Year Book September 5 2013 This is a compilation of articles and emails I shared with the people during the year. Based on your feedback and likings I have chosen the best ones. You may want to share it with your friends and colleagues. It’s a small contribution from my side to increase financial literacy in the country. I request you to please help me in spreading the message :) Vinayak Sapre

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Year

Book

September 5

2013 This is a compilation of articles and emails I shared with the people during

the year. Based on your feedback and likings I have chosen the best ones.

You may want to share it with your friends and colleagues. It’s a small

contribution from my side to increase financial literacy in the country. I

request you to please help me in spreading the message :)

Vinayak Sapre

2

INDEX

(1) Guru Vani - 3

(2) The Secret to happiness - 4

(3) Patience is the Key - 6

(4) Revolutionary changes in Health Ins… - 7

(5) Control the controllable - 8

(6) Is your employer depositing your EPF - 9

(7) How you choose to mess… - 10

(8) Because I care ☺ - 14

(9) How to protect yourself from inv scams - 15

(10) The most important attribute - 16

(11) Retirement planning for individuals - 17

(12) 5 Reasons you are earning…. - 18

(13) Why do we need financial planning - 21

3

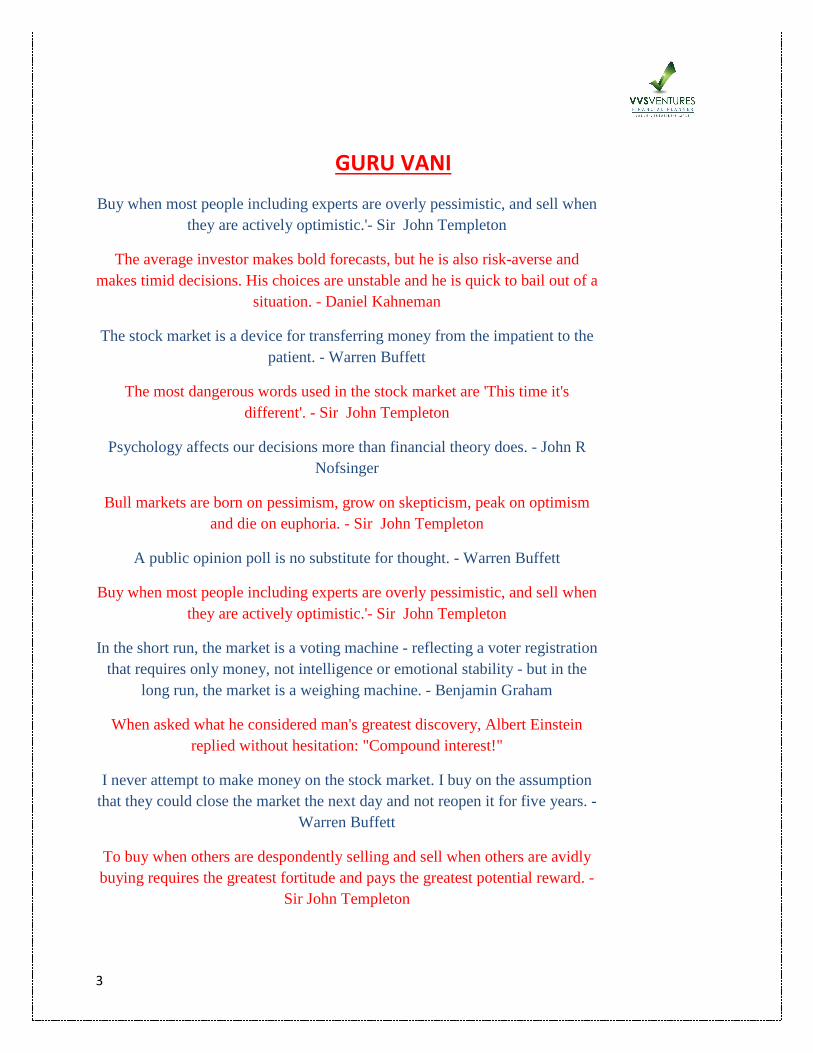

GURU VANI

Buy when most people including experts are overly pessimistic, and sell when they are actively optimistic.'- Sir John Templeton

