University of Nigeria Virtual Library Serial No Author 1 AGU, Cletus Chike Author 2 Author 3 Title The Role of Commercial Banks in Mobilization and Allocation of Resources for Development in Nigeria Keywords Description The Role of Commercial Banks in Mobilization and Allocation of Resources for Development in Nigeria Category Social Sciences Publisher Publication Date Signature

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

University of Nigeria Virtual Library

Serial No

Author 1

AGU, Cletus Chike

Author 2

Author 3

Title The Role of Commercial Banks in

Mobilization and Allocation of Resources for Development in Nigeria

Keywords

Description The Role of Commercial Banks in

Mobilization and Allocation of Resources for Development in Nigeria

Category

Social Sciences

Publisher

Publication Date

Signature

CLETUS CHlKE AGU ' - f THE ROLE OF COMMERCIAL B A N ~ S IN MOBILIZATION AND ALLOCATION OF RESOURCES FOR DEVELOPMENT

IN NIGERIA *

* * - + - ,

U

Excerpt from

Savings and ~suelopmeht

THE ROLE OF COMMERCIAL BANKS IN MOBILIZATION AND ALLOCATION OF RESOURCES FOR DEVELOPMENT IN NIGERIA .

C#ur Chlke Agu. University College of Nocth Wales

The need to develop domestlc financial market institutions and patterns of behavlour necessary to generate and mobilize scarce capital funds as a key condition originated In the classic work of Schurnpeter '. Since then so great an interest has been aroused among students that the role of financial institutions, particularly commercial banks, In the emnomic development 01 the developing countries has come under increasing scrutiny by students, as shown in the studies of a small but growing band of economists such as Gurley, Shaw, Gerschenkron, Goldsmith, Adelman, Morris, Cameron, McKinnon and others 2.

Although the relative magnitude of the impact attributed to banks and other financial institutions in developing countries differ among these authors, there is an acceptable consensus that financial resource is a very important, if not the most important factor, in economic development 3. However, empirical research has neither proved nor disproved that financial resource is the key performance indicator of development In the developing economies 4. Nevertheless, there is a considerable body of historkat evidence to substantiate the relationship between financial resources and emnomic development. For instance, the variety of theories of economic development ranging from Harrod-Domar type growth model to Rostow type 11 take-off theories have one thing conceptually in common: it is the notion that the availability of savings is a precondition of continuing growth '.

1 ,!A. Schumpeler, The Theory of Economic Development, CamMdge Mass. Harvard Unkersity Press, 1934. 2 See J. Ouiley and E.S. Shaw, Financial Aspects 6( Economic Devebpmenl *, American E m i c Review, Dec. 1955, Vol. 45 No. 4 pp. 513-538; A. Gerschenkron, Ecwwmk Backwardness h HistorlCeI Perspective: A T

Book 01 Essays, Cam- Mass 1962; R.W. Goldsmith, Financial Structure and Development, New Haven 1869. 1. Adelman and C. Morrls, Performance Criteria For Evaluating E m i c Development Potentiel: An OperatiOnal Approach W, Ck~arler/y Journal of Emits, Vd. 62, pp. 260-280; R. Cameron, Bsnking in the Early Stages of Industrisiization, London: Oxford University Press 1967; R. McKlnnon, Money and Capital In E m b Development, Washington DC: Bmkings Instiition 1973. 3 Sharma says: I any one scarce factor associated with underdevelopment ... Is singled out, it &M be capital W . K.S. Sharma, a The role 01 financial interrnedlades in mobilization and allocation of resources for rural development W , (Abstract) Indian Economic Journal, 1978, Vol. 26, No. 2. 4 T. HiiiriJ.and J. Wlseman, ASpecZs ot the Mobllizatim d Savings in LDCs. Wsarssiq P e r 54, 1981. 5 Rostow noted: -virtually wltlmut exception, the takeoff periods have been marked by the extension 01 banking institutions which expanded the supply oi working capital, and in most cases also by en expansbn in

SAVING3 ANO DEVELOPMENT - NO. 2 - ls&9 - Vlll

Hav1 8COf exte cour obje outs mob reqi hanr othe Dev How

ing accepted the historical evidence that financial resource is very important for iomic development, then mobilization of financial resources from both internal and lrnal sources becomes crucial in achieving rapid economic take-off in developing itries. For an economy that wants to increase Its real capital formation, the lctive mustpe to provide a climate receptive to importation of resources from ,id8 and the encouragement of domestic savlngs. Since financlal resource ~Ilization problem Is very closely tied up with savings problem the latter approach lire$ an institutional arrangement which encourages and mobilizes savings on one d, and which channels savings so mobilized lnto productive investment on the w.

ll I l lVW I lVl l l FIVIU4

exchange constrs Besides, foreign country from the experiences have for higher stand; sources of finam economic develo

eloping countries are generally characterized by low rate of domestic savings. fever, the inadequacy of domestic savings rate seems rather exaggerated. With

few exceptions, namely the very poor countries, the gross domestic savings rate has been found to be fairly high in large number of developing countries. What is really lacking is the efficiency in the process by which savings being accumulated in the economy are translated lnto savings usuable for productive investment 6. Maintenance of high investment level is largely a function of domestic savings performance, capital in41n1ar hnm ahrn9d serves more as a catalyst and as a factor in relaxing foreign

lint than as a major factor in supporting rising levels of investment '. capital, no matter how large the inflow, cannot absolve a recipient I task of mobilizing domestic resources. In developing countries 1 shown that foreign capital alone cannot create any permanent basis 3rd of living in future and that greater dependence on domestic :e facilitates m e the successful implementation of any planned pment.

Greater dependel of independent wc internal resource:

the range d kmg tern St-s of E m i c G 6 See A Mauri, - A f

1977. (I) , pp. 14-26. relevame for less dew 7 See V.V. Bathla ar and policies *, Worm 1

noe on domestic sources of capital, therefore, requires a wide range 311 organised and adapted financial institutions which have to mobilize s for the purpose of capital formation and allow the capital to be

n financing done by a centrat, formally organised capital market r. W.H. Rostow, The Irowih. London: Cambddge University Press 1960. p. 48. mlicy to mobifire rural savlngs In less developed countries W , Sevlngs 8 d Devel-, D.R. Khatkhate and K.W. Riechel, - Multipurpose banking: its natum, scope end

sloped countries *. IMF Staff Papers, Spet. 1980, 27, (3), pp. 478-51 6. td Jacob Meerman, w Resenre mobilization in developing countries: financial Institutions 3evelopmen1, 1978 vol. 6, No. 1, p. 48.

