169 Validation of SCF Using FVU: After completing the preparation of the SCF using FPU or own back office, NL-OO/NL-AO shall validate the output file with File Validation Utility (FVU) provided by CRA. It is mandatory for NL-OO/NL-AO to validate the file using the latest FVU provided by CRA. Only the SCF which is successfully passed through FVU can be uploaded to NPS-Lite system. NPS-Lite system will reject the file if the same has not passed through latest version of FVU before upload to NPS-Lite system. To validate the SCF through FVU, the user shall double click on the FVU icon at the path where FVU is installed. Once the user clicks on the ’FVU.JAR’, the FVU will open as displayed in below Figure 15: Figure 15 Input File Name with Path 1) NL-OO/NL-AO user shall specify the name (with the .txt extension) of the input file (including the path) i.e. the name of the SCF to be passed through FVU for validation. 2) The Input file name should not contain any special characters e.g., \ / etc and should not exceed 8 characters. 3) The file to be passed through FVU should be in “.txt” format only. 4) User can enter the path or he can select the same by clicking the ‘Browse’ button on the extreme right of the option ‘Input File Name with Path’. Error/Upload & Control Sheet Report File Path 1) User will have to specify the path where either an ‘error files’ or ‘upload file’ along with the control total sheet is to be generated and saved by the FVU on successful completion of validation of the file. It is advisable to use the same path as the input file path. For error file or upload file, User shall only specify the path and should not specify any file name. FVU will provide the name for output file by default. 2) User can enter the path or can select the same by clicking the ‘Browse’ button on the extreme right of the ‘Error/Upload & Control Sheet Report File Path’. 3) It is mandatory for the User to fill both ‘Input File Name with Path’ and Error/Upload & Control Sheet Report File Path’. ‘Validate’ button will remain disabled till both fields are not entered properly.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

169

Validation of SCF Using FVU:

After completing the preparation of the SCF using FPU or own back office, NL-OO/NL-AO shall validate the

output file with File Validation Utility (FVU) provided by CRA. It is mandatory for NL-OO/NL-AO to validate the

file using the latest FVU provided by CRA. Only the SCF which is successfully passed through FVU can be

uploaded to NPS-Lite system. NPS-Lite system will reject the file if the same has not passed through latest

version of FVU before upload to NPS-Lite system.

To validate the SCF through FVU, the user shall double click on the FVU icon at the path where FVU is installed.

Once the user clicks on the ’FVU.JAR’, the FVU will open as displayed in below Figure 15:

Figure 15

Input File Name with Path

1) NL-OO/NL-AO user shall specify the name (with the .txt extension) of the input file (including the path) i.e. the name of the SCF to be passed through FVU for validation.

2) The Input file name should not contain any special characters e.g., \ / etc and should not exceed 8 characters.

3) The file to be passed through FVU should be in “.txt” format only. 4) User can enter the path or he can select the same by clicking the ‘Browse’ button on the extreme right

of the option ‘Input File Name with Path’.

Error/Upload & Control Sheet Report File Path

1) User will have to specify the path where either an ‘error files’ or ‘upload file’ along with the control total sheet is to be generated and saved by the FVU on successful completion of validation of the file. It is advisable to use the same path as the input file path. For error file or upload file, User shall only specify the path and should not specify any file name. FVU will provide the name for output file by default.

2) User can enter the path or can select the same by clicking the ‘Browse’ button on the extreme right of the ‘Error/Upload & Control Sheet Report File Path’.

3) It is mandatory for the User to fill both ‘Input File Name with Path’ and Error/Upload & Control Sheet Report File Path’. ‘Validate’ button will remain disabled till both fields are not entered properly.

170

4) After selecting the input and output folder, User should click the ‘Validate’ button to validate the Subscribers Contribution File. If the file is successfully validated, FVU will show a message as per below Figure 16 and create the output file with extension ‘.fvu’. FVU will also create a control sheet (an HTML report) in the path specified in the ‘Error/Upload File Path’ as shown below.

Figure 16

5) While validating the SCF, FVU will perform the validations as mentioned below: FVU will check whether input file is text file having ‘.txt’ extension. FVU will check whether user has provided all the mandatory details. FVU will check whether the NL-OO, NL-AO, NL-CC Reg. No., PRAN are format level and structurally

correct. FVU will check whether ‘Total Subscriber records’ are equal to the total contribution records for all

the Subscribers. FVU will check whether ‘Subscribers Control Total’ is equal to the sum of Subscribers contributions

for all the subscribers. FVU will check whether ‘Co-contribution Control Total’ is equal to the sum of Co-contributions for

all the subscribers. FVU will validate whether contribution amount is greater than zero (Contribution amount should

not be zero at the same time in Subscriber contribution and co-contribution column) and is not negative.

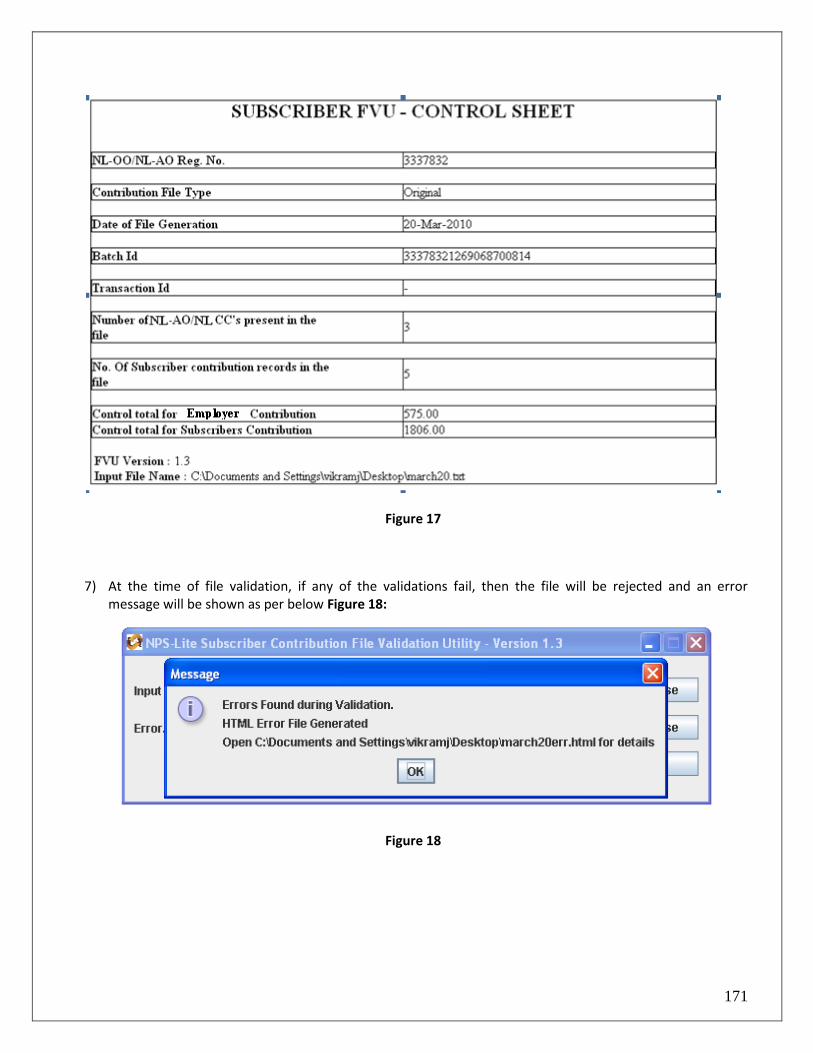

6) On successful validation, FVU will generate an output file with extension “.fvu” at location specified in the field ‘Error/Upload & Control Sheet Report File Path” Along with output file, FVU will also generate an “.html” file showing control totals (No. of Subscriber records, total contribution, etc.) as shown below in Figure 17:

171

Figure 17

7) At the time of file validation, if any of the validations fail, then the file will be rejected and an error message will be shown as per below Figure 18:

Figure 18

172

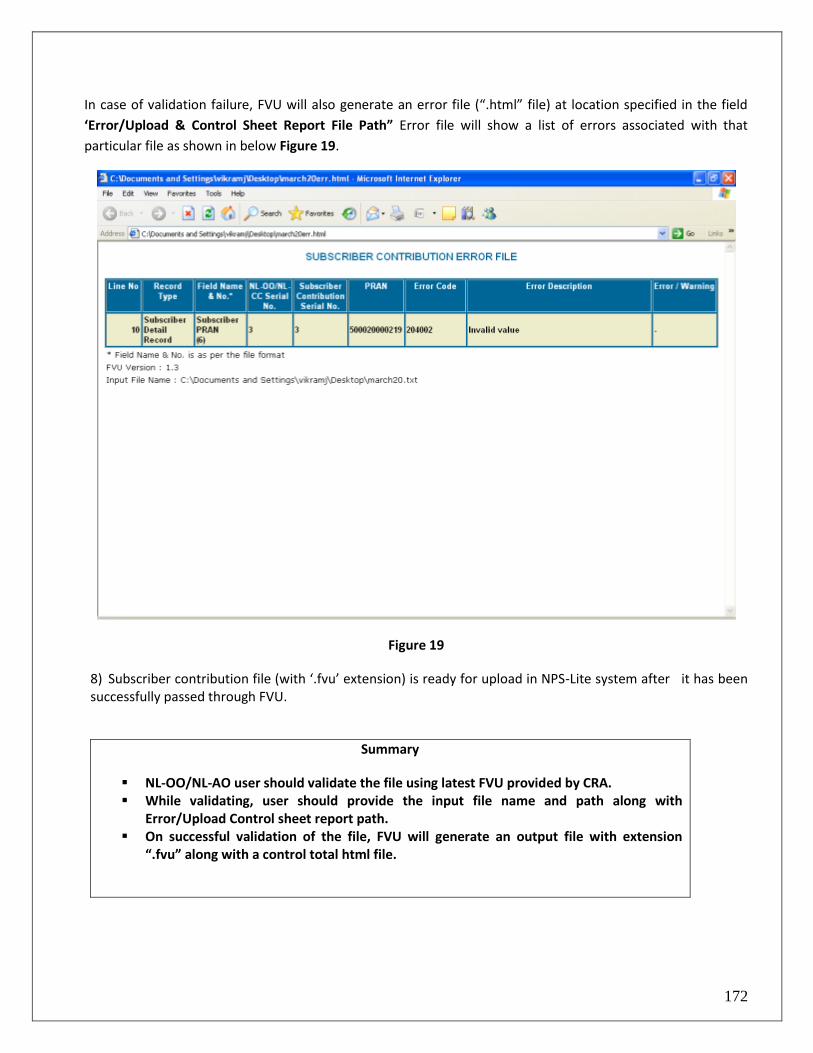

In case of validation failure, FVU will also generate an error file (“.html” file) at location specified in the field

‘Error/Upload & Control Sheet Report File Path” Error file will show a list of errors associated with that

particular file as shown in below Figure 19.