The average investor makes bold forecasts, but he is also risk-averse and makes timid decisions. His choices are unstable and he is quick to bail out of a

situation. - Daniel Kahneman

The stock market is a device for transferring money from the impatient to the patient. - Warren Buffett

The most dangerous words used in the stock market are 'This time it's different'. - Sir John Templeton

Psychology affects our decisions more than financial theory does. - John R Nofsinger

Bull markets are born on pessimism, grow on skepticism, peak on optimism and die on euphoria. - Sir John Templeton

A public opinion poll is no substitute for thought. - Warren Buffett

Buy when most people including experts are overly pessimistic, and sell when they are actively optimistic.'- Sir John Templeton

In the short run, the market is a voting machine - reflecting a voter registration that requires only money, not intelligence or emotional stability - but in the

long run, the market is a weighing machine. - Benjamin Graham

When asked what he considered man's greatest discovery, Albert Einstein replied without hesitation: "Compound interest!"

I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years. -

Warren Buffett

To buy when others are despondently selling and sell when others are avidly buying requires the greatest fortitude and pays the greatest potential reward. -

Sir John Templeton

4

The Secret to Happiness “Happiness is when what you think, what you say, and what you do are in harmony.”

― Mahatma Gandhi

What is Happiness?

Happiness is the state of well-being characterized by emotions ranging from contentment to intense joy.

When I think of Happiness I am reminded of the movie ‘Chalo Dilli’. Lara Dutta portrays the role of a sophisticated rich woman from Mumbai and Vinay Pathak portrays the role of a boorish, go lucky, over confident middle class person from Delhi. One of the oft repeated lines by Vinay Pathak in any situation that they face together is ‘Konse Badi Baat Ho Gi, Ji’! Lara has all the money and life that she wants whereas Vinay has a bedridden wife and very little money. What stands out is the ability of these two characters to cope with situations that life throws at them every minute during their long journey to Delhi.

So what is the secret to Happiness? A pioneering research by Sonja Lyubomirsky, a research psychologist, professor and author of the book,‘ The How of Happiness’ reveals that the Secret to Happiness is contributed by three factors:

1. Genetics accounts for 50% of our Happiness

2. Life circumstances and situations accounts for 10% of our Happiness

3. Power to change accounts for 40%

The scientific evidence confirms what Gandhi had said long ago. That we can increase our happiness by what we think, what we say and what we do. Don’t you think it is amazing that we have the power to be happy? I mean 40% is in our control!! Life Circumstances or situations contribute just 10%. Yet, we lay so much emphasis on the 10%. Reminds me of the Asset Allocation Theory which says for better portfolio returns ‘timing’ contributes only 10%. Yet most investors try ‘timing’ the market! Will reserve another day to write on the ‘Asset Allocation’ principles!

Yes…I do agree that sometimes we do face life situations that do not make us happy. That could only be temporary. I strongly believe that with a positive attitude in life and focusing on what we can control will bring more joy and happiness in our lives on a sustainable basis.

5

Sonja Lyubormirsky explains further on How to achieve Happiness:

“If we observe genuinely happy people, we shall find that they do not just sit around being contented. They make things happen. They pursue new understandings, seek new achievements, and control their thoughts and feelings. In sum, our intentional, effortful activities have a powerful effect on how happy we are, over and above effects of our set points and the circumstances in which we find ourselves. If an unhappy person wants to experience interest, enthusiasm, contentment, peace, and joy, he or she can make it happen by learning the habits of a happy person.”

Research Credit: Money Quotient

6

Patience is the key

Date 17/01/2013

I was going through the long term track record of few schemes and found that Reliance growth

fund-growth option recently crossed the NAV of 500. It means somebody who had invested 1

lac in Oct 95 in the fund, today the value of his/her investments is in excess of 50 lacs. It means

50 times in approximately 17 years. Another fund Franklin India Blue chip Fund has given 48

times returns (After adjusting bonus) since Jan 1997 i.e. in 16 years. However I doubt any one

would have stayed invested for so long.

Let’s look at the other advantages one would had enjoyed (a) Liquidity (b) One can sell in piece

meal unlike real estate.

