Transfer Pricing Workshop Experience in the wake of the Italian transfer pricing documentation requirements implemented in 2010 in view of the preparation of the financial statements and TP documentation for FY 2011 and beyond Milan, March 15 and April 17, 2012 Rome, March 21 and April 18, 2012

Transfer pricing workshop March April 2012 - eng version

Oct 21, 2014

Slide of our tax workshop on Italian transfer pricing developments and experience - March-April 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Transfer Pricing Workshop

Experience in the wake of the Italian transfer pricing documentation requirements implemented in

2010 in view of the preparation of the financial statements and TP documentation for FY 2011 and

beyond

Milan, March 15 and April 17, 2012

Rome, March 21 and April 18, 2012

2

Milan

Michele Ghiringhelli – [email protected]

Gaetano Pizzitola – [email protected]

Patrizia Occhiuto – [email protected]

with the participation of Giusi Lamicela, Stefano Luvisutti and Antonio Sgroi

Rome

Gaetano Pizzitola

Michele Ghiringhelli

Daniele Sabatini – [email protected]

Fabio Zampini – [email protected]

Francescomaria Serao – [email protected]

with the participation of Giusi Lamicela, Luca Gasparrini, Marianna Delle Foglie and Marta Selicato

Speakers

Transfer Pricing Workshop - March-April 2012

3

TP: Corporate governance, tax risk management and tax planning

Intercompany transactions – the burden of tax documentation and other corporate and regulatory

compliance

Interaction between tax functions and other business functions in the drafting of the group policy

documentation

Best practices in the implementation of a common strategy by both corporate tax functions and

external tax consultants

Critical review of past experience

Experience in the preparation of the documentation until FY 2010

Experience in tax audits

Case Law

Evaluation of the TP documentation from a criminal tax law standpoint

TP documentation in case of business restructuring, black list, abuse of law, and PE claims

TP Management: ex post documentary compliance and APA

The burden of (documentary) proof in Italy and in other Countries – consistent approach vs Country by

Country approach?

Pros and Cons of the different approaches

Conclusions

Agenda

Transfer Pricing Workshop - March-April 2012

Part One

TP: Corporate governance, tax risk management and tax planning

5

Intercompany transactions – the burden of tax documentation and other corporate and

regulatory compliance

Interaction between tax functions and other business functions in the drafting of the group

policy documentation

Best practices in the implementation of a common strategy by both corporate tax functions

