What to make of steel in 2009 Presentation to SMA Annual Members Conference Washington DC May 19, 2009

What to make of steel in 2009 Presentation to SMA Annual Members Conference Washington DC May 19, 2009.

Dec 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

What to make of steel in 2009

Presentation to

SMA Annual Members Conference

Washington DC

May 19, 2009

www.first-river.com2

What to make of steel in 2009

A dangerous place for forecasting

Plenty to worry about Pursuing unhappiness Some confident

predictions

A dangerous place for forecasting

www.first-river.com4

• Rare (highly improbable)• Hard to predict (except in retrospect)• Consequential

Last year’s message…Black swan events are:

www.first-river.com5

Other forecasting miseries

Missed 2008 – in September! Recalibrated 2009 several times Q1 6 reasons why it won’t be so bad this

time (October 2008)

– Global economic growth (3% to -2.8%)

– Industrialization

– Capacity management

– Chinese industry rationalization

– Renewed consolidation

– Growth, Environment & Energy

A man who predicts the future is lying – even if he’s right Arab proverb

www.first-river.com6

What to do/think?

Avoid too much emotional commitment to one outcome

Avoid to much organizational commitment to one outcome

Consider all outcomes equally possible

Be ready

Plenty to Worry About

www.first-river.com8

World steel forecastApparent steel use forecast & y-o-y change 2008 to 2009

NAFTA

Europe

CIS

Dev. Asia

Brazil

China ME&A

India

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Y-o

n-Y

ch

ang

e

0

100

200

300

400

500

600

700

800

900

Developed Developing

M T

on

ne

s A

pp

are

nt

Ste

el U

se

2008 2009

-27%

-8%

2008: 1,197MT to 2009: 1,019MT ~15% decline

Developed world consumption from 36% to 31% of total

www.first-river.com9

2009 in a long term contextGlobal steel annual production changes

Year Decline

1 1921 -38%