Can we think of any asset class which has given such kind of returns in the last 15 years. Yes

your favorite asset class has not delivered this kind of return (I am talking about real estate and

gold).

Having said that I am not trying to say that people should invest all their money in equities, it is

one’s asset allocation which plays the most important role. Also I am not suggesting that going

forward one should invest only in these two funds. Neither I am suggesting that these

performances will be repeated.

The only message I am trying to convey from here is ‘Give

time to your equity investments the way you give time to your

real estate investments’.

Because Patience is the key.

Disclaimer : Mutual fund investments are subject to market risks. Please read all scheme related

documents carefully.

7

Revolutionary Changes in Health Insurance

IRDA has issued “Health Insurance Regulation 2013” with a deadline of October 2013 to implement the

same. Once implemented these changes will be revolutionary and bring lot of relief and advantage to

the policy holder. Please read on the few imported points listed below

• All Insurance Companies to provide Health Insurance for an entry age of 65 years. This means

that no company can deny you Insurance cover till age of 65 years.

• No upper age limit for renewal of policy, that is lifelong renewal

• An Insurer cannot deny the renewal or increase premium based on the individual claim

experience

• A grace period of 30 days to be introduced to continue the policy after the due date without a

break

• Free Look period of at least 15days to be provided from the date of receipt of policy to review

and return the policy, if not acceptable

• The cumulative Bonus accrued may be reduced at the same rate at which it is accrued.

• Coverage provided against non allopathic treatment, with the condition that the treating

institution is recognized by the government

• No need to settle claim proportionately if you have multiple policies. Insured can choose the

company to make the claim

• Standard List of excluded expenses for all the companies

• Standard Pre authorization and claim form

• 46 commonly used terms standardized

• Details of the past claim cannot be called for by the same insurer, thereby reducing the paper

work in event of a claim

• Claims to be paid directly by the Insurance company and not by the TPA, reducing the

turnaround time in claim payment

• Claims cannot be rejected by the TPA

• Existing group policy from the employer can be ported into an Individual policy, provided there

is a window of 45 days

• Combination products to be offered, where term and health Insurance is available under a single

policy

The regulation has identified and overcome very important challenges that a consumer was facing. With

growing need, this stern step by IRDA has created a conducive environment for an individual to enjoy

maximum benefit from health Insurance.

8

Control the Controllable 28/08/2013

There are too many bad news floating around. You pick up the news paper it is full of bad

news, you go on FB, Twitter, people are only posting negative comments. Stock market is

negative,bond market negative, real estate unaffordable , inefficient government, high

inflation, scams etc. etc. Honestly no one knows how long it will last or how fast it will recover.

People who are talking negative may turn positive as things start improving and vice versa.

However as a layman what should I do? I think the answer lies with us. The following steps one

need to follow.

(1) People need to define the objectives i.e. decide on goals and then prioritize them.

(2) Then make provisions for contingencies. 6 months house hold expense should be kept

aside in uncertain times

(3) Revisit your investment portfolio and align it with the objectives

(4) Don’t listen to the ‘intellectual thoughts’ like market will go to 15k or it will touch 25k.

Remember the objective of your life is not to see 50k BSE level but to have a happy and

tension free life.

(5) Don’t invest just because market is cheap or expensive. Invest only when you have a

objective. Don’t board a train if you don’t know the destination. And if the destination is

at long distance, don’t panic as soon as you board the train.

(6) From chai wala to CEO, everyone is discussing Rupee movement. Life goes on. ‘Control

the controllable’

9

How to find out if your employer is depositing your EPF contribution

or not?

Let me share with you some steps you should follow, to find out if your company is depositing

your EPF contribution properly or not.

1. First thing is the do not rely on hearsay’s here and there. It might happen that you come to

know from someone that your company is not depositing your EPF money, but it might not

always be true. Delays happens at times .

2. Every month on 25th , your employer is suppose to send few documents to EPFO department

to intimate them on

• Form – 2 (for new member during the month)

• Form – 5 (detail of new joinees during the month)

• Form – 10 (detail of left employees during the month)

• Form – 12 – (Details of money deducted from employees salary)

3. The best thing is to first contact your employer and ask them for a copy of these forms for

last 2-3 months, do double check if they deposited the money or not.