and external tax consultants

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

6

TRANSFER PRICING AS A MEAN OF CORPORATE GOVERNANCE

Business strategies

Management and functional control

Business value

Market and shareholder minority expectations

Directors’ Liability

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

7

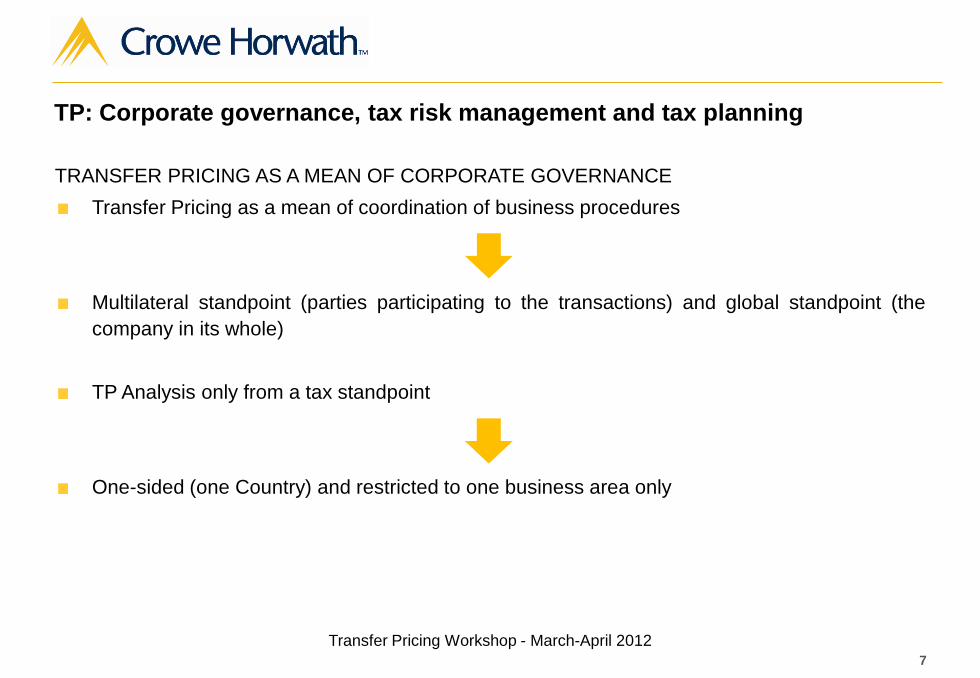

TRANSFER PRICING AS A MEAN OF CORPORATE GOVERNANCE

Transfer Pricing as a mean of coordination of business procedures

Multilateral standpoint (parties participating to the transactions) and global standpoint (the

company in its whole)

