Trade Openness, Education and Growth Parantap Basu 1 Durham University Keshab Bhattarai 2 University of Hull December 2008 Preliminary, Commets Welcome 1 Department of Economics and Finance, Durham University, 23/26 Old Elvet, Durham DH1 3HY, UK. e-mail: [email protected]. 2 Business School, University of Hull, HU6 7RX, Hull, UK. email: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Trade Openness, Education and Growth

Parantap Basu1

Durham University

Keshab Bhattarai2

University of Hull

December 2008

Preliminary, Commets Welcome

1Department of Economics and Finance, Durham University, 23/26 Old Elvet,

Durham DH1 3HY, UK. e-mail: [email protected] School, University of Hull, HU6 7RX, Hull, UK. email:

Abstract

A signi�cant positive relationship exists between the trade share and educational

spending to GDP implying that countries which are more open on the trade front

also spend more on education. An open economy endogenous growth model with

human capital is developed to understand this stylized fact. The model demon-

strates that countries with greater cognitive skill spends more on education, and

grow faster. These countries open up on the trade front to �nance import of

physical capital which becomes scarce due to the diversion of resources to educa-

tion. The model highlights the importance of the productivity of human capital

or cognitive skill as an important economic fundamental determining the comove-

ment between trade share and education share. The Variance decomposition of

the shocks also con�rm that cognitive skill is important.

JEL Classi�cation: F41, O11, O33, O41

Keywords: Growth, Openness, Human capital, Cognitive Skill

1 Introduction

A plethora of literature exists about the relationship between openness and

growth. Grossman and Helpman (1990) show how openness promotes inno-

vation and growth in an open economy. Barro (1991) Mankiw, Romer and

Weil (1992), Jogenson and Fraumeni (1992), Parente and Prescott (2002))

took closed economy endogenous growth model to study theoretically and

empirically the link between growth and education leaving the trade issue

aside. Earlier Manning (1982) had shown how an increase in the educational

activity could reduce the amount of factors available for production of goods

and services in the short run but actually expands the production possibility

set when the level of skill rises in the long run. The literature has grown

further in recent years. Cartiglia (1997) had shown how trade liberalization

in skill scarce country leads to a higher investment in human capital and

creates the pattern of comparative advantage on international trade. Using

a multisectoral general equilibrium model Kim and Kim (2000) �nd that

education enhances mobility of workers across industries by enhancing their

human capital and removes the poverty trap. In a study of skill based wage

di¤erentials in Taiwan, Chang (2003) used a dynamic general equilibrium

model to establish how the education and the international trade were im-

portant factors in determining these wage di¤erentials. Basu and Guariglia

(2007) point out that FDI can complement human capital and could be bene-

�cial for growth at the expense of greater inequality. Despite all these studies

less is known whether countries which are more open on the trade front also

invest more in human capital. This is the central question addressed in this

paper.