Figure 19

8) Subscriber contribution file (with ‘.fvu’ extension) is ready for upload in NPS-Lite system after it has been successfully passed through FVU.

Summary

NL-OO/NL-AO user should validate the file using latest FVU provided by CRA. While validating, user should provide the input file name and path along with

Error/Upload Control sheet report path. On successful validation of the file, FVU will generate an output file with extension

“.fvu” along with a control total html file.

173

Upload of SCF to NPS-LITE System:

After validating the SCF through FVU, NL-OO/NL-AO shall upload the output file having ‘.fvu’ extension to NPS-Lite system. NL-OO/NL-AO shall upload the file using the user ID and I-Pin allotted by the CRA at the time of NL-OO/NL-AO registration. For all the SCFs uploaded till 18.30 hrs (6:30 PM) in the NPS-Lite system on T (“T “ being the day of upload), system will generate the Transaction id on T+1 day. The transaction id along with the Contribution Submission Form will be visible to the NL-OO/NL-AO which can be download and print. NPS-Lite will generate the transaction id only for the successfully accepted SCFs. NPS Lite Contribution Submission Form will contain NL-AO/NL-OO id, NL-AO/NL-OO address, transaction id, amount to be deposited in the bank etc. This form is to be submitted by the NL-AO/NL-OO to the Trustee Bank while depositing the contribution amount. Note:

If a file is uploaded on T prior to 6:30 pm, then the transaction id will be displayed to the user on T+1 after 10 am. E.g. If the NL-OO/NL-AO has uploaded SCF on 02.04.2010 till 6.30 pm then, transaction id will be displayed on 03.04.2010 after 10.00 am)

If a file is uploaded on T after 6:30 pm, then the transaction id will be displayed to the user on T+2 after 10.00 am. E.g. If the NL-OO/NL-AO has uploaded SCF on 02.04.2010 after 6.30 pm then, transaction id will be displayed on 04.04.2010 after 10.00 am)

Process of upload

1) NL-OO/NL-AO user shall log-in to NPS-Lite system using its user id and I-Pin as password. On accessing the NPS-Lite system, login page will be displayed to the user as shown below in Figure 20:

174

Figure 20

2) On this page, the user shall enter his user id and I-Pin as password for login. If the user id and password provided by the user is valid, home page will be displayed to the user. NL-OO/NL-AO user shall select “Contribution Details – File Upload” option from the menu as shown below in Figure 21 to upload the required SCF.

175

Figure 21

3) On selection of the option “Contribution Details – File Upload”, NPS-Lite will display a screen as shown

below in Figure 22 to upload the files:

176

Figure 22

(Note: If the appropriate configuration of internet explorer and Java J2SE is not installed on the machine, then in

the event of selection “Contribution Details – File Upload option“, no details will be displayed to the user on the

screen.)

4) In the above screen, user shall select the ‘Add Files’ option to add the SCFs to be uploaded. Once user selects ‘Add Files’ button, a window will be displayed as shown below in Figure 23 to select the files to be uploaded. The user shall select the files to be uploaded (with ‘.fvu’ extension) and click on the “Open” button to load the file. User can select multiple files with help of “Ctrl” key as shown below in Figure 23:

177

Figure 23

5) Once the file(s) is loaded, the html will display certain information about the file as mentioned below and shown in Figure 24 below:

i. Serial Number ii. File Name

iii. Path iv. Size of the file and v. The last modified date & time.

178

Figure 24

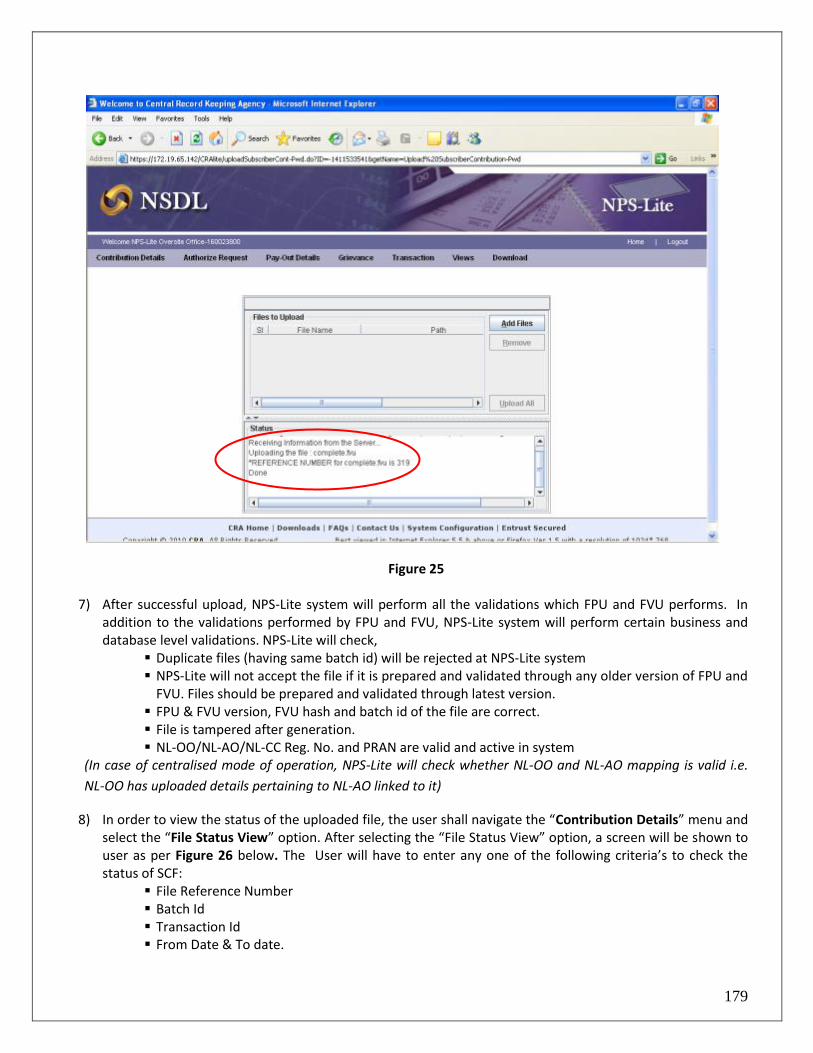

6) Once the file is successfully loaded, the user shall upload the file by clicking on the ’Upload All’ option. If upload of file(s) is successful; NPS-Lite will display the status of the file as ‘Uploaded in NPS-Lite’ and will generate a unique File Reference Number (FRN) which will be displayed to the user as shown below in Figure 25. User may note the FRN for record purpose. User can use this FRN for viewing the status of the file at a later stage.

179

Figure 25

7) After successful upload, NPS-Lite system will perform all the validations which FPU and FVU performs. In addition to the validations performed by FPU and FVU, NPS-Lite system will perform certain business and database level validations. NPS-Lite will check,

Duplicate files (having same batch id) will be rejected at NPS-Lite system NPS-Lite will not accept the file if it is prepared and validated through any older version of FPU and

FVU. Files should be prepared and validated through latest version. FPU & FVU version, FVU hash and batch id of the file are correct. File is tampered after generation. NL-OO/NL-AO/NL-CC Reg. No. and PRAN are valid and active in system

(In case of centralised mode of operation, NPS-Lite will check whether NL-OO and NL-AO mapping is valid i.e.

NL-OO has uploaded details pertaining to NL-AO linked to it)

8) In order to view the status of the uploaded file, the user shall navigate the “Contribution Details” menu and select the “File Status View” option. After selecting the “File Status View” option, a screen will be shown to user as per Figure 26 below. The User will have to enter any one of the following criteria’s to check the status of SCF:

File Reference Number Batch Id Transaction Id From Date & To date.

180

Figure 26

Once the user provides sufficient details, the status of the uploaded file will be shown to user as per Figure 27

below.

181

Figure 27

9) If the all the validations are successful, NPS-Lite will update the status of the file as “Accepted” and will generate a unique 13 digit Transaction id (unique acknowledgement number generated by NPS-Lite for SCF). Along with the other details, the system will also display Batch id and the remark as “Awaiting Fund Details” as shown below in Figure 28.

182

Figure 28

10) Along with Transaction id, NPS-Lite system will also generate the Contribution Submission Form (CSF) as shown below in Figure 29 for successfully accepted files. NL-OO/NL-AO shall click on the hyperlink provided at ‘View’ under Subscriber Contribution Submission Form as shown in above Figure 28 in order to view the details of the CSF. NL-OO/NL-AO shall download and print the Contribution Submission Form.

11) The CSF will contain NL-OO/NL-AO Reg. No., address, transaction id, amount to be deposited in the bank, etc and a counterfoil for Trustee Bank to issue acknowledgement to NL-OO/NL-AO. This form is to be submitted by the NL-OO/NL-AO to the Trustee Bank while depositing the contribution amount. In case NL-OO/NL-AO intends to transfer the funds through RTGS/NEFT instruction, he may refer to Point No. _______ of this document. NL-OO/NL-AO may print an additional copy for its record purpose. A prototype of this form is given below in Figure 29.

