Valuation Case Study on Technics Oil & Gas

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Valuation Case Study on

Technics Oil & Gas

Disclaimer and Declaration

The objective of the presentation is for educational

purposes. The full content of the presentation is for

illustration purposes only and should not be used as

investment recommendations. AB Maximus and its

presenters are not responsible for all investment activities

conducted by the participants and cannot be held liable

for any investment loss.

The company and presenters may have personal interest

in the particular shares presented.

Agenda

Company Background 1

Industry Analysis 2

Valuation 3

Risk 4

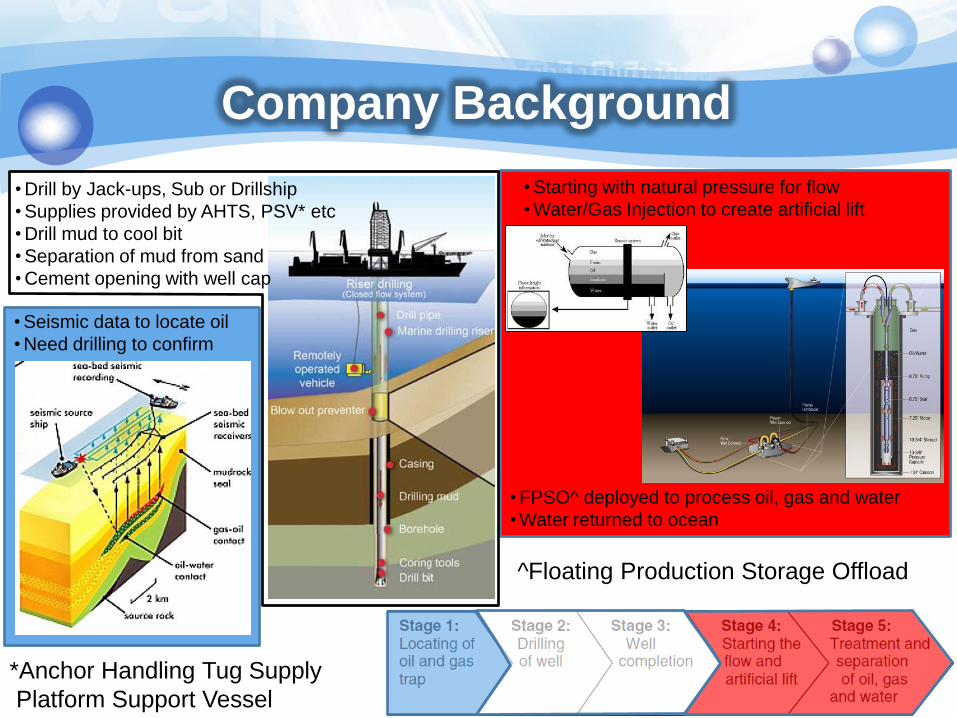

Company Background

Technic Oil & Gas is in

the design and fabrication of process

modules and equipment

that are integrated

