SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO> Page 1 Kim Nguyen [email protected] +84 8 3824 2897 ext. 2140 10 May 2017 INDUSTRIALS – VIETNAM Key figures Market cap (USD mn) 1,826 Market cap (VND bn) 41,459 Outstanding shares (mn) 322.4 52W high/low (VND 1,000) 138.0/108.0 Average 2M volume (share) 366,320 Average 2M value (USD mn) 2.06 Average 2M value (VND bn) 46.68 Foreign ownership (%) 26.12 State ownership (%) 0 Management ownership (%) N.A. Stock performance Source: Bloomberg Company Snapshot VJC is a privately-owned Low Cost Carrier (LCC) airline in Vietnam. It was established on 23rd July 2007, and commenced the first commercial flight on 24th December 2011 with the Ho Chi Minh City - Hanoi route. Total passengers served by VJC reached 14.05 mn pax in 2016 after 4 years of operation. As of 31 Dec 2016, VJC operates a fleet of 41 aircraft, in which 19 aircraft are funded by SLB and 1 aircraft is owned by the company via financial lease. Other aircraft include 15 dry leases and 6 wet leases. VJC achieved a domestic market share of 40.8% as of 31 Dec 2016, an increase from 37.1% as of 31 Dec 2015, according to a report by the Civil Aviation Authority of Vietnam (CAAV) INITIATION REPORT Cost advantage enables competitive pricing Investment case: Thanks to a low fuel input cost, along with declines in other operation costs, VJC has been offering very competitive pricing to passengers in order to tap into Vietnam‟s underserved low cost airline market in recent years. Nevertheless, in line with the global airline industry outlook, VJC‟s core earnings growth appeared to peak in 2016, with previous record high growth rates being challenging to replicate. The peak stemmed from such advantages as a low fuel cost environment, declining ex-fuel Cost Available Seat Kilometers (ex-fuel CASKs), and high passenger volume growing from a low base. Catalysts: Domestic market will rise in 2017-2019 and then experience a slowdown. VJC‟s positive passenger growth mainly comes from seizing market share from its competitors and passengers from other traditional transportation methods. However, the domestic market may gradually saturate in the next 2-3 years when total capacity increases along with expected new players such as Vietstar Airlines and AirAsia, which will push VJC to expand internationally in a more aggressive fashion. Strong capacity expansion in international routes. From 2017, VJC will aggressively open new international routes within a radius of 2,500 nautical miles, with average flight duration of roughly 5-6 hours to destinations such as Korea and Japan. Its strategic markets will be ASEAN and Northeast Asia including Taiwan, Hong Kong, Mainland China, Korea, and Japan. Passenger yields may continue to remain low in order to gain market share. We expect VJC‟s international yield to remain low in 2017 as the initial phase of its aggressive expansion begins. To counteract such low yield figures, VJC aims to aggressively expand to longer international flights, along with targeting a higher income class. Yields are expected to slightly improve from 2018 onwards, corresponding with increasing fuel prices and a stable flight route network. A fuel cost uptrend is the largest risk, but hedging might partly render the risk subdued. Amid the expected pick-up of jet fuel prices in 2017, VJC plans to hedge 30%-35% of the total fuel cost. At the same time, the company will receive a delivery of the A320 NEO aircraft model, the most fuel efficient model in its holdings, which will partly reduce the impact of a fuel price surge. Valuation: Combining the DCF method and the 1 year target P/E of 13x, and adjusted EV/EBITDAR of 7x (premium compared with industry average, attributable to VJC‟s duopoly positioning in the Vietnamese LCC segment and high growth in the initial phase of operation), we arrive at a 1 year target for VJC of VND 140,400/ share (+8%). We recommend to HOLD the stock. Risks: (1) fuel price uptrend; (2) increase in domestic airport fees; (3) overcapacity due to significant capacity expansion; (4) volatility of sales and lease back earnings (5) Financial risk and FX risk HOLD - 1Y Target Price: VND 140,400 Current price: VND 130,500 VietJet Aviation Joint Stock Company (VJC: HOSE)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 1

Kim Nguyen

+84 8 3824 2897 ext. 2140

10 May 2017

INDUSTRIALS – VIETNAM

Key figures

Market cap (USD mn) 1,826

Market cap (VND bn) 41,459

Outstanding shares (mn) 322.4

52W high/low (VND 1,000) 138.0/108.0

Average 2M volume (share) 366,320

Average 2M value (USD mn) 2.06

Average 2M value (VND bn) 46.68

Foreign ownership (%) 26.12

State ownership (%) 0

Management ownership (%) N.A.

Stock performance

Source: Bloomberg

Company Snapshot

VJC is a privately-owned Low Cost Carrier (LCC)

airline in Vietnam. It was established on 23rd July

2007, and commenced the first commercial flight

on 24th December 2011 with the Ho Chi Minh

City - Hanoi route. Total passengers served by

VJC reached 14.05 mn pax in 2016 after 4 years

of operation. As of 31 Dec 2016, VJC operates a

fleet of 41 aircraft, in which 19 aircraft are funded

by SLB and 1 aircraft is owned by the company

via financial lease. Other aircraft include 15 dry

leases and 6 wet leases.

VJC achieved a domestic market share of 40.8%

as of 31 Dec 2016, an increase from 37.1% as of

31 Dec 2015, according to a report by the Civil

Aviation Authority of Vietnam (CAAV)

INITIATION REPORT

Cost advantage enables competitive pricing

Investment case: Thanks to a low fuel input cost, along with declines in other operation

costs, VJC has been offering very competitive pricing to passengers in order to tap into

Vietnam‟s underserved low cost airline market in recent years. Nevertheless, in line with

the global airline industry outlook, VJC‟s core earnings growth appeared to peak in 2016,

with previous record high growth rates being challenging to replicate. The peak stemmed

from such advantages as a low fuel cost environment, declining ex-fuel Cost Available

Seat Kilometers (ex-fuel CASKs), and high passenger volume growing from a low base.

Catalysts:

Domestic market will rise in 2017-2019 and then experience a slowdown. VJC‟s

positive passenger growth mainly comes from seizing market share from its

competitors and passengers from other traditional transportation methods. However,

the domestic market may gradually saturate in the next 2-3 years when total capacity

increases along with expected new players such as Vietstar Airlines and AirAsia,

which will push VJC to expand internationally in a more aggressive fashion.

Strong capacity expansion in international routes. From 2017, VJC will

aggressively open new international routes within a radius of 2,500 nautical miles,

with average flight duration of roughly 5-6 hours to destinations such as Korea and

Japan. Its strategic markets will be ASEAN and Northeast Asia including Taiwan,

Hong Kong, Mainland China, Korea, and Japan.

Passenger yields may continue to remain low in order to gain market share.

We expect VJC‟s international yield to remain low in 2017 as the initial phase of its

aggressive expansion begins. To counteract such low yield figures, VJC aims to

aggressively expand to longer international flights, along with targeting a higher

income class. Yields are expected to slightly improve from 2018 onwards,

corresponding with increasing fuel prices and a stable flight route network.

A fuel cost uptrend is the largest risk, but hedging might partly render the risk

subdued. Amid the expected pick-up of jet fuel prices in 2017, VJC plans to hedge

30%-35% of the total fuel cost. At the same time, the company will receive a delivery

of the A320 NEO aircraft model, the most fuel efficient model in its holdings, which

will partly reduce the impact of a fuel price surge.

Valuation: Combining the DCF method and the 1 year target P/E of 13x, and adjusted

EV/EBITDAR of 7x (premium compared with industry average, attributable to VJC‟s

duopoly positioning in the Vietnamese LCC segment and high growth in the initial phase

of operation), we arrive at a 1 year target for VJC of VND 140,400/ share (+8%). We

recommend to HOLD the stock.

Risks: (1) fuel price uptrend; (2) increase in domestic airport fees; (3) overcapacity due

to significant capacity expansion; (4) volatility of sales and lease back earnings (5)

Financial risk and FX risk

HOLD - 1Y Target Price: VND 140,400 Current price: VND 130,500

VietJet Aviation Joint Stock Company (VJC: HOSE)

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 2

Table of Contents

1. BACKGROUND INFORMATION ON VJC .............................................................................................................................................. 3

1.1. Company profile........................................................................................................................................................... 3

1.2. VJC’s milestones .......................................................................................................................................................... 3

1.3. Sales and lease back business model adoption ....................................................................................................... 4

1.4. Company structure ...................................................................................................................................................... 4

1.5. Charter capital increase ............................................................................................................................................... 5

1.6. Shareholders’ Structure .............................................................................................................................................. 5

1.7. Fleets and expansion plans ........................................................................................................................................ 6

1.8. Network structure ......................................................................................................................................................... 7

2. HISTORICAL PERFORMANCE .............................................................................................................................................................. 8

2.1. Financial: impressive growths and margins ............................................................................................................. 8

2.2. Operation: Strong cost-focus advantage but low yields ....................................................................................... 11

3. INDUSTRY OVERVIEW ........................................................................................................................................................................ 13

3.1. Global Airlines Industry ............................................................................................................................................ 13

3.2. Vietnam Aviation Industry ........................................................................................................................................ 15

3.3. VJC’s growth Outlook ............................................................................................................................................... 18

4. EARNINGS ESTIMATES....................................................................................................................................................................... 21

4.1. 2017-2019 business plans ......................................................................................................................................... 21

4.2. 2017 estimates ........................................................................................................................................................... 21

4.3. 2018-2023 estimates .................................................................................................................................................. 22

5. VALUATION .......................................................................................................................................................................................... 23

5.1. DCF method ................................................................................................................................................................ 23

5.2. Peers comparison ...................................................................................................................................................... 23

5.3. Investment view and recommendation.................................................................................................................... 24

5.4. Risks and issues ........................................................................................................................................................ 24

APPENDIX: ANNUAL FINANCIAL STATEMENTS ..................................................................................................................................... 25

ANALYST CERTIFICATION......................................................................................................................................................................... 26

RATING ........................................................................................................................................................................................................ 26

DISCLAIMER ................................................................................................................................................................................................ 26

CONTACT INFORMATION .......................................................................................................................................................................... 27

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 3

1. BACKGROUND INFORMATION ON VJC

1.1. Company profile

VJC is one of two low cost carriers (LCCs) and the only private-owned carrier in Vietnam. The

company was established on 23rd July 2007, and commenced the first commercial flight on 24th

December 2011 with the Ho Chi Minh City - Hanoi route. Total passengers served by VJC

reached 14.05 mn pax in 2016 after 4 years of operation, representing a CAGR of 64.51% since

2013.

As of 31 Dec 2016, VJC operates a fleet of 41 aircraft, in which 19 aircraft are funded by SLB

and 1 aircraft is owned by the company via financial lease. Other aircraft include 15 dry leases

and 6 wet leases. The airline owns an intensive network, with 37 domestic routes and 23

international routes.

VJC achieved a domestic market share of 40.8% in 2016, an increase from 37.1% in 2015, with

the metric based on total passengers boarding domestically via Vietnam-based airlines,

according to Civil Aviation Authority of Vietnam (CAAV)‟s report.