4. The best way for a common man and most convenient option is to file a RTI against EPFO and

ask them all these questions . Mention your EPF account number, your employer Code and

simply ask if your employer has been depositing your contribution or not.

Conclusion

Mostly the big size employers might be depositing the Employee Provident Fund money

properly on time, but some of the companies which are small sized or whose owners and

management teams are unethical might be into these illegal activities of not depositing

employees hard earned money. Its always a good idea to spend some time to be assured, in-

case you feel your company is one of those who are not depositing EPF amount with EPFO

10

How you CHOOSE to mess your financial life and never realise !

Do you make a choice or take decisions in your financial life ? A lot of people had not

taken many important actions in their financial life, which they should have taken long

back!. You have to understand that you are making a choice by not taking those actions.

When you take some action or do not take an action, deep down you are actually making a

choice in your financial life, which we will see now.

Let me give you some examples

1. Buying Endowment & Moneyback Policies

Most of the people who take the decision of buying Endowment and Moneyback Life

Insurance policies , they say that they are buying it because they save Income Tax and

trust the company and want safe returns. Now that’s their decision, however they have to

be understand that deep down they are making some choices which are unspoken …

• They are choosing to get below inflation returns on their investments

• They are choosing to put money in something which is illiquid and might not help them

in emergencies

• They are choosing not to cover their family with a higher life cover

2. Buying a ULIP from Life Insurance company.

• They are choosing to pay high charges out of their premium

• They are choosing to save tax u/s 80 C (up to one Lakh) as if there is no other less cost,

better tax saving avenues.

• They are choosing to withdraw after 5 years of lock-in with negligible gain and wasting the

mortality charges ( for the insurance cover) they paid from the premium.

3. Not buying a Term Plan

“I don’t think I will die” or “It does not give back money at the end” – this is

the general reasoning behind not taking a Term Insurance plan by many people. Now,

11

again, it’s their decision based on their belief, but deep down they are making some

choices which are

• They are choosing a life of struggle for their family, in case they are no more in this world

• They are choosing to pass on all the debt and tension to their spouse and children in

future

• They are choosing that their children and family might not lead a great comfortable life

in future if they are not around.

4. Not buying Health Insurance

“I will take it next month” and “I drive carefully and I am healthy , so I don’t

need it” are the top most reasons given by those who avoid taking health insurance.

Again, they feel it’s a right decision and I am not commenting if it’s right or wrong, but

surely they are choosing few things in their life and for their family …

• They are choosing a situation where their entire wealth accumulated till date, might wipe

out in Health related issues, someday

• They are choosing to get into a situation where they might have to run around for money

to fund health related expenses

• They are choosing to constantly worry about big ticket health related expenses if any.

5. Not creating a WILL

It’s a decision taken by almost all of us. “We are still young”, “I will do it once

my net-worth is at least 1 crore” etc., are the common reasons behind not

making a WILL. However deep down you are making few choices and you have to

accept them …

• You are choosing a lot of frustration, chaos and running around for your legal heirs

• You are choosing, that your family will have to meet lawyers, go to courts and spend lots

of money and effort to get what they deserve

12

• You are choosing to create a confusing situation, where your legal heirs fight with each

other and try to justify who deserves what

6. Not hiring a Financial Planner (when you really need it)

“I can do it myself, I was a bright student all my life”, “They charge a lot for

what they do”, are some of the reasons given by investors for not hiring a Financial

Advisor for themselves. It’s their decision based on their beliefs, but deep down you are

making some choices …

• You are choosing to still do trial and error and play with your financial life

• You are choosing to not organize yourself and get into a dedicated structure which can

improve your financial life

• You are choosing to focus on what you will spend (fee to Advisor) rather than what you

will get out of the whole exercise.

• You are choosing to delay your actions and rely on yourself for taking actions and get

disciplined which most fails most of the times.

