STM Group: Auto - Tractors Submitted By: UM14001 Abhijeet Dash UM14037 Goutam Rao UM14056 Sukanya Dash

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

STM Group: Auto - Tractors

Submitted By:UM14001 Abhijeet DashUM14037 Goutam RaoUM14056 Sukanya Dash

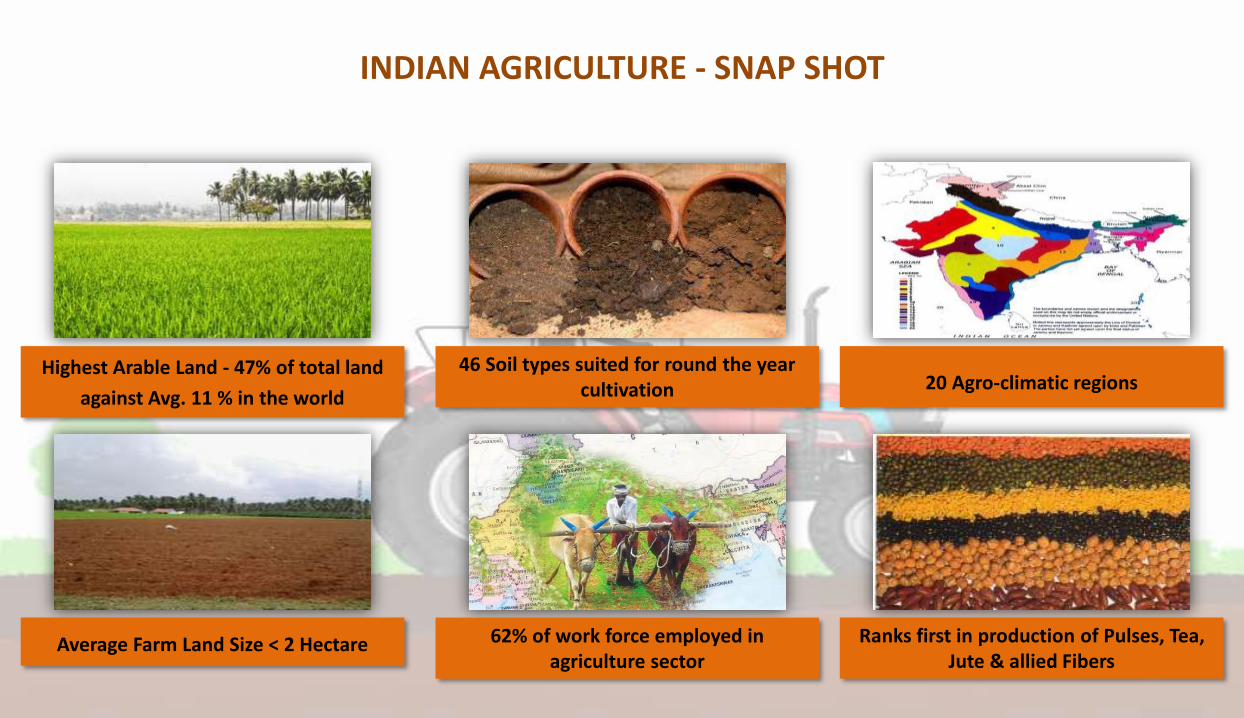

INDIAN AGRICULTURE - SNAP SHOT

Highest Arable Land - 47% of total land

against Avg. 11 % in the world

46 Soil types suited for round the year cultivation 20 Agro-climatic regions

Average Farm Land Size < 2 Hectare 62% of work force employed in agriculture sector

Ranks first in production of Pulses, Tea, Jute & allied Fibers

AGRI LABOR

60

250

30

175

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010

Men Wages (Rs./Day) Women Wages (Rs./Day)

Shortage of agricultural labor across the country due to increase In labor wages & Urbanization.

