Who will become a global financial center, Shanghai or Hong Kong? Cheung Yan-leung Dean & Professor (Chair) of Finance School of Business Hong Kong Baptist University

Who will become a global financial center, Shanghai or Hong Kong? Cheung Yan-leung Dean & Professor (Chair) of Finance School of Business Hong Kong Baptist.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Who will become a global financial center,Shanghai or Hong Kong?

Cheung Yan-leungDean & Professor (Chair) of Finance School of Business Hong Kong Baptist University

Agenda

1. The definition of Global financial centre

2. Global Financial Centre Index

3. Background & advantage of Shanghai

4. Background & advantage of Hong Kong

5. Threat of Shanghai

6. How to face to the Competition

Global Financial Center

“have sufficient critical mass of financial services institutions to dispense with intermediaries and to connect international, national and regional financial services participants directly”

(City of London)

Global Financial Centres Index (GFCI)

Published by the Z/Yen Group of the City of London

A ranking of the competitiveness of financial centre based 57 instrumental factors and an online questionnaire on 26,629 financial centre assessments

Ratings for 62 financial centres calculated by a ‘factor assessment model’.

Instrumental factors

Provided by a number of reputable organizations; Executive MBA Global Rakings (financial Times), Human Development Index (UNDP), Business Environment (Economist Intelligence Unit), Corruption Perception Index (transparency International), Ease of Doing Business Index (world Bank), Global Competitiveness Index (World Economic Forum) etc…

Online Questionnaire

A simple questionnaire of not more than 20 questions

About the market perception on the ranking of Global Financial Centres

Five Key Aspects People

• Availability of good personnel, the flexibility of the labor market, business education and the development of ‘human capital’

Business Environment • Regulation, tax rates, levels of corruption,

economic freedom and the ease of doing business. Regulation, a major component of the business environment

Five Key Aspects Market Access

• The levels of securitization, volume and value of trading in equities and bonds, as well as the clustering effect of having many firms involved in the financial services sector together in one centre.

General Competitiveness• Overall competitiveness of centres in terms of

more general economic factors

Five Key Aspects

Infrastructure • Focus on the cost and availability of buildings

and office space, it also includes other infrastructure factors such as transport

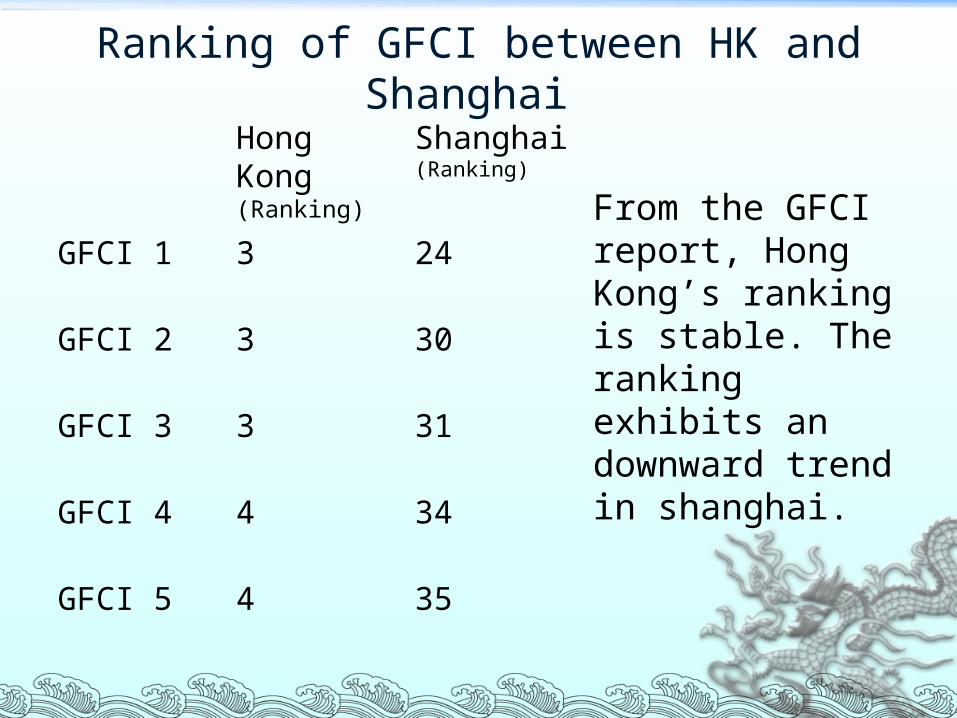

From the GFCI report, Hong Kong’s ranking is stable. The ranking exhibits an downward trend in shanghai.