7. Over spending right now as if there is no tomorrow

“Life happens NOW”, “If I don’t spend, what’s the point of earning well”, “I

will earn more in future, let me enjoy today” – These are the top most things you

will hear people saying who over spend (more than they should). One can comment easily

if it’s right or wrong, but let’s not get into it, it’s their decision and there is nothing wrong

in it, just that these people need to understand the choices they are making

without realizing them

• They are choosing to have a struggling financial life in future in case tomorrow does not

turn out to be like what they imagined

• They are choosing to have a better today at the cost of tomorrow

• They are choosing to be working for more years in future, because they will not have

wealth when they are old.

13

• They are choosing to have a less comfortable life later in life, when responsibilities

increase and opportunities decrease

Conclusion

At the end of the day, you always choose something in your life out of the decision you

make. This is true for all the aspects of life, including your financial life. So understand

that you are fully responsible for what you get. Be responsive and make a financial plan

with the advice of Finance planner.

14

Because I care ☺☺☺☺

Either drink or drive

Keep your mobile fully charged

Don’t go to overcrowded places

Save your spouse’s no. as husband/wife/home instead of real names or nick

names

Don’t party/get friendly with unknown people. Today is not the best day to make

new friends.

Do not return missed calls received from numbers starting with

+92,#90 and #09. Your SIM will be cloned and can be used for terror

purposes. Report on Page 13, TOI 2/7/12.

15

How to protect yourself from investment scams

Source : www.moneycontrol.com

It looks like routine that at least once a month you read some news about investors being cheated. The

amount runs into crores of Rupees and the number of investors into thousands. It is difficult to

understand how people continue to get cheated time and again.

Let us look at the recent news item. This was a multi-level marketing scheme, where the instead of

household items to be purchased, the investors were buying gold from a jeweler. The person was also

promised a regular income if one is able to get new members. The return on investment was mouth-

watering.

However, like all other Ponzi schemes, this one also relied on the greed of the investors and

unfortunately, the investors obliged. Like any other scheme, this one also paid the investors some

money for a few months and then stopped. It is only then that the investors realized that they were

taken for a ride.

Considering the recurrence of such events, it is important that we look at the ways to stay away from

such schemes. Are there any common characteristics? Are there any shields available? Well, some of the

common traits are:

• Promise of huge returns in fact, the returns promised are often unbelievable

• Positioning of the scheme as exclusive or only for a few people

• Showing urgency that the opportunity may not last long

• The scheme may be operating outside the regulatory environment

Out of the above, it is the first where you should start to be cautious. Let us be clear that we are asking

you to be cautious, which means to check all the details. You do not have to outright reject any scheme

that shows above characteristics.

The next step is to see if there are some shields available. Well, the most powerful shield one has is the

right to ask. You are allowed to ask any number of questions and get satisfactory answers before you

sign your cheque. Ask questions to understand how such an operation can be sustained. When someone

is promising very high returns, the same may be possible for a short time or if someone has some

technological breakthrough. It is impossible to generate very high returns from a common investment

avenue like Gold for a sustained period of time. If someone is talking about investment in stock markets

or real estate to generate higher returns, rest assured each one comes with some risk equity has risk of

volatile prices, real estate has risk of locking away your money.

Next time if someone tells you that the opportunity may go away, think about the choices

you have: “What is better? To lose an opportunity or to lose your capital? Lost opportunity

may come back ...”

16

That Most Important Attribute

Harish Rao

When is a refrigerator not a refrigerator? When it is available in Chicago, when needed in New York.

With this example, Philip Kotler made us understand the importance of distribution and availability of

the product.

Similarly, if one were to use in the scope of Financial Products, we can paraphrase it thus :

When is an asset not an asset? When it does not give cash, when most needed.We are talking about

Liquidity. An important attribute that describes the ease with which an asset can be converted to cash,

with least amount of loss in value.

While talking about Liquidity, two things come to mind. Why is it such an important factor in analysing

investment choices? And more importantly, why is it – many a time – overlooked?

Answering the first part is easy. Access to our money or cash, especially when required, is one of the

prime considerations in investing. We need money in time to pay school fees, to fund an emergency in

the hospital, to purchase a consumer durable or to enjoy a holiday. Our assets and investments need to

do give us the money to lubricate our daily life.