to form production and storage facilities for

O&G* exploration and production

Source: Company’s Annual Report 2012 *Oil & Gas

• Seismic data to locate oil

• Need drilling to confirm

• Drill by Jack-ups, Sub or Drillship

• Supplies provided by AHTS, PSV* etc

• Drill mud to cool bit

• Separation of mud from sand

• Cement opening with well cap

• Starting with natural pressure for flow

• Water/Gas Injection to create artificial lift

• FPSO^ deployed to process oil, gas and water

• Water returned to ocean

Company Background

^Floating Production Storage Offload

*Anchor Handling Tug Supply

Platform Support Vessel

Modules Source: Company’s Annual Report 2012

*

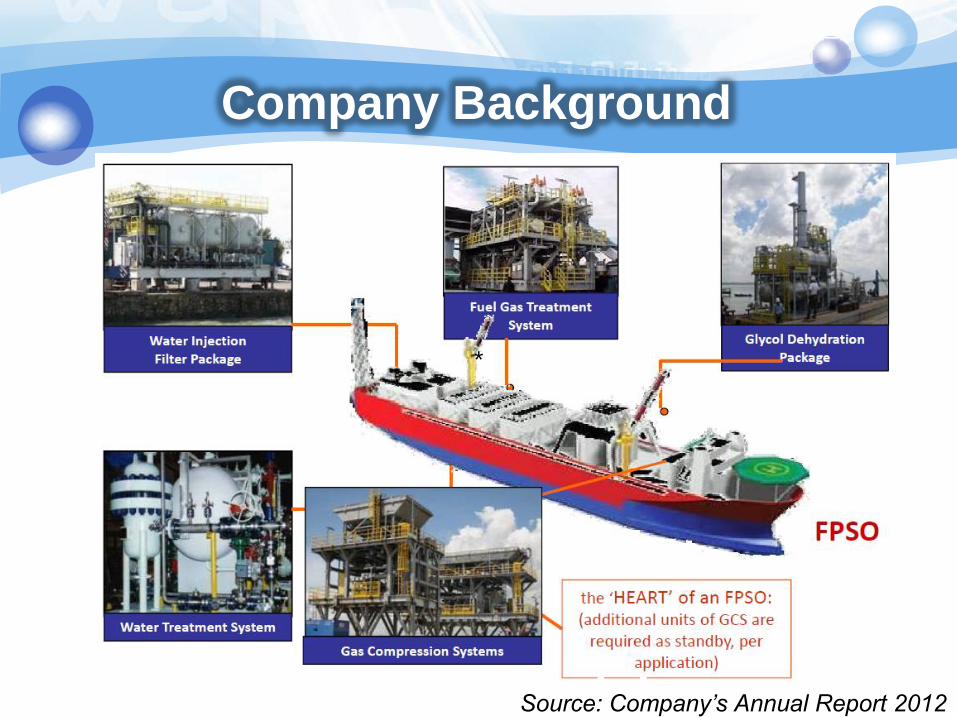

Company Background

Company Background

Source: Company’s Annual Report 2012

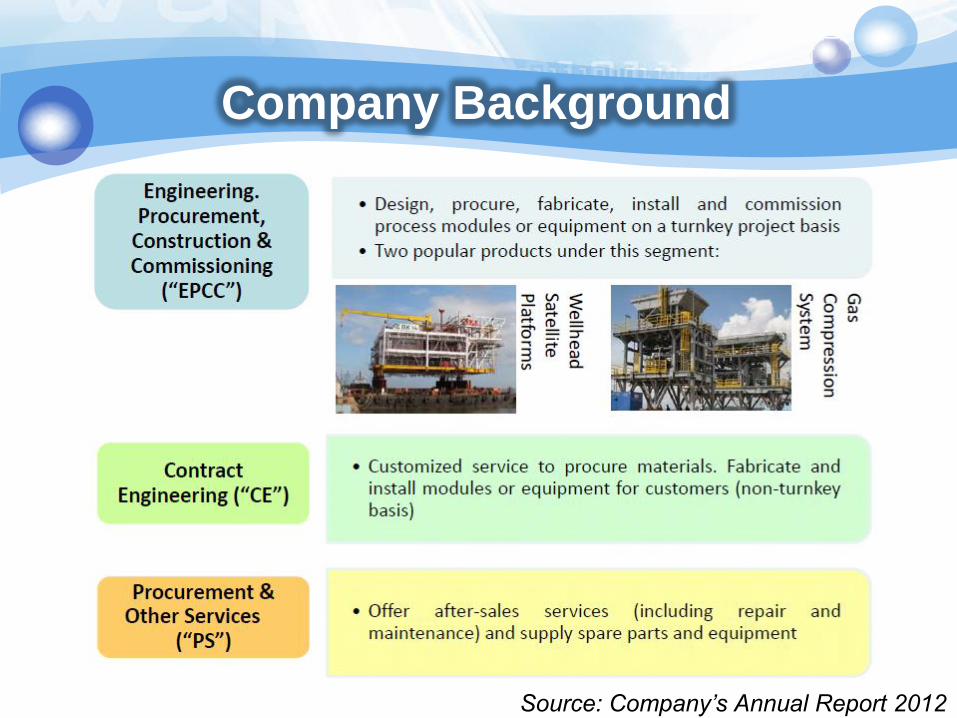