C.C. M U . THE ROLE OF COMMERCW. BANKS IN NIGERIA

and freely into desired development ventures. Commercial went of financial institutions, should be thus the major relevant rhich encourage and mobilize savings and channel savings into first, because of their network of offices, second, because

ugh normal credit operations often activate savings lying idle mause the banks' liabilities which are part of money supply are attract savers '.

aper thus is to expbre in the light of past trends, the rote and ,anks a3 financial intermediaries in mobilizing domestic financial nent and the constraints in the efficient performance of this role.

rle of commerclsl banks

rain macroeconomic function of commercial banks. Commercial ermediaries because of their intermediation role. Intemediation :ess of mediation through institutions and instrument, between mders and ultimate borrowers. It is the process of collecting stitutions and their channelling of the Savings to investors. At the

ruamenral l e v e l or nnancial development, where savers are users of their own funds, capital formation can take place without generating financial assets at a very limited extent thereby limiting very seriously the rate of economic development. But with the development of borrowing in the stage of financial development, decisions to save and invest became separated. Thus the mechanism to bridge this dichotomy becomes essential. This mechanism can take two forms: (i) the creation of financial liabilities on primary securities whereby funds of the surplus economic units are transferred to deficit economic units. This is the direct channelling of funds of surplus spending units to deficit spending units (ii). Indirect financial claims consisting of demand and savings deposits via the commercial banks or other financial intermediaries from where funds of the surplus economic units are made available to those wanting to spend on real capital investment. It is noteworthy that for a vatiety of reasons such as the risk of default, risk of capital loss, risk of loss of value due to inflation and risk of liquidity the first method - the direct channelling of funds from savers to investors - has declined in importance.

8 8es D~A. Khalkhate and K.W. Riechel4p. cit. ..

Furthennore, the availability of a wide menu of portfolio choice of instruments to the public has made the method less attractive. Direct placement of financial liabilities with surplus units seriously limits the volume of savings mobillzed and reduces the dependence of lnvestors on external sources of finance. lnvestors depend on their own funds or retained earnings which in turn limit the size of feasible investment. A developed financial market should provide actual and potential savers and borrowers with the oppoftunity, the cholce and information necessary for optimum savings and allocation of investment within a competitive system. Thus efficiently operating financial market enhance the rate of domestic savings 9. Implied is that the existence of adequately developed financial markets also means that the decision to save and the decision to invest need not be taken by the same economic unit. Commercial banks through their intermediation role between savers and investors affect the volume as well as mobilization of savings, by providing the market with the diversification of instruments that will meet the precise liquidity needs of savers and at the same time making financial resources available to the investors over a relatively long period in accord with their needs. Since they operate with larger portfolios than individuals, commercial banks are less exposed to the effects of default or variation in income or capital value. These advantages they pass on to their depositors so that the liabilities they issue - deposits - are less risky than the individual loans or investments the banks hold in their asset portfolios. Unfortunately there has been a limited appreciation of the influence of financial technology embodied in the quality and variety of financial instruments developed by financial institutions, on savings and capital formation in developing countries such as Nigeria due to the dominant influence of Keynesian macroeconomic development lo. According to the standard Keynesian macroeconomic theory:

S = f (I, i, W) (1 1

S = Rate of savings I = Income

9 W. Ness, Rnanciat markets hnovatlon as a development strategy: initial results lrom Brazilian experience a, E&momC Development end Cullurai Change, April, 1974, 22, pp. 453-472. 10 Bhatia emphasizes this point. See R.C. Bhatia, Benking Stmfure and Pedmence: A Case stu& Of he lndian Banking Systm: 195&6& Ph.0. Dissertation: West Virginia University 1978; and also G. Mathur. = Policy for lor&term development -. lndian Journal of Soclal Sciences, Sept. 1971, pp. 2634.

C.C. AOU - THE R Q E OF COMMERCIAL BANKS IN NIGERIA

i - Rate of interest W = Wealth Financial technology is not among the explicit arguments of the above equation. The reason for this omission can be traced to the Keynesian a portfolio balance theory which divlded wealth accumulation into sets of sequential decision'- the decision to save and then the decision to hold the savings in some form of wealth, which involves asset choice. The portfolio balance approach assumes that the decision to save precedes the decislon to invest and consequently. the availability of different kinds of financial assets which provide a degree of choice in the portfolio balancing process, will not influence the level and rate of savings. 8ecause sychronlzation of the receipt and disbursement of income is an Important objective of saving entities, the kind of financial instruments made available by financial intermediaries will affect the magnitude of savings. Savings, therefore, cannot be regarded as a given datum available for portfolio choice. The volume of savings Is influenced by financial technology and therefore equation (1) may be respecified as: S = 1 (I, i, W, 1)

where t = ZZAjn

I n

and Ajn = the monetary value of the nth asset of the jth institution of the financial market.

The technology (t), bwve r , depends on a number of factors: the extent to which the business units depend on external sources for their finance, and how much on internal financing, the degree of reliance on the financial technique for promoting economic growth, the degree d monetization of the economy, and how far intermediation by financial institutions satisfies the portfolio preferences of both lenders and borrowers by transforming the obligation of the borrowers into a more attractive set for lenders by reducing the level of risk associated with it. In economies where dependence on internal finance is high and where the degree of monetization is low, the role of the financial system in the co-ordination of savings and investment decisions may be only peripheral. Most investment is self-financed so that independent savings and investment decisions may involve only relatively small proportions of total saving and investment ooerations. There are also other tecniaues of collectina savinas and chanl al instn - -

I9

3. The performance of oommwclal banks

It Is usually argued tRat the problems of promotion and mobilizallon of savings in Nlgeria, and in fact other developing countries, are caused by inade uacies in the structure of financial markets. and the density of financlal intermediariesq1. Suppod for this argument has m e from some empirical evidence that has shown savings to be responsive to the number, availability and efficiency of financial markets 12. One of the reasons why financial development may instigate an increase in the aggregate volume of real savings is the direct institutional effect 13. This implies that saving is institution elastic m, and the existence of financial institutions may p m t e high marginal propensities to save. Furthermore, development of financial markets and the multiplication of financial Institutions are expected to affect the form of savings and mix of deposits 14.

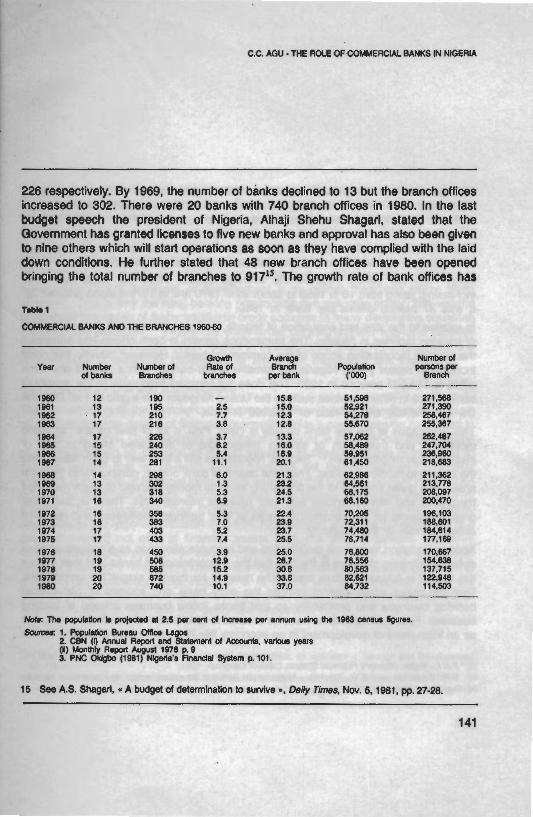

It is therefore necessary to examine the growth of branch network of commercial banks in Nigeria because it gives a snapshot of the physical structure of the commercial banking system and the scope for effective mobilization of savings. Nigeria operates a nation-wide branch banking system as opposed to unit banking system, and there is no law limiting the branching of commercial banks within and among the nineteen states. There has been a remarkable Increase in recent years in the number of branch bank off ices in the country. As Table 1 indicates there were only 190 bank off ices owned by 12 banks in t 960. By 1 964, the number of banks and branch offices rose to 17 and

