CHAPTER 1 INTRODUCTION 1.1 PROFILE OF GENERAL I NSURANCE INDUSTRY History of Indian Insurance Market Insurance in India goes back to the time of the British. The first life insurance company to operate in India the Oriental Life Insurance Company was established in 1818in Calcutta. It was, however, a British company. The first Indian insurance company, the Bombay Mutual Life Assurance Society started its operations in1871. In 1956 the Indian life insurance industry was made up of 154 domestic life insurers, 16 foreign life insurers and 75 provident funds, and was still governed by the Insuran ce Act of 1938.In 1956 all life insurance companies were nationali zed, the story of non-lif e insurance in India is no diff erent. Though Lloyd. Insurance pioneered general insurance way back in 1688, the first non-life insurance company to set up shop in India was the Triton Insurance Company of Calcutta. In1907, the first Indian general insurer, the Indian Mercantile Insurance Company started its operations. The New India Assurance Company Ltd. was incorporated in1919. In 1972, the non-life insurance business in the country was nationalized and the GIC (General Insurance Corporation of India) was formed as a holding company with four subsidiaries: The National Insurance, Oriental Insurance, Uni ted India Insurance and the New India Assurance Company Ltd.Since then, insurance in India had a protect ive wall built around it, to keep it local players Market. The above companies control led the insuran ce industry for 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 1/56

CHAPTER 1

INTRODUCTION

1.1 PROFILE OF GENERAL INSURANCE INDUSTRY

History of Indian Insurance Market

Insurance in India goes back to the time of the British. The first life

insurance company to operate in India the Oriental Life Insurance Company was

established in 1818in Calcutta. It was, however, a British company. The first

Indian insurance company, the Bombay Mutual Life Assurance Society started its

operations in1871. In 1956 the Indian life insurance industry was made up of 154

domestic life insurers, 16 foreign life insurers and 75 provident funds, and was

still governed by the Insurance Act of 1938.In 1956 all life insurance companies

were nationalized, the story of non-life insurance in India is no different. Though

Lloyd. Insurance pioneered general insurance way back in 1688, the first non-life

insurance company to set up shop in India was the Triton Insurance Company of

Calcutta. In1907, the first Indian general insurer, the Indian Mercantile Insurance

Company started its operations. The New India Assurance Company Ltd. was

incorporated in1919. In 1972, the non-life insurance business in the country was

nationalized and the GIC (General Insurance Corporation of India) was formedas a holding company with four subsidiaries: The National Insurance, Oriental

Insurance, United India Insurance and the New India Assurance Company

Ltd.Since then, insurance in India had a protective wall built around it, to keep it

local players Market. The above companies controlled the insurance industry for

1

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 2/56

nearly 30 years or so. Current Insurance Market Structure General Insurance

business in India was under complete control of four Governments insurance

companies for nearly three decade. After much deliberation finally the market

was opened for competition from December2000 and also Government has de-

linked four Public sector companies from holding company GIC to operate as

independent company. In addition to four Public Sectors insurance companies

the Insurance Regulatory and Development Authority (.IRDA.)Has issued

licenses to the eight Private

1.2 COMPANY PROFILE

ICICI Lombard General Insurance Company

ICICI Lombard General Insurance Company Limited is a 74:26 joint

venture between ICICI Bank Limited and the US-based $ 26 billion Fairfax

Financial Holdings Limited. ICICI Bank is India's second largest bank; while

Fairfax Financial Holdings is a diversified financial corporate engaged in general

insurance, reinsurance, insurance claims management and investment

management. Lombard Canada Ltd., a group company of Fairfax Financial

Holdings Limited, is one of Canada's oldest property and casualty insurers.

ICICI Lombard General Insurance Company received regulatory approvals to

commence general insurance business in August 2001.

HIGHLIGHTS OF ICICI Lombard

India 's number one private general insurance company

First general insurance company in India to be ISO 9001:2000 certified

Highest brand recall

Simple and fast documentation

2

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 3/56

Lightning fast claims settlement

Instant online policy issuance

Comprehensive product line

Highest security level offered through 128-bit encryption in case of online

data exchange.

First company to provide digitally signed documents through an online

interface.

Achieved financial breakeven in first full year of operations

Achieved underwriting breakeven in second year of operations

About Fairfax

Fairfax Financial Holding Limited is a financial services holding

company whose corporate objective is to achieve a high rate of return on

invested capital and build long-term shareholder value. It provides services in the

area of financial services, general insurance, reinsurance, insurance claims

management and investment management. Fairfax Group is amongst the largest

shareholder of ICICI Bank with about 4.5% shareholding

ABOUT ICICI Bank

• Second largest bank in India with asset size of over US $ 24 billion

• A network of 540 branches /offices and over 1,700 ATMs

• Presence across all financial products

• Only FI in India to pierce sovereign rating• Listed at the NYSE, around 72% of the company’s equity is held by

foreign investors

• Technology-enabled products and processes

3

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 4/56

GROUP COMPANIES

Domestic subsidiaries

o ICICI Securities Limited

o ICICI Venture Funds Management Company Limited

o ICICI Prudential Life Insurance Company Limited

o ICICI Lombard General Insurance Company Limited

o ICICI Home Finance Company Limited

o ICICI Investment Management Company Limited

o ICICI Trusteeship Services Limited

o ICICI Brokerage Services Limited *

o ICICI Distribution Finance Private Limited

International subsidiaries

o ICICI Bank UK Limited

o ICICI Bank Canada

o ICICI Securities Holdings Inc

o ICICI Securities Inc

o ICICI International Limited

Home Insurance

Insure your home and its contents against natural calamities like fire,

earthquake, flood, gas cylinder explosion, fire due to electric short circuit as well

as man-made disasters like burglary

4

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 5/56

CHAPTER 2

NEED, OBJECTIVES, SCOPE AND

LIMITATIONS OF THE STUDY

2.1 NEED FOR THE STUDY

ICICI Lombard’s home insurance division was started in October 2004.

