Masaryk University Faculty of Economics and Administration Field of Study: Business management ERP SYSTEM, NEW TRENDS, PROCESSES OF SYSTEM SELECTION, SALES, IMPLEMENTATION AND SUPPORT ERP systém, nové tendence, proces výběru, prodeje, implementace a údržby Diploma thesis Thesis supervisor: Author: Ing. Jaromír Skorkovský, CSc. Bc. David DURANTI Brno, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Masaryk Universi ty

Faculty of Economics and Administration

Field of Study: Business management

ERP SYSTEM, NEW TRENDS, PROCESSES OF

SYSTEM SELECTION, SALES,

IMPLEMENTATION AND SUPPORT

ERP systém, nové tendence, proces výběru, prodeje,

implementace a údržby

Diploma thesis

Thesis supervisor: Author:

Ing. Jaromír Skorkovský, CSc. Bc. David DURANTI

Brno, 2014

Name and surname of author: Bc. David Duranti

Ti t le of the diploma thesis : ERP system, new trends, processes of

system selection, sales, implementation

and support

Ti t le of the diploma thesis in Czech: ERP systém, nové tendence, proces

výběru, prodeje, implementace a údržby

Academic department : Business management

Thesis supervisor: Ing. Jaromír Skorkovský, CSc.

Dissertat ion year : 2014

Annotation

Subject of the thesis “ERP system, new trends, processes of system selection, sales, implementation

and support” is analysis of providing ERP as a Service which is compared to the predominant

on-premise model. In the theoretical part, the technology of cloud computing, ERP system

and the implementation process are described. In the practical part of the thesis analysis of the

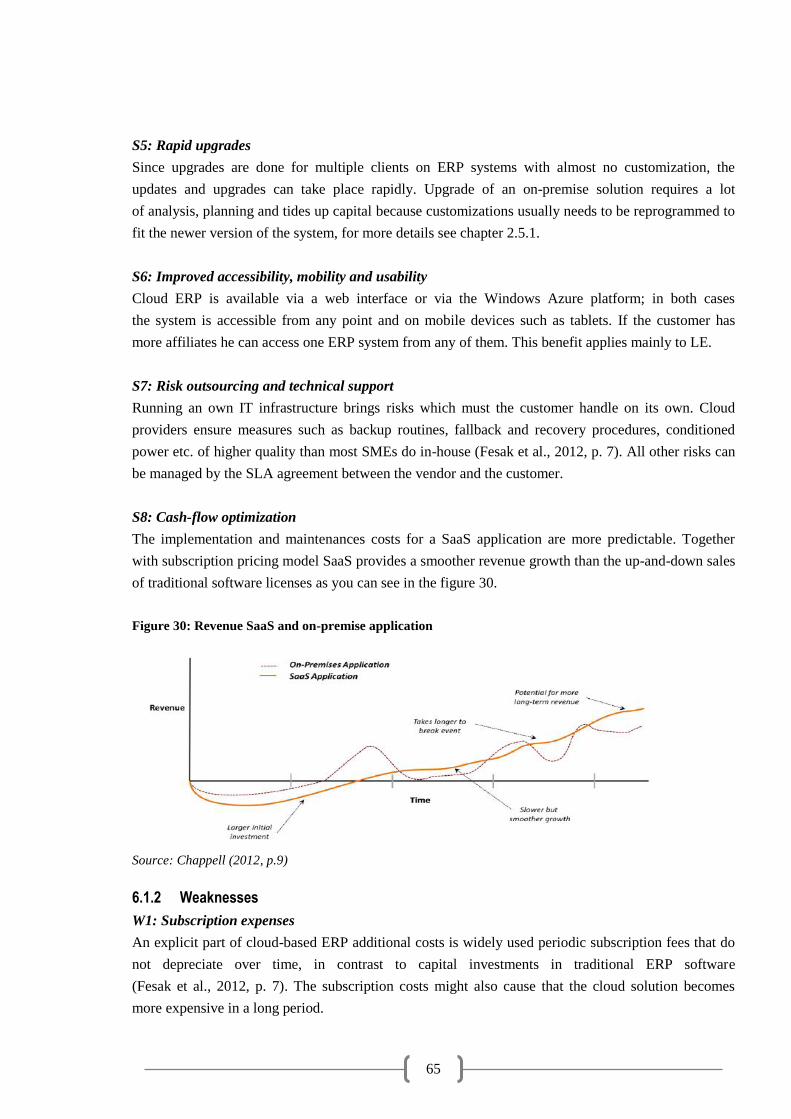

vertical solutions "PrintVis cloud" for the printing industry is conducted. This solution is

compared to traditional on-premise variants of the same product.

Anotace

Předmětem diplomové práce „ERP systém, nové tendence, proces výběru, prodeje, implementace a

údržby“ je analýza poskytování ERP systému jako služby a srovnání se současně

převládajícím „on-premise“ modelem. V teoretické části práce je představena technologie

cloud computing, ERP systém a proces implementace. V praktické části práce je analyzováno

vertikální řešení „PrintVis in cloud“ pro polygrafický průmysl. Toto řešení je srovnáno

s tradiční „on-premise“ variantou stejného produktu.

Keywords

ERP, cloud computing, on-premise, SaaS, IaaS, PrintVis, MS Dynamics NAV 2013,

Implementation of an ERP system.

Klíčová slova

ERP, cloud computing, on-premise, SaaS, IaaS, PrintVis, MS Dynamics NAV 2013,

Implementace ERP systému.

Declaration

Hereby I declare that I disposed the Diploma Thesis “ERP system, new trends, processes of system

selection, sales, implementation and support” by myself under the supervision of Ing. Jaromír

Skorkovský, CSc. and that I stated all the used literary resources and other scientific sources according

to legislation, internal regulations of Masaryk University and internal management acts of Masaryk

University and the Faculty of Economics and Administration.

In Brno 14th May 2014

Si gna t ur e o f t he au t ho r

Acknowledgement

Here I would like to express my gratitude to my supervisor Ing. Jaromír Skorkovský Csc., for valuable

comments and expert advice, which contributed to the development of this thesis. In addition, I would

like to thank companies NAVERTICA a.s., ARDAN S.r.l. and NovaVision A/S for their time,

information and provided opportunity to participate on cloud pilot projects without which this thesis

couldn’t be conducted.

TABLE OF CONTENTS

INTRODUCTION ................................................................................................................................ 13

THEORETICAL PART ...................................................................................................................... 13

1 CLOUD COMPUTING ................................................................................................................ 16

1.1 ESSENTIAL CHARACTERISTICS ................................................................................................. 16 1.2 SERVICE DELIVERY MODELS .................................................................................................... 17

1.2.1 Software as a service (SaaS) ............................................................................................ 17 1.2.2 Infrastructure as a service (IaaS) ..................................................................................... 18 1.2.3 Platform as a service (PaaS) ............................................................................................ 18

1.3 DEPLOYMENT MODELS ............................................................................................................ 18 1.3.1 Private cloud .................................................................................................................... 18 1.3.2 Community cloud .............................................................................................................. 18 1.3.3 Public cloud ...................................................................................................................... 18 1.3.4 Hybrid cloud ..................................................................................................................... 18

1.4 SUBSCRIPTION PRICING MODELS ............................................................................................. 19 1.4.1 Pay as you go ................................................................................................................... 19 1.4.2 Pay per user ..................................................................................................................... 19

1.5 ECONOMICS OF THE CLOUD ..................................................................................................... 19 1.5.1 Supply-side savings .......................................................................................................... 20 1.5.2 Demand-side aggregation ................................................................................................ 21 1.5.3 Multitenant efficiency ....................................................................................................... 21 1.5.4 Overall impact .................................................................................................................. 22

2 ERP ................................................................................................................................................ 24

2.1 EVOLUTION OF ERP ................................................................................................................. 24 2.2 ERP DELIVERY MODELS .......................................................................................................... 25

2.2.1 On-premise ERP ............................................................................................................... 26 2.2.2 Cloud ERP ........................................................................................................................ 26 2.2.3 Hosted ERP ...................................................................................................................... 26

2.3 PROCESS OF SALE AND SELECTION .......................................................................................... 26 2.3.1 Buying decision making.................................................................................................... 26 2.3.2 Customer lock-in .............................................................................................................. 27 2.3.3 Marketing ......................................................................................................................... 28 2.3.4 Try-it-Buy-it model ........................................................................................................... 29

2.4 PROCESS OF IMPLEMENTATION ................................................................................................ 30 2.4.1 Critical success factors .................................................................................................... 30 2.4.2 Knowledge management................................................................................................... 31 2.4.3 Cloud ERP implementation .............................................................................................. 32

2.5 PROCESS OF MAINTENANCE ..................................................................................................... 33 2.5.1 Maintenance tasks ............................................................................................................ 33 2.5.2 Cloud ERP maintenance .................................................................................................. 34

PRACTICAL PART ............................................................................................................................ 36

3 PRESENTATION OF THE COMPANIES AND PARTNER MODEL .................................. 36

3.1 PARTNER MODEL ..................................................................................................................... 36 3.1.1 NAVERTICA ..................................................................................................................... 37 3.1.2 NovaVision Software ........................................................................................................ 37 3.1.3 ARDAN ............................................................................................................................. 38

4 MICROSOT DYNAMICS NAV 2013 ......................................................................................... 39

4.1 FOCUSED ON CLOUD ................................................................................................................ 39 4.1.1 Rapid implementations .................................................................................................... 41 4.1.2 Multitenancy in MS NAV R2 2013 ................................................................................... 41 4.1.3 Customizations ................................................................................................................. 43 4.1.4 Licensing .......................................................................................................................... 43

4.2 PRINTVIS 2013 ...................................................................................................................... 44 4.2.1 Licensing .......................................................................................................................... 45

4.3 PRINTVIS 2013 IN CLOUD ...................................................................................................... 46 4.3.1 Accelerated Sales Process ............................................................................................... 47 4.3.2 Accelerated Implementation Process ............................................................................... 49

4.4 WINDOWS AZURE .................................................................................................................... 50 4.4.1 Interface ........................................................................................................................... 51 4.4.2 Pricing examples .............................................................................................................. 52 4.4.3 Comparison with on-premise ........................................................................................... 53

5 MARKET ANALYSIS ................................................................................................................. 55