11 Lewis observed: - There fs a whole range of saving institution that can be develop ed... Experience shows mat the amount of savings depend pa* on how widespread these facilities are; if they are pashed rlgM under the individual's nose, to the extent of having street ~avings groups, or factory groups. or even deductions from earnings at source, people save more than if the nearest savings institution is some distance away m. W.A. Lewis. The Theory ot Emnomic Growth, New Yo*: Preeger 1970. 12 See U.T. Wai, financial lntennediarles and Natkmal Savlngs h Developing Countries. New Yolk: Praeger, 1972. 13 A.!. A M . CMmmIal0anks and E m I c Develapmsnt. The Thelance d Eastern A?ric&, New Y o k Praeger, 1977. 14 For example. Weisbrod found that the C6nvenlence of branch banking perrnlts customers lo hold Iowa balances in non Interest bearing demand acOOun1.s and mespondlgly IO hoid higher balances in less liquid high yielding ass~ts. S.R. Weisbrod. The Convenience bias in branch banking and e m i c s of scale m,

' Federal Reserve Bank o! New York, Research Paper No. 8013. 1980.

C.C A6U - TkE ROC€ OF COMMERCLAL BANKS IN NIGERIA

%r al banks declined to t3 but the branch offices nnks with 740 branch offices in 1980. In the last UigeAa, Alhaji Shehu Shagari, stated that the five new banks and approval has also been given :ions as soon as they have complied with the laid that 48 new branch offices have been opened

es to 917". The growth rate of bank offices has

Awra &an#

per bank

15.8 15.0 12.3 12.8 13.3 16.0 18.8 20.1

Mmber of Populallan W m s per ('000) Branch

61,598 271 ,SM 52,821 271,390 5(,278 258,457 55,670 255,367 57.082 252.487 58.488 247,704 59.951 a , g M ) 61,450 21 8.683 62.888 21 1,362 64,561 213.778 66.175 208,097 66.160 200,470 70,205 166,103 72,311 188,801 74,480 184,814 78,714 177.188 78.8'3 170.887 76.556 154.838 80,583 137,715 82,621 122,948 84.732 114.503

I k m w per mun using the 1983 m s t m Ilgums.

SAWNCIS AND OEMLWENT - NO. 2 - 1964 - Wll

been positive recorded in 19 of Rural Banl December 19e out of the 91 7 of which were Apart from tf increasing, risi It was 37 bra In relatlon to t of banking fac the savings m increase in re off ice to 1 143 bank offices ir US with 1 :6,C This implicatic mobilized, an institutions to I b L - ----I- *- I

wer the period 1960-80, with the highest rate of 15.2 per cent being 178. This encouraging increase in bank offices was due to the first phase king Scheme which lasted for the period 1977-80. By the end of 30, for instance, a total of 200 bank offices have been established, and bank offices by November 1982, 273 were located in the rural areas,all opened under the Government rural Banking Scheme. -~e period 1960-64 the average branch office per bank has been ing from 16 in 1965 to abut 25 in 1970 and in 1975 it stood at about 26. mch offices per bank in 1980. he size and population of Nigeria, however. there Is still the inadequacy :ilities in Nigeria. The tremendous growth in bank o f f i i s has enhanced tobilization scope of the commercial banks. However, despite this great cent years, Nigeria still remains under-banked with a ratio of one bank 103 persons in 1980. This does not compare favourably to the density of I other countries such as the United Kingdom with a ratio of 1 :40,000, the I00 and, a ratio of 1:52,000 in India 16.

)n ol the low bank density is clear. First, e bt of savings are not Wing d thus a lot of savings remain idle or dissipated owing to lack of mobilize them 17. Second, Nigeria has still a tong way to go in habituating

u w vwuta UJ modern bankina. Third. the dearth of bank offices, particularly in the rural lformal money markets of much maligned urious interest rates. There is, therefore, I their savings mobilization and resource

areas, has given impetus to ;he flouhshing in merchants and money lenders with their us1 great prospects for the commercial banks ir allocation role in the economy. Another limitation to savings mobilization and defective banking structure is the fact that thl are biased in favour of urban areas. The re2 First the major urban centres provide the banking business and profitability so that b business. Financial institutions must be crea as an instrument of development in an econt

16 P.N.C. I k i , Nlgerla's Flnam'al Sysfem, London: L 17 D.R. Khatkhate and K.W. Riechel, Multiirpose developedcountries *. op. dl.

I resource allocation as a consequence of e concentration of banks and their offloes %sons for this are simple but unfortunate. easy basis and sources of commercial ~anks follow business instead of leading led in anticipation of needs for credit and )my like Nigeria, instead of waiting on the

Dngman. 1981. banking: Its rialwe, scope and relevance lor less

C.C. AGU - THE ROLE dl: COMMERCIAL BANKS H NIGERIA

ic demand and supply. Second, the established banks ne of savings seeking to be mobilized and channelled le rural areas. It is often argued that since the rural subsistence level, there is very little that can be

msumption. Because of this, it has not been realised , though in small units per Individual, exist in the rural serves of productivity do exist somewhere in the rural ~f develapment is to gather them and utilize them banking programme is a welcome policy. The volume faditional credit societies in many developing countries ly the commercial banking system was until recently ch tended to establish their branches where there is a iinesses of few urban merchants and traders.

nedialion

mlal banking system and indeed the financial system iancial intermediation in a country can be measured in ally acceptable measure is the financial interrelations of market value of all financial claims outstanding to cal assets plus the net foreign balance 19. Another instruments issued by the financial institutions to those uhich indicates the degree of institutionalization of r shortcomings notwithstanding, are not meaningfully ion. The FIR, far example, assumes the existence of a inancial assets held, but also of national wealth - I balance. Similarly the measure of a new issues - of lose of other economic units assumes the existence of indicator is of limited use in economies where the stitors are informal money markets where reliable data Id debts are impossible m.

sl , The Brirtsh Finendat System, London: McMinan 1973. m ' c Devek-pnenf: The Experlenocr of Eastern Africe. cp. cit.

.t national output )n by the ratio of ~ a l output (GDP). ts of the financial put is used as a is supplemented tings deposits to diversification of

mand deposits to Y supply. Money nand deposits. It )P has increased per cent in 1981.