TP Analysis only from a tax standpoint

One-sided (one Country) and restricted to one business area only

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

8

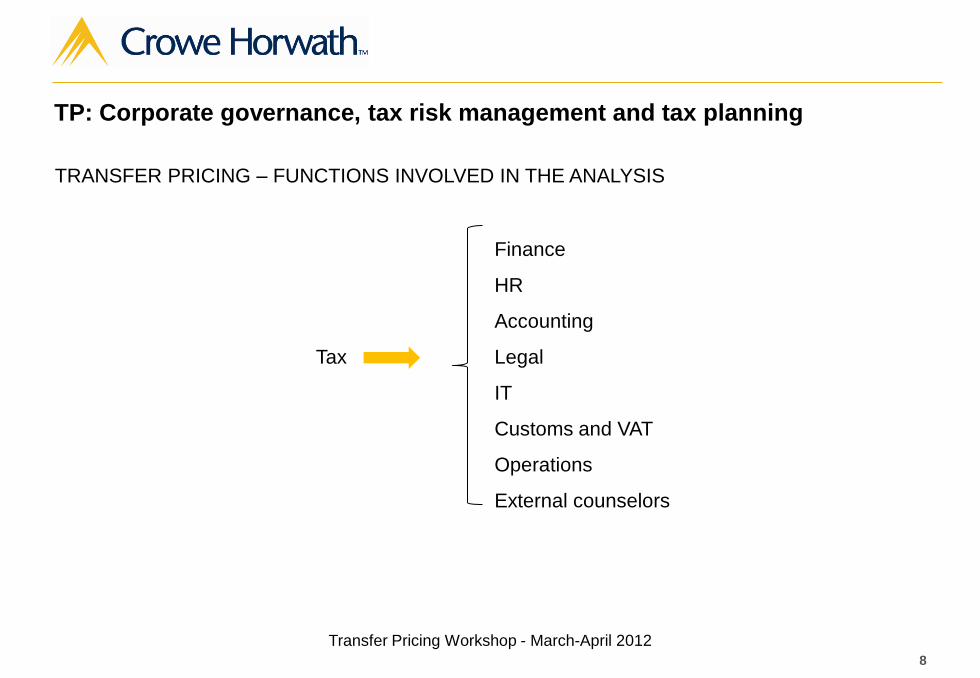

TRANSFER PRICING – FUNCTIONS INVOLVED IN THE ANALYSIS

Finance

HR

Accounting

Tax Legal

IT

Customs and VAT

Operations

External counselors

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

9

TRANSFER PRICING – INCOME TAXATION VS OTHER TAXES

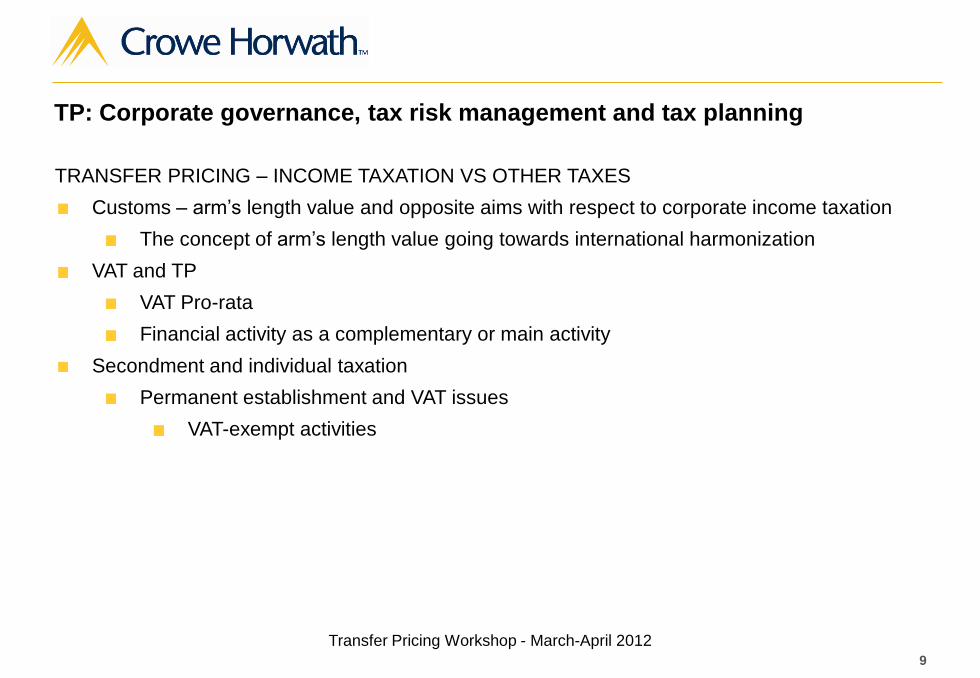

Customs – arm’s length value and opposite aims with respect to corporate income taxation

The concept of arm’s length value going towards international harmonization

VAT and TP

VAT Pro-rata

Financial activity as a complementary or main activity

Secondment and individual taxation

Permanent establishment and VAT issues

VAT-exempt activities

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

10

TRANSFER PRICING AND RISK MANAGEMENT

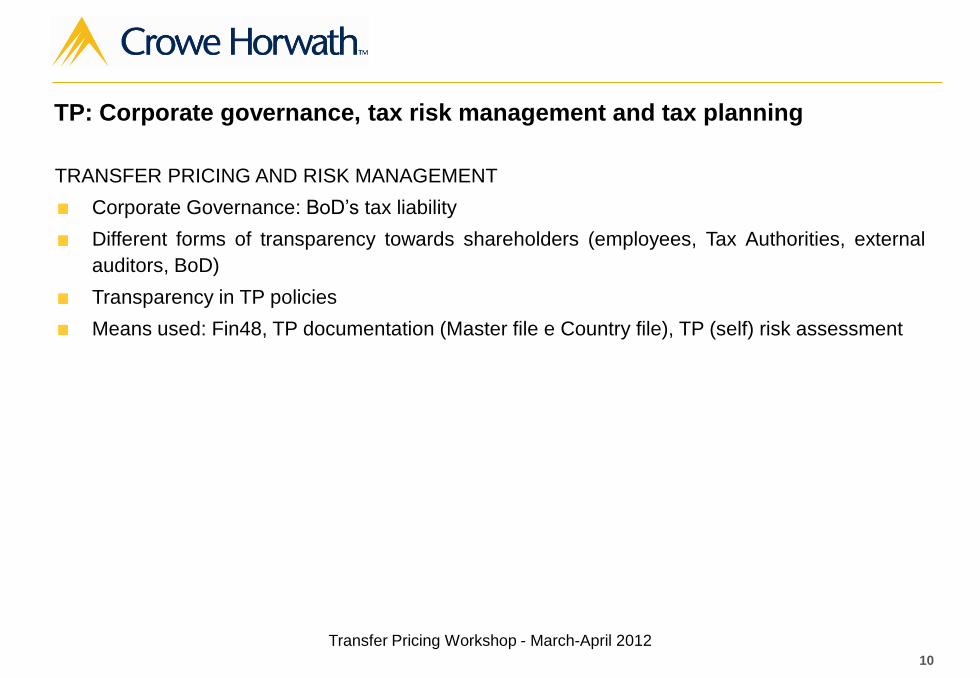

Corporate Governance: BoD’s tax liability

Different forms of transparency towards shareholders (employees, Tax Authorities, external

auditors, BoD)

Transparency in TP policies

Means used: Fin48, TP documentation (Master file e Country file), TP (self) risk assessment