183

Figure 29

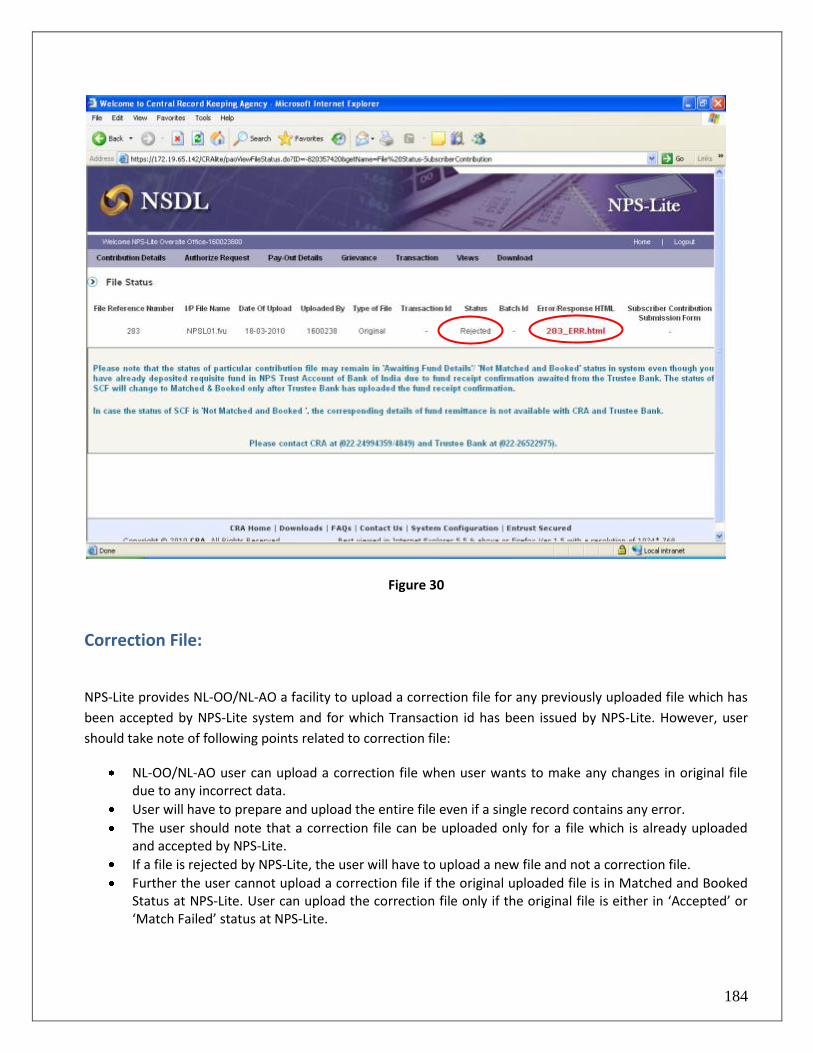

Rejection of SCF:

If the file validation is not successful due to reasons such as invalid PRAN, invalid FPU version, invalid NL-OO/NL-AO mapping etc, NPS-Lite will reject the file and will update the status of the file as “Rejected” as shown below in Figure 30. NPS-Lite system will also generate an error file containing the reasons for rejection. NL-OO/NL-AO can view and download this error file from NPS-Lite, by providing the FRN at the time of viewing the status of the SCF uploaded. NPS-Lite will not generate the transaction id for such rejected files as shown below in Figure 29.

.

184

Figure 30

Correction File:

NPS-Lite provides NL-OO/NL-AO a facility to upload a correction file for any previously uploaded file which has

been accepted by NPS-Lite system and for which Transaction id has been issued by NPS-Lite. However, user

should take note of following points related to correction file:

NL-OO/NL-AO user can upload a correction file when user wants to make any changes in original file due to any incorrect data.

User will have to prepare and upload the entire file even if a single record contains any error.

The user should note that a correction file can be uploaded only for a file which is already uploaded and accepted by NPS-Lite.

If a file is rejected by NPS-Lite, the user will have to upload a new file and not a correction file.

Further the user cannot upload a correction file if the original uploaded file is in Matched and Booked Status at NPS-Lite. User can upload the correction file only if the original file is either in ‘Accepted’ or ‘Match Failed’ status at NPS-Lite.

185

Procedure for preparation and validation of correction file

For preparing the correction file using FPU, the user has to first select the type of contribution file as

“Correction” and mention the transaction id in the field provided. The user should note that the transaction id

is mandatory in case, type of contribution file is ‘Correction’. The correction file is to be prepared and validated

on the same lines as a regular file using FPU & FVU. The entire file will be rejected if the transaction id of the

original file for which the correction file is being uploaded is not mentioned. The view given to the user will be

as shown in the Figure 31 below:

Figure 31

Procedure for upload of correction file:

For uploading the correction file into NPS-Lite, the user has to the follow the same procedure that was adopted

to upload a regular file. In case of a correction file upload, NPS-Lite will perform the following additional

validations:

1) For correction file, NPS-Lite will check for the existence of the Original Transaction id which is provided in the file. In case transaction id doesn’t exist in the NPS-Lite system, the NPS-Lite will reject the correction file.

186

2) NPS-Lite will check the status of the original file. If the original file is in ‘Matched and Booked’ status, NPS-Lite will reject the correction file.

3) No new Transaction id will be generated for successful upload of correction file. System will accept the same transaction id for correction file.

4) In case the correction file is processed successfully, it will replace the previous file for which the correction file is uploaded. The status of the earlier file will be changed to “Cancelled”.

5) On successful acceptance of correction file, NPS-Lite will generate the contribution submission form. The User shall download and print this form and submit the same to Trustee Bank along with the Contribution amount.

6) The Transaction id of the original file will be used to track the file. 7) In case the correction file is processed successfully in NPS-Lite system, NPS-Lite will mark the status of this

correction file as ‘Accepted’ as shown in figure 32 below.

Figure 32

187

Summary

NL-OO/NL-AO user can upload a correction file when user wants to make any changes in original file due to any incorrect data

If a file is rejected by NPS-Lite, the user will have to upload a new file and not a correction file.

Cannot upload a correction file if the original uploaded file is in Matched and Booked Status at NPS-Lite

No new Transaction id will be generated for successful upload of correction file

Correction file is processed successfully, it will replace the previous file for which the correction file is uploaded

Transaction id of the original file will be used to track the file

Transfer of Funds to Trustee Bank:

6.1. Deposit of Contribution amount in Trustee Bank:

Once the file has been successfully uploaded and CSF generated, the NL-OO/NL-AO shall take a print of the CSF.

The user shall submit the CSF at the Trustee Bank along with the contribution amount as appearing in the CSF.

The NL-OO/NL-AO user has to ensure that the following activities are performed before submitting the CSF to

the Trustee Bank:

1) The CSF should be printed and the relevant blank fields (e.g. payment details) should be filled. The user may print an additional copy for its record and future reference.

2) If the mode of payment is through cheque or DD, the user has to mention in the CSF the Cheque / DD number, the date of the cheque/DD and the name of the bank, branch from where the cheque/DD has been drawn.

3) The amount deposited by the user should be exactly equal to the amount mentioned in the CSF. If NL-OO/NL-AO deposits an incorrect amount, then the trustee bank shall not accept the same.

4) The user has to ensure that the counterfoil of the CSF is given by the Trustee Bank, as the same should be maintained as an acknowledgement for record purpose and future reference in case of any discrepancy.

5) In case fund confirmation file is not uploaded by Trustee Bank within T+4 days (T being the day of upload to NPS-Lite), an email alert will be sent to NL-OO/NL-AO from the CRA. On receipt of the alert, NL-OO/NL-AO shall contact the Trustee Bank for upload of the fund confirmation file.

Transfer of funds through Electronic Fund Transfer (NEFT/RTGS):

NL-OO/NL-AO can also transfer the funds to the Trustee Bank using electronic fund transfer facility such as

NEFT/RTGS. While transferring the funds electronically, NL-OO/NL-AO should provide the following details to

the Remitting Bank (which initiates the NEFT/RTGS transfer instruction):

188

NPS Trust Account number

IFSC of NPS Trust Account

NL-OO/NL-AO Reg. No.

Transaction id

The amount to be transferred should be equal to amount in SCF for the Transaction id mentioned above. NL-

OO/NL-AO should ensure that the Remitting Bank provides the details of NL-OO/NL-AO Reg. No. and

Transaction id along with the NEFT/RTGS instruction to the Trustee Bank. This information should be provided

in the field 7495 (Sender to receiver information, line no. 4) of RTGS message (R-41) for RTGS transfers. For

NEFT transfers, this information should be provided in the field 7002 (Origination of remittance) of the NEFT

message.

In the absence of the above information, Trustee Bank will not be in a position to upload the fund receipt

details to the CRA. In such cases, the money shall be transferred to the PFM for investment but posting to the

Subscribers’ account will take place only after the exact details of the fund transferred are submitted to the TB.

NL-OO/NL-AO should track the status of the contribution and follow up with the Trustee Bank if the payment

details are not reflecting in the NPS Lite system.

6.3. Tracking the status of contribution amount transferred to Trustee Bank

The NL-OO/NL-AO user can check in the NPS-Lite system whether trustee bank has uploaded the details to

NPS-Lite for the receipt of contribution amount from NL-OO/NL-AO. To check the details uploaded by bank,

user will have to view the status of the uploaded file in NPS-Lite system by entering the file reference number

through “File Status View” as shown in figure 26 and will press submit button. Once the user provides

sufficient details, the status of the uploaded file will be shown to user as per Figure 29. The file status view

contains a hyperlink on batch id. By clicking on hyperlink, complete uploaded details of the file will be displayed

along with the file details. NPS-Lite system will also show the corresponding amount uploaded by the trustee

bank. If the amount of SCF is matching with Fund receipt confirmation file (FRC) uploaded by bank, then the

status of the file will be shown as ‘Matched and Booked’ as shown below in Figure 33:

189

Figure 33

In case the file is in “Match Failed” status, NL-OO/NL-AO should check whether the amount transferred to

Trustee Bank is matching with the amount mentioned in SCF. If the amount transferred is same, NL-OO/NL-AO

should intimate the Trustee Bank for resolving the discrepancy. Trustee Bank then shall upload a file with

corrected records.

*Note: - NL-OO/NL-AO must ensure that the status of the file on NPS-Lite system is matched and booked

after the funds are transferred to the trustee bank. In case FRC has not been uploaded and the file status is

not showing ‘matched and booked’ status within the stipulated period of T+4 working days, the NL-OO/NL-

AO and the TB must reconcile immediately.

190

Summary

NL-OO/NL-AO shall deposit the total amount as per Contribution Submission Form at the Trustee Bank.

If funds are transferred through electronic transfer such as NEFT/RTGS, NL-OO/NL-AO should ensure NL-OO/NL-AO Reg. No. and Transaction ID is provided by Initiating Bank (Accredited Bank of NL-OO/NL-AO) in the electronic instruction.

NL-OO/NL-AO shall receive an email alert if fund confirmation receipt is not uploaded by Trustee Bank within three days of deposit.

NL-OO/NL-AO should follow up with the Trustee Bank where status of SCF is shown as ‘Match Failed’ in the NPS-Lite.

Summary of Activities

1) Receipt of NPS contributions from the Subscribers. 2) Consolidation of Subscriber contribution details by the NL-OO/NL-AO. 3) Preparation of contribution files using latest version of FPU/Back-office. 4) Validation of the file through latest version of FVU.

