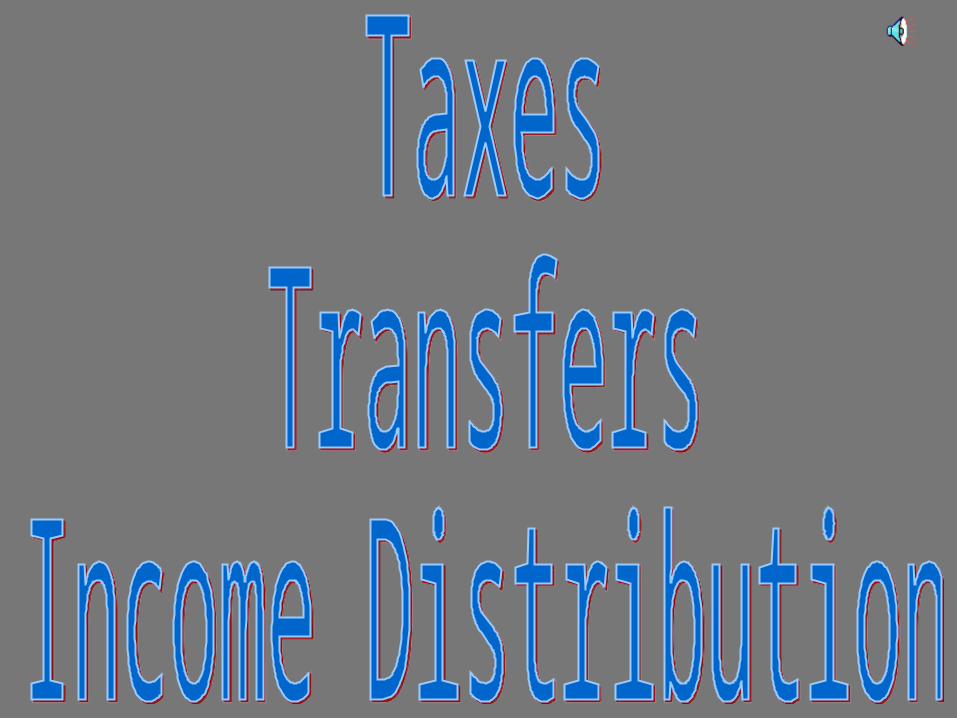

Types of Taxes personal income tax (all types of income) payroll tax (15.3 % of wage and salary income) corporate income tax (corporate profits) excise.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Types of Taxes

• personal income tax (all types of income)

• payroll tax (15.3 % of wage and salary income)

• corporate income tax (corporate profits)

• excise tax (gasoline, liquor, sales)