Hence the company wanted to know to what extent the people were aware of

ICICI Lombard General insurance company and their perception towards home

insurance products. Hence this research was undertaken. The company wanted

to assess whether the present level of marketing efforts is sufficient or not and

the medium of communication which was most effective in creating awareness.

Hence it’s need for this research.

5

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 6/56

2.2 OBJECTIVES

2.2.1 Primary Objective

To assess the level of awareness of the brand “ICICI Lombard”

general insurance company in Bangalore.

2.2.2 Secondary Objectives

To assess the level of awareness about different types of insurance and

the companies operating in the general insurance domain.

To assess the relative importance of home insurance among different

insurance products.

To assess the extent of the “need for home insurance” as perceived by the

public and their reasons.

To estimate the degree of brand recall achieved through logo, slogan and

Company name.

To assess the role of different media in generating awareness about the

brand “ICICI Lombard”.

6

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 7/56

2.3 SCOPE OF THE STUDY

This study undertaken for ICICI Lombard aims to study and

understand the awareness level of the company and the market potential for

home insurance among the individuals residing in south east Bangalore,

This has been done by preparing the questionnaire which contains

questions put forth to the prospective individual’s, which would help in analyzing

the profile and individual’s perception towards home insurance, factors

influencing the individuals in going for home insurance, and awareness of variousschemes and insurance companies.

This study would help in determining the future market potential for

home insurance. The study would also help ICICI Lombard to direct their

marketing efforts by identifying customer preference and also the role of different

media in creating awareness.

7

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 8/56

2.4 LIMITATION OF THE STUDY

The area of study is limited to south east region of Bangalore only,

hence the results may not be true for other geographical areas. Validity &

Reliability of the data obtained depends on the correctness of the responses by

the respondents, The time at the disposal of the researcher was limited and the

size of the sample comparing to the population was very less and hence it cannot

be said to represent the whole population.

8

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 9/56

CHAPTER 3

RESEARCH METHODOLOGY

A proper research Methodology is imperative to derive meaningful

inferences and conclusions from the study. The Methodology followed for this

study is as follows.

3.1 RESEARCH DESIGN

In this market survey, the design used is “descriptive” in nature.

The information is collected from the individuals and analyzed with the

help of different statistical tools for describing the relationship between various

types of variables pertaining to market potential for home Insurance. Moreover

Cross table Analysis has been done for multivariate data and information has

been obtained to meet the objectives of the study.

9

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 10/56

3.2 DATA

3.2.1 Nature of Data

Both primary and secondary data are used in this study in order to

meet the requirements of the objectives. Under the study primary data was

collected by using a Questionnaire.

3.2.2 Source of Data

The Primary data was collected from the individuals residing in southeast Bangalore, with the help of the questionnaire, which was prepared after

getting inputs from the experts and executives in ICICI Lombard. Secondary data

are sourced from General Insurance Companies, Magazines, Books, Pamphlets,

Websites etc.

3.3 METHOD OF DATA COLLECTION

Structured Questionnaire method is used as an instrument for

collecting information from the individuals. A Pilot study was conducted based on

which a few changes were made in the Questionnaire.

3.4 SAMPLING

Since the population of consumers of general Insurance is large in

number, researcher was unable to collect information from all individuals due to

limitation of time. So part of the population is taken for analyzing and generating

the findings.

10

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 11/56

3.4.1 Sampling Unit

The respondents of the study are individuals residing in Jaya nagar,

Bansankari, Indira nagar and Koramangala, which are parts of Bangalore south

east.

3.4.2 Sample Size

The sample size was computed using the confidence level of 90%

and error level of ± 5%. The formula used for calculating the sample size is

N = z2 * p. q = 240(Calculations shown in appendix - V)

e2

3.4.3 Sampling Method

Cluster sampling method is used. The area to be surveyed was

divided into blocks. A number of blocks was chosen at random. Every household

in the chosen block was surveyed.

3.5 TOOLS USED

The data has been analyzed mainly by using the following methods,

namely.Cross Tabulation and Percentage method supplemented by appropriatecharts. Preference of the Respondents for different insurance products has been

analysed using Ranking method.

11

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 12/56

3.5.1 Percentage Analysis

This is a univariate analysis where the percentage of a particular

factor with different categories is calculated, in order to help one get fair an idea

regarding the sample and there by that of the population.

3.5.2 Cross Tabulation

While percentage analysis is applicable to single variable, cross

tabulations help in identifying relationship between different variables.

3.5.3 Ranking method

This type of analysis is particularly useful when the purpose of the

question is to identify the preferences of the sample among different choices.

