Welsom Space Power August 2008 1 CONFIDENTIAL Subject to NDA Welsom Space Power Business Plan A lucrative opportunity in PV solar arrays for space based energy creation V5.7 23. April 2009 Breakthrough Technology for the fossil fuel free economy Vacuum deployment of MSRS Technologies CP1 ® polyimide 20-meter boom (source NASA)

Welsom Space Power August 2008 1 CONFIDENTIAL Subject to NDA Welsom Space Power Business Plan A lucrative opportunity in PV solar arrays for space based.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Welsom Space Power

August 2008 1CONFIDENTIAL Subject to NDA

Welsom Space Power Business Plan

A lucrative opportunity inPV solar arrays for space based energy

creationV5.7 23. April 2009

Breakthrough Technology for the fossil fuel free economy

Vacuum deployment of MSRS Technologies CP1® polyimide 20-meter boom (source NASA)

Welsom Space Power

April 2009 2

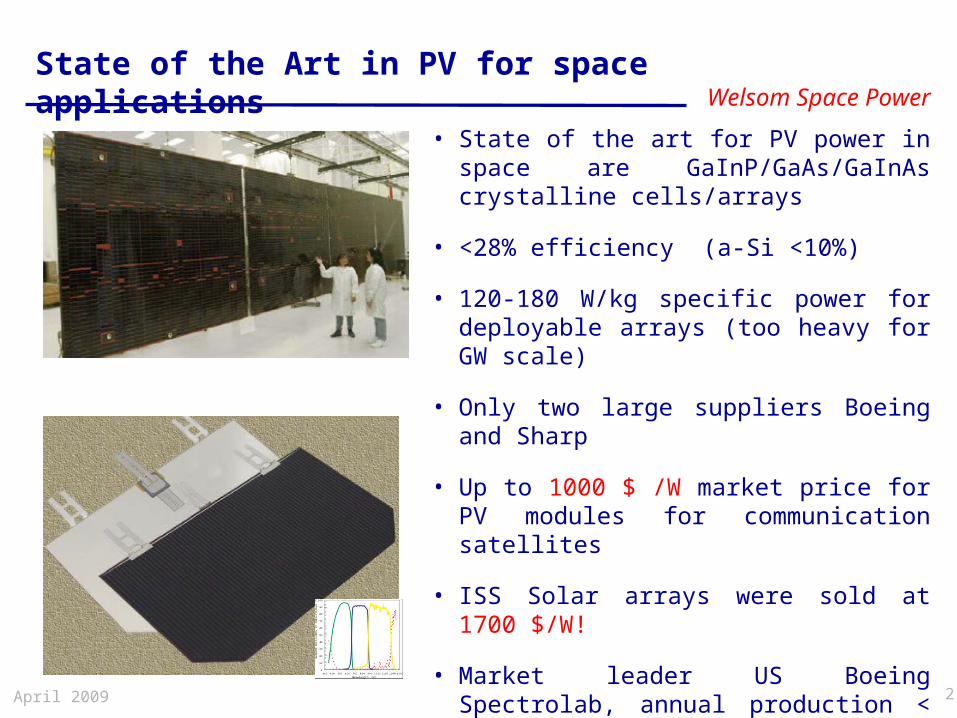

State of the Art in PV for space applications

• State of the art for PV power in space are GaInP/GaAs/GaInAs crystalline cells/arrays

• <28% efficiency (a-Si <10%)

• 120-180 W/kg specific power for deployable arrays (too heavy for GW scale)

• Only two large suppliers Boeing and Sharp

• Up to 1000 $ /W market price for PV modules for communication satellites

• ISS Solar arrays were sold at 1700 $/W!

• Market leader US Boeing Spectrolab, annual production < 1.3MW or <1% of total PV world market 1.3GWpa

• Space PV is today still a niche market, but with >1 B$ annual turnover!

Welsom Space Power

April 2009 3

FutureHistory

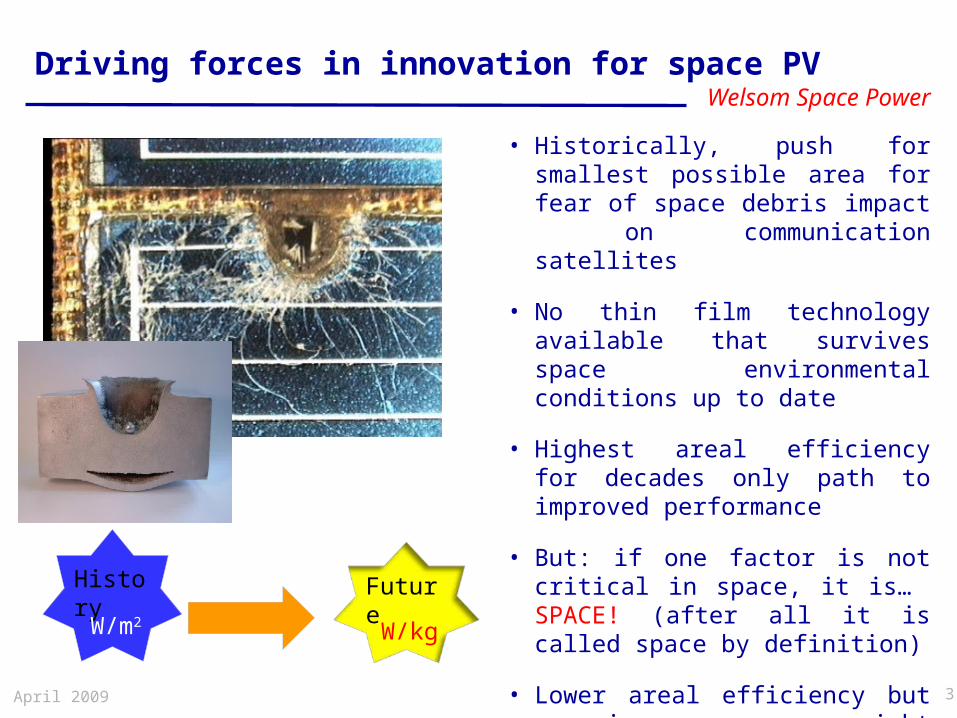

Driving forces in innovation for space PV

• Historically, push for smallest possible area for fear of space debris impact on communication satellites

• No thin film technology available that survives space environmental conditions up to date

• Highest areal efficiency for decades only path to improved performance

• But: if one factor is not critical in space, it is… SPACE! (after all it is called space by definition)

• Lower areal efficiency but superior weight dramatically pushes specific power W/kg, which is far more important in space applications due to launch cost of > 10‘000$/kg

W/m2 W/kg

Welsom Space Power

April 2009 4

Why is PV for space advancing so slowly?