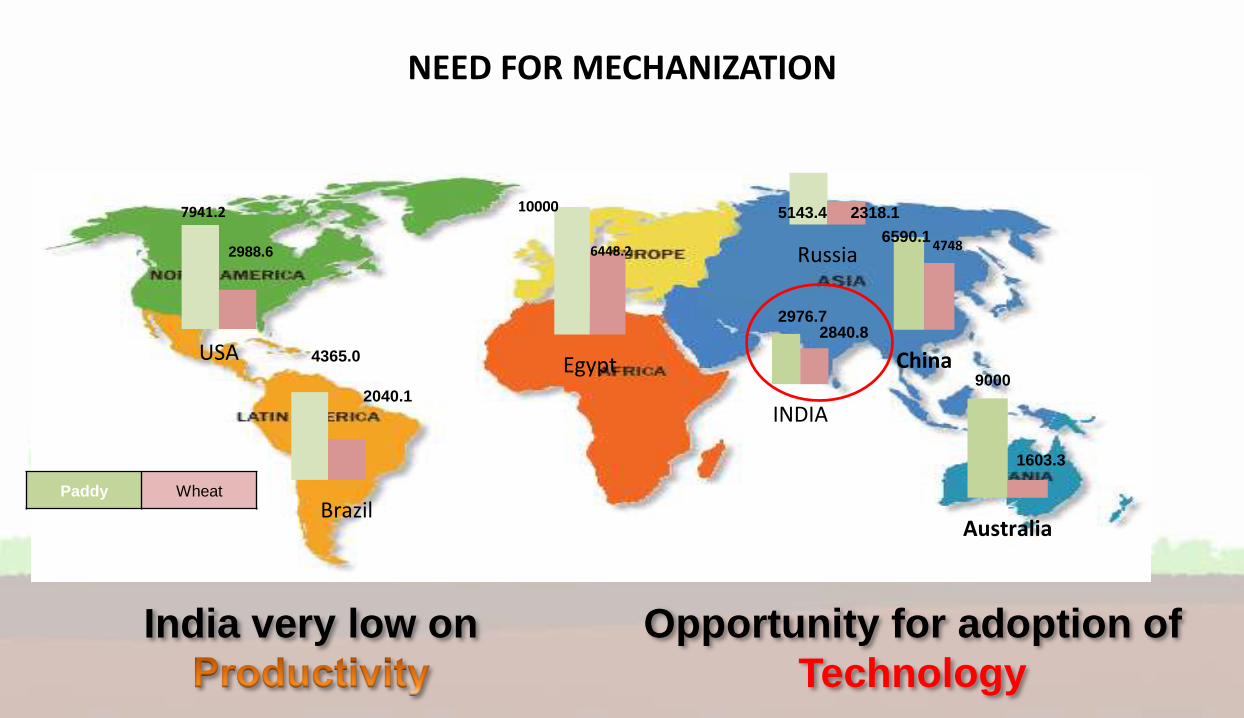

NEED FOR MECHANIZATION

Paddy Wheat

USA

7941.2

2988.6

China

47486590.1

Egypt

6448.2

10000

AustraliaBrazil

4365.0

2040.19000

1603.3

Russia

5143.4 2318.1

INDIA

2976.72840.8

India very low on Opportunity for adoption of

Technology

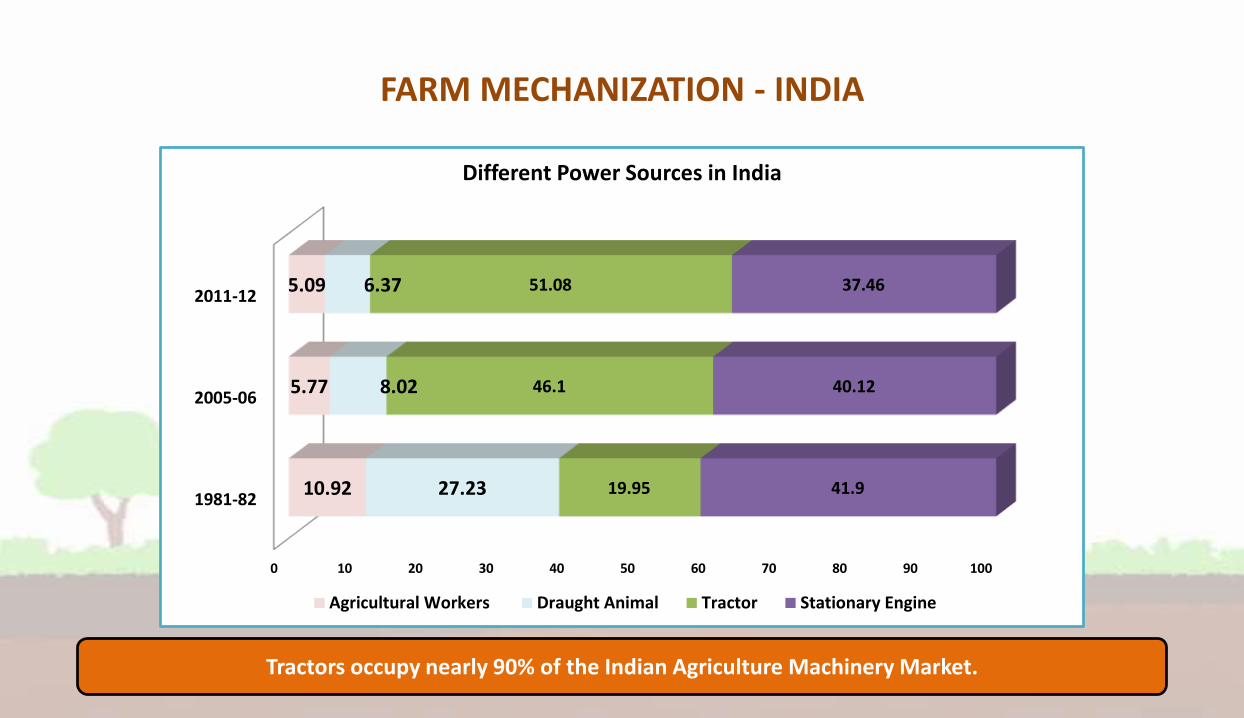

FARM MECHANIZATION - INDIA

0 10 20 30 40 50 60 70 80 90 100

1981-82

2005-06

2011-12

10.92

5.77

5.09

27.23

8.02

6.37

19.95

46.1

51.08

41.9

40.12

37.46

Different Power Sources in India

Agricultural Workers Draught Animal Tractor Stationary Engine

Tractors occupy nearly 90% of the Indian Agriculture Machinery Market.

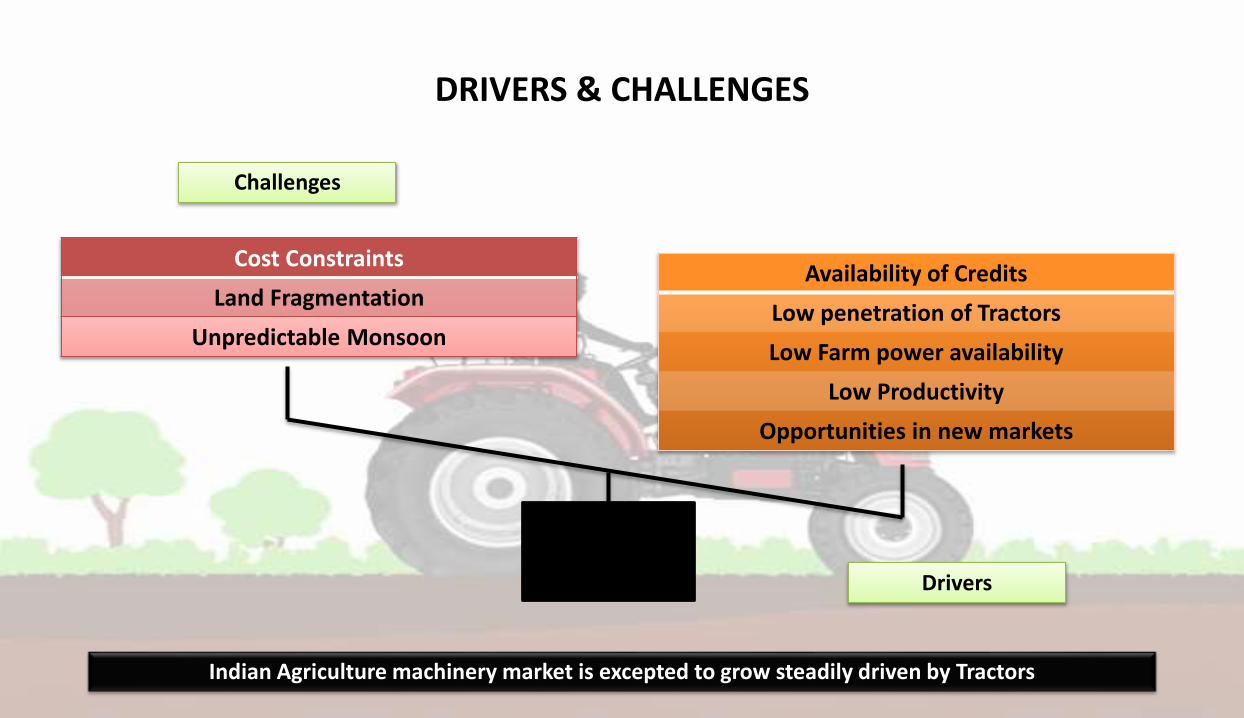

DRIVERS & CHALLENGES

Availability of Credits

Low penetration of Tractors

Low Farm power availability

Low Productivity

Opportunities in new markets

Cost Constraints

Land Fragmentation

Unpredictable Monsoon

Challenges

Drivers

Indian Agriculture machinery market is excepted to grow steadily driven by Tractors

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

• War surplus tractors and bulldozers imported

• Central and State Tractor Organizations set up to develop and promote the supply and use of tractors

1945 to 1960.