I r w nlyrtasi prvpuriwrl vr J I. t p r cer l r was rewrauu In I Y to, w e d , the growth of financial assets of commercial banks outpaced product. The long-run growth trend in the ratio reflects the impoitant role of commercial banks and their financial technology in the savings mobilization and thereby in the development of the economy. The ratio of demand deposits to money supply increased from 34.2 per cent in 1960 to 55.1 per cent in 1965, and after a period of fluctuating trend (1965-73), it recorded 55.8 per cent in 1974 and 58.1 per cent in 1979. Since money supply is here narrowly defined to embrace only currency in the hands of the non-bank public and demand deposits with commercial banks, a high ratio of demand deposits to money supply indicates the greater use of bank money than of currency. This is indicative also of increased banking habit and thereby greater scope for savings mobilization by the commercial banks. The proportion of savings and time deposits to money supply for . . . . . . . . a --A

* cent in 1960 to 65.9 per cent in rerage of the ratio of the demand eposits to money supply were 46 iply a moderately high degree of

tne same perlca nas nsen conslaeramy rrom ;?-L.u per 1979 and then to 62.8 per cent in 1981. The annual at deposits to money supply and the savings plus time dc per cent and 51.5 per cent respectively.-~0th ratios in financial intermediation.

21 K. Kwmng. - Benklng and (Inancu In Africa: a review arm bp. 247-263.

CE OF COMMERCIAL BANKS M NlGERlA

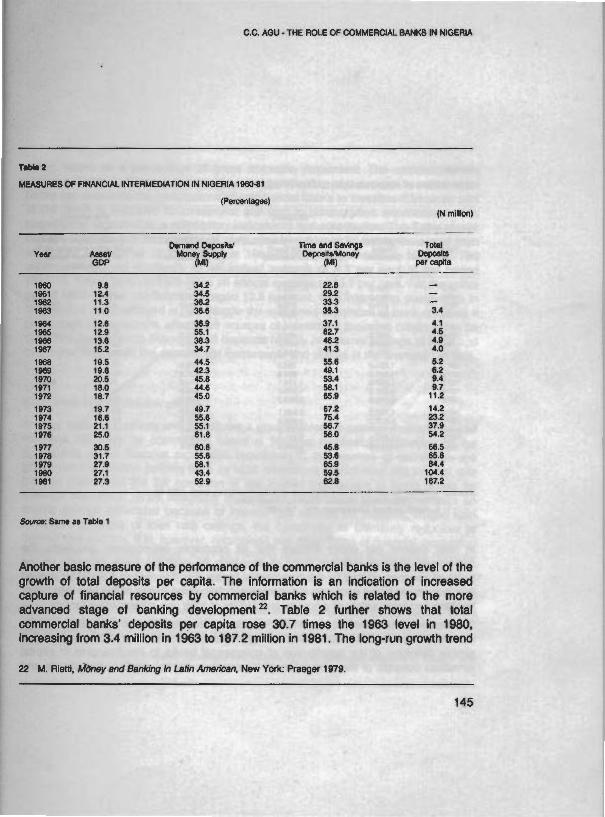

Tam 2

MEASURES OF FINANCUL MTERMEDUTlON fN NIGERIA 196Mt

S c u m Same a8 Table 1

Another bask measure of Ihe petforrnance of the mmercial banks is the level of the growth of total deposits per capita. The information is an Indication of Increased capture of financial resources by commercial banks which is related to the more advanced stage of banking developmentn. Table 2 furlher shows that total commercial banks' deposits per capita rose 30.7 times the 1963 level in 1980, increasing from 3.4 million in 1963 to 187.2 million in 1981. The long-run growth trend

22 M. Rlenl, h e y and Banking In LsHn Americen, New York: Praeger 1979,

SAVINGS AND DEVELOPMENT - NO. L - 1BM - Vlll

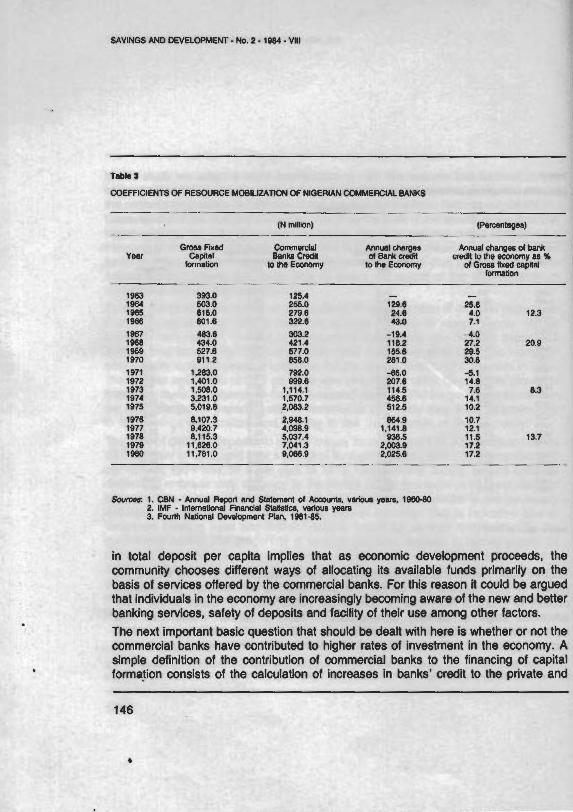

COEFFICIENTS OF RESOVRCE MOBILIZATION OF NIGERIAN COMMERCIAL BANKS

(N mlllbn) (Percantagaa) -.

Graas Mad Cwnrorciel mual chafglw h n u d chaw8 d bank Ydar Cspilal Bank8 Credlt d Bank abdl nedlt to the oconmy aa K

b a t i n lo me Emomy do Iha Ewmmy 01 Gross Uxed q f i e l formation

~ ~ U ~ C B B : 1. CBN - 2. IMF - I 3. Fourth

in total dew community cl basis of sen+ that individual banking servi~ The next imp commercial b simple definit formation cor

kmud Repbn and Stalemen1 of h u n t s , vadoua years. 1WiI-W nlernetional Flnanclal Slallsticq varbus years Natiinal DBvelopment Plan, 1881-85.

Jt per capita Impfies that as emnomic development proceeds, the m e s different ways of allocating its available funds primarily on the ces offered by the commercial banks. For this reason it oould be argued Is in the economy are increasingly becoming aware of the new and better ces, safety of deposits and facility of their use among other factors. wtant basic question that should be dealt with here is whether or not the tanks have contributed to higher rates of investment in the economy. A ion of the contribution of oommercial banks to the financing of capital mists of the calculation of increases in banks' credit to the private and

C.C. AGU -THE ROLE OF COMMERCIAL BANKS IN NIGERIA

~rcentage of gross domestic investment. The calculations are ough this coefficient of mobilization of resources by commercial 10 contributions of commercial banks to investment because part ted to investment and part to consumption expenditures, It Is as a satisfactory indicator of that contribution. The Table shows mobilization of resources by commercial banks increased from 1 12.3 per mnt in 1964-66 to 20.9 per cent in 1967-70. The rastically to an annual average of 8.3 per cent in the period In 197&80 'to an annual average of 13.7 per cent. For the entire efficient averaged 13.6 per cent. One interesting observation in

., --,,,cient is that despite the sustained expansion of bank credit as a percentage of investment, alternative sources of investment financing continued to be dominant. Indeed such financing still depends heavily on internal savings of firms and to a lesser degree on the sale of deM instruments and shares in the financial markets.