• Extremely high entry barriers for newcomers due to complex space heritage requirements

• Bureacratic hurdles in government organisations like NASA, ESA preventing disruptive innovation

• Limited public private partnerships so far in driving innovation

• Perception based on historic experience, space applications are considered intrinsically long in transfer from laboratory to real use

• BUT:

• Strong private US entrepreneurs entering the space market due to liberalization and lack of NASA funding, such as Richard Branson, Bigelow Aerospace, SpaceX are pushing innovation and increase market dynamics

• Global cooperations not only encouraged but actively pushed, unleashing unprecedented synergies in radical innovations such as SBSP

Welsom Space Power

April 2009 5

What is the key strength of Switzerland?

• Switzerland is the world‘s pioneer in thin film photovoltaic basic research, pushed since 1994 by University of Neuchâtel, PV laboratory of IMT

• IMT ist the established long term strategic partner of Oerlikon OC Solar, operating the industrial PV R&D Lab Oerlikon SPTec in Neuchâtel since 2003

• IMT is the scientific partner of Bertrand Piccard‘s Solar Impulse Project www.solarimpulse.com

• A private consultant is expert technology and business consultant with relevant PV industry background including cost of ownership and manufacturing know how.

Welsom Space Power

April 2009 6

What led to the global WELSOM consortium?

• Independent discovery by US private entrepreneur Kevin Reed, looking for innovative solutions in retinal implant structures with photosensitive materials

• Unique UV sensitive polymers by US Mantech-SRS company proved of superior dual use also for large area PV thin film applications, discovered in 2005

• First scientific publication at PV conference in Hawaii 2006

• After intense lobbying pushed by Kevin Reed, global partners could be convinced to seriously look into a cooperation both in core group and supply chain

• Nearly two years of negotations led by Reed, a private consultant and IMT led to a worldwide exclusive technology contract for commercialization of thin film based PV technology for space applications, signed in September 2007

• Welsom has a global monopoly for ultralight advanced PV technology for space!

Welsom Space Power

April 2009 7

Welsom Executive summary

• Welsom = Weightless Solar Modules, acronym by Consortium partners

• Welsom has proprietary technology to produce space solar power arrays that are 35 times lighter and 100 times smaller in stowed volume than existing arrays.

• Welsom will use this technology to produce solar power systems for space and high altitude applications in the 10-100 kW range.

• Our unique selling proposition (USP): Welsom can manufacture these leading products at one tenth of the price of our competitors.

• Welsom currently seeks €1.2M as the first stage of a €21.6M 3-tranche investment with a 5-year IRR of 48%.

• The initial €1.2M investment can be returned in 4 years with an IRR of 50%. Optional is a right to convert cash contribution to equity after incorporation

• Preferred is MOU combining first two funding stages in one contract to extend planning security, €1.2M and €2.7M with separate equity conversion factor, release of second stage based on successful milestone 0 (proof of concept)

Welsom Space Power

April 2009 8

Company overview

• Welsom is currently organized as a contract among partners of a consortium with the intent to incorporate in Switzerland, HQ preferred in Zug.

• Consortium members include:

- Institut de Microtechnique’s Photovoltaic Laboratories, University of Neuchâtel (IMT), Switzerland.

- Mantech-SRS Technologies, Inc. of Huntsville (MSRS), Alabama, USA

- SESCRC Bioengineering Research, Anaheim, California, USA

- Private business and PV technology consultant, Switzerland.

Welsom Space Power

April 2009 9

Product summary

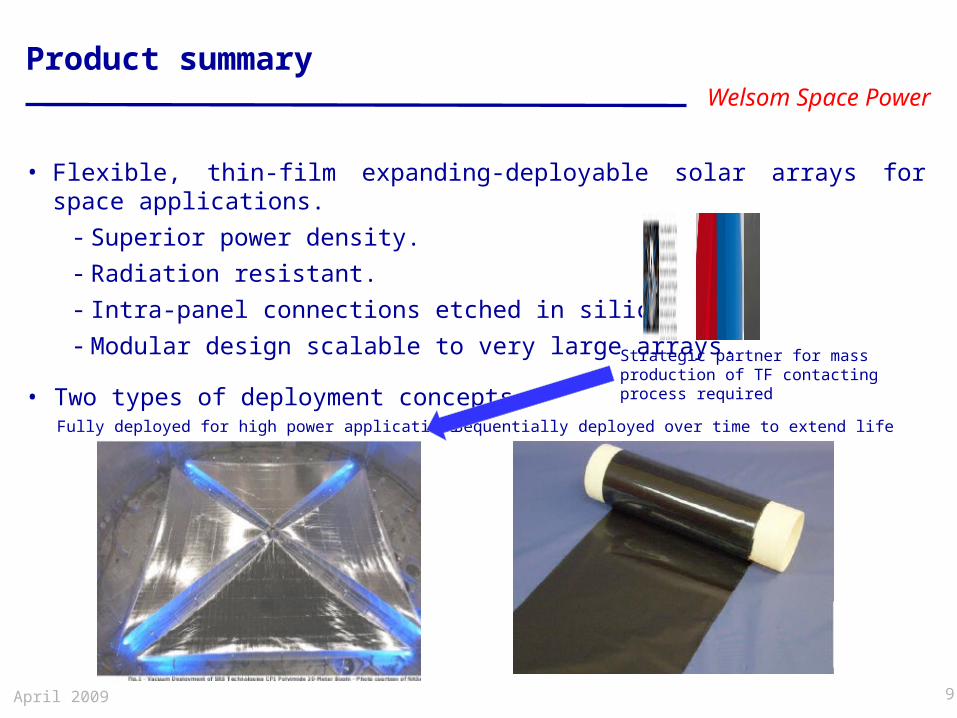

• Flexible, thin-film expanding-deployable solar arrays for space applications.

- Superior power density.

- Radiation resistant.

- Intra-panel connections etched in silicon.

- Modular design scalable to very large arrays.

• Two types of deployment conceptsFully deployed for high power applications Sequentially deployed over time to extend life

Strategic partner for mass production of TF contacting process required

Welsom Space Power

April 2009 10

Competitive advantage

• Flexible, thin-film expanding-deployable solar arrays for space applications.

• Exclusive access to NASA-developed LaRC-CP1® and MSRS-developed CORIN™ polymers:

- Flight-tested with ultra lightweight superstrates and radiation resistance.

• Exclusive access to Oerlikon's terrestrial-based solar power array equipment:

- Based on Welsom’s relationship with IMT.

• Exclusive access to IMT's thin-film talent, know-how, and relevant IP.

• First mover advantages:

- First thin-film, flexible arrays for space applications.

- Preparations underway for flight demonstration aboard Genesis-2 commercial space station.

- Will have production equipment ready to go shortly after flight testing.

• All the advantages result in a unique selling proposition for Welsom: We can manufacture our products at one tenth of the price of our competitors!