1

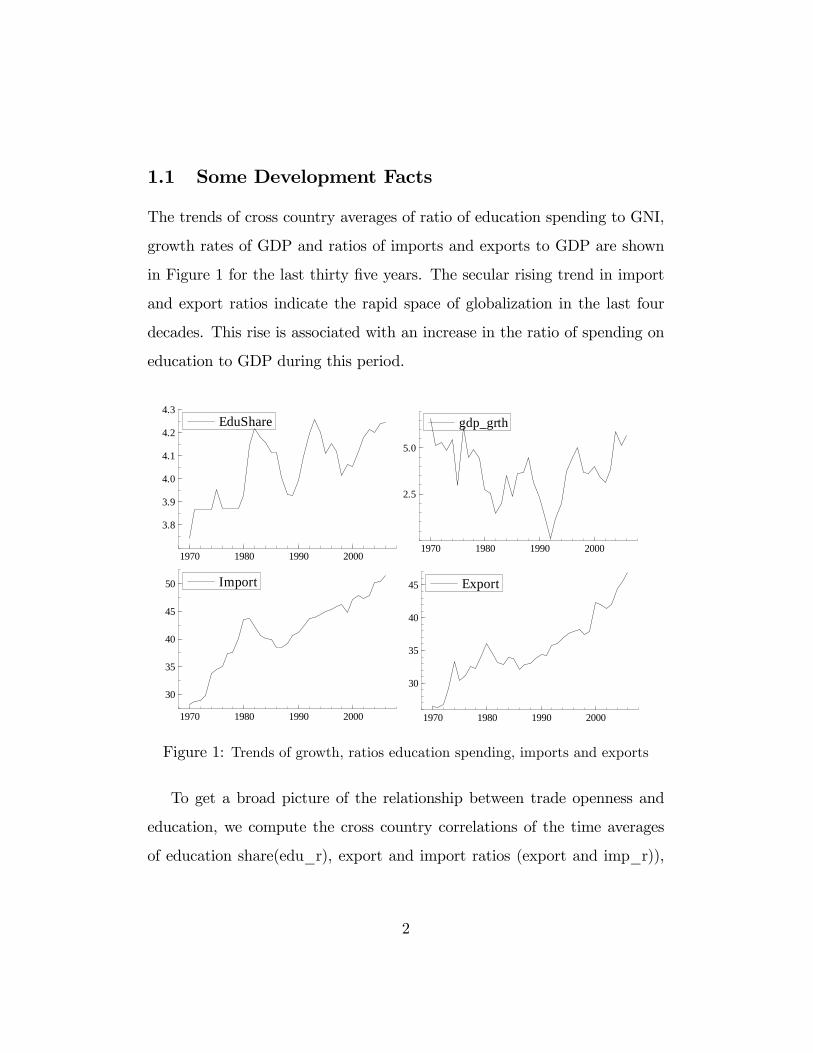

1.1 Some Development Facts

The trends of cross country averages of ratio of education spending to GNI,

growth rates of GDP and ratios of imports and exports to GDP are shown

in Figure 1 for the last thirty �ve years. The secular rising trend in import

and export ratios indicate the rapid space of globalization in the last four

decades. This rise is associated with an increase in the ratio of spending on

education to GDP during this period.

1970 1980 1990 2000

3.8

3.9

4.0

4.1

4.2

4.3EduShare

1970 1980 1990 2000

30

35

40

45 Export

1970 1980 1990 2000

30

35

40

45

50 Import

1970 1980 1990 2000

2.5

5.0

gdp_grth

Figure 1: Trends of growth, ratios education spending, imports and exports

To get a broad picture of the relationship between trade openness and

education, we compute the cross country correlations of the time averages

of education share(edu_r), export and import ratios (export and imp_r)),

2

growth rate (Growth) and total trade ratio (Trade_r).1

Table 1: Correlation coe¢ cients among ratios education spending, imports,

exports and growth

Edu_r Export Growth Imp_r Trade_r

Edu_r 1

Export_r 0.23 1

Growth -0.16 0.1687 1

Import_r 0.23 0.81 0.14 1

Trade_r 0.24 0.95 0.16 0.94 1

Correlations in Table 1 reveal the positive and signi�cant relation between

export share and education spending ratios implying that a country with a

higher spending on education has higher ratio of export to GDP. 2

1See http://www.esds.ac.uk/international/ and www.undp.org for detailed data source.

All the series came from the World Bank�s Development Indicator (WDI) database which

covers 206 countries.2Table 1 also re�ects a negative correlation between growth rates and education spend-

ing. This re�ects the fact that low income countries tend to grow faster than higher income

countries which makes the education share to correlate negatively with growth. To verify

this conjecture, we sort the data between low income and high income countries. For

low income countries, the correlation is -0.17 while for high income countries it is .002.

Also a panel regression of country growth rates on education shares after controlling for

country speci�c e¤ects provides a positive coe¢ cient which is not statistically signi�cant.

Given that the cross country growth shows tremendous disparity, locating only educa-

tion as a single explanatory variables may not be the way to determine education-growth

relationship.

3

The positive correlations between trade openness and education share are

reasonably robust with respect to �ner partitions of countries. Table 2 re-

ports the panel regression of export share and import shares on education

share after controlling for country speci�c e¤ects. The coe¢ cients of ed-

ucation share is statistically signi�cant at the 5% level in both regressions.

Panel ADF tests are run for each series to check for spurious correlations.

ADF test statistics are signi�cantly less than the critical value of -3.45.at 1

percent level of signi�cance indicating stationarity of each series. 3

Table 2: Panel Regressions of Export Ratio on Education Spending Ratio

Dep Variable: Export Ratio Coe¢ cient T-Value

Constant 10.61 4.33

Education ratio 2.58 4.54

R-square = 0.034; N =14; T=36 (1971-2006)

The aim of this paper is to understand this positive robust relationship

between trade openness and education. Our principal query is: why do coun-

tries which are more open on the trade front also invest more in education?

We answer this question in terms of a well articulated endogenous growth

3While running this panel regression, we controlled for country heterogeneity, and con-

ditional convergence. This is done by adding dummies for groups of countries, and adding

growth rate and level of GDP as regressors. Full details of these regressions are omitted

for brevity but available from the authors upon request.

4

Table 3: Panel Regressions of Import Ratio on Education Spending Ratio

Dep variable: Import Ratio Coe¢ cient T-Value

Constant 12.42 5.19

Education ratio 2.41 4.55

R-square = 0.034; N =14; T=36 (1971-2006)

Table 4: Test for Stationarity for Variables Included in Above Regressions

Edu_r Exp_r Imp_r

ADF test -3.669*** -6.237** -5.715**

lag 0 1 1

model where education is a prime driver of growth. Our model identi�es

the productivity of human capital as a crucial fundamental responsible for

the comovement between trade openness and education spending. A higher

productivity of human capital can result from a higher cognitive skill of the

pupils which could enhance the returns from schooling.4 A higher returns

to schooling provides the nation an incentive to divert resources from the

goods to education sector. A shortage of imported physical capital makes

it necessary for the economy to open up more on the trade front. Countries

with a higher cognitive skill parameter will then invest more in education

and also be more open on the trade front. We demonstrate this in terms

4The high cogntivie skill of pupils could result from a host of factors including better

quality of schooling, as well as �scal subsidy to education. The recent in�uential paper by

Hanoushek and Woessman (2008) highlights the importance of cognitive skill in determing

cross-country earnings and growth di¤erential.