• Initiated local production began with five manufacturers producing a total of 880 units per year. Eicher, Gujarat Tractors, TAFE, Escorts, M&M.

1961 to 1970.

• Six new manufacturers were established during this period

• Escorts Ltd began local manufacture of Ford tractors in 1971 in collaboration with Ford, UK.

• Credit facilities for farmers continued to improve

1971 to 1980.

• A further five (Auto Tractors, Haryana Tractors, United Auto Tractors, Asian Tractors, VST Tillers) manufacturers began production during this period but only last one survived in the increasingly competitive market place.

• Then India a net importer up to the mid-seventies became an exporter in the 80's mainly to countries in Africa.

1981 to 1990.

• Since 1992 it has not been necessary to obtain an industrial license for tractor manufacture in India.

• By 1997 annual production exceeded 255000 units and the national tractor park had passed the two million mark.

• Many new manufacturers like Bajaj Tempo, New Holland, John Deere have started production.

1991 onwards

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

History & Evolution Consumer Analysis Industry Life cycle Market Size

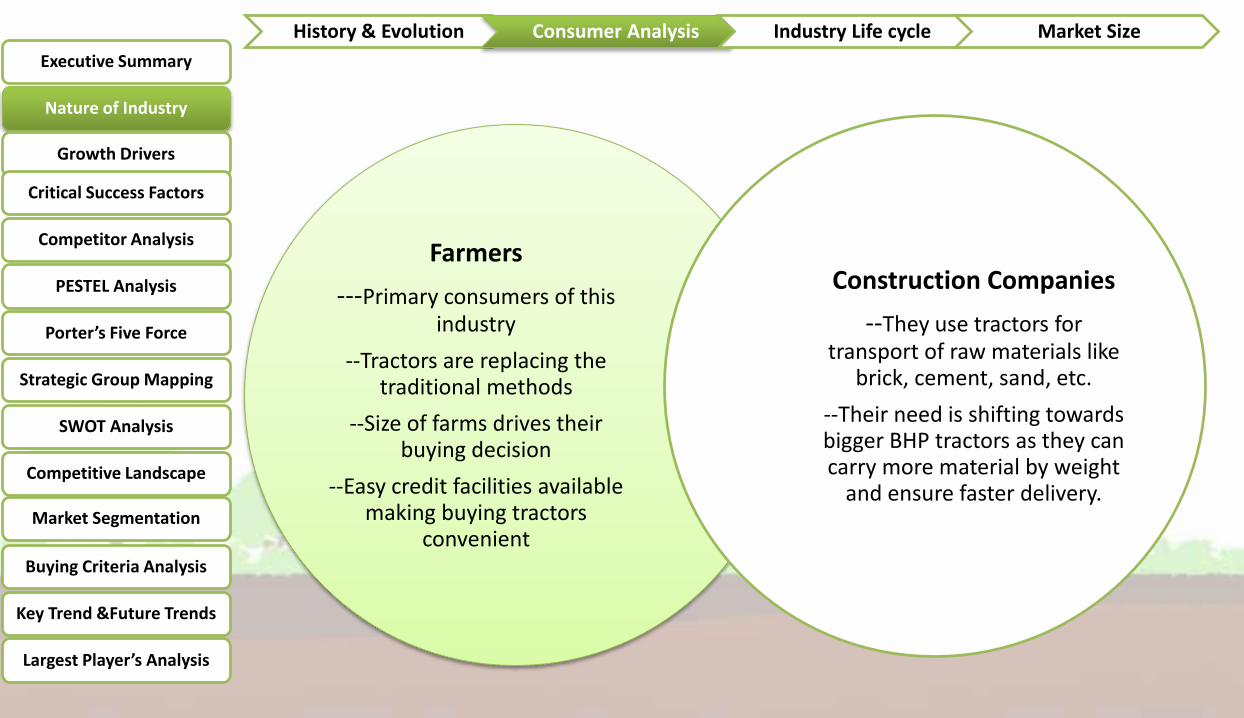

Farmers

---Primary consumers of this industry

--Tractors are replacing the traditional methods

--Size of farms drives their buying decision

--Easy credit facilities available making buying tractors

convenient

Construction Companies

--They use tractors for transport of raw materials like

brick, cement, sand, etc.

--Their need is shifting towards bigger BHP tractors as they can carry more material by weight

and ensure faster delivery.