Ranking of GFCI between HK and Shanghai

Hong Kong (Ranking)

Shanghai(Ranking)

GFCI 1 3 24

GFCI 2 3 30

GFCI 3 3 31

GFCI 4 4 34

GFCI 5 4 35

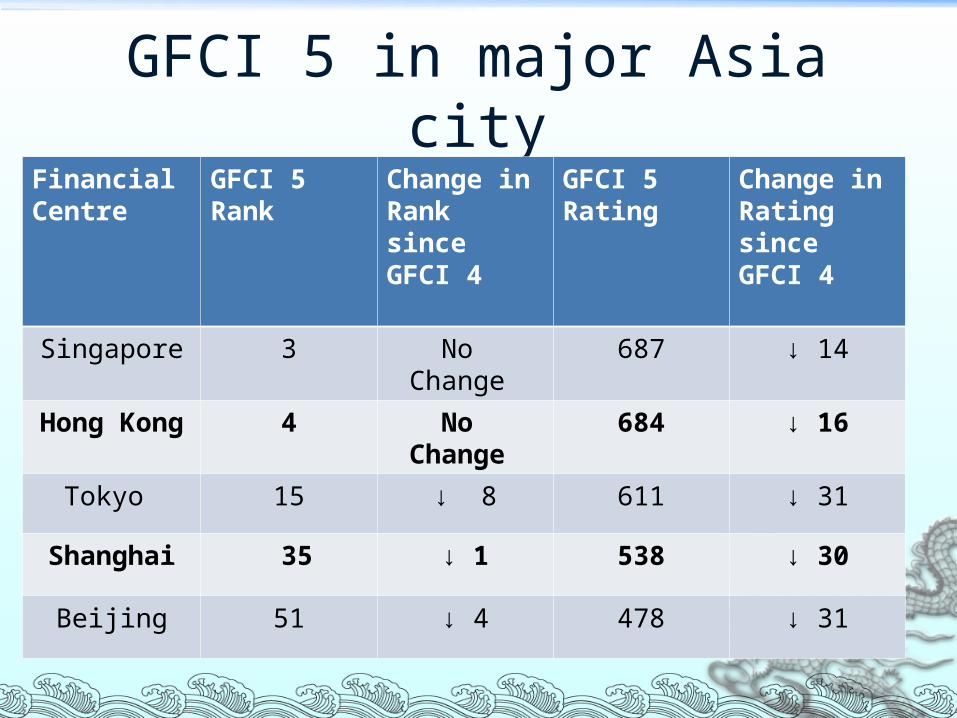

GFCI 5 in major Asia cityFinancial Centre

GFCI 5Rank

Change in Ranksince GFCI 4

GFCI 5Rating

Change in Ratingsince GFCI 4

Singapore 3 No Change 687 ↓ 14

Hong Kong 4 No Change 684 ↓ 16

Tokyo 15 ↓ 8 611 ↓ 31

Shanghai 35 ↓ 1 538 ↓ 30

Beijing 51 ↓ 4 478 ↓ 31

Shanghai: market background

Financial centre in 1930’s Security market closed down in 1949 Slow development between 1949 to 1978 Shanghai’s re-emergence as a financial centre

in 1990 Stock exchange re-opened in 1990 Largest capital raising market in Asia, 2007 (1)

