Medicare Made Clear™

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Medicare Made Clear™

Medicare Made Clear™

Top Medicare questions

2

1 Who is eligible for Medicare?

2 What are my coverage options?

3 When can I enroll?

4 What are my next steps?

5 Once I am covered by Medicare, how could I save money?

6 Where can I find more information?

Medicare Made Clear™

Medicare Made Clear™

4

Original Medicare (Parts A and B)

U.S. citizen and resident (at least five consecutive years)

65 years old Special situation For example, people of any age with end-stage renal disease (ESRD) or amyotrophic lateral

sclerosis (ALS)

ELIGIBILITY

Medicare Made Clear™

5

Original Medicare (Parts A and B)

ELIGIBILITY

Medicare Made Clear™

Medicare Made Clear™

Medicare Made Clear™

Coverage options

7

COVERAGE OPTIONS

Medicare Made Clear™

+

Original Medicare

8

COVERAGE OPTIONS

Medicare Made Clear™

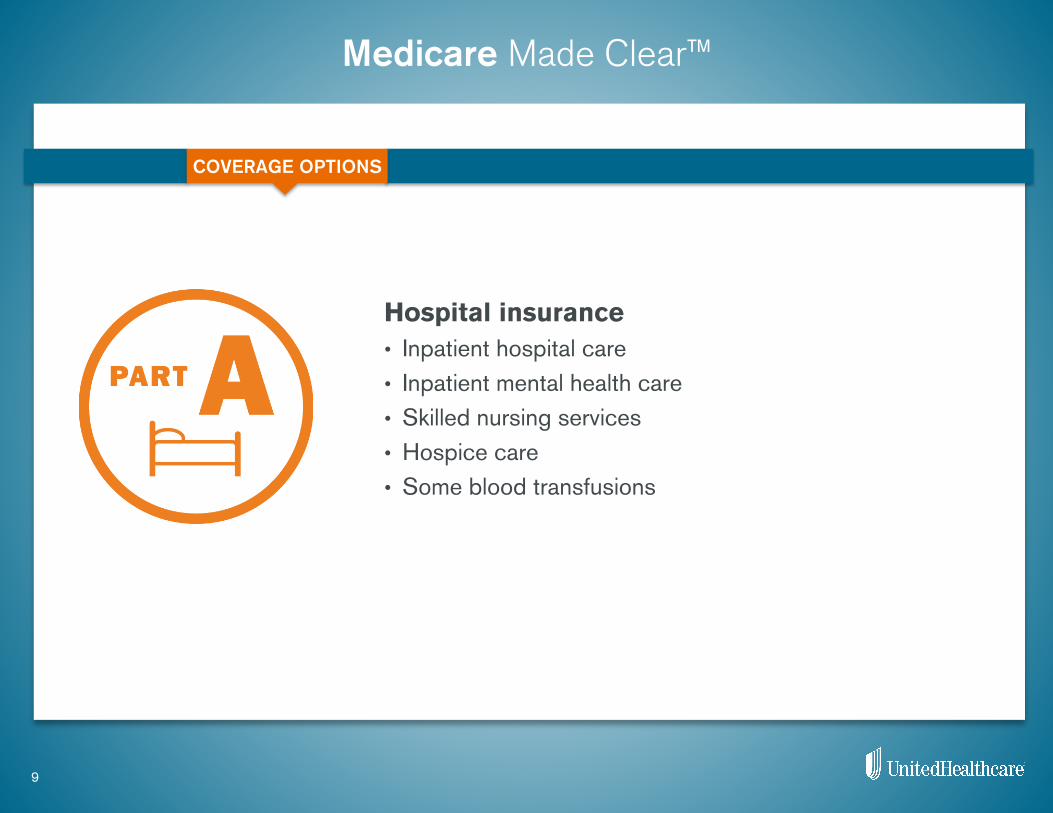

Hospital insurance • Inpatient hospital care • Inpatient mental health care • Skilled nursing services • Hospice care • Some blood transfusions