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

History & Evolution Consumer Analysis Industry Life cycle Market Size

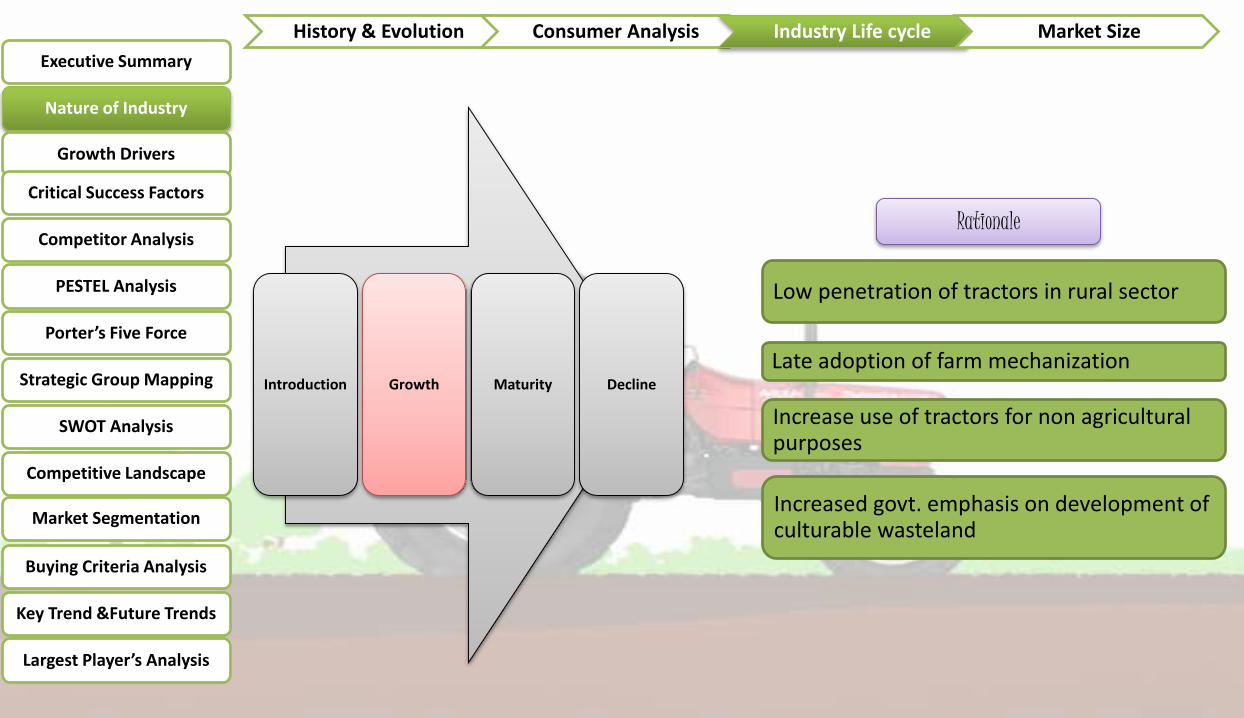

Rationale

Low penetration of tractors in rural sector

Late adoption of farm mechanization

Increase use of tractors for non agricultural purposes

Increased govt. emphasis on development of culturable wasteland

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

History & Evolution Consumer Analysis Industry Life cycle Market Size

Introduction Growth Maturity Decline

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

History & Evolution Consumer Analysis Industry Life cycle Market Size

Expansion and Extension of Agricultural land

Value additions in Farming

Return on Investment (RoI)

Credit and money availability

Government support for agriculture and rural development

Buoyancy in rural income supports tractor growth

Monsoons

Scarcity of farm labour

Increasing non-agricultural application

Strong replacement demand

Export Sales

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Customer relations and Service

• providing end-to-end services to customers is expected to be a key differentiator

Technological Innovation

• develop superior insights into what customer’s value and accordingly develop innovations that satisfy and delight the customers

Sales and Distribution Networks

• Makes the system robust and acts as source of knowledge pertaining to the preferences of the customers

Strategic Alliance

• powerful instrument to catalyse the organizational forces

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

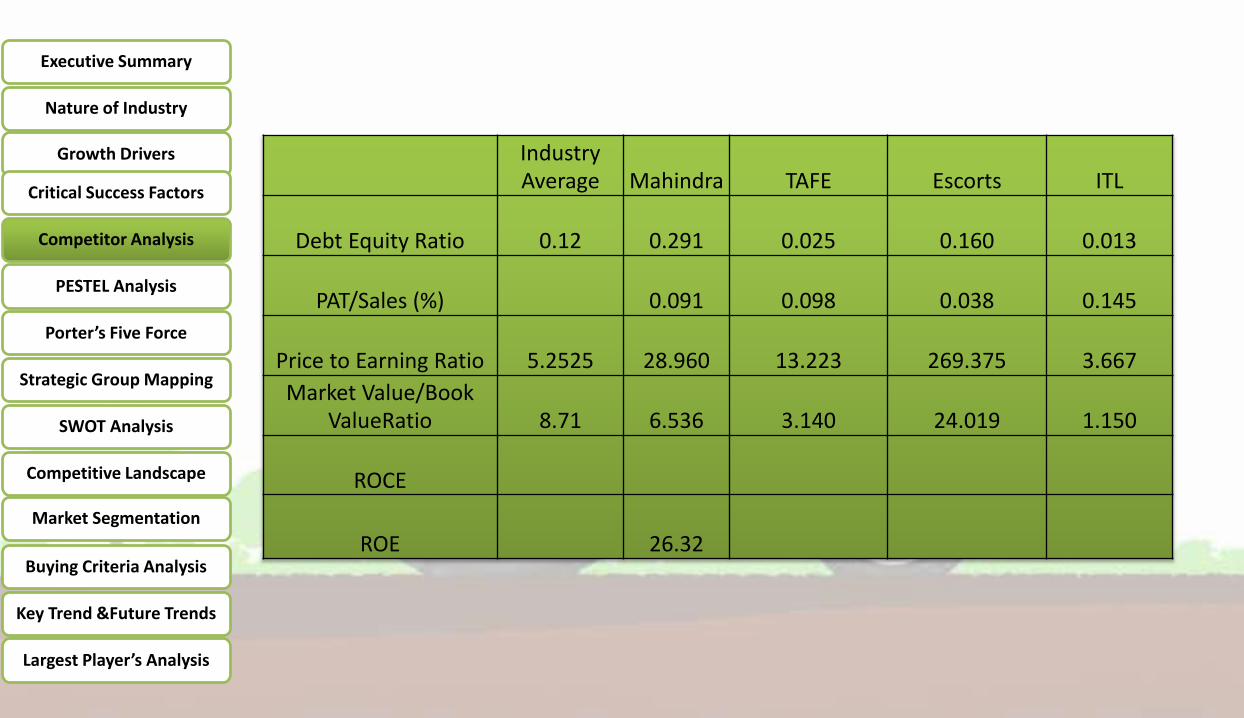

Industry Average Mahindra TAFE Escorts ITL

Debt Equity Ratio 0.12 0.291 0.025 0.160 0.013

PAT/Sales (%) 0.091 0.098 0.038 0.145

Price to Earning Ratio 5.2525 28.960 13.223 269.375 3.667

Market Value/Book ValueRatio 8.71 6.536 3.140 24.019 1.150

ROCE

ROE 26.32

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Political Economic Social Technological Environmental Legal

Govt. stress

on

mechanizati

on to boost

grain

production

Subsidy on

agricultural

loans from

government

Regaining “

Agricultural

dynamism”,

a key goal

of eleventh

Five year

plan

Change in

taxation

policy

100% FDI

policy

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Political Economic Social Technological Environmental Legal

Credit

extended by

commercial

banks, state

land

development

banks and

regional rural

banks.

Cost of

tractors in

India is the

cheapest in

world .Hence

there exists

tremendous

scope for

exports.