It’s the second part that is a mystery. Why is it that investors ignore liquidity and make investment

choices that either lock in their money for the longest time or are difficult to liquidate without a loss in

intrinsic value. A ten year single premium policy may look safe and attractive right now. But have you

thought about liquidity? Is there an extra return to compensate for the lack of liquidity? Investing in real

estate may look appealing, especially if there are surplus funds to be deployed and a tax-break to be

availed. But what if money is required a few years down the line – can the asset be quickly sold without

loss in realisation? The reason : Investors are blinded by other factors – returns, safety or brand – that

they forget liquidity.

In my opinion, liquidity is one of the most important attributes in selecting an asset class or investment.

It ranks right at the top alongside Return and Risk.

Think. What was the use in buying a great plot of land, when it could not fund your father’s by-pass

surgery or having a beautiful diamond necklace, when that was not the ticket to your son’s US

education. You had to fall back on the liquid options, didn’t you. Speak to your investment advisor about

liquidity today. It’s mighty important.

Harish Rao is a Money Management Coach having his own Financial Planning Training unit, Simple

Equation. He is a Science Graduate and MBA. He is a keen quizzer, having featured in Siddharth Basu's

Mastermind in BBC.

17

Retirement Planning for Individuals

Children grow looking at their father as a hero. In the growing years and many often afterwards

also they try to follow the footsteps of father. Most of the investment decisions also show the

same trend, for example love for a particular asset class.

Whilst most of us are getting acquainted with the term financial planning, we still don’t put any

extra effort to know it further. While we have seen our parents making provisions for our

education or our sister’s marriage, we have never seen them making provisions for their

retirement. And that’s where we commit mistake, when it comes to making a financial plan for

ourselves.

I have come across many young ‘educated’ couples who will buy child plans and marriage plans

of insurance for the kid, the agent will start the premium on the kid’s birthday to add emotional

element to it and when you talk about their retirement plan it is very low in the list of priorities.

I know many of the financial advisors who don’t have a retirement plan.

Few reasons why Retirement Planning is of utmost importance:

(1) High burn out in jobs. Because of the high stress level it’s very difficult to continue

working till 58

(2) No pension

(3) Maintaining same life style

(4) Higher medical expenses due to increasing no. of private players

(5) Higher life expectancy

(6) No dependency on the kid

(7) Rate of inflation

When should one start planning for retirement?

As soon as the adequate insurance cover is taken by way of term plan, health insurance etc.

One should start investing towards retirement. To begin with it can be as small as 2000 p.m.

and increasing it gradually.

There will be ups and downs during the investment period and should be taken as ups and downs of

life instead of panicking. Consider that you are planting a tree which will give you shade during your

retirement. It will go through all kinds of weathers to become a tree.

18

5 Reasons you are Earning More Money and

You're Still Miserable

Whether you're a millionaire or a middle-class father of two, we all make the same mistakes

when it comes to money – we think the more we earn, the happier we'll be.

If you really want to buy yourself a more fulfilling life, it's not how much money you earn that

matters, but figuring out the right way to spend it.

That's the idea explored in a fascinating new book, "Happy Money: The Science of Smarter

Spending," written by a pair of renown behavioral scientists, Dr. Elizabeth Dunn and Dr.

Michael Norton.

"When it comes to increasing the amount of money they have, most people recognize that

relying on their own intuition is insufficient, spawning an entire industry of financial advisors,"

they write. "But when it comes to spending that money, people are often content to rely on

their hunches about what will make them happy."

That all ends with this book. We've combed through and highlighted five ways to change the

way you think about money that will make you happier in the long-run.

1. You're buying too many things and not enough experiences.

A world where anything and everything can be yours with a credit card and access to the

Internet, it's easy to get swept up by material things.

But if you recognized the fact that you could get more satisfaction out of a $50 dinner with

friends than that big screen TV or new iPhone, it might change the way you shop.

"Research shows experiences provide more happiness than material goods in part because

experiences are more likely to make us feel connected to others," Dunn and Norton write.

"Understanding why experiences provide more happiness than material goods can also help us

to choose the most satisfying kinds of experiences."