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

11

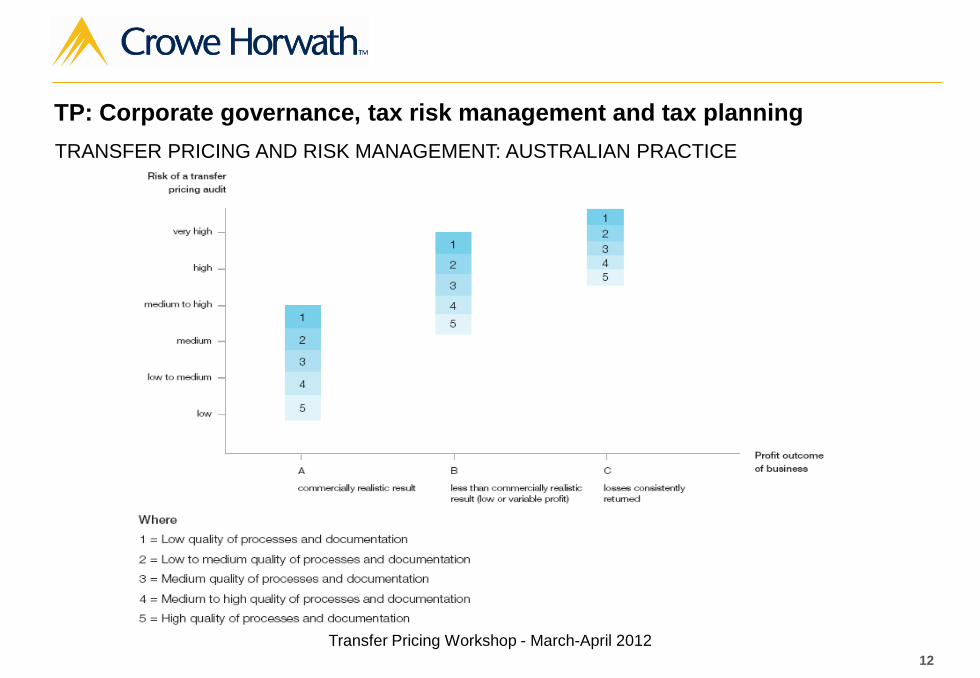

TRANSFER PRICING AND RISK MANAGEMENT: AUSTRALIAN PRACTICE

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

12

TRANSFER PRICING AND RISK MANAGEMENT: AUSTRALIAN PRACTICE

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

13

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

Entities having a direct or indirect influence on the company so that the decision-making process

is altered

Protection of business assets

Protection of market and shareholder interest

Transparency and integrity of conduct

Internal control rules aiming at the correct management of the company

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

14

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

Italian Civil Code: ensure business asset integrity for the protection of minority shareholders and of

third party creditors

Directors’ interests

Intercompany transactions

Content of the explanatory notes to the financial statement

Direction and coordination

Liability

Advertising

Reasons underlying the decisions

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

15

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

International Accounting Standard 24 – ensure that the financial statements are inclusive of the

supplementary information that show that its assets and financial situation together with its

economic result may have been affected by the existence of related parties and of intercompany

transactions

Information on intercompany transactions

CONSOB Regulation no. 17221 dated March 12, 2010 for companies listed in the stock market

and CONSOB Code of Conduct

Transparency and substantial/procedural consistency of the transactions from which conflicts

may arise

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

16

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

Italian Civil Code: no fair value definition provided

CONSOB Regulation no. 17221 (and amendments that followed), article 3, adopted as per

article 2391-bis of the Italian Civil Code: “for equivalent conditions to market or standard ones”

such as the “same conditions to those usually adopted with third parties for transactions of

corresponding nature, size or risk, or based on prescribed rates or prices or those adopted on

entities with which the issuer is obliged by law to contract at a certain price”

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

17

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

IAS 24: intercompany transactions carried out at same conditions to those adopted in

transactions between independent parties

OIC 12: “arm’s length conditions” are not the quantitative conditions related to the price.

Explanatory Report to the Decree: “arm’s length conditions” should not be considered only

those related to the “price” of the transaction and to the related elements, but also the reasons

that have led to the decision of closing the transaction with related parties as opposed to

independent ones

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

18

INTERCOMPANY TRANSFER PRICING TRANSACTIONS

Italian Civil Code: no information concerning the kind of documentation that needs to be prepared

with reference to intercompany transactions is provided

As per article 5 of the CONSOB Regulation no. 17221 (and amendments that followed), “with

reference to major transactions the companies prepare a document that provides relevant

information and that is drafted in compliance to appendix no. 4”