Company Background

Reputable Customer Base

Source: Company’s Annual Report 2012

Company Background

Global Reached

Source: Company’s Annual Report 2012

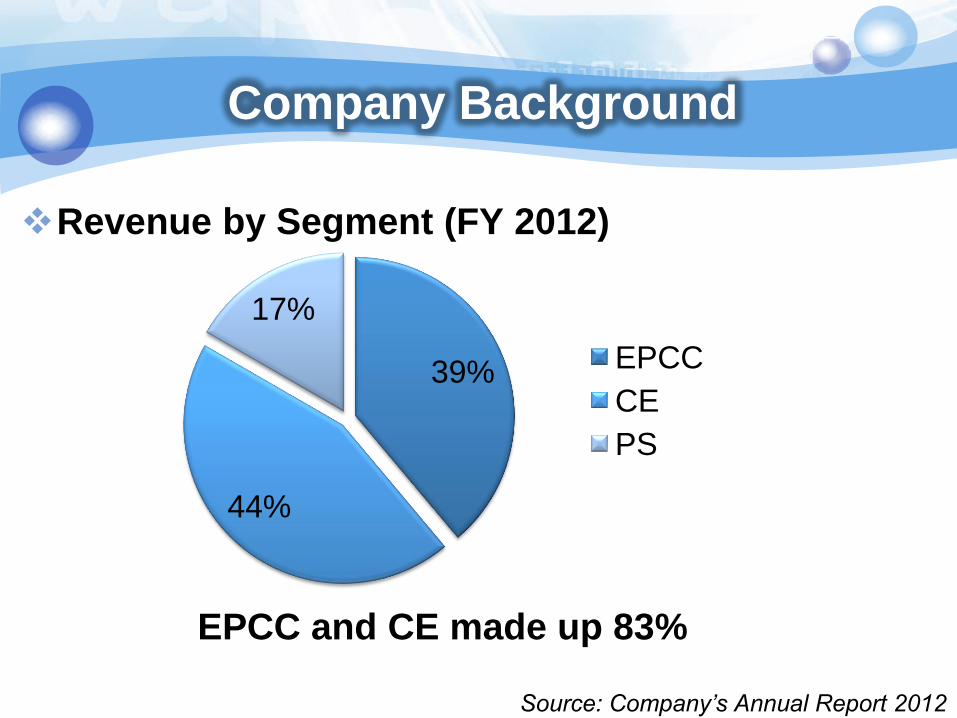

39%

44%

17%

EPCC

CE

PS

Company Background

Revenue by Segment (FY 2012)

EPCC and CE made up 83%

Source: Company’s Annual Report 2012

Company Background

Revenue by Geography (FY 2012)

Mainly in Asean

Source: Company’s Annual Report 2012

22%

52%

26% Singapore

Asean ex Singapore

Others

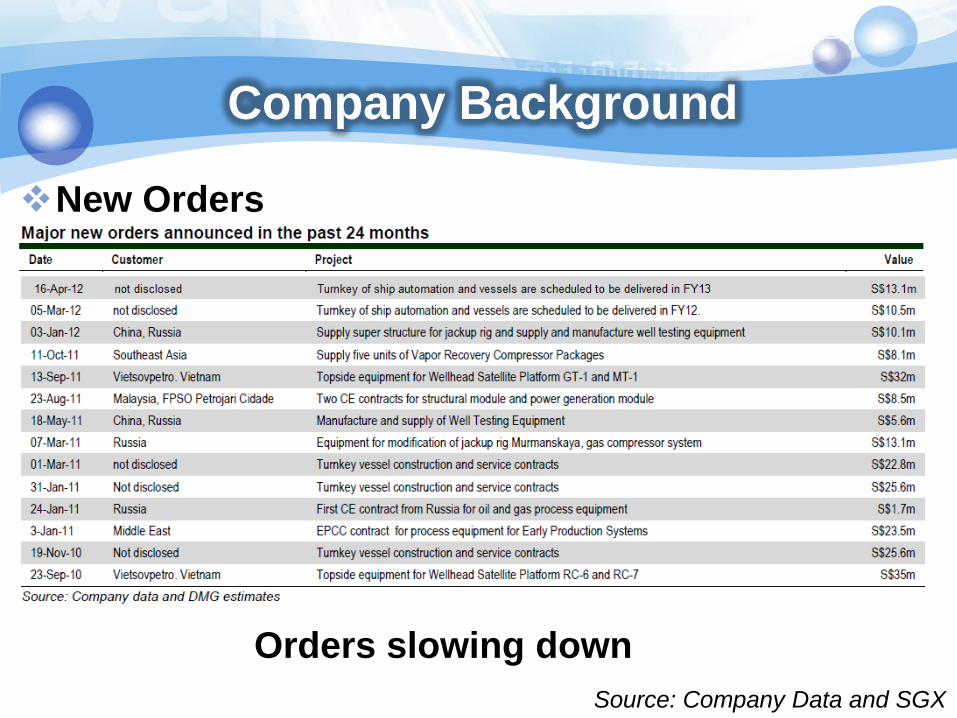

Company Background

New Orders

Orders slowing down

Source: Company Data and SGX

Company Background

Potential synergy with Eversendai

Subcontracting of heavy jacket fabrication

Presence in Malaysia, tapping into Petronas capex

Strong business contact in Middle East

Acquisition of Vietnam yard (VOFE*)