To help, here are four questions they suggest asking before you spend money on an experience

that may not be as happiness-inducing as others:

1. Does this bring me together with other people?

2. Will this make a memorable story that I will tell for years to come?

19

3. Is this experience in line with who I am or who I'd like to become?

4. Is this a unique opportunity and something I can't compare to things I've done before?

2. You're more focused on getting more money than buying more time.

Sometimes, we get too caught up in either working hard to save a buck or working hard to earn

a buck to realize what really matters – our time.

"Research suggests that people with more money do not spend their time in more enjoyable

ways on a day-to-day basis," the authors write."Wealthier individuals tend to spend more of

their time on activities associated with relatively high levels of tension and stress, such as

shopping, working, and commuting."

On the flip side, penny-pinchers sometimes take saving too far. When you trade your time for

some kind of monetary payoff (saving $20 on a flight by staying up all night on Kayak.com or

using your vacation to earn over-time pay), you could be sacrificing your overall happiness in

the process.

Now, if you get a high from saving five cents on a gallon of gas by driving 10 miles out of your

way, then fine. But most people would be happier spending a little extra money to get home 20

minutes earlier for dinner.

3. You think a McMansion will make you happy.

What could possibly be more satisfying than ditching that old starter home you and your

spouse moved into during your broke newlywed years?

Two studies cited in "Happy Money" prove otherwise.

When researchers followed groups of German homeowners five years after they moved into

new homes, they all wound up saying they were happier with their newer house. But there was

one problem: They weren't any happier with their lives. The same was true in a study of Ohio

homeowners in which it turned out they weren't any happier with their lives than renters.

"Even in the heart of middle America, housing seems to play a surprisingly small role in the

successful pursuit of happiness," Dunn and Norton write. "If the largest material purchase most

of us will ever make provides no detectable benefit for our overall happiness, then it may be

time to rethink our fundamental assumptions about how we use money."

20

4. You're letting yourself have too much of a good thing.

When you've got unlimited financial resources, it may seem stupid to deny yourself simple

pleasures that you've come to enjoy, like new jewelry or an expensive bottle of wine with

dinner every evening.

But when you reach that point of material over-saturation, you could be killing the potential to

make yourself any happier.

"This is the sad reality of the human experience: The more we're exposed to something, the

more its impact diminishes," Dunn and Norton write. "Knowing we have access to wonderful

things undermines our happiness by reducing our tendency to appreciate life's small joys."

You think if the McRib were always on the menu, people would line up to get a taste every day?

Probably not. Instead, try to make things you really enjoy a special treat you only allow yourself

once in a while. It will pack a much happier punch.

5. You're investing too much in yourself and not enough in other people.

Like love, it stands to reason that the happier you are with yourself, the more likely it is that

you'll bring happiness to others. But Dunn and Norton suggest flipping that idea on its head.

Make others happier first and you'll bring yourself happiness in the process. It sound obvious,

but you'd be surprised how many of us forget it.

"In [a study] of more than 600 Americans, personal spending accounted for the lion's share of

most people's budgets," they write. "But the amount of money individuals devoted to

themselves was unrelated to their overall happiness. What did predict happiness? The amount

of money they gave away. The more they invested in others, the happier they were."

That being said, you may wonder why you don't really feel all that much happier after donating

a bag of clothing to Goodwill or cutting a check to the Red Cross. The real happiness comes

from seeing your money at work.

We're big fans of charitable organizations that allow donors to see where their money goes in

real time. Kiva.org is a micro-lending site that employs a host of workers whose sole job is to

write reports on the progress of their borrowers so donors are always in the loop. Dunn and

Norton suggest DonorsChoose.org, which also lets donors see their gifts making a difference.

21

Why do we need financial planning?

◦ Prepare for financial needs – house, education, child’s marriage, medical emergencies

◦ Get rid of debt

◦ Proper retirement planning

◦ Creation of wealth

FINANCIAL PLANNING = FUTURE PLANNING

______________________________________________________________________

About Vinayak Sapre

� A graduate in Management with over 10 years of work experience in the financial industry.

� Worked with some of the world’s leading Finance companies like Franklin Templeton Investments and AIG Investments

� In depth knowledge and understanding of the various investment products

Visit us at www.vvsventures.com

Disclaimer: I have not written all the articles. Some of them are forwards received from different

sources.

Related Documents