Welsom Space Power

April 2009 11

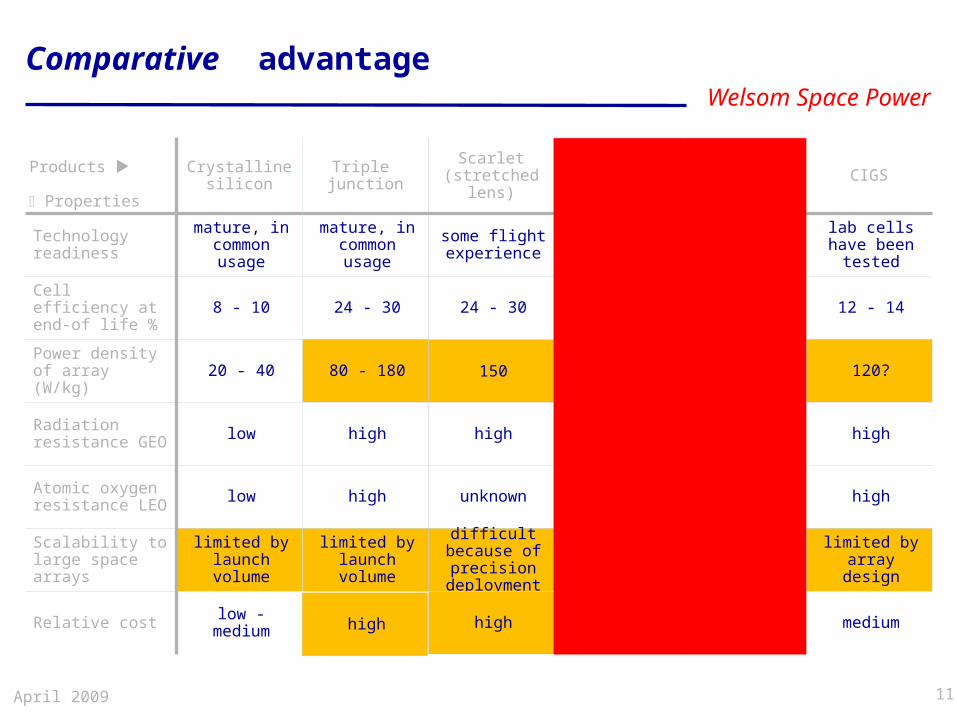

Comparative advantage

Crystallinesilicon

Triple junction

Scarlet (stretched

lens)

LaRC-CP1®a-SI:H

CORINTM

a-Si:H CIGS

Technology readiness

Cell efficiency at end-of life %

Power density of array (W/kg)

Radiation resistance GEO

Atomic oxygen resistance LEO

Scalability to large space arrays

Relative cost

mature, in common

usage

8 - 10

20 - 40

low

low

limited by launch volume

low - medium

24 - 30

80 - 180

high

high

limited by launch volume

high

some flight experience

24 - 30

150

high

unknown

difficult because of precision

deployment

high

flown in ISS, lab cells tested

8 - 9

1'370

superior

low

very easy

very low

manufactured + lab tested for atomic

oxygen

8 - 9

1'370

superior

high

very easy

very low

lab cells have been tested

12 - 14

120?