1.2. VJC’s milestones

2007: Founded as Vietnam‟s first privately-owned airline

2011: Commenced the first commercial flight from HCMC to Hanoi on Christmas Day 2011

2012: Fleet grew to 5 aircraft operating across 10 domestic routes

2013: Launched first international flight from HCMC to Bangkok, Thailand

2014: Opened new operating hub in Danang City and signed a purchasing contract for 100

aircraft from Airbus, bringing a total of 19 aircraft in VJC's fleet, with the rest to be delivered at a

later date. Passenger volume accounted for a 29.6% share of domestic air transportation.

2016: Signed a purchase contract with Boeing for 100 B737 MAX 200 aircraft in May 2016, and

another contract with Airbus for 20 A320 CEO and NEO aircraft in September 2016. VJC

officially became an IATA member in August 2016

2017: Listing on HOSE on 28th Feb 2017, officially became the International Air Transport

Association (IATA) full member on 18th Feb 2017

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 4

1.3. Sales and lease back business model adoption

VJC pursues the sale and leaseback model, which is rather popular among global LCCs such

as Indigo, Virgin Australia, Lion Air, SpiceJet, and Norwegian. It purchases new aircraft in large

orders at steep discounts in order to sell the units to leasing companies at more favorable prices

and then in turn leases those aircraft back. Leasing fees and term commitments are fixed over

the leasing period of 6-12 years and non-cancellable. Gains recognized from these transactions

accounted for 40-60% of VJC‟s PBT in 2015 and 2016. In the coming year, the gains will be

dependent upon a timely aircraft delivery schedule. VJC‟s reputable lessors or lease managers

include GE Capital Aviation Services, AWAS Aviation Capital, CIT Aerospace International,

Celestial Aviation Trading 43 Limited, ACG Aircraft Leasing Ireland Limited and ALAFCO

Aviation Lease and Finance Company.

Thanks to SLB model, VJC can benefit from: (1) It does not require a significant upfront CAPEX

in order to fund the fleet; (2) Gains from SLB are used to fund owned aircraft and deposit for

future aircraft deliveries; (3) Keep young fleet which helps save operation cost, including the

heavy D-check. However, when it comes to a fall in travel demand, the airline will face

overcapacity and leads to significant drop in load factors. In that case, the airline can partly

lease them out or arrange for early return of aircraft with certain penalty payments.

The nationally-owned Vietnam Airlines (HVN: UPCOM) currently owns a fleet of more than 90

aircraft. HVN‟s model requires a significant amount of upfront cash raised via borrowing in order

to finance the fleet (its D/E was 3.5x as of 2016 vs. VJC‟s D/E ratio of 1.44x during the same

period). HVN‟s CAPEX used to be mainly funded from the State Budget or through Government

guaranteed foreign debts. As such, HVN has to incur abundant interest expenses, depreciation,

and FX risks for USD denominated debt, which may potentially impact the company‟s earnings

performance. However, in 2017 HVN also plans to receive 4 aircraft via SLB in order to reduce

debt financing.

1.4. Company structure

VJC has 5 subsidiaries. It has 4 100%-owned subsidiaries which are primarily involved in SLB

activities in Singapore, Ireland and British Virgin Island. SLB activities are conducted via these

companies. VietJet Air Cargo JVC, a cargo handling company with a charter capital of VND

10bn, is VJC's remaining subsidiary with 90% ownership.

VJC’s subsidiaries

Subsidiaries Business Date of operation Ownership

VietJet Air Cargo JVC (Vietnam) Cargo 27-Aug-14 90%

VietJet Air IVB No.I Limited (British Virgin Islands) Aircraft business 27-May-14 100%

VietJet Air IVB No.II Limited (British Virgin Islands) Aircraft business 27-May-14 100%

VietJet Air Singapore Pte. Ltd (Singapore) Aircraft business 27-Mar-14 100%

VietJet Air Ireland No.I Limited (Ireland) Aircraft business 3-Jun-16 100%

Source: VJC

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 5

Affiliate: VJC owns 9% in Thai VietJet Air JSC Ltd, founded in November 2014. Thai Vietjet

operates 2 international routes between Bangkok-HCMC and Bangkok-Hanoi, as well as other

international charter flights. As of 2016, VJC has subleased 1 aircraft to Thai VietJet. In the

future, VJC plans to reassign, sell, or lease of a portion of the delivered aircraft from Airbus and

Boeing in the aforementioned contracts to Thai VietJet.

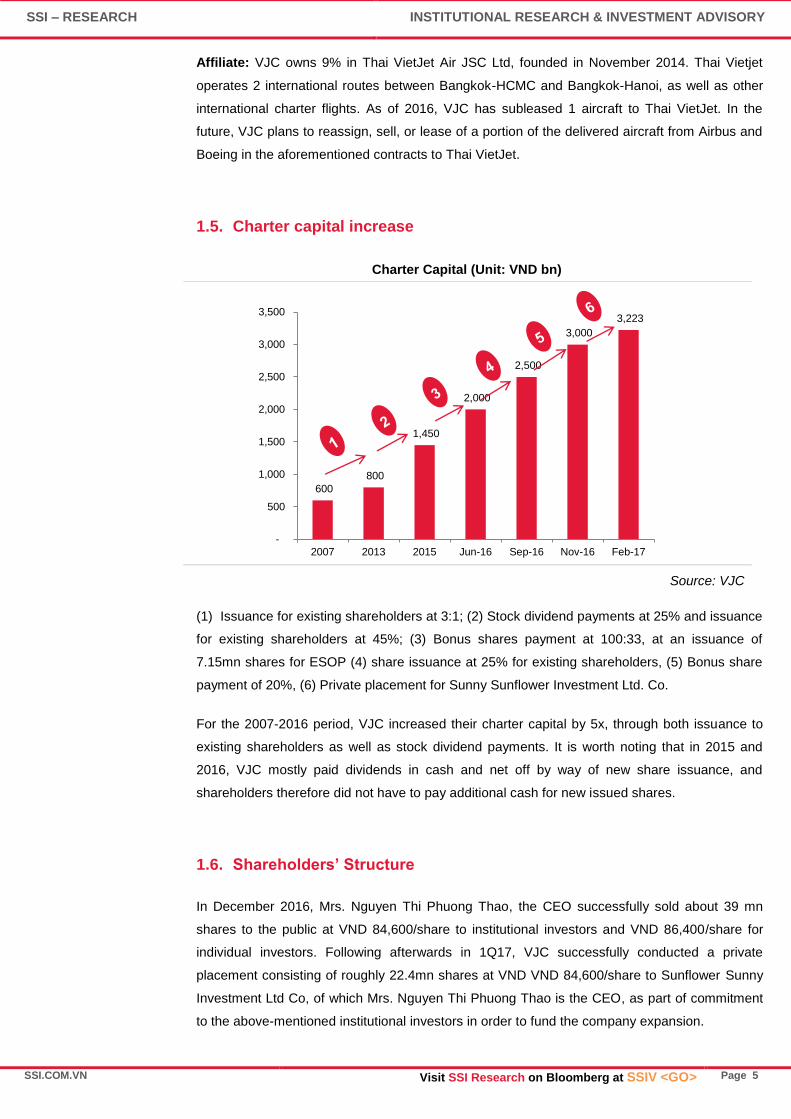

1.5. Charter capital increase

Charter Capital (Unit: VND bn)

Source: VJC

(1) Issuance for existing shareholders at 3:1; (2) Stock dividend payments at 25% and issuance

for existing shareholders at 45%; (3) Bonus shares payment at 100:33, at an issuance of

7.15mn shares for ESOP (4) share issuance at 25% for existing shareholders, (5) Bonus share

payment of 20%, (6) Private placement for Sunny Sunflower Investment Ltd. Co.

For the 2007-2016 period, VJC increased their charter capital by 5x, through both issuance to

existing shareholders as well as stock dividend payments. It is worth noting that in 2015 and

2016, VJC mostly paid dividends in cash and net off by way of new share issuance, and

shareholders therefore did not have to pay additional cash for new issued shares.

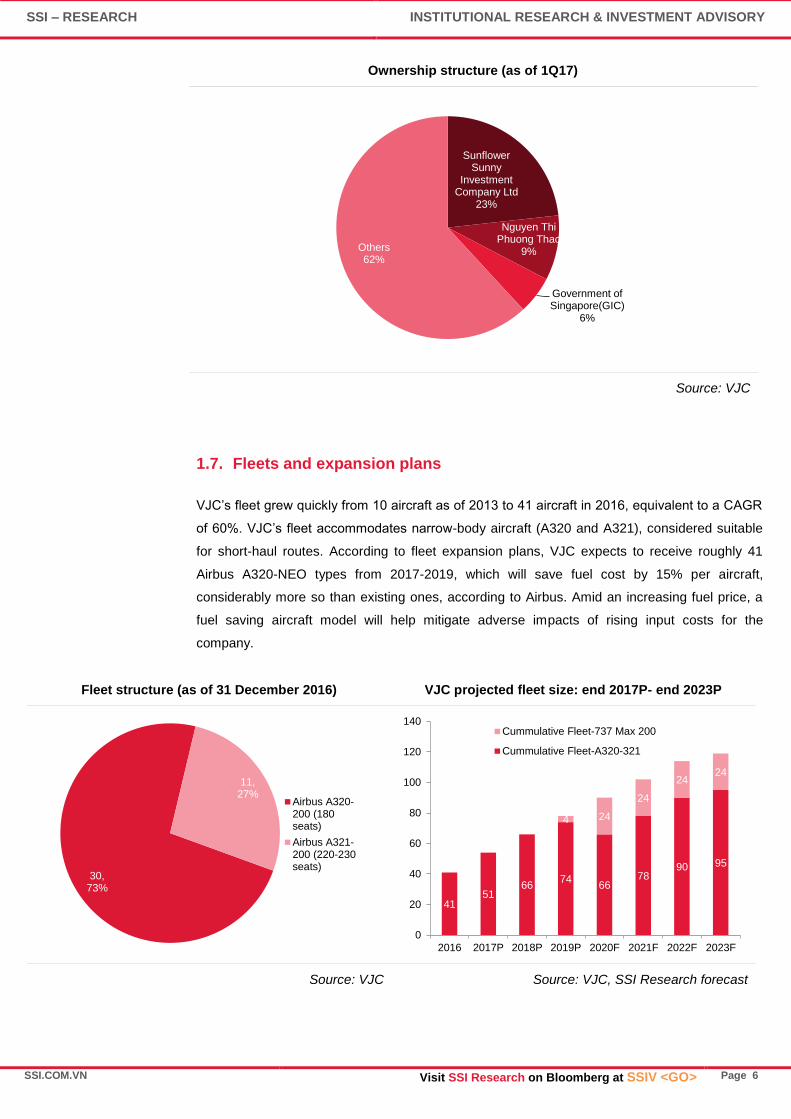

1.6. Shareholders’ Structure

In December 2016, Mrs. Nguyen Thi Phuong Thao, the CEO successfully sold about 39 mn

shares to the public at VND 84,600/share to institutional investors and VND 86,400/share for

individual investors. Following afterwards in 1Q17, VJC successfully conducted a private

placement consisting of roughly 22.4mn shares at VND VND 84,600/share to Sunflower Sunny

Investment Ltd Co, of which Mrs. Nguyen Thi Phuong Thao is the CEO, as part of commitment

to the above-mentioned institutional investors in order to fund the company expansion.