The respondents indicated the importance they assign to different

types of policies. The ranking was in the order of “1” for most important and “5”

for the least important. While doing the analysis the first rank was given a

weightage of 5 and the least rank was given the weightage of 1.

The rank assigned by all the respondents was cumulated using the

weightage. Accordingly the type of policy with the larger cumulative weightage

was ranked number 1 and so on.

12

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 13/56

3.5.3 Questionnaire

The questionnaire includes both open ended and closed ended

questions with multiple choices, Open-ended questions enable wide range of

responses. This enables the respondent to express his views in his own

words.However this is difficult to tabulate and analyse.

Close-ended questions offer a limited choice of response .Respondents

find these easier to complete.Close-ended questions can also be tabulated and

analysed more easily.

13

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 14/56

CHAPTER 4

ANALYSIS AND INTERPRETATION

4.1 ANALYSIS OF DATA

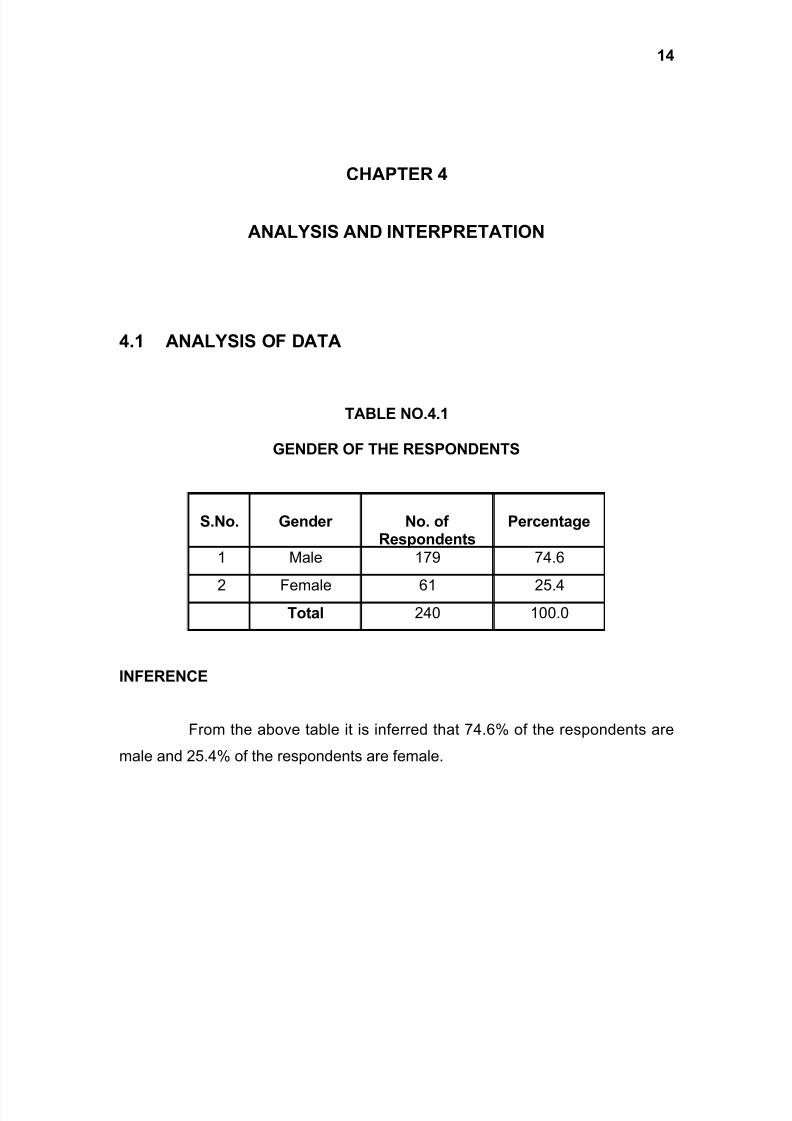

TABLE NO.4.1

GENDER OF THE RESPONDENTS

S.No. Gender No. of Respondents

Percentage

1 Male 179 74.6

2 Female 61 25.4Total 240 100.0

INFERENCE

From the above table it is inferred that 74.6% of the respondents are

male and 25.4% of the respondents are female.

14

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 15/56

15

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 16/56

TABLE NO. 4.2

AGE OF THE RESPONDENTS

S.No. Age No. of Respondents

Percentage

1 20-30 81 33.8

2 31-40 69 28.8

3 41-50 43 17.9

4 51-60 14 5.8

5 61-70 22 9.2

6 71-80 6 2.5

7 >80 5 2.1

Total 240 100.0

Average age of respondents = 39.375

INFERENCE

From the above table it is inferred that, 33.8% of the respondents are

in the age group of 20-30 years followed by 28.8% of the respondents who are in

the age group of 31-40 years followed by 17.9% of the respondents who are in

the age group of 41-50 years followed by 5.8% of the respondents who are in the

age group of 51-60 years followed by 9.2% of the respondents who are in the

age group of 61-70 years followed by 2.5% of the respondents who are in the

age group of 71-80 years and 2.1% of the respondents who are in the age group

of above 80 years.