5) Upload of the validated file to NPS-Lite system. 6) Track the status of files uploaded in NPS-Lite. 7) Upload fresh (new) files, in case the files are rejected at NPS-Lite 8) Printing of contribution submission form (CSF). 9) Deposit of contribution amount with the CSF at the Trustee Bank. 10) Co-ordination with Trustee Bank in case the FRC is not uploaded within three days of submission of CSF on

receipt of alert from NPS Lite.

********************************************************

191

Annexure 10 - Flyer for NPS Lite

192

193

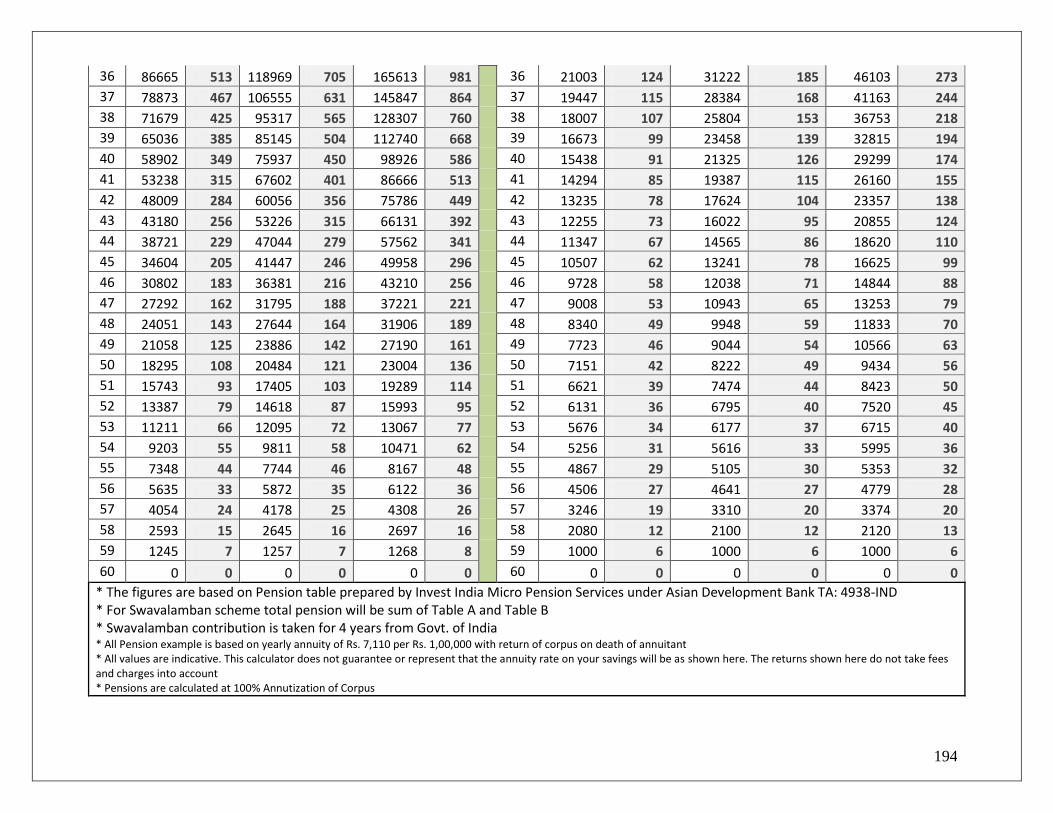

Annexure 11 – Return Calculator

Table A: Corpus and Monthly Pension

Table B: Swavalamban Corpus and Monthly Pension

Subscribers Contribution 100 GoI's Yearly Contribution Amount (for 4 years) 1000

Co-Contribution 0 Total Monthly Contribution 100

Age

Corpus at

Monthly

Pension at

Corpus at

Monthly

Pension at

Corpus at Monthly

Pension at

Age

Swavalamban

Corpus at

Swavalamban

Monthly Pension

at

Swavalamban

Corpus at

Swavalamban

Monthly Pension at

Swavalamban

Corpus at

Swavalamban

Monthly Pension

at

8% 8% 10% 10% 12% 12% 8% 8% 10% 10% 12% 12%

18 412049 2441 774430 4588 1496511 8867 18 83928 497 173594 1029 354529 2101

19 379321 2247 699886 4147 1326952 7862 19 77711 460 157812 935 316544 1876

20 349101 2068 632408 3747 1176477 6971 20 71954 426 143466 850 282628 1675

21 321197 1903 571326 3385 1042938 6179 21 66624 395 130423 773 252347 1495

22 295431 1750 516034 3058 924429 5477 22 61689 366 118567 703 225310 1335

23 271640 1609 465983 2761 819259 4854 23 57120 338 107788 639 201169 1192

24 249672 1479 420676 2493 725925 4301 24 52889 313 97989 581 179615 1064

25 229388 1359 379664 2250 643096 3810 25 48971 290 89081 528 160371 950

26 210659 1248 342539 2030 569589 3375 26 45343 269 80983 480 143188 848

27 193365 1146 308933 1830 504356 2988 27 41985 249 73621 436 127847 757

28 177396 1051 278513 1650 446465 2645 28 38875 230 66928 397 114149 676

29 162651 964 250976 1487 395090 2341 29 35995 213 60843 360 101919 604

30 149036 883 226049 1339 349496 2071 30 33329 197 55312 328 90999 539

31 136464 809 203485 1206 309035 1831 31 30860 183 50284 298 81249 481

32 124856 740 183059 1085 273127 1618 32 28574 169 45713 271 72544 430

33 114138 676 164570 975 241261 1429 33 26457 157 41557 246 64771 384

34 104241 618 147834 876 212981 1262 34 24498 145 37779 224 57831 343

35 95103 563 132683 786 187885 1113 35 22683 134 34345 203 51635 306

194

36 86665 513 118969 705 165613 981 36 21003 124 31222 185 46103 273

37 78873 467 106555 631 145847 864 37 19447 115 28384 168 41163 244

38 71679 425 95317 565 128307 760 38 18007 107 25804 153 36753 218

39 65036 385 85145 504 112740 668 39 16673 99 23458 139 32815 194

40 58902 349 75937 450 98926 586 40 15438 91 21325 126 29299 174

41 53238 315 67602 401 86666 513 41 14294 85 19387 115 26160 155

42 48009 284 60056 356 75786 449 42 13235 78 17624 104 23357 138

43 43180 256 53226 315 66131 392 43 12255 73 16022 95 20855 124

44 38721 229 47044 279 57562 341 44 11347 67 14565 86 18620 110

45 34604 205 41447 246 49958 296 45 10507 62 13241 78 16625 99

46 30802 183 36381 216 43210 256 46 9728 58 12038 71 14844 88

47 27292 162 31795 188 37221 221 47 9008 53 10943 65 13253 79

48 24051 143 27644 164 31906 189 48 8340 49 9948 59 11833 70

49 21058 125 23886 142 27190 161 49 7723 46 9044 54 10566 63

50 18295 108 20484 121 23004 136 50 7151 42 8222 49 9434 56

51 15743 93 17405 103 19289 114 51 6621 39 7474 44 8423 50

52 13387 79 14618 87 15993 95 52 6131 36 6795 40 7520 45

53 11211 66 12095 72 13067 77 53 5676 34 6177 37 6715 40

54 9203 55 9811 58 10471 62 54 5256 31 5616 33 5995 36

55 7348 44 7744 46 8167 48 55 4867 29 5105 30 5353 32

56 5635 33 5872 35 6122 36 56 4506 27 4641 27 4779 28

57 4054 24 4178 25 4308 26 57 3246 19 3310 20 3374 20

58 2593 15 2645 16 2697 16 58 2080 12 2100 12 2120 13

59 1245 7 1257 7 1268 8 59 1000 6 1000 6 1000 6

60 0 0 0 0 0 0 60 0 0 0 0 0 0

* The figures are based on Pension table prepared by Invest India Micro Pension Services under Asian Development Bank TA: 4938-IND * For Swavalamban scheme total pension will be sum of Table A and Table B * Swavalamban contribution is taken for 4 years from Govt. of India * All Pension example is based on yearly annuity of Rs. 7,110 per Rs. 1,00,000 with return of corpus on death of annuitant * All values are indicative. This calculator does not guarantee or represent that the annuity rate on your savings will be as shown here. The returns shown here do not take fees and charges into account * Pensions are calculated at 100% Annutization of Corpus

195

Annexure 12 – FAQs on NPS Lite/Swavalamban

Updated on 24th Dec 2010

1. What is NPS Lite? Answer: NPS Lite is a model specifically designed to bring NPS within easy reach of the economically

disadvantaged sections of the society. NPS Lite is extremely affordable and viable due to its optimized functionalities available at reduced charges.

2. What are the key differences between NPS and NPS Lite?

Answer: NPS Lite model broadly has similar functionalities as the regular NPS model. However, some of the services would not be available at individual subscriber level directly; instead these services would be provided at Aggregator level and the individual can avail of those services through aggregators.

3. Who is an Aggregator?

Answer: Aggregator is the point of interaction between its underlying subscriber and the NPS Lite architecture. Aggregator shall perform the functions relating to registration of subscribers, undertaking Know Your Customer (KYC) verification, receiving contributions and instructions from subscribers and transmission of the same to designated NPS Lite intermediaries. Entities only approved by PFRDA would act as Aggregator in NPS Lite for their underlying subscribers.

4. Who is eligible to be an aggregator?

Answer: The entities desirous of taking on the role of aggregator must meet the eligibility criteria prescribe by PFRDA under the Regulations for Aggregators under NPS Lite 2010. Broadly the criteria’s are: Must be registered under an act/law of Central or state government Must have constituent mass for NPS Lite and have established capability with proven

track record in the area of their operation. Must be financially viable and have formal governance structure Must meet prescribed net worth criteria Must have capability to manage large customer databases suitable to their

organisation and must meet other technology parameters and cash management capabilities prescribed by PFRDA

*PFRDA may, at its discretion, relax some, or all of these eligibility criteria on a case to case basis, in the initial stages of development of the sector. For details on eligibility conditions, please refer section 9 of Regulations for Aggregators under NPS Lite 2010, available on www.pfrda.org.in

5. How is aggregator enlisted?

Answer: Any institution/ organization intending for registration as Aggregator under NPS Lite is required to submit a Letter of Consent to PFRDA, in the prescribed format. Prescribed format can be downloaded from PFRDA website www.pfrda.org.in. The details submitted would be evaluated by PFRDA on case to case basis. PFRDA will issue Appointment letter to the selected entity, based on which an Aggregator would execute Agreement with Central Record Keeping Agency (CRA). Selected entity would then proceed through prescribed registration process with CRA and post registration entity would be eligible to operate under NPS Lite.