Deteriorating

foreign

exchange

situation in

western

country, poor

buying

capacity and

comparatively

cheaper

import of

second hand

tractor from

developed

country

inflation may

provoke

higher wage

demands

from

employees

and raise

costs

higher

national

income

growth may

boost demand

for a firm's

products

Less interest

rate charged

by banks for

agricultural

inputs

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Political Economic Social Technological Environmental Legal

Increase in awareness among the farmers for the

need of farm mechanization and are keen to acquire

tractor

Due to land fragmentation

farmers with small land holding are

not buying tractor

There is need for more tilling due to

depletion of moisture and

repeated cultivation of land .

Animal power available is too

inadequate to meet power demand of

our farmers.

More farmers are opting for multiple cropping over last decade. Country's gross cropped area increased by about

4.7%.

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

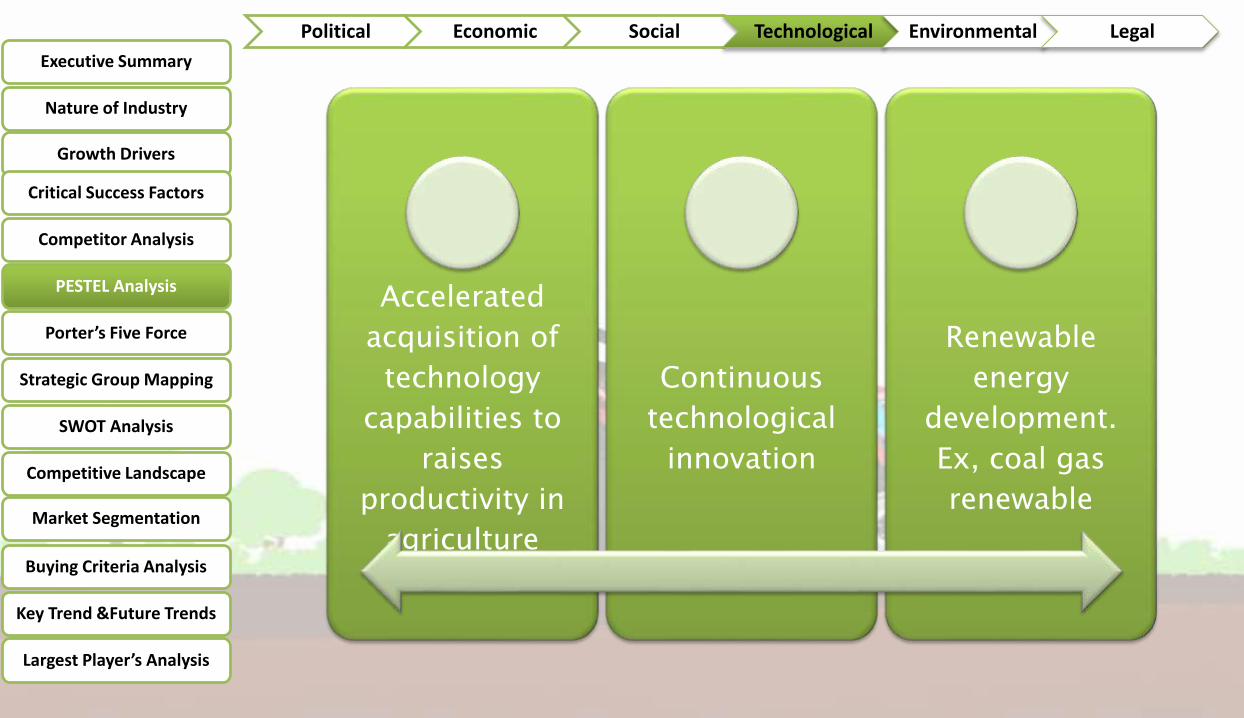

Political Economic Social Technological Environmental Legal

Accelerated

acquisition of

technology

capabilities to

raises

productivity in

agriculture

Continuous

technological

innovation

Renewable

energy

development.

Ex, coal gas

renewable

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

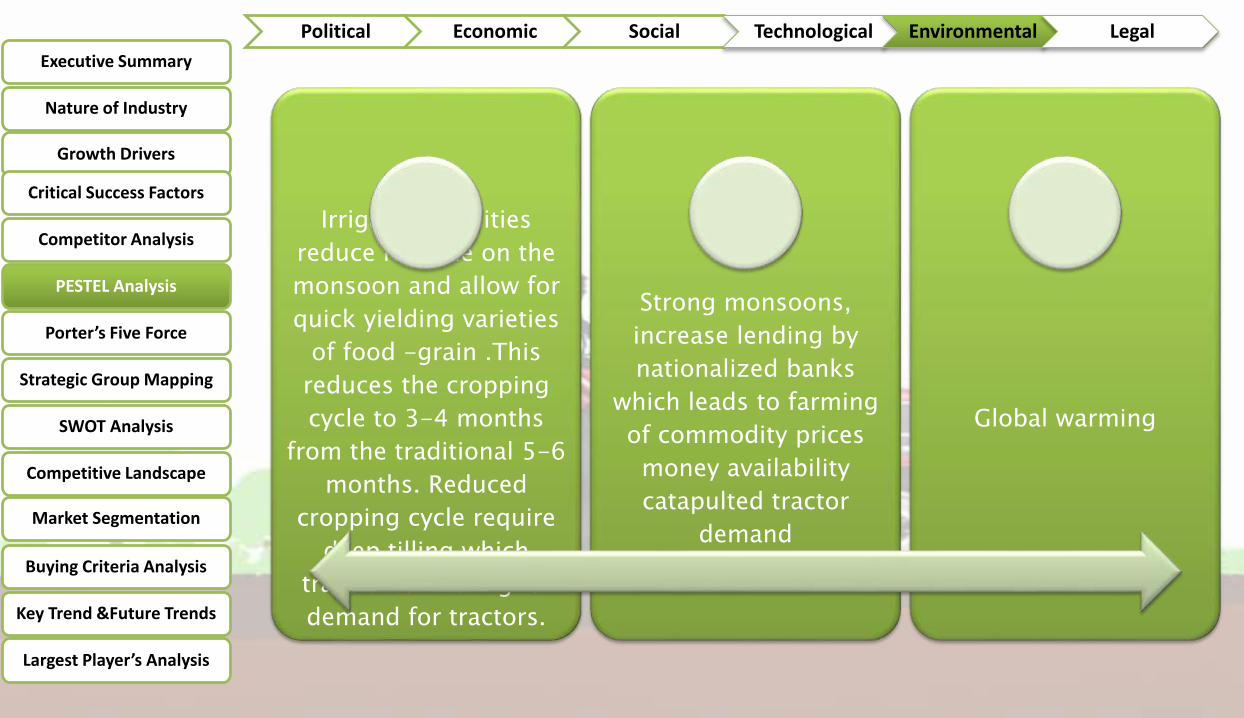

Political Economic Social Technological Environmental Legal

Irrigation facilities

reduce reliance on the

monsoon and allow for

quick yielding varieties

of food -grain .This

reduces the cropping

cycle to 3-4 months

from the traditional 5-6

months. Reduced

cropping cycle require

deep tilling which

translates into higher

demand for tractors.