5.1 GLOBAL ERP MARKET ............................................................................................................ 55 5.1.1 Cloud-born players .......................................................................................................... 56 5.1.2 ERP delivery models ........................................................................................................ 58

5.2 NEW TRENDS IN ERP ............................................................................................................... 60 5.3 ERP MARKET IN SOUTH AFRICA ............................................................................................. 62

5.3.1 Cloud computing .............................................................................................................. 63 5.4 ERP MARKET IN THE CZECH REPUBLIC .................................................................................. 64

5.4.1 IT service spending .......................................................................................................... 64 5.4.2 Current ERP market ........................................................................................................ 64 5.4.3 EU cloud computing incentives ....................................................................................... 65 5.4.4 Printing industry .............................................................................................................. 65

6 SWOT ANALYSIS ....................................................................................................................... 68

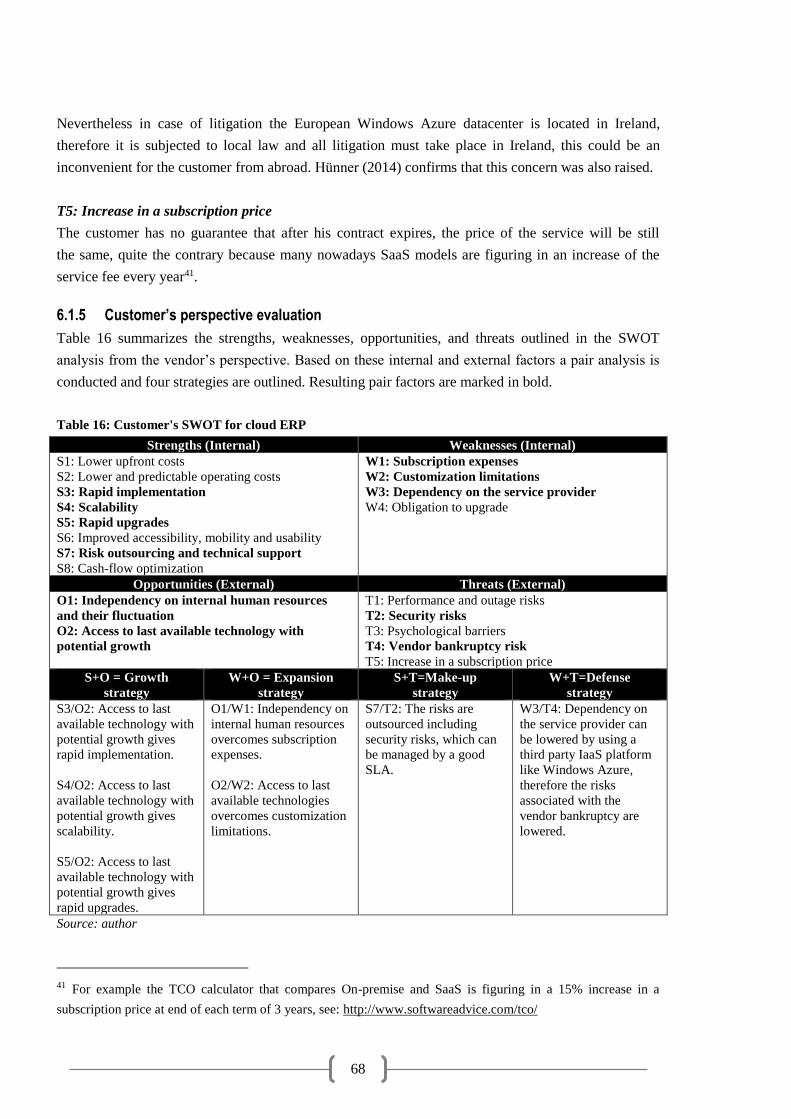

6.1 CUSTOMER’S PERSPECTIVE ..................................................................................................... 68 6.1.1 Strengths .......................................................................................................................... 68 6.1.2 Weaknesses ...................................................................................................................... 69 6.1.3 Opportunities ................................................................................................................... 70 6.1.4 Threats ............................................................................................................................. 70 6.1.5 Customer’s perspective evaluation .................................................................................. 72

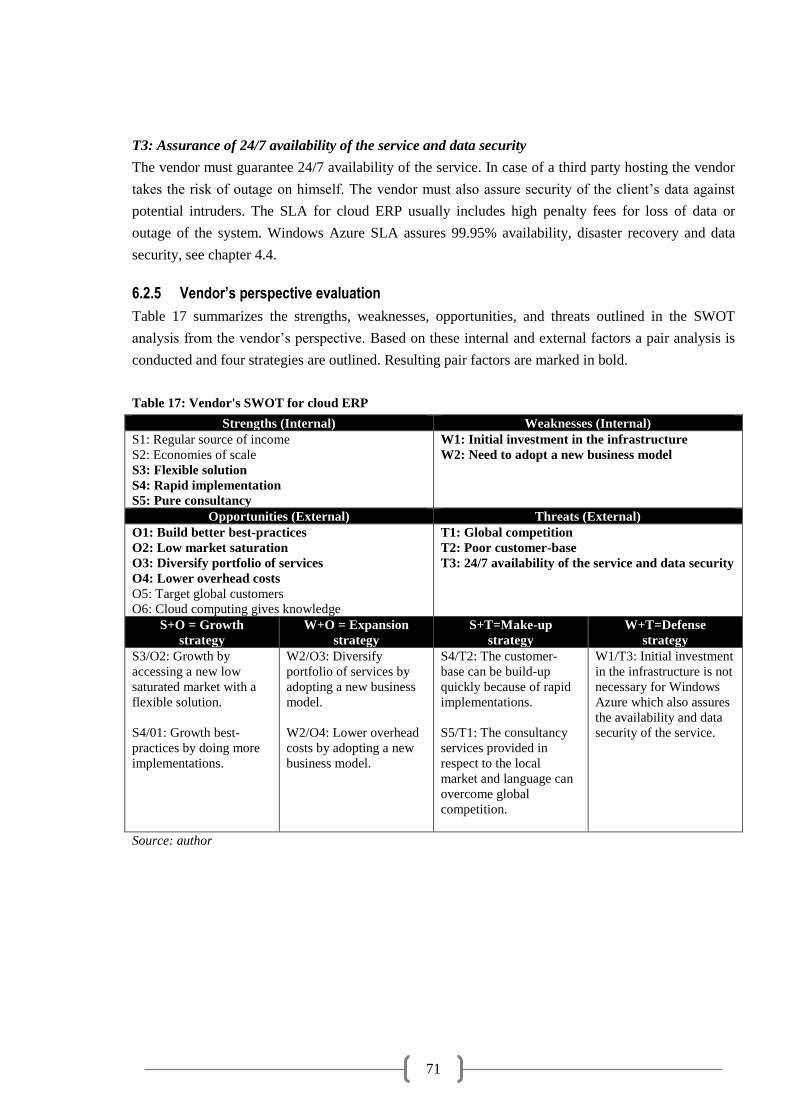

6.2 VENDOR’S PERSPECTIVE ......................................................................................................... 73 6.2.1 Strengths .......................................................................................................................... 73 6.2.2 Weaknesses ...................................................................................................................... 73 6.2.3 Opportunities ................................................................................................................... 74 6.2.4 Threats ............................................................................................................................. 74 6.2.5 Vendor’s perspective evaluation ...................................................................................... 75

7 CASE STUDY ............................................................................................................................... 76

7.1 PROJECT OVERVIEW ................................................................................................................ 76 7.1.1 Model Company ............................................................................................................... 76 7.1.2 Model assumptions and limitations ................................................................................. 76

7.2 TCO FOR PRINTVIS 2013 ........................................................................................................ 77 7.2.1 Up-front costs .................................................................................................................. 78 7.2.2 Divestment costs .............................................................................................................. 80 7.2.3 Operational costs ............................................................................................................. 81 7.2.4 Comparison ...................................................................................................................... 82 7.2.5 Discounted cash flow model ............................................................................................ 84

7.3 PROPOSED SOLUTION AND NOTICE TO THE RESULTING CONTEXT .......................................... 85

SUMMARY, CONCLUSIONS AND FUTURE RESEARCH ......................................................... 87

PROPOSED MEASURES ................................................................................................................... 90

REFERENCES ..................................................................................................................................... 91

LIFT OF PICTURES ........................................................................................................................... 96

LIST OF TABLES ............................................................................................................................... 96

LIST OF FIGURES ............................................................................................................................. 97

LIST OF ACRONYMS ....................................................................................................................... 97

LIST OF APENDICES ........................................................................................................................ 99

9

INTRODUCTION

Enterprise resource planning (ERP) is a core business application practically for every single medium

and large enterprise. This market segment is becoming extremely saturated, thus prompt vendors

to look for new opportunities. ERP systems are becoming no longer a fancy solution only for large

businesses; smaller companies also want a piece of the action. On the other hand due to its costs,

complexity and inflexibility, ERP still remains out of reach for most of them.

One of the current biggest phenomenon, which seems to address these obstacles and pushing barriers

of business applications further is cloud computing. This technology is still emerging and walking

on its cutting edge might be challenging and risky but at the same time highly lucrative

as Gartner (2011) says: “There is always a risk of adapting the technology too soon, but there is

also a risk, perhaps a bigger risk, of adapting the technology too late.” It looks like newly cloud

adopters have achieved tremendous growth during the past five years focusing on the unpenetrated

SME segment. Today’s major ERP companies are seeing this transition and they also want to join

the “cloud-run”. Nevertheless adopting the cloud approach means rethink the whole ERP business

and alternating established selection, selling, implementation, and maintenance processes.

This thesis research focuses on the ERP in cloud approach which is compared with the traditional

on-premise model. For the practical application the “Microsoft Dynamics NAV 2013 in cloud”

with a vertical solution “PrintVis in cloud” for printing industry will be chosen. These products are

Microsoft’s respond to the paradigm shifting towards cloud ERP, and both were released just recently.

Motivation for this thesis research is the newness and unexplored nature of the subject. This thesis is

dedicated for ERP implementation partners and clients who are looking to adopt the ERP in cloud with

the particular focus on printing industry. The main goal of this thesis is to describe the changes

in the selection, selling, implementation and maintenance processes with the application on the above

mentioned ERP system. Furthermore, outline the benefits and drawbacks of the ERP in cloud

and the potential market segment. Research questions and hypothesis are determined as following:

Q1: “What are the estimated costs and time of implementation of the cloud solution in comparison

with on-premise model?”