9

COVERAGE OPTIONS

Medicare Made Clear™

Costs • Most people don’t pay a monthly premium • You pay only your deductible for a hospital stay of

fewer than 60 days

Enrollment • You can’t be turned down because of your medical history

or a pre-existing condition

Coverage • Stays of more than 60 days require a daily copay • Multiple stays may mean multiple deductibles • You can go to any qualified hospital in the U.S. that accepts

new Medicare patients • Hospital care outside the U.S. isn’t usually covered

Fast facts

10

COVERAGE OPTIONS

Medicare Made Clear™

Doctor and outpatient visits • Physician services • Outpatient hospital services • Ambulance • Outpatient mental health • Laboratory services • Durable medical equipment (wheelchairs, oxygen, etc.) • Outpatient physical, occupational and speech-language therapy • Some preventive care

11

COVERAGE OPTIONS

Medicare Made Clear™

Costs • No maximum out-of-pocket • For coinsurance, you pay 20% of Medicare-approved cost • Part B has a monthly premium that is determined by your income • May have higher premiums if you join after your

initial enrollment period

Enrollment • You can’t be turned down because of your medical history

or any pre-existing condition

Coverage • You can get care throughout the U.S., but generally

not outside the country • Participating physicians who accept new Medicare patients • Some preventive health care is provided

Fast facts

12

COVERAGE OPTIONS

Medicare Made Clear™

• Medicare Part A and Part B deductibles, coinsurance and premiums

• Medicare Part B excess charges (amount billed over what Medicare agrees to pay)

• Prescription drug coverage • Additional benefits such as

hearing and dental

What’s not covered

13

COVERAGE OPTIONS

Medicare Made Clear™

Medicare Advantage plan

14

COVERAGE OPTIONS

Medicare Made Clear™

Medicare Advantage plan • Combines Part A and Part B and, in many cases,

includes prescription drug coverage • Offered by private insurance companies like

UnitedHealthcare® • Often includes additional benefits like routine vision

care, hearing care, wellness services and nurse phone line support

15

COVERAGE OPTIONS

Medicare Made Clear™

Eligibility for Part C • Must be enrolled in Medicare Parts A and B • Must live in plan service area • Eligibility is not affected by health or

financial status • Must not have end-stage renal disease

(ESRD)*

16

*There are special rules for ESRD. People with ESRD may be able to join a Medicare Special Needs Plan (SNP) if one is available in their area.

COVERAGE OPTIONS

Medicare Made Clear™

Costs • Plan premiums and terms can change from year to year • Must continue to pay your Part B monthly premium

Coverage • Convenience of one single plan • Many plans include prescription drug coverage (Part D) • Coverage is often limited to a service area — unless it’s an emergency • May be required to see doctors and hospitals that are included in the

plan’s network • May offer additional benefits not covered by Medicare

like dental, vision, hearing and preventive care

Fast facts

17

COVERAGE OPTIONS

Medicare Made Clear™

Coordinated care plans • Health Maintenance Organization (HMO) plans • Preferred Provider Organization (PPO) plans • Special Needs Plans (SNP) • Health Maintenance Organization Point of Service

(HMO-POS) plans

Other plans • Private Fee-For-Service (PFFS) plans • Medical Savings Account (MSA) plans

Types of Part C plans

18

COVERAGE OPTIONS

Medicare Made Clear™

Prescription drug plan

19

COVERAGE OPTIONS

Medicare Made Clear™

Helps with the cost of prescription drugs • Only offered through private insurance companies • You must continue to pay your Part B premium

20

COVERAGE OPTIONS

Medicare Made Clear™

Costs • Prescription drug coverage varies from plan to plan • Catastrophic coverage protects you from very high

drug costs • Benefits can change each year

Coverage • Each plan has a list of drugs that it covers • Make sure your drugs are covered before you enroll

in a plan • The list of drugs can change each year

Enrollment • Coverage is not automatic • Penalties may apply if you enroll late

Fast facts

21

COVERAGE OPTIONS

Medicare Made Clear™

Formulary: A list of drugs that the insurance plan covers

Many drug plans have a tiered formulary. That means the plan divides drugs into groups called “tiers.” Generally, the lower the tier, the lower your copay.

