VAT IN BANGLADESH LOCALIZATION FOR BUSINES CENTRAL Requirement Analysis and design references ABSTRACT A high-level description of functional requirements for Bangladesh localisation requirements with reference to VAT ACT 2012 provisions and their impact on Microsoft Dynamics Business Central XYZ [Course title]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

VAT IN BANGLADESH

LOCALIZATION FOR

BUSINES CENTRAL Requirement Analysis and design references

ABSTRACT A high-level description of functional requirements

for Bangladesh localisation requirements with

reference to VAT ACT 2012 provisions and their

impact on Microsoft Dynamics Business Central

XYZ [Course title]

Confidential || Not for public circulation P a g e | 1

VAT and Supplementary Duty Act 2012 (VAT ACT 2012) with ERP implications

Contents Background information ........................................................................................................................ 2

Overview ......................................................................................................................................... 2

Revision history ............................................................................................................................... 2

Key Features: ................................................................................................................................... 2

Tax Rules ................................................................................................................................................. 3

VAT Registration and Turnover Tax enlistments Requirements ......................................................... 3

VAT Classifications and Coverage ....................................................................................................... 6

Importance of Economic Activities ................................................................................................. 6

VAT coverage exemptions .............................................................................................................. 6

VAT Rates ........................................................................................................................................ 7

Taxable Supply .................................................................................................................................... 8

VAT Mechanism .................................................................................................................................. 9

Input Output Coefficient ................................................................................................................... 10

Input VAT credit ................................................................................................................................ 10

Partial Input Tax ................................................................................................................................ 10

Withholding VAT ............................................................................................................................... 11

Reverse Charge Of VAT ..................................................................................................................... 11

VAT effected documents / applications for accounting purposes .................................................... 11

Tax Invoice .................................................................................................................................... 11

Integrated Tax invoice and withholding Certificate ...................................................................... 12

Books and records ......................................................................................................................... 12

VAT software ................................................................................................................................. 12

Online VAT services ....................................................................................................................... 12

ERP mapping implications:................................................................................................................... 13

Impact on setup information ............................................................................................................ 13

Impact on master data ...................................................................................................................... 13

Impact on Documents & transactions .............................................................................................. 14

Impact on processes ............................................................................ Error! Bookmark not defined.

Impact on reporting ............................................................................. Error! Bookmark not defined.

Mushak form mapping ...................................................................................................................... 15

Confidential || Not for public circulation P a g e | 2

Annexure ............................................................................................................................................... 16

Screen Designs .................................................................................................................................. 16

Report Designs .................................................................................................................................. 16

Mushak Form Designs ................................................................................................................... 16

Table relations ERD ........................................................................................................................... 16

Background information

Overview

D365 Business Central requires Bangladesh localization features. This requirement includes a portion

which will provide users to enable Bangladesh Tax accounting functions. The functions will include

Bangladesh VAT setup, accounting and reporting features. This document intends to layout the

understanding over the requirements, the mapping to the Business Central w1 design and also lays

down high level design impact to customize some of the requirements which does not fit directly

with W1 configuration options. This document will be updated from time to time during the course

of study, design and development lifecycle.

Revision history

Doc Version Release Ref Description of changes

Key Features:

The VAT localization will require the users to

• Keep registration information

• Maintain VAT Rules with respect to various types of transactions

• Maintain VAT Rules with respect to various types of goods and services

• Carry out transaction level computation and tracking of amounts resulting in calculated VAT

under various transaction scenarios such are Invoicing, adjustments and collections.

• Allow users to setup various reporting requirements in order to prepare and submit VAT

returns and related reports as prescribed by the VAT authorities in Bangladesh from time to

time.

Confidential || Not for public circulation P a g e | 3

Tax Rules

Following is a high-level understanding of the present VAT rules. The documentation is being carried

out in month of March 2021 and will be subject to future changes prescribed by the local authorities

from time to time.

VAT Registration and Turnover Tax enlistments Requirements

⮚ The VAT ACT 2012 is effective from July 1st, 2019.