Q2: “Could the cloud solution of PrintVis be the future for the printing industry? Main

benchmarks are estimated number and size of possible clients feasible for this solution,

other metrics will be outlined in the thesis.”

H1: “PrintVis in cloud solution implementation project can reduce up to 30% of both customer’s

budget and implementation time.”

10

H2: “For companies in the printing industry below fifty employees considering an ERP adoption

PrintVis in cloud represents a better solution than on-premise PrintVis in the horizon of ten years.

Metrics will be outlined in the thesis.”

Structure of the thesis

The theoretical part is subdivided into two chapters. First chapter defines the cloud computing.

During last decade there was no clear and widely accepted definition of Clouds in the literature that

should help to determine the areas of research and explore new application domains for the usage

of the Clouds. National Institute of Standards and Technology (NIST) novel comprehensive definition

released in 2011 should be now accepted as a way for standardization of cloud services for both

providers and consumers. The first chapter is also dedicated to the underlying economics of cloud

computing examined by Microsoft. The second chapter focuses on the ERP, its evolution through

time, delivery models, and the changes linked with the cloud approach in selection, selling,

implementation, and maintenance processes.

The practical part is subdivided into five chapters, covering thus chapters 3-7. The third chapter

describes the companies involved in this thesis research, presenting the interrelation between them

with focus on NAVERTICA which is the main recipient of this thesis research. The fourth chapter

describes the MS Dynamics NAV 2013 and PrintVis 2013 with the weight given on the cloud

approach. In the end of this chapter, the Windows Azure cloud platform is described. The fifth chapter

is dedicated to the market analysis. Firstly, the global ERP market is analyzed, new trends are outlined

and then NAVERTICA’s strategic markets – South Africa and Czech Republic are analyzed in more

detail. In the end of the chapter a quick financial analysis of the printing industry in Czech Republic is

conducted. The sixth chapter consist in a SWOT analysis of the cloud ERP solution from both

customer’s and vendor’s perspective. In the final chapter a case study is conducted. The case study is

based on an actual implementation of PrintVis for a NAVERTICA’s client. The implementation was

delivered as on-premise, in our case study we reengineer this project as cloud-based and build

a comparison model.

Data Collection

The literature review is conducted mainly from recent articles and complementary data are collected

directly from Microsoft and NovaVision, as no unifying literature on this subject was found

both in Czech and international resources. The relation between key terms is discussed

with consultants in NAVERTICA.

Due to explorative nature of the subject, semi-structured interviews are chosen as this enables

also refining the questions and answers, if needed. Validity of interview data can be verified

from complementary data sources and interviews can be used for exploring relationships

of phenomena and for creation of new hypothesis (Regnell, 2011, p. 16).

11

The target group of interviewees is employees in the companies NAVERTICA, NovaVision,

and ARDAN. Within this group heterogeneous respondents who would offer a different perspective

on the cloud solution are spotted. Interviews are adjusted for each respondent based on his role

in an implementation project of an ERP solution. All the respondents have deep understanding of ERP

business. Interviews for NovaVision aims on the cloud solution of PrintVis which they started

to implement through pilot campaigns since April, 2013. Example of the interviews question can be

found in the Appendix G. The series of interviews will be conducted over a long period starting

with my internship in ARDAN in July – November. Afterwards interviews will continue until April,

2014.

Table 1: Respondents overview

Respondent Role Company

Guido Codini Project manager, Consultant ARDAN

Kit Tomshøj Salesperson NovaVision

Jörg Hüner Senior Consultant NovaVision

Tomáš Miklík Consultant NAVERTICA

František Vymazal Project manager, Consultant NAVERTICA

Petr Turek Salesperson NAVERTICA

Source: author

12

THEORETICAL PART

1 CLOUD COMPUTING

Cloud systems are hardware-based services offering compute, network and storage capacity where

hardware management is highly abstracted from the buyer, buyers incur infrastructure costs as variable

OPEX and infrastructure capacity is highly elastic (Forrest, 2009, p. 12). Cloud computing represent

nowadays one of the most important trends in ICT and IS technologies (Basl, 2011, p. 45).

In the hype period of cloud computing software vendors were often advertising their solutions

as cloud-based without actually meeting the criteria which a cloud solution requires. The expectations

were high and cloud was more of a fuzz word which stood for a cutting edge technology. Cloud

computing wasn’t standardized and there were many different definitions available in the literature

often contradicting each other. Apart from the technological innovation cloud computing is linked

with new business model that need to be understand. Vendors that haven’t understood this model can’t

perceive nor provide the benefits of cloud computing and they put the entire concept in a bad light.

CEO of NetSuite, which is a cloud-born ERP company, claims: “There are real clouds and fake

clouds. The fake clouds are people who are taking existing technology and saying, ‘We can host it for

you, and that’s the cloud’” (Nelson, 2010). The cloud computing was standardized in 2011

by the National Institute of Standards and Technology (NIST).

1.1 Essential characteristics

NIST (2011) defines five essential characteristics that must embrace a system to be qualified

as a cloud solution. There characteristics are:

• On-demand self-service: A consumer can unilaterally provision computing capabilities,

such as server time and network storage, as needed automatically without requiring human

interaction with each service provider.

• Broad network access: Capabilities are available over the network and accessed through

standard mechanisms that promote use by heterogeneous thin or thick client platforms

(e.g., mobile phones, tablets, laptops, and workstations).

• Resource pooling: The provider’s computing resources are pooled to serve multiple

consumers using a multitenant model, with different physical and virtual resources

dynamically assigned and reassigned according to consumer demand. There is a sense

of location independence in that the customer generally has no control or knowledge

over the exact location of the provided resources but may be able to specify location

at a higher level of abstraction (e.g., country, state, or datacenter). Examples of resources

include storage, processing, memory, and network bandwidth.

• Rapid elasticity: Capabilities can be elastically provisioned and released, in some cases

automatically, to scale rapidly outward and inward commensurate with demand.

To the consumer, the capabilities available for provisioning often appear to be unlimited and

can be appropriated in any quantity at any time.

13

• Measured service: Cloud systems automatically control and optimize resource use

by leveraging a metering capability 1 at some level of abstraction appropriate to the type

of service (e.g., storage, processing, bandwidth, and active user accounts). Resource usage can

be monitored, controlled, and reported, providing transparency for both the provider

and consumer of the utilized service.

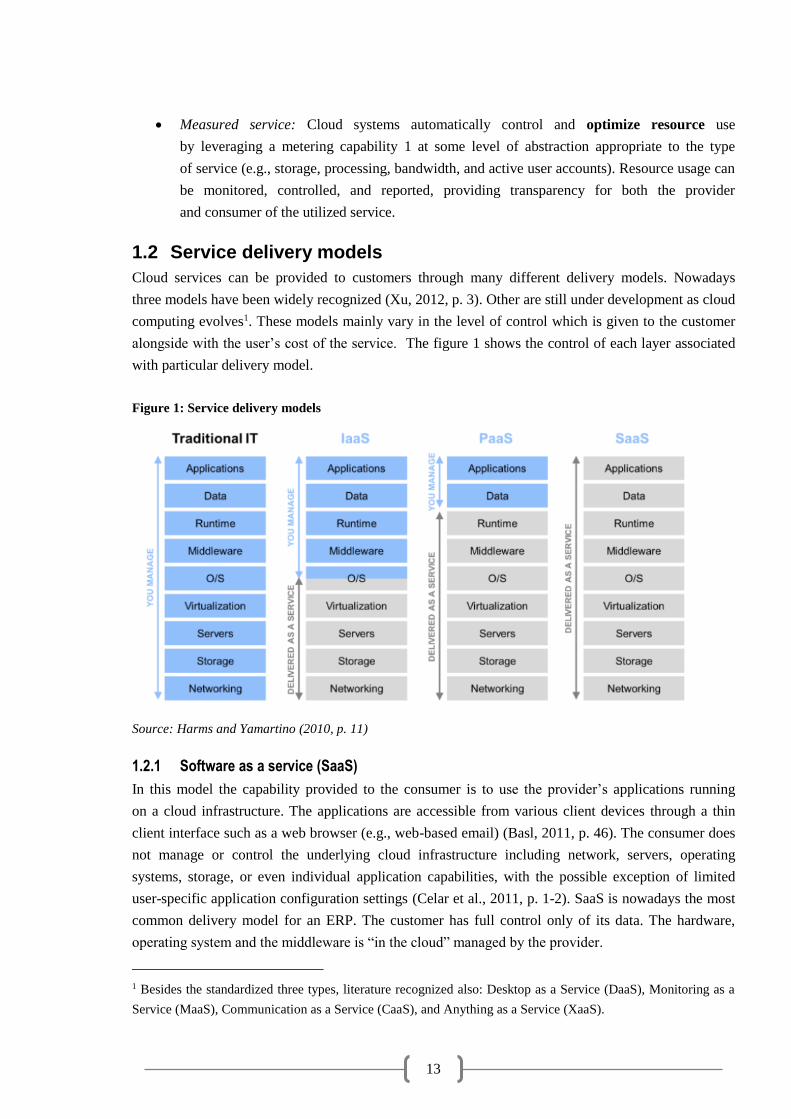

1.2 Service delivery models

Cloud services can be provided to customers through many different delivery models. Nowadays

three models have been widely recognized (Xu, 2012, p. 3). Other are still under development as cloud

computing evolves1. These models mainly vary in the level of control which is given to the customer

alongside with the user’s cost of the service. The figure 1 shows the control of each layer associated

with particular delivery model.

Figure 1: Service delivery models

Source: Harms and Yamartino (2010, p. 11)

1.2.1 Software as a service (SaaS)

In this model the capability provided to the consumer is to use the provider’s applications running

on a cloud infrastructure. The applications are accessible from various client devices through a thin

client interface such as a web browser (e.g., web-based email) (Basl, 2011, p. 46). The consumer does

not manage or control the underlying cloud infrastructure including network, servers, operating

systems, storage, or even individual application capabilities, with the possible exception of limited

user-specific application configuration settings (Celar et al., 2011, p. 1-2). SaaS is nowadays the most

common delivery model for an ERP. The customer has full control only of its data. The hardware,

operating system and the middleware is “in the cloud” managed by the provider.

1 Besides the standardized three types, literature recognized also: Desktop as a Service (DaaS), Monitoring as a

Service (MaaS), Communication as a Service (CaaS), and Anything as a Service (XaaS).