Part D formulary

22

COVERAGE OPTIONS

Medicare Made Clear™

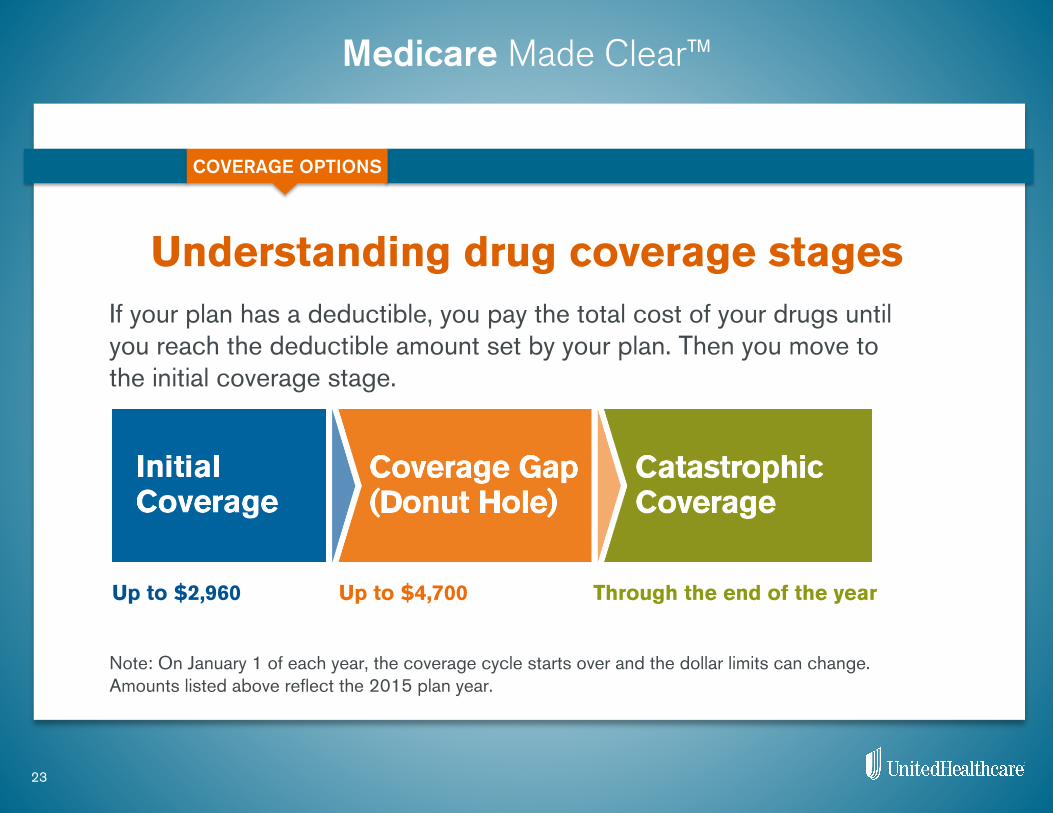

Understanding drug coverage stages

23

If your plan has a deductible, you pay the total cost of your drugs until you reach the deductible amount set by your plan. Then you move to the initial coverage stage.

Up to $2,960 Up to $4,700 Through the end of the year

Note: On January 1 of each year, the coverage cycle starts over and the dollar limits can change. Amounts listed above reflect the 2015 plan year.

COVERAGE OPTIONS

Medicare Made Clear™

Example

24

Heavy prescription drug spending. Enrico, age 66, has several chronic conditions. Without coverage he spends more than $950 a month on drugs. He has Original Medicare (Medicare Part A and Part B), plus a stand-alone Medicare Part D drug plan with a $330 annual premium. Because his drug costs are high, he reaches Stage 3, catastrophic coverage.