high

high

limited by array design

medium

mature, in common

usage

Products

Properties

Welsom Space Power

April 2009 12

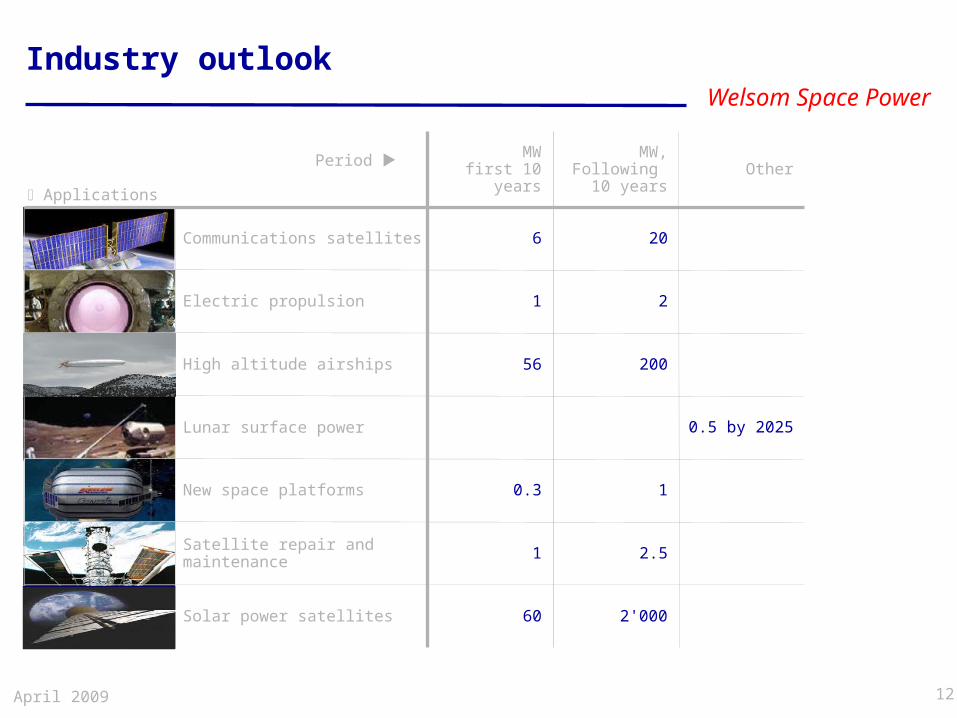

Industry outlook

MWfirst 10 years

Communications satellites

Electric propulsion

High altitude airships

Lunar surface power

New space platforms

Satellite repair and maintenance

Solar power satellites

6

1

56

0.3

1

60

Period

Applications

MW, Following

10 years

20

2

200

1

2.5

2'000

0.5 by 2025

Other

Welsom Space Power

April 2009 13

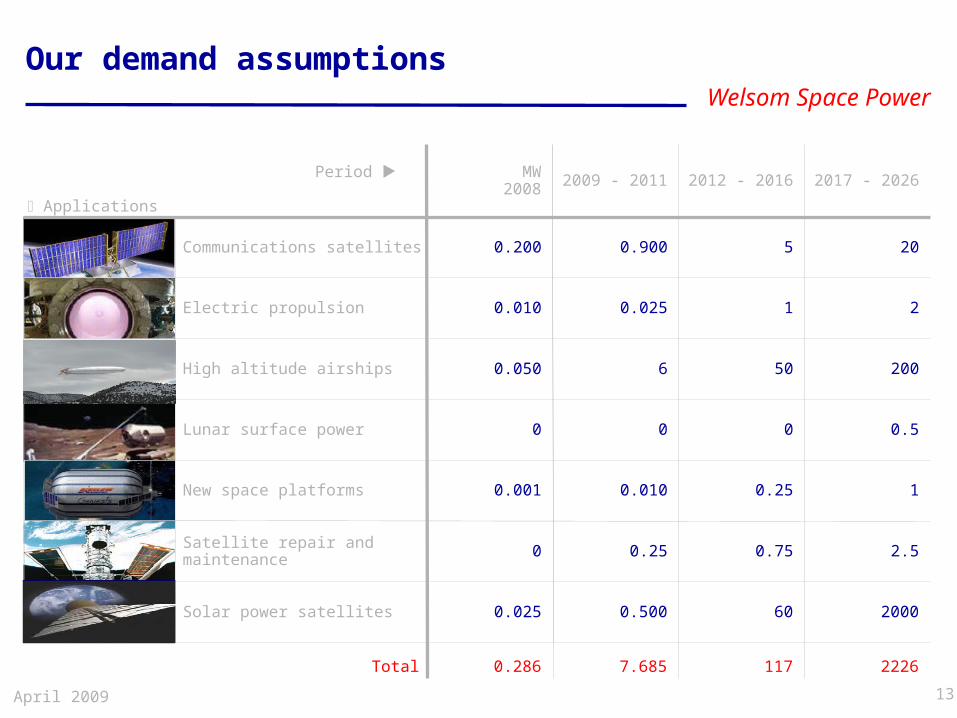

Our demand assumptions

Total 22261170.286 7.685

20

2

200

0.5

1

2.5

2000

5

1

50

0

0.25

0.75

60

2017 - 2026MW2008

Communications satellites

Electric propulsion

High altitude airships

Lunar surface power

New space platforms

Satellite repair and maintenance

Solar power satellites

0.200

0.010

0.050

0

0.001

0

0.025

Period

Applications

2009 - 2011

0.900

0.025

6

0

0.010

0.25

0.500

2012 - 2016

Welsom Space Power

April 2009 14

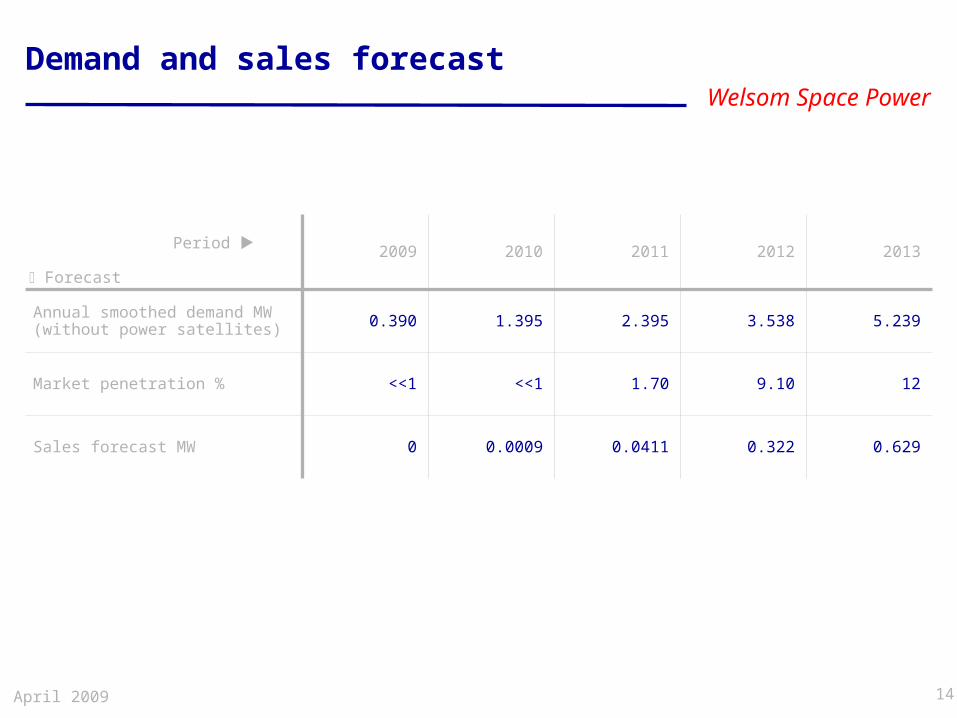

Demand and sales forecast

0.390

<<1

0

2009

5.239

12

0.629

3.538

9.10

0.322

20132010

Annual smoothed demand MW (without power satellites)

Market penetration %

Sales forecast MW

1.395

<<1

0.0009

Period

Forecast

2011

2.395

1.70

0.0411

2012

Welsom Space Power

April 2009 15

Applications

Customers

●Bigelow

Comsats

BoeingDLREADS AstriumESAHiltonHolland America

Lockheed MartinLTAMitsubishiNASANASDAOrbital SciencesScaled CompositesSpaceXSS / LoralStrato-TexThales Alenia SpaceUS Dept.of Defense

Newspace

High altitudeairships

Electric propuls.

Satellite repair

Lunar surface power

Solarpowersats Milsats

Gov. contracts

Kistler

● ● ● ● ● ●●● ● ● ● ●

● ● ●●●

●●●

● ● ● ● ●●●

●●

● ●●

●●

● ● ●●●

● ●●●

Major potential customers

Welsom Space Power

April 2009 16

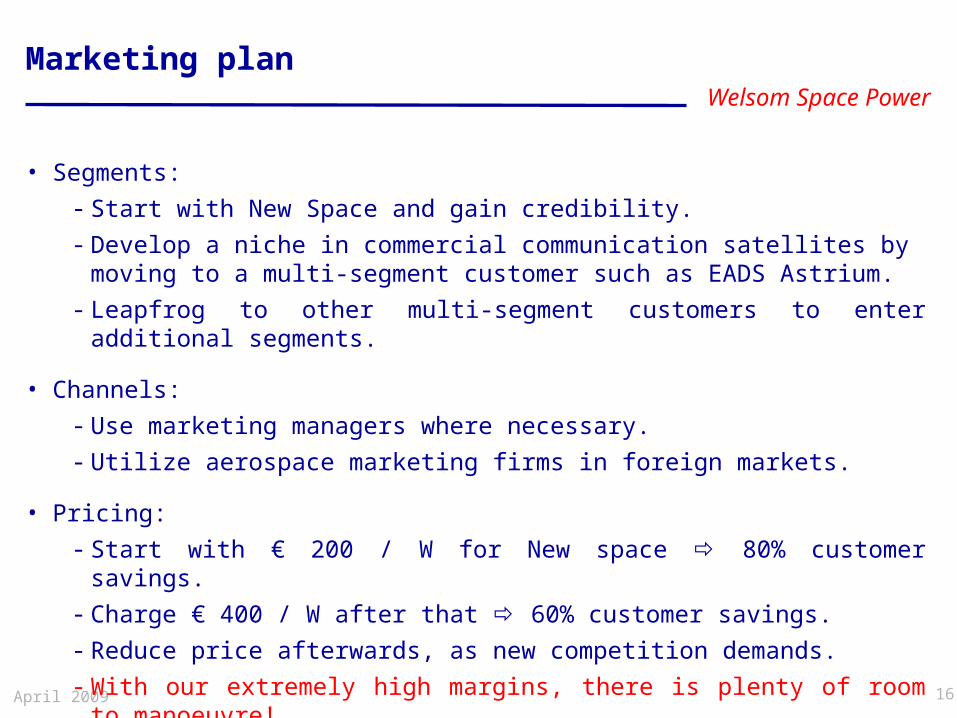

Marketing plan

• Segments:

- Start with New Space and gain credibility.