14

1.2.2 Infrastructure as a service (IaaS)

In this model the capability provided to the consumer is to provision processing, storage, networks,

and other fundamental computing resources where the consumer is able to deploy and run arbitrary

software, which can include operating systems and applications. The consumer does not manage

or control the underlying cloud infrastructure but has control over operating systems; storage,

deployed applications, and possibly limited control of select networking components (e.g., host

firewalls) (Celar et al., 2011, p. 1-2). Infrastructure as a service is also used in the ERP in cloud

solution as an underlying platform, where the system is deployed e.g. Windows Azure. This type of

delivery model offers bigger possibilities in terms of management for the customer. He can control its

data, middleware and also the operating system.

1.2.3 Platform as a service (PaaS)

This type of service is nowadays not used in the ERP in cloud solutions. In this model the capability

provided to the consumer is to deploy onto the cloud infrastructure consumer-created or acquired

applications created using programming languages and tools supported by the provider. The consumer

does not manage or control the underlying cloud infrastructure including network, servers, operating

systems, or storage, but has control over the deployed applications and possibly application hosting

environment configurations (Celar et al., 2011, p. 1-2).

1.3 Deployment models

Deployment models differentiate between where the underlying cloud computing hardware is placed

and which part of data are shared between users.

1.3.1 Private cloud

In the private cloud data and processes are handled as a one to one. Private clouds don’t share the

application, thus significantly undermine the multitenancy condition. The multitenancy occurs only on

a hardware level by resource pooling in a data centers. Private clouds can be used

for deploying an ERP system. In this case, the ERP can be customized at the cost of multitenancy.

This approach is nowadays typical for LE that chooses a cloud service.

1.3.2 Public cloud

The public cloud services are offered via the internet; the supplier provides a control mechanism for its

users only. Public cloud is the only deployment model that satisfies all the conditions for cloud

and brings all the benefits and drawbacks of cloud computing. This model is most common for the

ERP solutions, where the application is shared across a large number of clients.

1.3.3 Hybrid cloud

Hybrid cloud is a combination of a public cloud interacting with a private one.

1.3.4 Community cloud

Community cloud is controlled and used by a group of organizations that share the same interests.

15

1.4 Subscription pricing models

Cloud computing applications are sold under “new” pricing models which enables the flexibility

of these solutions. The most common models include “pay-as-you-go”, “pay-per-user”.

1.4.1 Pay as you go

In this model the customer pays only when he uses the service per a given unit e.g. per time,

per gigabyte, per processor time etc. This model associates directly provided cloud resources

with the customer usage of the service.

1.4.2 Pay per user

In this model the customer pays a fixed price per user per a given time unit (mostly month).

This model is less flexible but on the other hand the customer knows in advance how much he is going

to pay for any period of time. For example NetSuite CRM price begins at 79 USD per month

for users2. These models can be combined with each other and also combined with a fixed price.

For example a price of a cloud ERP can figure in a fixed price for implementation + price per user

accessing the service + price per computing power consumed.

1.5 Economics of the cloud

In this chapter we will outline economic efficiency of the cloud. “Underlying economics have a much

stronger impact on the direction and speed of disruption as technological challenges are resolved

or overcome through the rapid innovation we have grown accustomed to” (Harms and Yamartino,

2010, p. 3).

Cheaper technology is high likely to be adopted over time. For example we can look at a shift

from the mainframe terminal model to the client/server model during 1989 to 1995. This technology

shift could be considered as an equally big shift, from an architectural perspective, as cloud computing

is today (Höllwarth, 2012, p. 46-47). Figure 2 shows the adoption curve within the period 1989-1995

Figure 2: Adoption curve of a client/server model

Source: “How convention shapes our market” longitudinal survey, Shana Greenstein (1997)

2 According to publicly available pricelist in 2012. Source: http://www.erpsoftware-news.com/2012/10/netsuite-

pricing-.html

16

From the figure 2 we can see that the “Mainframe Only” approach have dropped from over 75%

to less than 25% within 15 years. The technology that was initially viewed as a “toy” technology

gradually replaced the mainframe model (Harms and Yamartino, 2010, p.3). A similar shift then

happened later with emergence of server virtualization. Several concerns from security issues to a

vendor lock-in raised and yet underlying economics of 20 to 30 percent savings3 compelled vendors to

overcome these concerns, and adoption quickly accelerated. Table 2 shows the technological and

economic aspects and related business model of the three above mentioned approaches.

Table 2: Cloud opportunity

Technology Economic Business Model

Mainframe Centralized compute and

storage

Optimized for efficiency

because of the high cost

High up-front costs for

hardware and software

Client/Server PCs and servers for

distributed compute,

storage, etc.

Optimized for agility

because of the low cost

Perpetual license for OS

and application software

Cloud Large DCs, ability to

scale, resource pooling,

broad network access

Optimized for efficiency

and elastic demand

Ability to pay as you go,

and only for what you use

Source: Author based on Harms and Yamartino (2010, p. 3)

The cost savings of the cloud are all about economies of scale. In economic terms, economies of scale

refers to the situation in where the cost of producing an additional unit of output (i.e., the marginal

cost) of a product (i.e., a good or service) decreases as the volume of output (i.e., the scale

of production) increases (Oza, 2012, s. 2). The economies of scale for the cloud can be divided in three

separate areas, which are supply-side savings, demand-side aggregation and multitenancy efficiency.

1.5.1 Supply-side savings

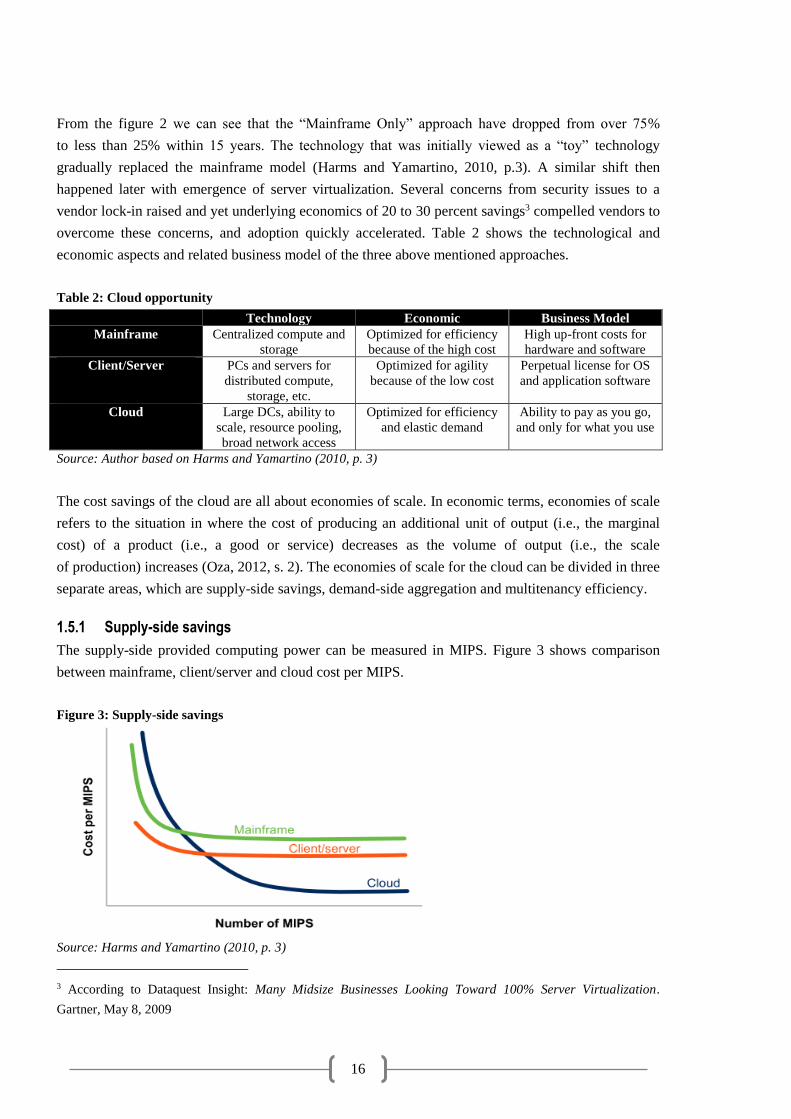

The supply-side provided computing power can be measured in MIPS. Figure 3 shows comparison

between mainframe, client/server and cloud cost per MIPS.

Figure 3: Supply-side savings

Source: Harms and Yamartino (2010, p. 3)

3 According to Dataquest Insight: Many Midsize Businesses Looking Toward 100% Server Virtualization.

Gartner, May 8, 2009

17

Reasons for the supply-side economies of scale are lower cost of electricity; lower infrastructure

labors costs and buying power of large DCs. Cloud computing is directly associated with Large DCs

because the computing power can be delivered anywhere via the internet.

The cost of electricity represents 15-20% of Total Cost of Ownership (TCO). Large DCs can pay less

than one-fourth of the national average electricity rate through bulk purchase agreements4.

The cloud service is provided through internet, thus the data center can take advantage of geographical

variability in electricity rates.

Infrastructure labor costs drops significantly at any scale due to “on demand self-service” character

of the cloud computing. While a single system administrator can service approximately 140 servers

in a traditional enterprise, in a cloud DC it would be thousands of servers. In closing infrastructure

deals operators of Large DC can get discounts up to 30 percent over smaller buyers thanks to their

buying power (Harms and Yamartino, 2010, p. 4).

1.5.2 Demand-side aggregation

The overall cost of IT is determined not only by the cost of capacity, but also by the degree to which

the capacity is efficiently utilized. In a non-virtualized data center, where each workload typically runs

on its own physical server the utilization has been extremely low around 5 to 10 percent.5 This low

level of utilization is a consequence of highly variable over time workloads which often demand large

amounts of resources in one minute and virtually none the next. The high variability arises from

service utilization randomness, time-of-day patterns, uncertain growth patterns etc.

A key economic advantage of the cloud computing is its ability to address variability in resource

utilization. By pooling resources, variability is diversified away, evening out utilization patterns.

The larger the pool of resources, the smoother the aggregate demand profile, the higher the overall

utilization rate, and the cheaper and more efficiently the IT organization can meet its end-user

demands (Harms and Yamartino, 2010, p. 8).