5

of an endogenous growth model in the tradition of Becker (1975) and Lucas

(1988) in an open economy context which is new in the literature.

The rest of the paper is organized as follows. The following section lays

out the model. Section 3 analyzes the long run properties of the model.

Section 4 performs short run analysis in terms of impulse responses and vari-

ance decompositions of shocks to goods and education productivity. Section

5 concludes.

2 The Model

The model is a small open economy adaptation of the Lucas-Uzawa (Lucas,

1988) model. There are two sectors, goods and education. The output in

the goods sector (yt) is produced with the help of imported physical capital

(kt) and home grown intangible or human capital (ht): Human capital is

augmented only with the aid of human capital and this activity is called

schooling. At any date t; a fraction lGt of human capital is allocated to the

goods sector and remaining fraction lHt is allocated to schooling. The human

capital evolves following the technology:

ht+1 = (1� �h)ht + AHtlHtht (1)

where AHt is the total factor productivity (TFP) in the education sector

at date t. This education TFP can be attributed to cognitive skills of pupils

in the home country. Quality of schooling and education subsidy could sig-

ni�cantly account for this variable. The introduction of this cognitive skill

6

variable is motivated by the recent work of Hanoushek andWoessman (2008).

Basu and Guariglia (2008) also use the same human capital investment tech-

nology to understand the e¤ect education on the pace of industrialization.

Final goods (yt) are produced with the help of human and physical capital

via the Cobb-Douglas production technology:

yt = AGtkt�(lGtht)

1�� (2)

where AGt is the the date t total factor productivity (TFP) in the goods

sector. We assume the following stationary stochastic processes for these

two TFP shocks around the steady state:

AGt ��AG = �G(AGt�1 �

�AG) + �

Gt (3)

AHt ��AH = �G(AHt�1 �

�AH) + �

Ht (4)

where�AGand

�AH as the steady state TFP of the goods and education

sectors. �G and �H are positive fractions and �Gt and �

Ht are white noises.

The goods are used for consumption (ct) and export (xt). The home

country faces a �xed price pk for investment goods (ikt ) . It �nances this

physical investment by a combination of export and foreign borrowing (bt)

at a �xed world interest rate, r�.

The resource constraint facing the country is:

ct + xt = yt (5)

7

xt + bt+1 = (1 + r�)bt + p

kikt (6)

ikt = kt+1 � (1� �k)kt (7)

The home country faces a borrowing constraint. The amount that it

can borrow in the international market is constrained by the current capital

stock which means:

bt � kt (8)

The timeline is as follows. At date t, the state of the economy is charac-

terized by kt, ht and bt. The home country after realizing the TFP shocks,

�Gt ; �Ht , makes decisions about goods production (yt), schooling (lHt), ex-

ports (xt); external borrowing (bt+1) and consumption (ct) which maximizes

the following expected utility functional.

E0

1Xt=0

�tU(ct)

subject to (2) through (8).

The lagrange at date t is:

Lt = Et1Ps=0

�sU(ct+s)+1Ps=0

�t+s[AGt+sk�t+s(lGt+sht+s)

1���ct+s�pkfkt+s+1�

(1� �k)kt+sg � (1 + r�)bt+s + bt+s+1]

+1Ps=0

�t+s[(1��h)ht+s+AHt+sf(1�lGt)ht+sg�ht+s+1]+1Ps=0

!t+s(kt+s�bt+s)

8

where �t; �t; !t are lagrange multiplier associated with the �ow budget

constraint (5), human capital technology, (1) and the borrowing constraint

(8).

First order conditions are:

ct : �tU 0(ct) = �t (9)

kt+1 : �tpk�Et!t+1 = Et�t+1fAGt+1�k��1t+1 (lGt+1ht+1g1��+(1� �k)pkg (10)

ht+1 : �t = Et�t+1f1� �h + AHt+1(1� lGt+1)g (11)

+Et�t+1fAGt+1(1� �)k�t+1h��t+1l1��Gt+1

lGt : �t(1� �)AGtl��Gt k�t ht1�� � �tAHht = 0 (12)

bt+1 : �t = Et(1 + r�)�t+1 + Et!t+1 (13)

3 Balanced Growth Properties

Hereafter we specialize to a logarithmic utility function, U(ct) to analyze the

long run and short run properties of the model. We also assume that the

borrowing constraint (8) binds. In the absence of any shock to technology,

9

there is balanced growth in the economy. Use (9) and (11) to to get the

following balanced growth (g) equation:

�t�t+1

= [1 +�AH � �h] (14)

= > 1 + g =ht+1ht

=kt+1kt

=ct+1ct

= �[1 +�AH � �h] (15)

From (10) one gets:

�t�t+1

= [�(�AG=p

k)l1��G (k=h)��1 + 1� �k] +!t+1pk�t+1

(16)