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

19

TRANSFER PRICING AND TAX PLANNING

Importance of the management model

Centralization

Decentralization

Impact of the globalization

Importance of the FAR (Functions, Assets and Risks)

Transfer pricing and business restructuring

Consistency between contractual schemes and economic substance

Transfer pricing as a mean of defense for the organizational structure of the group

TP: Corporate governance, tax risk management and tax planning

Transfer Pricing Workshop - March-April 2012

Part Two

Critical review of past experience

21

Experience in the preparation of the documentation until FY 2010

Experience in tax audits

Case Law

Evaluation of the TP documentation from a criminal tax law standpoint

TP documentation in case of business restructuring, black list, abuse of law, or PE claims

Critical review of past experience

Transfer Pricing Workshop - March-April 2012

22

CRITICAL TRANSACTIONS

Management Fees preliminary inherence and back up documentation

Royalties determination of the arm’s length value

Safe harbor’s limits

Financial Transactions group’s rating and warranties

Secondment functional analysis

OECD draft on Permanent Establishment (Art.5)

OECD Commentary art. 15

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

23

FURTHER CRITICAL ASPECTS

TNMM base costs, statutory vs fiscal

Italian tax principles, IAS, US GAAP, management reporting?

Budget, Standard or Actual Cost?

Gross margins functional compatibility and availability of financial data

Comparables inclusion of companies subject to tax sector studies or simplified budget

Comparables searches pan- European vs domestic searches and reference period

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

24

EXPERIENCE IN TAX AUDITS

Penalty protection Adopted method

Formal or substantial mistakes or omissions

Search selections’ criteria

Incoherence of the comparables functional profile

Lack of adequate information

Penalty application Missing information on instrumental assets used

Incomplete documentation or incorrect information

Importance of an advanced cross examination: particular complexity/inadequacy reasonably not

accepted by the taxpayer/adjustment for an amount higher than € 10 million

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

25

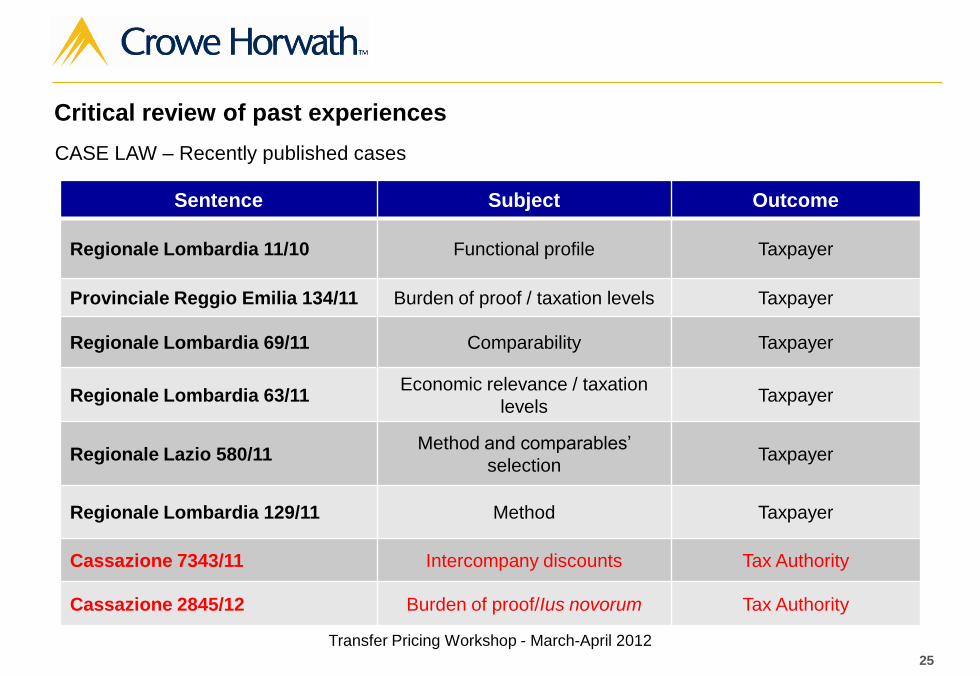

CASE LAW – Recently published cases

Sentence Subject Outcome

Regionale Lombardia 11/10 Functional profile Taxpayer

Provinciale Reggio Emilia 134/11 Burden of proof / taxation levels Taxpayer

Regionale Lombardia 69/11 Comparability Taxpayer

Regionale Lombardia 63/11 Economic relevance / taxation

levels Taxpayer

Regionale Lazio 580/11 Method and comparables’

