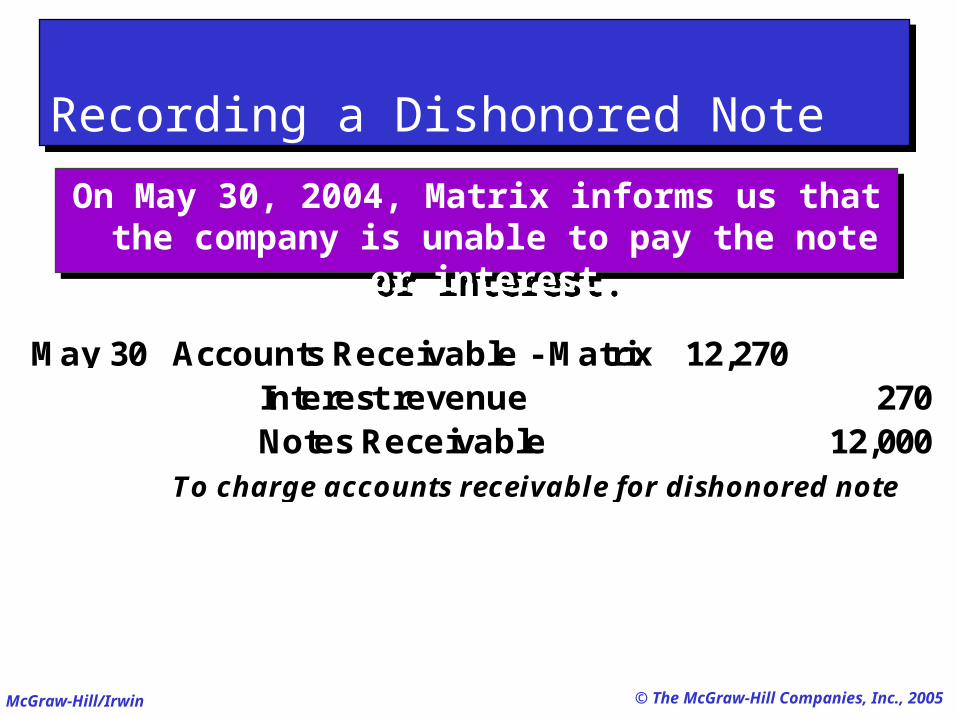

Recording a Dishonored NoteRecording a Dishonored Note

On May 30, 2004, Matrix informs us that the company is unable to pay the note or interest.On May 30, 2004, Matrix informs us that the company is unable to pay the note or interest.

May 30 Accounts Receivable - Matrix 12,270 Interest revenue 270 Notes Receivable 12,000

To charge accounts receivable for dishonored note

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

When a note receivable is outstanding at the end of an accounting period, the company

must prepare an adjusting entry to

accrue interest income.

When a note receivable is outstanding at the end of an accounting period, the company

must prepare an adjusting entry to

accrue interest income.

Recording End-of-Period Interest AdjustmentsRecording End-of-Period Interest Adjustments