Using (14) and (16), one gets:

�k=h

lG

�1��=

��AG

pk(�AH + �k � �h)� !t+1

�t+1

(17)

Next use (13) to obtain:

!t+1�t+1

=�t�t+1

� (1 + r�) (18)

Now use (10) to obtain

!t+1�t+1

=�t�t+1

pK � [�AG�(k=h)

��1l1��G + (1� �k)pk] (19)

Use of (18) and (19) yields:

10

�t�t+1

=1 + r� �

�AG�(k=h)

��1l1��G � (1� �k)pk1� pk =

1� pk + r� ��AG�(k=h)

��1l1��G + �kpk

1� pk(20)

Equating (15) and (20)

pk � 1 + ��AG(kt=ht)

��1l1��G � �kpk � r�pk � 1 = 1� �h +

�AH (21)

Next use (1) and (15) to solve for lH

lH = � � (1� �h)(1� �)=�AH (22)

Along a balanced growth path time allocations to goods and education

sectors are lG; lH are constants.The long run growth (15) is independent of

the �nancial market conditions, r� and pk. This happens because education

is the prime driver of growth in this model. Since the education sector does

not require tangible capital, a changes in user costs of physical capital (r�

and pk) have no e¤ects on the growth rate.

Plugging (22) into (21) one can uniquely solve k=h which is:

kt=ht =

24 ��AG

(pk � 1) (AH � �h) + pk�k + r�

351=(1��) (1��+(1��h)(1��)=�AH)(23)

A rise in the user cost of physical capital (r� and pk) lowers kt=ht: On the

other hand, a rise in the TFP in the goods sector,�AG has a positive e¤ect

11

on kt=ht to keep the marginal product of physical capital constant because

the balanced growth rate (15) is independent of�AG:

3.1 Education Share in GDP

Since education is a distinct good the issue arises whether it counts towards

GDP or not. In the present model, we assume that the households produce

education with the nonmarket time allocated to it. The education is a purely

nontraded good which does not pass through any organized market. We,

therefore, do not count this as a part of �nal good. However, while computing

the ratio of education spending to GDP, one has to be careful about the

shadow price of education and GDP because of the two sector nature of the

model. To this end, we use the lagrange multipliers associated with each

good. The share of education in GDP based on (5) and (1) is thus given by:

Educ =�t�AH lHht�tyt

Using (12) we get:

Educ =(1� �)lH

lG(24)

3.2 Export and Import Shares in GDP

We use ratios of export and import to GDP (yt),to measure openness of the

economy. It is straightforward to compute these ratios without resorting to

any shadow price adjustment. Use the current account equation (6):

12

xt + kt+1 = (1 + r�)kt + p

k[kt+1 � (1� �k)kt]

Divide through by kt and using the balanced growth rate (15) to get

xtyt=��(1� �h + AH)(pk � 1) + �(1 + r�)� �(1� �k)pk

MPK(25)

where the denominator is basically the marginal product of capital (MPK)

given as follows:

MPK = (pk � 1)AH + pk(�k � �h) + �h + r� (26)

Next de�ne the import share in GDP as:

mt

yt=pk(kt+1 � (1� �k)kt)

yt(27)

which after using the balanced growth rate (15) and the aggregate pro-

duction function reduces to:

mt

yt=�pkf�(1 +

�AH � �h)� (1� �k)gMPK

(28)

3.3 Baseline Calibration

This model is de�ned in terms of eight parameters,�AG ,

�AH , pk ,r�; �; �; �h; �k

which describe the preferences, technology and accumulation processes in the

economy. Our primary query is: what could contribute to a positive cross

country correlation between openness and education as seen in the data?.

13

An inspection of the education share (24) and the export and import share

equations (25) and (28) reveals that two important technology parameters,�AH and �h link the education and openness. A higher

�AH ; or a lower �h

raises the allocation of human capital to the research sector (equation 22)

and this drives up the education/GDP share (24).

How do these two parameters impact two trade share variables, xt=yt and

mt=yt in (25) and (28)? This is not analytically obvious. To �nd answer we

resort to a numerical comparative dynamics based on a baseline calibrated

model.

Parameters, �; �; �k are �xed at the conventional levels as in many studies

including Prescott (1986). The world interest rate r� is �xed at 3% consistent

with the Bank of England estimate5 . The remaining four parameters are

chosen to match a baseline world growth rate of 3%, about 30% world average

export or import shares consistent with Figure 1 and 50:50 time allocation

between goods production and schooling . Table 5 reports the baseline values

of these parameters.