- Develop a niche in commercial communication satellites by moving to a multi-segment customer such as EADS Astrium.

- Leapfrog to other multi-segment customers to enter additional segments.

• Channels:

- Use marketing managers where necessary.

- Utilize aerospace marketing firms in foreign markets.

• Pricing:

- Start with € 200 / W for New space 80% customer savings.

- Charge € 400 / W after that 60% customer savings.

- Reduce price afterwards, as new competition demands.

- With our extremely high margins, there is plenty of room to manoeuvre!

Welsom Space Power

April 2009 17

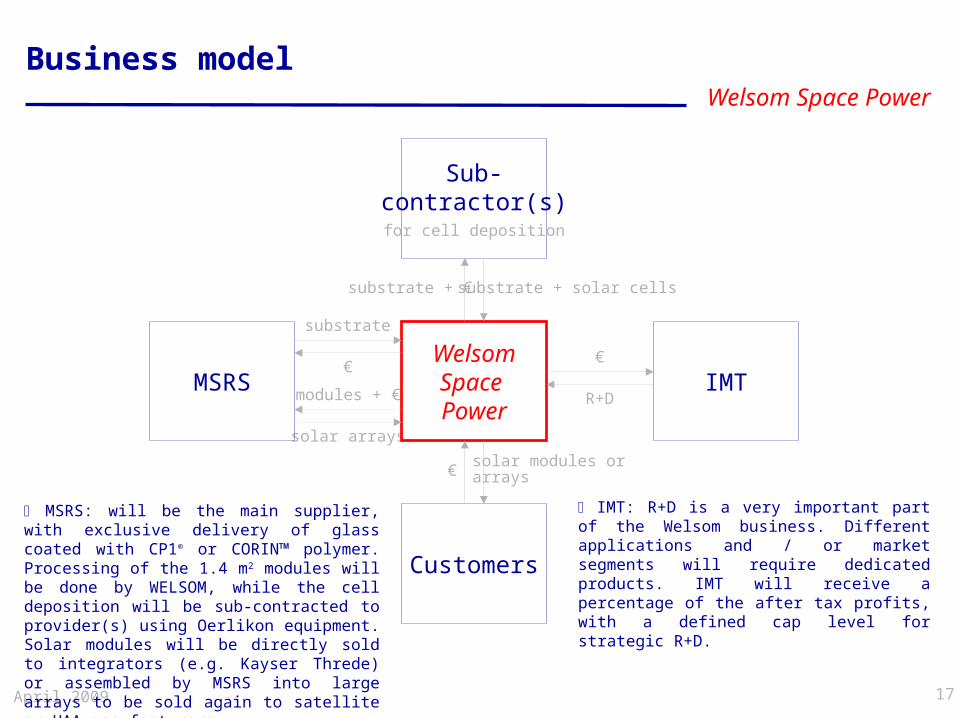

Business model

solar arrays

WelsomSpace Power

MSRS IMT

Customers

Sub-contractor(s)for cell deposition

substrate

€€

R+Dmodules + €

substrate + € substrate + solar cells

€solar modules orarrays

MSRS: will be the main supplier, with exclusive delivery of glass coated with CP1® or CORIN™ polymer. Processing of the 1.4 m2 modules will be done by WELSOM, while the cell deposition will be sub-contracted to provider(s) using Oerlikon equipment. Solar modules will be directly sold to integrators (e.g. Kayser Threde) or assembled by MSRS into large arrays to be sold again to satellite or HAA manufacturers.

IMT: R+D is a very important part of the Welsom business. Different applications and / or market segments will require dedicated products. IMT will receive a percentage of the after tax profits, with a defined cap level for strategic R+D.

Welsom Space Power

April 2009 18

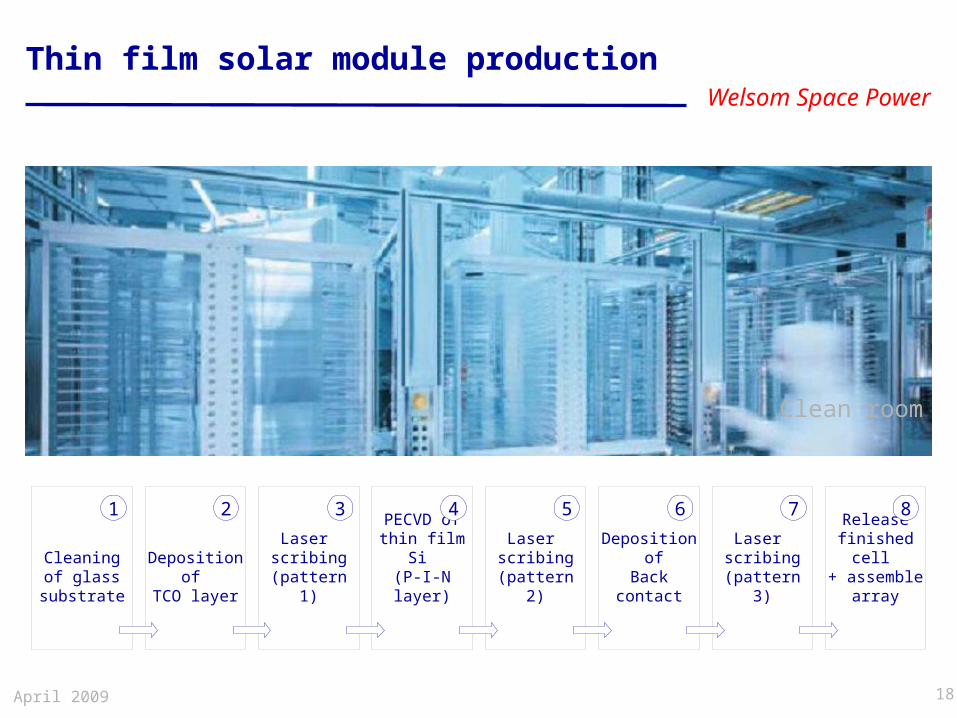

Thin film solar module production

Cleaning of glass

substrate

Deposition of

TCO layer

Laser scribing

(pattern 1)

PECVD of thin film Si (P-I-N layer)

Laser scribing

(pattern 2)

Laser scribing

(pattern 3)