selection Taxpayer

Regionale Lombardia 129/11 Method Taxpayer

Cassazione 7343/11 Intercompany discounts Tax Authority

Cassazione 2845/12 Burden of proof/Ius novorum Tax Authority

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

26

CASE LAW

Tax Court decisions favorable to taxpayers in past years

Non sufficiently motivated and detailed tax audits

Solid defenses based on substance

Most TP judgments with analysis on factual elements

Importance of a detailed defense based on facts

Limited number of case law decisions

Tax amnesty effect

Adhesion and conciliations

Unpublished cases?

Recent Supreme Court judgments against taxpayers fully motivated on a factual/legal

standpoint

Corroboration of Court decisions based on a factual approach

Inadequate factual defense by the Judge of Merits

Is it realistic to expect such a favorable trend in the future?

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

27

EVALUATION OF THE TRANSFER PRICING DOCUMENTATION FROM A CRIMINAL TAX LAW

STANDPOINT

Twofold profile

Transactions not justified by any economic reason

Fraudulent misrepresentation

Coincidence between factual reality and documentation content

Quantification problems both in excess or in deficiency – exclusion as per article 4 of

Legislative Decree 74/2000

Relevance of the explanatory notes on intercompany transactions and lack of criminal intent

aimed at tax evasion

Explanatory Report to Legislative Decree 74/2000: taxpayer’s good conduct affects the evaluation

on penalties in presence of specified criteria

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

28

TRANSFER PRICING DOCUMENTATION IN CASE OF BUSINESS RESTRUCTURING, BLACK

LIST, ABUSE OF LAW OR HIDDEN PE CLAIMS

Transfer pricing documentation and economic substance of business restructuring

transactions

Transfer pricing documentation to prove black list exemptions

Transfer pricing documentation and problems concerning the reclassification of PEs

Critical review of past experiences

Transfer Pricing Workshop - March-April 2012

Part Three

TP Management: ex post documentary compliance and APA

30

The burden of (documentary) proof in Italy and in other Countries – consistent approach vs

Country by Country approach?

Pros and Cons of the different approaches

TP Management: ex post documentary compliance and APA

Transfer Pricing Workshop - March-April 2012

31

The burden of (documentary) proof in Italy and in other Countries – consistent approach vs

Country by Country approach?

Country by Country approach: obstacle to the free movement of people & capitals

Country by Country approach: different compliance is anti-economic

OECD: Chapter V of the 2010 Guidelines: “reasonable efforts”

