Version as of 24-06-2011. Proportionate Regulatory Policies for the MSME Sector BENEL P. LAGUA President and COO Small Business Corporation Philippines

Version as of 24-06-2011. Proportionate Regulatory Policies for the MSME Sector BENEL P. LAGUA President and COO Small Business Corporation Philippines.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Version as of 24-06-2011.

Proportionate Regulatory Policies for the MSME Sector

Proportionate Regulatory Policies for the MSME Sector

BENEL P. LAGUAPresident and COO

Small Business CorporationPhilippines

Presentation Outline

1. Importance of MSME Sector2. Role of Government3. General Practices on Proportionate

Regulatory Policies4. The Philippine Response5. Policy Execution6. Conclusion

*The views expressed herein are the author’s and do not necessarily reflect the position of the Small Business Corporation.

Importance of MSME Sector The economic impact of MSMEs:

MSMEs make up 99.6% of total Philippine establishments and makes the following contributions to the Philippine economy 61% of employment 32% of value-added 60% of exports

MSMEs are largely dependent on the banking system for financing

MSMEs are disadvantaged due to size, higher unit transaction cost, perceived risks, and financial infrastructure distortions

The Role of Government in MSME Development

Facilitate MSMEs’ access to credit from formal institutions by:

Crafting policies that will allow for a borderless credit access by MSMEs and ensuring effective implementation of such policies

Creating a regulatory environment for banks conducive to MSME lending

Capacitating both banks and MSMEs Absorbing some costs of programs aimed at

increasing MSMEs’ access to credit Addressing market failure, leveling the

playing field

Proportionate Policies

“One size does not fit all”

Regulation and supervision can be expensive to implement, and costly when it fails

Need for affirmative action and tiered regulation—

Differing regulatory requirements based on market capitalization

Reduce discrimination Scale regulatory treatment

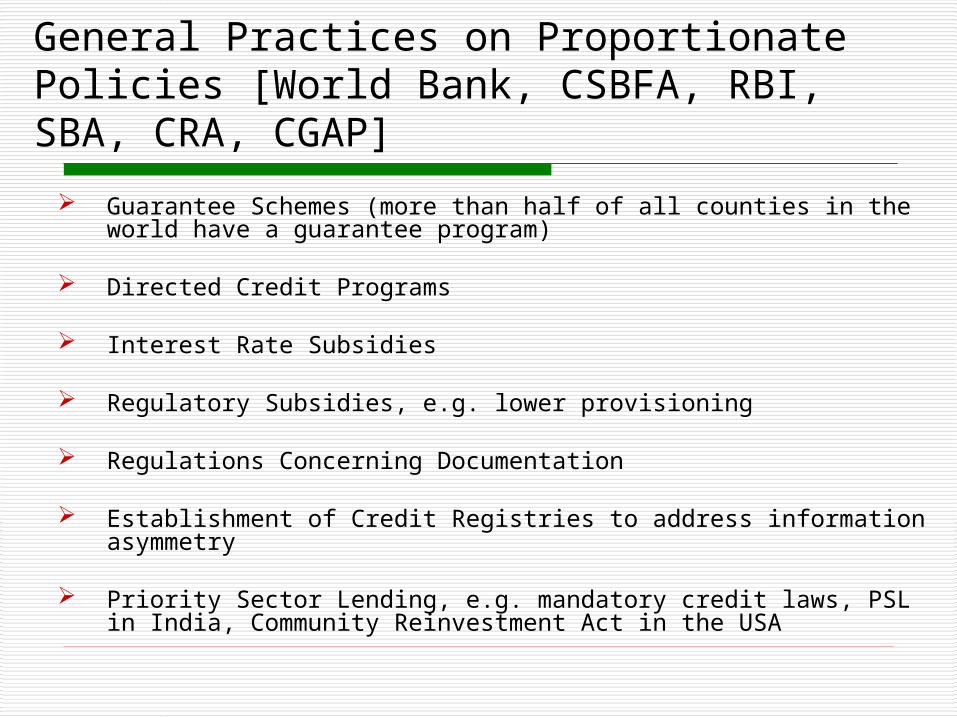

General Practices on Proportionate Policies [World Bank, CSBFA, RBI, SBA, CRA, CGAP]