16

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 17/56

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 18/56

TABLE NO. 4.3

OCCUPATION OF THE RESPONDENTS

S.No. OccupationNo. of

RespondentsPercentage

1 Salaried 121 50.4

2 Self employedprofessional

26 10.8

3 Self employedbusiness

36 15.0

4 Retired 35 14.6

5 Housewife 18 7.5

6 Others 4 1.7

Total 240 100.0

INFERENCE

From the above table it is inferred that 50.4% of the respondents are

salaried employees, 10.8% of the respondents are self-employed professionals,

15.0% of the respondents are self-employed in business, 14.6% of the

respondents are retired, 7.5% of the respondents are housewives and 1.7% of

the respondents belong to “others” category and are Students or unemployed

persons.

18

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 19/56

19

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 20/56

TABLE NO. 4.4

ANNUAL INCOME LEVEL OF THE RESPONDENTS

S.No. Annual incomeNo. of

RespondentsPercentage

1 <2Lakhs 138 57.5

2 2-4Lakhs 72 29.9

3 4-6Lakhs 19 7.9

4 6-8Lakhs 4 1.7

5 >8Lakhs 7 2.9

Total 240 100.0

INFERENCE

From the above table it is inferred that, 57.5% of the respondents

belong to the annual income group of less than Rs.2 lakhs, 29.9% of the

respondents belong to the annual income group of Rs.2lakhs – Rs.4lakhs, 7.9%

of the respondents belong to the annual income group of Rs.4lakhs – Rs6lakhs,1.7% of the respondents belong to the annual income group of Rs.6lakhs –

Rs.8lakhs and 2.9% of the respondents belong to above Rs.8lakhs income

group.

20

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 21/56

21

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 22/56

TABLE NO. 4.5

UNAIDED RECALL LEVEL OF ICICI LOMBARD (GIC)

S.No. CompanyNo. of

RespondentsPercentage

1 Not able to recall 168 70.0

2 Recall ICICILombard

72 30.0

Total 240 100.0

INFERENCE

From the above table it is inferred that, 30% of the respondents were

able to recall the company name “ICICI Lombard” with out any assistance and

70% of the respondents were not able to recall the company name with out any

assistance.

22

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 23/56

23

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 24/56

TABLE NO. 4.6

UNAIDED RECALL OF THE INSURANCE COMPANIES

S.No. Companies

No. of

Respondents

Percentage

1 Bajaj Allianz 19 7.9

2 Cholamandalam 3 1.3

3 HDFC-Chubb 5 2.1

4 Iffco-Tokyo 0 0

5 ICICI Lombard 72 30

6 Oriental Insurance 67 27.9

7 Royal Sundaram 9 3.8

8 Reliance 7 2.9

9 Tata AIG 40 16.7

10 United India Assurance 29 12.1

11 Others 70 29.2

12 Not Aware of any company 33 13.75

INFERENCE

From the above table it is inferred that with out any assistance, (7.9%)

of the respondents were able to recall the company “Bajaj Allianz”, (1.3%) of the

respondents were able to recall the company “Cholamandalam, (2.1%) of the

respondents were able to recall the company “HDFC-Chubb“,(30%) of the

respondents were able to recall the company name “ICICI Lombard”,

(27.9%) of the respondents were able to recall the company “Oriental Insurance“,

(3.8%) of the respondents were able to recall the company “Royal Sundaram“,

(2.9%) of the respondents were able to recall the company “Reliance“, (16.7%) of

the respondents were able to recall the company “Tata AIG“, (12.1%) of the

respondents were able to recall the company “United India Assurance”, (29.2%)

of the respondents were able to recall other companies which are not listed

above, and (13.75%) of the respondents were not able to recall any company

name with out any assistance.

24

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 25/56

TABLE NO. 4.7

COMPANY RECOGNITION THROUGH LOGO AND INFLUENCE OF

ADVERTISING MEDIA

MediaCompany recognition

Cannotidentify

IciciIcici

LombardTotal

-101

(42.08%)

101(42.08%)

Print(PR)39

(16.25%)10

(4.17%)49

(20.42%)

Television(TV)49

(20.42%)

10

(4.17%)

59

(24.58%)Hoardings(HD)

9(3.75%)

10(4.17%)

19(7.92%)

Salespeople(SP)

14(5.83%)

19(7.92%)

33(13.75%)

PR,TV,HD6

(2.5%)2

(0.83%)8

(3.33%)

PR,TV9

(3.75%)3

(1.25%)12

(5.0%)TV,SP 4

(1.67%)0

4(1.67%)

INFERENCE

From the above table it is inferred that 42.08% of the respondents

were not able to recall the company name with the assistance of “LOGO”.

57.92% of the respondents were able to recall the company name with

assistance of logo. Among those who were able to recall, 16.25%were able to

recall “ICICI” and 4.17%were able to recall “ICICI Lombard” and they were aware

of the logo through Print media, 20.42%were able to recall “ICICI” and

4.17%were able to recall “ICICI Lombard” and they were aware of the logo

through Television, 3.75%were able to recall “ICICI” and 4.17%of were able to

recall “ICICI Lombard” and they were aware of the logo through advertisement

25

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 26/56

Hoardings, 5.83%were able to recall “ICICI” and 7.92%were able to recall “ICICI

Lombard” and they were aware of the logo through Sales people, 2.5%were able

to recall “ICICI” and 0.83%were able to recall “ICICI Lombard” and they were

aware of the logo through Print media, Television and advertisement hoardings,

3.75%were able to recall “ICICI” and 1.25%were able to recall “ICICI Lombard”

and they were aware of the logo through Print media and Television, 1.67%

were able to recall “ICICI” and they were aware of the logo through Television

and Sales people.