Release finished cell + assemble

array

Deposition of

Back contact

1 2 3 4 5 6 7 8

Clean room

Welsom Space Power

April 2009 19

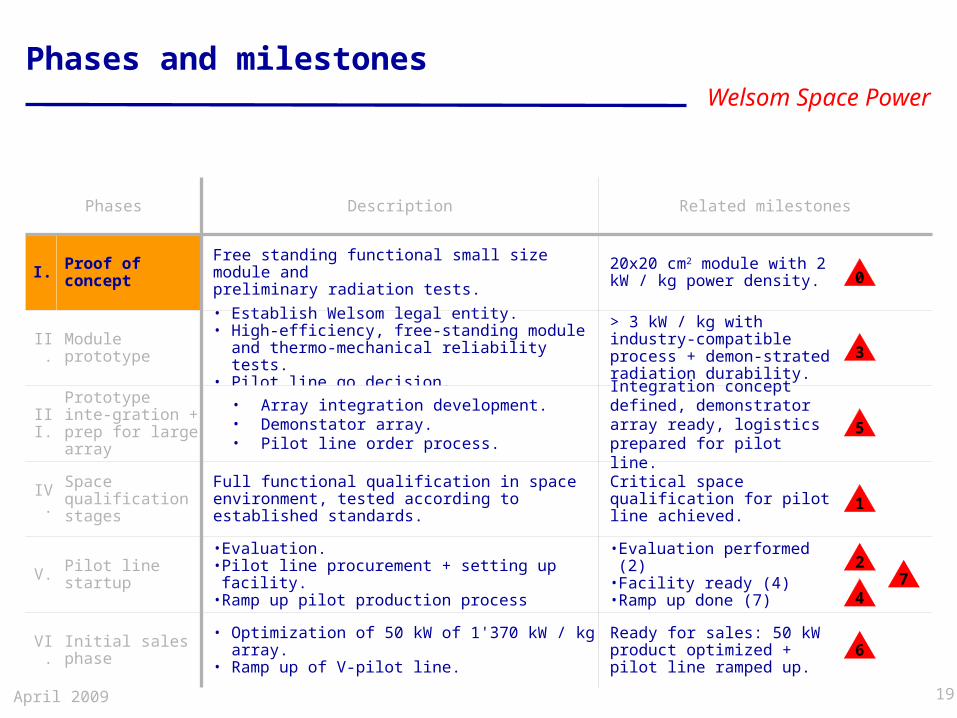

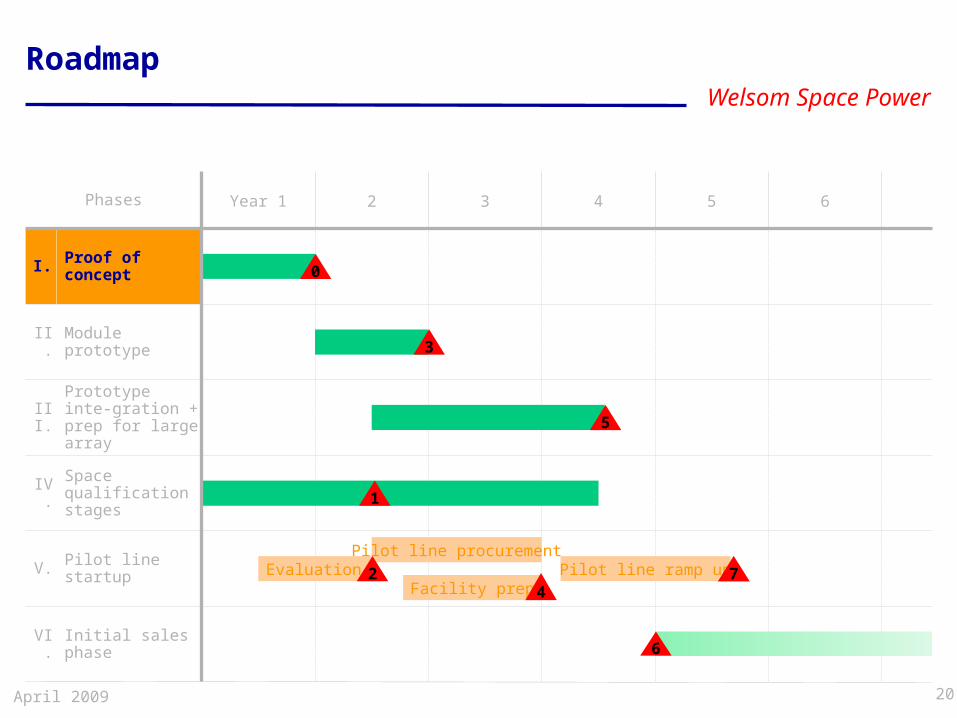

Phases and milestones

0

1

2

3

4

5

6

7

Phases

Proof of concept

Prototype inte-gration + prep for large array

Pilot line startup

Initial sales phase

Module prototype

I.

III.

V.

VI.

II.

Description

Free standing functional small size module and preliminary radiation tests.

•Evaluation.•Pilot line procurement + setting up facility.•Ramp up pilot production process

• Optimization of 50 kW of 1'370 kW / kg array.• Ramp up of V-pilot line.

• Establish Welsom legal entity. • High-efficiency, free-standing module and

thermo-mechanical reliability tests. • Pilot line go decision.

Space qualification stages

IV.

• Array integration development.• Demonstator array. • Pilot line order process.

Full functional qualification in space environment, tested according to established standards.

Related milestones

20x20 cm2 module with 2 kW / kg power density.

> 3 kW / kg with industry-compatible process + demon-strated radiation durability.

•Evaluation performed (2)•Facility ready (4)•Ramp up done (7)

Critical space qualification for pilot line achieved.

Integration concept defined, demonstrator array ready, logistics prepared for pilot line.

Ready for sales: 50 kW product optimized + pilot line ramped up.

Welsom Space Power

April 2009 20

Roadmap

Year 1 2 3 4 5 6Phases

Proof of concept

Prototype inte-gration + prep for large array

Pilot line startup

Initial sales phase

Module prototype

I.

III.

V.

VI.

II.

Space qualification stages

IV.

0

1

3

5

6

EvaluationPilot line procurement

Facility prep2

4Pilot line ramp up 7

Welsom Space Power

April 2009 21

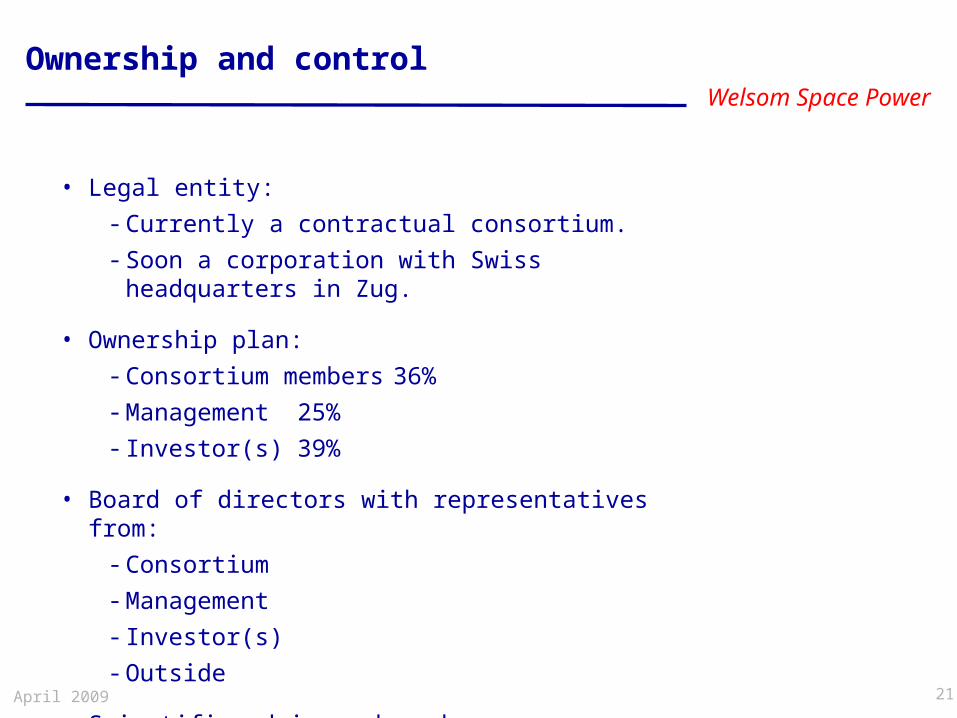

Ownership and control

• Legal entity:

- Currently a contractual consortium.