2 1932 -27%

3 1931 -27%

4 1945 -25%

5 1919 -24%

6 1908 -22%

7 1930 -21%

8 1914 -21%

9 1938 -19%

10 2009F

-15%

11 1982 -9%

12 1975 -9%

13 1958 -7%

14 1918 -6%

15 1944 -5%Source: worldsteel, First River

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Ye

ar

on

Ye

ar

Ch

an

ge

in P

rod

uc

tio

n

www.first-river.com10

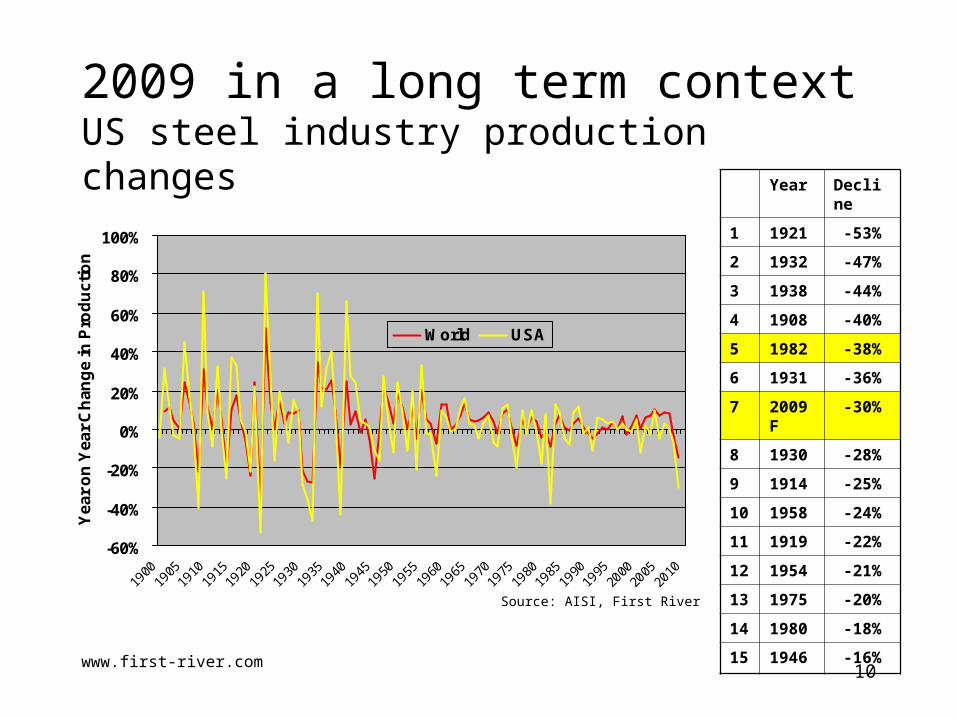

2009 in a long term contextUS steel industry production changes

Year Decline

1 1921 -53%

2 1932 -47%

3 1938 -44%

4 1908 -40%

5 1982 -38%

6 1931 -36%

7 2009F

-30%

8 1930 -28%

9 1914 -25%

10 1958 -24%

11 1919 -22%

12 1954 -21%

13 1975 -20%

14 1980 -18%

15 1946 -16%

Source: AISI, First River

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Ye

ar

on

Ye

ar

Ch

an

ge

in P

rod

uc

tio

n

World USA

www.first-river.com11

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-3% -2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Change in GDP (%)

Ch

an

ge

in S

tee

l De

ma

nd

%GDP forecast indicates 20-25% drop in US finished steel demand

Sources: AISI, US BEA, IMF, First River

2008

1980

1982

1975

IMF World Economic Outlook April 2009

US 2009 GDP Forecast: -2.8%

2009

www.first-river.com12

0

25

50

75

100

125

150

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Mill

ion

To

ns

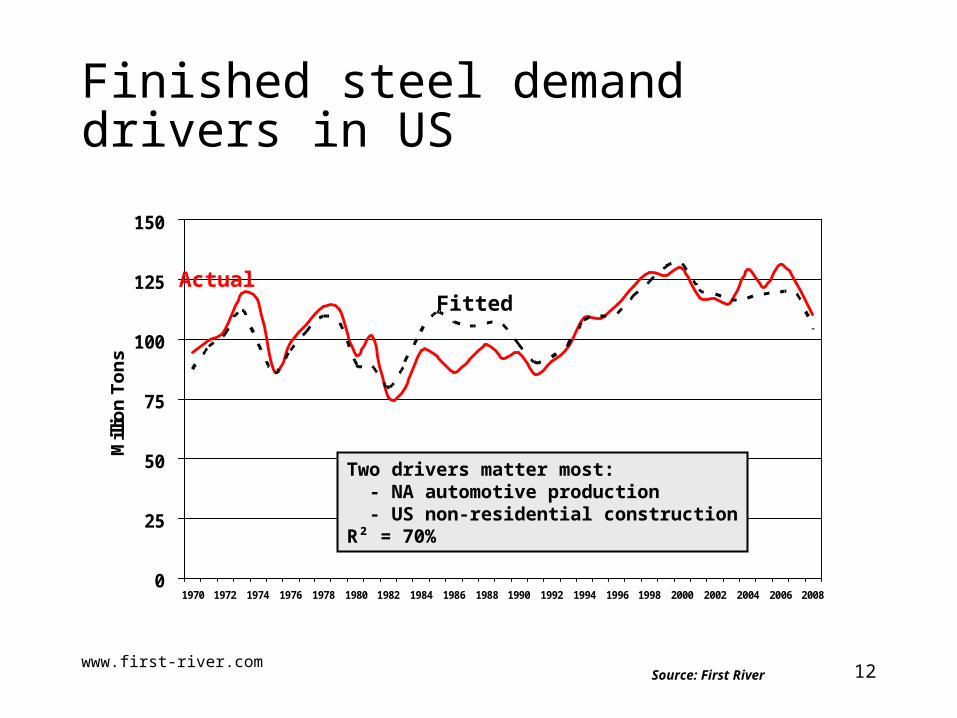

Finished steel demand drivers in US

ActualFitted

Two drivers matter most: - NA automotive production - US non-residential constructionR² = 70%

Source: First River

www.first-river.com13

14.7

13.7

12.3

10.0

12.6

8.2

4

8

12

16

20

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010F 2012F

Mill

ion

Veh

icle

s

NA automotive production forecastBelow 15 million thru 2013

Source: CSM Worldwide (March 2009)

35% drop this yearAverage 11.8 2009-2013

www.first-river.com14

Big 3 participation in car productionBig 3, Others units & share 1985-2008, US only