⮚ Business Entities having turnover exceeding BDT 5000000 will be required to enlist for

Turnover Tax.

and

⮚ entities having turnover exceeding BDT 30,000,000 will be required to register for VAT.

⮚ What Constitutes “Turnover”?

VAT Act 2012 defines Turnover as all money received or receivable against supply of taxable

goods or the rendering of taxable services by means of economic activities.

For the purpose of assessing the eligibility for registration and enlistment, Turnover shall not

include:

o The value of Exempted supply

o The value of sales of capital asset

o The value of supply made as a consequence of permanently closing down an

economic activity

o The value of sale of an organization of economic activity or any portion thereof.

⮚ The following entities will be required to register for VAT regardless of turnover threshold:

o Supplier/ Manufacturer/ Importer of goods or services which are subject to SD ACT.

o Any person recommended by NBR. NBR has issued a list of providers of 175 such

goods and services which are subject to tax

o Import Export

o Supplier of goods of services through tender, work order or contract.

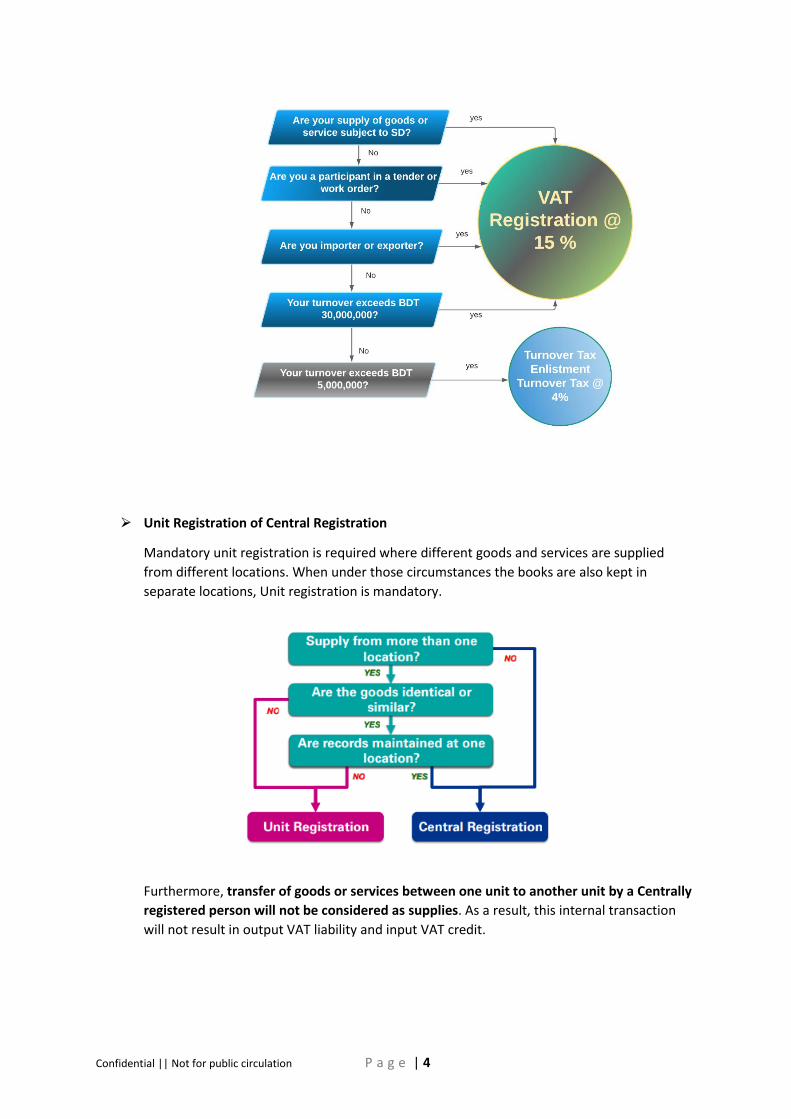

High Level Decision support diagram in order to decide registration requirements

Confidential || Not for public circulation P a g e | 4

⮚ Unit Registration of Central Registration

Mandatory unit registration is required where different goods and services are supplied

from different locations. When under those circumstances the books are also kept in

separate locations, Unit registration is mandatory.