26

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 27/56

27

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 28/56

TABLE NO. 4.8

COMPANY RECOGNITION THROUGH SLOGAN AND INFLUENCE OF

ADVERTISING MEDIA

MediaCompany recognition

Cannotidentify

IciciIcici

LombardTotal /

percentage

-174

(72.5)174

(72.5)

Print (PR)8

(3.33)6

(2.5)14

(5.83)

TV5

(2.08)7

(2.92)12(5)

Hoardings(HD) 07

(2.92)

7

(2.92)Sales people

13(5.42)

24(10.0)

37(15.42)

PR,TV,HD 02

(0.83)2

(0.83)

INFERENCE

From the above table it is inferred that 72.5% of the respondents were

not able to recall the company name with the assistance of “SLOGAN”. 27.5% of

the respondents were able to recall the company name with assistance of

slogan. Among those who were able to recall,3.33% were able to recall “ICICI”

and they were aware of the slogan through Print media, 2.5% were able to recall

“ICICI Lombard” and they were aware of the slogan through Print media, 2.08%

were able to recall “ICICI” and they were aware of the slogan through Television,

2.92% were able to recall “ICICI Lombard” and they were aware of the slogan

through Television, 2.92% of were able to recall “ICICI Lombard” and they were

aware of the slogan through advertisement Hoardings, 5.42% were able to recall

“ICICI” and they were aware of the slogan through Sales people, 10.0% were

able to recall “ICICI Lombard” and they were aware of the slogan through Sales

people, 0.83% were able to recall “ICICI” and they were aware of the slogan

through Print media, Television and advertisement hoardings.

28

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 29/56

TABLE NO.4.9

COMPANY RECOGNITION AND ASSOSIATION WITH TYPE OF INSURANCE-THROUGH NAME, LOGO AND SLOGAN

Kind of insuranceNo. of

RespondentsWho Said Yes

No. of RespondentsWho Said No

Total /percentage

Cannot identify66

(27.5)66

(27.5)

Automobile Insurance10

(4.17)

10(4.17)

Health Insurance4

(1.67)

4(1.67)

Travel Insurance8

(3.33)

8

(3.33)

Home Insurance36

(15.0)

36(15.0)

General insurance116

(48.33)

116(48.33)

Total /Percentage

174(72.5)

66(27.5)

240(100)

INFERENCE

From the above table it is inferred that, (72.5)% of respondents were

able to recognize the company with the assistance of the company name, slogan

and logo, (4.17%) of the respondents said the company is associated with

Automobile Insurance, (1.67%) of the respondents said the company is

associated with Health Insurance, (3.33%) of the respondents said the company

is associated with Travel Insurance, (15.0%) of the respondents said the

company is associated with Home Insurance, (48.33%) of the respondents said

the company is associated with General insurance, (27.5%) of the total

respondent were not aware the company.

29

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 30/56

30

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 31/56

TABLE NO.4.10

AWARENESS LEVEL OF THE TYPES OF INSURANCE

S.No. TypesNo. of

RespondentsPercentage

1 Not aware 15 6.3

2 Automobile(A) 142 59.17

3 Health(H) 139 57.91

4 Travel(T) 90 37.5

5 Home(Ho) 134 55.83

6 A, H, T, Ho 65 27.1

7 A, H, Ho 13 5.4

8 A,H,T 8 3.3

9 H,T, Ho 6 2.5

10 A,H 22 9.2

11 A,T 2 .8

12 A, Ho 6 2.5

13 H, Ho 2 .8

14 T, Ho 1 .4

INFERENCE

From the above table it is inferred that 27.1% of the respondents are

aware of all types of general insurance namely automobile, health, travel and

home insurance. On the other hand 6.3% of the respondents are not aware of

any of the general insurance products. The remaining 66.6% of the sample have

varying degrees of awareness about the various general insurance products as

detailed below.

31

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 32/56

55.83% of the respondents are aware of home insurance, 59.17% of

the respondents are aware of automobile insurance,57.91% of the respondents

are aware of health insurance, 37.5% of the respondents are aware of Travel

insurance,9.2% of the respondents are aware of automobile and health

insurance,5.4% of the respondents are aware of automobile, health and home

insurance,3.3% of the respondents are aware of automobile, health and travel

insurance, 2.5% of the respondents are aware of automobile and home

insurance, 2.5% of the respondents are aware of health, travel and home

insurance, 0.8% of the respondents are aware of automobile and travel

insurance and 0.8% of the respondents are aware of health and home insurance.

32

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 33/56

33

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 34/56

TABLE NO. 4.11

RELATIVE IMPORTANCE OF TYPES OF INSURANCE POLICY

S.No. Policy typesWeightage

scoreRank

1 Automobile 632 III

2 Health 761 II

3 Travel 344 V

4 Home 617 IV

5 Life 1040 I

INFERENCE

From the above table the relative importance assigned by the

respondents to different types of insurance can be clearly inferred.

‘Life insurance’ occupies Ist rank with the highest score of 1040 points.

‘Health insurance’ occupies IInd rank with the score of 761 points.

‘Automobile insurance’ occupies IIIrd rank with the score of 632 points.

‘Home insurance’ occupies IVth rank with the score of 617 points.

‘Travel insurance’ occupied Vth rank with the low score of 344 points.