600

800

1,450

2,000

2,500

3,000

3,223

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2013 2015 Jun-16 Sep-16 Nov-16 Feb-17

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 6

Ownership structure (as of 1Q17)

Source: VJC

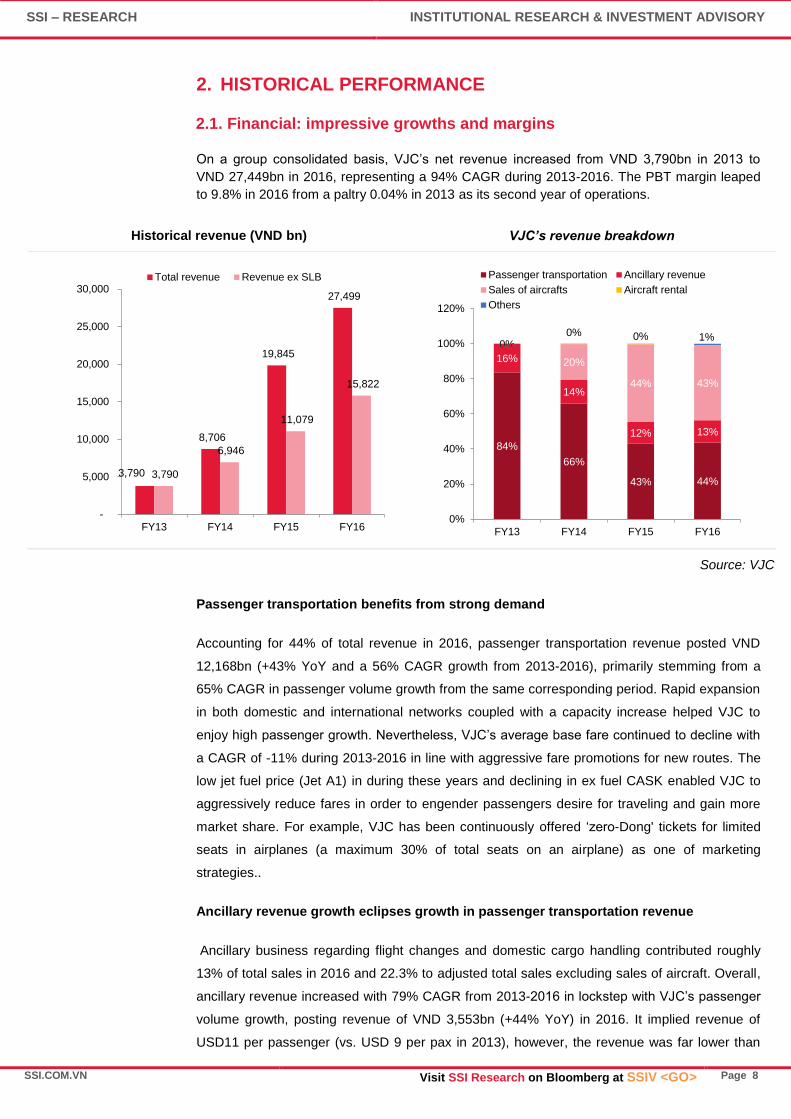

1.7. Fleets and expansion plans

VJC‟s fleet grew quickly from 10 aircraft as of 2013 to 41 aircraft in 2016, equivalent to a CAGR

of 60%. VJC‟s fleet accommodates narrow-body aircraft (A320 and A321), considered suitable

for short-haul routes. According to fleet expansion plans, VJC expects to receive roughly 41

Airbus A320-NEO types from 2017-2019, which will save fuel cost by 15% per aircraft,

considerably more so than existing ones, according to Airbus. Amid an increasing fuel price, a

fuel saving aircraft model will help mitigate adverse impacts of rising input costs for the

company.

Fleet structure (as of 31 December 2016) VJC projected fleet size: end 2017P- end 2023P

Source: VJC Source: VJC, SSI Research forecast

Sunflower Sunny

Investment Company Ltd

23%

Nguyen Thi Phuong Thao

9%

Government of Singapore(GIC)

6%

Others 62%

30, 73%

11, 27%

Airbus A320-200 (180seats)

Airbus A321-200 (220-230seats)

41 51

66 74

66 78

90 95

4 24

24

24 24

0

20

40

60

80

100

120

140

2016 2017P 2018P 2019P 2020F 2021F 2022F 2023F

Cummulative Fleet-737 Max 200

Cummulative Fleet-A320-321

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 7

1.8. Network structure

Within only 5 years of operation, VJC aggressively expanded from 1 route (Hanoi-HCMC) in

2011 to 37 domestic routes and 23 international routes as of 31 December 2016.

VJC's network structure by number of routes International flight frequency

Source: VJC

Intensive domestic network: The Company has established extensive domestic passenger

routes, connecting to 22 airports in Vietnam. The routes originating from Ho Chi Minh City,

Hanoi, Danang, Cam Ranh and Haiphong account for 92% of VJC‟s total domestic routes, and

imply roughly 76% of total Available Seat Kilometer (ASK) from domestic routes. In order to

capture the upcoming growth of the domestic air travel segment, VJC aims to increase flight

frequencies in these 5 operating hubs.

China and North Asia Countries is VJC’s largest international market. As VJC initially

focused on the domestic market, their international network has appeared small in the past few

years, accounting for only 38% of the total amount of routes. VJC increased from 2 international

routes in 2012 to 23 routes as of 2016 (excluding charter flights). Among those, routes

connecting Vietnam to Greater China-Hongkong, Taiwan, Korea and ASEAN countries play as

VJC‟s strategic ones, accounting for 38%, 15%, 19% and 28% of total international flights per

week respectively.

Domestic 62%

ASEAN 8%

China-Hongkong

20%

Taiwan 3%

Korea 7%

ASEAN 28%

China-Hongkong

38%

Taiwan 15%

Korea 19%

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 8

2. HISTORICAL PERFORMANCE

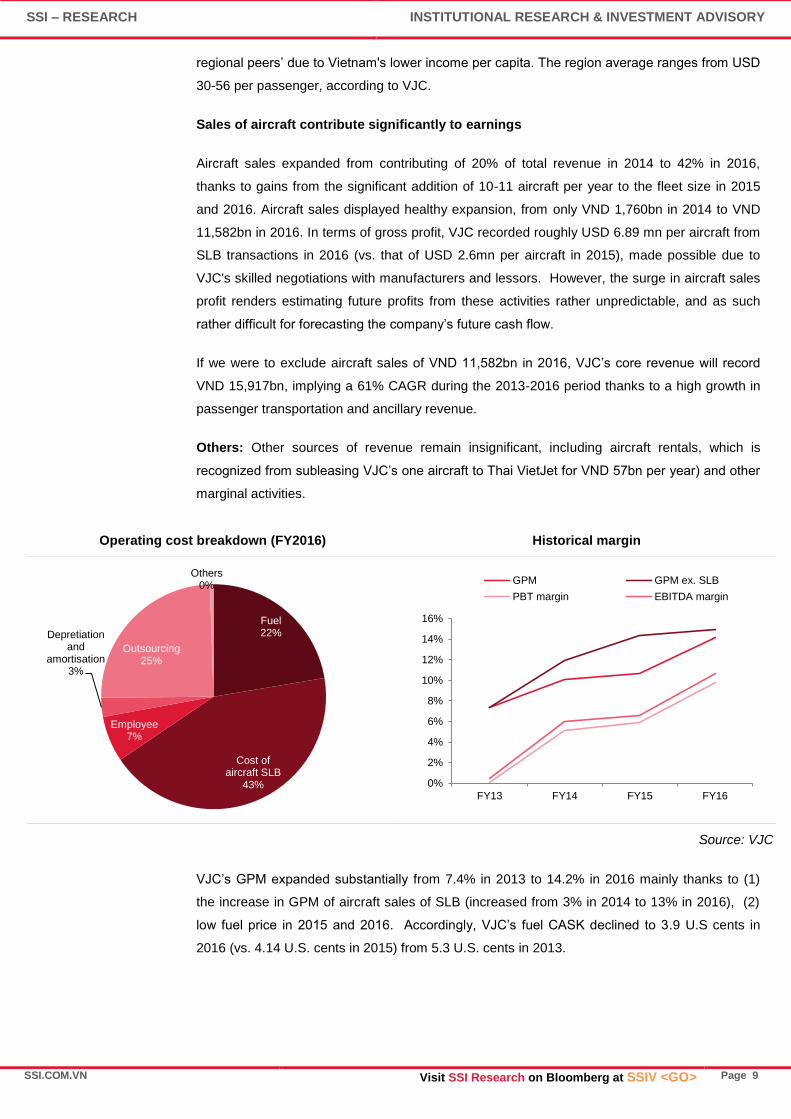

2.1. Financial: impressive growths and margins

On a group consolidated basis, VJC‟s net revenue increased from VND 3,790bn in 2013 to

VND 27,449bn in 2016, representing a 94% CAGR during 2013-2016. The PBT margin leaped

to 9.8% in 2016 from a paltry 0.04% in 2013 as its second year of operations.

Historical revenue (VND bn) VJC’s revenue breakdown

Source: VJC

Passenger transportation benefits from strong demand

Accounting for 44% of total revenue in 2016, passenger transportation revenue posted VND

12,168bn (+43% YoY and a 56% CAGR growth from 2013-2016), primarily stemming from a

65% CAGR in passenger volume growth from the same corresponding period. Rapid expansion

in both domestic and international networks coupled with a capacity increase helped VJC to

enjoy high passenger growth. Nevertheless, VJC‟s average base fare continued to decline with

a CAGR of -11% during 2013-2016 in line with aggressive fare promotions for new routes. The

low jet fuel price (Jet A1) in during these years and declining in ex fuel CASK enabled VJC to

aggressively reduce fares in order to engender passengers desire for traveling and gain more

market share. For example, VJC has been continuously offered „zero-Dong' tickets for limited

seats in airplanes (a maximum 30% of total seats on an airplane) as one of marketing

strategies..

Ancillary revenue growth eclipses growth in passenger transportation revenue

Ancillary business regarding flight changes and domestic cargo handling contributed roughly

13% of total sales in 2016 and 22.3% to adjusted total sales excluding sales of aircraft. Overall,

ancillary revenue increased with 79% CAGR from 2013-2016 in lockstep with VJC‟s passenger

volume growth, posting revenue of VND 3,553bn (+44% YoY) in 2016. It implied revenue of

USD11 per passenger (vs. USD 9 per pax in 2013), however, the revenue was far lower than

3,790

8,706

19,845

27,499

3,790

6,946

11,079

15,822

-

5,000

10,000

15,000

20,000

25,000

30,000

FY13 FY14 FY15 FY16

Total revenue Revenue ex SLB

84%

66%

43% 44%

16%

14%

12% 13%

0%

20%

44% 43%

0% 0% 0% 1%

0%

20%

40%

60%

80%

100%

120%

FY13 FY14 FY15 FY16

Passenger transportation Ancillary revenue

Sales of aircrafts Aircraft rental

Others

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 9

regional peers‟ due to Vietnam's lower income per capita. The region average ranges from USD

30-56 per passenger, according to VJC.