3.3. Fmancial repression effects

Another factor that affects and constitutes a great problem to savings mobilizatlon and resource allocation by commercial banks is financial repression. According to the proponents of the financial repression hypothesis. 23, the sources of repression are government legislation policies such as legal restrictions on activities and interest rate policies that distort the full operation of the market mechanism in fixing prices for financiai resources. Since according to them the repressions show their effects on limited savings generated because of interest rate ceilings on deposits, limited loan resources &cause of loan rate ceilings, the hypothesis Is ultimately reducible to interest rate policies. It is, however, recognised that other forms of financial repression might result from other factors, such as portfolio regulations and oligopolistic financial markets ".

23 See R. Cameron, Banklng and Eamomic Dewlopment: Sbme Lessons of Hisfoty, ((ed.) New York Oxford Unhrerslly Press 1972. R.M. McKmnon. Money and Capr'kl in E m m l c Development, Washington DC: Brooking Inst iMh 1973. E. Shew, Financial Deepining in Economic Development, London: Oxford Universlly Press 1973. 24 V. Galbis, a An analytical aspect of interest rate policies in Less developed countries m, Savings and Devefopment 1982 (6). pp. 1 1 1-1 67.

on the level d Interest rates on o the rate of Inflation. To test the rest rates relative to the rate of iterest, that is the nominal rates ,ltive over a period of time, then it. ression, rather that would imply

and administered. Consequently ince or scarcity of capital in the t a very low and statlc level over

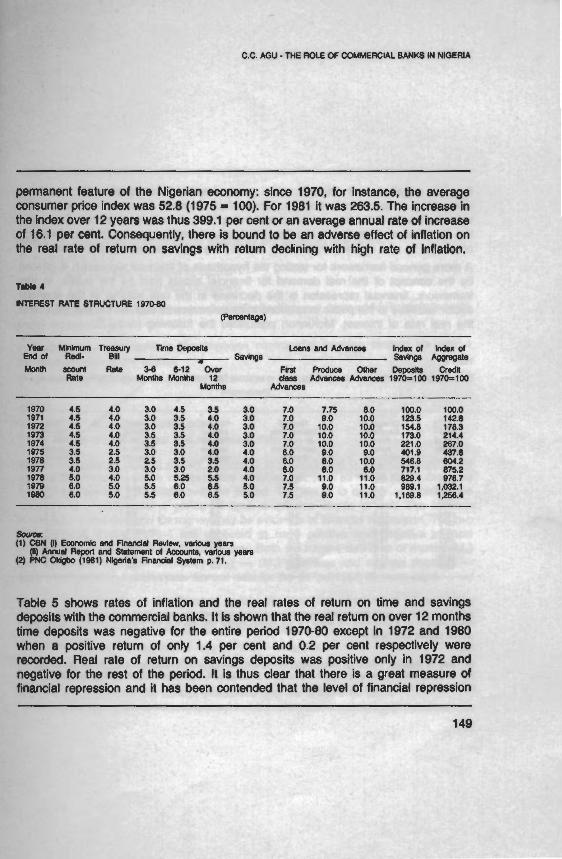

Lllw JwanU lVl lVUU l=asvl Illur, ,., wll~vlw yvvdrnrnent borrow from the public at a very cheap price z. A second reason that has been used to justify the policy ?flow and static interest rates regardless of economic circumstances is the Keynesian postulate that a low interest rate implies a high rate of investment. This justification is based on a misinterpretation of Keynesian investment theory which is not necessarily applicable under full employment with inflation There are other less plausible reasons of low interest rates policy, There is the argument that low and stable interest rates can help strengthen the stability of the financial institutions because low interest rates on their liabilities help to protect their earnings; there is also the influence of the well known u usury law n which limits the payment of interest on moral grounds. Table 4 shows the interest rate structure in the economy. A cursory look at the Table reveals the static nature of the interest rate over a period, For instance, for five years, 1970-74, interest rates on savings deposits remained low and static at 3 per cent, it rose marginally in 1975 to 4 per cent and remained the same till 1978. The same is true of the time deposit rates and the minimum rediscount rate - the CBN minimum lending rate. There would have been nc rate of Inflation had been I

25 To quote the Central Bank Government should obtain h e fir necessarily conditioned the rafe Tpasury bll issues made W . See 26' V. GalMs, Analytical asp Develment 1982, 2 (6), pp. 1 1 1

>thing wortying about the static and Im interest rates, it the ,table over the years. But it was not. lnflation has become a

: of Nlgerla: The Central Bank has elso been concerned 10 see that l a m il requires on the mosl economical ba&. These conslderahons have at which Federal Government loan operations have been undertaken and CBN, Annual Repoff and Statemenf of A m n t s Dec. 1980, p. 19. I& of interest rate policies in less developed countries =, Savings and -167.

C.C. AGU - THE ROLE OF COMMERCIAL 8ANKS IN NIQERIA

permanent feature of the Nigerlan a consumer price index was 52.8 (1975 the index over 12 years was thus 399, of 16.1 per cent. Consequently, there the real rate of return on savings H

T W 4

INTEREST RATE STRUCTURE 197080

Year Mlnlrrmm T m m y h Oepoelm EM OI MI- Bnr MMh mwm Rats 34 6-12 Or

Rate Months M o m 1: Mon

s7umr (1) C8N (I) E-b and flnanclal Asvlow, vwbtm,

(11) Annual Repon and Steternen1 of Accounts, va~ (2) PNC 0- (1081) Nlgerla'a Financial System p.