1.5.3 Multitenant efficiency

The previously described supply-side and demand-side economies of scale can be also achieved

to a certain extend by using virtualization and server hosting. But there is another important source

of economies of scale that can be harnessed only in true cloud multitenant architecture.

4 Source: U.S. Energy Information Administration (July 2010) and Microsoft. While the average U.S.

commercial rate is 10.15 cents per kilowatt hour, some locations offer power for as little as 2.2 cents per kilowatt

hour.

5 Based on: The Economics of Virtualization: Moving Toward an Application-Based Cost Model, IDC,

November 2009

18

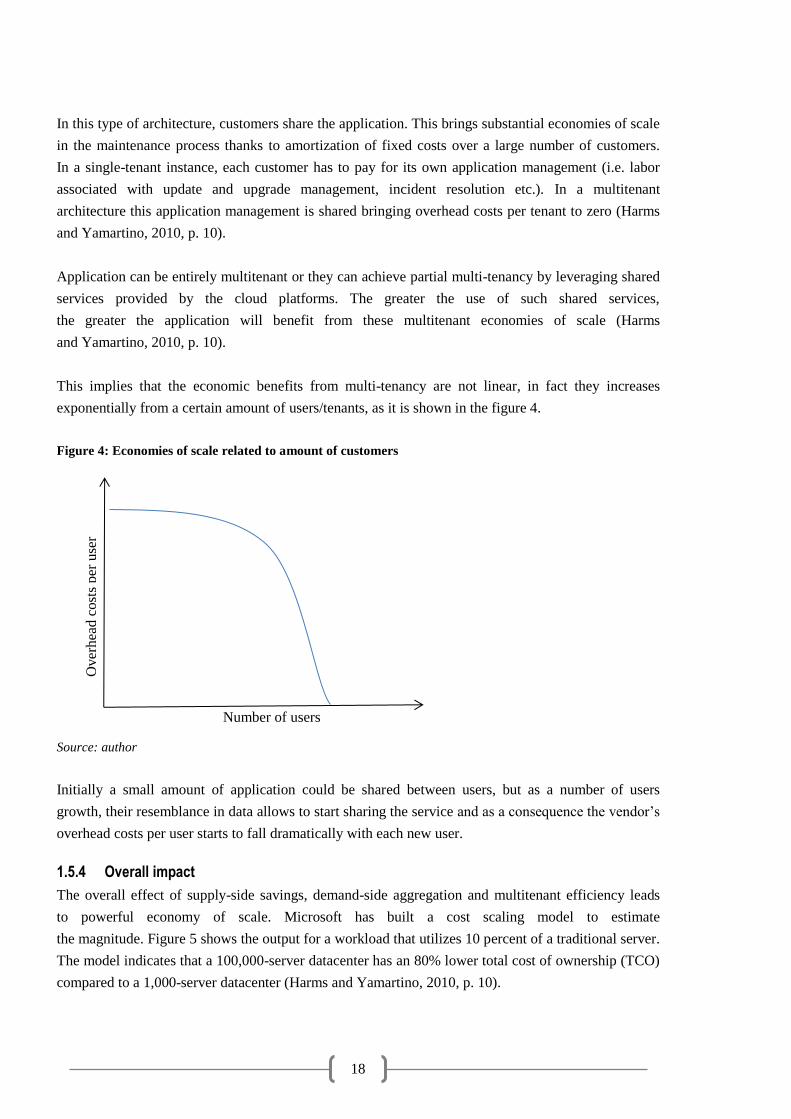

In this type of architecture, customers share the application. This brings substantial economies of scale

in the maintenance process thanks to amortization of fixed costs over a large number of customers.

In a single-tenant instance, each customer has to pay for its own application management (i.e. labor

associated with update and upgrade management, incident resolution etc.). In a multitenant

architecture this application management is shared bringing overhead costs per tenant to zero (Harms

and Yamartino, 2010, p. 10).

Application can be entirely multitenant or they can achieve partial multi-tenancy by leveraging shared

services provided by the cloud platforms. The greater the use of such shared services,

the greater the application will benefit from these multitenant economies of scale (Harms

and Yamartino, 2010, p. 10).

This implies that the economic benefits from multi-tenancy are not linear, in fact they increases

exponentially from a certain amount of users/tenants, as it is shown in the figure 4.

Figure 4: Economies of scale related to amount of customers

Source: author

Initially a small amount of application could be shared between users, but as a number of users

growth, their resemblance in data allows to start sharing the service and as a consequence the vendor’s

overhead costs per user starts to fall dramatically with each new user.

1.5.4 Overall impact

The overall effect of supply-side savings, demand-side aggregation and multitenant efficiency leads

to powerful economy of scale. Microsoft has built a cost scaling model to estimate

the magnitude. Figure 5 shows the output for a workload that utilizes 10 percent of a traditional server.

The model indicates that a 100,000-server datacenter has an 80% lower total cost of ownership (TCO)

compared to a 1,000-server datacenter (Harms and Yamartino, 2010, p. 10).

Number of users

Over

hea

d c

ost

s per

use

r

19

Figure 5: Total cost of ownership in the cloud

Source: Harms and Yamartino (2010, p. 10)

Microsoft’s partners argue that renting a cloud infrastructure from a third party, for example Windows

Azure, can’t drive profits to them (Miklík, 2014). The above figure shows that this is actually not

the case. Large data centers provide economies of scale up to 80% of Total Cost of Ownership (TCO),

thus delivering profit to themselves, partners and customers.

20

2 ERP

There are many definitions of ERP systems in the literature; moreover the definition has been

changing alongside with the evolution of ERP systems. Klaus el al. (2000, 141) have summarized

more than 100 articles related to ERP systems and defined ERP from three perspectives:

“First, and most obviously, ERP is a commodity, a product in the form of computer software. Second,

and fundamentally, ERP can be seen as a development objective of mapping all processes and data

of an enterprise into a comprehensive integrative structure. Third, ERP can be seen as the key element

of an infrastructure that delivers a solution to business.”

2.1 Evolution of ERP

In the early days of business applications most organization designed, developed and implemented

own in-house computing systems. These were legacy systems based on programing languages such

as COBOL, ALTGOL and FORTRAN (Liaquat and Hossain, 2002, p. 4). In 1960 IBM have

developed the first software for material requirement planning – MRP (Vymětal, 2010, p.26). Besides

General Ledger, MRP was the first off-the-shelf business application (Orlicky, 1975, p. 37). MRP

supported the bill-of-materials across all products and parts in one or more plants. Furthermore, this

solution contained bill-of-materials processors (demand-based planning) and forecasting algorithms

(Klaus et al., 2000, p.144). From technological perspective MRPs ran on mainframes, thus requiring

huge upfront investments.

Many other companies started to build their own MRP solutions. SAP, Oracle and Infor were born

in 1970s. Under the pressure of these companies development of MRP accelerated significantly

and in the late 1970s, Material Requirement Planning evolved into Manufacturing Resource Planning

– MRP II (Vymětal, 2010, p.26). Production planning became much more complex and accurate, as it

is shown in figure 6.

Figure 6: Production planning within MRP II

Source: author based on (Klaus et al., 2000, p. 145)

In the late 1980s the MRP II approach was extended in order to include all business-administrative

and technical functions of a company, although integration of these functions remained an issue.

The late MRP II systems included shop floor, distribution management, project management, finance,

human resource and engineering, thus becoming already very close to what is known as today’s ERP

(Liaquat and Hossain, 2002, p. 4). The ERP term started to appear in the literature.

21

In 1992 SAP R/3 system was released, which was the first integrated ERP. This started a new stage

as marketplace gained considerable momentum after 1995 accompanied by strong ERP coverage

in the trade press (Klaus et al., 2000, p. 152). From technological perspective ERP systems started

to run on a client/server architecture model lowering significantly hardware costs, thus allowing

medium enterprises to afford these solutions.

After 1995 vendors started adding more modules and functionality to their core modules giving birth

to the “extended ERP” or ERP II. Basl (2008) defines ERP II to cover following areas (above the

standard ERP):

• Supply Chain Management (SCM),

• Customer Relationship Management (CRM), and

• Business Intelligence (BI)

The core difference is the Business Intelligence functionality which combines data gathering, data

storage and knowledge management with analysis to provide input to the decision process (Negash

and Gray, 2008, p. 175).

Cloud computing is considered to be a next step in the history of enterprise software e.g. Luoma

and Nyberg (2011, p. 3-4); Gartner (2012) and others. Despite the idea of cloud computing is rather

old, first ERP systems started to occur in the New Millennium. These first pioneer solutions were

provided by „Application service providers” and they were basically hosted solutions. The cloud

computing took off in the mid-2000s and during a very turbulent era many under radar ERP solutions

were born. The “cloud-run” started after the economic crisis of 2008 for two reasons.

Firstly, the restricted loan policy, which took place, has frozen large investment in on-premise ERP.

Secondly, the saturation of the LE market has prompt ERP vendors to look for new opportunities.

New cloud born players such as NetSuite and Salesforce have gone through an astonishing period of

growth during 2009-2014. This didn’t remain unheeded by the major three ERP players (SAP, Oracle,

Microsoft), which have responded to the market demand releasing own cloud solutions of their on-

premise ERPs during the period 2011-2013.

2.2 ERP delivery models

The response of existing players gives ERP customers today a range of deployment options. They can

choose on-premise ERP, hosted ERP, cloud-enabled ERP, or a hybrid deployment of any of them.

The varied responses by traditional ERP providers to the threat from new cloud-only ERP vendors

have created market uncertainty (Scavo et al., 2012).

22

2.2.1 On-premise ERP

On-premise ERP solutions are usually sold via a license model. The software is then loaded onto

servers and computers in-house. The enterprise controls the infrastructure and platforms. Furthermore,

the enterprise handles and absorbs the costs of maintaining the servers and the space they require,

as well as disaster recovery (Fesak et al., 2012, p. 2).

2.2.2 Cloud ERP

Cloud ERP systems are sold via a subscription pricing model, see chapter 1.4 and delivered

to the customer via SaaS. Cloud computing essentially enables an outsourcing arrangement

of the IT department, where enterprise software is hosted on a SaaS vendor’s or third party

infrastructure and rented to a customer at a fraction of the costs compared with on-premise solutions

(Faasen et al., 2013, p. 36). Cloud-based ERP solutions appear to provide a number of benefits related

to sizable cost savings, competitive advantage enhancements, and flexibility of the solution.