Bond and commodity markets have been established in recent year

(1) : Source :Shanghai Stock Exchange Fact Book 2007

13

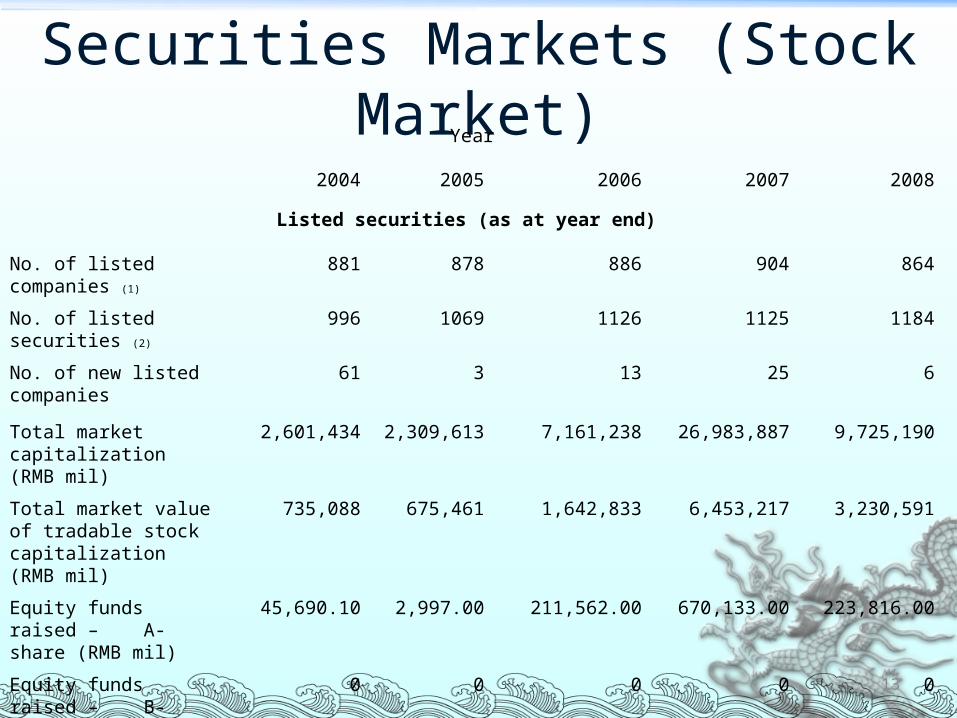

Securities Markets (Stock Market)Year

2004 2005 2006 2007 2008

Listed securities (as at year end)

No. of listed companies (1)

881 878 886 904 864

No. of listed securities (2) 996 1069 1126 1125 1184

No. of new listed companies

61 3 13 25 6

Total market capitalization (RMB mil)

2,601,434 2,309,613 7,161,238 26,983,887 9,725,190

Total market value of tradable stock capitalization (RMB mil)

735,088 675,461 1,642,833 6,453,217 3,230,591

Equity funds raised – A-share (RMB mil)

45,690.10 2,997.00 211,562.00 670,133.00 223,816.00

Equity funds raised – B-share (RMB mil)

0 0 0 0 0

(1) All the A & B Share listed on the Exchange are included.

(2) listed securities : include A, B share, Fund, ETF, Warrant T-Bond, Debenture CB & Bond Repo

Source: Shanghai Stock Exchange, Wind

The key competitiveness areas in shanghai

Location Shanghai is located at the Changjiang Delta, that is

the central part of China. Large hinterland , such as Jiangsu, Anhui, provide

larger labor support and potential market Historical factor

Shanghai has been a major China’s financial centre in 1930

Lower labor cost Compare with Hong Kong

Language – Putonghua

The key competitiveness areas in shanghai

Strong government support Shanghai announced in April 1990 its plan to

develop the Pudong New Area, and its ambition to re-emerge as a major international financial centre by 2010,

Recently, State Council of China government declared to support for Shanghai’s plan to become an international financial center by 2020

Hong Kong market background

Grown rapidly in 1990’s Because of “red-chip” and “H-share”

Hong Kong Exchange and Clearing Co. Ltd. was established in 2000, merged by The Stock Exchange of Hong Kong, The Hong Kong Futures Exchange and The Hong Kong Clearing Ltd.