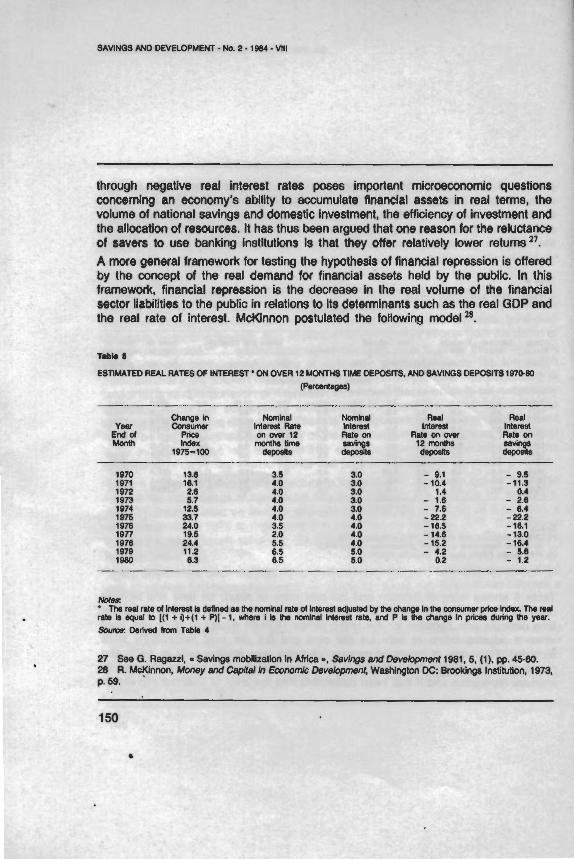

Table 5 shows rates of inflation ant deposits with the commercial banks. I time deposits was negative for the i when a positive return of only 1.4 recorded. Real rate of return on sa negative for the rest of the period. I financial repression and it has been

conomy: since 1070, for instance, the average i = 100). For 1981 It was 263.5. The increase in ,I per cent or an average annual rate of increase t is bound to be an adverse effect of inflation on rith return declining with high rate of Inflation.

3 the real rates of return on time and savings t is shown that the real return on over 12 months ntire period 1970-80 except In 1972 and 1980 per cent and 0.2 per cent respectively were

wings deposits was positive only in 1972 and t is thus clear that there is a great measure of contended that the level of financial represslon

SAWNQS AN0 DEVELOPMENT No. 2 . 1 WJ4 - Vlll

Ihrough negative real interest rates poses imp0 concerning an economy's ability to accumulate fin, volume of national savings and domestic investment, the allocation of resources. It has thus been argued 11 of savers to use banking institutions Is that they a A more general framework for testing the hypothesis by the concept of the real demand for financial as framework, financial repression is the decrease in sector liabilities to the public in relations to its determ the real rate of interest. McKinnon postulated the

Tk* 6

ESTIMATED REAL RATES OF INTEREST ON OWR 12 MONTHS TIME DEF (Permagen)

22%; Nomlnal M h d Year Interest Ren, Intersst

End of Price an over 12 Rate on Manth Index month6 time savings

1@75=100 depils depodw

~rtant micr08COmlc questions ancial assets in real terms, the , the efficiency of investment and hat one reason for the reluctance lffer relatively lower returns 27.

of financial repression is offered ;sets held by the public. In this the real volume d the financial inants such as the real GDP and following model

w Intefw

Rate on wer 12 montha deposb

Real lnlerest Rate on savlngr deposlta

el rate 01 k r m l adjusled by the chm* In- consumer price hdex The real tta mrnhal h(8resl rate, and P b !he change In p r i dwlng the year.

n In =, Sews 8nd De~lopmsn( 1981.5, (I], pp. 45-60. mmmic Devekpment, WWaington DC: Brooking8 Institution, 1973,

C.C. AGU -THE AOLE OF CbMMEROlAL M K S R HIQEFII.4

whe

Y =

whe Y is

I "VPl

I OPP I ignc

havl den ineli

I detc r w and havl

It is this ela: In h In h

Ire ')d = the demand for financial assets by the publlc In real terms. 8 the real BOP. the average rate of return to capital

P = the expected real rate of Interest.

7e explanatory variables have a positive effect on real demand for finenclal assets 3r repression.

esting the hypothesis In the Nigerian commercial Mnking system we use a lified version of the model: ' = f (Y, "'~t-1) (2)

tre the GDP at current market prices

t-I is the rate of Inflation and represents the

onunity cost of holding money relative to alternative real or financial assets. We ,red the inclusion of the interest rates variables because as noted above the rates e been more or less static ov0t the period. The test is to determine whether the land for money over a period of time is inflation elastic or not. The inflation asticity of the demand for money may be evidence of financial repression. The two wminants Y and PtlPt-1 are expected to have positive and negative impacts sctively on the real demand for money. Both the narrow definition of money (M,] the broad definition of money (M2) - (M,) plus time and savings deposits -

e been used in the analysis. Annual data for the period 1960-80 were used. .

1 common practlce in the literature to take the logarithm of equation (2) and since suits our analysis because it enables the interpretation at the coefficients as

licities, the logarithm form of equation (2) yields: /ldl/p = In all + a12 InY -1- ar3 In "'/Pt-1 + a,, ui (3) & / P = ~n 82, + an InY at- an ~n R / ~ t - ~ + n~ u, (4)

whe Ire the all, become the various elasticities and the ul the error term.

SAVINGS AND DEVELOPMEW. No. 2 - 1884 . Vlll

The tesl results are presented here: In Mdl4P = 2.3449 + 0.53581nY + 1.006111 R/~t-l

(0.0247) (0.0575) ' A = 0.964 d.w = 2.1 In P ~ P = 2.4732 + 0.5941 1nY + 1.126111 R/Pt-l

(0.0276)* (0,0644) ' R 3 0.963 d.w = 1.6 Below each coefficient is the standard error,

Statistically significant at 1 per cent level.

From the test results above it is seen that a considerable proportion of the depende variable Is explained by the explanatory variables. The Durbin-Watson statistics (d.n, of 2.1 and 1.6 for the estimates of equations (3) and (4) respectively indicate the absence of first order positive and negative autocollinearity in the data used for the regression analysis. All the coefficients are statistically significant at less than 0.01 probability. Of particular interest Is a13 and a,, the Inflation elasticity of demand for money. The coefficients have theoretically unexpected sign, indicating that increases in the rate of inflation leads to increases in the demand for money. This ignores the opportunity cost of holding money. The explanation that may, perhaps, be offered for this is that because of the future expectation of further inflationary pressures people hold more money particularly when there were no alternative assets that can serve as a hedge against inflation. More importantly, the coefficients of a13 and am indicate elasticities of 1 .Ot and 1.1 3 respectively. This implies that the narrow and broad definitions of money - MI and M2 - respectively are inflation elastic. The finding, therefore, rejects the hypothesis of financial repression in Nigeria. However, as Kwarteng in a similar analysis contends, the inflation elasticity of demand for money in Nigeria may be due not so much to the non-existence of financial repression in the Nigerian economy, in fact there is some evidence of financial repression in Nigeha as per the low levels of the real return on deposit, but rather to the higher increases in export revenues from oil and thus in income during the 1976s 29.