Many authors agree on the unwillingness of SMEs to adopt on-premise ERP software due to the high

up-front costs and risk involved (Buonanno et al., 2005, p. 420) and for example Forrest (2009, p. 20)

claims: “Cloud offerings are very cost effective for SME primarily because of the subscription based

pricing schemes that typically re-quire significantly lower upfront investments”.

2.2.3 Hosted ERP

Hosted ERP systems are a hybrid solution where a customer rents the hardware from the vendor and

lease the license. The ERP is delivered in a private cloud, thus with a limited multitenancy efficiency.

This solution was provided in early 2000s by Application service provider (ASP).

2.3 Process of sale and selection

Nowhere is the buying experience changing more than in the software industry. In order to sell cloud

ERP to SMEs a whole new business model is required. The following chapter will describe the impact

of cloud ERP on customer’s perception of the service, buying decision making and service marketing.

2.3.1 Buying decision making

Large IT sales transaction between a vendor and its customer are the result of negotiations based

on a common understanding of several parameters (Brill, 2013, s.2). The basic relationship

is captured in the figure 7.

23

Figure 7: Information and the Commercial Negotiation

Source: Brill (2013, p.2)

Both the vendor and the customer have imperfect and mutually influenced assessments

of the negotiation based on their perception of the highly complex parameters involved. The customer

makes a buying decision based on the six parameters of commercial negotiation outlined

in the figure 7. “Use-cases & Future growth” usually plays the highest role (Brill, 2013, p.2).

Traditional on-premise selling model consists in a series of presentations called demos where the sales

team does its best to make a prospect6 understand how the system handles his typical business cases.

While prospects get a demonstration of the product capabilities, they usually don’t have opportunity

to get hands-on experience with the product.

Reducing the risk of limited knowledge of the product is one of the biggest advantages of the cloud

solution. According to Domergue (2009) when selling cloud solutions the real value is unveiled

to the customer. Since cloud solutions are available through internet, there is no need to install

the system in customer’s facilities and the customer can try the solution with demo data online.

This typical SaaS sales process often leads to an initial sale of only few seats. This is certainly

a drawback for a vendor, but a small initial sale implies a relatively low initial price, which minimizes

the requirements for drawn-out evaluations of return on investment. Moreover if the system proofs its

real value, it will inevitably acquire more users within an organization (Chappell, 2012, p.11).

2.3.2 Customer lock-in

Customer lock in is a common phenomenon in ERP business because of large investment needed,

information asymmetry and high switching costs. The customer buys the product without actually

knowing if the solution will meet his expectations. On the other hand the vendor’s interest is to sell

the product no matter what. Once the solution is live high switching costs keeps the customer locked

6 In the ERP business a potential customer is referred as prospect.

"The Deal"

Vendor

Commercial Negotiation

•Expected vs. Actual budget

•Competitive information

•Use-cases & Future growth

•Licensing & Pricing rules

•Complete Purchase History

•Assets in the IT Environment

Customer

24

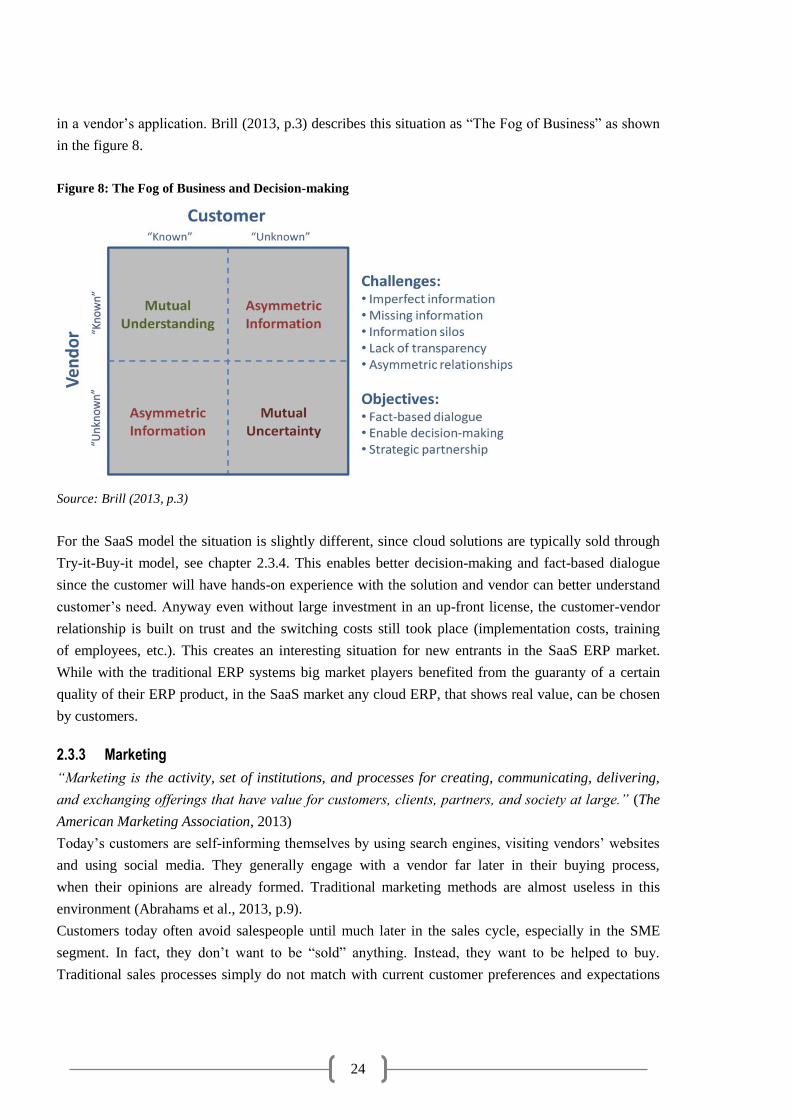

in a vendor’s application. Brill (2013, p.3) describes this situation as “The Fog of Business” as shown

in the figure 8.

Figure 8: The Fog of Business and Decision-making

Source: Brill (2013, p.3)

For the SaaS model the situation is slightly different, since cloud solutions are typically sold through

Try-it-Buy-it model, see chapter 2.3.4. This enables better decision-making and fact-based dialogue

since the customer will have hands-on experience with the solution and vendor can better understand

customer’s need. Anyway even without large investment in an up-front license, the customer-vendor

relationship is built on trust and the switching costs still took place (implementation costs, training

of employees, etc.). This creates an interesting situation for new entrants in the SaaS ERP market.

While with the traditional ERP systems big market players benefited from the guaranty of a certain

quality of their ERP product, in the SaaS market any cloud ERP, that shows real value, can be chosen

by customers.

2.3.3 Marketing

“Marketing is the activity, set of institutions, and processes for creating, communicating, delivering,

and exchanging offerings that have value for customers, clients, partners, and society at large.” (The

American Marketing Association, 2013)

Today’s customers are self-informing themselves by using search engines, visiting vendors’ websites

and using social media. They generally engage with a vendor far later in their buying process,

when their opinions are already formed. Traditional marketing methods are almost useless in this

environment (Abrahams et al., 2013, p.9).

Customers today often avoid salespeople until much later in the sales cycle, especially in the SME

segment. In fact, they don’t want to be “sold” anything. Instead, they want to be helped to buy.

Traditional sales processes simply do not match with current customer preferences and expectations

25

(Abrahams et al., 2013, p.9). The engagement point of on-premise compared to cloud (SaaS) is shown

in the figure 9.

Figure 9: Buying cycle evolution

Source: Chappell (2012, p.11)

Internet has become a key element in software business, and it is crucial for the marketing strategy

of software firms throughout the business cycle. Areas that have been affected by internet include

for example promotion, sales, payments, downloading the product, after-sale services, updates,

and monitoring accounts. Internet is especially potential marketing medium for smaller software firms,

because it can help them to better compete with larger competitors (Hu and McNaughton, 2011,

p. 107).

2.3.4 Try-it-Buy-it model

The line between Sales and Marketing is blurred for Cloud ERP partly because of the Try-it-Buy-it

model. The whole idea is rooted in providing the software to the customer before he buys it

for a limited time period or with limited functionality. Customer is than more willing to buy

the product, since he has perceived its real value.

The concept is not entirely new, proprietary packaged software was and still is commonly offered

as shareware, trial ware which is based on the same concept. Offering ERP systems via this model was

unthinkable before cloud computing. This approach was immediately adopted by cloud-born ERP

players like NetSuite, Salesforce and others7.

For example NetSuite offers a “test drive”8 of their ERP for a trial period of 14 days. The customer has

to do an online registration where he specifies basic details of his company. Afterwards he gets the

access to a demo company tailored to the industry segment he specified. He is also assisted by a

specialized consultant. Furthermore he gets the access to the manual which guides him through the

“test drive”.

7 Already many partners started to offer Dynamics NAV in cloud; these partners use the Try-it-Buy-it model. For

example: http://www.saasplaza.nl/dynamics-nav-azure-cloud.html

8 Source: http://www.trajectoryinc.com/ns_evaluationsales.html

26

2.4 Process of implementation

Process of implementation of an ERP is the most critical, as well as, the most resource consuming

phase of the project (Haddara and Zach, 2011, p.4). LI et al. (2006) divides the ERP implementation

process into six stages: initiation, adoption, adaptation, acceptance, routinization and infusion.

Microsoft has developed a similar six stage methodology called “Sure Step” for its ERP systems,

which can be seen in the figure 10.

Figure 10: Implementation project stages

Source: author based on Microsoft’s “Sure Step” methodology

The diagnostic phase defines the project scope and project plan, initial training is given

to the customer. In the analysis phase business processes are identified and document at high level.

Main goal of the design phase is conduct a fit/gap analysis9 and re-engineer business processes

in order to match them with the ERP system. The output of design phase and therefore the targeted

functionality of the ERP system have to be agreed and signed with the customer. In the development

phase all the programming work is conducted, this includes mainly customization of the ERP system.

This phase includes also data migration. This is usually also the most time-consuming phase

of the implementation project. In the deployment phase the ERP system is installed and configured.

Beside installation, configuration and feature deployment, the phase focuses on testing at system level.

When the system is ready to go live the implementation enters the operation phase. Here additional

training and support is given to the customer.

The whole implementation process is accompanied with workshops, trainings, project current state

evaluation etc. The Sure Step methodology is very specific in particular tasks that are related

to the project. This standardization is critical to make the project plan and management effective

and therefore the whole implementation process smoother.