Potential orders from Chevron, which has a 50-fixed-

platform investment plan there over the next 10 years

Source: Company Data and SGX *Vietnam Offshore Fabrication & Engineering Co

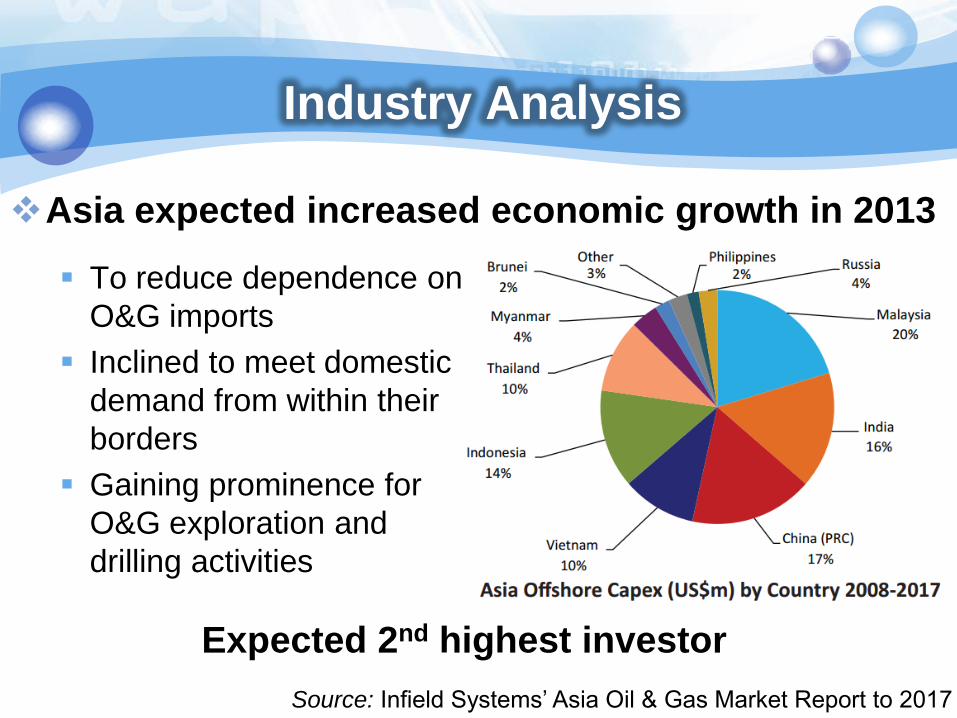

Industry Analysis

To reduce dependence on

O&G imports

Inclined to meet domestic

demand from within their

borders

Gaining prominence for

O&G exploration and

drilling activities

Source: Infield Systems’ Asia Oil & Gas Market Report to 2017

Expected 2nd highest investor

Asia expected increased economic growth in 2013

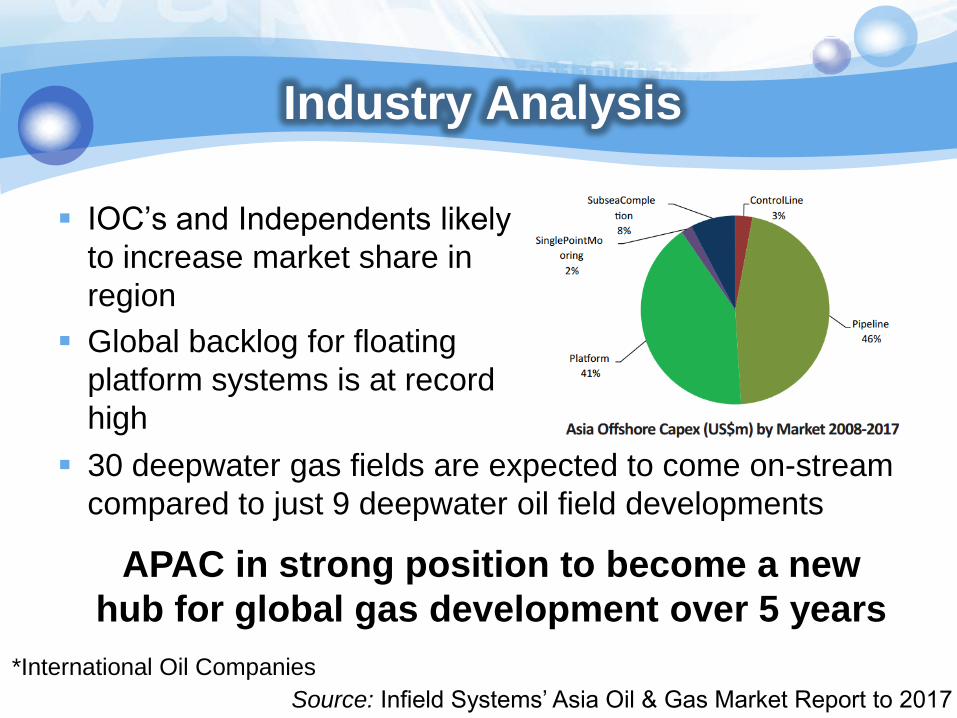

Industry Analysis

IOC’s and Independents likely

to increase market share in

region

Global backlog for floating

platform systems is at record

high

Source: Infield Systems’ Asia Oil & Gas Market Report to 2017

APAC in strong position to become a new