Guarantee Schemes (more than half of all counties in the world have a guarantee program)

Directed Credit Programs

Interest Rate Subsidies

Regulatory Subsidies, e.g. lower provisioning

Regulations Concerning Documentation

Establishment of Credit Registries to address information asymmetry

Priority Sector Lending, e.g. mandatory credit laws, PSL in India, Community Reinvestment Act in the USA

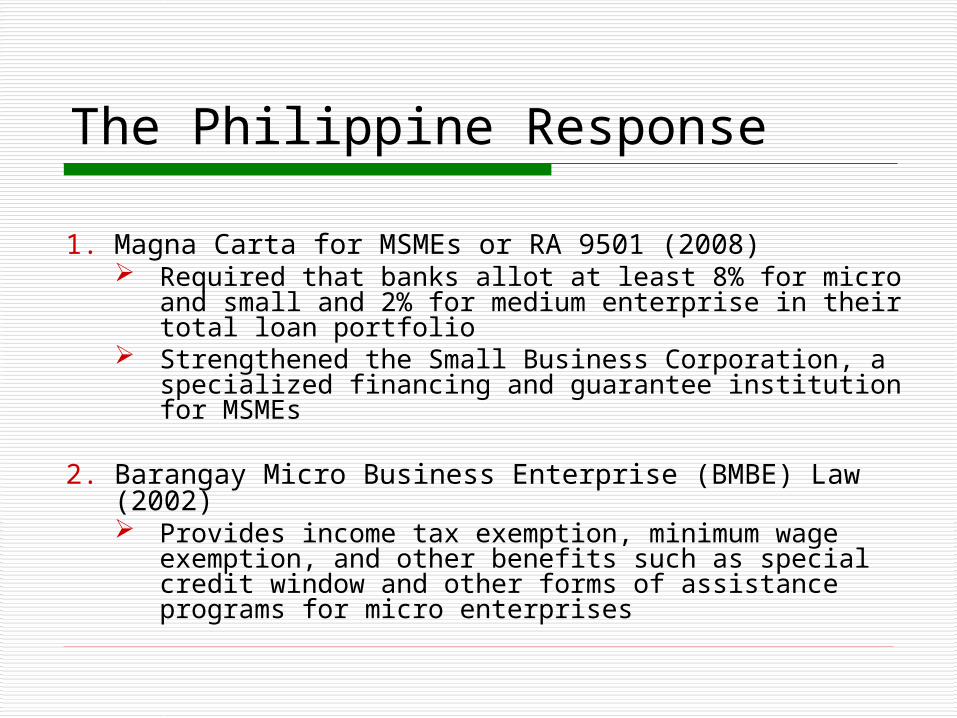

The Philippine Response

1. Magna Carta for MSMEs or RA 9501 (2008) Required that banks allot at least 8% for micro and

small and 2% for medium enterprise in their total loan portfolio

Strengthened the Small Business Corporation, a specialized financing and guarantee institution for MSMEs

2. Barangay Micro Business Enterprise (BMBE) Law (2002) Provides income tax exemption, minimum wage

exemption, and other benefits such as special credit window and other forms of assistance programs for micro enterprises

The Philippine Response3. Credit Information System Act or CISA (2008) or RA 9510

Mandates the creation of a credit information bureau that will serve as a central registry of repository of credit information including credit history and financial condition of borrowers

Promotes an efficient credit information system that will address financial institutions’ concerns on all their credit-related activities

4. Bangko Sentral ng Pilipinas (BSP) Regulations and Circulars on SME Lending

Capital requirements, loan documentation, risk weights

5. BSP Regulatory Framework on Microfinance: Encouraged the establishment of microfinance-oriented banks

and has a specialized microfinance regulatory unit. This allowed non-collateralized lending to the sector based on cash flow.