Source: Ward’s automotive, FRC

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,00019

85

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

'000

's o

f U

nit

s

30%

40%

50%

60%

70%

80%

90%

100%

%

Big 3 Others Big 3 Share - rhs

www.first-river.com15

1,467

1,505

1,246

1,0941,131

1,397

0

500

1,000

1,500

2,000

2,500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010F 2012F

Mill

ion

Sq

uar

e F

eet

US non-residential construction No return to level of late 1990s thru 2013

Source: FW Dodge (Spring 2009)

22% drop 2008 to 2010Average 1,300 2009-2013

www.first-river.com16

115

110

100

90

80

0

25

50

75

100

125

150

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010F 2012F

Mill

ion

To

ns

US finished steel demand forecastWeak throughout forecast period

Actual ADC

Forecast

Source: CSM, FW Dodge, WSA, First River

30-40% drop this year

110

68 (WSA)

www.first-river.com17

Operating rates for rest of 2009

Million TonsFull Year

2009Q1 Est. Q2-Q4

US ADC all steel products 75.0 16.5 58.5

- Net Imports 12.0 3.5 8.5

Finished Steel Production 63.0 13.0 50.0

Finished steel production as % of peak shipments (110 MT)

57% 47% 61%

Source: AISI, MSCI, First River

Risk is to the downside

www.first-river.com18

0

20

40

60

80

100

120

140

2004-08 2009-13 2015

Mill

ion

To

ns

ADC Finished Steel Production Net Finished Imports

Average US demand & production2009-2013

~20% average decline Recovery by 2015?

www.first-river.com19

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Cap

acity

Util

izat

ion

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Cap

acity

Util

izat

ion

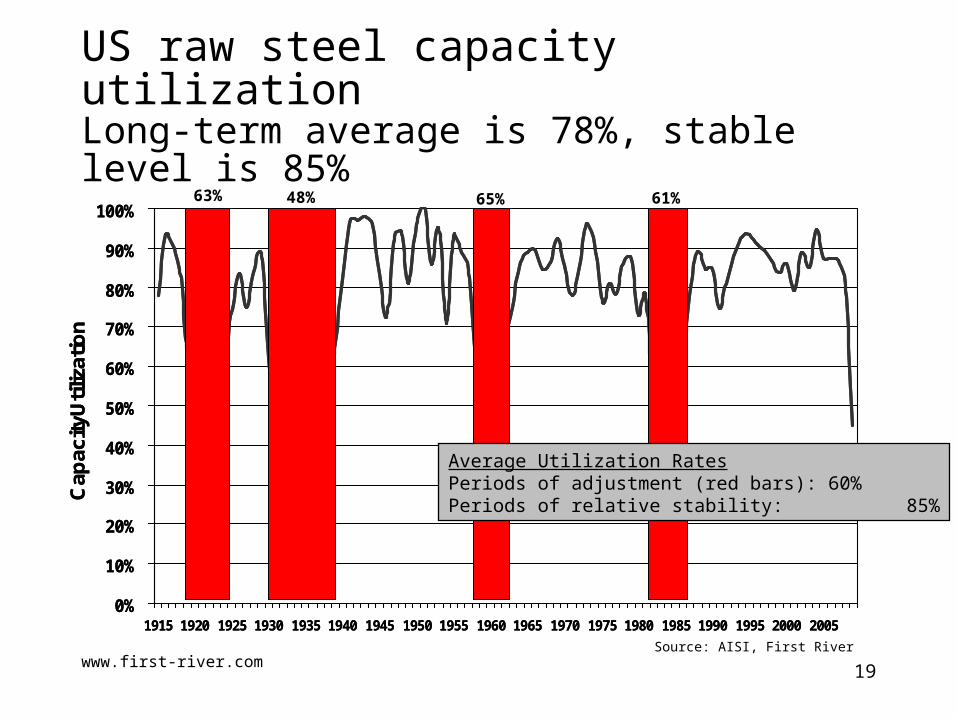

US raw steel capacity utilizationLong-term average is 78%, stable level is 85%

Source: AISI, First River

63% 48% 65% 61%

Average Utilization RatesPeriods of adjustment (red bars): 60%Periods of relative stability: 85%

www.first-river.com20

Future raw steel capacity requirementA 30 MT issue?

2009-2013

Raw Steel Production 85.0

Capacity utilization “stable periods” 85%

= Target raw steel capacity 100.0

2008 raw steel capacity incl. additions

132

= “Excess” Capacity 32Source: First River

www.first-river.com21

2009 – Part of a notable recession

(4)

(2)

0

2

4

6

8

10

12

14

16

18

20

Mo

nth

s

Duration GDP Recovery to Prior GDP

Source: NBER, First River

GD

P L

os

s (

%)

1973-1975 1981-1982 1990-1991 2001 2007-2009?