hub for global gas development over 5 years

30 deepwater gas fields are expected to come on-stream

compared to just 9 deepwater oil field developments

*International Oil Companies

Industry Analysis

Source: Company’s Annual Report 2012

O&G CAPEX on the rise

Various key players announced plans to increase

CAPEX over the next few years

BP Plc boost US$27b (2014 – 2020) from US$19.1 in

2011

Indonesia’s Pertamina boost 15% (US$6.7b) in 2013

Malaysia’s Petronas expected to invest US$59b over

next 5 years to position as regional O&G hub

Valuation

Methodology

Discounted Free Cashflow to Firm (FCFF)*

Price to Earnings Ratio (PE)

Dividends Yield

* Project the future FCFF from business and discount to present value

Valuation

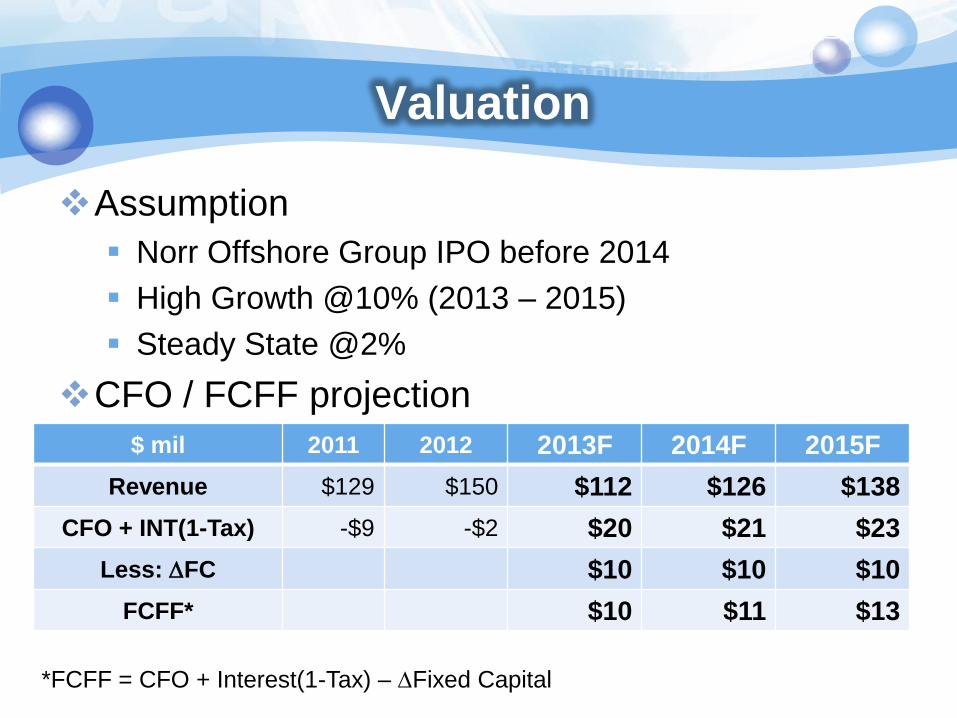

Assumption

Norr Offshore Group IPO before 2014

High Growth @10% (2013 – 2015)