196

6. What are the roles and responsibilities of aggregator? Answer: The aggregators shall be responsible for:

a) Promotion of NPS and awareness about the need for old age income security among its constituent group members.

b) Meeting the ‘Know Your Customer’ requirements in respect of potential NPS subscribers as mandated under AML/CFT requirements.

c) KYC requirements in case of NPS Lite subscribers shall be governed by provisions of RBI Master Circular no RBI/2008-09/72 dated July 01, 2008 and as amended from time to time till separate orders on this aspect are issued by PFRDA.

d) Discharge of responsibilities relating to fund and data upload within prescribed time limits. e) Collection of contributions from subscribers and ensuring its passage to Trustee Bank. f) Ensuring availability of services including distribution of Annual Statement of Transactions and

showing online statements to its underlying subscribers as mandated under NPS-Lite. g) Handling grievances received from subscribers and their resolution. h) Any other responsibility as assigned to them by PFRDA to ensure protection of subscribers’

interest.

7. Where are the CRA-FCs located? Answer: CRA-FC is the facilitation centre appointed by CRA for the purpose of accepting the application

for allotment of PRANs. Details of CRA-FC are available at NSDL website www.nsdl.co.in and CRA website www.npscra.nsdl.co.in. Aggregator/NL-AO shall submit Subscriber Registration Form to CRA-FC and If no CRA-FC is available at the city where Aggregator/NL-AO is located, it may visit the CRA-FC at any nearby city.

8. Is it mandatory to get oversight office, account office and collection centre get registered? Answer: Yes, it is mandatory for oversight office, account office and collection centre get registered.

However, if required a single office can be registered for more than one role. For ex:

NL-OO will register itself with CRA and also facilitate the registration of the underlying NL-AOs.

NL-CCs which are attached to the NL-AO will forward the completed registration forms to the concerned NL-AO.

197

For the purpose of NL-CC registration, NL-AO shall collect the NL-CC registration forms, certify the details and forward it to CRA.

9. Can the aggregator, oversight office, account office and collection centre registration forms be

modified? Answer: No the registration forms are prescribed by PFRDA and can’t be modified.

10. What infrastructure and capacity is required for an oversight office and collection centre? Answer: NL-OO/NL-AO should have the following software/hardware as a minimum requirement to

access NPS-Lite system.

Software Environment (Pre-requisites for installation of FPU & FVU)

Software Minimum Requirement

Browser Internet Explorer 6.0 and above

Java Run Time

Environment

JRE 1.5 downloadable freely from www.java.com

Operating Systems Windows 2000 Professional / Windows XP

With the software environment as indicated in the table above, the NL-OO/NL-AO shall install FPU (File Preparation Utility) & FVU (File Validation Utility) on a desktop machine whose minimum hardware requirements are provided in the following table.

Hardware Environment (Pre-requisites)

Hardware Minimum Requirement

Processor Intel Pentium IV / Celeron (2.66 GHz or Higher CPU).

Memory Minimum 512 MB RAM.

11. How much security deposit aggregator has to deposit?

Answer: Aggregators shall provide Security deposit to PFRDA as per below table

198

12. What is the process of depositing security deposit? Answer: Each entity enlisted as an aggregator shall have to submit a security deposit to PFRDA, in the form of a demand draft or a bank guarantee from a scheduled commercial bank.

13. Whom should aggregator contact for any information on Swavalamban/NPS Lite? Answer: Based on nature of information required, aggregator can approach PFRDA or CRA (NSDL) Mumbai office.

14. Is it compulsory for all workers enrolled with aggregator to join NPS Lite? Answer: It would depend upon the Aggregators arrangement with its underlying subscribers; however Swavalamban/NPS Lite is voluntary in nature.

15. What is Permanent Retirement Account Number (PRAN)? Answer: It is 12 digits unique Permanent Retirement Account Number allotted by CRA to each

Subscriber registered in NPS-Lite system.

CRA will print and dispatch to the NL-AO, the PRAN Kit for the newly registered subscribers. The PRAN Kit will contain the PRAN card, Subscriber master details and an information leaflet on NPS-Lite.

16. After registration when does subscriber receives PRAN card?

Answer: Within 20 days of submission of application, the subscriber receives PRAN Card though NL-CC.

17. When a subscriber joins NPS Lite, is he automatically becomes eligible for Swavalamban scheme? Answer: The Swavalamban scheme is applicable only to those persons who has provided Swavalamban

declaration during registration and are eligible as per “Swavalamban guidelines” Issued by Ministry of Finance vide F.No. 13/1O/2006-PR dated 18th June 2010. For details refer www.pfrda.org.in

18. Can the subscriber registration form be modified? Answer: Yes, the subscriber registration form can be modified based on inputs from subscriber.

19. Is it mandatory for subscriber to have a bank account? Answer: Bank Account is optional at the time of Subscriber Registration. However it is mandatory to

have bank account at the time of withdrawal.

20. How much minimum and maximum a subscriber can contribute in the scheme? Answer: Minimum contribution amount at the time of Registration - Rs 100. Though there is no

Minimum contribution requirement per year, however minimum of Rs 1000 contribution per year is recommended. Those desirous of availing Swavalamaban scheme of Govt. of India must invest at least Rs 1000 during the year and maximum of Rs. 12000. The maximum investment limit prescribed by RBI vide their master circular number RBI/2008-09/72 dated 1st July 2001 for “ Small Deposit Accounts” shall be applicable for each NPS account opened under NPS Lite, till PFRDA prescribes separate limits.

199

21. If a subscriber has Provident Fund contribution but does not declare it, can he/she still avail the Swavalamban Scheme? Answer: At the time of joining the NPS, the subscriber has to declare whether he/she falls within the

definition of Unorganised sector as defined in Para 3 of “Swavalamban Scheme – Operational Guidelines” and would also declare that his contribution would range between Rs. 1,000 to Rs. 12,000 per annum. If subsequent to opening the NPS account, it is found that the subscriber has made a false declaration about his eligibility for the benefits under this scheme or has been wrongly given the benefit of government contribution under this scheme for whatever reason, the entire government contribution will be deducted along with penal interest as may be specified from time to time If the status of the subscriber changes to ineligible after joining the NPS, he/ she should immediately declare so and the benefit of government contribution will not accrue to the subscriber's account after the date on which the subscriber becomes ineligible

22. If a subscriber availing Swavalamban Scheme finds a regular job in a Government institution, can

he/she continue transacting in the Swavalamban Account? Answer: If the status of the subscriber changes to ineligible after joining the NPS, he/ she should

immediately declare so and the benefit of government contribution will not accrue to the subscriber's account after the date on which the subscriber becomes ineligible

23. What is centralized and decentralized mode of operation for data and fund transfer?

Answer: At the time of registration, Aggregator shall have to specify the ‘Model of Operation’ it intends to adopt, in NL-OO registration form. An Aggregator can adopt any one of the following Model of Operations.

a) Centralised Model:

Under this Model, NL-OO shall prepare a consolidated NL-AO wise subscriber contribution file. NL-OO shall collect the details of the contributions received and upload the same in the NPS Lite system. NL-OO shall also make one consolidated payment to the trustee bank for the contributions accepted.

b) Decentralised Model:

Under this Model, each NL-AO shall prepare subscriber contribution file based on contributions received and upload the same into NPS Lite system. NL-AO shall also make payment related to contribution accepted to the trustee bank.

24. What is transaction id and its relevance? Answer: It is unique ID generated by the NPS Lite system on successful acceptance of subscriber

contribution form (SCF). In NPS Lite system transaction id would be generated on the next day of contribution upload.

25. What is the time line to upload data in system? Answer: Timelines are as depicted below:

200

26. What is the time line to deposit contribution in bank? Answer: Same as above

27. By when the aggregator will get confirmation of data upload from CRA-Lite? Answer: Same as above

28. By when the aggregator will have to upload the fund info in CRA system? Answer: Same as above

29. What is the process to transfer fund to trustee bank? Answer: If the mode of payment is through cheque/DD, the NL-OO/NL-CC has to mention in the CSF

the Cheque/DD number, the date of the cheque/DD and the name of the bank, branch from where the cheque/DD has been drawn. The amount deposited by the NL-OO/NL-CC should be exactly equal to the amount mentioned in the CSF.

NL-OO/NL-AO can also transfer the funds to the Trustee Bank using electronic fund transfer facility such as NEFT/RTGS.

30. What tools/utilities/standards are developed or prescribed under NPS Lite?

Answer: To facilitate the digitization and consolidation of the pension contribution details of the Subscribers, CRA has developed a utility called File Preparation Utility (FPU). It is a JAVA based utility which can be easily installable on a desktop machine. For ease of use, the utility is based on the MS Excel format. There is a separate FPU for NL-OO and NL-AO.

31. Can these tools/utilities be downloaded from CRA website?

201

Answer: NL-OO/NL-AO can freely download the FPU from CRA website www.npscra.nsdl.co.in available at Download/Software download/Utilities.

32. Is it mandatory to use FPU/FVU? Answer: Aggregator may use the File Preparation Utility (FPU) provided by CRA or use its own back

office software (which shall generate the required files as per format prescribed by CRA) for preparation of SCF. In either case, the file generated should be validated using the File Validation Utility (FVU). The FPU and FVU tools will be made available for download from the CRA website.

33. How and in what duration aggregator and subscriber will receive his/her contribution statement? Answer: Annual account statement will be send once in a year in printed form to aggregator.

Aggregator would further distribute it to its underlying subscribers.

34. What is charge structure under NPS Lite? Answer: NPS Lite offers Indian citizens a low cost option for planning their retirement. Charge structure under NPS is as follows:

Intermediary Activity Charges Method of Deduction

Central Record Keeping Agency (CRA)

Account Opening Charges

Rs. 35/- ( Digitization will be carried out by CRA – FC)

Through cancellation of units from each subscriber pension account

Annual Maintenance Charges1

Rs. 70/- per annum with 12 free subscriber contributions per financial year.

Transaction Charges2

Nil for first 12 transactions and Rs. 5/- per transactions beyond 12 free subscriber contributions in each year

Trustee Bank

Per transaction emanating from a Non RBI location3

Rs. 15 (Trustee Bank, levies collection charges of Rs. 15 per transaction for collection of funds, only at Non RBI Centers)

Through NAV deduction

Custodian4 (On asset value in custody)

Asset Servicing Charges

0.0075% p.a for Electronic segment & 0.05% p.a for Physical Segment

Through NAV deduction

PFM Investment Management Fee5

0.0009% p.a (PFMs get a fee of Rs 90,000 for every Rs.1000 crores of corpus they manage.