Thru Q1 2009

1980

Thru May 2009

www.first-river.com22

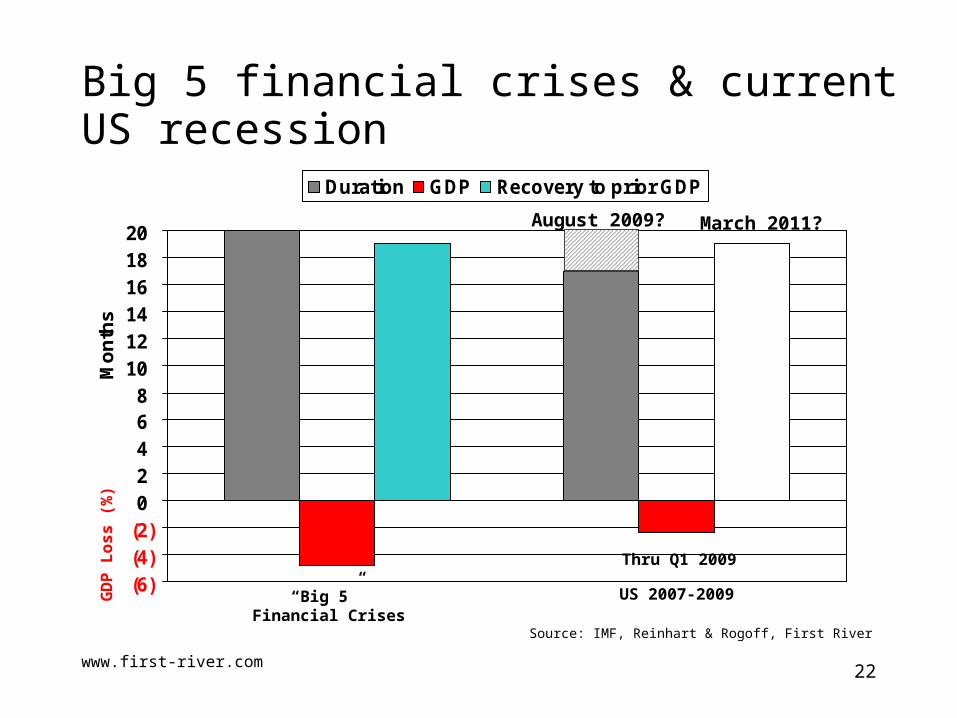

Big 5 financial crises & current US recession

(6)(4)(2)02468

101214161820

Mo

nth

s

Duration GDP Recovery to prior GDP

Source: IMF, Reinhart & Rogoff, First River

GD

P L

os

s (

%)

“Big 5” Financial Crises

US 2007-2009

August 2009?

Thru Q1 2009

March 2011?

Pursuing unhappiness

www.first-river.com24

THE YEAR THE BOTTOM FELL OUT FOR STEEL

STEEL MILLS COMPLAIN ON

EXPORTS OF SCRAP

Not since 1959, when the steel industry was in the middle of a 15-month slump, have steel executives gathered… for their annual meeting under worse circumstances. Seven out of 10 steel companies operated in the red during the first quarter, and losses are expected to mount in the second quarter. Nearly 30 percent of the nation's steelworkers have been laid off, and industry analysts, who just a month ago were quibbling over whether shipments for the year would slide below 80 million tons, now expect them to be under 70 million tons…

FORECASTS WORSENING FOR STEEL

Industry economists who had predicted as recently as January that steel shipments would equal last year's level of 87 million tons, have scaled back those forecasts to about 80 million tons - the low reached in the severe sales slump that developed after the 1974-75 recession. Some even say that shipments will drop below 80 million tons for the first time since 1963, when the industry shipped 75.5 million tons.