Steady State @2%

CFO / FCFF projection

$ mil 2011 2012 2013F 2014F 2015F

Revenue $129 $150 $112 $126 $138

CFO + INT(1-Tax) -$9 -$2 $20 $21 $23

Less: DFC $10 $10 $10

FCFF* $10 $11 $13

*FCFF = CFO + Interest(1-Tax) – DFixed Capital

Valuation

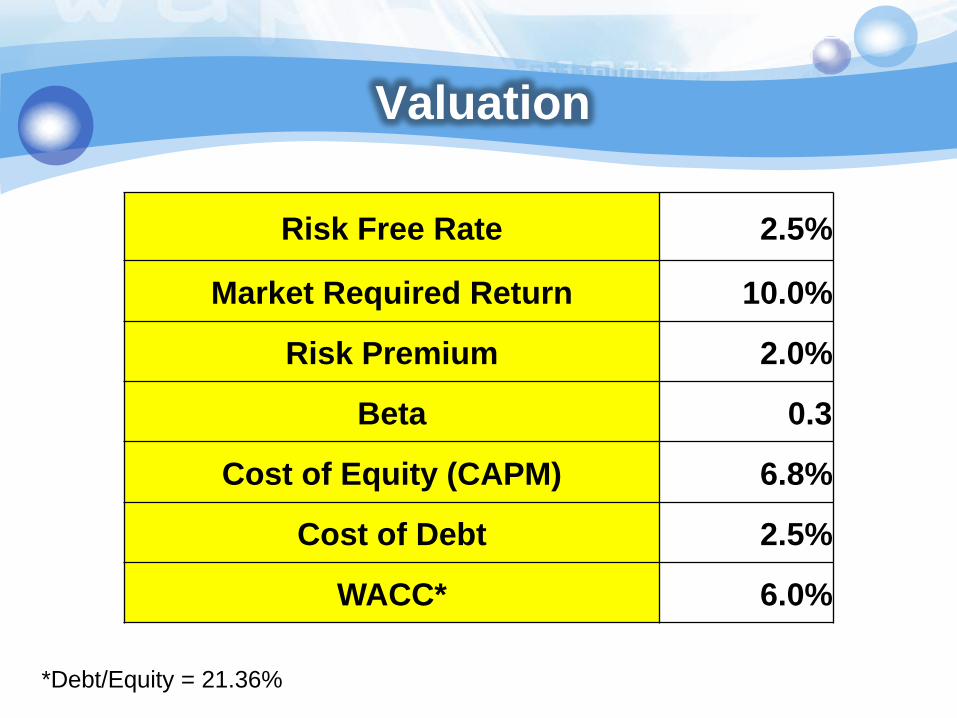

Risk Free Rate 2.5%

Market Required Return 10.0%

Risk Premium 2.0%

Beta 0.3

Cost of Equity (CAPM) 6.8%

Cost of Debt 2.5%

WACC* 6.0%

*Debt/Equity = 21.36%

Valuation

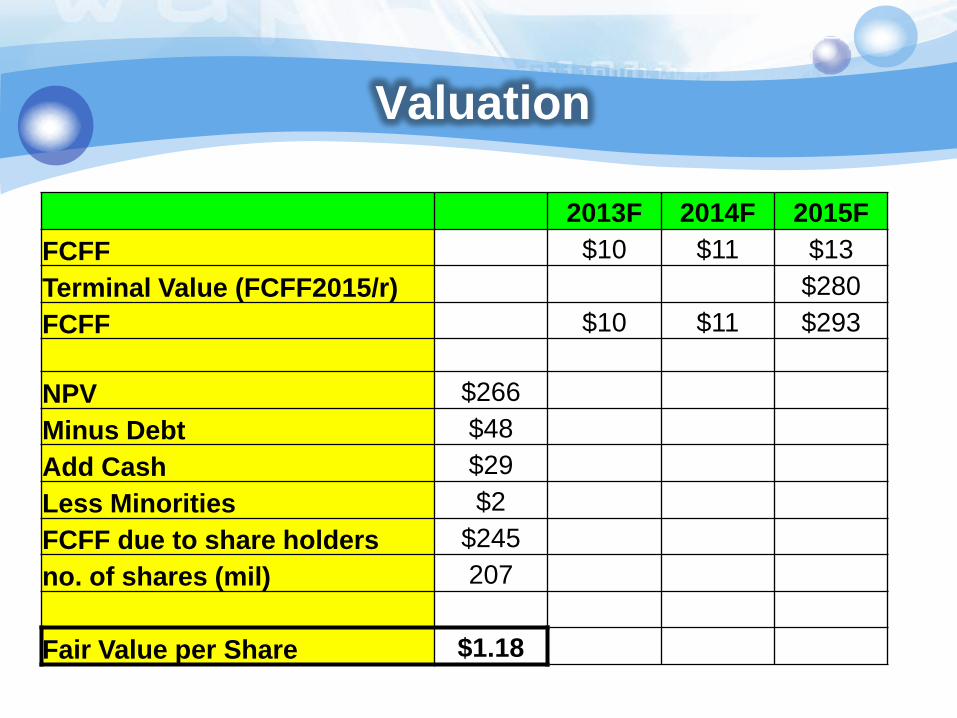

2013F 2014F 2015F

FCFF $10 $11 $13

Terminal Value (FCFF2015/r) $280

FCFF $10 $11 $293

NPV $266

Minus Debt $48

Add Cash $29

Less Minorities $2

FCFF due to share holders $245

no. of shares (mil) 207

Fair Value per Share $1.18

Valuation

FCFF Valuation

Fair Value per share (est. at 1 Jan 2013)