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

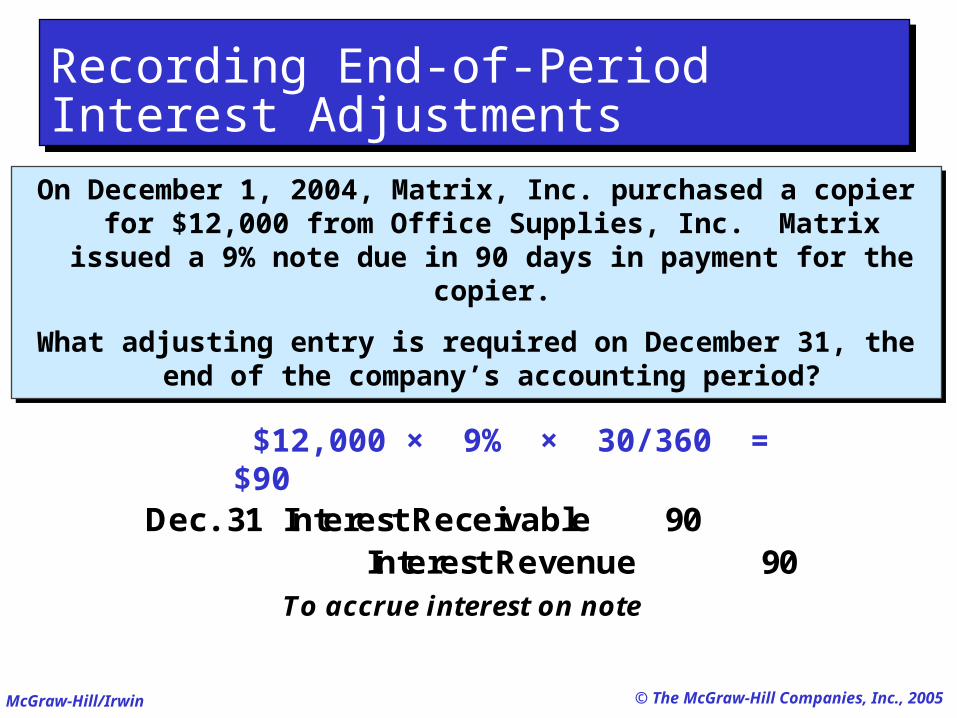

Recording End-of-Period Interest AdjustmentsRecording End-of-Period Interest Adjustments

On December 1, 2004, Matrix, Inc. purchased a copier for $12,000 from Office Supplies, Inc. Matrix issued a 9%

note due in 90 days in payment for the copier.

What adjusting entry is required on December 31, the end of the company’s accounting period?

On December 1, 2004, Matrix, Inc. purchased a copier for $12,000 from Office Supplies, Inc. Matrix issued a 9%

note due in 90 days in payment for the copier.

What adjusting entry is required on December 31, the end of the company’s accounting period?

$12,000 × 9% × 30/360 = $90

Dec. 31 Interest Receivable 90 Interest Revenue 90

To accrue interest on note

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

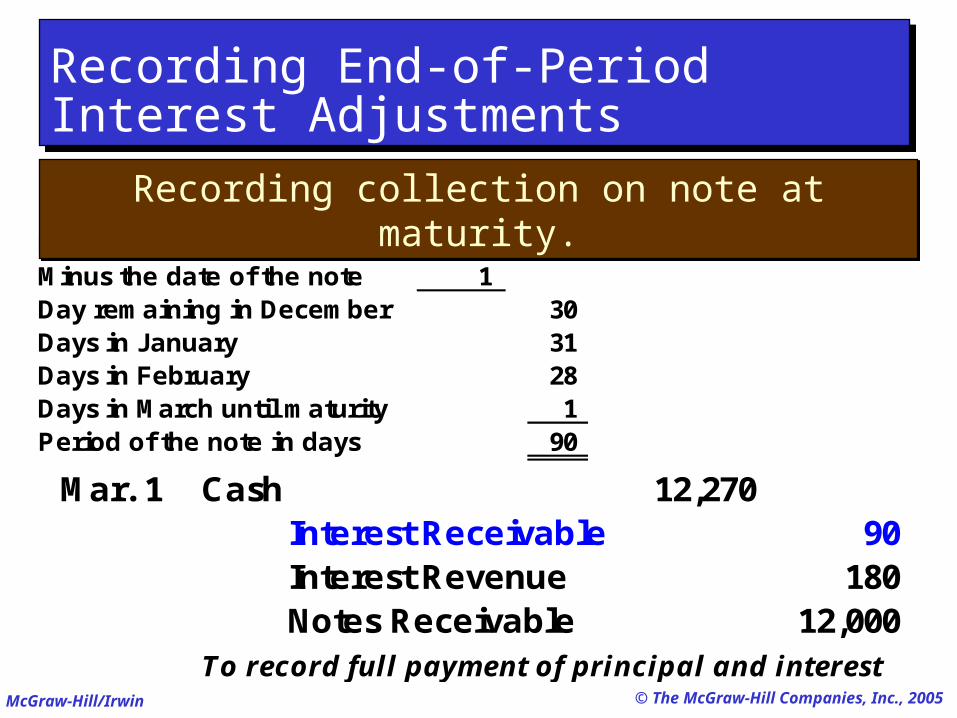

Recording End-of-Period Interest AdjustmentsRecording End-of-Period Interest Adjustments

Days in December 31 Minus the date of the note 1 Day remaining in December 30 Days in January 31 Days in February 28 Days in March until maturity 1 Period of the note in days 90

Mar. 1 Cash 12,270 Interest Receivable 90 Interest Revenue 180 Notes Receivable 12,000

To record full payment of principal and interest

Recording collection on note at maturity.Recording collection on note at maturity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