Strong monsoons,

increase lending by

nationalized banks

which leads to farming

of commodity prices

money availability

catapulted tractor

demand

Global warming

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

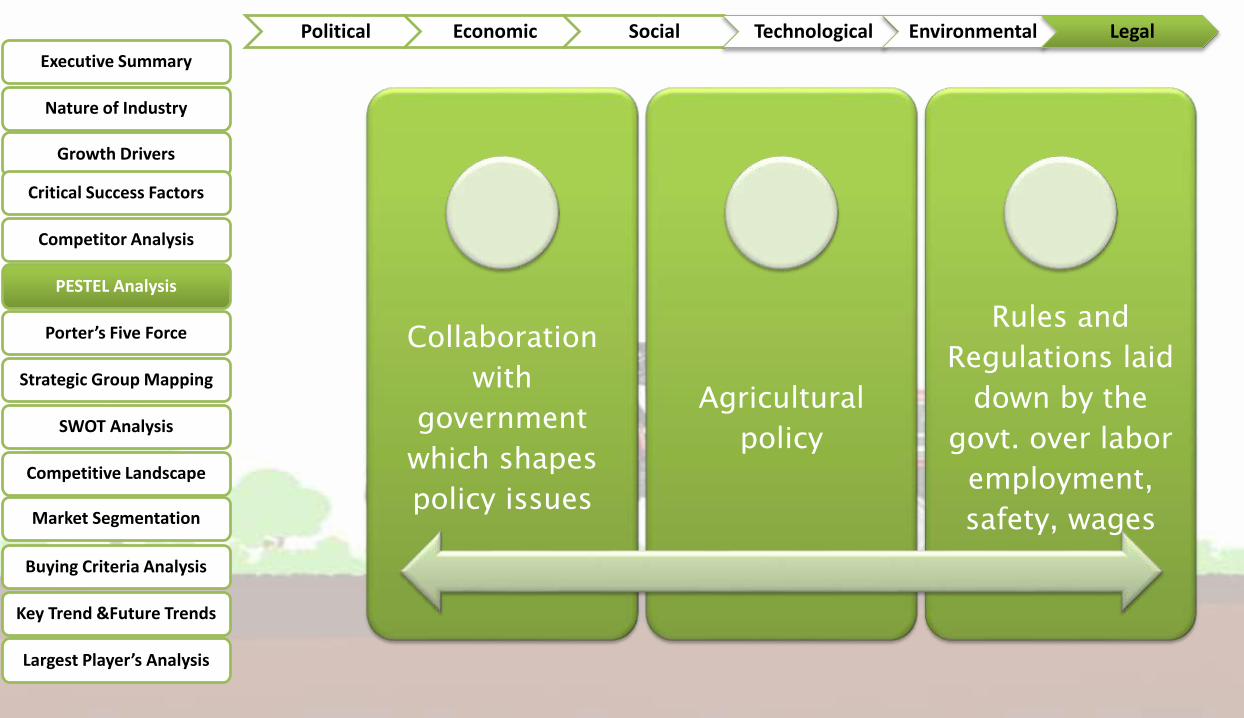

Political Economic Social Technological Environmental Legal

Collaboration

with

government

which shapes

policy issues

Agricultural

policy

Rules and

Regulations laid

down by the

govt. over labor

employment,

safety, wages

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

Varying density

of consumer

base across

locations

Firms: buyers

concentration

ratio is 1:20000

(but only 4

major players)

High switching

costs for buyers

Key

factors

for

analysis

Some places are

over tractorised

and some are

under

tractorised.No of players in

an industry

determine how

effectively the

demands can be

met

Mostly a tractor

is one time buy

for the farmers

Rationale

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

Minimal chance

of forward

integration

Too many

suppliers

Switching cost

is less for

tractor

companies

Key

factors

for

analysis

It requires large

capital and

technological

expertise,

making it

unviable in the

part of the

suppliers.This reduces

the dependency

on a single

supplier

The raw

materials are

generic and

widely available

from many

suppliers.

Rationale

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

Total No of

firms (Listed

as well as

Unlisted)

No of large

firms

Entry of

foreign

players

Larger

M&As

Key

factors

for

analysi

s20

4

They may

bring high

technological

innovation

and expertise

hence better

products.

This makes

the existing

firms bigger

and hence

brings more

rivalries.