• estate and gift tax

• tariffs on imports

• property taxes

Federal Taxes14_01

PERCENT OFFEDERAL TAXREVENUE

50

Personal income taxes

Payroll taxes

Corporate income taxes

Excise taxes

Tariffs Estate and gift taxes

40

30

20

10

0

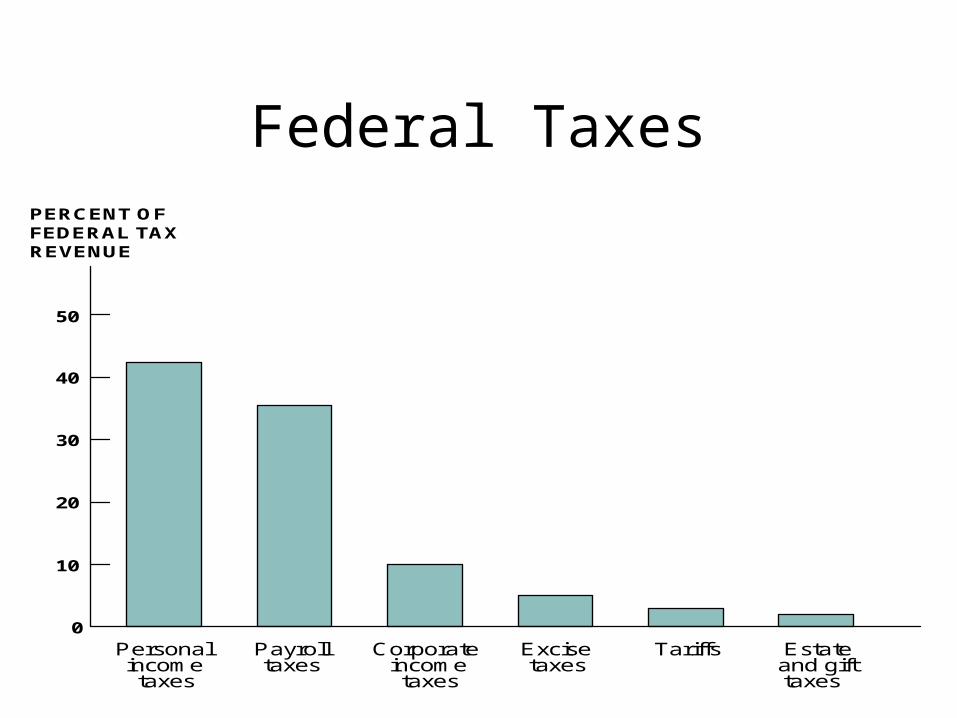

Income Tax Terminology

• taxable income = income less• exemptions ($2550 per person)

• deductions (e.g. $4000 for single taxpayer

• marginal tax rate– tax paid on an additional dollar earned

• average tax rate– total taxes as a percent of total income

14_02ABBREVIATED 1040 FORMLine 37 Taxable incomeLine 38 Tax

Schedule X Use if your filing status is Single

If the amount onForm 1040, line37, is:

Over

$024,00058,150

121,300263,750

But notover

$24,00058,150

121,300263,750

- - - - - - -

Enter onForm 1040,line 38

of theamountover

- - - - - - - - - - 15%28%31%36%

39.6%

$3,600.00 +13,162.00 +32,738.50 +84,020.50 +

$024,00058,150

121,300263,750

Schedule Y-1 Use if your filing status is Married filingjointly or Qualifying widow(er)

If the amount onForm 1040, line37, is:

Over

$040,10096,900

147,700263,750

But notover

$40,10096,900

147,700263,750

- - - - - - -

Enter onForm 1040,line 38

of theamountover

- - - - - - - - - - 15%28%31%36%

39.6%

$6,015.00 +21,919.00 +37,667.00 +79,445.00 +

$040,10096,900

147,700263,750

Taxableincome

Marginaltaxrates

Progressive, Regressive, or Proportional?

14_03

MARGINAL

TAX RATE

(PERCENT)

40

30

20

10

50,000 100,000 150,000 200,000 250,000

TAXABLE INCOME (DOLLARS)

300,0000

What is the Flat Tax?