Furthermore, transfer of goods or services between one unit to another unit by a Centrally

registered person will not be considered as supplies. As a result, this internal transaction

will not result in output VAT liability and input VAT credit.

Confidential || Not for public circulation P a g e | 5

⮚ List of enlisted persons

The Board shall preserve a correct and updated list of all the persons registered or enlisted under this

Act, where the following things shall remain included, viz: –

(a) Name and address of the registered or enlisted person;

(b) Business name or names, if there is any, by which the said registered or enlisted person conducts

his economic activities;

(c) Business Identification Number of the person;

(d) If the said person is separately registered for his branch unit, the business name, address and

Business Identification Number of every branch unit;

(e) The date on which registration or enlistment has come into effect; and

(f) Latest status of registration or enlistment

⮚ Business Identification Number

Subject to the provisions of Rule 117, Business Identification Number shall be used in the following

cases, viz: –

(a) All other imports-exports except baggage imports;

(b) Registration of land or building in the name of registered or enlisted person;

(c) Obtaining Import Registration Certificate and Export Registration Certificate;

(d) Making any supply to a withholding entity;

(e) Participation in any tender;

(f) Enlistment in any organization;

(g) Approval of Bond License;

(h) Approval of bank loan in favour of registered or enlisted person; and

(I) In any other case determined by an order of the Board

Confidential || Not for public circulation P a g e | 6

VAT Classifications and Coverage

Importance of Economic Activities

VAT Act 2012 imposes VAT on “economic activities”. The Act defines economic act economic activity

as any activity carried out regularly or continuously for supply or any goods or services or immovable

property.

o Exempted Supplies

o Taxable Imports

o Taxable Supply

o Imported Services

VAT coverage exemptions

o VAT exempted Goods

The ACT provides in the first schedule exemption on certain goods and services as well

as specific exemptions through Statutory orders.

o VAT exempted Services

o Basic services for livelihood

o Social Services

o Cultural Services

o Financial Services

o Transportation Services

o Certain Other services

o Zero Rate VAT Goods

o Supply of any goods from inside to outside Bangladesh

o Temporarily imported Goods

o Deemed export

o Supply of goods for the purpose of repairs, maintenance or modification and

supply or stores and spare parts to ocean going ship and aircraft engaged in

international transport

o Zero Rated VAT services

o Services given physically on goods situated outside Bangladesh at the time of

supply of services

o Services given relating to the temporarily imported goods under Customs Act.

o Service given to a recipient situated outside Bangladesh at the time of supply

o Supply of telecommunication services by a Telecom supplier to a non-resident

telco supplier.

Confidential || Not for public circulation P a g e | 7

VAT Rates

Confidential || Not for public circulation P a g e | 8

Taxable Supply

the value of a taxable supply is the amount derived by reducing the tax fraction

VAT / (100 + VAT)

TARIFF VALUE GOODS

Confidential || Not for public circulation P a g e | 9

VAT Mechanism Previous VAT legislations’ requirements led to having positive VAT balance (VAT receivable) before

making any sales which led to refund situations and adverse cash flow impacts. The VAT Act 2012

redefined the manner of VAT payment by allowing VAT to be paid on net basis at period ends,

resulting in situations of favourable cash flow and VAT receivables.

Net Vat is therefore payable within 15 days of the following month end at the time of submission of

VAT returns.

Computation of the Net VAT Payable

Increasing Adjustment Decreasing Adjustment

Withholding Tax Negative amount carried forward from previous period

consequence of annual reassessment VAT paid in advance

For not making payments through banking channels Withholding Tax

Input tax and VAT on being registered consequence of annual reassessment

Payment of any interest, monetary penalty, fee, etc In relation to second hand goods purchased for resale

Change in tax rate policy insurance, lottery, lucky draw, raffle draw, house

undertakings

Change in tax rate

Confidential || Not for public circulation P a g e | 10

Input Output Coefficient Price declarations are not required to be filed under VAT Act2012.