In theory, the Philippines is adopting the menu of

proportionate regulatory policies.

What is the problem?

Policy Execution1. a) Magna Carta for MSMEs or RA 9501 (2008)

On the mandatory credit allocation Compliance report too broad / Not transparent Overall, banking sector appear to be compliant with the

requirements of the law, but at the margin especially in micro and small—8.5% vs. mandated 8.0%

Individual performance of banks reveal, however, that many big banks remain under-complied

Some banks cover for the deficiency of other financial institutions

Lending figures to micro and small business sector is flat over the past 10 years—Negative real growth is observed.

Moral Hazard problem; Penalty structure for non-compliance is cheap/uniform and biased against smaller banks

Policy Execution1. b) Magna Carta for MSMEs or RA 9501 (2008)

On SB Corporation

Self-sustaining. No government infusion in the past 19 years. Declares Dividends.

No sovereign guarantee. Another GFI whose main mandate is guarantee for (large) export firms has a sovereign guarantee feature.

Limited capitalization when benchmarked against guarantee corporations in Asia; multiple objectives. Recent increased capitalization remains in paper

Supervision not much different from “standard” prudential supervision of banks

Policy Execution1. b) Magna Carta for MSMEs or RA 9501 (2008)

On SB Corporation

No clear appreciation of nature of guarantee corporation Costs incurred by the government in implementing MSME

financing programs (e.g credit guarantees) may not be directly recoverable using revenues per se as a measure

Full cost recovery could not be achieved without compromising the objective of facility finance to small business.

Cost-recovery can be measured through the underlying economic impact of MSME programs (i.e taxes for government, productivity, employment, income, economic growth, etc.)…[Canada SBFA Report]

Policy Execution

2. Barangay Micro Business Enterprise (BMBE) Law (2002)

Reluctance from executing agencies (i.e DOF and LGUs concerned about losses due to tax exemption granted to BMBEs)

3. Credit Information System Act or CISA (2008) or RA 9510

Still awaiting full implementation after almost 3 years that the law has been signed

Lack of funds to support the mandate, including the creation of the credit information corporation

Policy Execution

4. a) Bangko Sentral ng Pilipinas (BSP) Regulations and Circulars on SME Lending

On Loan Documentation:

Requires the submission of BIR-submitted Income Tax Return (ITR) upon loan application, including its waiver of confidentiality and its annual submission

Moratorium on submission granted for MSMEs, but to expire in December 2011

After 2011, small business loans without documents to be classified as “especially mentioned”

ITRs rarely reflect true condition of an enterprise. Should the exemption be extended?

Policy Execution4. b) Bangko Sentral ng Pilipinas (BSP) Regulations and

Circulars on SME Lending

On loan classification

Reduced risk weight of MSME portfolio from 100% to 75%

Subject to conditions like meeting certain prudential norms, including PDR of not more than 5% and a highly diversified portfolio with not less than 500 accounts

Questions on appropriateness of conditional prudential standards to enjoy risk weight reduction benefit

Policy Execution4. c) Bangko Sentral ng Pilipinas (BSP)

Regulations and Circulars on SME Lending

On loan classification

Loans to exports to the extent guaranteed by SBC with 20% risk weight

Loans to exporters to the extent guaranteed by GFSME with 0% risk weight so long as these are outstanding upon merger

Loans to exporters guaranteed by SBC in post-merger as 20% risk weight though these may be renewals

Is the reduced risk weight sufficient incentive to banks utilizing the guarantee?