$1.18

Current market value per share (as at 18 Jan 2013)

$1.035

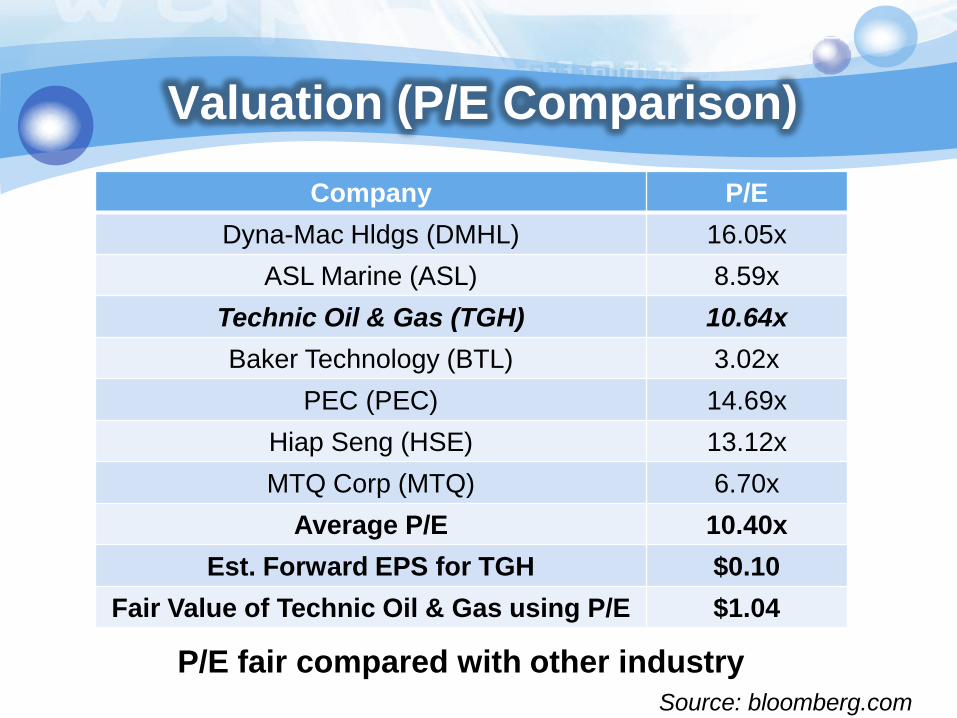

Valuation (P/E Comparison)