Registered and enlisted persons are required to file Input-Output coefficient declarations in Mushak

Form 4.3.

This is required to be filed 15 days prior to the date of supply whenever the first supply of a new

goods/ services is made or first supply after a change is required in the input-output coefficient.

This is a prerequisite to obtain Input VAT credit.

Input VAT credit A registered Person shall be entitled to an input VAT credit for any taxable import or taxable supply

made to that person for conducting their economic activities and taxable supplies.

The VAT Act 2012 allows input credit for most the supplies received excluding the following:

o Expenses for exempted goods and services

o Expenses not mentioned in the input-output coefficient declaration

o Expenses related to supplies that are subject to Turnover TAX (VAT), VAT at specified rates

or VAT at a rate less than 15%.

o Expenses over BDT 100,000 for which payment is made without banking channel.

o Imported services for which output VAT has not been shown in VAT returns

o Claim of input VAT credit which has not been made either in the VAT period in which VAT is

paid or within the 2 succeeding VAT period.

o Expenses for which the VAT invoice (Mushak Form 6.3) does not mention the name, address

and BIN of both purchaser and supplier.

o VAT paid on inputs that have not been entered into the Purchase Register prescribed by the

Rules

Partial Input Tax If a registered person is not entitled to full input VAT credit, their entitlement to such input credit

against imports and acquisitions shall be calculated in a proportionate manner as follows:

I X (T/ A)

Where -

I is the total amount of input tax originating from imports or acquisitions

T is the amount paid on all the taxable supplies during the tax period

A is the amount paid by the registered person on all the supplies during a tax period

Part of total consideration of Supply

In case where a person pays or is liable to pay part of the consideration for a taxable supply any

input tax credit to which the person is entitled to, shall be calculated on the basis of the amount of

consideration such person pays or is liable to pay.

Confidential || Not for public circulation P a g e | 11

Withholding VAT (VDS) Responsibility to withhold Tax or VAT Deducted at Source (VDS) as per provisions of VAT Act 2012

falls on the following types of entities: -

o Government Entity

o Non-government entity approved by NGO affairs or DG Welfare Services

o A bank, insurance company or similar financial institution

o A post-secondary educational institution

o A limited company

Certain cases are mentioned where VDS is not required by the responsible entities or where the

Mushak 6.3 is not provided in prescribed format by supplier.

Reverse Charge Of VAT The VAT Act 2012 provides clear provision for VAT on imported services under the concept of

reverse charge.

The imported services will be taxable supply in the hands of the recipient and hence it has to be

shown under Output VAT consideration. Simultaneously the importer will be liable to show the

applicable VAT under the input VAT credit portion.

VAT on imported services unless exempted, will be applicable even if importer is not registered or

required to be registered. However, in this case the person will not be able to obtain the benefit of

Input credit.

VAT effected documents / applications for accounting purposes

Tax Invoice

All registered suppliers are required to issue 2 copies of serially numbered Tax invoices on or before

the date when VAT becomes on such supplies containing the following information: -

a) Date and time of the issue of the invoice

b) Name, address and BIN of both the supplier and buyer if the supply value is greater than BDT

25000

c) Description of the goods and services

d) Quantity of the goods supplied

e) The value of the supply (both exclusive of VAT and inclusive of VAT)

f) The VAT rate applicable to the supply

Confidential || Not for public circulation P a g e | 12

g) The amount of VAT payable

h) Any other information prescribed by the board.

Supply from multiple locations: -

Invoice should be serialised for each location

This number along with the name and address of the location should be mentioned

Integrated Tax invoice and withholding Certificate

A registered person who makes a supply to a withholding entity shall issue an integrated tax invoice

and withholding certificate containing the prescribed information. Refer (Mushak 6.3)

Books and records

All prescribed documents to be customized as per company’s formats and templates.

All records to be maintained for at least 5 years or in case of disputes, till the settlement of disputes.

VAT software

NBR has made it mandatory for all entities having turnover exceeding BDT 50,000,000 in the

previous financial year to maintain their VAT related books in software prescribed by the VAT

authority. Such software should be from NBR approved developer.