Policy Execution4. d) Bangko Sentral ng Pilipinas (BSP) Regulations and

Circulars on SME Lending

On unsecured loans

In theory, no technical prohibition for granting of loans without collateral except for DOSRI limits

However, an unsecured loan for banks’ risk-based CAR is a 100% risk weight on capital

Also, in the event the loan turns past due, loan loss provisioning is immediately high

Not eligible for rediscounting Effectively, there is disincentive to lending without

collateral

Policy Execution4. e) Bangko Sentral ng Pilipinas (BSP)

Regulations and Circulars on SME Lending

Supported the creation of independent Credit Surety Fund (CSF) set aside by LGUs

Provides guarantee which secures the loan of MSMEs with local banks and facilitates lending without collateral

CSFs are too small and without muscle; model is not cognizant of how guarantee programs work

Policy Execution4. f) Bangko Sentral ng Pilipinas (BSP) Regulations and

Circulars on SME Lending

Reserve Requirements

PFIs of SB Corp are exempted from reserve requirements by BSP under SBC Wholesale Lending Program, encouraging banks to expand their MSME loan portfolio

However, BSP also runs its rediscounting window, sometimes at concessionary/subsidized rates, in competition with GFIs’ wholesale lending programs

Policy Execution5. Bangko Sentral ng Pilipinas (BSP) Regulatory

Framework on Microfinance

Issuance of circulars governing the practice of microfinance in the banking sector—rediscounting, recognition of microfinance (no collateral, loan documentation), allow branching, etc.

Modified Manual of Examination Promotion and Advocacy Philippines cited by EIU as having the best overall

regulatory environment for microfinance on banks. However, BSP does not cover NGOs and cooperatives.

Conclusion

Execution is opaque Implementing rules not following the spirit of basic law Under-funded and undersized programs—not

commensurate to mandate; unwillingness to make the investment

Inter-agency conflict—apparent weakness in coordination

Business model inconsistent with program objectives Costs and benefits of some proportionate regulatory

schemes not well-measured Objectives are at cross-purpose Major changes in Microfinance; Uneven policy

execution in SME Finance.

Conclusion

Government intervention by way of proportionate regulatory action must:

Focus on reducing risks and transaction costs associated with MSME lending

Balance the benefits of regulation/supervision against the costs and risks of no regulation/supervision

Aim for consistency across stakeholders and institutions

Conclusion

Government intervention by way of proportionate regulatory action must:

Serve as co-investor, thus, a source of risk capital

Educate private capital on how to lend to SME (capacity building)

Channel capital in strategic directions

Be designed for effective implementation, execution, and enforcement

Be “enlightened”

References1. ADB (2000), “The Role of Central Banks in Asia and the Pacific: Overview” (

http://www.adb.org/Documents/Books/Central_Banks_Microfinance/Overview/chap_05.pdf)

2. Canada Small Business Financing Act (2009), “Comprehensive Review Report 2004-2009),” [ http://dsp-psd.pwgsc.gc.ca/collections/collection_2010/ic/Iu188-1-2009-eng.pdf ]

3. CGAP (2011), “Recommendations for Proportionate Regulation and Supervision of Microfinance,” INCITRAL Colloquium on Microfinance

4. Clinton, Lindsay (2010), “India Journal: What’s Policy Got to Do With Social Enterprise?” (http://blogs.wsj.com/indiarealtime/2010/12/06/india-journal-whats-policy-got-to-do-with-social-enterprise/)

5. Fan, Qimiao (The World Bank), Presentation during the “Workshop on Improving Access to Finance for SMEs in Asia-Pacific Region, June 16-17, 2008

6. http://blogs.worldbank.org/allaboutfinance 7. http://dnb.com.au/Header/News/Banking_on_SMEs/indexdl_7334.aspx8. http://www.philstar.com/Article.aspx?publicationSubCategoryId=66&articleId=6975379. Sibold, S. (2005), “Addressing the Burden of Regulation in Canada—The Case for

Proportionate Regulation,” (http://www.tfmsl.ca/Documents/StephenSiboldPropReg.pdf)10. Thornley, B. et al (2011), “Case 12: Priority Sector Lending,” in Impact Investing, A

Framework for Policy Design and Analysis (http://www.pacificcommunityventures.org/insight/impactinvesting/report/12-Priority_Sector_Lending.pdf)

11. Wikipedia, Community Reinvestment Act (http://en.wikipedia.org/wiki/Community_Reinvestment_Act)

Related Documents