- Soon a corporation with Swiss headquarters in Zug.

• Ownership plan:

- Consortium members 36%

- Management 25%

- Investor(s) 39%

• Board of directors with representatives from:

- Consortium

- Management

- Investor(s)

- Outside

• Scientific advisory board.

Welsom Space Power

April 2009 22

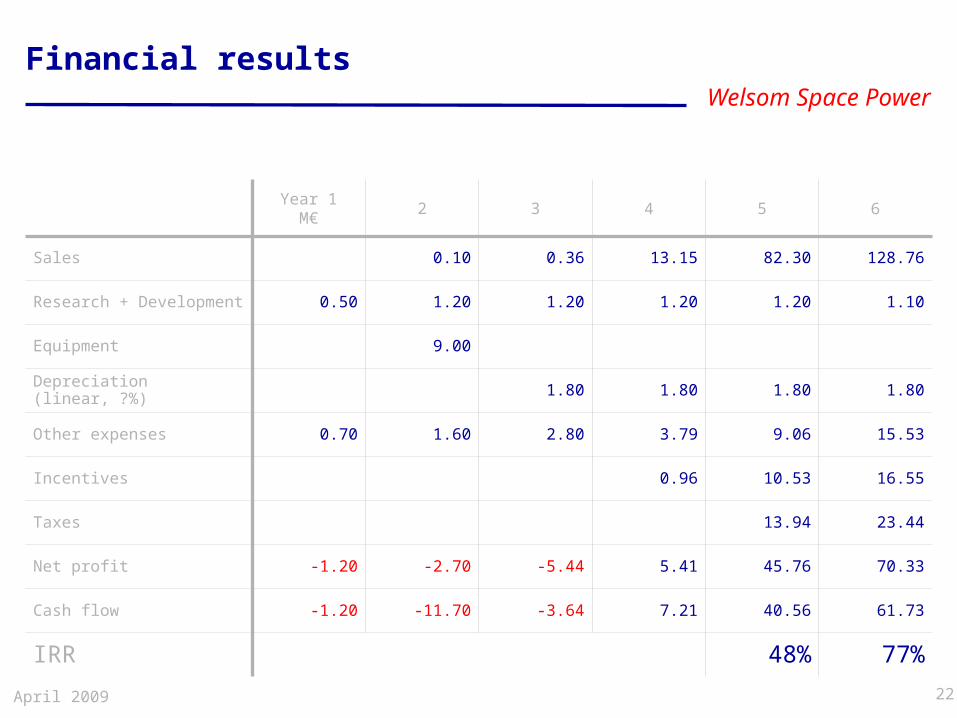

Financial results

77%48%

61.7340.567.21-3.64-11.70-1.20

70.3345.765.41-5.44-2.70-1.20

23.4413.94

16.5510.530.96

15.539.063.792.801.600.70

1.801.801.801.80

9.00

1.101.201.201.201.200.50

128.7682.3013.150.360.10Sales

Research + Development

Equipment

Depreciation (linear, ?%)