Online VAT services

The new VAT rules 2016 makes it easy to use internet-based portals of NBR to conduct the following

activities: -

1. Register for VAT or Turnover Tax

2. Submission of VAT or Turnover Tax returns

3. Deposit VAT or Turnover Tax amount through digital platforms of NBR and Sonali Bank

Limited.

Confidential || Not for public circulation P a g e | 13

ERP mapping implications:

We will try to asses the impact in configurations and customization over W1 version of the Business

Central application in the following section.

Possible use of existing setup options

• VAT Posting Setup using VAT business posting groups and VAT Product Posting groups

• Storing the combination of the VBPG and VPPG to store the rates mentioned under standard

VAT, truncated VAT, trade VAT, specific tariff value VAT, Advance VAT

Possible Customization Areas

• WHT journal setup options and computation at invoice and payment journals

• Advance Tax payments and settlements with invoices

• Reverse Charge Mechanism

• Tax return computation

• Input credit allocations and I/O coefficient related calculations

Impact on setup information • Company Tax information containing registration and listing requirements

• declarations related to the services (input-out coefficient calculation and date declared for

every coefficient.

• VAT transaction type entry options

• VAT rates with effective date control

• Exemption criteria option

• Input out credit qualifying criteria

• Advance Tax qualifying criteria

Impact on master data • Customer Master Data

o Link to VAT business posting type

o Export Customer type

o Registration number

o Address of the registered office

o Exemption details

o WHT applicable

o WHT posting group

• Vendor Master Data

o Link to VAT business posting type

o Import vendor flag with validation with address data

o Registration number

Confidential || Not for public circulation P a g e | 14

o Address of the registered office

o Exemption details

o WHT applicable

o WHT posting group

• Items Master Data

o Link to input output coefficient details

o Link to VAT product posting group

• VAT Business Posting Groups

• VAT product Posting Groups

• VAT posting Setup

• Chart of accounts

o Flag to identify as VAT subledger

• Setup for WHT posting profile

• Setup for Advance Tax posting profile

•

Impact on Documents & transactions • Purchase Orders / Quotes / Invoices / Transfer Orders

• Sales Orders / Quotes / Invoices

• Payment Journals

• Receipt Journals

Typical Transactions scenarios:

Following scenarios are considering WHT cases

Sales Invoice

Dr Customer 1000

Cr VAT Payable

100

Cr Revenue

1000

Cash receipt

Dr Bank 1000

Dr TDS receivable 100

Cr Customer

1100

Purchase Invoice

Dr Purchases 500

Dr Input VAT 50

Cr Vendor

550

Payment Journal

Dr Vendor 550

Dr WHT Payable 50

Cr Bank

500

Confidential || Not for public circulation P a g e | 15

Mushak form mapping Mushak Forms being studied and design impact to be considered for mapping with various ledgers

and tables:

• 2.1.1

• 2.3

• 4.3.1

• 6.1.1

• 6.2.1

• 6..3

• 6.5.1

• 6.10

• 9.1

Confidential || Not for public circulation P a g e | 16

Annexure

Screen Designs

Report Designs

Mushak Form Designs

• 2.1.1

• 2.3

• 4.3.1

• 6.1.1

• 6.2.1

• 6..3

• 6.5.1

• 6.10

• 9.1

Table relations ERD

Confidential || Not for public circulation P a g e | 17

TAX & VAT calculation Plus invoicing & Journal Entries:

Customer Invoice to be provided by Vendor:

A = Sales

Sl# Particular Amount Formaula

1 Price excl. AIT & VAT 95.00

2 AIT 5.00 =5/(100-5)*D6

3 Price excl. VAT 100.00

4 VAT 15.00 =D8*15%

5 Price incl. AIT & VAT 115.00

Vendor Invoice to be Extracted by Customer:

B = P

urch

ase

Sl# Particular Amount Formaula

5 Price incl. AIT & VAT 115.00

4 VAT 15.00 =15/(100+15)*D15

3 Price excl. VAT 100.00

2 AIT 5.00 =D17*5%

1 Price excl. AIT & VAT 95.00

In Case of Standard Rate & Input tax credit applicable:

Name of Accounts Debit Credit

A. Account Receivable 110

AIT 5

Sales 100

Output VAT 15

Bank 110

Account Receivable 110

Output VAT will be Adjusted with Input VAT

Suppos for this material input VAT was BDT 7:

Then:

(Form

9.1

)

Input output Co-efficient (Form 9.1)

Output VAT at Standard Rate 15

Input VAT -7

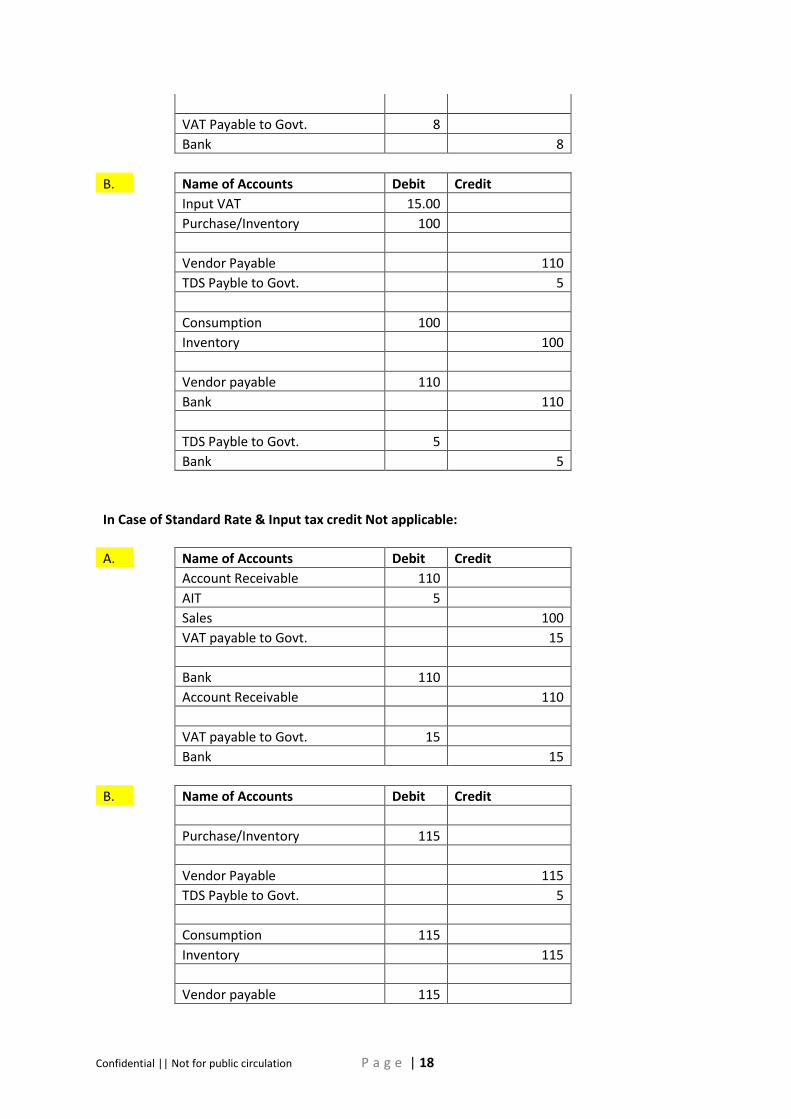

Net Payable to Govt. 8

Name of Accounts Debit Credit

Output VAT 15

Input VAT 7

VAT Payble to Govt. 8

Confidential || Not for public circulation P a g e | 18

VAT Payable to Govt. 8

Bank 8

B. Name of Accounts Debit Credit

Input VAT 15.00

Purchase/Inventory 100

Vendor Payable 110

TDS Payble to Govt. 5

Consumption 100

Inventory 100

Vendor payable 110

Bank 110

TDS Payble to Govt. 5

Bank 5

In Case of Standard Rate & Input tax credit Not applicable:

A. Name of Accounts Debit Credit

Account Receivable 110

AIT 5

Sales 100

VAT payable to Govt. 15

Bank 110

Account Receivable 110

VAT payable to Govt. 15

Bank 15

B. Name of Accounts Debit Credit

Purchase/Inventory 115

Vendor Payable 115

TDS Payble to Govt. 5

Consumption 115

Inventory 115

Vendor payable 115

Confidential || Not for public circulation P a g e | 19

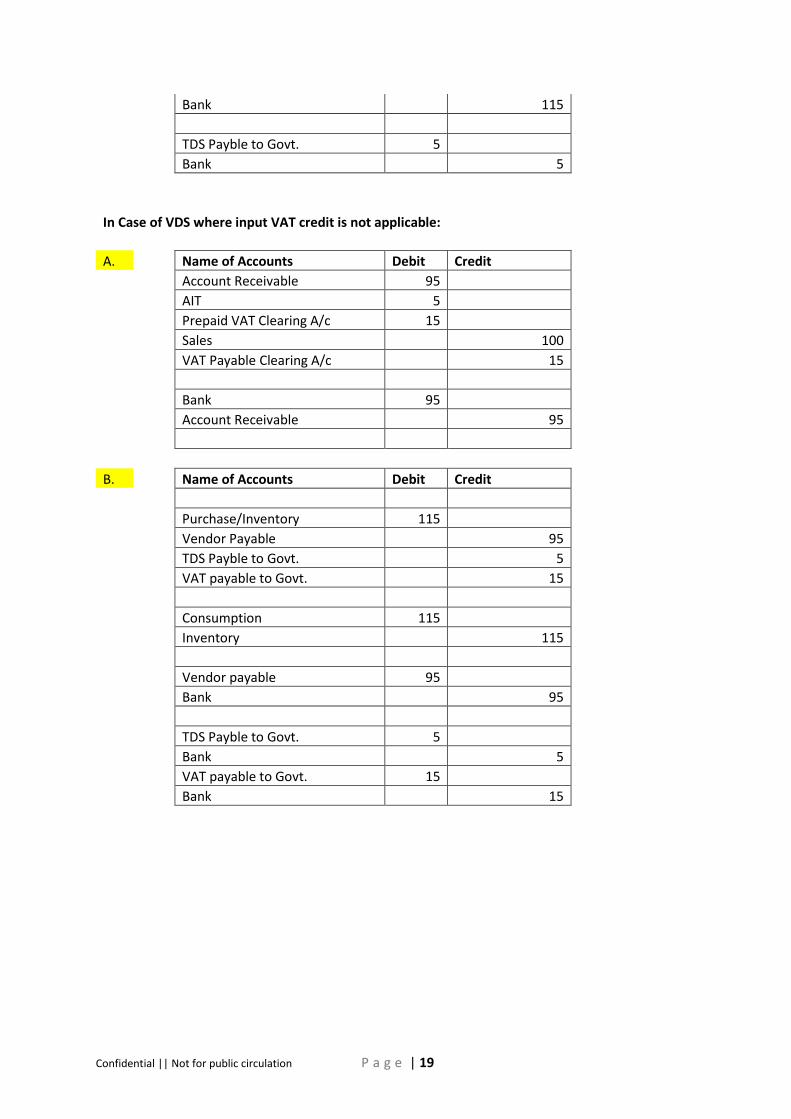

Bank 115

TDS Payble to Govt. 5

Bank 5

In Case of VDS where input VAT credit is not applicable:

A. Name of Accounts Debit Credit

Account Receivable 95

AIT 5

Prepaid VAT Clearing A/c 15

Sales 100

VAT Payable Clearing A/c 15

Bank 95

Account Receivable 95

B. Name of Accounts Debit Credit

Purchase/Inventory 115

Vendor Payable 95

TDS Payble to Govt. 5

VAT payable to Govt. 15

Consumption 115

Inventory 115

Vendor payable 95

Bank 95

TDS Payble to Govt. 5

Bank 5

VAT payable to Govt. 15

Bank 15

Related Documents