UNUSUAL ALLIANCE

SEEKING TO POSTPONE

POLLUTION CURBS ON

STEEL INDUSTRY

www.first-river.com25

THE YEAR THE BOTTOM FELL OUT FOR STEEL

STEEL MILLS COMPLAIN ON

EXPORTS OF SCRAP

Not since 1959, when the steel industry was in the middle of a 15-month slump, have steel executives gathered… for their annual meeting under worse circumstances. Seven out of 10 steel companies operated in the red during the first quarter, and losses are expected to mount in the second quarter. Nearly 30 percent of the nation's steelworkers have been laid off, and industry analysts, who just a month ago were quibbling over whether shipments for the year would slide below 80 million tons, now expect them to be under 70 million tons…

FORECASTS WORSENING FOR STEEL

Industry economists who had predicted as recently as January that steel shipments would equal last year's level of 87 million tons, have scaled back those forecasts to about 80 million tons - the low reached in the severe sales slump that developed after the 1974-75 recession. Some even say that shipments will drop below 80 million tons for the first time since 1963, when the industry shipped 75.5 million tons.

UNUSUAL ALLIANCE

SEEKING TO POSTPONE

POLLUTION CURBS ON

STEEL INDUSTRY

1982

www.first-river.com26

No déjà vu all over again

No functional union agreement or relationship Unconsolidated industry Poorly invested, inefficient facilities Unfocused industry diversified outside steel Lots of government ownership around the world No prospects for industrialization among 2Bn+ people Little transparency in prices, inputs, costs, production & demand

Far fewer prospects for recovery in 1982 than 2009

www.first-river.com27

The pursuit of unhappinessThe situation is hopeless, but not serious

Glorification of the past– Nothing worthy in the present

Obsession with precedents for unprecedented times– Nothing worth learning from the present

The Fatal Glass of Beer– No escaping the sins of too much leverage

General paranoia & fatalism– They’re out to get us– Nothing we do will make any difference

www.first-river.com28

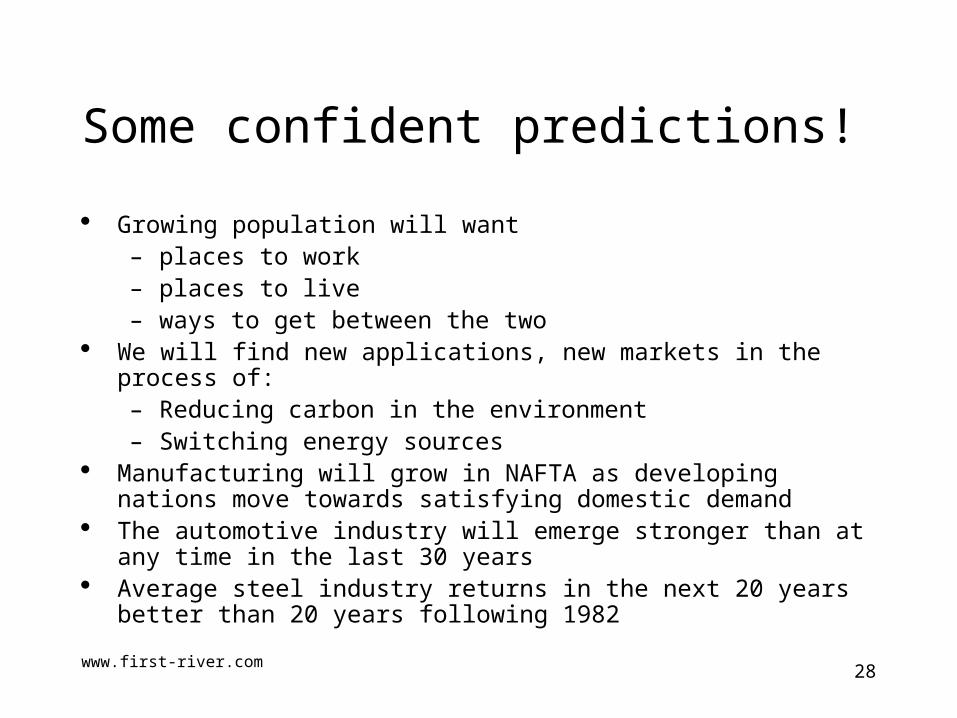

Some confident predictions!

Growing population will want– places to work– places to live– ways to get between the two

We will find new applications, new markets in the process of:– Reducing carbon in the environment– Switching energy sources

Manufacturing will grow in NAFTA as developing nations move towards satisfying domestic demand

The automotive industry will emerge stronger than at any time in the last 30 years

Average steel industry returns in the next 20 years better than 20 years following 1982

www.first-river.com29

What to make of steel in 2009?

A scary ride to the bottom?

A turning point A wake-up call for

the developed world Strategies

reconsidered Some retrenchment

Related Documents