Company P/E

Dyna-Mac Hldgs (DMHL) 16.05x

ASL Marine (ASL) 8.59x

Technic Oil & Gas (TGH) 10.64x

Baker Technology (BTL) 3.02x

PEC (PEC) 14.69x

Hiap Seng (HSE) 13.12x

MTQ Corp (MTQ) 6.70x

Average P/E 10.40x

Est. Forward EPS for TGH $0.10

Fair Value of Technic Oil & Gas using P/E $1.04

Source: bloomberg.com

P/E fair compared with other industry

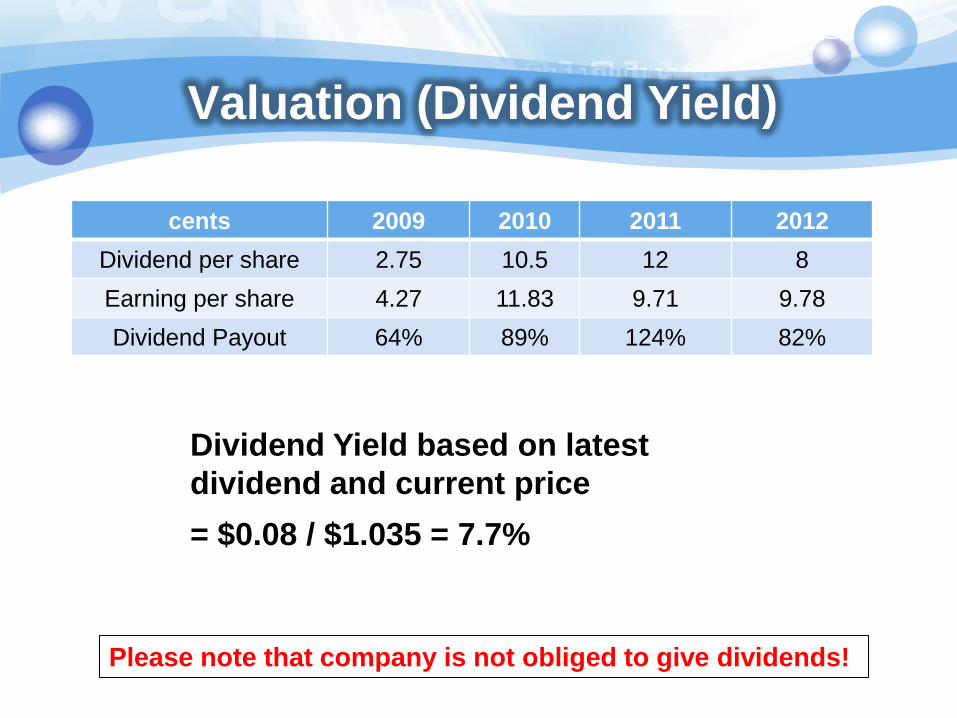

Valuation (Dividend Yield)

cents 2009 2010 2011 2012

Dividend per share 2.75 10.5 12 8

Earning per share 4.27 11.83 9.71 9.78

Dividend Payout 64% 89% 124% 82%

Dividend Yield based on latest

dividend and current price

= $0.08 / $1.035 = 7.7%

Please note that company is not obliged to give dividends!

Trading Data

52 Weeks Trading Range $0.818 - $1.065

Avg Volume (3 mths) 223,000

Market Cap $232 mil

Source: bloomberg.com

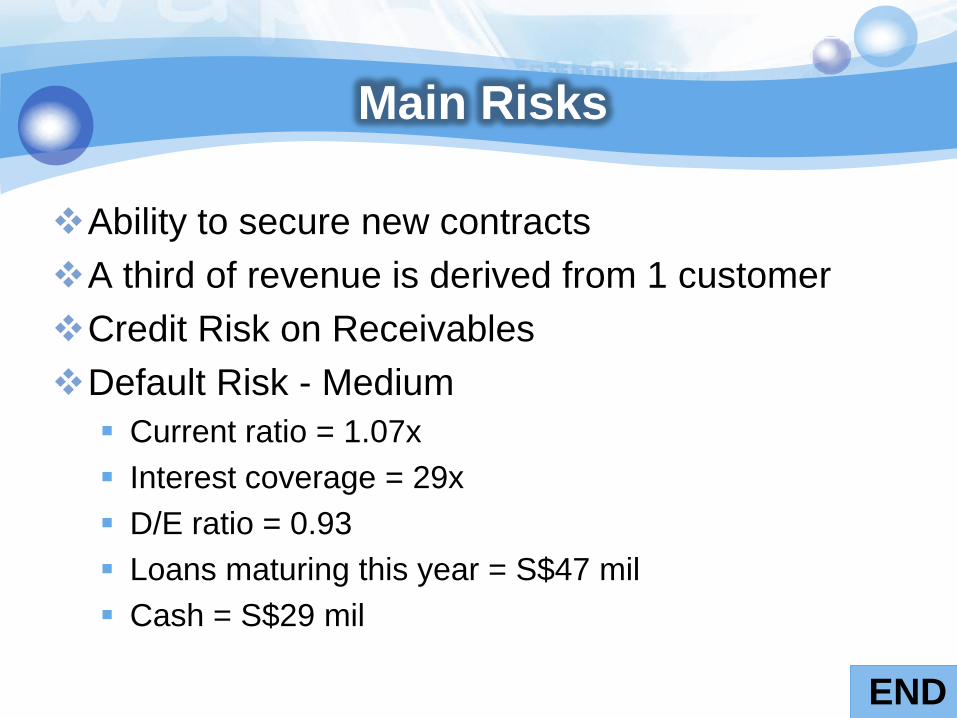

Main Risks

Ability to secure new contracts

A third of revenue is derived from 1 customer

Credit Risk on Receivables

Default Risk - Medium

Current ratio = 1.07x

Interest coverage = 29x

D/E ratio = 0.93

Loans maturing this year = S$47 mil

Cash = S$29 mil

END

Related Documents