34

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 35/56

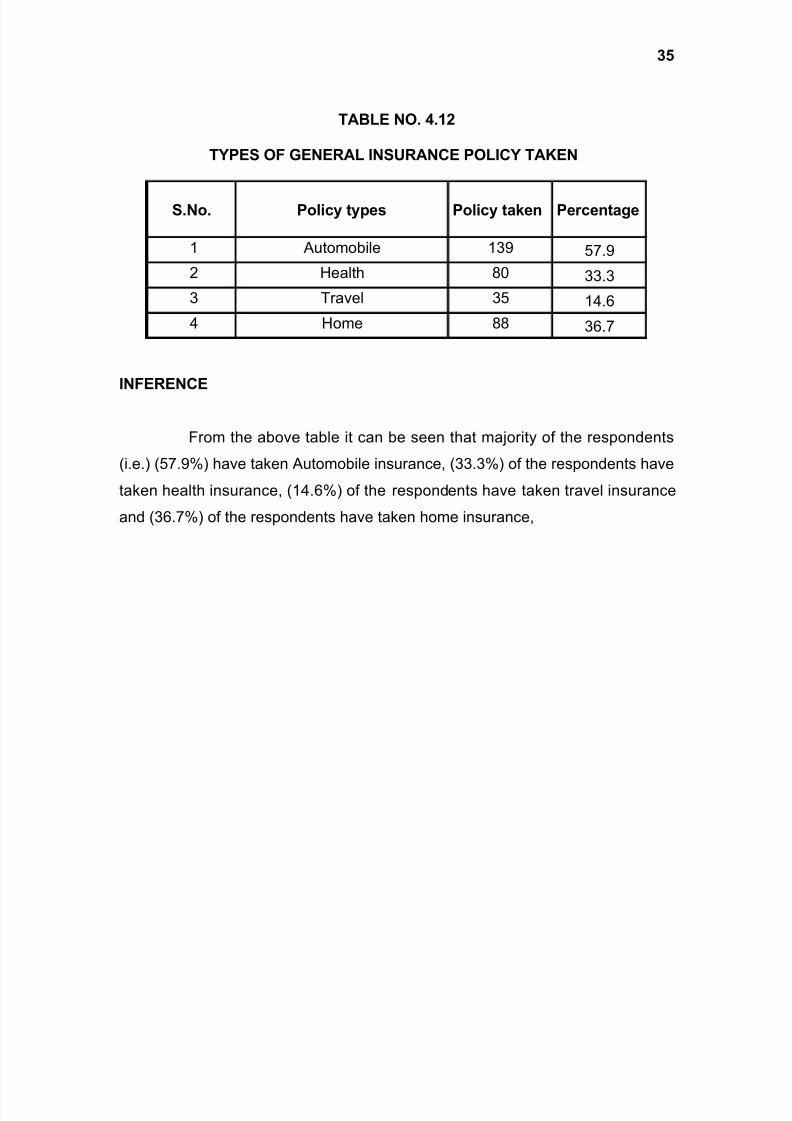

TABLE NO. 4.12

TYPES OF GENERAL INSURANCE POLICY TAKEN

S.No. Policy types Policy taken Percentage

1 Automobile 139 57.9

2 Health 80 33.3

3 Travel 35 14.6

4 Home 88 36.7

INFERENCE

From the above table it can be seen that majority of the respondents

(i.e.) (57.9%) have taken Automobile insurance, (33.3%) of the respondents have

taken health insurance, (14.6%) of the respondents have taken travel insurance

and (36.7%) of the respondents have taken home insurance,

35

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 36/56

36

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 37/56

TABLE NO. 4.13

TYPES OF POLICY TAKEN BY CLIENTS OF ICICI LOMBARD

S.No. Policy types No. of Respondents Percentage

1. AUTOMOBILE 17 22.372. HEALTH 6 7.893. TRAVEL 5 6.584. HOME 55 72.375 AUTO,HOME 7 9.22

INFERENCE

From the above table it is clearly understood that,(22.37%) of the

respondents have taken automobile insurance,( 7.89%) of the respondents have

taken health insurance, (6.58%) of the respondents have taken travel insurance,

(72.37%) of the respondents have taken home insurance,(9.22%) of the

respondents have taken automobile and home insurance,

37

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 38/56

38

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 39/56

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 40/56

40

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 41/56

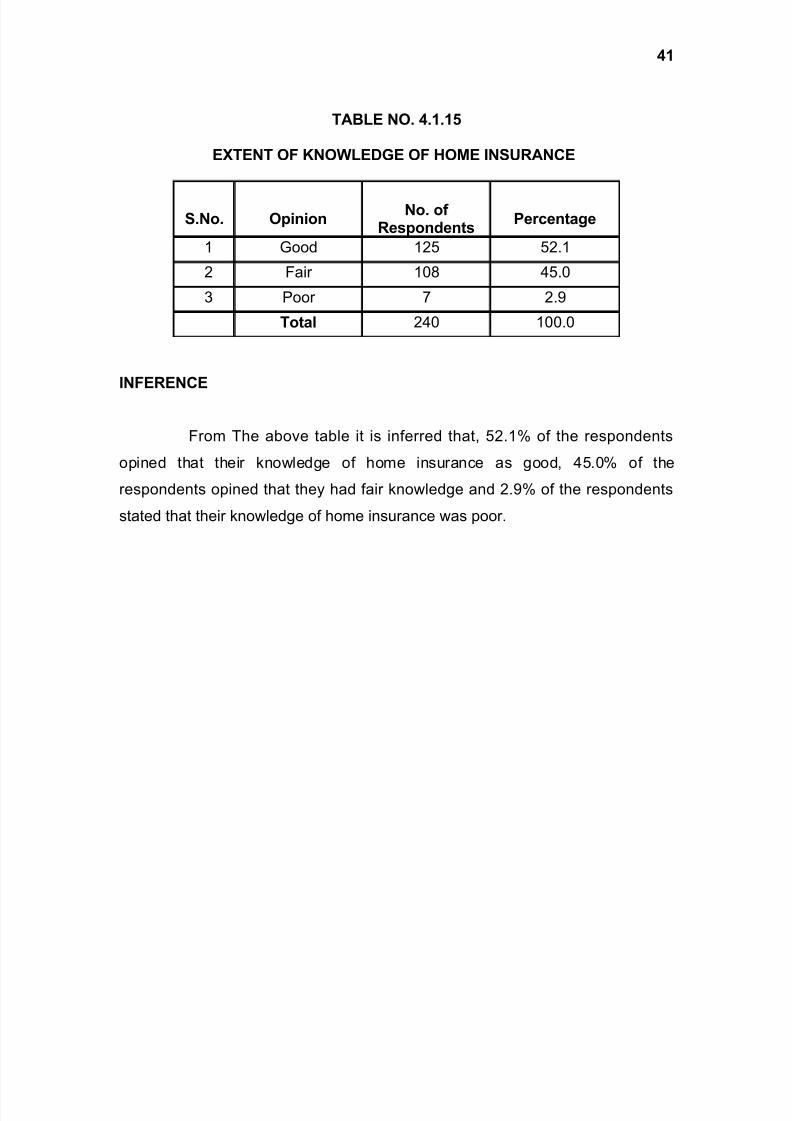

TABLE NO. 4.1.15

EXTENT OF KNOWLEDGE OF HOME INSURANCE

S.No. OpinionNo. of

RespondentsPercentage

1 Good 125 52.1

2 Fair 108 45.0

3 Poor 7 2.9

Total 240 100.0

INFERENCE

From The above table it is inferred that, 52.1% of the respondents

opined that their knowledge of home insurance as good, 45.0% of the

respondents opined that they had fair knowledge and 2.9% of the respondents

stated that their knowledge of home insurance was poor.

41

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 42/56

TABLE NO. 4.16

OPINION ABOUT NEED FOR HOME INSURANCE

S.No. Opinion No. of Respondents Percentage

1 Necessary 200 83.3

2 Not necessary 21 8.8

3 No idea 19 7.9

Total 240 100.0

INFERENCE

From The above table it is inferred that, (83.3%) of the respondents

opined that home insurance is Necessary, (8.8%) of the respondents opined that