• Big exemption – $35000 would be the “zero-bracket” amount for

a family of four

• Flat rate for all income above

• Hall-Rabushka version: – Tax wage and salary income at the household

level– Interest, dividends taxed at the firm level

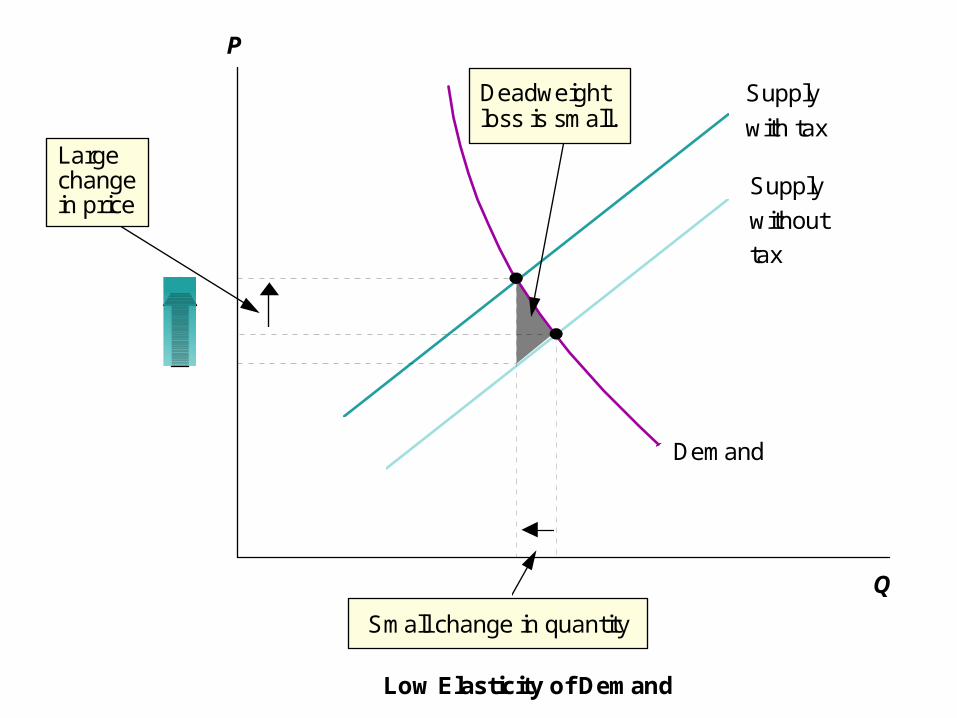

Review of the Effect of Putting a Tax on a Commodity

• Price rises, but by less than the tax

• Quantity declines

• Deadweight loss – size depends on how much quantity declines

• Incidence of the Tax– who bears more of the burden of the tax

• consumers or firms?

– Depends on how much the price rises

14_04A

Large change in price

Low Elasticity of Demand

Supply

with tax

Supply

without

tax

Q

P

Demand

Deadweight loss is small.

Small change in quantity

14_04B

P

High Elasticity of Demand

Q

Supply with tax

Supply without tax

Demand

Deadweight loss is large.

Large change in quantity

Small change in price

14_04C

Deadweight loss is small.

P

Low Elasticity of Supply

Q

Demand

Supply with tax

Supply without tax

Small change in price

Small change in quantity

14_04D

P

High Elasticity of Supply

Q

Supply with tax

Supply without tax

Demand

Deadweight loss is large.

Large change in quantity

Large change in price

Effect of a Tax on Labor Income

14_05WAGE PAID TO WORKER

HOURS OF WORK

Labor demand

New labor supply

Old labor supply

Labor supply shifts up because of the tax increase.

Quantity of labor reduced by this amount

Payroll Tax: Firm versus Worker14_06 WAGE PAID

TO WORKER

HOURS OF WORK

Old demand

Supply

Wage paid to worker falls.

New demand

Old supply

Demand

New supply

Here the employer pays the tax: the labor demand curve shifts down.

Here the worker pays the tax: the labor supply curve shifts up.

But the eventual impact is the same: the length of the black arrows are the same on the left and the right.

WAGE PAID TO WORKER

HOURS OF WORK

Tax

Decline in after- tax wage

Wage paid to the workerrises slightly, but afterthe tax is paid, thedecline in the after-tax wage is the same as when the employer pays the tax.

Effects of Tax Rate Changes on Tax Revenues (T14.1 Modified)

TaxRevenuesT = twL

TaxRate(t)

WagePer hour(w)

HoursWorked(L)

$8000 .4 $20 1000

$8400 .6 $20 700

$6400 .8 $20 400

The Laffer Curve14_07

TAX REVENUE0

TAX RATE (PERCENT)

Revenue first increases as the tax rate increases and then declines.

100

The Dynamic Scoring Debate

• Consider cutting the tax rate from .6 to .4

• Before the tax cut, L = 700 hours– thus: 0.6 times $14000 = $8400

• Static scoring, L stays at 700 hours– thus: 0.4 times $14000 = $5400

• Dynamic scoring, L rises to 1000 hours– thus: 0.4 times $20000 = $8000

The Equality-Efficiency Trade-Off:

As tax rates get higher (in an effort to improve equity) there is less production (less efficiency)

and perhaps less revenue to redistribute

Transfer Payments

• Means-tested programs– family support programs (formerly AFDC until

welfare reform of 1996)– medicaid– food stamps– Earned Income Tax Credit (EITC)

• Social Insurance Programs– social security– medicare– unemployment insurance

Two Welfare Reform Options

14_08

Incomefrom work

HOURS OF WORK

TOTAL INCOME

HOURS OF WORK

HOURS OF WORK

Reform by phasing out payments more slowly

Reform by paying less welfare

TOTAL INCOME

TOTAL INCOME

Welfare is paid to those with high incomes.

Welfare payment is small to the very poor.