Sales of aircraft contribute significantly to earnings

Aircraft sales expanded from contributing of 20% of total revenue in 2014 to 42% in 2016,

thanks to gains from the significant addition of 10-11 aircraft per year to the fleet size in 2015

and 2016. Aircraft sales displayed healthy expansion, from only VND 1,760bn in 2014 to VND

11,582bn in 2016. In terms of gross profit, VJC recorded roughly USD 6.89 mn per aircraft from

SLB transactions in 2016 (vs. that of USD 2.6mn per aircraft in 2015), made possible due to

VJC's skilled negotiations with manufacturers and lessors. However, the surge in aircraft sales

profit renders estimating future profits from these activities rather unpredictable, and as such

rather difficult for forecasting the company‟s future cash flow.

If we were to exclude aircraft sales of VND 11,582bn in 2016, VJC‟s core revenue will record

VND 15,917bn, implying a 61% CAGR during the 2013-2016 period thanks to a high growth in

passenger transportation and ancillary revenue.

Others: Other sources of revenue remain insignificant, including aircraft rentals, which is

recognized from subleasing VJC‟s one aircraft to Thai VietJet for VND 57bn per year) and other

marginal activities.

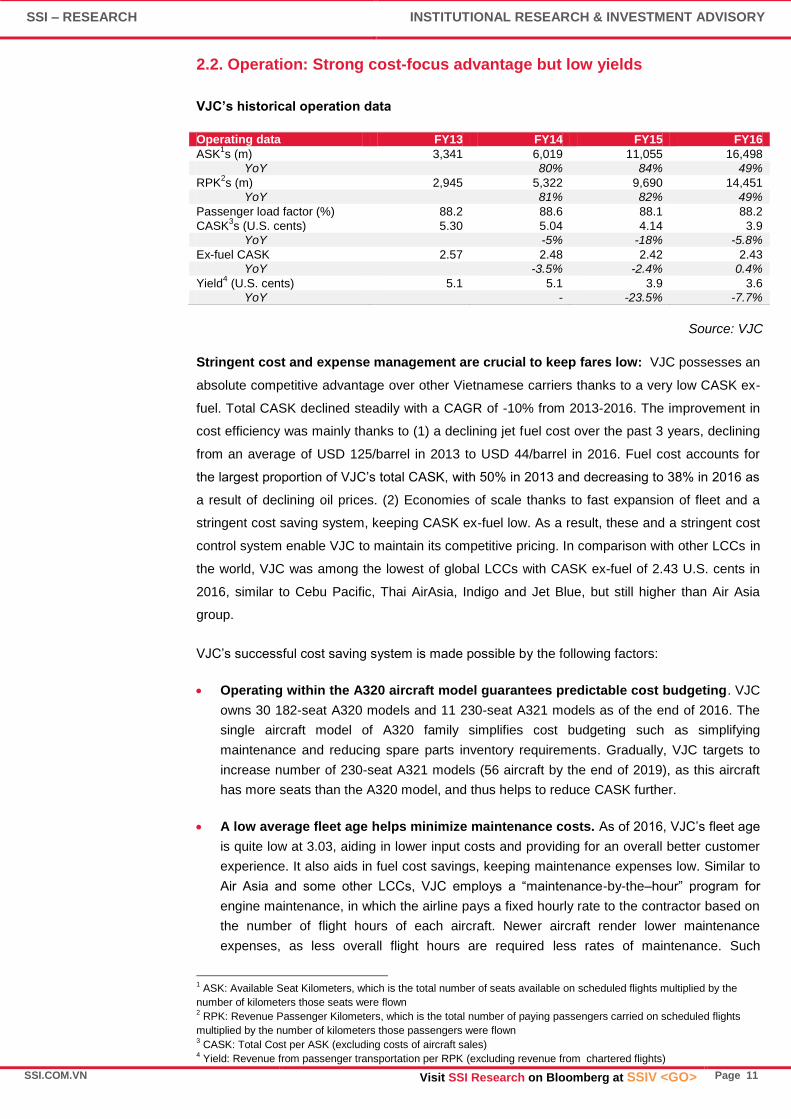

Operating cost breakdown (FY2016) Historical margin

Source: VJC

VJC‟s GPM expanded substantially from 7.4% in 2013 to 14.2% in 2016 mainly thanks to (1)

the increase in GPM of aircraft sales of SLB (increased from 3% in 2014 to 13% in 2016), (2)

low fuel price in 2015 and 2016. Accordingly, VJC‟s fuel CASK declined to 3.9 U.S cents in

2016 (vs. 4.14 U.S. cents in 2015) from 5.3 U.S. cents in 2013.

Fuel 22%

Cost of aircraft SLB

43%

Employee 7%

Depretiation and

amortisation 3%

Outsourcing 25%

Others 0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

FY13 FY14 FY15 FY16

GPM GPM ex. SLB

PBT margin EBITDA margin

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 10

Average Jet fuel and VJC’s GPM ex. SLB from 2013-2016

Source: VJC, IATA

If we were to exclude profit from SLB, VJC‟s GPM would achieve 14.9% in 2016, significantly

expanding from 7.4% in 2013. VJC‟s fuel cost accounts for 22% of COGS (excluding SLB‟s

aircraft cost, fuel should have contributed 39% of COGS in 2016). The global oil price staged a

decline from its yearly peak of roughly USD 112 per barrel in 2012, and began trending

downwards from 2013-2016 at a CAGR of -26% Consequently, jet fuel costs also fell from its

highest level of USD 124.5/barrel in 2012 to USD 52.1/barrel (~ CAGR of -25%) in 2016. The

low oil price in recent years has encouraged LLCs like VJC to reduce air fares and encourage

air travel. Given that the Vietnamese market is highly price sensitive with limited premium

demand, the low oil price environment provides an opportunity for VJC to lower fares and

increase market share.

In line with sales growth and cost reductions, VJC‟s PBT and EBITDA margins improved to

9.8% and 10.7% in 2016 vs 0.04% and 0.5% in 2013. VJC manages to continually maintain a

passenger load at 88% (domestic routes: 89%; international routes: 84%) in recent years. High

passenger loads enable the company to maintain a healthy RASK/CASK spread, which

improved to 0.46 US cents in 2016 from 0.09 U.S cents in 2013 (but slightly declined compared

with 0.59 U.S cents in 2015).

124.5

114.8

66.7

52.1

7.4%

11.9%

14.4% 13.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

20

40

60

80

100

120

140

2013 2014 2015 2016

Jet fuel price (USD/barrel) GPM ex. SLB

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 11

2.2. Operation: Strong cost-focus advantage but low yields

VJC’s historical operation data

Operating data FY13 FY14 FY15 FY16

ASK1s (m) 3,341 6,019 11,055 16,498

YoY 80% 84% 49%

RPK2s (m) 2,945 5,322 9,690 14,451

YoY 81% 82% 49%

Passenger load factor (%) 88.2 88.6 88.1 88.2

CASK3s (U.S. cents) 5.30 5.04 4.14 3.9

YoY -5% -18% -5.8%

Ex-fuel CASK 2.57 2.48 2.42 2.43

YoY -3.5% -2.4% 0.4%

Yield4 (U.S. cents) 5.1 5.1 3.9 3.6

YoY - -23.5% -7.7%

Source: VJC

Stringent cost and expense management are crucial to keep fares low: VJC possesses an

absolute competitive advantage over other Vietnamese carriers thanks to a very low CASK ex-

fuel. Total CASK declined steadily with a CAGR of -10% from 2013-2016. The improvement in

cost efficiency was mainly thanks to (1) a declining jet fuel cost over the past 3 years, declining

from an average of USD 125/barrel in 2013 to USD 44/barrel in 2016. Fuel cost accounts for

the largest proportion of VJC‟s total CASK, with 50% in 2013 and decreasing to 38% in 2016 as

a result of declining oil prices. (2) Economies of scale thanks to fast expansion of fleet and a

stringent cost saving system, keeping CASK ex-fuel low. As a result, these and a stringent cost

control system enable VJC to maintain its competitive pricing. In comparison with other LCCs in

the world, VJC was among the lowest of global LCCs with CASK ex-fuel of 2.43 U.S. cents in

2016, similar to Cebu Pacific, Thai AirAsia, Indigo and Jet Blue, but still higher than Air Asia

group.

VJC‟s successful cost saving system is made possible by the following factors:

Operating within the A320 aircraft model guarantees predictable cost budgeting. VJC

owns 30 182-seat A320 models and 11 230-seat A321 models as of the end of 2016. The

single aircraft model of A320 family simplifies cost budgeting such as simplifying

maintenance and reducing spare parts inventory requirements. Gradually, VJC targets to

increase number of 230-seat A321 models (56 aircraft by the end of 2019), as this aircraft

has more seats than the A320 model, and thus helps to reduce CASK further.

A low average fleet age helps minimize maintenance costs. As of 2016, VJC‟s fleet age

is quite low at 3.03, aiding in lower input costs and providing for an overall better customer

experience. It also aids in fuel cost savings, keeping maintenance expenses low. Similar to

Air Asia and some other LCCs, VJC employs a “maintenance-by-the–hour” program for

engine maintenance, in which the airline pays a fixed hourly rate to the contractor based on

the number of flight hours of each aircraft. Newer aircraft render lower maintenance

expenses, as less overall flight hours are required less rates of maintenance. Such

1 ASK: Available Seat Kilometers, which is the total number of seats available on scheduled flights multiplied by the

number of kilometers those seats were flown 2 RPK: Revenue Passenger Kilometers, which is the total number of paying passengers carried on scheduled flights

multiplied by the number of kilometers those passengers were flown 3 CASK: Total Cost per ASK (excluding costs of aircraft sales)

4 Yield: Revenue from passenger transportation per RPK (excluding revenue from chartered flights)

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 12

maintenance includes daily maintenance, A-checks (every 600 hours of operation), B-

Checks (every 160-180 flight hours), C-Checks (every 6,000 flight hours), and heavy

maintenance D-checks (every 6 years). In addition, this program will also enable budgeting

to be more predictable and simplified. Therefore, VJC keeps retiring old aircraft with more

than 6 year leasing term contracts (including dry leased and wet leased aircraft) and

replacing with new ones in order to maintain a relatively low average fleet age.

Increased block hours drives CASK to decline as aircraft is well utilized. VJC‟s

average aircraft utilization rate improved on a yearly basis, from 11.9, 12.4, and 13.3 block

hours per day in 2013, 2014 and 2015 respectively. 2016 maintained 13.1 block hours of

last year. The airline targets to maintain high block hours per day in the near future by

increasing the frequency of night flights for domestic routes as well as number of

international flights. VJC‟s block hours per day is the highest among global LCCs (vs. block

hours per day of Air Asia: 12.4, Indigo: 11.4, Easy Jet: 11.1, Ryan Air: 9). Hence, it helps

the company to maintain a competitive CASK amid aggressive capacity expansion.