Rationa

le

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

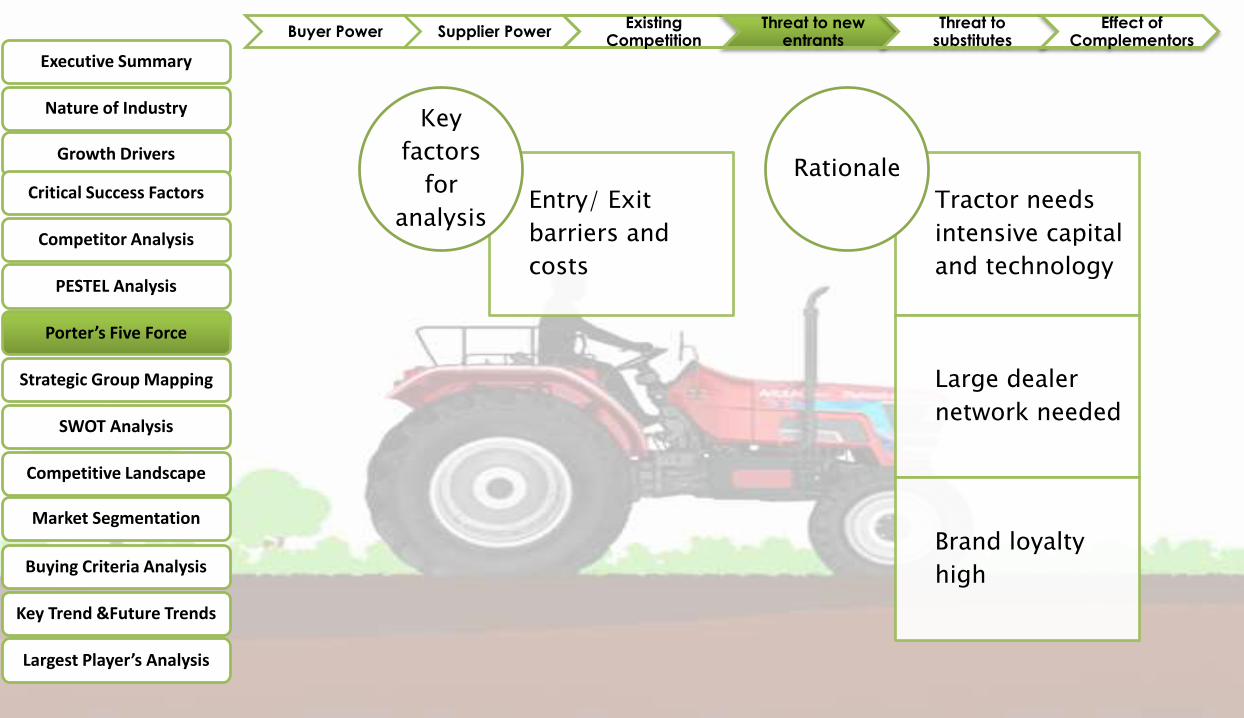

Entry/ Exit

barriers and

costs

Key

factors

for

analysisTractor needs

intensive capital

and technology

Large dealer

network needed

Brand loyalty

high

Rationale

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

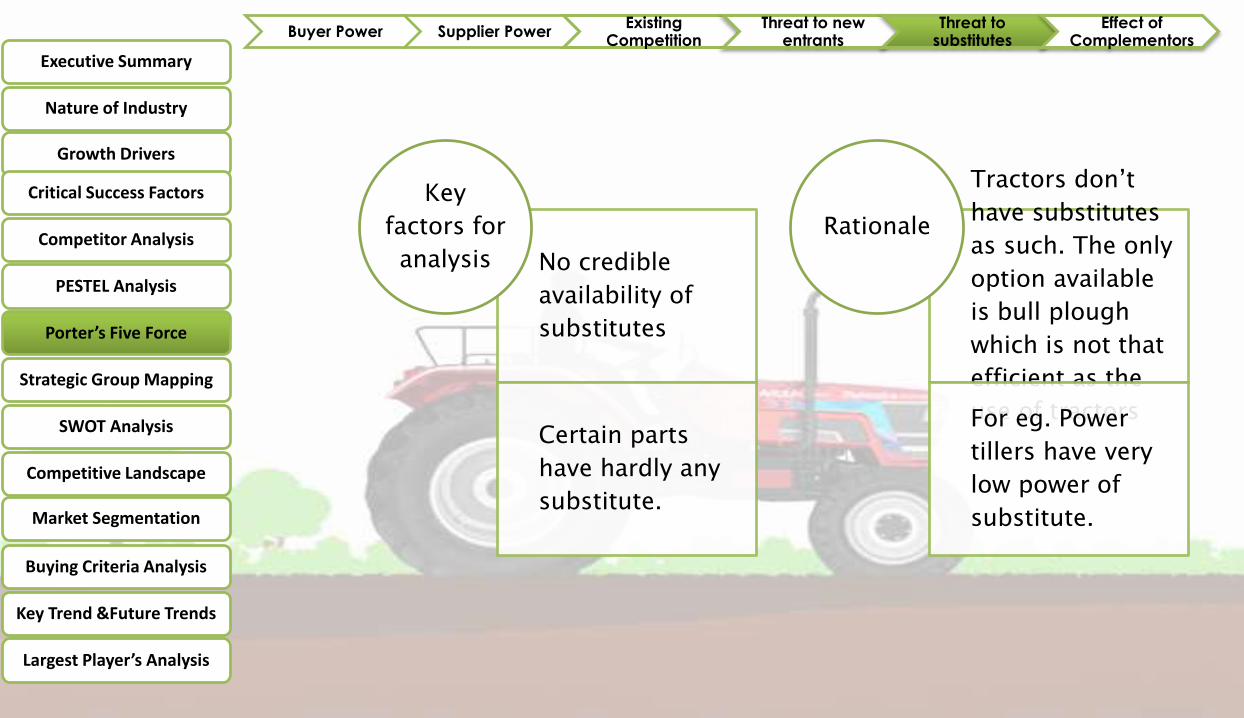

No credible

availability of

substitutes

Certain parts

have hardly any

substitute.

Key

factors for

analysis

Tractors don’t

have substitutes

as such. The only

option available

is bull plough

which is not that

efficient as the

use of tractorsFor eg. Power

tillers have very

low power of

substitute.

Rationale

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Buyer Power Supplier PowerExisting

CompetitionThreat to new

entrantsThreat to

substitutesEffect of

Complementors

High number

of

complements

increases

demand.

Key

factors

for

analysis

For eg. Plow

needs to be

complemented

with tractor for

its use.