Welfarepayment

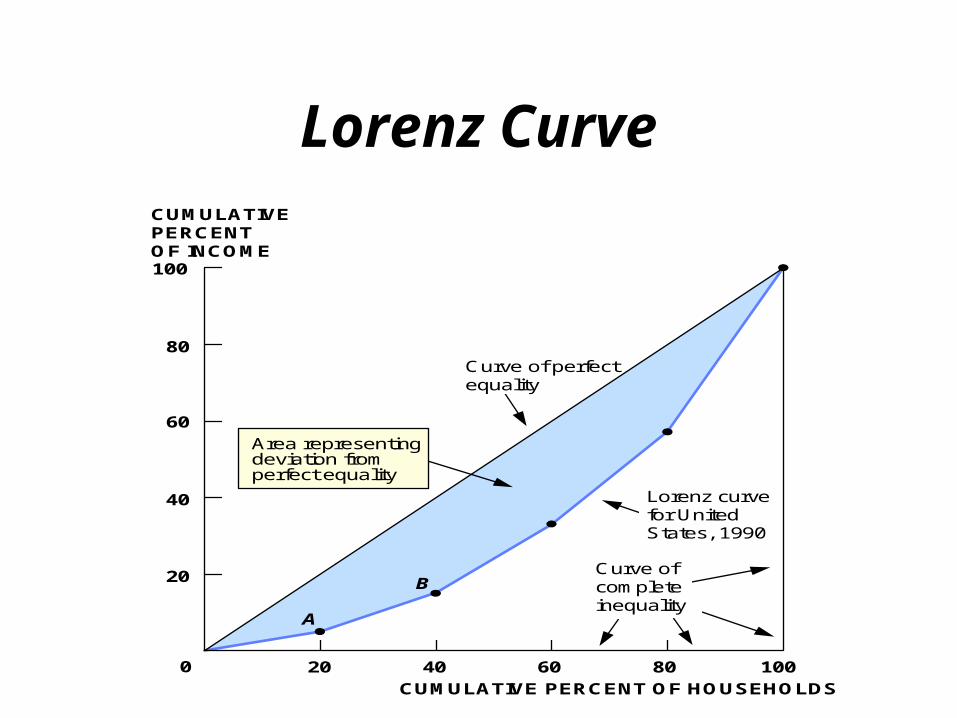

Income Distribution in the U.S.