Low sales and marketing costs via the internet and mobile application bookings. VJC

focuses on developing their internet distribution channel through their website and mobile

platform. 23% of ticket sales were conducted through website and the mobile application in

2016. It helped VJC significantly reduce distribution costs in comparison with traditional

channels such as booking agencies, booking offices and others. However, all of these

agencies and booking offices ultimately direct customer orders to either the website or the

mobile application to book ticket. Therefore, to eliminate redundancy, VJC distributes their

tickets via online channel more than 90% of the time. Every year, the sales expense per

ASK was 0.13 U.S. cents- 0.14 U.S. cents, or 4% of the total CASK, which is quite low.

Low yield: Due to competitive pricing and short distance flights, VJC‟s passenger yields

have been declining from 2013 to 2016, achieving 51 U.S. cents in 2013 and decreasing to

35 U.S. cents in 2016 (equivalent to -12% CAGR). Declining in yield was mainly driven by

aggressive promotion, stimulated by a sustained low fuel price in 2015 and 2016, as well as

expanded capacity. Other drivers include VJC's focus on the domestic market,

concentrating on lower-yield but higher frequency short distance flights.

COGs breakdown (FY2016) VJC’s historical yield growth

Source: VJC, SSI Research

Fuel 22%

Cost of aircraft

SLB 43%

Employee 7%

Depretiation and

amortisation

3%

Outsourcing

25%

Others 0%

-25%

-20%

-15%

-10%

-5%

0%

5%

2014 2015 1H16 2016

Average total base fare growth Yield growth

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 13

3. INDUSTRY OVERVIEW

3.1. Global Airlines Industry

Global airline productivity has increased during the period of 2005-2016, according to a

report by Boeing and the International Air Transport Association (IATA). In 2016, IATA

estimated that global airlines‟ net profitability improved by 1% YoY, posting an after tax profit of

USD 35.6 bn (vs. the operating profit industry average of only USD 4.3bn in 2005). Last year,

the global airlines industry benefited from healthy revenue and profit growth thanks to a 5.9%

YoY growth in total RPK and reduced jet fuel cost (down 22% YoY).

Specifically in Southeast Asia after the South China Sea crisis in 2014, the region has enjoyed

a boom in air travel demand till now thanks to (1) more stable geopolitics, (2) low jet fuel cost

and (3) strong air travel demand within the region.

2017 Outlook: Global airlines industry might deliver negative earnings growth due rising

oil prices

For 2017, IATA forecasts the global airline industry after tax profit to achieve USD 29.8n in

2017, down 16% YoY, representing potentially difficult years grappling with an expected rising

oil price. IATA forecasts the jet fuel price may reach USD 65/barrel in 2017 from USD 52/barrel

in 2016, up 25% YoY. As a result, fare promotions spurred on by lower oil prices may shrink in

2017, slowing global traffic growth to 5.1% (from 5.9% in 2016).

Performance of global airlines industry vs. Jet fuel cost

Source: IATA

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E2017F

Jet fuel price (USD/barrel) Operating margin Net profit margin

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 14

Long term outlook: Air travel demand will continue to grow

For the 2015-2034 periods, IATA is still optimistic about global air travel demand. It expects

global passenger numbers to reach 7.3 billion by 2034, implying an annual 4.1% growth. One of

Boeing's reports titled “Current Aviation Market Outlook” also shows that global aviation wi ll

continue to accelerate with a CAGR of 4.9% from 2015-2034, mainly thanks to stronger global

GDP growth of 3.1% by 2034 with a brighter outlook upon emerging countries. Among major

markets, Boeing suggests that air travel demand within Asia will prove the strongest growth,

with an annual growth of 6.2% in RPKs from 2015-2034.

Source: Boeing

Southeast Asia is one of the most active regions of LCCs. The region is seen as one of the

pioneer regions to employ the LCC business model. It grew to nearly 20,000 weekly commercial

flights, with a fleet total of 623 aircraft in 2016 (+7% YoY) according to CAPA. Due to rapid

expanding capacity, competition is fierce across the region, with crowded LCC fleets and

competitive air fares in a low fuel cost environment in recent years. CAPA forecasts that the

total LCC fleet in the region will grow by 11% YoY, reaching a total of 693 aircraft in 2017. As

such, this development will create a more intense competition landscape. Nevertheless,

according to Boeing the Southeast Asia aviation industry is expected to grow by 4.6% a year

through 2034. Urbanization and the expatriate population are rapidly rising in the region, which

will further contribute to healthy travel demand and industry growth. Additionally, the adoption of

the ASEAN Single Aviation Market will also strongly support industry growth. The ASEAN

Single Aviation Market will liberalize the region‟s air services, specifically among ASEAN

countries, benefiting both passengers and airlines alike.

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

SSI.COM.VN Visit SSI Research on Bloomberg at SSIV <GO>

Page 15

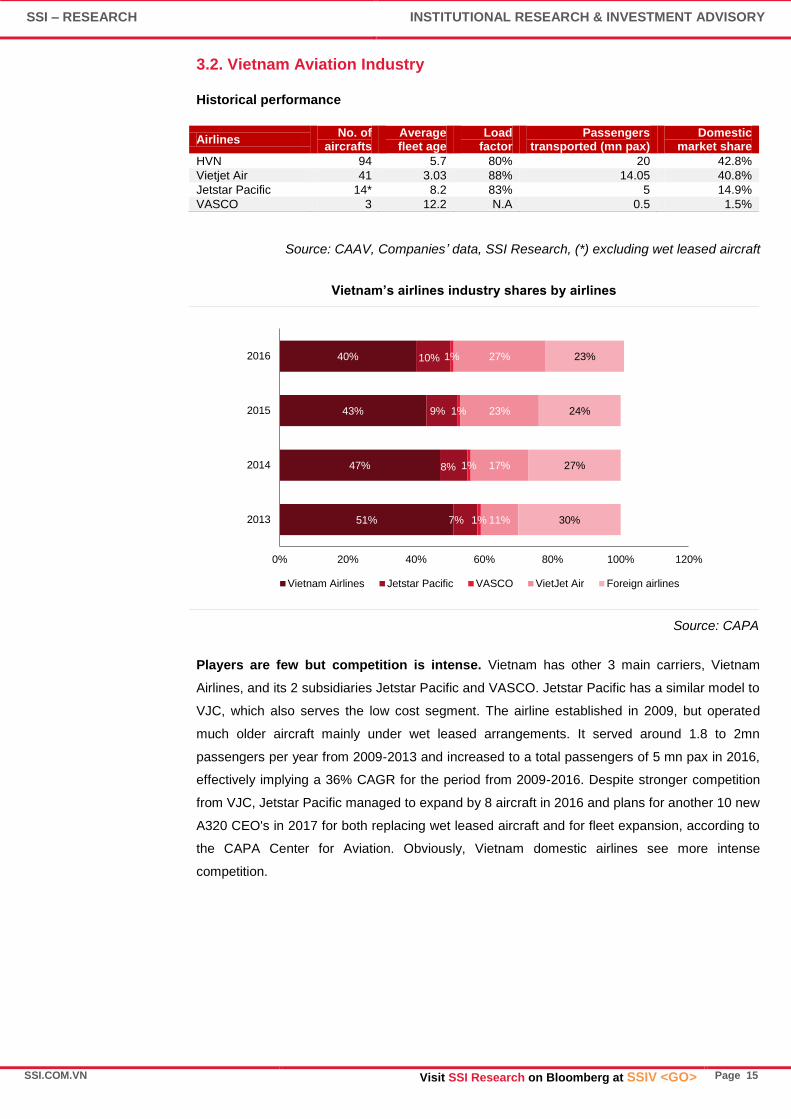

3.2. Vietnam Aviation Industry

Historical performance

Airlines No. of

aircrafts Average fleet age

Load factor

Passengers transported (mn pax)

Domestic market share

HVN 94 5.7 80% 20 42.8%

Vietjet Air 41 3.03 88% 14.05 40.8%

Jetstar Pacific 14* 8.2 83% 5 14.9%

VASCO 3 12.2 N.A 0.5 1.5%

Source: CAAV, Companies’ data, SSI Research, (*) excluding wet leased aircraft

Vietnam’s airlines industry shares by airlines

Source: CAPA

Players are few but competition is intense. Vietnam has other 3 main carriers, Vietnam

Airlines, and its 2 subsidiaries Jetstar Pacific and VASCO. Jetstar Pacific has a similar model to

VJC, which also serves the low cost segment. The airline established in 2009, but operated

much older aircraft mainly under wet leased arrangements. It served around 1.8 to 2mn

passengers per year from 2009-2013 and increased to a total passengers of 5 mn pax in 2016,

effectively implying a 36% CAGR for the period from 2009-2016. Despite stronger competition

from VJC, Jetstar Pacific managed to expand by 8 aircraft in 2016 and plans for another 10 new

A320 CEO's in 2017 for both replacing wet leased aircraft and for fleet expansion, according to

the CAPA Center for Aviation. Obviously, Vietnam domestic airlines see more intense

competition.

51%

47%

43%

40%

7%

8%

9%

10%

1%

1%

1%

1%

11%

17%

23%

27%

30%

27%

24%

23%

0% 20% 40% 60% 80% 100% 120%

2013

2014

2015

2016

Vietnam Airlines Jetstar Pacific VASCO VietJet Air Foreign airlines

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

Passengers volume carried by Vietnamese airlines Domestic passenger carried shares in 2016

Source: GSO, SSI Research Source: CAAV

According to the General Statistics Office of Vietnam (GSO), total passengers transported by

Vietnamese airlines are estimated to grow 30.3% YoY to roughly 40.5 mn pax in 2016 (vs. that

of 27% YoY in 2015), representing a CAGR of 19% from 2010-2016. The encouraging growth

was attributable to (1) Sustained strong GDP (growth of 6.2%in 2016), resulting in an increase

of roughly 5% in per capita GDP growth reaching USD 2,095 bn, which highly correlated with air

travel per capita growth and correspondingly accelerated airlines industry growth; (2)

international tourists to Vietnam by air increased by 31% YoY compared with a flat growth YoY

in 2015; and (3) low fuel prices encouraged airlines to reduce air fares, sparking travel demand.

Industry outlook

2017

In our opinion, we believe that Vietnam‟s airline industry will continue to experience positive

growth in the coming years due to the following drivers:

GDP growth of Vietnam at 6.2% in 2017, according to the IMF forecast (Government‟s

target: 6.7%, SSI Research‟s forecast: 6.6% in 2017 vs. 6.21% in 2016), leading to GDP

per capita to increase to USD 2,199 (+5% YoY), and should significantly benefit airlines.

We also forecast Vietnam‟s exports and imports to grow by 6.5% YoY and 10% YoY

respectively, making a wider implication of expected higher air transportation and a boost in

air travel demand overall.

International tourist traffic to Vietnam is expected to grow to 12% YoY in 2017 from the

average of 9.48% over the last five years, originating from the recent government initiative

to boost the tourism sector. The aviation industry is the largest beneficiary of Vietnam‟s

robust tourism growth in the coming years.

Low cost carriers (LCCs) will continue to win more passengers from traditional

transportation modes such as railway and bus, with more affordable air fares amid a rising

domestic middle class. Underdeveloped infrastructure such as highways and bridges

30%

6%

-1%

13%

44%

27% 30%

19%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

2010

2011

2012

2013

2014

2015

2016E

2017F

Mn

pa

x

Passengers Passenger YoY

42.8%

40.8%

14.9%

1.5%

Vietnam Airlines

Vietjet Air

Jetstar Pacific

VASCO

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

causing time consuming delays will also be a variable in an increase of passengers to opt

for air travel.