Through NAV deduction

202

35. What are the charges levied by the Aggregator for providing the NPS-Lite services?

Answer: The aggregators are not authorized to collect any sum from the subscribers towards their own fee/service charges.

36. When does the Annual Maintenance charge of Rs.70 get deducted every year? Answer: Annual Maintenance Charges will be deducted through cancellation of subscriber units at the

end of each quarter. 37. Is the Annual Maintenance Charge of Rs.70 applicable once the Pension (annuity) payouts begin?

Answer: Subscriber will not be charged any Annual Maintenance charges once the Annuity payout begins.

38. Rs.70 is charged per year as Account Maintenance Charges. What would happen to the Account if there is not enough money in it to cover the charges? Answer: Account will become dormant and no transaction will be allowed.

39. What is “subscriber acquisition cum retention model”? Answer: Under subscriber acquisition cum retention model, the remuneration shall be based on a “per

capita sum” paid for each subscriber enrolled during the year and all those accounts (enrolled in previous years) which remained active during the year. Each account enrolled and retained during the year must have a minimum annual contribution of Rs 1000/- in each account for making the aggregator eligible for remuneration. The “per capita sum” shall be uniform and fixed by PFRDA from time to time. This sum for the FY 2010-11 shall be Rs 50/- per eligible NPS Lite account.

40. What is the charge/commission sharing ratio between aggregator and approved “Facilitator under NPs Lite” or a “consortium” in partnership with a private entity? Answer: The terms of engagement, level of service and fees for the same shall be negotiated between

the aggregator and PoP/facilitator and settled between them. PFRDA shall not be responsible for such arrangement(s) and the aggregator in this case shall not be entitled to receive any additional remuneration other than that prescribed under regulations.

41. What will happen when the subscriber stops depositing money in account? Answer: If the subscriber stops depositing contribution to scheme then 20% of the pension wealth may

be withdrawn as lump sum and he would be required to invest at least 80% of the pension wealth to purchase a life annuity from any IRDA – regulated life insurance company.

42. Can a relative/friend of the subscriber deposit money into the Subscriber’s NPS-Lite A/c using the PRAN, through the SAME aggregator within India? Answer: Yes. Anybody on behalf of Subscriber can deposit money with the Aggregator.

203

43. Can a registered subscriber deposit contribution through any Aggregator using same PRAN? Answer: At present, subscriber can deposit the contribution through the same Aggregator only where

he/she registered.

44. How can a subscriber get the pension (annuity) payouts?

Answer: Pension payout to the subscriber is as per the table below.

45. If the subscriber dies after couple of years of contribution, who gets the right to receive the money accumulated? Answer: In such an unfortunate event, option will be available to the nominee to receive 100% of the

NPS pension wealth in lump sum. However, if the nominee wishes to continue with the NPS, he/she shall have to subscribe to NPS individually after following prescribed procedure.

46. Can a subscriber withdraw contribution before the age of 60? If yes, what percentage/amount? Answer: Subscriber can withdraw contribution before the age of 60; however he would be required to

invest at least 80% of the pension wealth to purchase a life annuity from any IRDA – regulated life insurance company. Maximum 20% of the pension wealth may be withdrawn as lump sum.

Vesting Criteria Benefit

At any point in time before 60 years of Age

You would be required to invest at least 80% of the pension wealth to purchase a life annuity from any IRDA – regulated life insurance company. Rest 20% of the pension wealth may be withdrawn as lump sum.

On attaining the Age of 60 years and upto 70 years of age

At exit you would be required to invest minimum 40 percent of your accumulated savings (pension wealth) to purchase a life annuity from any IRDA-regulated life insurance company.

You may choose to purchase an annuity for an amount greater than 40 percent. The remaining pension wealth can either be withdrawn in a lump sum on attaining the age of 60 or in a phased manner, between age 60 and 70, at the option of the subscriber.

Death due to any cause In such an unfortunate event, option will be available to the nominee to receive 100% of the NPS pension wealth in lump sum. However, if the nominee wishes to continue with the NPS, he/she shall have to subscribe to NPS individually after following due KYC procedure.

204

47. Upon death of Subscriber, what is the procedure if the Nominee is not eligible to be an NPS-Lite Subscriber? Answer: In such case, Nominee will receive 100% of the NPS pension wealth in lump sum. Option to

continue with the NPS in individual capacity will not available to the nominee.

48. If a subscriber is in dire need of money but has another 5 years to cover to become 60 yrs of age, is there any way the lock-in period can be reduced so that the money may be accessed? Answer: Subscriber can withdraw 20% of the pension wealth as lump sum anytime before attaining age

of 60

49. How is grievance registered? Answer: Call Centre/Interactive Voice Response System (IVR)

Aggregator on behalf of its underlying subscriber can contact the CRA call centre at toll free telephone number 1-800-222080 and register the grievance. Aggregator/NL-AO will have to authenticate itself through the use of T-pin allotted at the time of registration under the NPS Lite. On successful registration of the grievance, a token number will be allotted by the Customer Care representative for any future reference.

Web based interface Aggregator on behalf of its underlying subscriber can register the grievance at the website www.npscra.nsdl.co.in with the use of the I-pin allotted at the time of registration under the NPS Lite. On successful registration, a token number will be displayed on the screen for future reference. Physical forms Subscribers can submit the grievance against their Aggregator in a prescribed format to CRA, who would forward it to PFRDA for resolution. The form prescribed is available on CRA website. Subscriber can also raise grievance against NL-AO/NL-OO in physical forms. CRA/NPS-Lite will compile all such grievances received from the subscribers and forward the same to PFRDA for necessary action. This will not be part of the NPS-Lite system and token number will not be generated for such grievances but the process will be outside the system.

50. How can subscriber track his submitted grievance against aggregator / CRA?

Answer: NL-AO can login to the NPS-Lite system and view the status of logged grievance. The NL-AO can search on the screen based on either the token number or the date range. The system will display the status of the grievance along with the details. For the resolved grievance, resolution details will also be shown. Aggregator can check the status of the grievance at the CRA website www.npscra.nsdl.co.in or through the Call Centre by mentioning the token number. Aggregator can also raise a reminder through any one of the modes mentioned above by specifying the original token number issued.

205

Section B – Swavalamban under NPS -

Unorganized Model

Annexure 1 – Offer Document

206

NATIONAL PENSION SYSTEM (NPS)

OFFER DOCUMENT (FOR BOTH TIER-I AND TIER –II)

NPS Pension nahi yeh Pran hain

207

NATIONAL PENSION SYSTEM THE REGULATOR Pension Fund Regulatory & Development Authority THE NPS TRUST

THE CENTRAL RECORDKEEPING AGENCY (CRA) National Securities Depository Limited (NSDL) THE CUSTODIAN Stock Holding Corporation of India Limited THE TRUSTEE BANK Bank of India

THE PENSION FUNDS (in alphabetical order)

ICICI Prudential Pension Funds Management Company Limited

IDFC Pension Fund Management Company Limited

Kotak Mahindra Pension Fund Limited

Reliance Capital Pension Fund Limited

SBI Pension Funds Private Limited

UTI Retirement Solutions Limited

POINTS OF PRESENCE (in alphabetical order)

Abhipra Capital Limited

Alankit Assignments Ltd

Allahabad Bank

Axis Bank Ltd.

Bajaj Capital Ltd.

Central Bank of India

Citibank N.A

Computer Age Management Services Pvt. Ltd.

ICICI Bank Limited

ICICI Securities Ltd

IDBI Bank Limited

IL &FS Securities Services Ltd

India Post NPS Nodal Office

Integrated Securities Ltd

Kotak Mahindra Bank Limited

Marwadi Shares and Finance Limited

Muthoot Finance Limited

Oriental Bank of Commerce

Reliance Capital Limited

State Bank of Bikaner and Jaipur

State Bank of Hyderabad

208

State Bank of India

State Bank of Indore

State Bank of Mysore

State Bank of Patiala

State Bank of Travancore

Steel City Securities Ltd

Stock Holding Corporation Of India Ltd

Syndicate Bank

The South Indian Bank Ltd.

Union Bank of India

UTI Asset Management Company Limited

UTI Technology Services Ltd.

Yes Bank Ltd

Zen Securities Limited

APPLICANT SHOULD NOTE THAT:

This Offer Document sets forth concisely the information about NPS that an applicant ought to know. Applicant should carefully read the Offer Document.

This Offer Document remains effective until a material change occurs. Material changes will be notified by Pension Fund Regulatory and Development Authority (PFRDA) to all subscribers.

PFRDA has been established to promote old age income security by establishing, developing and regulating pension funds, to protect the interests of subscribers to schemes of pension funds and for matters connected therewith or incidental thereto.

NPS, regulated by PFRDA, is a defined contribution pension system which is now being offered on voluntary basis to all citizens of India other than government employees covered by NPS.

209

Table of Contents

Abbreviations and Definitions ...............................................................................................................................211

Abbreviations ...........................................................................................................................................................211

Definitions ................................................................................................................................................................211

NPS Features ............................................................................................................................................................212

Who can join? ..........................................................................................................................................................212

Who cannot join? .....................................................................................................................................................212

How to enroll in the NPS? ........................................................................................................................................212

How much does a subscriber need to contribute? ..................................................................................................213

What are the benefits of joining the NPS? ..............................................................................................................213

When can a subscriber withdraw the amount? .......................................................................................................214

Tax Benefits ..............................................................................................................................................................215

What investment choice does the subscriber have? ...............................................................................................215

Charges .....................................................................................................................................................................217

Other Matters ..........................................................................................................................................................218

Power to make guidelines and give directions ........................................................................................................218

Investment Guidelines .............................................................................................................................................218

NPS ARCHITECTURE .................................................................................................................................................219

PFRDA .......................................................................................................................................................................219

NPS Intermediaries ..................................................................................................................................................220

NPS Trust ..................................................................................................................................................................220

Functions of NPS Trust .............................................................................................................................................220

Services provided by CRA to Subscribers .................................................................................................................221

Functions of Trustee Bank........................................................................................................................................221

Functions of POP ......................................................................................................................................................224

SERVICES TO SUBSCRIBERS ......................................................................................................................................225

Terms & Conditions ..................................................................................................................................................226

Risks..........................................................................................................................................................................226

EXPLANATORY NOTE ON SPECIFIC RISKS IN DEBT MARKETS AND CAPITAL MARKETS ............................................226

210

Risks associated with Debt / Money Markets (i.e. Markets in which Interest bearing Securities or Discounted

Instruments are traded) ...........................................................................................................................................226

Risks associated with Capital Markets or Equity Markets (i.e. Markets in which Equity Shares or Equity oriented

instruments are issued and traded) .........................................................................................................................228

NPS - TIER- II account .....................................................................................................................................................228

Table summarizing the main features of Tier-II account .........................................................................................229

211

Abbreviations and Definitions In this Offer Document, the following words and expressions shall have the meaning specified below, unless the context otherwise requires:

Abbreviations ASP Annuity Service Provider

CGMS Centralised Grievance Management System

CRA Central Recordkeeping Agency

DC Defined Contribution

GRC Grievance Redressal Cell

GRM Grievance Redressal Mechanism

IMA Investment Management Agreement

IPO Initial Public Offer

KYC Know your Customer

NPS National Pension System

NRA Normal Retirement Age

PFs/PFMs Pension Funds/Pension Fund Managers

PFRDA Pension Fund Regulatory and Development Authority

POP Point of Presence

POP-SP Point of Presence – Service Provider (Authorized branches of POP for NPS)

PRA Permanent Retirement Account

PRAN Permanent Retirement Account Number

TB Trustee Bank

FEMA Foreign Exchange Management Act

Definitions Applicable NAV

Unless stated otherwise in the Offer Document, 'Applicable NAV' is the Net Asset Value at the close of a Working Day.