29 K Kwarbng. Banking and finance in Africa: A review eRl& =,op ck, p. 281.

1 52

C.C AQU - THE ROCE OF COMMEbClAL BANKS M NlGERU

We have so far assumed that savings and investment are respectively interest elastic. The question is whether a free and positive interest rate policy advocated by rne proponents of the financial repression hypothesis would lead to higher savings and investment than hitherto in Nigeria. Admittedly, the policy whereby commercial bank pay very low Interest rate of about 4 per cent on Interest bearing depdsits and at the same time charge as high as 7-11 per cent on their loans and advances is discouraging enough to savers. It is likely to have a negative effect on the perlorrnanca of the commercial banks' saving mabilkation and resource allocation role. An examination of Table 4, however, shows that saving is interest inelastic. For example from 1970 to 1974 interest rate remained static at 3 per cent and for the period 1975-78 it was also static at 4 per cent, rising marginally to 5 per cent In 1979-80. Over the same period, savings index continued to rise steadily with spectacular increase of 81.9 per cent in 1975 of 1974 level. An explanation usually offered by bankers for this is that the small savers do not undertake saving with an objective of earning interest income but rather as a mere safe custody for an unexpected contingencies. As H to give credence to this view Hitiris and Wiseman contend that for the few under-developed countries for which it was possible to study the relationship between interest rates and savings, the net impact of real interest rate on aggregate savings was found to be insignificant or even negative, suggesting that higher rates of interest are associated, if anything, with lower real savings M. On the investmen! side, how far an Increase in interest rate will deter investment is dependent on the expected return on investment. Take, for instance, the peri i 1970-74 when the return being declared by industrial and commercial enterprises in Nigeda were of the order of 100 per oent on the capital invested, first-class prime advances rates remained static at 7 per cent [see Table 4). Other advances, however, rose by 2 percentage point from 8-10 per cent. This type of increase is hardly likely to be decisive in the investors' plans and decisions to invest if the expected return will be reduced not so significantly or may not in fact, in spite of the resultant increase in costs, go up even more. It foilows therefore, that what is important for Nigerian investors seeking funds in the boom conditions of 1970-76 Is not so much the rate of

30 T. HlNris and J. Wiseinan, Aqoects ot the MoblRzaHon d S a v b In LDCs, op. M. See also J.G. Williamson, Personal saving in developing counbies: an International cress-section h0m Asia r. The Ec01w)rnic Recad, June 1968.

SAYINGS AN0 DEVELOPMENT - NO. 2 - 1984. Wll

thls assettion :el despite the

u cost n h determining the demand for and supply of rural credit ". This explains why, as Table 4 shows, the index of loans continued to show a rising trend in spite of the rise in the produce and other advances rates in the period 1970-74. In 1978 when both rates were 11 per cent respectively. the index of loans rose 9.76 times the 1970 level when the rates were 7.75 per cent and 8 per cent for produce and other advances respectively.

Commercial banks. the most important component of the Nigerian financial system, are the most important saving mobilization and financial resource allocation institutions in Nigeria 33. These roles make commercial banks essentially a phenomenon of development. In performing these roles in the Nigerlan emnomy, it was found that the banks have potential scope and prospects for mobilizing financial resources and allocating them to productive investments. These scope and prospects have to be exploited quickly by enlarging the number ot bank offiies and also by the banks branching into the rural areas where a lot of savings lie idle or dissipated and where productive investment projects do not take off because of lack of financial institution to mobilize and channel the funds so mobilized into productive activities. The analysis raises an important question: whether the assumed repressive measures are indeed repressive. This is because the proponents of the financial repression

31 P.N.C. Oklgbo. Nigeria's financial Syslem, London: Longman 1981, op. dt. 32 0. Ragazzi, rn Savings mobilization in Africa a, qp. clt. 33 Bhatia and Khatkhate emphasized these roles when they d d : In essence three main L regarding the influem of financial intermediaries: first, their Impact on the growth of savlngs, espec household sector; second, their role in financialiretion of these savlngs (that Is savings in a finandal ' third their ability to ensqre the most efficient transformation of mobilized funds Into real capital I

Bhatie and D.R. Khatkhate, Financial intermediation, savlngs mobilization and entrepreneurial de the Aftlcan experience *, I F M Stan Papers, March 1975, vol. 22. pp. 132-159.

Bum exist :ially of the I form); and 1. See R.J. velopment:

C.C. AGU - THE ROLE OF COMMERCIAL BANKS IN NIGERIA

such a t Nigeria, As Adewunml rightly noted, the proponents of the financial repression hypothesis based their studies in advanced countries and went on to Interpret the result without suffklent qualifications for the developiq countries with entirely different environments 34. It is ObVIous that the envlronmenis dlffer not only In varlety and volume of financial instruments and institutions but also in the interrelatjons of different subsectors and sophistication of activities and operations. If it is realised that the Nigerian commercial banking system was until recently dominated by foreign banks which maintained strong oligopolistic bank market structure, it will be fully appreciated that competitive market structure does not exist in Nigeria. Consequently, interest rate management may not be regarded as a substitute for the determination of interest rates by competitive market forces, but as necessary alternative when conditions for the existence of competitive market conditions are not present and cannot be readily established 35. In the absence of competitive market structure, positive interest rate policy could potentially destabilise financial markets, increase the power of oligopolistic financial firms to exploit market imperfections by increasing the interest spreads between loan and deposit rates, and simply perpetuate the existence of a financial environment with rather low deposit rates of Interest. To establish an adequate level and structure of interest rates in this peculiar situation, there is need for government intervention to aid the market j6.

Thus while financial repression through interest rates ceiling may discourage savings in Nigeria it is not as serious as has been postulate by the apostles of the financial repression hypothesis. The commercial banks should nevertheless offer simple, intelligible and convenient financial instruments yielding a positive real return. Even if low, real interest rates on deposits should encourage savings mobilization by the

REFERENCES

Addman Irma and Monls Cynthia, Performance Criteria for evaluating @mwmic devekpmsnt potential; an operatbnal approach, The CkrWerIy Journal 01 Ecwtomlcs, 1 M (62), 286-86.

Adelman Irma and )Abnls Cynthia, S6Cbty. P M i s and Economic Development: A duanNteNve Appraech, John Hopkim Univeroity Press, Balmore. 1887,

Adermnmi W., Lam Management in Nigerian Banks: A Study of the Efllotency or Commefcial Banks' Landlyl Func(ion In A DevebpIng E m m y . Ph. D. Thesis Unlvenily of Wales, 1981.

Agu C.C.. Rural Banking: a strategy lor ~ r a l development an epprarsal. Gavlnge andDewlapment, 1-1983-VII.

AbdI AM lssa, Cbmmedel Banks end Eoorxwnic Developmeni: The ExpExperem d Eastern A f k Praeger, New York, 1977.

Bhalla Ramesh Chender,+nking Sirvcfure and Fedomme: A Case Study d Wm Man Bcnking System 19M-68, Ph. b. Dissertation. West Vltginia University. 1978.

Bhala A.J. and Khatkhate Deene R., Financial tntenedlatlon, ravings mobilization and entrepreneurla1 development. The African Experience. IMF Stafl Paper, March 1975.

BhaR V.V, and Meman Jamb, Resourn mobNzation in develc$+ng cuuntrbs' financial InstMnbns and policie~ WorM D19~kpment. 1. 1978.

Cameron R., Banking h, the Early Stages of Induslrkrllzari~m, Word Unlverelty Press, London, 1978.

Carnercnr R. ed., Banklng and Economic Uevelopmenl Some Lessvns ol History, WOxford University Prese, New Yark, 1972.