Hong Kong market background

Focus on product development in recent year Warrant Callable Bull/Bear Contracts (CBBC) Exchange-Traded Funds (ETFs) Real Estate Investment Trusts (REITs)

The largest derivative warrant market in the world , 2007

18

Securities Markets (Stock Market)

Year2004 2005 2006 2007 2008

Listed securities—Main board (as at year end)

No. of listed companies 756 934 975 1048 1087

Domestic (1) 882 925 967 1039 1077

Foreign (2) 10 9 8 9 10

No. of listed securities 1,971 2,448 3,184 5896 5654

No. of new listed companies

49 57 56 82 47

Total issued capital (HK$mil)

431,926.99 704,903.12 892,349.40 953,098.38 972,135.97

Total market capitalization (HK$mil)

6,629,176.75 8,113,333.48 13,248,820.50 20,536,462.82 10,253,588.78

Equity funds raised (HK$mil)

276,202.61 298,237.42 516,011.88 571,078.35 418,187.43

(1) All the China incorporated enterprises with H shares listed on the Exchange are included.

(2) A listed company would be counted as a foreign company if it is incorporated overseas AND has a majority of its business outside Hong Kong

Source: Hong Kong Exchange Fact Book 2004 to 2008.

The key competitiveness areas in Hong Kong

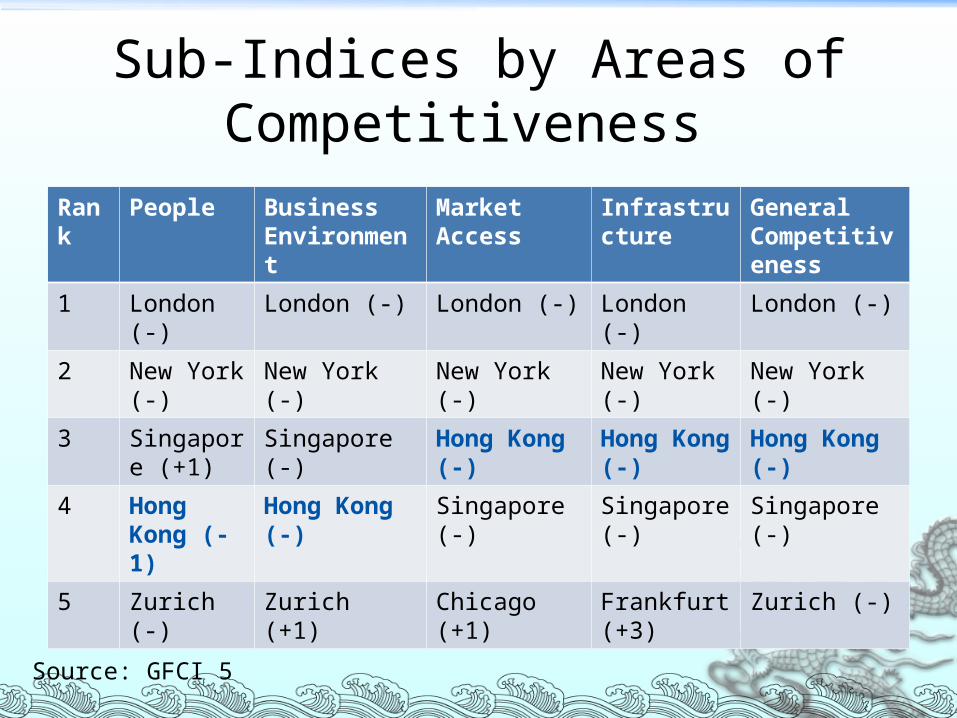

From the GFCI 5 report, Hong Kong has performed well in all of the sub-Indices by Area of competitiveness. Include: People Business Environment Market Access Infrastructure General Environment Competitiveness