Aggressive capacity expansion added in 2017 (Vietjet: 12 new aircraft, Jetstar: 6 aircraft,

Vietnam Airlines: 5 aircraft) will result in more air fare promotions, thus prompting air travel

demand.

Despite the above advantages, we expect demand growth to be somewhat affected in 2017

onwards with the variable of the expected global oil price recovery. Additionally, airline capacity

expansion is another variable, with 27 additional aircraft to be delivered in 2017 as stated

above, which will lower airline industry passenger loads. Nevertheless, the negative impact of

lower passenger loads per plane is expected to be outstripped by the overall positive volume

growth of passenger growth across all routes industry-wide.

Long term

Vietnam is ranked as the 5th

fastest growing market in terms of passenger growth per

year, and the 7th fastest growing industry from 2016-2035 by IATA. According to the most

updated forecast by IATA, Vietnam aviation will continue to grow at an annual rate of 7.3%,

being the 7th fastest growing market of countries that IATA tracks. The growth will be largely

supported by: (1) sustained strong GDP growth of 6.5% and 6.3% in 2017 and 2018 (Source:

IMF, 2017), leading to an improvement in per capita GDP growth. We expect GDP per capita to

reach USD 2,692 by 2020, a CAGR of 5% from 2016-2020, according to our SSI Research

forecast. (2) Positive international tourist volume growth is expected to persist over the next 5

years. Vietnam is among the fastest growing countries regarding international tourist arrivals,

reporting a 9.5% CAGR from 2010-2015 (after Thailand with 9.5%). It is forecast to continue to

see a CAGR growth of 7.9% from 2015-2020 (Euromonitor, 2016 quoted by VJC). (3) Increased

urbanization rates will also support the trend of domestic air travel in the future. Urbanization is

expected to grow at a CAGR of 1% from 2015-2020(IFM, 2014) and reach roughly 38-40% by

2020 (according to the Vietnamese government‟s 5 year development plan), implying a

continuous rise in Vietnam's middle class. Overall, bright key macro-economic growth drivers as

above mentioned will continue to support the Vietnamese aviation industry over the next 5

years.

Improved aviation infrastructure will better facilitate air travel demand: First, the

monopoly entity Airport Corporation of Vietnam plans to expand designed capacity of its all 22

airports with a 13% CAGR from 2016-2019, in which the Noi Bai International Airport, Tan Son

Nhat Airport and Da Nang Airport will be expanded by 6%, 15% and 29% CAGR respectively. In

addition, Long Thanh International Airport project with 25 mn passengers in designed capacity

may be operational by 2025. As such, the infrastructure expansion will ease the bottleneck in

trunk routes, connecting the 3 largest airports to improve passenger service and further

promote air travel for both domestic and international passengers.

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

3.3. VJC’s growth Outlook

VJC‟s top-line will benefit from higher seat capacity thanks to an upcoming aggressive fleet

expansion. This will be partly offset by low yield due to strong competition and continuously

offering low fares in newly established routes.

Domestic market will rise in 2017-2019 and then experience a slowdown

We expect high growth of VJC mainly comes from seizing market share from its competitors

and passengers from other traditional transportation methods such as trains and buses.

According to the GSO and the Civil Aviation Authority of Vietnam, total passengers traveling by

train and bus were 10 mn and 3 mn pax per year respectively. As such, there is still room for

VJC to gain more market share from these modes of transportation. However, the domestic

market may saturate in the next 2-3 years, which will push VJC to expand internationally in

more aggressive fashion.

In 2017, VJC’s domestic passenger volume growth will be mainly driven by growth in

existing trunk routes: As of 2016, its 26 routes fly out from one of the 2 main airport hubs

of Hanoi, Ho Chi Minh City together comprise for about 70% of domestic flights. VJC will

add more capacity onto these routes in 2017 to capture the growing demand of the country.

These routes have quite high frequencies of more than 7 flights per week with high

passenger loads. Overall, VJC forecasts that passenger volume in domestic trunk routes

will grow by approximately 20% YoY this year.

New domestic routes: VJC commenced 6 domestic new routes including Hanoi - Tuy

Hoa, Haiphong - Phu Quoc, Haiphong - Dalat, Haiphong - Buon Me Thuot, Nha Trang -

Thanh Hoa and Hanoi - Hue with 4-7 flights per week in May 2016 and 2H16. These will

contribute to 2017 growth as operating in the entire year. However, these routes‟

frequencies are quite low due to low demand. Passenger load factors for these routes are

expected to be lower than the trunk routes. In 2017, VJC plans to open 4 additional routes.

As VJC‟s flight network covers almost all airports in Vietnam, there will be limited

opportunities for further domestic expansion. VJC targets to increase scheduled domestic

routes to 45 by the end of 2019 (vs end of 2016: 37 routes and end of 2017P: 41 routes).

Strong capacity expansion in international routes

From 2017, the airline will over the next coming years aggressively open new international

routes within a radius of 2,500 nautical miles, average flight duration of roughly 5-6 hours to

destinations such as Korea and Japan.

Existing routes Vietnam-destinations: Originally cutting the ribbon with the

commencement of the Bangkok – Hanoi route back in 2013, currently VJC‟s international

network comprises of 23 routes, including:

4 routes to South Korea, directly competing with Eastar Jet, Air Busan, Jeju Air, Jin Air,

and T‟way.

2 routes to Taiwan, facing competition with Vanilla Air(Tokyo-HCMC via Taipei) and

Tigerair Taiwan;

8 routes to China, with 7 Chinese LCC competitors; In Southeast Asia resides the

fiercest competition for VJC's core market, namely AirAsia and other local LCCs.

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

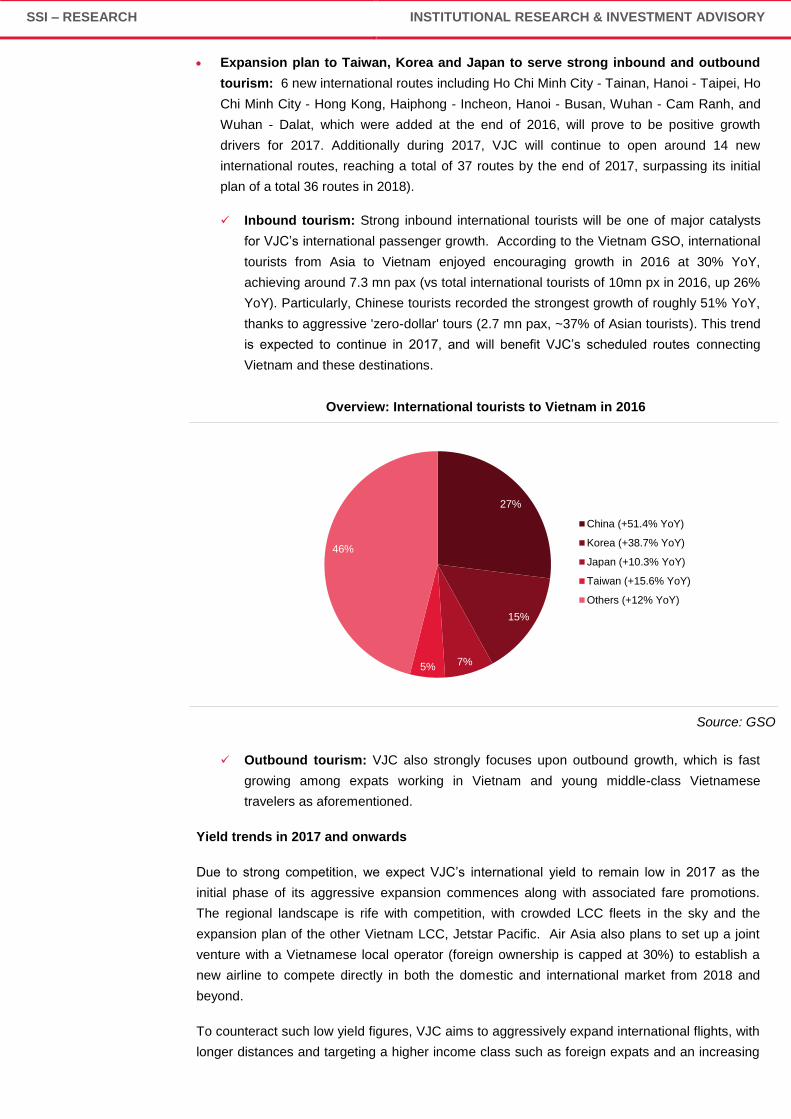

Expansion plan to Taiwan, Korea and Japan to serve strong inbound and outbound

tourism: 6 new international routes including Ho Chi Minh City - Tainan, Hanoi - Taipei, Ho

Chi Minh City - Hong Kong, Haiphong - Incheon, Hanoi - Busan, Wuhan - Cam Ranh, and

Wuhan - Dalat, which were added at the end of 2016, will prove to be positive growth

drivers for 2017. Additionally during 2017, VJC will continue to open around 14 new

international routes, reaching a total of 37 routes by the end of 2017, surpassing its initial

plan of a total 36 routes in 2018).

Inbound tourism: Strong inbound international tourists will be one of major catalysts

for VJC‟s international passenger growth. According to the Vietnam GSO, international

tourists from Asia to Vietnam enjoyed encouraging growth in 2016 at 30% YoY,

achieving around 7.3 mn pax (vs total international tourists of 10mn px in 2016, up 26%

YoY). Particularly, Chinese tourists recorded the strongest growth of roughly 51% YoY,

thanks to aggressive 'zero-dollar' tours (2.7 mn pax, ~37% of Asian tourists). This trend

is expected to continue in 2017, and will benefit VJC‟s scheduled routes connecting

Vietnam and these destinations.

Overview: International tourists to Vietnam in 2016

Source: GSO

Outbound tourism: VJC also strongly focuses upon outbound growth, which is fast

growing among expats working in Vietnam and young middle-class Vietnamese

travelers as aforementioned.

Yield trends in 2017 and onwards

Due to strong competition, we expect VJC‟s international yield to remain low in 2017 as the

initial phase of its aggressive expansion commences along with associated fare promotions.

The regional landscape is rife with competition, with crowded LCC fleets in the sky and the

expansion plan of the other Vietnam LCC, Jetstar Pacific. Air Asia also plans to set up a joint

venture with a Vietnamese local operator (foreign ownership is capped at 30%) to establish a

new airline to compete directly in both the domestic and international market from 2018 and

beyond.

To counteract such low yield figures, VJC aims to aggressively expand international flights, with

longer distances and targeting a higher income class such as foreign expats and an increasing

27%

15%

7% 5%

46%

China (+51.4% YoY)

Korea (+38.7% YoY)

Japan (+10.3% YoY)

Taiwan (+15.6% YoY)

Others (+12% YoY)

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

number of Vietnamese tourists with the means to go abroad for vacations and other occasions.