UE: Code of conduct of 2006

PATA: Documentation package of 2003

ICC: Sample Documentation Package of 2008

TP Management: ex post documentary compliance and APA

Transfer Pricing Workshop - March-April 2012

32

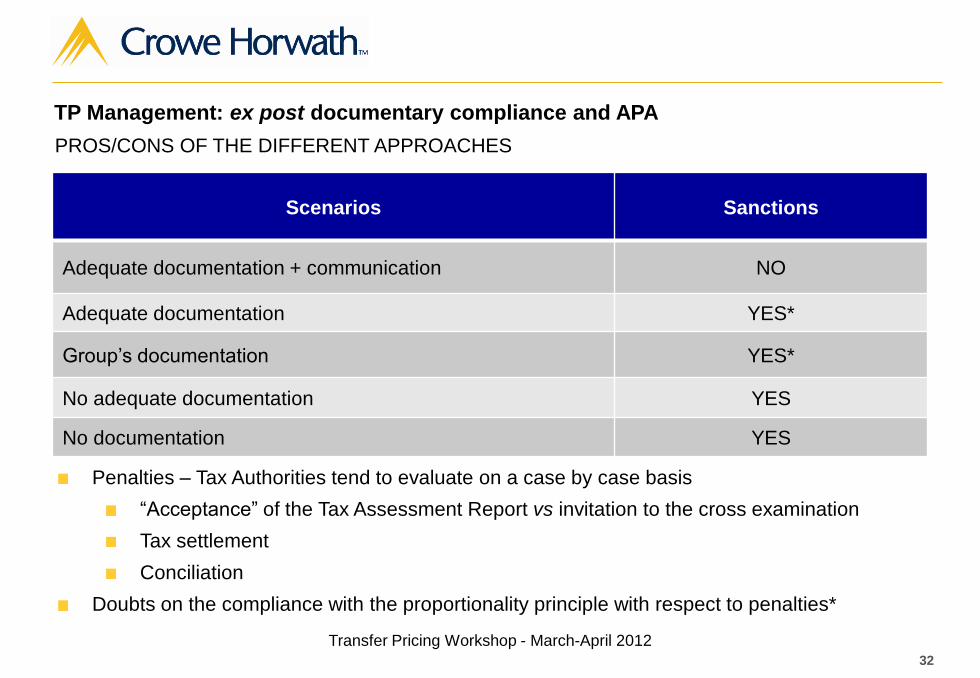

PROS/CONS OF THE DIFFERENT APPROACHES

Scenarios Sanctions

Adequate documentation + communication NO

Adequate documentation YES*

Group’s documentation YES*

No adequate documentation YES

No documentation YES

Penalties – Tax Authorities tend to evaluate on a case by case basis

“Acceptance” of the Tax Assessment Report vs invitation to the cross examination

Tax settlement

Conciliation

Doubts on the compliance with the proportionality principle with respect to penalties*

TP Management: ex post documentary compliance and APA

Transfer Pricing Workshop - March-April 2012

33

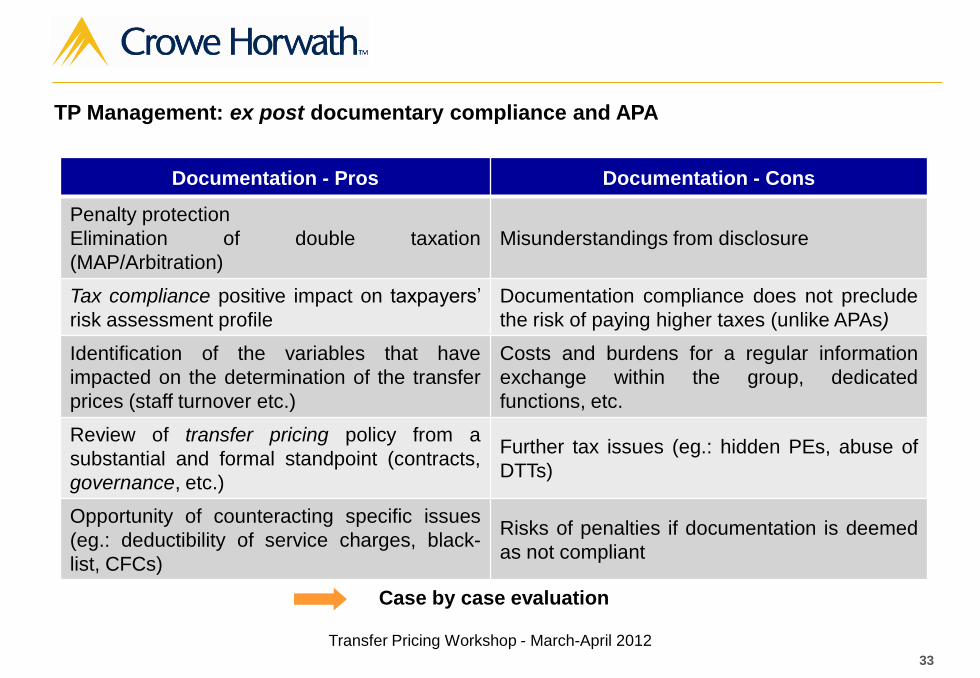

Documentation - Pros Documentation - Cons

Penalty protection

Elimination of double taxation

(MAP/Arbitration)

Misunderstandings from disclosure

Tax compliance positive impact on taxpayers’

risk assessment profile

Documentation compliance does not preclude

the risk of paying higher taxes (unlike APAs)

Identification of the variables that have

impacted on the determination of the transfer

prices (staff turnover etc.)

Costs and burdens for a regular information

exchange within the group, dedicated

functions, etc.

Review of transfer pricing policy from a

substantial and formal standpoint (contracts,

governance, etc.)