The Sure Step methodology recognizes “Rapid Implementation” which is applicable for the cloud

solutions. The Rapid Implementation skips the Analysis, Design and Development phases because it

delivers a packaged business specific solution with minimal or no customizations. This solution is

applicable for the environment where customer’s business processes are not considered as complex

and the vendor is already familiar with the main business process specific to the industry.

2.4.1 Critical success factors

Despite the standardization, implementation projects still fail to meet the budget and buyer’s

expectations in most of the cases (Austin et al., 2003, p.3), also 2014 ERP Report (2014, p.11),

9 The analysis consists in identifying whether the present system fits the requirements, and if any such gaps are

identified, they are recorded in a prescribed format.

Diagnostic Analysis Design Development Deployment Operation

27

and 2013 ERP Report (2013, p. 13). This is due to the variability within ERP implementation projects

which makes them hard to standardize and forecast possible obstacles in the implementation project.

Various authors have offered many sets of critical success factor for the implementation phase

of an ERP system. LEYH and CRENZE (2010, p.229-230) have conducted a research over 185

relevant papers and identified top three following critical success factors:

- Project management

- User training

- Top management support.

Implementation of a cloud ERP in small enterprises differs from an on-premise implementation

mainly in the second identified success factor which is the “user training”. In cloud the training is

conducted mostly online and via e-learning materials. This “Do-it-yourself” approach is crucial

to keep the low budget, however it loads a lot of critical tasks on the customer-side. Krishnamurti

(2014) claims that key people in small enterprises are already overloaded with work thus collaborating

on the ERP implementation is always challenging.

2.4.2 Knowledge management

Knowledge management has been identified as one of the most important critical success factors in

ERP implementation (LI et al., 2006), (Deng and Bian, 2008). The implementation project length,

therefore cost, is deeply influenced by the experience build from previous implementations. LI et al.

(2006, p. 167) quotes in their research of the impact of KM on ERP implementation: “Although

realizing ERP is an implementation process, it is also a process of knowledge creation,

storage/retrieval, transfer and application from the knowledge management perspectives.”

Despite recognizing KM as significant factor during ERP implementation the magnitude of the impact

remains uncertain. Figure 11 shows the possible impact of knowledge accumulated during

implementations based on Li et al (2006) research.

Figure 11: Impact of knowledge accumulation on costs of the implementation

Source: author based on Li et al. (2006).

Number of implementations

Co

st r

educt

ion [

%]

28

Figure 12 shows that in the first implementation, there is a lot of to be learned. The diagnostic and

analysis phase together with workshops eats-up for a big slice of the budget. Every implementation

consists in learning customer’s and industry’s specific business processes, in order to do the best setup

of the ERP system. Vendors than use this know-how in future implementations, this is also referred as

“building best practices”. When the partner has build-up a lot of experience with the solution, the

impact of the knowledge accumulated from one additional implementation is nearly zero. According

to Miklík (2014) the initial effect could be around 20-30% of cost reduction per implementation. This

also depends on the company’s knowledge management system, especially how the knowledge is

stored.

Cloud ERP systems enable much higher level of knowledge building-up since they are focused

on high volumes, more implementations imply greater knowledge accumulation. The standardization

in the cloud is also easier. As a consequence costs of cloud implementations will fall more rapidly

than in the case of on-premise implementations and they will be also easier to forecast. On the other

hand the knowledge is an also a prerequisite in the cloud. In order to conduct a rapid implementation

significant knowledge about the business processes specific for the industry are necessary.

2.4.3 Cloud ERP implementation

Microsoft emphasized that in order to offer to a customer additional value of the Cloud-based solution,

the implementation must be far faster. All aspects of the implementation must be streamlined

significantly, as the hereinafter graphic illustrates, for the following reasons (Abrahams et al., 2013,

p.32):

1. User training becomes self-serve and web-based. Overall, better product design also drives

down the need for training.

2. Reporting becomes more “packaged”, and the need for custom reporting declines as result.

3. Configuration and setup is Cloud-based, “templatized” and automated.

The figure 12 above shows a comparison of tasks affected during the implementation process of a

cloud solution.

29

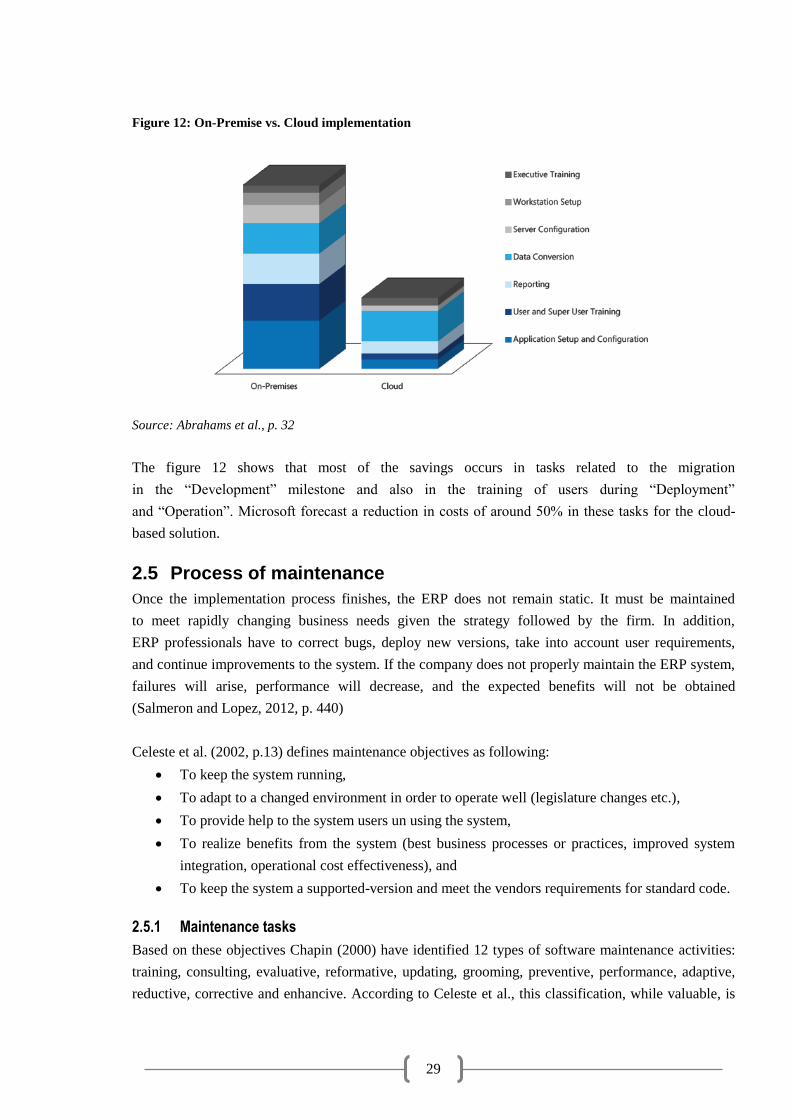

Figure 12: On-Premise vs. Cloud implementation

Source: Abrahams et al., p. 32

The figure 12 shows that most of the savings occurs in tasks related to the migration

in the “Development” milestone and also in the training of users during “Deployment”

and “Operation”. Microsoft forecast a reduction in costs of around 50% in these tasks for the cloud-

based solution.

2.5 Process of maintenance

Once the implementation process finishes, the ERP does not remain static. It must be maintained

to meet rapidly changing business needs given the strategy followed by the firm. In addition,

ERP professionals have to correct bugs, deploy new versions, take into account user requirements,

and continue improvements to the system. If the company does not properly maintain the ERP system,

failures will arise, performance will decrease, and the expected benefits will not be obtained

(Salmeron and Lopez, 2012, p. 440)

Celeste et al. (2002, p.13) defines maintenance objectives as following:

• To keep the system running,

• To adapt to a changed environment in order to operate well (legislature changes etc.),

• To provide help to the system users un using the system,

• To realize benefits from the system (best business processes or practices, improved system

integration, operational cost effectiveness), and

• To keep the system a supported-version and meet the vendors requirements for standard code.

2.5.1 Maintenance tasks

Based on these objectives Chapin (2000) have identified 12 types of software maintenance activities:

training, consulting, evaluative, reformative, updating, grooming, preventive, performance, adaptive,

reductive, corrective and enhancive. According to Celeste et al., this classification, while valuable, is

30

believed to be deficient in an ERP context because it does not consider the benefit of doing

maintenance. Celeste et al. (2002, p.14) then defines activities and their initiators in an ERP Customer-

Vendor relationship. These are outlined in table 3.

Table 3: Activities in ERP maintenance

Activity Initiator

Implementing internal change-requests ERP-using organization’s system users and IT staff

Responding or handling user-support requests ERP-using organization’s system users

Upgrading to new versions/releases Vendor

Performing patches Vendor

Source: author based on Celeste et al, p. 14

Implementing internal change-requests entail changes to the system properties such as data

dictionary, programs, screens, user interfaces, and/or documentation. These comprise data correction,

adaptation to the external environment, and enhancement of the existing functionality, and additional

functionality.

Responding or handling user-support requests is usually related to software system training, and

consultation on the system usage and functionality. In a case study conducted by Celeste et al., this

accounted for 59% of total maintenance effort10.

Upgrading to new versions/releases occurs usually over a longer period of 3-5 years and its costs are

strongly based on the complexity of the system. The complexity is reported to be a function

of the system size, system age, quality of the original system, the amount of maintenance done

previously, and software development practices (Banker et al., 1989, p. 254). The biggest factor

in the maintenance complexity is the amount of customization done during implementation and post-

implementation (Banker et al., 1989, p. 255). Customizations slow the whole maintenance efficiency

because each modification may cause extra effort in impact analysis, and re-testing the whole system

(Celeste et al., 2002, p.14). Therefore maintenance costs are increasing over time. Consequently this

may result in situations where the upgrade costs exceeds costs of a implementing a solution from

scratch.

Performing patches comprise following areas: Fixing bugs that are found in the standard code,

Adapting the ERP system to conform to a changed environment, such as Government regulations,

and Keeping the existing system up to the vendor’s standard version. These activities usually accounts

for the smallest part of maintenance.