Sub-Indices by Areas of Competitiveness

Rank

People Business Environment

Market Access

Infrastructure

General Competitiveness

1 London (-) London (-) London (-) London (-) London (-)

2 New York (-)

New York (-) New York (-) New York (-)

New York (-)

3 Singapore (+1)

Singapore (-) Hong Kong (-)

Hong Kong (-)

Hong Kong (-)

4 Hong Kong (-1)

Hong Kong (-) Singapore (-) Singapore (-)

Singapore (-)

5 Zurich (-) Zurich (+1) Chicago (+1) Frankfurt (+3)

Zurich (-)

Source: GFCI 5

The key competitiveness areas in Hong Kong

People Well educated labor Our universities have top rankings in the world flexible immigration policy

Business Environment• Simple and straightforward tax regime in both of

corporate and personal tax• Laissez fare economy• Stable country currency system-Linked to the U.S. dollar• free flow of information

The key competitiveness areas in Hong Kong

Business Environment (Cont’)• Low corruption rate• The World Bank publishes a measure of regulation and

corruption under the title Governance Matters. Hong Kong stands in top ranking

The key competitiveness areas in Hong Kong

Market Access• High access to international market• No barrier for the foreign exchange • Concentration of international banks and

financial institutions Infrastructure

• Sufficient A-Grade office • has been continuously improving and

upgrading the infrastructure

Threat From Shanghai Rapid improvement in business

environment • Infrastructure • Living quality• Human resource

Replay Hong Kong to become a “gateway” to China market

The report of GFCI 5 shows that the investors concentrate on shanghai rather than Hong Kong

Threat From ShanghaiThe Centres Where New Offices will be Opened

The GFCI 5 report shows that the investors prefer Shanghai for their future investment rather than Hong Kong

Source: GFCI 5

Threat From Shanghai

The report reflects that the investor recognizes the role of Shanghai will be more significant in the foreseeable future.

Source: GFCI 5

Centers Likely to Become More Significant

What should we do?

Bond Market Development The bond market develops slowly. Up to July

2007, the total amount of corporate bond was up to USD 82 billion, while in 2002 that is USD 53.3 billion.

Hong Kong market can facilitate more China Enterprises to issue corporate bond.

What should we do?

Insurance Industry Development “Hong Kong remains a strong financial centre

and is in 3rd or 4th place in all industry sector sub-indices, except Insurance, and in all areas of competitiveness.”

Source: Comment from GFCI 5 report

What should we do?

Improve the quality of the listing company

Hong Kong should focus on the improvement of transparency for listing companies.

Frequency of financial reports remains limited to annual and interims, whole reporting deadlines is well below international best practice.

What should we do?

Diversify our industrial structure

Hong Kong should diversify the industry, for example: Biological technology, education, tourism, logistics, as well as IT and other high-tech industries

Now, Hong Kong focuses mainly on the tertiary industries, esp. financial industry

What should we do?

Regulation of the financial institutions “Lehman brother” event leads the public to

lose confidence to the financial institutions. Financial crisis shows that Hong Kong needs

to strengthen the regulation framework for the financial institutions

It is wishful thinking that financial institutions can be self-regulated.

What should we do?

Strengthen the co-operation to Guangdong Region

Hong Kong needs to focus not only on the “hardware” co- operation with Guangdong Region only.

Hong Kong lacks of co-operations in education, training, tourism, financial server etc with Guangdong Region

Can we co-operation?Before full convertibility of the RMB Hong Kong can be a “bridge” for the

Chinese and foreign companies the wealth management centre Offshore RMB settlement centre Can be a “instructor” to the Shanghai for

develop the financial centre.

Can we co-operation?

After full convertibility of the RMB To separate the role, similar to New York

and Chicago Shanghai can focus on the traditional

business related to local enterprise and citizen, such as stock, bond and banking service.

Can we co-operation?

After full convertibility of the RMB (cont’) Our international market experience can

help Chinese company to develop their business into oversea market

Hong Kong can focus on business related to financial innovation, derivative product, wealth management, foreign exchange

The gateway for the South Asian investor to China market

~END~

Related Documents