Further tax issues (eg.: hidden PEs, abuse of

DTTs)

Opportunity of counteracting specific issues

(eg.: deductibility of service charges, black-

list, CFCs)

Risks of penalties if documentation is deemed

as not compliant

Case by case evaluation

TP Management: ex post documentary compliance and APA

Transfer Pricing Workshop - March-April 2012

34

INTERNATIONAL TAX RULING – APA

Unilateral international tax ruling

Bilateral APA in application of DTTs

TP Management: ex post documentary compliance and APA

Transfer Pricing Workshop - March-April 2012

35

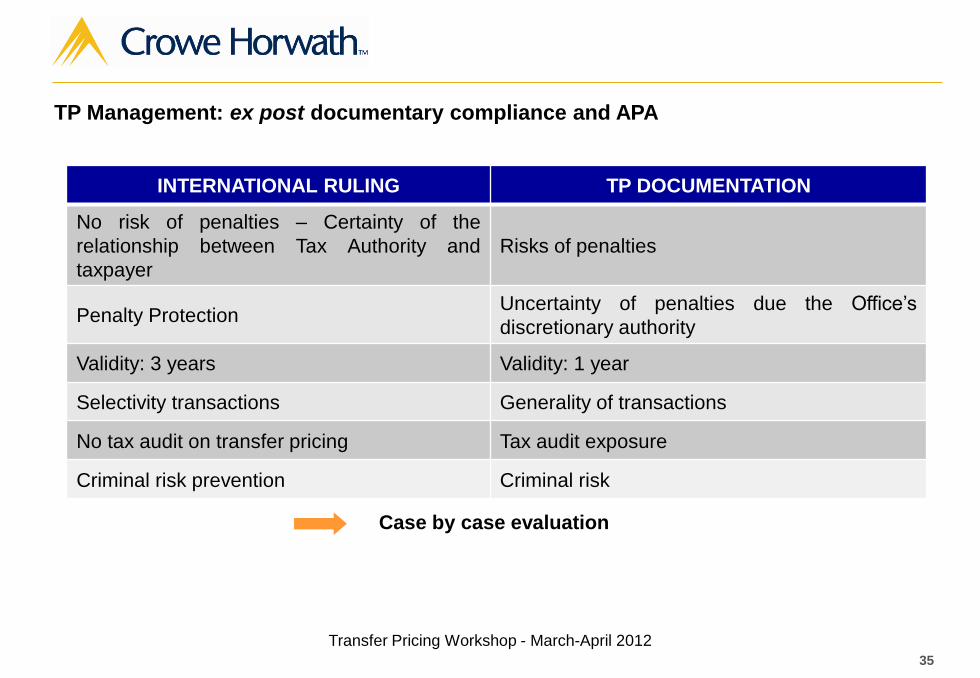

INTERNATIONAL RULING TP DOCUMENTATION

No risk of penalties – Certainty of the

relationship between Tax Authority and

taxpayer

Risks of penalties

Penalty Protection Uncertainty of penalties due the Office’s

discretionary authority

Validity: 3 years Validity: 1 year

Selectivity transactions Generality of transactions

No tax audit on transfer pricing Tax audit exposure

Criminal risk prevention Criminal risk

TP Management: ex post documentary compliance and APA

Case by case evaluation

Transfer Pricing Workshop - March-April 2012

Conclusions

37

Impact of the new tax law

The transfer pricing dogmas and their limitations

Case by case evaluation pros/cons submission of documentation

Prospective approach to the TP documentation

Review of the documentation prepared for the years up to 2010

Timing constraints and uncertainties because of detailed compliance rules

Risk of Copy & Paste approach

Master/Local vs Monster File

Consistency of the TP methods adopted taking into account the company’s facts

Impact of the economic recession and crisis

Impact of the overall group policy

Different approaches used by taxpayers and consultants during tax audits

Defensive

Preventive

Pros of a robust defense during tax audit rather than after

Conclusions

Transfer Pricing Workshop - March-April 2012

38

For participating and for Your contributions to the discussion - See you soon!

Roundtables in the pipeline

May 2012: Monti Government Tax Reform Bill – Impact on multinationals

June 2012: Business Restructurings under the OECD TP Guidelines, Chapter IX – Italian

practice and experience (business purpose, permanent establishment, exit tax, black list and

… transfer pricing - Best practice for tax risk management purposes)

Crowe Horwath – Cross-Border Tax & Transfer Pricing Services – Milan – Rome

Gaetano Pizzitola Michele Ghiringhelli

Thank-You

Transfer Pricing Workshop - March-April 2012

Related Documents