COVERAGE OPTIONS

Total annual drug costs without a Medicare Part D drug plan ($950 per month x 12 months) $11,400

Annual premium for Part D drug plan ($27.50 per month x 12 months) $330

Stage 1 – Initial coverage (Enrico’s share during this stage) $720

Stage 2 – Coverage gap (his additional cost-sharing up to the limit) $3,980

Stage 3 – Catastrophic coverage (his share during this stage) $236

Total Enrico pays out-of-pocket for the year $5,266

Total annual savings with Medicare Part D plan: $6,134

Medicare Made Clear™

Standardized Medicare supplement insurance plan

25

COVERAGE OPTIONS

Medicare Made Clear™

• Helps cover some of what Medicare Parts A and B don’t — such as coinsurance, copayments and deductibles

• Offered by private insurance companies • Plans are named A, B, C, D, F, G, K, L, M, N,

and a high-deductible plan, F • Benefits vary by plan • Generally, the more comprehensive the coverage,

the higher the premium

Medicare supplement insurance plan

26

COVERAGE OPTIONS

Medicare Made Clear™

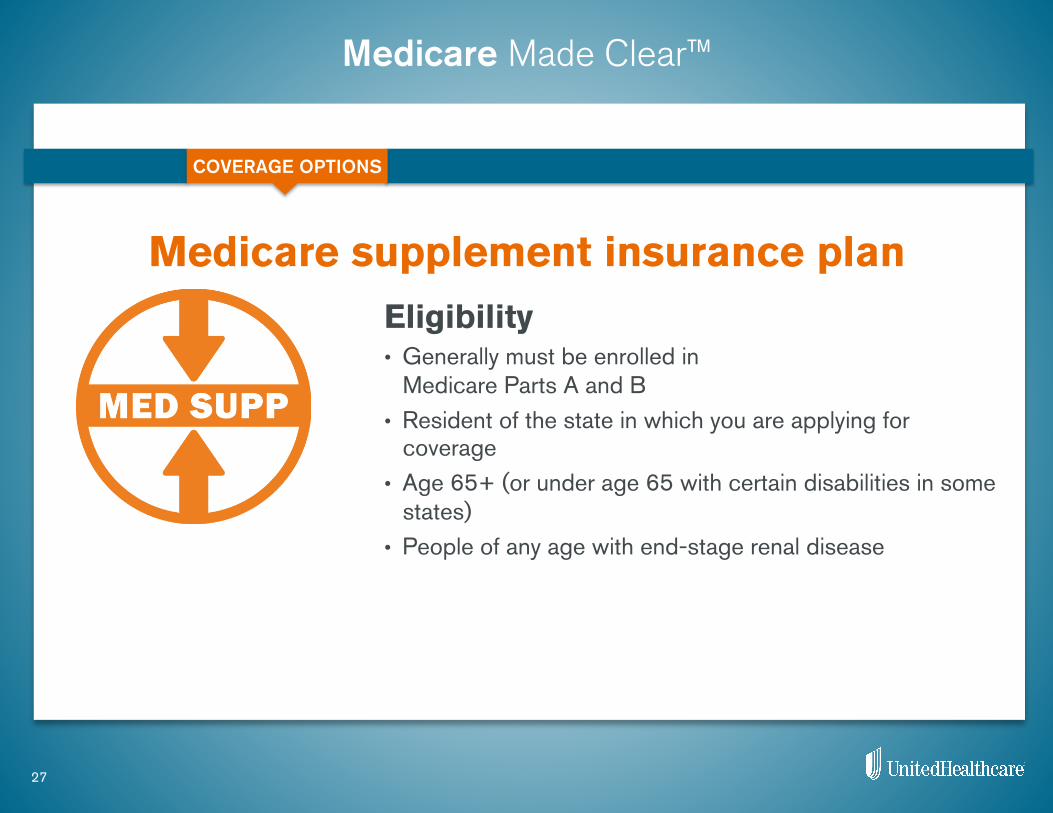

Medicare supplement insurance plan Eligibility • Generally must be enrolled in

Medicare Parts A and B • Resident of the state in which you are applying for

coverage • Age 65+ (or under age 65 with certain disabilities in some

states) • People of any age with end-stage renal disease

27

COVERAGE OPTIONS

Medicare Made Clear™

Costs • Helps with some of the out-of-pocket costs not paid by Medicare • Premiums vary based on the plan and insurance carrier