2.5.2 Cloud ERP maintenance

Many authors11 claim that maintenance of a cloud ERP solution is much cheaper. The reasons behind

consider mainly energy, infrastructure and upgrade costs. Infrastructure and energy costs are moved

10 The percentage based on a single case study a single SAP implementation, therefore cannot be adopted as

wide-applicable.

31

from the customer-side to the vendor-side and upgrade costs are shared across a large amount

of customers due to multitenancy. Taking into account the economics of scale because of falling

overhead costs per customer outlined in chapter 1.5.3, the impact of cost savings in the maintenance

process is significantly bigger than in the selling, selection or implementation process.

From the vendor’s revenue perspective the cloud solution is also interesting. ERP maintenance is

an important source of incomes. A report (Jaconson, 2007) indicates that this revenue represent

around 36 percent of total ERP revenues. Cloud maintenance consists almost solely of training and

support services which have nowadays the highest profit margin around 70-80% among all

maintenance tasks described.12 Therefore despite having much lower amount of revenues, the profit

may look very promising for the cloud. Codini (2013) says that: “Cloud enables the true consultancy

potential of the ERP vendor, which should be the ultimate target of every ERP consulting company”.

In other words cloud delivers packaged know-how.

11 According to literature research done by Fesak (2012) 12 NetSuite profit margin on maintenance in 2012-2013.

32

PRACTICAL PART

3 PRESENTATION OF THE COMPANIES AND PARTNER

MODEL

3.1 Partner model

Microsoft Dynamics products are sold through partners all over the world. Partners act like Value

Added Resellers (VARs). Kelly (2012, s. 205) defines VARs as “partners who adds services that

an ISV cannot or do not wish to provide, such as an additional line of support, or support in the native

language.” In Microsoft VAR model, VAR handles the sales process; provide additional know-how

and localization of the product. They also provide professional services to help customers use

the product or integrate in into their existing systems i.e. customizations. The risk and revenues are

shared between Microsoft and its partners.

Complex add-ons or vertical solution can be developed by a third-party entity, which is basically

a company that develops a software build on some Microsoft Dynamics solution e.g. MS Dynamics

NAV. These companies act like Independent Software Vendors (ISVs). Gartner (2013) defines ISVs

as “a company whose primary function is to distribute software.” These ISVs sells the vertical solution

independently from Microsoft.

This research is a result of cooperation with NovaVision - the ISV selling the PrintVis solution and

both NAVERTICA and ARDAN which are Microsoft’s and NovaVision’s VARs. The relation

between these companies is shown in the figure 13. ARDAN was chosen to contribute to this research

because of extensive experience with the PrintVis solution and company strategy shift towards selling

PrintVis in cloud.

Figure 13: Partner model

Source: author

Figure 14 shows the cooperation between Microsoft, the ISV partner, and VARs partners. NovaVision

have to pay a commission for developing a vertical-solution based on MS Dynamics NAV and for

33

reselling licenses. NAVERTICA (or ARDAN) have to pay for reselling licenses of MS Dynamics

NAV and the vertical solution to NovaVision.13 Other costs involve maintenance fees.

3.1.1 NAVERTICA

NAVERTICA a.s. has been involved in the development and implementation of ERP systems since

1990 (previously under the name, FUTURE Engineering). NAVERTICA are headquartered in the

Czech Republic, with offices in Prague, Brno as well as in Bratislava, Slovakia. Additionally, the

company has a presence in Southern Africa with NAVERTICA SA, a daughter company with offices

in Johannesburg, South Africa.

NAVERTICA has continually fulfilled the requirements necessary to obtain Microsoft Gold Certified

Partner status since 2002 and was awarded many times as Microsoft Dynamics President’s Club.

NAVERTICA specialized in ERP and CRM solutions based on Microsoft Dynamics. In addition to

this, they manage a division, that is dedicated to the delivery of solutions such as intranet and

customer portals based on Microsoft SharePoint and also provides consultation services in the area

of integrated management systems (ISO 9001, ISO 14001, ISO 27001, etc.), with the former often

serving as an essential step in the delivery of a complex ERP or SW system.

Years of experience in the engineering has provided the know-how to deliver substantial added value

alongside ERP and SW systems. This added value is often higher than the value of the supplied system

and hence NAVERTICA commitment is to deliver “A Better Bottom Line” for the customer14.

In cooperation with partners NAVERTICA have developed and implemented Vertical Solutions for

the following segments:

• Service management

• Property management

• Rental and leasing management

• Health care

• Retail optical

• Government sector

• Manufacturing

• Engineering

• Printing industry

• Steel service and processing

• Material cutting/allocations

3.1.2 NovaVision Software

NovaVision Software A/S was founded in 1997 with goal to create an ultimate IT solution for printing

industry. The vision was also, to create a piece of software that could be implemented without many

13 Prior to NAV 2013, the VAR had to buy separately the standard MS Dynamics NAV from Microsoft

and the vertical solution from the ISV. 14 Source: navertica.com

34

customizations and thereby securing upgradeability for our customers.15 NovaVision choose to build-

up the solution on Microsoft Dynamics NAV which had proven to be the best possible platform to

obtain this goal. NovaVision has more than 250 customers around the globe with 30 partners

representing more than 40 countries.

3.1.3 ARDAN

ARDAN is a consulting company based in Milan, founded in 2010 as part of group “Gruppo i3”. The

company specializes itself on printing industry within the SME area. ARDAN provides practical and

innovative solutions, able to respond to the information, organizational, managerial and technological

need of a company. ARDAN implements “PrintVis” based on MS Dynamics NAV or “Print &

Packaging” based on MS Dynamics AX. ARDAN has around 20 clients, of which many companies

represent the biggest market players in the Italian and European printing industry.

15 Source: NovaVision profile presentation for partners available:

http://www.printviswiki.com/w/images/8/88/NovaVision_Profile_Presentation.ppt

35

4 MICROSOT DYNAMICS NAV 2013

“ERP systems are like wine: they get better with age” (ROYS and BABIC, 2008, p. 7). Microsoft

Dynamics NAV 2013 is the latest product of the Dynamics NAV family for small and midsize

businesses. It features new Office 2013 looking interface, closer integration with other Microsoft’s

products such as SharePoint, Outlook and Excel and better Business Intelligence. The Role-Tailored

client, which was firstly introduced in the Microsoft Dynamics NAV 2009 as an addition

to the “Classic” client has now murdered his older brother. Role-Tailored client offers a different

interface of the ERP system based on user’s assigned role. The user interface hides the complexity

of the system away from the users. This helps users to see only the relevant part of the ERP for them.

A real change has been done beneath the surface in the new three-tiered architecture

(ROYS and BABIC, 2008, p. 8). This goes far beyond the subject of this thesis, thus shortly put the

three-tiered is a precondition to have a scalable system that handles more users, internal departments

or even companies. With the three-tiered architecture it is also possible to expose any part

of the system as a Web service on the internet The NAV 2013 features a full web client, which has

been connected to the three-tier architecture. This is essential for having “a true cloud” architecture.

Together with other changes this made MS Dynamics NAV 2013 a first cloud-enabled Dynamics’

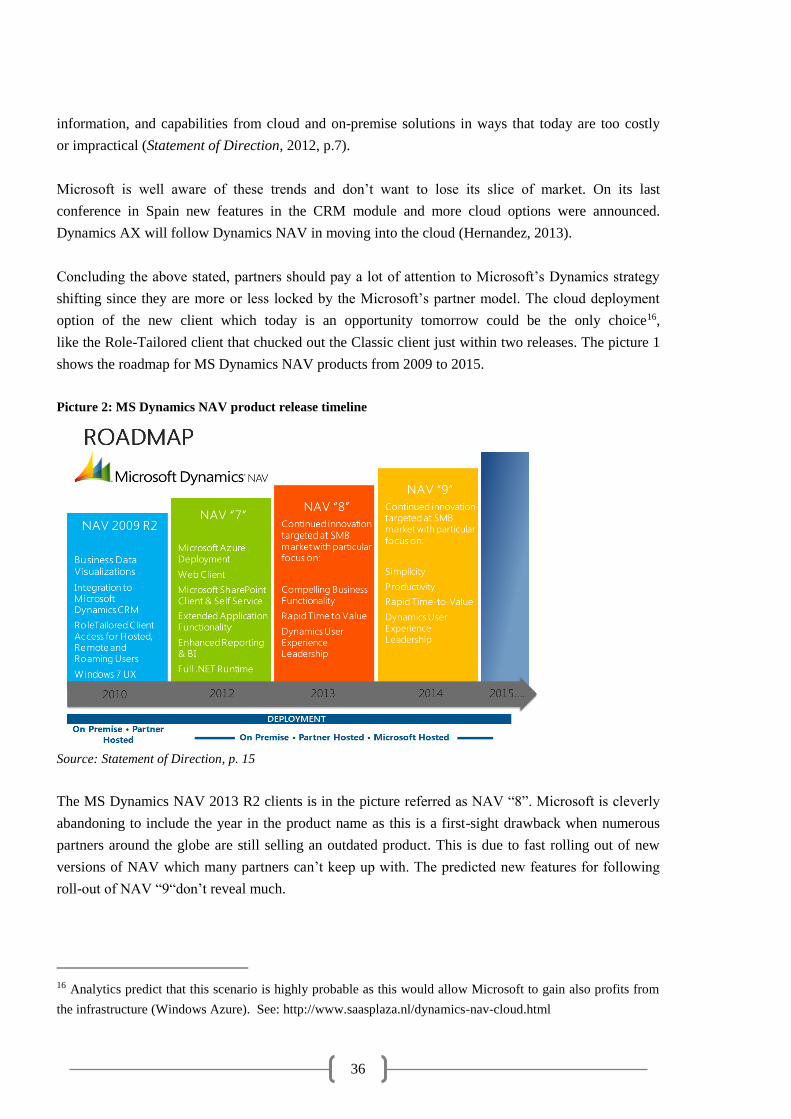

family product. Other features of this release are outlined in the picture 1 below.

Picture 1: Microsoft Dynamics NAV 2013 features

Source: Microsoft

4.1 Focused on cloud

The Cloud means both substantial opportunity and the requirement to change. The emphasis on cloud

computing in the market today has been on deployment to the cloud to reduce costs. This is

an opportunity to re-imagine business applications that deliver rich experiences with services,

36

information, and capabilities from cloud and on-premise solutions in ways that today are too costly

or impractical (Statement of Direction, 2012, p.7).

Microsoft is well aware of these trends and don’t want to lose its slice of market. On its last