As such, yield is expected to slightly improve from 2018 onwards, corresponding with

increasing fuel prices and a stable flight route network. Adding to this is the undercurrent

variable of increasing demand from the Vietnamese middle class for LCC's and other Asian

countries which as a whole will support the yield to stabilize. However, the road to significant

recovery will also be marked by intense competition over the next 2-3 years

Low base provides a launching pad for VJC’s ancillary revenue growth

VJC‟s ancillary revenue accounted for 22% of total revenue in 2016 (excluding SLB revenue),

compared to an average 26.1% of other LCCs (for example Air Asia: 25%, Spirit Airlines:

38.7%). VJC‟s ancillary revenue achieved USD 11.4 per pax (declining 6% YoY, but up 14%

compared with 2015), still lower than the industry average of $43 USD per person. Therefore,

ancillary revenue still has large room to grow via changes of extensions to non-refundable

tickets and oversized luggage, as well as in-flight retails.

Revenue from SLB activities

VJC continues to pursue the SLB model and expects to record profit recognition from aircraft

sales, which will not require significant upfront CAPEX for acquiring new aircraft. In 2017, VJC

plans to add 17 new aircraft in which 15 will be SLB.

The company believes that it can maintain high SLB gains in 2017 as the received aircraft are

all A321 considered favorable by lessors. Additionally, the Company believes they have better

bargaining power over manufacturers and lessors thanks to its excellent performance recently.

In total, SLB gain is conservatively projected at USD 90mil by VJC in 2017. The revenue is

expected to contribute roughly 40-47% to VJC‟s total revenue from 2017-2019.

A fuel cost uptrend is the largest risk, but hedging might partly render the risk subdued:

Amid the expected pick-up of jet fuel prices in 2017, of roughly 25 % (forecast by IATA). VJC

plans to hedge 30-35% of the total fuel cost (In fact, in 1Q17, average fuel jet price increased

by 47% YoY and -7% YTD). At the same time, the company will receive 5 A321-NEO aircraft in

2017, which will partly reduce the impact of fuel price surge with fuel efficiency gains of 15% per

aircraft.

Historical Jet fuel A1 price

Source: Bloomberg

0

20

40

60

80

100

120

140

160

4/27/2012 4/27/2013 4/27/2014 4/27/2015 4/27/2016 4/27/2017

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

4. EARNINGS ESTIMATES

4.1. 2017-2019 business plans

Positive passenger volume growth and low cost will help VJC‟s core revenue and net profit to

enjoy encouraging growth from 2017-2019. Besides, the company also plans to continue

recognizing revenue from SLB in the coming years. It plans to pay a 50% dividend (30% cash

and 20% stock) over the next 3 years.

VND bn 2017P 2018P 2019P

Revenue 42,018 48,767 56,998

YoY 49% 16% 17%

Net profit 3,395 4,406 4,950

YoY 36% 30% 12%

Dividend (on par) 50% 50% 50%

+Cash 30% 30% 30%

+Stock 20% 20% 20%

Fleet delivery schedule (total)Number of aircraft at year end 51 66 78

A320(New delivery) 28 32 38

A321-200(New Delivery) 56 59 64

Source: VJC

4.2. 2017 estimates

Based on VJC‟s fleet expansion and new route openings, we forecast that VJC‟s 2017 net

revenue will achieve VND 39,387bn (+43% YoY). Net income might reach VND 3,103bn (+24%

YoY). Our forecast based on the following summary of our analysis:

Passenger volume will achieve roughly 18.9 mn passengers in 2017, increasing by 34%

YoY thanks to (1) the 4 new domestic routes featuring 3-7 flights per week, and the 6

international routes with 3-6 flights per week added in 2H16. These flights will contribute

growth to both passenger transportation and ancillary revenue. (2) In terms of opening new

routes, VJC targets to launch 4 domestic and 14 international routes in 2017. Overall, total

ASK is subjected to an increase of 38% YoY in 2017.

We expect VJC's to maintain its passenger load ratios, at 87% for domestic routes and 82%

in international routes (vs. 88% and 82% in 2016 respectively).

We expect that revenue from SLB activities will record VND 16,915bn (+46% YoY),

attributable to gains recognized from 15 new aircraft being delivered during the year for

SLB. We assume that gross profit may be recorded at USD 6mn per aircraft

We assume that the average jet fuel price will increase by 14% YoY.

Jet Fuel Quarterly assumption in 2017

USD/barrel 1Q 2Q 3Q 4Q Average

2016 43.9 55.3 56.5 61.2 54.2

2017F 64.8 62 58 62 61.9

YoY 48% 12% 3% 1% 14%

Source: Bloomberg, SSI Research assumption

Gross profit margin will slightly decline to 12.4% in 2017 due to the expected fuel cost hike

and lower GPM of SLB at 12% (vs 13% in 2016)

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

4.3. 2018-2023 estimates

We forecast that VJC‟s total passenger volume will grow at 13% CAGR. Domestic passenger

volume will grow at 10% CAGR, and international passenger volumes may enjoy a CAGR of

23% due to a rise from a low base. In summary, from 2018-2023, we expect total revenue and

net profit of VJC will grow at CAGRs of 19% and 20% respectively thanks to significant revenue

and gain from SLB recognized from Airbus and Boeing contracts. We assume that VJC may

receive 39 aircraft per year from 2020-2023, according to schedule delivery.

We assume that VJC will purchase and own 2 aircraft per year.

VJC’s operating data assumptions

VJC: Group operating data FY15 FY16 FY17E FY18E FY19E FY20E FY21E FY22E FY23E

RPKs(m) 9,690 14,451 21,891 26,607 32,063 37,090 42,233 47,233 52,449

ASKs (m) 11,055 16,498 25,715 34,237 42,983 51,114 58,826 66,056 73,733

Passenger load factor

Domestic 89% 89% 87% 87% 86% 85% 85% 85% 85%

International 84% 83% 82% 82% 82% 81% 80% 80% 80%

Yield per RPK (U.S. cents) 4.03 3.80 2.76 2.82 2.84 2.82 2.81 2.79 2.77

Average jet fuel price (USD/bbl) 66.70 52.10 59.39 64.74 66.36 67.87 69.23 69.92 69.92

Appreciation of USD against VND 3% 1% 2% 2% 2% 2% 2% 2% 2%

Source: VJC, IATA, World Bank, SSI Research forecats

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

5. VALUATION

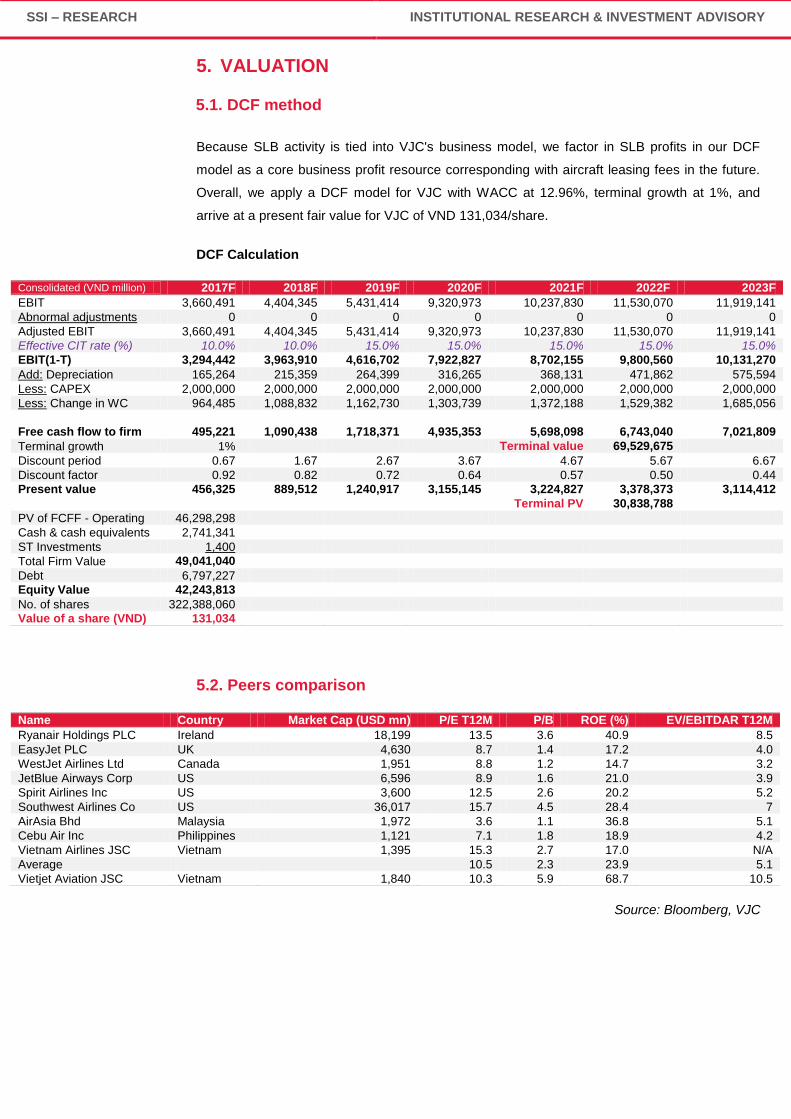

5.1. DCF method

Because SLB activity is tied into VJC's business model, we factor in SLB profits in our DCF

model as a core business profit resource corresponding with aircraft leasing fees in the future.

Overall, we apply a DCF model for VJC with WACC at 12.96%, terminal growth at 1%, and

arrive at a present fair value for VJC of VND 131,034/share.

DCF Calculation

Consolidated (VND million) 2017F 2018F 2019F 2020F 2021F 2022F 2023F

EBIT 3,660,491 4,404,345 5,431,414 9,320,973 10,237,830 11,530,070 11,919,141

Abnormal adjustments 0 0 0 0 0 0 0

Adjusted EBIT 3,660,491 4,404,345 5,431,414 9,320,973 10,237,830 11,530,070 11,919,141

Effective CIT rate (%) 10.0% 10.0% 15.0% 15.0% 15.0% 15.0% 15.0%

EBIT(1-T) 3,294,442 3,963,910 4,616,702 7,922,827 8,702,155 9,800,560 10,131,270

Add: Depreciation 165,264 215,359 264,399 316,265 368,131 471,862 575,594

Less: CAPEX 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000 2,000,000

Less: Change in WC 964,485 1,088,832 1,162,730 1,303,739 1,372,188 1,529,382 1,685,056

Free cash flow to firm 495,221 1,090,438 1,718,371 4,935,353 5,698,098 6,743,040 7,021,809

Terminal growth 1% Terminal value 69,529,675

Discount period 0.67 1.67 2.67 3.67 4.67 5.67 6.67

Discount factor 0.92 0.82 0.72 0.64 0.57 0.50 0.44

Present value 456,325 889,512 1,240,917 3,155,145 3,224,827 3,378,373 3,114,412

Terminal PV 30,838,788

PV of FCFF - Operating 46,298,298

Cash & cash equivalents 2,741,341

ST Investments 1,400

Total Firm Value 49,041,040

Debt 6,797,227

Equity Value 42,243,813

No. of shares 322,388,060

Value of a share (VND) 131,034

5.2. Peers comparison

Name Country Market Cap (USD mn) P/E T12M P/B ROE (%) EV/EBITDAR T12M

Ryanair Holdings PLC Ireland 18,199 13.5 3.6 40.9 8.5

EasyJet PLC UK 4,630 8.7 1.4 17.2 4.0

WestJet Airlines Ltd Canada 1,951 8.8 1.2 14.7 3.2

JetBlue Airways Corp US 6,596 8.9 1.6 21.0 3.9

Spirit Airlines Inc US 3,600 12.5 2.6 20.2 5.2

Southwest Airlines Co US 36,017 15.7 4.5 28.4 7

AirAsia Bhd Malaysia 1,972 3.6 1.1 36.8 5.1

Cebu Air Inc Philippines 1,121 7.1 1.8 18.9 4.2

Vietnam Airlines JSC Vietnam 1,395 15.3 2.7 17.0 N/A

Average 10.5 2.3 23.9 5.1

Vietjet Aviation JSC Vietnam 1,840 10.3 5.9 68.7 10.5

Source: Bloomberg, VJC

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

5.3. Investment view and recommendation

At the current price of VND 130,500/share, VJC is trading at 2017 and 2018 P/E of 13x and

12x, respectively and adjusted EV/EBITDAR of 7.2x and 5.6x, which are quite fair compared to

industry average. Combining DCF method and 1 year target P/E of 13x and adjusted

EV/EBITDAR of 7x (premium compared with industry average attributable to the duopoly

position in Vietnamese LCC segment and high growths in the initial phase of operation). We

arrive at a 1 year target for VJC of VND 140,400/ share (+8%). We recommend to HOLD the

stock.