Enrollment • Guaranteed right to enroll during your

Open Enrollment Period (OEP) • This period begins the first day of the month that you are enrolled in

Medicare Part B, and in most states it lasts for six months • Coverage can be denied if you enroll late

Coverage • Goes with you anywhere in the U.S. • Guaranteed to continue as long as you pay your premium on time and

have not made any material misrepresentation on your application for insurance

Fast facts

28

COVERAGE OPTIONS

Medicare Made Clear™

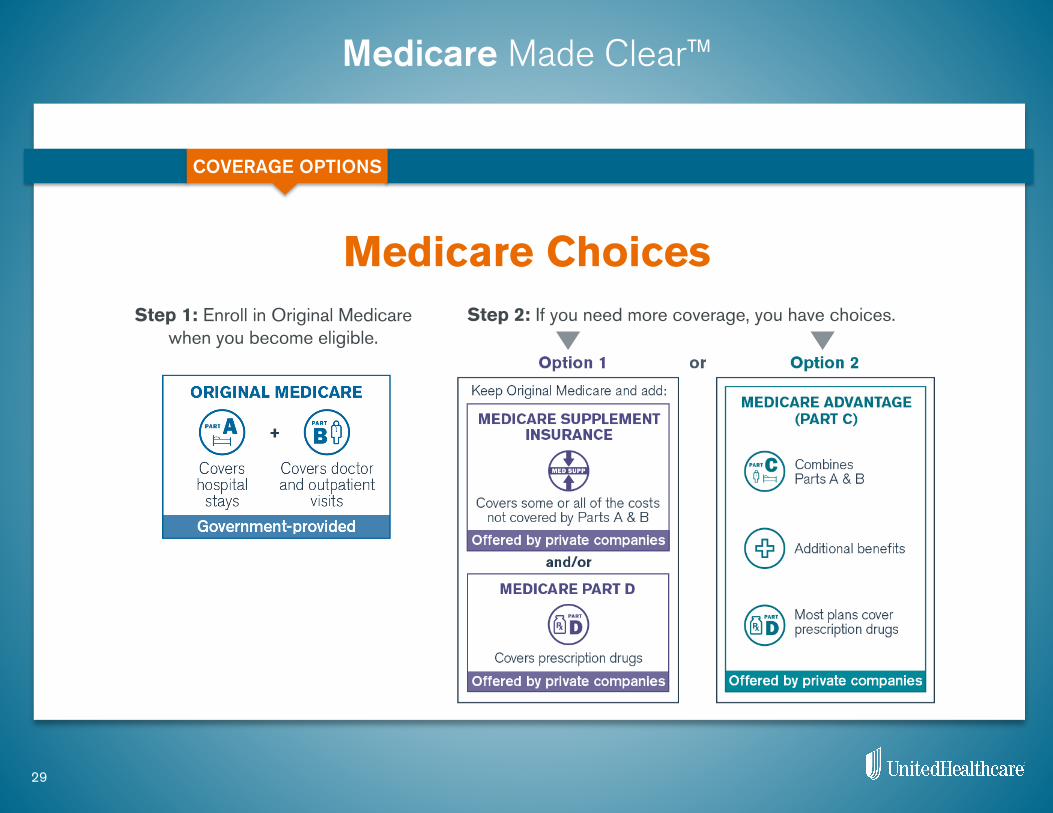

Medicare Choices

29

COVERAGE OPTIONS

Step 1: Enroll in Original Medicare when you become eligible.

Step 2: If you need more coverage, you have choices.

Medicare Made Clear™

Medicare Made Clear™

Parts A and B

ENROLLMENT

When can I first enroll? • The three months before your 65th birthday, the month of, and the three months after • Enrollment in Part A is automatic if you are already receiving Social Security Benefits

What if I’m late? • For Part A, usually no penalties (unless you didn’t pay enough into Social Security) • For Part B, premiums will be higher after the Initial Enrollment Period (unless you qualify for an exception)

31

YOUR ELIGIBILITY MONTH

65

Initial Enrollment Period

THREE MONTHS AFTER THREE MONTHS BEFORE

Medicare Made Clear™

32

ENROLLMENT

Enrolling after the Initial Enrollment Period. Susan waited to sign up for Part B three full years after she was eligible. She’ll pay a 10% penalty for each full 12-month period she waited. The penalty is added to the Part B monthly premium, which is $104.90 in 2015.