Table 5: Baseline Parameters�AG

�AH pk r� � � �h �k

1.2 .088 1.5 0.03 0.36 0.96 0.015 0.1

5see:http://www.bankofengland.co.uk/statistics/rates/baserate.pdf

14

Table 6: Comparative Dynamics with Respect to AH

Scenarios�AH lGt lHt xt=yt g mt=yt kt=ht

1 0.088 0.488 0.512 0.324 0.030 0.324 1.435

2 0.098 0.442 0.558 0.325 0.040 0.340 1.255

3 0.108 0.405 0.595 0.325 0.049 0.355 1.110

4 0.118 0.374 0.626 0.326 0.059 0.371 0.991

5 0.128 0.348 0.652 0.326 0.068 0.385 0.892

6 0.138 0.320 0.674 0.326 0.078 0.398 0.808

7 0.148 0.306 0.694 0.327 0.088 0.411 0.736

8 0.158 0.289 0.711 0.327 0.097 0.424 0.674

9 0.168 0.275 0.725 0.328 0.107 0.436 0.620

10 0.178 0.261 0.739 0.328 0.116 0.447 0.573

Tables 6 and 7 report the comparative dynamics of the steady state vari-

ables with respect to changes in�AH and �h respectively. A higher

�AH

can be interpreted as an improvement in the quality of the human capital

or cognitive skill as in Hanoushek and Woessman (2008). The model pre-

dicts that a higher�AH induces agents to investment more time in education

and less time in goods production because education has a higher marginal

return vis-a-vis goods production. As agents transfer resources away from

goods to education, the physical to human capital ratio falls (last column of

the Table 6), and growth rate rises. As long as the relative price of capital

(pk > 1) such a scarcity of physical capital raises the marginal product of

physical capital (due to diminishing returns to factor proportion) as seen in

15

Table 7: Comparative Dynamics with Respect to dh

Scenarios �h lGt lHt xt=yt mt=yt g kt=ht

1 0.015 0.488 0.512 0.3243 0.3244 0.030 1.435

2 0.016 0.488 0.513 0.3243 0.3236 0.030 1.437

3 0.016 0.487 0.513 0.3243 0.3228 0.029 1.439

4 0.017 0.487 0.513 0.3242 0.3220 0.029 1.441

5 0.017 0.487 0.513 0.3242 0.3211 0.028 1.443

6 0.018 0.487 0.513 0.3242 0.3203 0.028 1.445

7 0.018 0.486 0.514 0.3242 0.3195 0.027 1.447

8 0.019 0.486 0.514 0.3241 0.3186 0.027 1.449

9 0.019 0.486 0.514 0.3241 0.3178 0.026 1.451

10 0.020 0.486 0.514 0.3241 0.3170 0.026 1.453

(26). Since the home country has the option to augment physical capital by

�nancing it through current account, it will take advantage of it by raising

its export and import share. Thus the country becomes more open on the

trade front. The bottomline is that as a consequence of higher�AH , the home

country invests more in education, its growth rises via the human capital

equation (1) and its trade share also increases. The e¤ect of a lower rate of

depreciation in �h is analogous to a higher�AHas can be read from Table 7

although its e¤ect is small compared to�AH .

16

4 Short Run Dynamics

Until now we only analyzed the steady states of the model. Such a steady

state analysis can be motivated by cross country comparison of various long

run averages such as average growth, trade share, education share. The

underlying assumption here is that each country is in di¤erent long run steady

states and the research question is what drives this cross country dispersion.

We identify TFP in each sector as a major fundamental for the cross country

dispersion of growth, education share and trade share. However, such a

long run analysis cannot re�ect how a country can respond to shocks to its

fundamentals. Analysis of this kind of within-country response to shocks

necessitates a short run analysis.

The short run system is given by equations (29) to (36) as following(The

appendix shows the derivation of these equations).

kt+1ht+1

=pk (1� �k) ktht + AGt(

ktht)�l1��Gt � ct

ht� (1 + r�) kt

ht

(pk � 1) f1� �h + AHt(1� lGt)g(29)

1 = mt+1:�AGt+1

�kt+1ht+1

���1l1��Gt+1 + (1� �k)pk � 1� r�

pk � 1 (30)

AGtAht

:l��Gt :(ktht)� =

mt+1

�AGt+1Aht+1

:l��Gt+1:(kt+1ht+1

)� f1� �h + AHt+1(1� lGt+1)g+ AGt+1�kt+1ht+1

��l1��Gt+1

�(31)

where mt+1 is the discount factor given by

17

mt+1 =�(ct=ht)

(ct+1=ht+1)

1

(AHt+1(1� lGt+1) + 1� �h)(32)

Export and import share equations are given by:

xtyt

= [1 + r� � pk(1� �k)](kt=yt) (33)

+(pk � 1)(kt+1=yt+1)(AGt+1=AGt)�kt+1=ht+1kt=ht

��f1� �h + AHtlhtg:

�lGt+1lGt

�1��

mt

yt= pk

"kt+1yt+1

:AGt+1AGt

:

�kt+1=ht+1kt=ht

���lGt+1lGt

�1��f1� �h + AHtlhtg � (1� �k):

ktyt

#(34)

The ratio of current account to GDP is de�ned as:

catyt=xtyt� mt

yt(35)

The physical capital:output ratio is given by the production function (2)

as:

ktyt= A�1Gt (kt=ht)

1��l��1Gt (36)

The education share equation is given by:

Educt =(1� �)lHt

lGt(37)

Finally the gorwth rate of output is given by:

18

yt+1yt

=AGt+1AGt

:

�AGt+1AGt

� �kt+1=ht+1kt=ht

��fAHtlHt + 1� �hg:

�lGt+1lGt

�1��(38)

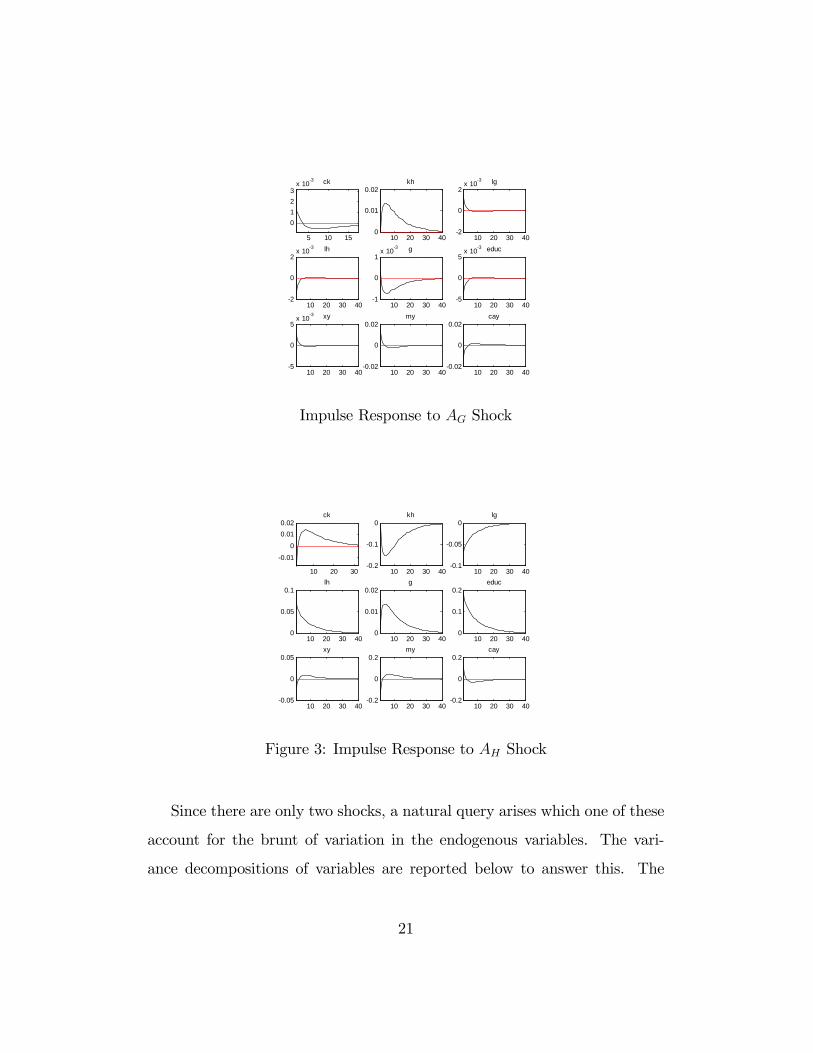

4.1 Impulse Responses

There are eight endoegenous variables namely, ct=ht , lGt; xt=yt, mt=yt,

Educt; CAt=yt; kt=ht; yt+1=yt and two exogenous variables, AGt and AHt:

Among these endogenous variables, only kt=ht is predetermined. The im-

pulse response analysis is based on loglinearlized deviations of these variables

from the steady state. Since this is a model of endgenous growth, the loglin-

earization is done around the balanced growth path described earlier. Figures

2 and 3 represent the impulse responses of various endogenous variables with

respect to shocks to goods TFP, AGt and education TFP, AHt respectively

given the baseline parameters as in Table 5.6 In response to goods TFP

shock, more time is devoted to goods production and this makes educational

investment fall. Growth rate of output rises monentarily as more goods are

produced but then it quickly turns negative due to paucity of investment in

human capital. On the current account front, the home country responds

to this shock by importing a lot more physical capital than exporting. This

makes the current account (cay) decline in the short run.7

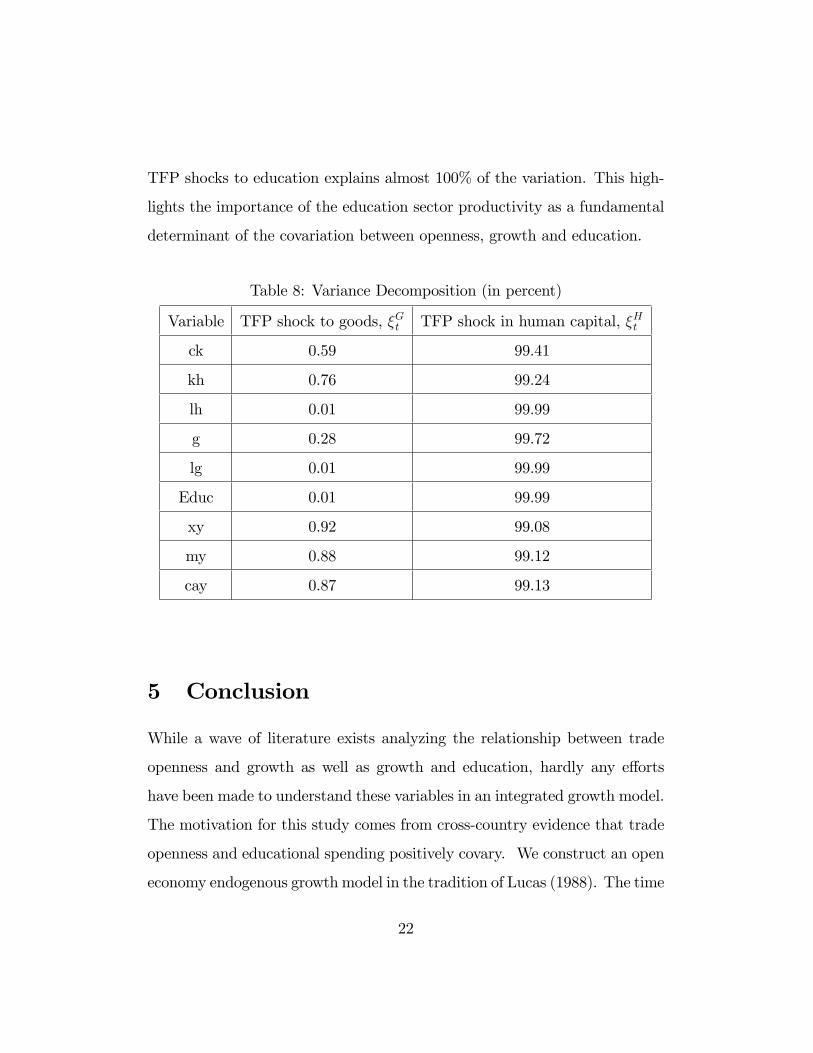

In response to an educational TFP shock the impulse response behaves

di¤erently. Agents devote more time to schooling less time to production of6 A variant of the algorithm of Blanchard and Kahn (1980) is used to plot the impulse

responses. All the calculations are done using DYNARE developed by Julliard (1996).7In the impulse response chart, ck = ct=kt , kh = kt=ht; xy = xt=yt; my = mt=yt,

cay = cat=yt:

19

�nal goods. Growth rate of output rises due to transfer of resources from

goods to education sector and then it picks up as more schooling increases the

human capital base. Both export and import shares fall although the latter

falls more than the former making the current account rise. At a later stage,

the nation starts allocating more resources to the goods sector which makes

import and export share rise. The current account shows greater volatility

in response to this shock.

Note the contrast between long run and short run e¤ects of AG: First, In

the long run scenario, a change in AG has neutral e¤ects on growth, education

and trade shares while this is not the case in the short run. A shock to goods

sector productivity has important e¤ects on time allocation to schooling and

hence growth and openness.

Second, the short run response of shocks to cognitive skill is remarkably

di¤erent from what we see in the long run. While in the long run, a higher

AH results in a higher trade share, a temporary positive shock to AH makes

the home country cut back in exports and imports to allow for growth in the

education sector. 8

8The short run correlation between trade share and education is negative while cross

country data suggets that it is positive. Note that the cross country correlations referes to

the long run comparision of countries which di¤er in terms of long run average TFP. This

basically means between-country variation in trade shares and education shares. The

short run analysis can be interpreted as within-country response of a transitory shock to

productivity.

20

5 10 15

0123

x 103 ck

10 20 30 400

0.01

0.02kh

10 20 30 402

0

2x 103 lg

10 20 30 402

0

2x 10

3 lh

10 20 30 401

0

1x 10

3 g

10 20 30 405

0

5x 10

3 educ

10 20 30 405

0

5x 103 xy

10 20 30 400.02

0

0.02my

10 20 30 400.02

0

0.02cay

Impulse Response to AG Shock

10 20 30

0.01

0

0.010.02

ck

10 20 30 400.2

0.1

0kh

10 20 30 400.1

0.05

0lg

10 20 30 400

0.05

0.1lh

10 20 30 400

0.01

0.02g

10 20 30 400

0.1

0.2educ

10 20 30 400.05

0

0.05xy

10 20 30 400.2

0

0.2my

10 20 30 400.2

0

0.2cay

Figure 3: Impulse Response to AH Shock

Since there are only two shocks, a natural query arises which one of these

account for the brunt of variation in the endogenous variables. The vari-

ance decompositions of variables are reported below to answer this. The

21

TFP shocks to education explains almost 100% of the variation. This high-

lights the importance of the education sector productivity as a fundamental

determinant of the covariation between openness, growth and education.

Table 8: Variance Decomposition (in percent)

Variable TFP shock to goods, �Gt TFP shock in human capital, �Ht

ck 0.59 99.41

kh 0.76 99.24

lh 0.01 99.99

g 0.28 99.72

lg 0.01 99.99

Educ 0.01 99.99

xy 0.92 99.08

my 0.88 99.12

cay 0.87 99.13

5 Conclusion

While a wave of literature exists analyzing the relationship between trade

openness and growth as well as growth and education, hardly any e¤orts

have been made to understand these variables in an integrated growth model.