Applicant An individual who has expressed interest in joining NPS and has duly completed all formalities.

Custodian Agency responsible for holding assets of the NPS Trust. Refers to the Stockholding Corporation of India Limited (SHCIL)

IMA Investment Management Agreement, entered into between NPS Trust and the Pension Funds .

Offer Document

This document, issued by PFRDA, making an offer to potential applicants to subscribe to NPS.

RBI Reserve Bank of India, established under the Reserve Bank of India Act, 1934.

Subscriber An individual who has become a member of the NPS

Unit holder Subscriber is also referred to as unit holder with respect to the units he/she owns.

Trust Deed The Trust Deed entered into between the NPS Trust and PFRDA, as amended up to date, or as may be amended from time to time.

Trust Fund The corpus of the Trust and all property belonging to and/or vested in the Trustees.

Working Day A day other than any of the following (i) Saturday or Sunday; (ii) a day on which banks including the Reserve Bank of India are closed for business or clearing and (iii) a day on which the Purchase and Redemption of Units is suspended.

212

NPS Features Pension Fund Regulatory and Development Authority (PFRDA) has been established by the Government of India, Ministry of Finance vide Notification F.No.5/7/2003-ECB & PR dated 10th October, 2003 to promote old age income security. The Government authorized PFRDA vide Ministry of Finance, Department of Financial Services letter No. 11(11)/2008-PR dated 29th July 2008 to extend NPS on a voluntary basis to all citizens of India including workers of the unorganized sector. NPS is now available to all citizens of India with effect from May 1, 2009, other than Government employees already covered under NPS. Under NPS following two types of accounts will be available to you:

Tier-I account: You shall contribute your savings for retirement into this non-withdrawable account.

Tier-II account: This is a voluntary savings facility. You will be free to withdraw your savings from this account whenever you wish.

While Tier-I account is available from May 1, 2009, the facility of Tier II account is offered from December 1, 2009 to all citizens of India including Government employees mandatorily covered by NPS. The details mentioned in this offer document pertain to both Tier-I & Tier II accounts. For details of Tier-II please see page – 15 Who can join? A citizen of India, whether resident or non-resident, subject to the following conditions:

You should be between 18 – 60 years of age as on the date of submission of his/her application to the POP/ POP-SP.

You should comply with the Know Your Customer (KYC) norms as detailed in the Subscriber Registration Form. The Subscriber Registration form attached with this Offer Document should be duly filled-in by the applicant and all terms and conditions mentioned therein should be duly complied with. All the documents required for KYC compliance need to be mandatorily submitted.

Who cannot join? The following applicants cannot join:

Undischarged insolvent: Individuals who are not granted an 'order of discharge' by a court.

Individuals of unsound mind: An individual is said to be of unsound mind for the purposes of making a contract if, at the time when he makes it, he is incapable of understanding it and of forming a rational judgment regarding its effect upon his/ her self-interest.

Pre-existing account holders under NPS. How to enroll in the NPS? To enroll in the NPS, you need to submit the attached Registration Form (UOS-S1) to the POP-SP of your choice. The list of POP – SPs is available on the PFRDA website www.pfrda.org.in, on the CRA website www.npscra.nsdl.co.in and on the website of the concerned POP. You may also contact the POPs listed at page10 of this offer document. NRIs should have an account with a bank based in India to open an account under NPS. The contributions made by the NRI would be subject to regulatory requirements as prescribed by RBI from time to time and FEMA requirements. After the account is opened, CRA shall mail a “Welcome Kit” to you containing the subscriber’s unique Permanent Retirement Account Number (PRAN) Card and the complete information provided by the subscriber

213

in the Subscriber Registration form. This account number will be the primary means of identifying and operating the account. You will also receive a Telephone Password (TPIN) which can be used to access your account on the call centre number (1-800-2220808). You will also be provided an Internet Password (IPIN) for accessing your account on the CRA Website (www.npscra.nsdl.co.in) on a 24X7 basis. How much does a subscriber need to contribute? For Tier-I You are required to make your first contribution at the time of applying for registration at any POP - SP. You are required to make contributions subject to the following conditions:

Minimum amount per contribution - Rs 500

Minimum contribution per year - Rs 6,000

Minimum number of contributions -01 per year Over and above the mandated limit of a minimum of 1 contribution, you may decide on the frequency of the contributions across the year as per your convenience. For details of contribution to Tier –II refer to page 14-15.

The subscriber can contribute the amount through cash, local cheque, demand draft or Electronic Clearing System (ECS) at his/her chosen POP-SP.

No outstation cheques shall be accepted. There will be a time lag between the time you deposit Cash/ Demand draft/cheque/ Electronic Clearing System (ECS) with the POP-SP and the time of credit of units to the PRA, which may range upto 15 working days at the time of initial registration and upto 7 working days for subsequent contributions. PFRDA will impose penalties on intermediaries in case of delay beyond this period. What are the benefits of joining the NPS?

It is voluntary- NPS is open to every Indian citizen. You can choose the amount you want to set aside and save every year.

It is simple- all you have to do is to open an account with any one of the POPs and get a PRAN.

It is flexible- You can choose your own investment option and Pension Fund Manager and see your money grow.

It is portable- You can operate your account from anywhere in the country, even if you change your city, job or your pension fund manager.

It is regulated- NPS is regulated by PFRDA, with transparent investment norms and regular monitoring and performance review of fund managers by NPS Trust.

On attaining the Normal Retirement Age (NRA) of 60 years – You will be required to compulsorily annuitize at least 40% of your pension wealth and the remaining 60% can be withdrawn as a lump sum or in a phased manner; in case, you opt for a phased withdrawal: Minimum 10% of the pension wealth should be withdrawn every year. Any amount lying to the credit at the age 70 should be compulsorily withdrawn in lump sum.

Withdraw any time before 60 years of age– In such case, you will have to compulsorily annuitize 80% of your accumulated pension wealth. The remaining 20% can be withdrawn as a lump sum.

214

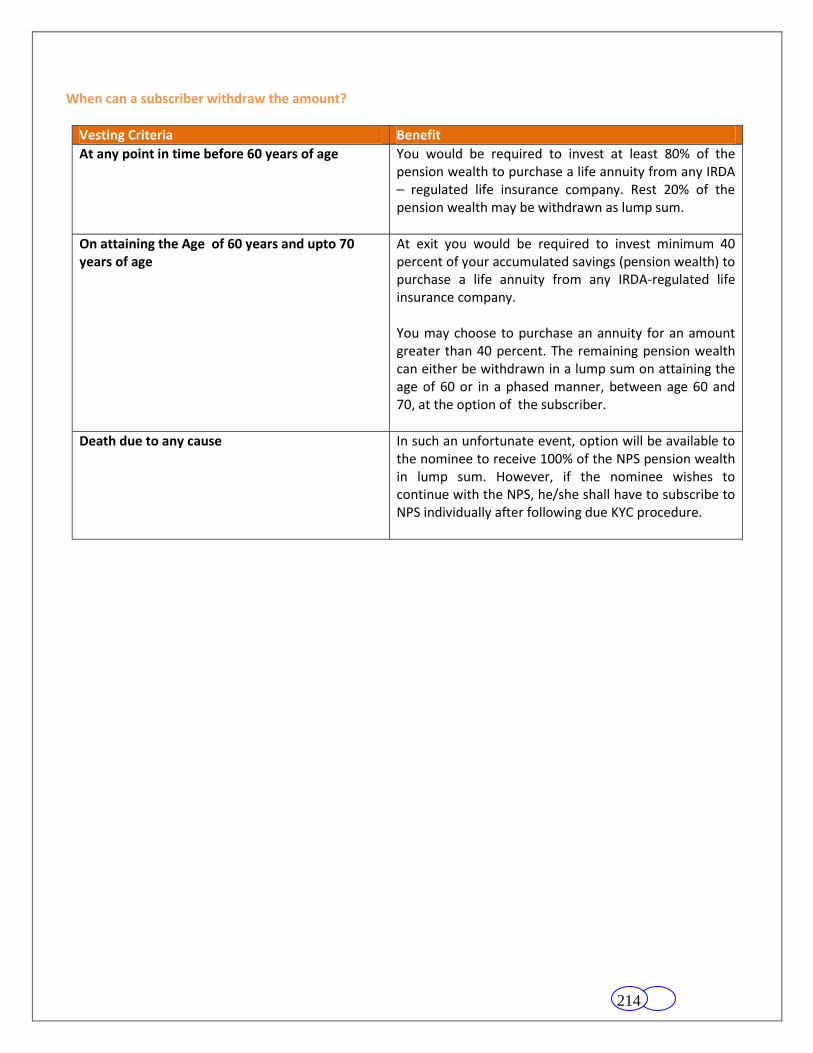

When can a subscriber withdraw the amount?

Vesting Criteria Benefit

At any point in time before 60 years of age You would be required to invest at least 80% of the pension wealth to purchase a life annuity from any IRDA – regulated life insurance company. Rest 20% of the pension wealth may be withdrawn as lump sum.

On attaining the Age of 60 years and upto 70 years of age

At exit you would be required to invest minimum 40 percent of your accumulated savings (pension wealth) to purchase a life annuity from any IRDA-regulated life insurance company. You may choose to purchase an annuity for an amount greater than 40 percent. The remaining pension wealth can either be withdrawn in a lump sum on attaining the age of 60 or in a phased manner, between age 60 and 70, at the option of the subscriber.