5.4. Risks and issues

General risk for all airlines

(1) Uptrends in fuel price will be negative for all airlines.

(2) Possible landing charge increases at the 7 largest airports in Vietnam for domestic routes

by ACV. According to ACV, the company together with Civil Aviation Authority of Vietnam

proposed to the Ministry of Transport to increase the landing charge at 7 airports including

Tan Son Nhat, Noi Bai, Da Nang, Cam Ranh, Phu Quoc, Vinh and Phu Bai Airport.

Specifically, domestic landing charges may increase and equal to a 50% charge from that

of international flights (from the current ratio of 34%). This should significantly impact the

airline industry GPM.

Specific risks for VJC

(1) As market share of VJC is already high, it might be difficult for the company to soak up

more market share and also to maintain high passenger loads per plane given the large

number of aircraft being delivered over the next 5-10 years.

(2) A large portion of VJC profits comes from the sale of new aircraft that the company buys in

bulk at deep discounts. On the one hand, this strategy has helped Vietjet Air increase

competitiveness by lowering ownership cost and operating costs. On the flip side, this

makes earnings more volatile. Furthermore, lease payment terms could be fixed and non-

cancellable, regardless of whether or not passenger traffic delivers.

(3) Financial risk and FX risk persists, with its payback lease terms with the lessors leaving the

company potentially vulnerable.

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

APPENDIX: ANNUAL FINANCIAL STATEMENTS

VND Billion 2015 2016 2017F 2018F

VND Billion 2015 2016 2017F 2018F

Balance Sheet

Income Statement

+ Cash 924 2,741 6,474 9,029

Net Sales 19,845 27,499 39,387 47,640

+ Short-term investments 270 1 0 0

COGS -17,736 -23,597 -34,517 -42,264

+ Account receivables 5,516 8,391 7,764 11,162

Gross Profit 2,110 3,902 4,870 5,376

+ Inventories 164 138 138 169

Financial Income 154 145 112 208

+ Other current assets 209 304 204 249

Financial Expense -562 -654 -711 -498

Total Current Assets 7,083 11,575 14,580 20,609

Income from associates 0 0 0 0

+ LT Receivables 2,060 3,843 4,278 5,099

Selling Expense -318 -518 -646 -773

+ Net Fixed Assets 29 1,047 2,882 3,667

Admin Expense -203 -189 -218 -226

+ Investment properties 0 0 0 0

Income from business operation 1,160 2,671 3,393 4,072

+ LT Assets in progress 137 181 181 181

Net Other Income 8 32 55 67

+ LT Investments 8 68 68 68

Profit Before Tax 1,168 2,703 3,448 4,138

+ Other LT Assets 2,727 3,348 4,832 5,917

Net Income 1,171 2,496 3,103 3,725

Total Long-Term Assets 4,962 8,487 12,242 14,933

NI attributable to shareholders 1,170 2,496 3,105 3,726

Total Assets 12,045 20,063 26,822 35,542

Minority interest 0 0 -2 -2

+ Current Liabilities 5,883 9,326 10,942 15,722

In which: ST debt 3,543 6,102 6,903 9,298

Basic EPS (VND) 0 0 9,630 11,559

+ Non-current Liabilities 4,015 6,002 7,440 8,622

BVPS (VND) 14,802 15,775 26,184 34,743

In which: LT debt 0 695 1,094 1,340

Dividend (VND/share) 0 0 4,000 3,000

Total Liabilities 9,897 15,329 18,382 24,345

EBIT 1,298 2,884 3,660 4,404

+ Contributed capital 1,450 3,000 3,224 3,224

EBITDA 1,308 2,930 3,826 4,620

+ Share premium 0 0 1,670 1,670

+ Retained earnings 686 1,703 3,518 6,277

Growth

+ Other capital/fund 12 31 30 -97

Sales 127.9% 38.6% 43.2% 21.0%

Shareholders' Equity 2,147 4,734 8,441 11,197

EBITDA 151.6% 123.9% 30.6% 20.8%

Total Liabilities & Equity 12,045 20,063 26,823 35,542

EBIT 155.2% 122.1% 26.9% 20.3%

NI 225.0% 113.2% 24.3% 20.0%

Cash Flow

Equity 122.2% 120.4% 78.3% 31.2%

CF from operating activities 852 1,636 3,928 1,882

Chartered Capital 81.3% 106.9% 7.5% 0.0%

CF from investing activities -1,201 -2,830 -2,000 -2,000

Total assets 56.9% 66.6% 33.7% 32.5%

CF from financing activities 740 2,986 1,805 1,673

Net increase in cash 391 1,792 3,732 2,555

Valuation

Beginning cash 527 924 2,741 6,474

P/E 0.0 0.0 13.3 11.1

Ending cash 924 2,741 6,474 9,029

P/B 0.0 0.0 4.9 3.7

P/Sales N.a N.a 1.0 0.9

Liquidity Ratios

Dividend yield N.a N.a 3.1% 2.3%

Current ratio 0.98 0.98 1.33 1.31

EV/EBITDA 1.8 1.4 10.8 8.9

Acid-test ratio 0.92 0.93 1.30 1.28

EV/Sales 0.1 0.1 1.0 0.9

Cash ratio 0.19 0.26 0.59 0.57

Net debt / EBITDA 1.79 1.14 0.73 0.34

Profitability Ratios

Interest coverage 10.01 15.96 17.21 16.56

Gross Margin 10.6% 14.2% 12.4% 11.3%

Days of receivables 6.3 15.9 9.1 0.8

Operating Margin 6.4% 10.2% 9.1% 9.0%

Days of payables 7.8 6.3 3.9 7.0

Net Margin 5.9% 9.1% 7.9% 7.8%

Days of inventory 2.7 2.3 1.5 1.3

Selling exp./Net sales 1.6% 1.9% 1.6% 1.6%

Admin exp./Net sales 1.0% 0.7% 0.6% 0.5%

Capital Structure

ROE 75.2% 72.5% 47.1% 38.2%

Equity/Total asset 0.18 0.24 0.31 0.31

ROA 11.9% 15.5% 13.2% 11.9%

Liabilities/Total Assets 0.82 0.76 0.69 0.69

ROIC 28.1% 30.9% 23.6% 20.8%

Liabilities/Equity 4.61 3.24 2.18 2.20

Debt/Equity 1.65 1.44 0.95 0.96

ST Debt/Equity 1.65 1.29 0.82 0.84

Source: VJC, SSIResearch

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

1. ANALYST CERTIFICATION

The research analyst(s) on this report certifies that (1) the views expressed in this research report accurately reflect

his/her/our own personal views about the securities and/or the issuers and (2) no part of the research analyst(s)‟

compensation was, is, or will be directly or indirectly related to the specific recommendation or views contained in this

research report.

2. RATING

Within 12-month horizon, SSIResearch rates stocks as either BUY, HOLD or SELL determined by the stock‟s expected

return relative to the market required rate of return, which is 18% (*). A BUY rating is given when the security is expected to

deliver absolute returns of 18% or greater. A SELL rating is given when the security is expected to deliver returns below or

equal to -9%, while a HOLD rating implies returns between -9% and 18%.

Besides, SSIResearch also provides Short-term rating where stock price is expected to rise/reduce within three months

because of a stock catalyst or event. Short-term rating may be different from 12-month rating.

Industry Rating: We provide the analyst‟ industry rating as follows:

Overweight: The analyst expects the performance of the industry over the next 6-12 months to be attractive vs. the

relevant broad market

Neutral: The analyst expects the performance of the industry over the next 6-12 months to be in line with the relevant

broad market

Underweight: The analyst expects the performance of the industry over the next 6-12 months with caution vs. the

relevant broad market.

*The market required rate of return is calculated based on 5-year Vietnam government bond yield and market risk premium derived from using

Relative Equity Market Standard Deviations method. Our rating bands are subject to changes at the time of any significant changes in the above

two constituents.

3. DISCLAIMER

The information, statements, forecasts and projections contained herein, including any expression of opinion, are based

upon sources believed to be reliable but their accuracy completeness or correctness are not guaranteed. Expressions of

opinion herein were arrived at after due and careful consideration and they were based upon the best information then

known to us, and in our opinion are fair and reasonable in the circumstances prevailing at the time, and no unpublished price

sensitive information would be included in the report. Expressions of opinion contained herein are subject to change without

notice. This document is not, and should not be construed as, an offer or the solicitation of an offer to buy or sell any

securities. SSI and other companies in the SSI and/or their officers, directors and employees may have positions and may

affect transactions in securities of companies mentioned herein and may also perform or seek to perform investment banking

services for these companies.

This document is for private circulation only and is not for publication in the press or elsewhere. SSI accepts no liability

whatsoever for any direct or consequential loss arising from any use of this document or its content. The use of any

information, statements forecasts and projections contained herein shall be at the sole discretion and risk of the user.

SSI – RESEARCH INSTITUTIONAL RESEARCH & INVESTMENT ADVISORY

WWW.SSI.COM.VN

SAIGON SECURITIES INC. Member of the Ho Chi Minh Stock Exchange, Regulated by the State Securities Commission

HO CHI MINH CITY 72 Nguyen Hue Street, District 1 Ho Chi Minh City Tel: (848) 3824 2897 Fax: (848) 3824 2997 Email: [email protected]

HANOI 1C Ngo Quyen Street, Ha Noi City Tel: (844) 3936 6321 Fax: (844) 3936 6311 Email: [email protected]

Page 27

4. CONTACT INFORMATION

Institutional Research & Investment Advisory

Kim Nguyen

Analyst, Industrials

Tel: (848) 3824 2897 ext. 2140

Phuong Hoang Hung Pham Giang Nguyen, ACCA

Deputy Managing Director, Associate Director Associate Director

Head of Institutional Research & Investment Advisory [email protected] [email protected]

Related Documents