HouseholdQuintile

Percent ofIncome

CumulativePercent

Lower 20% 5 5

Second 20% 11 16

Third 20% 17 33

Fourth 20% 24 57

Top 20% 43 100

Lorenz Curve14_11

CUMULATIVE PERCENT OF HOUSEHOLDS

CUMULATIVE PERCENT OF INCOME100

80

60

40

20

20 40 60 80 100

Curve of perfect equality

Lorenz curve for United States, 1990

Curve of complete inequality

B

A

Area representing deviation from perfect equality

0

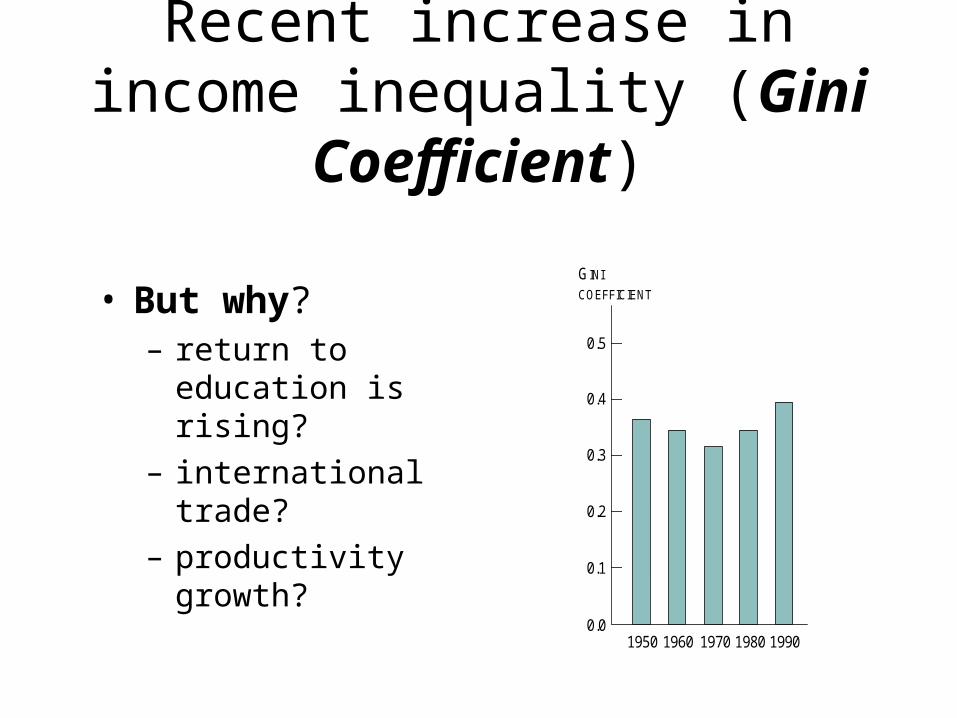

Recent increase in income inequality (Gini Coefficient)

• But why? – return to education is

rising?

– international trade?

– productivity growth?

14_12

GINI

COEFFICIENT

0.4

0.3

0.2

0.1

0.01950 1960 1970 1980 1990

0.5

Poverty Rate in the United States

14_13

20

15

10

5

01970 1980 1990 1994

25

30

35

40

PERCENT

1960

Poverty rate

for aged

Poverty rate

for children

Overall poverty rate

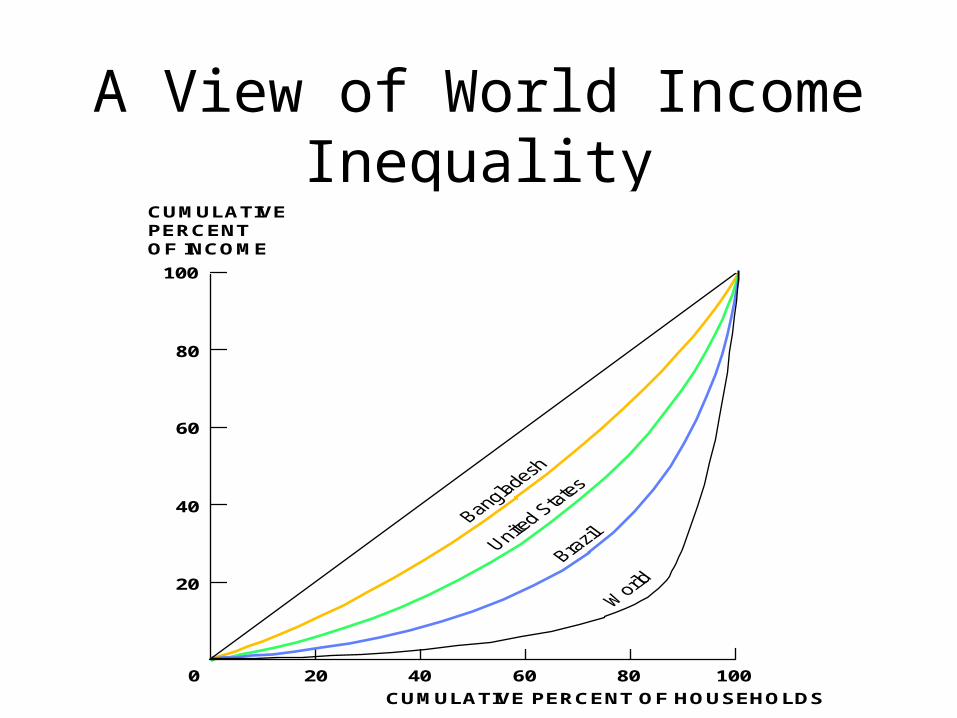

A View of World Income Inequality

14A

CUMULATIVE PERCENT OF HOUSEHOLDS

CUMULATIVEPERCENTOF INCOME

100

80

60

40

20

20 40 60 80 1000

People Moving from Quintile to Quintile

• About 60 percent of households move from one quintile to another quintile over a ten year span– About one-half of those in the bottom quintile

move out of the bottom quintile – About one-half of those in the top quintile

move out of the top quintile

1000 Points of Light?

Related Documents