The motivation for this study comes from cross-country evidence that trade

openness and educational spending positively covary. We construct an open

economy endogenous growth model in the tradition of Lucas (1988). The time

22

allocation between goods production and schooling is an essential ingredient

of human capital growth. Our model identi�es the productivity of human

capital as a crucial fundamental causing this comovement between education

and trade openness. This fundamental can be interpreted as cognitive skill

along the lines of a recent literature which pinpoints cognitive skill as a critical

determinant of growth. While cognitive skill is an exogenous technology

variable in our model, future research can delve deeper into the underlying

reasons for the cross country di¤erences in cognitive skills.

References

[1] Barro R. J.(1991) Economic Growth in Cross Section of Countries, Quar-

terly Journal of Economics, May, 407-433.

[2] Basu P and A Guariglia (2008) Does low education delay structural

transformation, Southern Economic Journal, forthcoming.

[3] Becker G.S. (1975) Human Capital, Columbia University, New York.

[4] Blanchard, O and C.M. Kahn (1980), The Solution of Linear Di¤erence

Models under Rational Expectations, Econometrica 48, pp. 1305-1313.

[5] Cartiglia F. (1997) Credit constraints and human capital accumulation

in the open economy, Journal of International Economics, 43, 221:236.

[6] Chang H C (2003) International trade, productivity growth, education

and wage di¤erential: A case study of Taiwan, Journal of Applied Eco-

nomics, 6:1:25-48.

23

[7] Findlay R and H Kierzkowski (1983) International trade and human cap-

ital: A simple general equilibrium model, Journal of Political Economy,

91:6:957-978.

[8] Grossman G.M. and E. Helpman (1990) Comparative Advantage and

Long-Run Growth, American

Economic Review, 80:4:796-815

[9] Hanushek E A and L Woessmann (2008) The Role of Cognitive Skills in

Economic Development, Journal of Economic Literature, 46:3:607-668,

September.

[10] Jogenson DW and B. Fraumeni (1992) Investment in Education and US

Economic Growth, Scandinavian Journal of Economics 94:51-70, Sep-

tember.

[11] Juillard, M (1996), Dynare: A Program for the Resolution and Simula-

tion of Dynamic Models with Forward Variables through the Use of a

Relaxation Algorithm, CEPREMAP, Couverture Orange, 9602,

[12] Kim S J and Y J Kim (2000) Growth gains from trade and education,

Journal of International Economics, 50:519-545.

[13] Lucas R.E. (1988) On the Mechanics of Economic Development, Journal

of Monetary Economics, 22:1: 3-42.

[14] Mankiw N.G., D. Romer and D. N. Weil (1992) Contribution to the

Empirics of Economic Growth,Quarterly Journal of Economics, 107:407-

437, May.

24

[15] Manning R. (1982) Trade, Education and Growth: The Small-Country

Case, International Economic Review, 23:1:83-106.

[16] Owen A L (1999) International trade and the accumulation of human

capital, Southern Economic Journal, 66:1:61-81.

[17] Parente S.L. and E.C. Prescott (2002) Barriers to Riches, MIT Press.

[18] Prescott, E.C. (1986), Theory Ahead of Business Cycle Measurement,

Federal Reserve Bank of Minneapolis, Quarterly Review; Fall.

[19] Romer, Paul (1989) Endogenous Technological Change, Journal of Po-

litical Economy, 98:5: Pt. 2: S71-S102.

25

6 Appendix

Use (5), (6), (7), (8) with equality to get:

kt+1 =pk(1� �k)kt + AGtk�t (lGtht)1�� � ct � (1 + r�)kt

pk � 1 (39)

Dividing (39) by (1), one gets (29).

(30) can be obtained by combining (9),(10) and (13).

Use (11) and (12) to obtain (31).

The discount factor (32) is basically �ct=ct+1 . This can be rewritten as

�f(ct=ht)=(ct+1=ht+1)g(ht+1=ht)�1: After using (1), one gets the expression

for (32).

To obtain the export share equation (33) , use (6) and (8) to obtain:

xt = (1 + r�)kt + (p

k � 1)kt+1 � pk(1� �k)kt

Divide through by yt to obtain

xtyt= (1 + r� � pk(1� �k))

ktyt+ (pk � 1)(kt+1

yt+1)(yt+1yt)

Next use the production function (2) and the human capital equation (1)

to obtain (33).

To get (34), use (27)

mt

yt=pk(kt+1 � (1� �k)kt)

yt

which can be rewritten as:

26

mt

yt= pk(

kt+1yt+1

:yt+1yt

� (1� �k)ktyt)

which after using the production function (2) and the human capital

equation (1) yields the expression (34).

The expression for (36) directly follows from the production function (2).

The expression for (37) is the same as the steady state expression (24).

The expression for the growth rate in (38) follows from the use of the

production function (2) and the human capital equation (1).

27

Related Documents