Example

2015 standard Part B premium $104.90

3 years x 10% = 30% of $104.90 $31.47

Susan’s part B monthly premium for 2015 $136.37

Medicare Made Clear™

When can I first enroll?

What if I’m late? Wait until the Open Enrollment Period (OEP), Oct. 15 – Dec. 7.

Parts C and D

33

ENROLLMENT

YOUR ELIGIBILITY MONTH

65

Initial Enrollment Period

THREE MONTHS AFTER THREE MONTHS BEFORE

Medicare Made Clear™

What if I work past age 65?

34

If working past age 65 • May enroll in Medicare Parts A and B • Recommend talking to your benefit administrator • Keep records of your health insurance coverage

Retiring after 65 • When retiring, you’re eligible for a Special Enrollment Period • Allows for 63 days after employer-sponsored coverage ends to enroll in a Medicare plan without penalty —

best to sign up before you retire to avoid a lapse in coverage

ENROLLMENT

Medicare Made Clear™

When can I first enroll? Your state may have a six-month guaranteed window that starts when you turn 65 and enroll in Part B.

What if I’m late? You can apply later but may be charged a higher premium due to existing health problems, or rejected depending on your health history.

Medicare supplement insurance plans

35

MONTH YOU QUALIFY

65

Open Enrollment Period

FIVE MONTHS AFTER

ENROLLMENT

Medicare Made Clear™

Medicare Made Clear™

1 Review enrollment periods

2 Research your options

3 Ask questions

4 Get answers

5 Find financial help

6 Enroll

7 Yearly review

NEXT STEPS

37

Medicare Made Clear™

Medicare Made Clear™

39

SAVING MONEY

Maximize your benefits • Utilize preventive services • Stay in your network • Look for “extra” benefits compared with

Original Medicare

Medicare Made Clear™

40

What should I think about as I compare my options?

Health status • Has my health changed?

Finances • Has my financial situation changed?

Location • Have I moved? (Could qualify for SEP) • Will I be away from my hometown for a

significant period of time in the next year? • How frequently do you travel and where?

My coverage needs • Are my doctors and hospital in-network? • Are my prescriptions covered? • Could I benefit from coverage for things

like a gym membership, routine dental care, hearing aids, etc.?

SAVING MONEY

Medicare Made Clear™

Medicare Made Clear™

RESOURCES

42

MedicareMadeClear.com • Videos • Newsletter • Quizzes • Tools • Answers

Medicare Made Clear™

National Medicare Education Week • UnitedHealthcare created National Medicare Education

Week (NMEW), September 15–21 • Designed to help consumers learn about Medicare

and find the coverage that meets their needs • More than 30 events across the country • Additional online tools and resources available

RESOURCES

43

Medicare Made Clear™

• Visit Medicare.gov

• Call 1-800-MEDICARE (1-800-633-4227), TTY 1-877-486-2048, 24 hours a day/7 days a week

• Call your State Health Insurance Assistance Program (SHIP) to see if you qualify for any financial assistance

Additional information resources

44

RESOURCES

Medicare Made Clear™

Medicare Made Clear™

Copyright ©2014 United HealthCare Services, Inc. All rights reserved. No portion of this work may be reproduced or used without express written permission of United HealthCare Services, Inc., regardless of commercial or non-commercial nature of the use. Plans are insured through UnitedHealthcare Insurance Company or one of its affiliated companies, a Medicare Advantage organization with a Medicare contract and a Medicare-approved Part D sponsor. Enrollment in the plan depends on the plan’s contract renewal with Medicare.

14_15 SPRJ20813 Y0066_140402_112351 Approved

46

Related Documents