CBN Annual R e p ? and Statement d Accounts, DeeemEer 1980.

Khatkhate Deene R. and Rbchel Klaus-Wall&, Multipurpose benking: its nature, *cope and relevam (or less developed cwnbies. IMF Staff Papers. September 1900.

Gatbls Vicente, Interest rate rnawmenl: the Latin American experience, Savings 8nd Devekpmnf, 1981.

Gerschenkron A.. Ecmomk Bednvedness In tfista-lcal Perspecfive. A Bodc 01 f , Haward University Press, Cambridge Mam, 1982.

Ooldsmith R.W., Financial Stnrciwe and Development, Yale Unlverslb Press, New Haven, 1969.

F. hehem, Indanesia: financial dwdopment and economic growth, Canadian h m b b n a l Devekpment Agency, 1980.

Gurley J. and E.S. Shew (1955), Flnandal aspects of soonomic development, Americen Economic Revleew, 45 (4) (Dec.) 515-38.

Hiris T. end J. Wisemen (1961). Aspects of Wm MoMlizatim d Saw k LDCs. Discussion Paper, 54.

Revd Jack, The i3fitish Fhramial System, Macrnillan, London. 1973. . .. . - - . - . . . . - . and O e v e ~ , 3, 1982, W.

C.C. AQU - THE RoLE OF COMMERCIAL BANKS H MQEMA

Lewls WA.. The 7Way ot Economtc Gmwth. Harper, New York, 1970.

Matturr G., Pollcy for bng-term development, Indian Jbwnsl kr SaclsI S d m ~ s , ~~ 1971.

MeKinnan Ranald, M m y end Cap#& m E m & Devehyment, The Bookings Institution. Washinglon DC, 1973.

WKlnnsn Rmakl &., Money and Finance in E m m k Development, 1076. Ness W.L.. FlnancleI mad& tnllwBms as a strategy: Initial results from Brazilian e ~ ' m , Eoonomic

Development and CullurPl C h m April 1974.

Oklgbo P.N.C.. Nigada's Financicll System, Lmgman. London, 1881. Ragazzl Glorgb. Savlnga mobllizatlon In A m , Sam end Devekpment, 1, 1W1, V. RleM Mado, Money and Banklng h Lath Amerka, Prosper. New Y M , 1D79.

Rostm W.W. (1 W), 7M Sfages d Ewrrcmrb Omwfh (London: CmtM@s Unlverslty Prase). Bhanna K.S., The role of lnancial intermedlades In rnabllizatlon and allocetlon of resources for rural

devebpmenl (Abstract). lndlan Economic Jownal, 2, 1978.

shaw Edward, Finencia1 Despening In Eamomlc Development, Oxlord Wnlverslty Press, London, 1973.

Schumpeter JA., The Theory of E m l o bevetopmenl, Haward Un-ersity Press, Cambridge Mass.. 1934.

Wal U. Tun. Flnamkl Mnnediaries and Natkmel Savings k, cbduphg CounMeJ. Preeger, New York, 1972.

LE ROLE DES BANQUES COMMERCIALES DANS LE PROCESSUS DE MOBILISATION ET D'ALLOCATION DES RESSOURCES POUR LE D~VELOPPEMENT AU NIGERIA

Les banques tmnmerciales, mposantes fondamentales du s y s t h financier au Ni- M ia , sont les &ablissements les plus importants qui favorisent et mobilisent l'dpargne vers des investisemenis productifs. Cela, 8 cause de la pdsence d'un ensemble de bureaux et de Q U I C ~ ~ ~ S et, du fait que te passif des banques, falsant partie de I'offre de monnaie, est tds liquide et attrayant pour les Bpargnants. Pour ce role impartant, tes banques commerciales sonf essentielles au phdnomhe de developpement. Le rble Nth4 par 18s banques commem'ales dims la mobilisation et la canalisation de I'dpargne financier dam I'&onomie de la Nigeria a 6td limit4 par deux facteurs impor-

SAWNQS AND bEVELOPMENT - NO. 2 - 1984. Vllt

tants: I) la faible densltd des bureaux apparfenant aux banques ~wmnerclales: une vaste partie du systhe Bcomique et en particulier les zones wales &ant encore &pouwues de services bancaires. Dens ie pays la densite bancaire esi fahte (on compte un bureau poor 1 14.503 personnes). Cela entraihe par obns&uent des habitu- des bancaires peu r8pandues, de faibles taux d14pargne et de canalisation des res- sources par ies banques cornmerciales. 2) La rdpression finan&re. A cause de I'ab- sence d'une politique active des taux d'intdrBt, les taux d'intmt reel sbnt nhatifs et prabablement ont d6favorisd la mobilisation de 114pargne des banques cornmerciales, Tautefois, tandis que la politique de lib6ralisatbn du faux d'intdr& p u t devenir n h s - saire pour mndre pdsitifs les faux d'int&r& reel; la politique de li~rallsation de la structure des taux d'intddt est contestde d cause de /'absence de conditions compdti- tives dans le syst&me bancaire. Cette politique pounait mnduire d une plus faible mobllisation de t'dpargne pouvant destabiliser les marches financiers et augmenter le pouvoir des entreprises financieres en forrne d'olippole. Ces dernikes pourraient tirer parti de cette situation et profiter des imperfections du march6 p w r accrofire /'&art entre les taux d'intdrdt sur les d w t s et sur les pMs. Le but des banques cornmerciales dam la mobilisation de I'dpargne p r r a i t elre plus facilement atteint en augmentant le nombre de leurs Males en partidier dans les zones rurales et en faisant adopter des politiques appmprides aux autorites mondtai- res. Ces politiqttes purraient &re merwlsagBes de fawns diff6rentes soit, en permeftant la IiMralisation de tous les taux d'intdrdt soit, en BtabWant m e politique dimBtionaire des taux d1int6rdt. Le choix, toutefois, devrait 6tre subordonnd 4 I'orientation gdndrale de la pditique Boonomique du pays. 11 faut se rappeler que, i4 cause de la nature specifique de 1'4conomie et du systhe des banques commemales, I'intewention des pouvoirs publics est encore ndmssaire dam le systdme bancaire do Nigeria p ~ u r ai-

u forces du march6 B Btablir un niveau admat des taux d'intdr6t.

Savlngs and Development, a quarterly review puMi6hed since 1977 by Finafrice Foundation -

FlNAFRlCA is a nm-profil bliitulla, eatebtished by CARIPLO - C W dl Risparmld delk Prdvinde Lwnberch Mian ( 1 1 ~ ) . Ita-gmJ being the prom- tim d social md ~oonomil! develapment ol less dvrelaped countries, * pecidly in AM= Ihmugh mesrch and rk#mrenWkn an savings moMliza- tion and finacid development, lechnlcsl asManw far Uw c m W t s d re- organlzatlorr of f'mandsl instilUIJbnB, Iratdng of bank staff.

Tlpegralis MORl - Via Gulcciardini. 8& - 21 100 Vared .

Related Documents