Death due to any cause In such an unfortunate event, option will be available to the nominee to receive 100% of the NPS pension wealth in lump sum. However, if the nominee wishes to continue with the NPS, he/she shall have to subscribe to NPS individually after following due KYC procedure.

215

Tax Benefits Tax benefits would be applicable as per the Income Tax Act, 1961 as amended from time to time.

What investment choice does the subscriber have?

The NPS offers you two approaches to invest your money:

Active choice - Individual Funds (Asset class E, Asset Class C, and Asset Class G )

Auto choice - Lifecycle Fund

Active choice - Individual Funds You will have the option to actively decide as to how your NPS pension wealth is to be invested in the following three options: Asset Class E - investments in predominantly equity market instruments. Asset Class C- investments in fixed income instruments other than Government securities. Asset Class G - investments in Government securities. Detailed investment guidelines are provided in the offer document under section “other matters” You can choose to invest your entire pension wealth in C or G asset classes and upto a maximum of 50% in equity (Asset class E). You can also distribute your pension wealth across E, C and G asset classes, subject to such conditions as may be prescribed by PFRDA. In case you decide to actively exercise your choice about investment options, you shall be required to indicate your choice of Pension Fund Manager (PFM) from among the six Pension Fund Managers (PFMs) appointed by PFRDA. In case you do not indicate any choice of PFMs, your form shall not be accepted by the POP-SP. While exercising an Active Choice, remember that your investment allocation is one of the most important factors affecting the growth of your pension wealth. If you prefer this “hands-on” approach, keep the following points in mind:

Consider both risk and return. The E Asset class has higher potential returns than the G asset class, but it also carries the risk of investment losses. Investing entirely in the G asset class may not give you high returns but is a safer option.

You can reduce your overall risk by diversifying your investment. The three individual asset classes offer a broad range of investment options, it is good not to put “all your eggs in one basket.”

The amount of risk you can sustain depends upon your investment time horizon. The more time you have before you need to withdraw from your account, the more is the risk you can take. (This is because early losses can be offset by later gains.)

Periodically review your investment choices. Check the distribution of your account balance among the funds to make sure that the mix you chose is still appropriate for your situation. If not, rebalance your account to get the allocation you want.

Auto choice - Lifecycle Fund

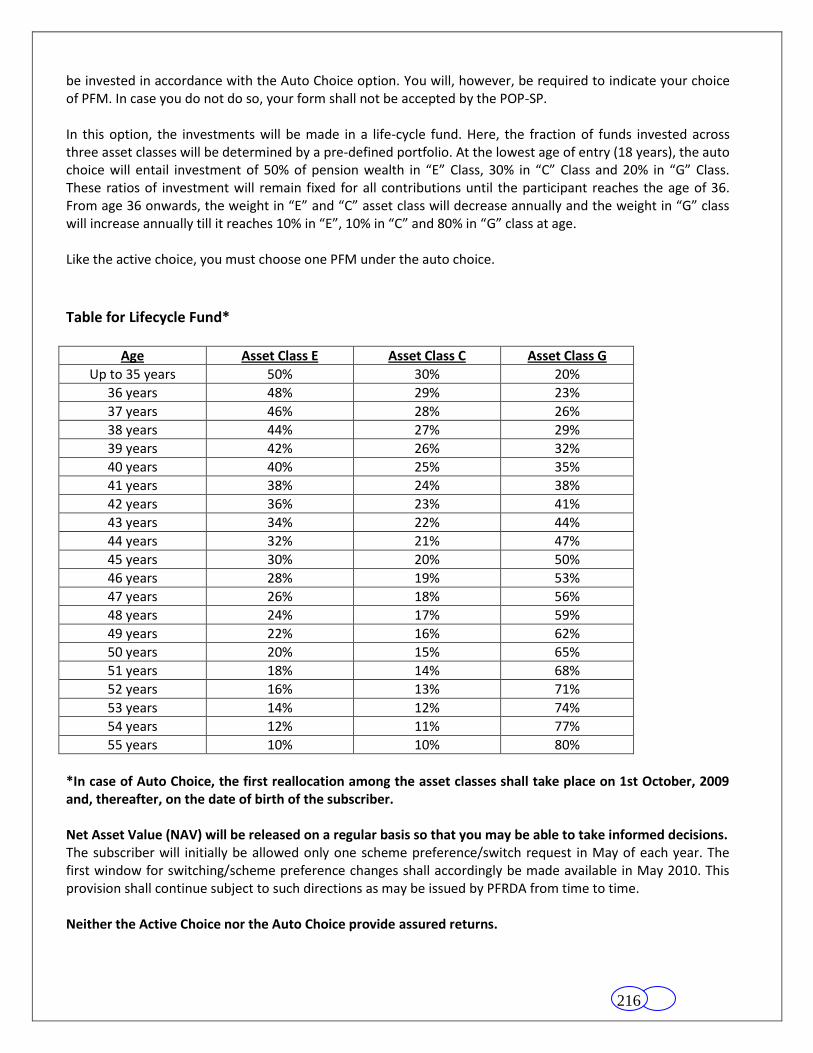

NPS offers an easy option for those participants who do not have the required knowledge to manage their NPS investments. In case you are unable/unwilling to exercise any choice as regards asset allocation, your funds will

216

be invested in accordance with the Auto Choice option. You will, however, be required to indicate your choice of PFM. In case you do not do so, your form shall not be accepted by the POP-SP.

In this option, the investments will be made in a life-cycle fund. Here, the fraction of funds invested across three asset classes will be determined by a pre-defined portfolio. At the lowest age of entry (18 years), the auto choice will entail investment of 50% of pension wealth in “E” Class, 30% in “C” Class and 20% in “G” Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36. From age 36 onwards, the weight in “E” and “C” asset class will decrease annually and the weight in “G” class will increase annually till it reaches 10% in “E”, 10% in “C” and 80% in “G” class at age. Like the active choice, you must choose one PFM under the auto choice.

Table for Lifecycle Fund*

Age Asset Class E Asset Class C Asset Class G

Up to 35 years 50% 30% 20%

36 years 48% 29% 23%

37 years 46% 28% 26%

38 years 44% 27% 29%

39 years 42% 26% 32%

40 years 40% 25% 35%

41 years 38% 24% 38%

42 years 36% 23% 41%

43 years 34% 22% 44%

44 years 32% 21% 47%

45 years 30% 20% 50%

46 years 28% 19% 53%

47 years 26% 18% 56%

48 years 24% 17% 59%

49 years 22% 16% 62%

50 years 20% 15% 65%

51 years 18% 14% 68%

52 years 16% 13% 71%

53 years 14% 12% 74%

54 years 12% 11% 77%

55 years 10% 10% 80%

*In case of Auto Choice, the first reallocation among the asset classes shall take place on 1st October, 2009 and, thereafter, on the date of birth of the subscriber. Net Asset Value (NAV) will be released on a regular basis so that you may be able to take informed decisions. The subscriber will initially be allowed only one scheme preference/switch request in May of each year. The first window for switching/scheme preference changes shall accordingly be made available in May 2010. This provision shall continue subject to such directions as may be issued by PFRDA from time to time.

Neither the Active Choice nor the Auto Choice provide assured returns.

217

Charges NPS offers Indian citizens a low cost option for planning their retirement. A 0.0009%* fee (based on assets under management) for managing your wealth, makes pension funds under NPS perhaps the world's lowest cost money managers. Following are the charges under NPS:

Intermediary Charge head Service charges* Method of Deduction

CRA

PRA Opening charges Rs. 50

Through cancellation of units

Annual PRA Maintenance cost per account

Rs. 2801

Charge per transaction Rs. 61

POP (Maximum Permissible Charge for each subscriber)

Initial subscriber registration and contribution upload

Rs. 40

To be collected upfront Any subsequent transactions

2 Rs. 20

Trustee Bank

Per transaction emanating from a RBI location Per transaction emanating from a non-RBI location

4

zero

Rs. 15

Through NAV deduction

Custodian5

(On asset value in custody) Asset Servicing charges 0.0075% p.a for Electronic

segment & 0.05% p.a. for Physical segment

Through NAV deduction

PFM charges Investment Management Fee3 0.0009% p.a. Through NAV

deduction

*Service tax and other levies, as applicable, will be levied as per the existing tax laws. There are no additional CRA charges for the maintenance of Tier –II account. For a detailed comparison of Tier-I & Tier –II, refer to Page15.

1

The number of accounts in CRA reaches 30 lakh the service charges, exclusive of Service Tax and other taxes as applicable, will be reduced further to Rs

250 (Rupees two hundred and fifty only) for annual PRA maintenance per account and Rs. 4 (Rupees four only) for charges per transaction. CRA’s charge for maintenance of your permanent retirement would include charges for maintenance of electronic information of the balances in your PRA, for incorporating changes to PRA details received by the CRA in electronic form, for sending annual account information once a year in printed form etc.

2These include

1. Regular subscriber’s contribution. 2. Change in subscriber details. 3. Change of investment scheme/fund manager 4. Processing of withdrawal request 5. Processing of request for subscriber shifting 6. Issuance of printed Account statement, 7. Any other subscriber services as may be prescribed by PFRDA

3The Investment Management Fee is inclusive of all transaction related charges such as brokerage, transaction cost etc. except custodian charges and

applicable taxes. The Investment Management Fee is calculated on the average monthly assets managed by the pension fund.

4 Trustee Bank charges are not charged to subscriber directly. Transaction refers to the entire chain of activities starting from receipt of electronic

instructions/ receipt of physical instrument to transfer of funds to the designated PFMs. On the outflow side, it would include all activities leading to credit of beneficiary account.

5Charges for Demat/Remat, Receipt of shares & SEBI charges are extra.

218

Other Matters

Power to make guidelines and give directions PFRDA may, from time to time, issue such directions and Guidelines to NPS intermediaries as may be necessary for protecting the interests of the subscribers. Investment Guidelines The PF will manage 3 separate schemes, each investing in a different asset class, being: Asset class E (equity market instruments) – The investment in this asset class would be subject to a cap of 50%. This asset class will be invested in index funds that replicate the portfolio of either BSE Sensitive index or NSE Nifty 50 index. These schemes invest in securities in the same weightage comprising an index. Asset class G (Government Securities) – This asset class will be invested in central government bonds and state government bonds Asset class C (credit risk bearing fixed income instruments) – This asset class will be invested in the following

instruments;