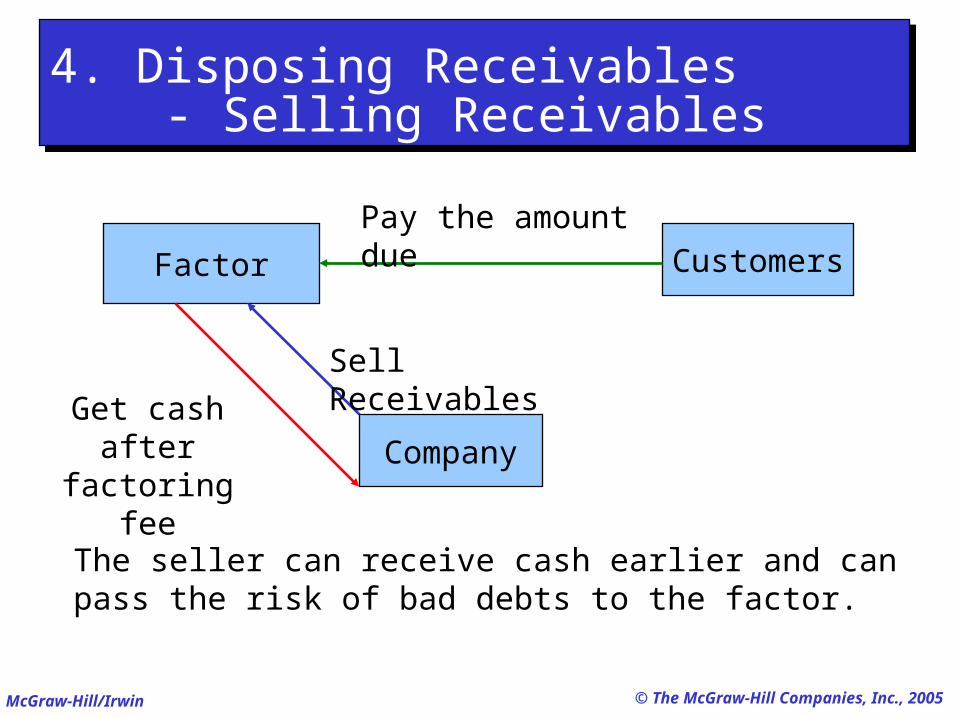

4. Disposing Receivables - Selling Receivables4. Disposing Receivables - Selling Receivables

Company

Factor Customers

Sell Receivables

Get cash after factoring fee

Pay the amount due

The seller can receive cash earlier and can pass the risk of bad debts to the factor.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Selling ReceivablesSelling Receivables

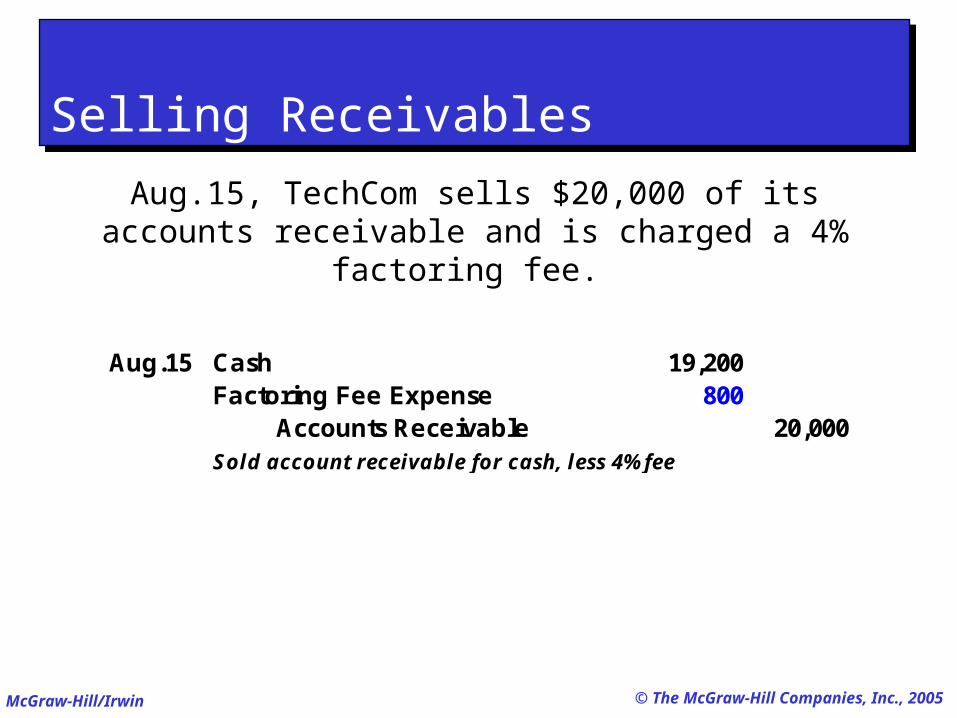

Aug.15, TechCom sells $20,000 of its accounts receivable and is charged a 4% factoring fee.