Other expenses

Incentives

Taxes

Net profit

Cash flow

IRR

Year 1M€

2 3 4 5 6

Welsom Space Power

April 2009 23

Total capital needs

21.608.509.004.10Total

5.063.861.20

2 - 3

1 - 2

Year and stage

12.642.449.001.20Prototype integration + array large area upscaling preparation

2.701.501.20Module prototype

1.200.700.50Proof of concept

R+DM€ Equipment Working

capital Total

0 - 1

3 - 4 Pilot line startup

Welsom Space Power

April 2009 24

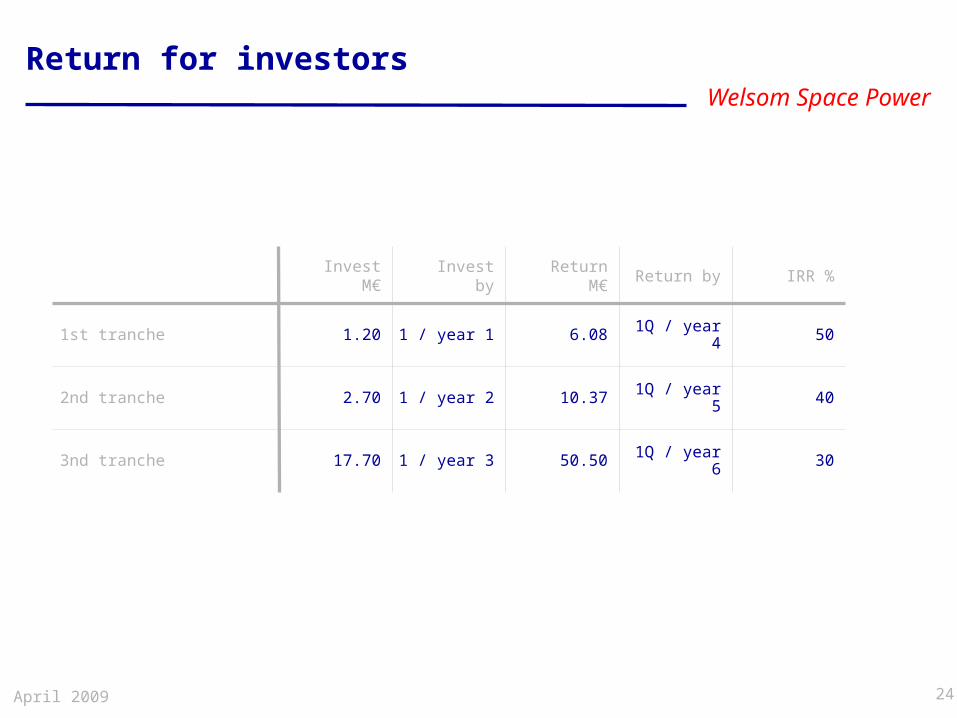

Return for investors

301Q / year 650.501 / year 317.703nd tranche

401Q / year 510.371 / year 22.702nd tranche

501Q / year 46.081 / year 11.201st tranche

InvestM€

Investby

ReturnM€

Return by IRR %

Welsom Space Power

April 2009 25

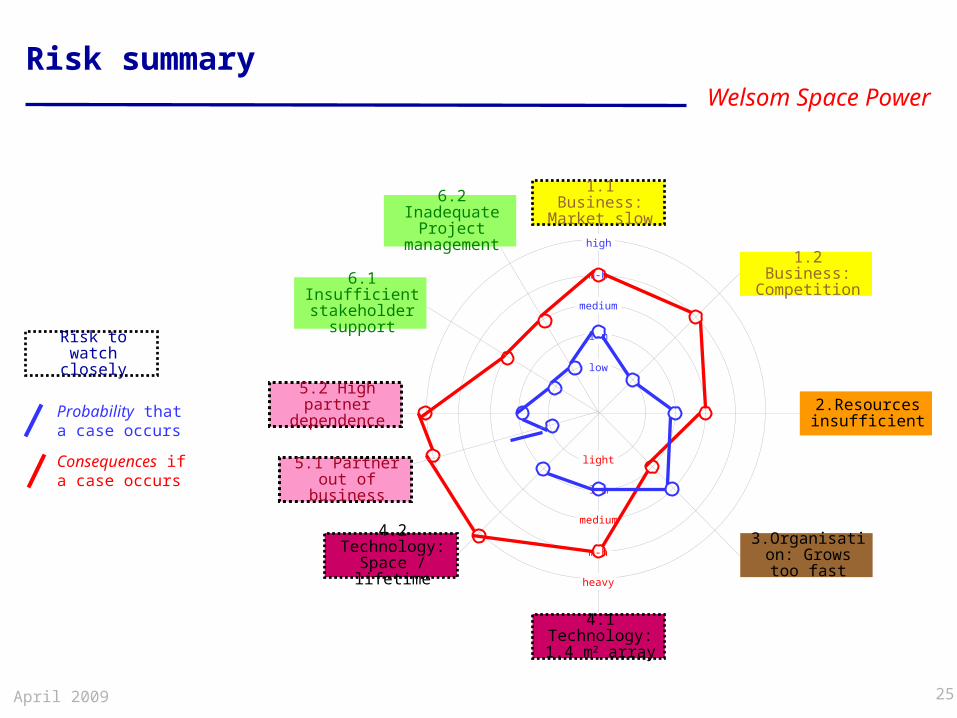

Risk summary

1.1 Business:Market slow

2.Resources insufficient

1.2 Business:Competition

4.1 Technology:1.4 m2 array

3.Organisation: Grows too

fast

4.2 Technology:

Space / lifetime heavy

high

medium

low

light

medium

m-h

l-m

l-m

m-h

Consequences if a case occurs

Probability that a case occurs

Risk to watch closely

5.1 Partner out of business

6.1 Insufficient stakeholder

support

5.2 High partner

dependence

6.2 Inadequate Project

management

Welsom Space Power

April 2009 26

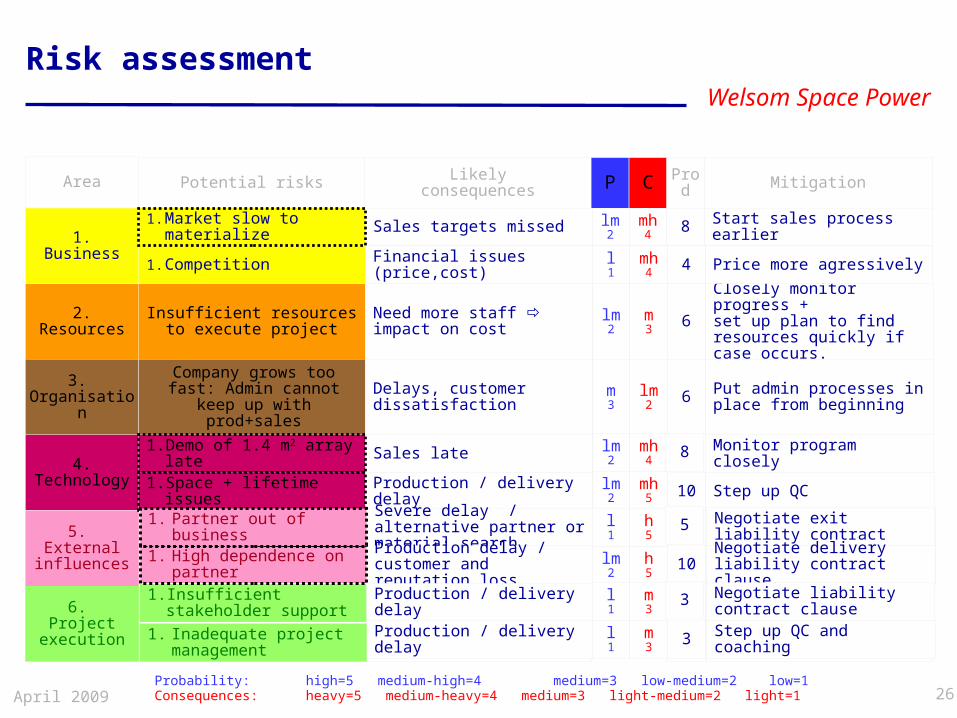

Closely monitor progress +set up plan to find resources quickly if case occurs.

lm2

m3 6Need more staff impact

on cost

Risk assessment

Probability: high=5 medium-high=4 medium=3 low-medium=2 low=1 Consequences: heavy=5 medium-heavy=4 medium=3 light-medium=2 light=1

Insufficient resources to execute project

Potential risksArea

2.Resources

3. Organisation

5. External

influences

6. Project

execution

Likelyconsequences MitigationP C

Start sales process earlierlm2

mh4

Prod

8

1. Competition

Sales targets missed

Financial issues (price,cost) Price more agressivelyl

1mh

4 4

Put admin processes in place from beginning

m3

lm2 6

Company grows too fast: Admin cannot keep up

with prod+sales

lm2

mh5 10

Monitor program closely

Step up QC

lm2

mh4

8Sales late

Production / delivery delay

4.Technology

1.Business

1. Market slow to materialize

1. Demo of 1.4 m2 array late

1. Space + lifetime issues

Delays, customer dissatisfaction

1. Insufficient stakeholder support

Severe delay / alternative partner or material searchProduction delay / customer and reputation lossProduction / delivery delay

Production / delivery delay

lm2

h5

l1

h5

l1

m3

l1

m3

10

5

3

3

Negotiate exit liability contractNegotiate delivery liability contract clauseNegotiate liability contract clause

Step up QC and coaching

1. High dependence on partner

1. Inadequate project management

1. Partner out of business

Welsom Space Power

April 2009 27

Contact

• The detailed Businessplan can be obtained after signing an NDA with the Welsom Consortium

• Please contact:

Mr. Kevin Reed Msc. , CMO SESCRC/ Welsom Space Power

914 N. Fairview Street, Anaheim CA 92801

Tel. +01 (714) 213-6857, Email [email protected]

WELSOM consortium will be leading the discussions with investors

Related Documents