Rationale

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

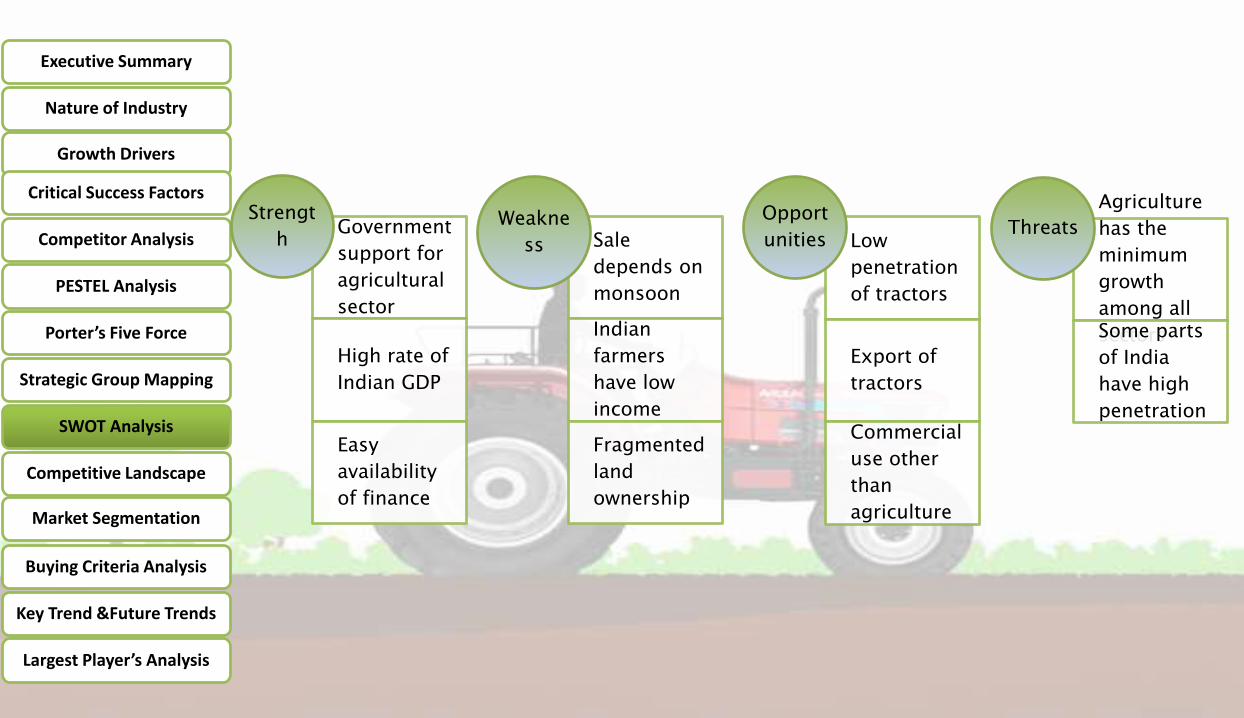

Government

support for

agricultural

sector

High rate of

Indian GDP

Easy

availability

of finance

Strengt

h Sale

depends on

monsoon

Indian

farmers

have low

income

Fragmented

land

ownership

Weakne

ss Low

penetration

of tractors

Export of

tractors

Commercial

use other

than

agriculture

Opport

unities

Agriculture

has the

minimum

growth

among all

sectorsSome parts

of India

have high

penetration

Threats

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Trends

Largest Player’s Analysis

Segments Horse Power Market Share (%) RegionalConcentration

Small Tractors 21-30 HP 23-25 North India

Medium Tractors 31-40 HP 53-56 West & South India

Large Tractors 41-50 HP 17 West India- Large Landholdings

Large Tractors > 50 HP 2-4 West India

31-50 HP Segment (Mid Segment)- 70%

Fastest growing Segment- >40 HP

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Developments

Largest Player’s Analysis

• Individual Customers & SMEs

• High SignificanceReputation of Brand

• Individual Customers & SMEs

• High SignificanceResale Value

• Individual Customers & SMEs

• High SignificanceAvailability of Finance

• Individual Customers & SMEs

• Low SignificanceSpecial Features

• Individual Customers & SMEs

• High SignificanceMargin Money

• Individual Customers & SMEs

• High SignificanceCustomer Relationship

• Individual Customers & SMEs

• High SignificanceParts Availability

Executive Summary

Nature of Industry

Growth Drivers

Critical Success Factors

Competitor Analysis

PESTEL Analysis

Porter’s Five Force

Strategic Group Mapping

SWOT Analysis

Competitive Landscape

Market Segmentation

Buying Criteria Analysis

Key Trend &Future Developments

Largest Player’s Analysis

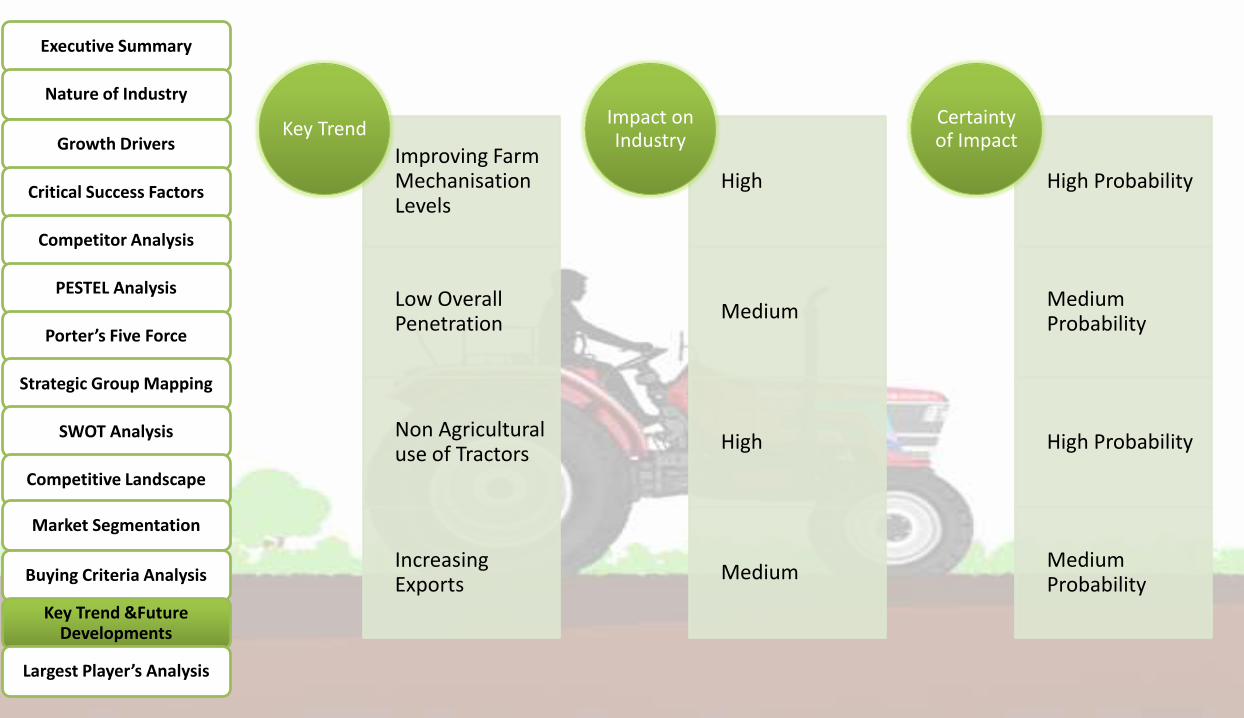

Improving Farm Mechanisation Levels

Low Overall Penetration

Non Agricultural use of Tractors

Increasing Exports

Key Trend

High

Medium

High

Medium

Impact on Industry

High Probability

Medium Probability

High Probability

Medium Probability

Certainty of Impact

Related Documents