Aug.15 Cash 19,200 Factoring Fee Expense 800

Accounts Receivable 20,000 Sold account receivable for cash, less 4% fee

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

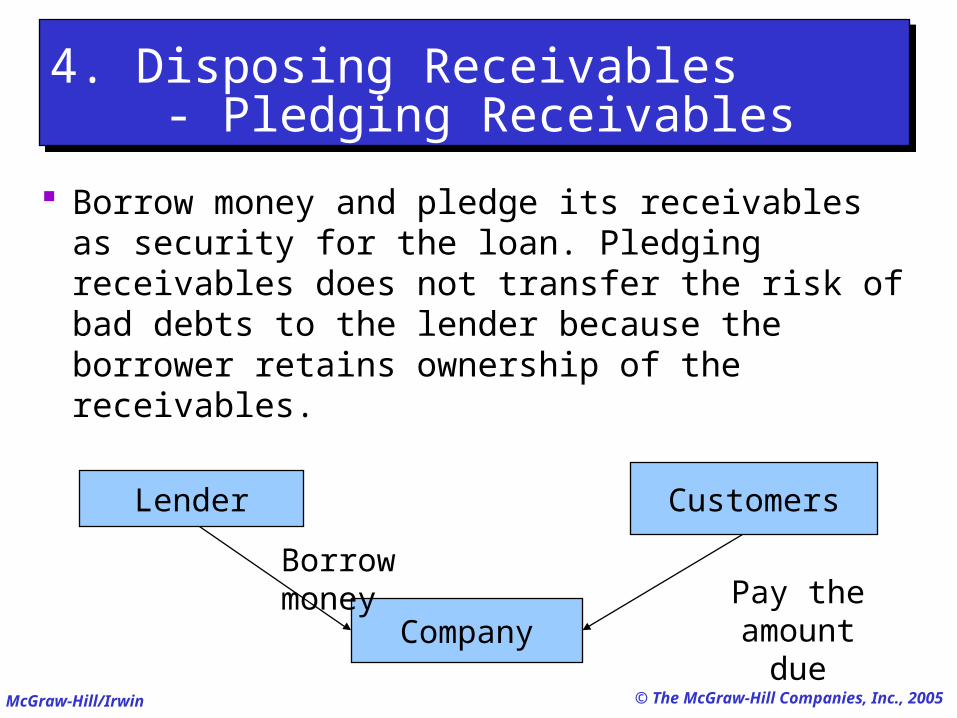

4. Disposing Receivables - Pledging Receivables4. Disposing Receivables - Pledging Receivables

Borrow money and pledge its receivables as security for the loan. Pledging receivables does not transfer the risk of bad debts to the lender because the borrower retains ownership of the receivables.

Company

Lender Customers

Borrow moneyPay the

amount due

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

Pledging ReceivablesPledging Receivables

TechCom borrows $35,000 and pledges its receivables as security.