home insurance is Not Necessary, (7.9%) of the respondents had no clear

opinion about the need for home insurance.

42

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 43/56

43

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 44/56

TABLE NO. 4.17

NEED FOR HOME INSURANCE- (REASONS)

S.No. Reasons

No. of

Respondents Percentage

1 Burglary(BUR) 102 42.5

2 Natural disaster(ND) 66 27.5

3 Peace of mind(PCE) 51 21.25

4 Cost is less(<CST) 45 18.75

5 BUR,ND,PCE,<CST 4 1.7

6 BUR,ND,PCE 5 2.1

7 BUR,ND,<CST 3 1.2

8 BUR,PCE,<CST 2 0.8

9 BUR,ND 16 6.6

10 BUR,PCE 2 0.8

11 ND,PCE 2 0.8

12 ND,<CST 2 0.8

13 PCE,<CST 4 1.7

INFERENCE

From The above table it is inferred, that the respondents opined that

home insurance is Necessary because of the following reasons.( 42.5)% feel

Burglary may occur, (27.5%) feel natural disaster may occur any time,(21.25)%

feel it gives peace of mind, (18.75)% feel it costs very less, (!.7)% accept with all

the four reason, (2.1)% feel Burglary, natural disaster may occur and it gives

peace of mind, (1.2)% feel Burglary, natural disaster may occur and it cost very

less, (0.8)% feel Burglary may occur, it gives peace of mind and it cost very less,

(6.6)% feel Burglary, natural disaster may occur, (0.8)% feel Burglary and it gives

peace of mind, (0.8)% feel natural disaster may occur and it gives peace of mind,

(0.8)% feel natural disaster may occur and it cost very less (1.7)% feel it gives

peace of mind and it cost very less.

44

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 45/56

TABLE NO. 4.18

REASONS WHY HOME INSURANCE IS NOT NECESSARY

S.No. ReasonsNo. of

RespondentsPercentage

1Nothing will

happen to home5 25.0

2 Waste of money 9 45.0

3Lack of

knowledge5 25.0

4Distrust about

honoring Claims1 5.0

Total 20 100.0

INFERENCE

From The above table it is inferred that among the 20 respondents who

felt home insurance is not necessary, (25.0) % of the respondents opined that

home insurance is Not Necessary because of the reason Nothing will happen to

home, (45.0%) of the respondents opined that taking home insurance is Waste of

money, (25.0%) of the respondents opined that they do not have the adequate

knowledge about home insurance, (5.0%) of the respondents opined that they

don’t trust general insurance companies to honor the claims in time.