Aug.20 Cash 35,000 Note Payable 35,000

Borrow money with a note secured by pledging receivables

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

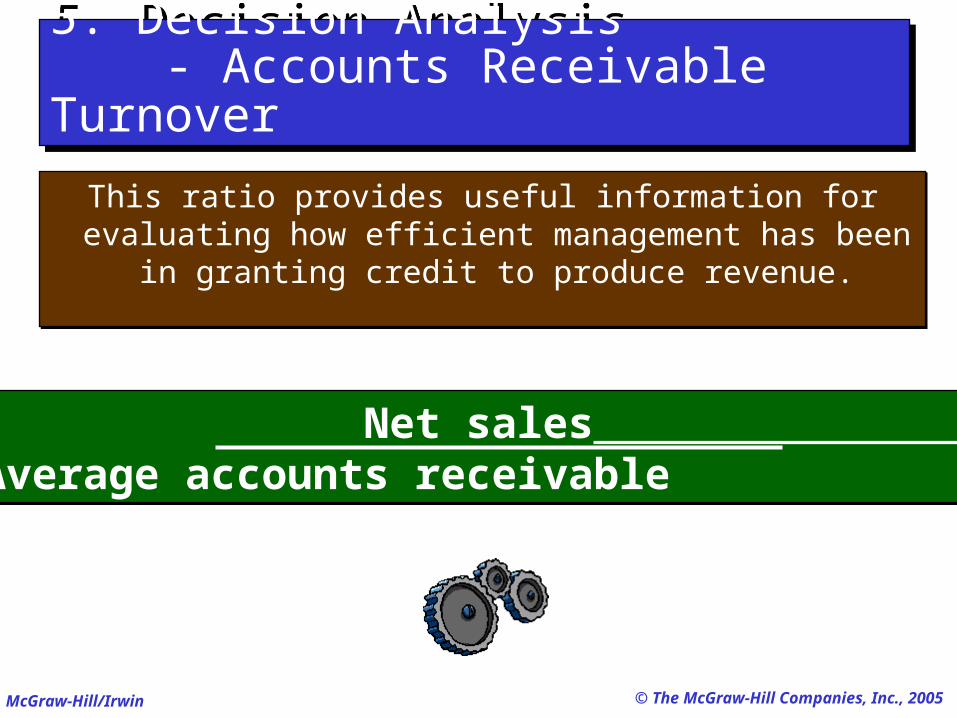

This ratio provides useful information for evaluating how efficient management has

been in granting credit to produce revenue.

This ratio provides useful information for evaluating how efficient management has

been in granting credit to produce revenue.

Net sales Average accounts receivable Net sales Average accounts receivable

5. Decision Analysis - Accounts Receivable Turnover5. Decision Analysis - Accounts Receivable Turnover

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

5. Decision Analysis - Supermarket5. Decision Analysis - Supermarket

1. Industry Characteristics High volume, Low profit margin Chain of stores

2. Key success factors Inventory control Store location decision

3. Companies for analysis Walmart Target

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

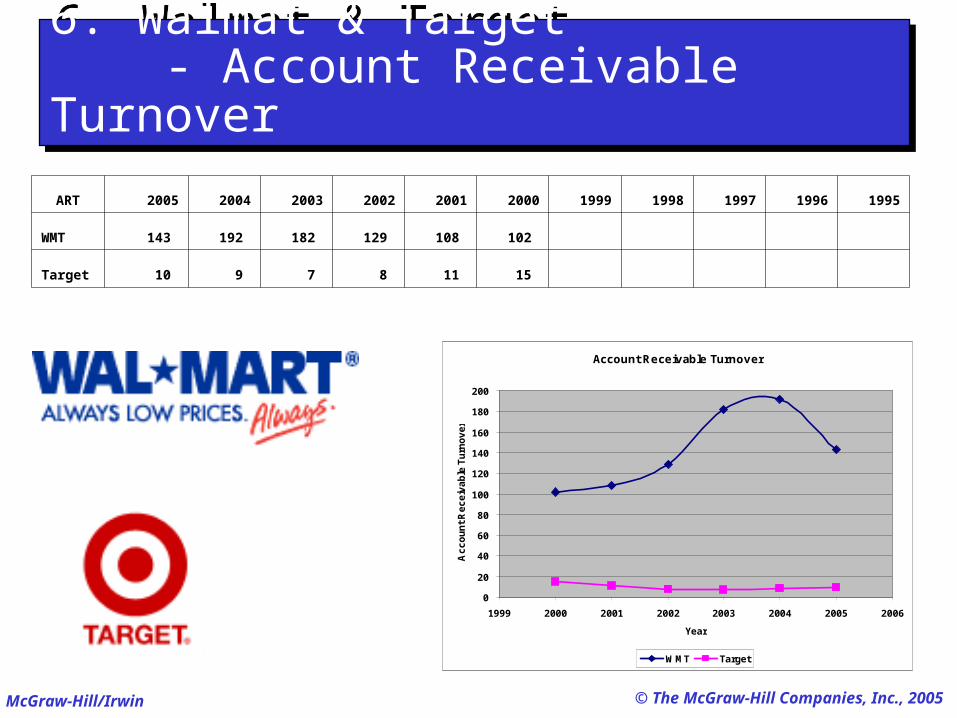

6. Walmat & Target - Account Receivable Turnover6. Walmat & Target - Account Receivable Turnover

ART 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995

WMT 143 192 182 129 108 102

Target 10 9 7 8 11 15

Account Receivable Turnover

0

20

40

60

80

100

120

140

160

180

200

1999 2000 2001 2002 2003 2004 2005 2006

Year

Ac

co

un

t R

ec

eiv

ab

le T

urn

ov

er

WMT Target

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

End of Chapter 9End of Chapter 9