45

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 46/56

46

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 47/56

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 48/56

48

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 49/56

TABLE NO. 4.20

COMPARISION OF PERCEIVED NEED FOR INSURANCE AND LEVEL OF

WILLINGNESS TO RECEIVE A SALE CALL

Level of willingnessOpinion on need for home insurance

NecessaryNot

NecessaryNo Idea Total

Definitely yes 14(5.83)

0 014

(5.83)Probably 43

(17.92)2

(0.83)7

(2.92)52

(21.61)Probably not 18

(7.5)4

(1.67)6

(2.5)28(11.67)

Definitely not 45(18.75)

10(4.17)

5(2.08)

60(25.0)

Already have 80(33.3)

5(2.08)

1(0.42)

86(35.833)

Total 200(83.33)

21(8.75)

19(7.92)

240(100)

INFERENCE

It is inferred from above, that only 5.83% said that home insurance is

necessary and they are willing to be approached by sales people. Around 18% of

the respondents who said home insurance was necessary expressed by saying

“probably they are willing” and 18.75% expressed that they do not want to be

disturbed by sales people.

49

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 50/56

CHAPTER 5

FINDINGS, SUGGESTIONS AND CONCLUSION

5.1 FINDINGS

Level of awareness-Home Insurance &Companies

Among the respondents, majority is salaried employees and most of

the respondents have annual income below Rs2Lakh.

Among the various types of insurance, only (27.1%) of the total

respondents are aware of all types of insurance such as Automobile, Health,

Travel and Home insurance. Majority of the respondents (around 60%) are awareof automobile insurance and next to it (58%) are aware of health insurance.

Among various general insurance products, Automobile insurance was

most commonly used (i.e.) with around 60% of the respondents using it, The next

most common used product was Home Insurance (36%) health insurance came

third with 33% of the respondents using it.

When the preference among various insurance products was studied,

majority of respondent’s ranked Life insurance as number 1, followed by Health

50

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 51/56

insurance as number 2, Automobile insurance as number 3 and Home insurance

was ranked 4th.

When opinion about the necessity of home insurance is studied,

majority of them (i.e.) 200 out of 240 respondents opined that it is necessary, but

still when the preference among the various insurance products is studied home

insurance was ranked at 4th place. When respondents who did not have a home

insurance policy were asked whether they were willing to be approached by

sales personnel, equal number of respondents replied affirmatively and

negatively.

When the awareness level of various companies providing Home

insurance was studied, majority of the respondents (i.e.) 70% of them, were

aware of ICICI Lombard Next to it around 50% of them were aware of Oriental

insurance and United India assurance and almost 40% of them are aware of

TATA AIG.

Most of the respondents expressed that they have good or fair

knowledge about home insurance.

Almost 90% of the respondents opined that home insurance is

“Necessary”. Responding to the question as to why home insurance was

necessary, 42.5% stated Burglary as the cause and 27.5% stated naturaldisaster as the reason

Among the total respondents, 10% opined that home insurance is Not

Necessary and among them (45%) fell it is a waste of money.

51

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 52/56

Brand awareness

Only (30%) of the total respondents were able to recall ICICI Lombard

with out any assistance, However, among the various insurance companies, the

recall of ICICI Lombard was the highest (i.e.) 72 out of 240 respondents could

name ICICI Lombard.

Many of respondents (20.42%) who identified ICICI through the LOGO

were influenced by television and (8%) of them who identified ICICI Lombard

were influenced by the sales people.

Most of respondents (5.42%) who identified ICICI through the

SLOGAN were influenced by sales people and most of the respondents (10%)

who identified ICICI Lombard were also influenced by the sales people.

Majority of respondents (72.5%) identified ICICI Lombard through the

assistance of the company name, logo and slogan and were able to recognize

the industry with which the company is associated. Among those respondents

(48.33%) of them recognized it is a general insurance company, (15%) of them

recognized it as a home insurance company.

52

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 53/56

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 54/56

5.3 CONCLUSION

The study could be concluded by saying that home insurance is

deemed to be a great necessity today, especially after natural disasters like

Tsunami took place. However priority wise, it has a lower priority when

compared with other forms of insurance like life, health and automobile.

ICICI Lombard has fairly good recall levels. The need, awareness and

preferences for home insurance can be enhanced by communicating the core

need of the product consciously.

54

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 55/56

REFERENCES

1. Umasekaran (2002), ' Research Methods for Business', John Wiley &

Sons, Inc. 4th edition.

2. Richard I. Levin, David S. Rubin (2002), 'Statistics for Management',

Prentice Hall of India Private Limited, New Delhi, 7th edition.

3. Kothari C.R (2002), 'Research Methodology', Wishwa Prakashan,

New Delhi, 2nd edition.

4. Philip Kotler (2003), ‘Marketing Management’, Pearson Education

Limited, Singapore, 11th edition.

6. Websites:

www.irda.com www.icici Lombard .com

www.google.com

8/6/2019 Yasir Final

http://slidepdf.com/reader/full/yasir-final 56/56

1-14,16,18,20,22,24,26,27,29,31,33,34,36,37,39,41,43,45,47,49,51,53-59

Related Documents